Three possibilities come to mind.

By Peter Diekmeyer, Canada, for Sprott Money:

Bank of Canada governor Stephen Poloz cited numerous worries plaguing the economy during his speech to Toronto’s financial elites at the prestigious Canadian Club. However, the title of Poloz’s presentation, “Three things keeping me awake at night” seemed odd, given positive recent Canadian employment, GDP and other data.

Poloz highlighted high personal debts, housing prices, cryptocurrencies and other causes for concern, along with actions that the BoC is taking to alleviate them. His implicit message was (as always) “We have things under control.” But if that’s all true, then Canada’s central bank governor should be sleeping like a baby. So, what is really keeping Mr. Poloz up at night? Three possibilities come to mind.

The Poloz Bubble

Firstly, far from just a housing bubble, Canada’s economy shows signs of being in the midst of an “everything bubble.” Bitcoin, for example, hovered near CDN $23,000 this week. Stock and bond valuations are not far behind in their relative loftiness. Worse for Poloz, who took office four years ago, his fingerprints are all over those bubble-like levels.

Canadian stock, bond and house prices were already at dizzying heights when Stephen Harper hired Poloz with the implicit expectation that he would juice up the economy, in preparation for what Canada’s then-Prime Minister knew would be a tough upcoming election.

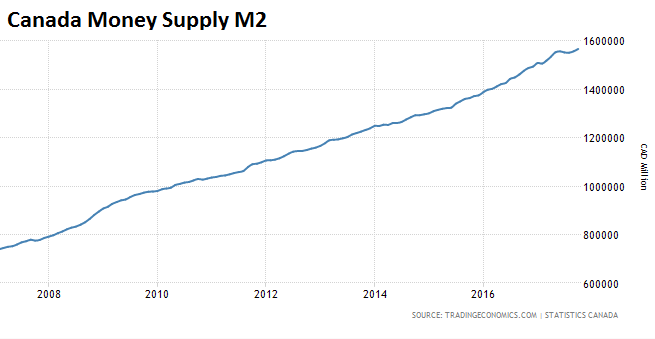

Poloz didn’t disappoint, promptly delivering a nice Benjamin Strong-styled “coup de whiskey” to asset prices in the form of two interest rate cuts, which brought the BoC’s policy rate down to just 0.50% during the ensuing months. Although Harper lost the election, loose BoC policy continues to provide the Canadian government with free money to borrow and spend as it wishes.

Here’s Canada’s ballooning Money Supply M2 (via Trading Economics):

More broadly, the Poloz BoC’s current policy, like that of the US Federal Reserve, is to boost asset prices even higher in the hope that the resulting wealth effect will trickle down to spur economic activity among ordinary Canadians.

At the household level, the BoC’s low interest rates enticed Canadian families to borrow themselves to the hilt. Businesses haven’t been that far behind. The upshot is that total government, business, and household debts are now in nosebleed territory with Canada’s economy seemingly on a knife’s edge, in danger of crumbling at the first patch of rough road.

Chained to a Ponzi

Another worry is that the Poloz BoC, by broadly mirroring the Federal Reserve’s actions, has firmly lashed Canada to a US economy which could prove to be an even bigger Ponzi than its own. America’s “everything bubble,” like Canada’s, has been stroked by a central bank that has been pushing credit growth at a rate faster than GDP growth, a textbook Ponzi scenario.

One result, as Grant Williams, co-founder of Real Vision Television, noted in a recent presentation, is that US stock prices are currently far higher than they were during the Internet and housing bubbles. “[Central bankers] keep hoping that this time is different,” Williams warned. “But ladies and gentlemen – it’s never different.”

Refusal to ring fence Canada

Another worry for Poloz to ponder, is that although the BoC has identified financial system interconnectedness as a key concern, the central bank has done little to ring fence Canada’s economy from huge global macro threats on the horizon.

That’s particularly true of the hundreds of trillions of dollars in global derivatives books, many of which are unquantifiable, as they are trading outside of traditional exchanges. This threat is particularly acute, as it was the failure of AIG, a derivatives player, to cover its bets (not the subprime mortgage and Lehman implosions as most assume) that sparked the 2008 financial crisis.

