Pricing of risk kicks bucket in record central-bank absurdity.

As the days pass, the perverse effects of central bank policies on the financial markets are getting more and more amazing. This includes the record-setting nuttiness now reigning in the European bond market, compared to the mere semi-nuttiness in the US bond market.

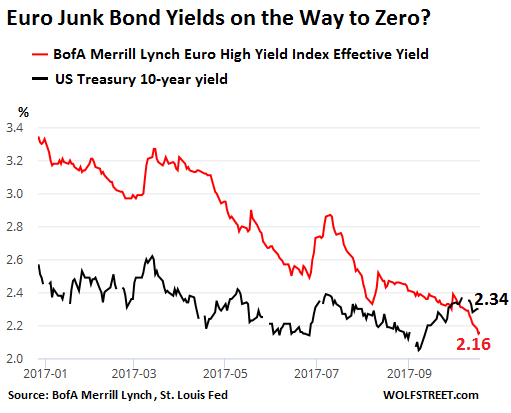

The 10-year yield of US Treasury Securities closed at 2.34% yesterday and at 2.33% today. This is low by historical standards. It’s barely above the rate of consumer price inflation as measured by CPI, which was 2.2% in September. This means that coupon payments barely make up for the loss of purchasing power. If inflation ticks up just a little, bondholders will be left in the hole. And a yield this low doesn’t compensate bondholders for any other risks, including duration risk, which can be significant. In other words, this is a bad deal.

But in this strange world, it looks practically sane, compared to the Draghi-engineered negative-yield absurdity that has overtaken the Eurozone, where the average yield of euro junk bonds – the riskiest bonds out there – dropped to 2.16%.

This chart, based on the BofA Merrill Lynch Euro High Yield Index via the St. Louis Fed, shows how the average euro junk-bond yield (red line) has plunged so far this year, on the way to what? Zero? The 10-year US Treasury yield (black line) has started rising in past weeks and, in late September rose above the euro junk bond yield for the first time ever:

This average junk-bond yield is based on a basket of below-investment-grade corporate bonds denominated in euros. Among the issuers are European subsidiaries of junk-rated American companies. For them, it’s nearly free money.

The nutty thing is this:

These euro junk bonds are rated below investment grade. They have been issued by over-indebted companies with a considerable risk of default. Liquidity is low in the corporate bond market, and it can be difficult to sell the bonds when the selling starts. And unlike the US government, which prints its own money, corporate entities can – and do – go bankrupt.

But the ECB has been buying all kinds of securities, including corporate bonds, in its efforts to push yields down. As yields fall, bond prices rise. And so it has created the largest credit bubble ever.

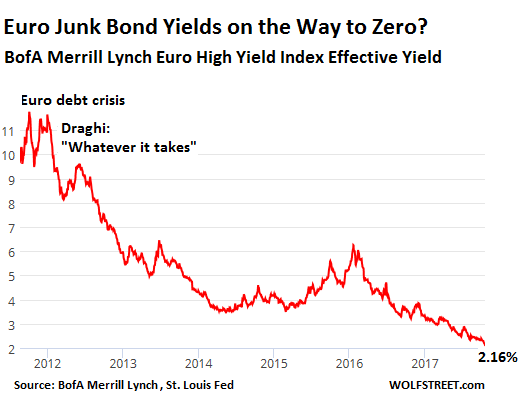

This started in the summer of 2012, when Draghi pronounced the magic words that he’d do “whatever it takes” the bring sovereign bond yields down. This was designed to save Italy and other periphery states from default. The average junk-bond yield had peaked during the debt crisis at around 11%, and at 25% during the Financial Crisis. By October 2013, it had dropped below 5% for the first time ever.

This chart shows the path of the euro junk bond yield since the debt crisis, from over 11% to 2.16%:

That the average euro junk bond yield is now 2.16% has special meaning when compared to the 10-year US Treasury yield that, at 2.34%, is so low that the Fed has been publicly fretting about it.

