How exposed are over-indebted household to rising interest rates?

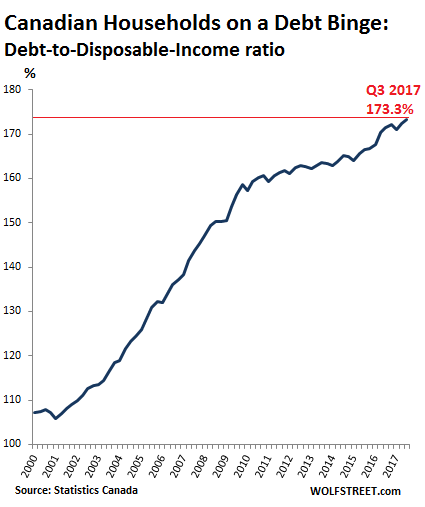

Household debt in Canada rose to a new record of C$2.11 trillion in the third quarter 2017, up 5.2% from a year ago and up 10.7% from two years ago, Statistics Canada said on Thursday in its quarterly report on national balance sheets. Mortgages accounted for 65.6% of the total. Canada’s infamous household-debt-to-disposable income ratio, one of the highest in the world, rose to a breath-taking record of 173.3%.

The ratio means that households, on average, owed C$1.73 for every dollar of after-tax income earned. This chart shows how the indebtedness in relationship to after-tax income has soared since 2001, when Canada’s housing boom took off in earnest:

While US households “deleveraged” somewhat during the Great Recession, mostly by defaulting on their debts when housing crashed and jobs vanished, Canadian households barely took a breather as there was no housing bust in Canada. Hence the consistently rising and record-breaking debt-to-disposable income ratio above.

Disposable income in 2016 got hit by “a significant downward revision,” based on new data received from Canada’s tax collection agency, Statistics Canada said. This resulted “in an upwards shift to this ratio.”

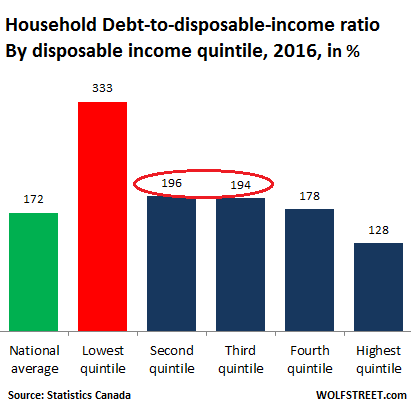

The debt-to-disposable-income ratio of 173%, scary as it is, is just a national average. But it’s not normally the top of the income categories that get in trouble. It’s the lower categories.

In a separate report also released on Thursday on the distribution of income and assets, Statistics Canada added to this debate:

Economy-wide debt-to-asset and debt-to-disposable-income ratios can mask the financial risk associated with increasing debt for a given group of Canadian households.

In 2016, the national average debt-to-disposable-income ratio was 172.1%. Decomposing this by household disposable income quintile reveals that the debt-to-disposable-income ratio for the bottom income earning households was 333.4%, while the debt-to-disposable-income ratio for the top was 128.3%.

This chart shows the debt-to-disposable-income ratio by income quintile. Households in the bottom 20% income category (red column) are far more at risk than top-earning households. Also note that in the second and third quintiles, where many mortgages are taken out, the debt-to-disposable income is approaching 200%:

In terms of a housing bust, the average homeowner gets through it just fine. It’s the most vulnerable homeowners that get in trouble. If only 10% of all homeowners default, it translates into a national mortgage crisis of the kind the US saw during the housing bust.

This comes as the value of residential real estate owned by households declined by $3.0 billion “due to weakening housing resale prices,” Statistics Canada said, adding. “This was the first quarterly decline since the first quarter of 2009.”

With home prices no longer guaranteed to soar, and with debt at record levels and growing, households are immensely exposed to higher rates. Variable-rate mortgages dominate in Canada. Many mortgages adjust nearly instantly to higher rates. Others might have fixed rates for up to five years, and then they adjust. Every quarter-point increase in interest rates puts more strain on homeowners.

When home prices soar reliably, the additional interest costs have little impact overall as troubled homeowners can always sell the home, and since its price has increased, pay off the mortgage. But when prices decline — as they did in Q3 for the first time since 2009 — the entire equation changes.

The Bank of Canada has raised rates twice this year by a quarter point each time – tiny baby steps. And it might raise rates more next year. But even these tiny baby steps push up mortgage costs for Canadian households. And the Bank of Canada is already getting very cold feet, in face of the mountain of interest-rate-sensitive household debt. Now the Bank of Canada and government authorities are trying to walk a fine line to contain the housing bubble without accidentally causing it to implode, with fallout hitting the rest of the housing-dependent Canadian economy.