Poloz, had he been ready to condone a recession, could have encouraged broader interest rate hikes to incentivize Canadian governments, businesses and households to pay down debts, build up savings and increase overall system stability. Similarly, instead of building up Canada’s gold reserves to cushion against potential external shocks, the supposedly-independent BoC (as noted above) makes nearly free money available to the big banks and the Canadian government.

Government and academic elites would argue that Poloz’s actions are understandable as he has only limited powers. They cite key constraints on the central bank’s actions. These range from the BoC’s agreement with the Department of Finance to target 2% inflation, the fact that the government has primary authority over foreign exchange purchases and by realpolitik which dictates that Canada has to follow US policies – or else.

Others, such as James Rickards, author of The Road to Ruin, would argue that Poloz is plagued with the same “group think” problem that faces Fed Chairmen. Almost all the top economists these days, despite obvious brilliance, remain trapped by Keynesian/econometrics educations they endured to get their graduate degrees, which left them with few ideas regarding how to generate growth other than to print more money.

Canada’s top central banker rarely deviates from his talking points. So, it’s almost impossible to know what he really thinks. However, a base case scenario suggests that Poloz (who has considerable private sector experience from his days at BCA Research) knows full well the treacherous position in which the BoC has placed the Canadian economy. If that’s true, it’s little wonder that he is having trouble sleeping. By Peter Diekmeyer, Canada, for Sprott Money

How exposed are over-indebted household to rising interest rates? Read… Canada Home Values Hit “First Quarterly Decline since Q1 2009” as Household Debt Binge Hits New High

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I wish you people would stop blaming John Maynard Keynes, one of the most intelligent and cultured men of the 20th century as well as its greatest economist.

Why don’t you try reading some of his books?

Agree with you. I don’t recall reading anything Keynes wrote to advocate round the clock infusions into the financial system, yet here Diekmeyer implies otherwise.

I’ve read a parts and two chapters of Keynes stuff. It’s hard because his terminology is older and non-standard.

But I can’t see Keynes not immediately understanding that pouring liquidity into a broken credit system is ineffective and just creates asset bubbles, very low rates of growth, and a politically dangerous disgruntled working class.

I just don’t see it, Keynes was smarter than that. And he didn’t have the same ideological and educational blinders on that most economists or wannabe economists have.

Well said.

Wolf, it’s painful to see you falling for this neoliberal trick.

If you want someone to blame start with neoclassic-bullshit (debt does not matter) and monetarists.

Hiho,

One, I’m not the author of the article (Peter Diekmeyer is the author, see byline).

Two, it’s just one line in the article toward the bottom, so enjoy the rest of the article.

+1 for the Vonnegut reference. :)

Very true, but then, there is always those who claims that intelligent people are more responsible for their actions than the dumb ones (there is no such rule in the universe).

In this case, the charge is that he should have known better than to propose that the government should spend when the proverbial seven lean years arrive. That he should known better that the elected representatives of the people can, by design, never tell bad times from good. It is baked into the system, which was not the case then.

Keynes isn’t the problem. His followers are. I’m pretty sure JMK would disown every single modern Keynesian if he were alive today.

The fact is, Keynes’s solutions were likely right for the time, when government spending was a tiny percentage of GDP. Now, with government spending accounting for anywhere from 40% to 60% of GDP in nearly all modern economies, Keynesian theory is about as useful as a snowplow in Bermuda.

Keynes himself would know that. His followers seem to think there are no limits to the application of his ideas. And they keep adding more complex and obscure mathematics (usually some form of differential calculus) in an effort to prove themselves right. I think it was Nassim Taleb who said “The calculus is to mathematics what Deepak Chopra is to philosphy”. That’s not verbatim, but I’m too lazy to look up the exact quote.

Calculus is to analysis what Deepak Chopra is to Bertrand Russell.

That was it. Thanks.

Keynes, and many other bloviating economists of the last century, provided the framework for the problem to snowball. Minsky gave a nice explanation for how these problems will eventually resolve themselves. Today the world’s currencies are marching inexorably toward their Minsky moment. No one knows which snowflake will land on top of the enormous currency build-up and cause the devastating avalanche crushing the economy – but the snow keeps falling the avalanche is coming.

After the economic avalanche of out of control inflation hits, the economists will trot out the old “no one could have ever predicted” excuse. No doubt Bernanke will be on TV explaining the whole thing could have been avoided if only he was still in command.

How can the followers be the problem without pinning (any) responsibility on the source?