US Treasury securities have a credit risk of near zero because the US government cannot go bankrupt because it can always print more money via the Fed. And the US Treasury market is the most liquid bond market in the world. The risks inherent in Treasuries are incomparably lower than those inherent in euro junk bonds with equivalent maturities. So investors should be paid a lot more for holding risky junk bonds.

Thanks to Draghi’s scorched-earth monetary nuttiness…

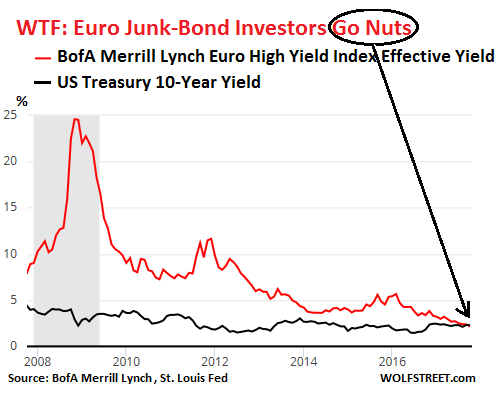

The 10-year US Treasury yield and the average euro junk bond yield over the longer term form this WTF chart:

The chart shows how investors used to be compensated with extra yield for taking on the very real risks of euro junk bonds, and how that risk premium completely disappeared over the past year, and how in recent days it even inverted.

Plenty of these junk bonds will default. Investors will be left to lick their wounds. And they know this. But these are institutional investors, such as pension funds and life insurance companies that offer pension products in Europe and elsewhere. They’re administering the future pension payouts of retirees. They’re plowing other people’s money into this junk-bond sinkhole because they’re obligated to.

The bag-holders are not money managers, but future retirees.

Some pension payouts beyond the required minimum (such as the Überschussbeteiligungen, as they’re called inimitably in German) have already gotten slashed, and many more will experience the same fate. In the process, the future consumption of these retirees is being slashed too — and there will be a lot of them in aging Europe. Borrow from tomorrow to commit this nuttiness today.

Draghi’s only hope is that he can keep this scheme together until his term expires in 2019, and that someone else will have to deal with and get blamed for the consequences.

In the US, the ballooning National Debt has magically disappeared from the political agenda, but the stock market has suddenly taken center stage. Read… Mnuchin Deploys Stock Market Bubble as Political Weapon

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

If the ECB is the only buyer of these bonds, then it’s a virtual yield, but has an impact on the yield of government bonds with probably negative yield to maturity. The future of Euro retirement funds looks bright /s. Imagine what the EU exit forces would be if the average Joe actually cared and understood all this stuff. Sadly, there is plenty of political scandals to keep them entertained.

The ECB doesn’t actually buy junk bonds, though it ends up with junk bonds when companies get downgraded to junk, but then it doesn’t sell those bonds.

The mechanism with which junk-bond yields are pushed down is via all other bonds, including bonds with negative yields. The ECB is taking bonds off the market essentially, and everyone is chasing bonds where they can get them, which creates demand for those bonds, which pushes down the yield. As the yield falls, investors chase ever riskier bonds to get a little yield, and eventually, they drive down the yield on the riskiest bonds out there. This is not virtual. This is real.

A tax lawyer once explained to me the problem with government pensions. Let’s say it takes you 20 years for your pension to vest. That means that every year you work, you have earned a 5% vesting interest.

That earning is income, and you should have to pay tax on that income. Why don’t you? Because it is exempt from taxation. Why? Because governments worldwide don’t want workers to have an individually enforceable right in pensions, which would allow them to go into court and control how the money they pay in, is invested–as well as the money paid in by the corporation. If they paid a tax on that earning, they would have that right. We live in an era in which the governing doctrine is that almost all control over almost all facts, is in the government.

Since workers don’t have this right, governments are free to load up pension plans with junk debt.

This is just one way in which governments make the population complicit in their policies. This is why it is impossible to say you have “earned” a pension, by virtue of a property “right.” You didn’t pay taxes on it? It’s not your property.

And when proposals have come from unions to have their members taxed on vesting interests as income, workers never allowed it. They wanted to keep that money.