But the risk appetite in housing continues as the housing & debt bubble ascends to the next level of risk. Read… Canadian Homeowners Take Out HELOCs to Fund Subprime Buyers Unable to get a Mortgage

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf, Maybe I am losing my mind but wouldn’t the 173% ration mean $1.73 for every $1 in after tax income. $173 if true is beyond scary it’s apocalypse.

I immediately thought the same thing.

Yes, there is a decimal point missing.

phil m,

No, you’re not losing your mind. I lost track of a dot :-]

thanks!

The issue is not what happens when the CA mortgage bubble pops, but how will their government handle it? In the 2008 US bubble the financial authorities flaunted the rule of law, by first bailing out failing banks, mark to myth mortgage asset accounting, and blocking the bankruptcy process so people could stay in their homes. The speculative bounce meant people who bought up distressed assets made out handsomely, those who were foreclosed stayed in their homes, or applied for section 8, and rebuilt their credit. There was damn little justice to any of it, and not as much pain as there might have been.

There apparently are no consequences in the financial markets, so we are right back where we were, while the Fed boils the mortgage frogs a quarter point at a time. The Fed is the orchestra leader and they are about to play a dirge, which will remind a lot of people of why they hate the Deep State.

In 2009-10 Canadians bought Florida real estate at rock bottom prices. I was in a real estate office one day when a realtor walked in with a manila envelope full of offers for a bunch of properties. I also heard her say she had Canadian clients for all their listings. Those buyers are now in the black by multiples. The debt in Canada may be hedged by US real estate to some extent.

Thank you for sharing your anecdote…very interesting

Yes, and don’t forget Canadian dollar was stronger than US dollar.

Many happy faces around here.

Cheers from Canada.

yes but the c$ is now weaker than the u$ & fl. r.e. is stagnating – especially the notoriously fickle so. fl. mkt.

The snowbirds who purchased property in FL or AZ after the bust have benefited not only from recovering property markets there, but by a falling CAD/rising USD. But they are a tiny minority among Canuck homeowners. Like Wolf’s article shows, it’s the bottom 3 quintiles – and the bottom one in particular – that will be in trouble. Nobody in the bottom 4 quintiles is hedged with Florida properties. Most of them have never gotten closer to FLA than watching Miami Vice re-runs, never mind owning property there.

good point petunia, however that tide may be turning , to wit :

https://www.azcentral.com/story/money/real-estate/catherine-reagor/2017/07/30/catherine-reagor-canadians-selling-more-homes-than-they-buying-phoenix-area/505404001/

This hedging business sounds like portfolio insurance back in the 1980s. And look how it all worked out. So basically this is how it’s going to shake out. Either:

1. Canada real estate starts to fall, leading to margin calls, leading to firesales in Florida (because there’s no time to do a proper sell), which feeds on itself.

2. US real estate values start to fall while Canadian RE values are starting to fall as well and now you are in the hole for both mortgages.

Is there hope? Yes. If Central Banks were to reverse course and go to negative rates, life is going to be grand.

Hedging does work but only for the first few that sells first.

I hear the Canadians are not flocking to Florida anymore due to changes in their health insurance policies.

True…a Canadian friend mentioned he and his wife now pay $3000 US per month here in Palm Beach county for medical insurance…partly because he has some ongoing medical issues…still, the cheap south Florida vacation condo is not looking cheap or even affordable …

I bet a lot of these condos do on the market in April/ May 2018….

Do those Canadians have Mandarin surnames?

Wolf

Does the Fed increasing interest rates affect mortgage rates in countries like Canada and Australia.

In Canada, yes the Bank of Canada (BoC, our FED) sets the policy interest rate, which affects mortgage rates. Banks offer either fixed rate or variable rate mortgages. You can effectively get a mortgage with a fixed rate for the length of the term agreed upon usually 2-5 years, but then when that’s over you have to set up a new term. Fixed is usually higher than variable but variable is a set amount plus prime (the policy rate).

In short if the prime rate is now 1% and I signed a fixed for 2.2% even if that 1% goes to 3% im shielded until my 2-5 yrs is up. Then I get hit when i sign my new term. If I’m on variable and I have a 1.9% rate (prime + .9%), when the BoC rate goes from 1% to 1.5% my mortgage rate rises to 2.4% almost immediately.

Canadian fixed mortgage rates are based on the bond market, as that is typically where the money is sourced for the term (max 5 years). Thus they are heavily influenced by the US Fed.