I never meant to absolve the source entirely. But we can probably find better – and more modern culprits – than some guy who died in 1945.

Bank loans and deficit spending both inject new money into the private sector. Problem is, the bank loans have to be repaid. ( Note deficits can be fed financed, no need for repayment… and Qe shows no inflation so long as resources such as labor is abundant.)

More deficit spending and fewer bank loans would be better.

Keynes promoted def spending when private sector is on its back, but probably thought spending should be in rough balance across the bus cycle.

But dollars are constantly draining from economy because world wide savers want them for their mattress, plus pop grows reducing dollars per person, plus to accommodate the small amount of inflation…

So a constant injection of cash that does not require repayment is necessary.

Incidentally, foreign savers desire for dollars explains the trade deficit… and so long as they prefer dollars to yuan or rubles or euros, the dollar will remain the reserve currency… has nothing to do with our nukes.

John k

“dollars are constantly draining from economy because world wide savers want them for their mattress”

A canard constantly stated, not true. Most “saved” dollars are loaned out by the banks. Thus they are NOT shrinking the economy.

Not only are Saving’s in Bank’s, not shrinking or stagnating the Economy, saving’s in Bank’s :

1 Stabilise Bank’s.

2 Enable Bank’s to leverage against them (So Growing the credit Based Economy further).

This is why Bank reporting of Cash and Banking Transactions. To the Tax (And Other) Authorities is VERY, counter productive.

As it encourages secret room’s full of black money, which are VERY counter productive. To the Bank Credit based Economy, as the Bank’s can not leverage lend, against secret rooms full of black money.

The Bureaucrat Takers with their ever increasing demands of MOORE for THEIR TAKE-HOME PAY.

Have shot a very big hole in their and the Economies Foot, with their . “Banks must reveal and report everything to us”. Position of self interest. As now the Bank’s dont have the Criminal and other monies, outside the reported-system, to work with. This SLOWS the Bank Credit based Economy considerably.

Yes, Keynes anticipated the end results of his ideas misused/abused to the excesses we see over the past 3 decades. I am sure he is one of the many rolling in graves just about now.

Oddly the bank of canada has been selling off Canadas gold reserves I beleive we are down to 70 ounces. The mantra was there are better returns out there. Re keynes. It is how our politicians have interprete what he had to say. Plus market manipulation has distorted the global markets so much Keynes would be aghast. The rea” Keynes

He didn’t blame Keynes, he blamed modern Keynesianism and the econometric macro-babblers who have made their careers in that school fo thought. Two entirely different things. Keynes himself would savage modern Keynesianism.

I agree with your assessment.

Keynes, for all his faults is one of the most fascinating men of the 20th century.

If people had read Keynes’s “Economic consequences of the Peace,” there would have been no Second World War in Europe.

Furthermore, Keynes’s General Theory has been badly misinterpreted by public policy officials, academics and modern economists. Keynes for example argued we should run deficits in bad times and surpluses in good times.

That said, Keynes did advocate:

1. The ‘euthanasia of the rentier,”

2. Governments using inflation to secretly extract wealth (from what he implied was an ignorant population)

3. Not worrying about the secular implications of public policy, because “In the long-run we are all dead.”

For those who want to pursue this further, I highly recommend Donald’s Moggridge’s biography of him.

Sadly, the public, and most American readers do not have time time to absorb these subtleties.

“3. Not worrying about the secular implications of public policy, because “In the long-run we are all dead.” ”

That is why his work is flawed.

His lifestyle group-think, did not involve his own children, who would have to clean up the mess.

This is the “I am all right Jack” Post WW II attitude, that the boomers onward have, as a mantra.

His Stimulate in Bad Times only had a Pay off in good times, written after to make it balanced and publishable, although his work was guaranteed publication by the Leftist who sponsored him..

The leftist have been doing what he advocated since WW II. Spend, and leave the debts for the others.

Greece is what eventually happens. As no Leftist ever pays off. In Greece there is no right, only hard, and center left. Which is called “Right” in greece.

Today’s Keynesianism is to Keynes as modern day liberalism is to the Worldly Philosophers- Mills, Smith….

Hi Tom

I haven’t read any of his books and am not an economist (just Joe average) but I’m of the understanding that Keynes advocated for Gov to spend on infrastructure to increase productivity and anything else to keep wages stable and support social cohesion.