So don’t tell me there are heroes and villains here. Every government tries to rope in the population to be part of the decision-making process. That way, when things collapse, people can’t simply “blame the government.” The people are also to blame.

Of course, if things get bad enough, people won’t care how complicit they are. Survival comes first–unless you can indoctrinate the population into the belief that under severe enough social circumstances, then it is right that they should die.

Anyway, this is the legal means by which governments are ruining pension plans.

Related to govt involvement in pensions:

What portion of the typical workers / retirees income/savings doesn’t the govt have a large hand in / know about?

Paycheck, 401k, IRA, Corp or govt Pension, SocSec, MediCare, MedicAid. Others? Prolly lots I’m not thinking of….

Point is, we have all been herded into a big financial pen in which the govt makes the rules on disbursement and prints the script at will.

How many people actually have cash/ or precious metals on hand outside of this system? It’s going to get uglier no matter what your position is, but at least holding assets outside the the purview of the govt, you are not destined to be a total pawn.

“How many people actually have cash/ or precious metals on hand outside of this system? It’s going to get uglier no matter what your position is, but at least holding assets outside the the purview of the govt, you are not destined to be a total pawn.”

To much cash is worthless as they will do a modi and change the currency (make parts of it worthless overnight $ 100.00’s Perhaps) with out prior notice.

Thing’s outsid the system should be considered by everybody.

There is a Rand report on the history of military pensions.

In 1940 they did not have computers to do all these calculations that your lawyer friend is talking about. To keep it simple they decided to underpay the military (and probably federal employees too) compared to their civilian counterparts and consider that as paid-in for retirement benefits later.

Once computers allowed these computations, the government required the military to set aside an amount in a virtual military trust fund to properly account for the cost of personnel. They started that virtual set aside account in the 80s at zero not taking into account any past reductions in pay that were not accounted for. So even if there was really money set aside (there isn’t just like social security), it did not reflect the previous pay-ins from underpaid salaries.

When retention became a problem, the government “caught up” military pay with civilians but they left the benefit formula the same. This means the pension benefit is calculated on a higher base wage than it was meant to, but…

…what is not understood about military pensions is that they are not based on total salary they are only based on a portion of pay which is approximately 70% of total pay today (less than in previous eras). So that 50% at 20 years you hear about is actually 35% which rarely compensates for the loss of income when one transitions out of the military.

So while one part of the formula appears to overpay, the other part takes it away. Military pensions have held steady compared to GDP since they began. Calls to cut military and federal pensions usually come with a lot of mis/dis-information.

I completely agree on your point about other pension funds being captured by the central bank distorted financial markets. I have no doubt they will not bail out pension funds like they did the banks. The transfer of wealth will be completed after the next crisis. Then they will go after military and federal pensions to match the destruction they created in the private sector and states.

The scheme in may nations for over 20 years has been to phase out, all, state funded, guaranteed, or backstopped pensions.

One of the next thing you will see is more of the.

Peopel are living longer so the “State Pension ” age must raise, to 70, then, 75 then 80 Etc, until almost nobody is ever eligible for one.

Australian and England are already 67 next it will be 70.

Its actually a race to see if they can lock out most of the post 58 baby-boomer tail-end for ever. As they are talking about raising the age again around 2020..

That’s a good explanation. So if QE unwinds there should be more bonds on the market (the Fed is buying less) and the HY spread should normalize? The standard reason for a drop in the yield of risky assets is improved economic activity, which even Yellen has come to doubt.

True price discovery, when it can no longer be deferred by the Keynesian counterfeiters and racketeers, is going to be cataclysmic.

and this is why i tell everyone to start a garden.

Maybe more than a garden? Maybe a rural hideaway which can supply more than a few vegetables?

There never will be true price discovery. Didn’t you know that the central banks have waived a magic wand and wished true price discovery away forever?

They are here to stay. It will be deferred forever.

You say that, but aren’t you concerned with what happens in 50 years? 100 years? 200 years?

These things can only be deferred so long and you must start worrying now about what may happen to your grandkids, or their grandkids, or their grandkids.