The Bank of Canada’s (BoC) Rate influences Canadian banks’ prime rates which are the basis for variable mortgage rates, lines of credit, HELOCs, etc…

The BoC historically tracks moves the Fed makes with a 90% correlation. These tracking moves typically lag the US. In general the BoC keeps rates slightly higher than the Fed to maintain attractiveness to keep people in the CAD$.

I’ve personally watched the explosion of house prices in Toronto since the early 2000’s, your average Joe thinks you can’t loose with real estate, and with mortgage insurance, and minimum down payments of 5%, for properties under $1 million these low rates and cobbling together only $50 grand made it a debt orgy and easy to carry.

There are new stress tests coming in, need to prove your household income, regardless of down payment, can service the mortgage at the prime rate plus 2%.

So far, it hasn’t even affected US mortgage rates :-]

Well the Canadians can do what we Americans have made an art of; suppress the real inflation figures and lie about the fake ones.

We’re already doing that. We’ve gotten quite good at hiding our inflation in “substitutions” and “hedonic adjustments”, just like you guys have.

I visited my son in Canada. 2 bacon cheeseburgers, 2 fries, 2 cokes totaled C$22.00 No, no inflation none at all.

And the Canadian Tim Horton’s coffee- 1 large cup C$2.10

StatsCan, once a well respected gatherer of solid info, is now another political too.

Boy, prices are certainly not falling where I live on Vancouver Island. Not one iota. In fact, it is the opposite. We moved the Father-in-Law near us a few years ago. His house has increased at least 25% in that time…maybe more. Prices are still rising and mucho building going on as folks have cashed out of the cities and move to smaller centres.

This is mid Vancouver Island. New hospital (brand new), sea walkways, ocean views, city of 35,000 with every service and convenience. A $400,000 home here would cost at least a million and one half in Vancouver or Victoria…maybe more. Folks have cashed in, put mega bucks in the bank, and now own their homes outright.

“Folks have cashed in, put mega bucks in the bank, and now own their homes outright.”. You do know there’s another side to the transaction no?

Those people have cashed out, taken out mega bucks from the bank and now owe money on their homes.

Paulo is one of a number of Canadians who show up here regularly to tell us how great everything is up here in Canada. Everyone is mortgage free, making money, driving new cars, and smiling. Nothing bad can happen in Canada. Ever.

What they forget – all of them – is that nearly every economic crisis is preceded by a lengthy period of bliss and seeming prosperity. A period during which it feels like nothing bad will ever happen again. And the more people feel like that, the less prepared they are for the giant $hitstorm that will soon be bearing down upon them.

Those debt figures cited by StatsCan are real. Not every neighbourhood is like Paulo’s neighbourhood. There is a festering pile of debt building up in Canada by the month. There is no easy out at this point. No Get Out of Debt Free card. A major financial reckoning is a certainty. One from which it will take a decade to recover.

It is not Paul’s problem reality that you can’t accept. This blog is bunch of the same people: doom and gloom for everything around us. Well economy is not crushed, cars are still selling in record numbers, real estate is more expensive than ever and it will just be more expensive, stock market is in record territory etc. Many people got rich, enjoy their life and you guys live in denial.

All I can say; Good luck to you.

Pride always come before a fall. Anyway here down under we have a ratio of over 190%. Someone may like to provide the exact figure. Not that’s anything to brag about. It just means we will be going down the “S” bend as well, sooner rather than later. Might say hello to our Canadian friends as we pass through together.

We are actually both holding hands as we get swept around the toilet bowl with ever increasing speed.

The thing is, Canadian median household net worth hit $295,000 in 2016. This is more than double the median household net worth of Americans. Canadians may have more debt, but on average they’re far richer than the neighbors to the south, and they have socialized medicare and other assorted social safety net programs that cushion any market imbalance. Oh yea, the Canadian economy is near full employment, energy prices are on the up again, and they’re attracting top global talent at historically high rates thanks to favorable pro-immigration programs.

Nicko – they are richer because of the real estate they own……if it falls in value, the debt will remain.

Just an anecdote, but I live in the GTA. It has been almost a decade where there have been lots of folks that look very successful, nice cars, clothes, big house……but many of them have used the rising house value as an ATM. As stated above, Cdn mortgages may be amortized over 25 years, but the interest rate is fixed for only a shorter term, like 2-5 years typically. What we see from other parents at the kids school is a lot of folks taking out a HELOC, say $50K, racking it up over 2-3 years and then rolling it into the mortgage when the term is up as the house price has increased. Works great – until it doesn’t.