Not goose the capital markets with free money is this somewhere accurate??

Mark

Yes. The financial markets in Keynes’ days was but a drop in the bucket versus the paper trading shadow economy we have today.

This is a global problem and it shows all the flaws in current economic thinking.

It’s time to learn from past mistakes.

The real estate boom, where would neoliberalism be without it?

2008 wouldn’t have happened for a start.

Even sparsely populated New Zealand has seen a real estate boom and has a large problem with homelessness; these are symptoms of neoliberalism. Ireland and Spain had house building and house price booms at the same time, it’s nothing to do with supply and demand.

The real estate boom features all the unknowns in today’s thinking, which is why they are global.

This simple equation is unknown.

Disposable income = wages – (taxes + the cost of living)

You can immediately see how high housing costs have to be covered by wages; business pays the high housing costs for expensive housing adding to costs and reducing profits. The real estate boom raises costs to business and makes your nation uncompetitive in a globalised world.

The unproductive lending involved that leads to financial crises.

The UK:

https://cdn.opendemocracy.net/neweconomics/wp-content/uploads/sites/5/2017/04/Screen-Shot-2017-04-21-at-13.53.09.png

The economy gets loaded up with unproductive lending as future spending power has been taken to inflate the value of the nation’s housing stock. Housing is more expensive and the future has been impoverished.

US:

https://cdn.opendemocracy.net/neweconomics/wp-content/uploads/sites/5/2017/04/Screen-Shot-2017-04-21-at-13.52.41.png

Unproductive lending is not good for the economy and led directly to 1929 and 2008.

Neoliberalism’s underlying economics, neoclassical economics, doesn’t look at private debt and so no one really knew what they were doing.

The real estate boom feels good for a reason that is not known to today’s thinkers.

Monetary theory has been regressing since 1856, when someone worked out how the system really worked.

Credit creation theory -> fractional reserve theory -> financial intermediation theory

“A lost century in economics: Three theories of banking and the conclusive evidence” Richard A. Werner

http://www.sciencedirect.com/science/article/pii/S1057521915001477

“…banks make their profits by taking in deposits and lending the funds out at a higher rate of interest” Paul Krugman, 2015. He wouldn’t know, that’s financial intermediation theory.

Bank lending creates money, which pours into the economy fuelling the boom; it is this money creation that makes the housing boom feel so good in the general economy. It feels like there is lots of money about because there is.

The housing bust feels so bad because the opposite takes place, and money gets sucked out of the economy as the repayments overtake new lending. It feels like there isn’t much money about because there isn’t.

They were known unknowns, the people that knew weren’t the policymakers to whom these things were unknown.

Sounds

What a good mind you have Sir.

The U.s. and Canada might as well ask Mr. Putin how much gold he would accept to recover our countries from the debochle that we find ourselves in. For it seems he is the only one with any economic experience and common sense.

Precisely Tom

He advocated government surpluses during booms–something that’s always neglected. Also, he was bedridden with grief after the Treaty of Versailles and predicted WWII.

Keynes mistook that economics was the instrument, but politics (vengeance) was the controlling hand.

Western countries are so similar to each other. With the Fed raising interest rates much more under a Republican President than a Democrat, does Canada’s central bank have a similar agenda?

Canadian here,

Scary scary post. It is true as far as I’m concerned; not with my generation and older, (I’m 62), but with the 40ish and younger set.

My kids are in this group, and while they are doing well and seemingly secure, they have never ever weathered tough times. I recently hired my son’s apprentice to help me with some wiring on a house I am building. He is 38. We were talking about this and that while working, and economics came up as well as debt. He remarked that my son had told him that we were poor when he was growing up. I started to laugh and said, “That’s probably because we lived in a small house and drove crap cars, in fact only had one old beater and I biked to work most days. We also didn’t do the Disneyland vacations, stuff like that. But, we had a house paid for and never had debt, ever. I was also able to work at a job of my choosing, rather than in the pulp mill or logging”. Then, he told me about his Dad and the story sounded similar. His Dad drove a travel bus for a living, but they had their own small home and were able to ski in the winter.

I asked him about his own debt level and he said it was really good, that he only owed $180,000 on his house. (a sub-division rancher). My son must owe $200,000 on his, but to be fair it is a bit of a riverfront estate and pretty awesome. But the point remains, if the economy burps, rates rise (like they did when I was in my twenties…..to 18%), or they lose employment for awhile, they risk losing it all. They don’t get it and continue to spend spend spend.

My son was once friends with a kid who just bought his first home last year. (I know his Dad). It was a fixer-upper on the beach, and cost $600,000. Parents helped them out, obviously. The kid is a deadbeat who talks a good line about being a carpenter, but I have seen him working and his work quality, and believe me he is not. He also drinks too much and now their 2 year old marriage is on the skids. It doesen’t take a scientist to write this looming story, does it? I expect he will live in his folks basement. Again.

Who buys a $600,000 first home? But that is just one example. I know many in this age group who routinely are in hoc $300-$400,000 for their first homes. It is absolute insanity. Many, if not most will be the examples to site going forward.

As my old friend Art (the barge loader) used to say…..(and these guys make a fortune loading log barges with cranes)…., “It isn’t what you can afford with your job/salary, and when you’re working, it’s what you can afford when you are not working”. Somehow, people have been lulled into believing that good times are here forever. I think it’s because of all those blue ribbons they got for just showing up, and being dropped off at school everyday so they wouldn’t have to walk in the rain. :-) Guess what? It’s going to start raining pretty hard one of these days, it always does.

We are being warned. Again. Good article.

Or as the doc said just before my last ‘exam’, “I’m sorry, but you will feel some discomfort for a moment”.

regards

Great post Paulo…hopefully your son has “absorbed” some of your wisdom

Paulo, that was an awesome post. Your anecdotes are as relevant as any “data”, and frankly a lot more useful. We have an obsession with measuring things nowadays, and as long as the measurers (i.e. the macroeconomists and policy gurus) tell us that things are OK, we assume there is nothing to worry about. Those of us who are old enough to have seen a few cycles (I’m late 40s) know that we in Canada have enjoyed an especially long period of prosperity.

In fact, there is something almost abnormal about how long we’ve gone since the last serious recession up here. The first half of the 1990s was the last real recession; 2001 and 2009 being mere blips on the map in comparison. (I won’t even count 2015-16, because unless you were in an energy producing province like Alberta or Saskatchewan or Newfoundland, that wasn’t a recession at all.) I really do fear that the under 40 crowd is oblivious to risk, because they have no collective memory of real hard times. And it’s not their fault either. Older people warning me of risk in my 20s sounded stodgy and out of touch, just like I’m sure I do to today’s youngsters. Even though I grew up in the 80s recession and entered the job market in the misery of the early 90s recession. I still thought the oldsters were foolishly cautious and risk-averse. I had to learn all the hard lessons myself. I was unteachable, so I can’t expect anything better from the kids today. All I can say is this: It’s not a “new paradigm”, it’s just an extended credit cycle. All credit booms end. This one will too.

I enjoyed reading your story and I’m not surprised by your amazement at the cavalier attitude many younger people seem to have regarding money and debt.

However, consider the possibility that these reckless actions may, in fact, be wise. Central banks have made the economy a game and we know who the winners and losers have been thus far but we don’t know how the game ends. I believe central banks (and the banking system) will continue to dilute the currencies and inflate away debts – if or when the typical worker earns $1 million per year will $600,000 borrowed to buy a water front home seem like a poor choice in retrospect.

Currencies are nothing more than electronic tokens created by the central banks and commercial banks. The monetary system is just a bookkeeping game. The banking system does the bookkeeping and keeps track of who owns the tokens but they also fudge the books adding more tokens into the economy (game) to enrich themselves and certain other players – put simply the bankers are cheating at the game. Eventually the players of the game, who must work for tokens, realize others earn many more tokens without working and begin to lose confidence and are no longer motivated to work for tokens – that is when the game comes to an unfortunate end for all of us (but your young friend will still own his nice waterfront property!!!)

Winner, winner chicken dinner! Borrow money and buy assets – let dilution of the currency pay your debts. In Seattle, in the year 2000, $100,000 was a lot to pay for a nice condo – today that sum is laughably small, about one year’s pay. Was the buyer foolish to stretch his finances to buy into the market 17 years ago – it would appear not. That is how the game is played.

There is no Karma, no moral center to the universe. Bad actors are not punished. How many bankers committed obvious, blatant fraud prior to the last crisis – how many were punished? You seem to expect reckless behavior to be punished but that’s just not how the game is played. The game rewards reckless (and often illegal) behavior.