The effect is that they are living significantly beyond their means, and would never pay off the mortgage. Would require a cut in spending/lifestyle to just stabilize their debt. It’s hard to explain to the kids they can’t have everything as they see all of their friends with the latest and newest toys. However, we are 2-3 years from being debt free (with a house in the GTA). Hopefully one day they will appreciate parents that are not dependent on them financially……..one day, maybe.

I can’t say what percentage this is, but I do believe some folk are going to steamrolled and won’t know what hit them.

The new rules for mortgages come into effect in a couple of weeks, and everyone has to qualify at 2% higher than the posted rate. People will qualify for about 20-25% less than before. Say goodbye to demand. Might get fugly next year in the great white north.

Well said Sector0ne

Problems don’t happen at the median and above. Problems happen in the lower wealth categories.

When the only major asset, the house, is fully leveraged and its price drops, the net worth turns negative. This would be combined with other consumer debt (credit cards) and no savings in the bank and no financial assets. That’s where the problems arise.

80% of that net worth is in housing.

https://www.statcan.gc.ca/daily-quotidien/171207/dq171207b-eng.htm

“Home equity has risen significantly since 1999, reaching a median reported value of $238,000 for Canadian homeowners in 2016. This was an increase of 12.8% from 2012 and 115.2% higher compared with 1999.”

Are you still comforted by the net worth figure? We’ll save the discussion about the unsustainability of rising net worth in the face of stagnating incomes for another day.

A far more informative measurement would be stating assets against liabilities.

$238,000 net worth on $238,000 assets and zero liabilities is a far different world than $238,000 net worth on $1,238,000 of assets and $1,000,000 liabilities.

Especially since the “off-balance sheet” liabilities of the average Canadian includes Government of Canada debt tied with Quebec and Ontario debt.

The Bank of Canada has raised rates twice this year by a quarter point each time – tiny baby steps. And it might raise rates more next year. But even these tiny baby steps push up mortgage costs for Canadian households.

——

For people in Canada with mortgages greater than $400,000, baby steps is not the word they would use to describe the shock of having rates rise when the media, their real estate agent, friends, family and even their bank told them not to worry because rates will never rise in their lifetime.

As for the high home prices and debt binge in Canada, we are still in denial. There was an article a while back stating certain cities have home prices that were higher than Manhattan when you compare the income of the people buying homes to the home value. I can’t convince anyone in Canada this is not normal: they really believe home prices are due to China, immigrants and Canada developing “world-renowned” cities that are attracting new people from across the world. Homeowners, speculators/flippers are not ready to listen, when you show them the sold data of homes in their area, dropping in price over the past 8 months, they just shut down.

I don’t think the Bank of Canada wanted to raise interest rates because it would decrease the amount of money people spent at Christmas (our biggest shopping season of the year). Next year will be interesting, especially if the US keeps raising rates.

The Fed has to increase interest rates, they don’t want to but they have. In Canada look for wage inflation, then you know that inflation is firmly entrenched in the economy. Look at these numbers for Sept, well over 2%, not looking pretty at all.

https://www.bls.gov/news.release/eci.nr0.htm

private industry 2.5

government 2.4

Agree that the real problems for Canadian home owners will be with those in the lower wealth categories … and particularly for those who, through excessive leveraging, have become multiple home owners. Quite some similarities between the current Canadian real estate situation and one that existed in the U.S. around 2007 ….

Take a read through another analysis that nicely complements this article:

https://betterdwelling.com/forget-subprime-canadian-real-estate-buyers-investors-crashed-the-us-market/

That article, and the NBER research, seem to indicate the opposite. It’s not the margins we need to worry about. It’s the middle class specuvestors with good incomes and good credit who caused the US housing collapse. I suspect they will do the same in Canada.

The only thing that drives the price of real estate in Canada just like in Australia and New Zealand of course is the Chinese. Interest rates only show how many locals other than local Chinese can compete with the local and foreign Chinese. Currently all the Chinese cornerstones are falling in price. Richmond Hill, Stouffville, Markham and Unionville. West Vancouver is also tanking. Home prices only follow the Chinese money. A fallacy is low interest rates drive the housing market. We all know that’s 100 percent false as every white area in Canada went no where in price when interest rates fell to near zero. Judging by the real estate market in China and knowing the Chinese will sell their worldwide holdings in real estate before they unload their native real estate in China the future looks bleak for housing in Canada. The Chinese totally destroyed the entire greater Toronto area and the residents aren’t very bright so it’ll take a long time before prices regress to the mean without the Chinese influence. The same can be said for the Vancouver area and Victoria.