Yes, but what about the poor sap that pays $1.2M for a dump in Seattle, without inspection, in need of a new roof, exterminator, and mold proofing.

That poor sap may find the stock market tanking in 2018, taking RE along with it. He’ll then be sitting in his $1.2M dump, regretting life. When Microsoft or Amazon lays him off because he’s over 40 and not a minority, he’ll be wondering where the money will come from for the home repairs that will allow him to sell his house for $700K in a down market.

Your hypothetical sap who pays $1.2M for a dump could always just walk away. Washington is a non-recourse state. If he fails to make mortgage payments the bank gets to take the house and the sap has no further obligation to the bank.

Of course your narrative would depend on a correction in the housing market – something the Fed will never allow again. If necessary the Fed would provide mortgages at 0% or even negative interest rates.

It is different this time. Name one other time in history when central banks have explicitly offered a guaranteed backstop to speculators of every asset. Assets are not in a bubble – what you are witnessing is the air coming out of the currency bubble. Everything seems expensive when valued in currency because central banks are destroying the purchasing power of currencies.

Van

The tokens aren’t free, even though they appear to be. The tokens are the yardstick which we use to measure value, in making decisions. They are the foundation of right and wrong in the economic engine we require to maintain civilization. Once the tokens are perceived to benefit the free riders and not the producers, then production of real value stagnates.

A $600,000 dollar beach front shack only has that value because the tokens, that have been made in excess, facilitate the bid up of an asset that actually has not improved or changed in value in any way. Only in token terms.

That means those that got in early, by accident or design, are winners via inflation, and those that are late to the party, usually because of their youth, are priced out.

So the price is paid by chipping away at our civilization. I see it in the cities all the time. Young locals that can’t afford to purchase a home because foreign tokens price them out of their own backyard. A price is paid when tokens are created, both foreign or domestic, whether an economist or a politician can see it or not.

It’s obvious that Poloz needs to be replaced by Paulo.

Really good post Paulo, spot on.

Best Regards

Steve

UK

Before 2008 I was following Bob Prechter and his admonition about brokerage “pooling” of assets seemed right, I mentioned it to my broker, who gave me the don’t panic speech, before I could do anything they set up separate state bank accounts to “ring fence” the problem. Now we know that the Fed will step up before any of these entities get even close to liquidating, or we hope we know. We know that Congress will pass any emergency measure the UST/Fed wants, just mentions tanks and streets together. There is a gentlemen’s agreement between counterparties, almost none of the global currency derivatives are registered, and about half the currency derivatives. The CBs have each others back. Go back to sleep.

You are correct. But, Janet Yellen is also correct to say no more financial crisis in her lifetime (unless you include currency crisis). The Fed, under Bernanke, believed it had discovered the economic holy grail – they could create as much electronic currency as they wanted and place it in any account required to stop any panic. The extra currency they create inflates only assets (they believe) and pushes wealth into the hands of those who are already wealthy – investors who can afford to speculate.

But because, wealth cannot be created simply by typing numbers into an account the wealth gained by affluent speculators must be lost by another party – in this case wager earners who have been told to save for retirement but are not comfortable speculating with currency they toiled so hard for. Central bankers have never had to work for their currency and thus don’t understand why wage earners are hesitant to join in financial speculation.

Economists, who have never worked an honest day in their lives, cannot understand the motivations of the masses who must earn money through hard work. This is why Keynes, Krugman, Bernanke, and the rest could never understand the economy and why they have always been so wrong.

Read Keynes, he understood. When Keynes talks of poverty it’s the real deal.

When Krugman, all the rest, mention poverty it’s like it’s just sort of unfair or something. So yeah mostly no.

The assets owners have reason to think it unfair that the value of their property is controlled by a small volume of transactions during a panic. The Fed thinks (rightly?) that if the collapse of asset prices is temporary then it is unfair to mark to market real assets while the market is distorted by margin selling of assets without collateral. This is why large firms make “block” trades, (gentlemen’s agreement) to avoid unpleasant volatility. They assume that the market will always go up (inflationism) and therefore at some future date their “deferred asset” will recover all of its value. The idea that bad investments ever need to be rooted out, or bad debt, is foreign to them, which is why DJTs idea for resolving bad debt will never get off the ground. All debt must be extended to maturity.

ATTENTION:

Go to the Grant Williams link contained in the article.

You WILL NOT be disappointed. A really excellent 30 minute video.

Well presented, containing many great charts. VERY telling.

IMO, Mr. Diekmeyer states what is most important right here (with my caps for emphasis):

“Government and academic elites would argue that Poloz’s actions are understandable as he has only limited powers. THEY CITE KEY CONSTRAINTS ON THE CENTRAL BANK’S ACTIONS. These range from THE BOC’s AGREEMENT WITH THE DEPARTMENT OF FINANCE TO TARGET 2% INFLATION, the fact that the government has primary authority over foreign exchange purchases AND BY REALPOLITIK WHICH DICTATES THAT CANADA HAS TO FOLLOW US POLICIES — OR ELSE.”

==================

“Realpolitik”, indeed. That single word represents an understatement if there ever was one. “Or else” is more to the point, but still doesn’t hit the bullseye, so I’ll take a shot at it.

“Or else” means that if the US’s political slaves in Canada do not do what the US dictates, the FBI, the CIA and, if necessary, the JSOC will “meddle” even more than it does now in Canada.

The US exerts its control over Canada and its other vassal states through its emabassies and “consulates”. For just one example, take a look at the consulate in Calgary — Oilberta’s REAL capitol:

https://ca.usembassy.gov/embassy-consulates/calgary/sections-offices/

Notice the details in the “Poltical and Economic Section”.

Then we have US FBI offices in Canada:

https://www.fbi.gov/contact-us/legal-attache-offices/americas/ottawa-canada

And the purpose of those offices:

https://www.fbi.gov/about/leadership-and-structure/international-operations

======

“For more than seven decades, the FBI has stationed special agents and other personnel overseas TO HELP PROTECT AMERICANS BACK HOME by building relationships with principal law enforcement, intelligence, and security services around the globe that help ensure a prompt and continuous exchange of information.

Today, we have 64 legal attaché offices—commonly known as legats—and more than a dozen smaller sub-offices in key cities around the globe, providing coverage for more than 200 countries, territories, and islands. Each office is established through mutual agreement with the host country and is situated in the U.S. embassy or consulate in that nation.

Our legal attaché program is managed by the International Operations Division at FBI Headquarters in Washington, D.C. This office keeps in close contact with other federal agencies, Interpol, foreign police and security officers in Washington, and national and international law enforcement associations. International liaison and information sharing are conducted in accordance with executive orders, laws, treaties, Attorney General Guidelines, FBI policies, and interagency agreements.”

======

“Canada’s” CISIS is part of the so-called “Five Eyes”:

https://en.wikipedia.org/wiki/Canadian_Security_Intelligence_Service

What I’d like to know is just exactly how often Canadian “public servants” at all levels of the “Canadian” government communicate with employees at all levels of the US government and just exactly WHAT is said in those communications. But I already know one thing for certain without knowing any of the exact details — the vast majority of that communication and control is “in the national interest” NOT of “Canada” but its US Elite masters.

The important, overriding thing for Candians to keep in mind is that when push comes to shove, Poloz and the rest of the provincial and federal public servants in the “Canadian” governments will do exactly what they are ordered to do by the US Elite.

To put it even more bluntly, “Canadian” economic and, especially, “foreign” policy are now being dictated by the US Elite. The good thing is that now the situation is so blatantly obvious that even semi-conscious adult Canadians now realize it. Their children, however, are still being “educated” into believing that Canada is still a sovereign nation that has a government that is capable of making decisions that are truly in the interest of the people of Canada.

I think having a more “Royalist” attitude (as opposed to “Republican”) is a good thing in respect to the concerns you raise.

Do you agree Ishkabibble?

Here’s a little addendum to my last comment.

“Trudeau government gag order in CIA brainwashing case silences victims, lawyer says”

http://www.cbc.ca/news/canada/canadian-government-gag-order-mk-ultra-1.4448933

Another nice gift of love from the US of A to its loyal ally, Canada.

All of these central banksters profess to be “worried,” but not so worried that they’ll step in forcefully to curb the Ponzi markets and asset bubbles created by their own monetary malpractice.

Subtitle: Schizophrenic BoC governor does not know what his left lobe is doing to his right lobe, which keeps him awake at night.

Oh, and how good that he is not loosing sleep over screwing the savers, and the prudent.

It’s amazing, looks like Cryptocurrency demonization is going to be a scapegoat for Neo Liberal Economic polices that have created this global mess. What a game plan!

Its over-leveraged Everywhere and has a socialist spender in Power.

He just cant say that.

So there is plenty to worry about.

QE is like laxative.

Just wait till it works.

Ask Steven Poo-Loose.

In Canada the bubble should pop but just seems to get pushed aside year after year. The government claims amazing employment numbers, but they come with a catch: http://www.huffingtonpost.ca/2017/12/01/less-than-half-of-canadas-prime-age-workers-kept-a-full-time-job-for-all-of-2015_a_23294345/

Part time jobs don’t pay the bills 5 yrs, 10 yrs or 20 yrs later. No retirements, no pensions, no savings for all the part-time working people in this “booming” nation. Too many signs point to failure for this system to stay afloat.

Keynes fundamental insight into the causes of the Great Depression was that the crash of 1929 and the contraction of the economy that followed was not to be cured by government and private austerity measures but rather by responding to what he called “the failure of demand”. His General Theory correctly stated that as long as this impulse towards belt-tightening continued the depression would continue.

Post-war neo-Keynesians such as Paul Samuelson and others extended this idea to propose that by Central Bank “fine tuning” interest rates we could control the money supply and achieve permanent stability and steady growth.

During the 1970’s a combination of a tight labor market caused by several million young men in the military during the Vietnam War and profligate guns AND butter spending by successive administrations, Democrat and Republican led to ruinous inflation, followed by the Fed induced period of stag-flation.

The response was to blame it all on Keynes, who I imagine was rolling over in his grave at being blamed for the outcome of the swinging 60’s and 70’s – the anti-thesis of the great depression.

And now he gets blamed again. Unfortunately, as many contemporary economists such Keen, Turner, and Kelton have pointed out, money creation can be an endogenous activity of private banks, that is not a matter of banks lending the funds of savers but rather as a matter of simply pushing the keys on a computer terminal. And, it is the unrestrained growth of private debt-based money that leads to the illusion of infinite riches through the illusion of wealth creating asset bubbles.

The problem isn’t Keynes. It’s out-of-control banks and financial markets.

Two predictions:

1) The insane guns and butter tax cut will eventually lead to inflation, because I do not believe the Republicans will be politically able to reduce spending by a like amount.

2) The equally unhinged run-up in asset prices will come to a crashing end, and fantasies about the Fed coming to rescue will prove to be just that. The Fed will once again stabilize the banking system. They will not however, be able to nor will they even try to put crashed asset prices back to the oxygen free upper atmosphere where they now reside.

“[Keynes]the contraction of the economy that followed was not to be cured by government and private austerity measures but rather by responding to what he called “the failure of demand”. His General Theory correctly stated that as long as this impulse towards belt-tightening continued the depression would continue.”

Which was baloney. The classic examples of Japan and Germany, laid waste and deeply impoverished following WWII are where people, forced to tighten their belts and accept lower wages work their asses off and gradually recover prosperity. Keynes himself states in his General Theory that the benefits of deficit spending (money printing) are felt immediately through increased employment; the inevitable inflation is only recognized later. The real beneficiaries of the massive increase in debt today are the banks which own the Fed and other CB’s obtaining funds virtually interest-free with which to accumulate productive assets for themselves. It is still 25% APR for their cardholders and virtually nothing for savers

As a lifelong entrepreneur, i can tell you that the problem is far from being ‘loose money’ per se. The problem is that loose money is ONLY available for housing.itismisdirected liquidity. If entrepreneurs had easier access to money- the economy – outside of housing- would flourish. Since banks ONLY lend on the basis of real estate assets backing loans, entrepreneurs have to borrow for a house they don’t need, the remortgage it to provide risc liquidity. The paucity of riskcapital is driving the housing asset bubble because banks are addicted to government Mortage loan guarantees.

This is an excellent point. Big business has all the money it needs.

In fact more than they need – as they are buying back stock at all-time bubble prices, because they can’t figure out where to invest their excess cash.

Here in Canada CFIB members all tell the same story: small businesses on the other hand, are starved for capital.

Mises had a term for this: “misallocation.” What an understatement. Thanks.