Afterall – your wouldn’t want to be wrong just because you didn’t have the patience (or life expectancy) to stay true to your convictions would you?

What kind of a weak copout is that?

I know plenty of folks who take no interest in any of this stuff, but it warms my heart to know they’re most probably wrong.

I think Joan of Arc was being sarcastic, as she often is.

These are bonds. They have a maturity date sometime over the next few years. They will either default or make it to maturity and be redeemed.

On those that default, investors will lose a lot of money.

On those that make it to maturity and get paid off, investors will about break even with inflation.

There is nothing to be deferred about these bonds.

However, if junk-bond yields are close to zero by then, it will be easy to issue new junk bonds, even for zombie companies, and use the proceeds to pay off the maturing bonds. And thus the “deferral.” But at some point, corporate entities tend to go bankrupt. Then it’s over for those bondholders.

Correction . Reality can be temporarily deferred . But reality being what it is despite all attempts at self delusion – Peter Pan thinking and the perception of immunity due to non-existent exceptionalism Reality will have its day . And when it does … suffice it to say all hell breaking loose is an understatement

Re the ‘deferral period’:

The term may be defined from the perpetrator’s point of view as “when I’ll be gone and you’ll be gone”. Then it becomes a hot potato. European kick the can is a viable counter strategy.

This concept should be useful in providing time horizons for this and that eventuality and how it is dealt with.

Joan

I believe the idea that a straw can break a camel’s back. There will come a time when something will unravel and all sorts of wonderful (sarc on) things will happen.

Gershon

Your precis of Wolf’s posting is a beauty to enjoy. CATACLYSMIC!

I have never seen a universal definition of “money”, I generally use currency, as the US Treasury prints currency and IOU’s as does the Fed and they have printed a lot, as most central banks have. The blow up should be spectacular, sadly it could end up in a depression.

Fed = Federal explosive device.

Gold is, and has always been money. CB’s hate it because it is and they can’t print it.

“All the money and all the banks in Christendom cannot control credit…Gold is money and nothing else.” – JP Morgan’s 1912 Congressional testimony on “the justification of Wall Street”

Currency is money in so much as it is backed by gold, and not the “full faith and credit” of a nation. With $20T in debt and untold $T’s in unfunded liabilities, how much is that currency really worth? About 4 cents since the formation of the Fed in 1913.

“Fiat money eventually always goes back to its intrinsic value – zero” – Voltaire

Free Lunch

All the mom & pop investors are buying the market today because we’re getting a new tax break. Nice.. May God bless all of them. They will need God’s help soon enough

Can you name an inverse ETF or 2 that would benefit from a Euro Junk bond crisis?

Perhaps of interest, Jim

http://www.zerohedge.com/news/2017-10-19/best-way-bet-fed-losing-control-bond-market

Watch, as US rates surge, lol.

Relax, Janet Yellen doesn’t believe we’ll see another financial crisis in our lifetime.

Everything will be free, including money. Reality no longer applies,,,,neither does gravity.

Gravity does apply. It is pulling down manna from the central banks.

And gravity applies to my income as well. I just finalized my taxes on 10-15 and 2016 was the worse year i’ve had in 10 at least. I knew it was bad but the level of suck was off the charts.

2014 was the last good year I had and fall of that year it was as if somebody had turned a switch and the work just dried up.

oddly, 2017 has been pretty good.

Wolf, did you see this piece in the WSJ from a couple weeks ago? Apparently they fell off the wagon too.

https://www.wsj.com/articles/looking-for-bubbles-in-all-the-wrong-places-1507208455

The writer’s reasoning is “…double-B-rated credits on both sides of the Atlantic trade at an almost identical spread level around 2.1 percentage points above their respective government-bond yields.”

Best part is how he ends the article, exclaiming “Bubble chasers should look elsewhere.”

Actually the spread-part of the statement is correct, when euro junk bond yields are compared to German yields, and US junk bond yields to US Treasuries.

The 10-year German yield today is 0.4% and the average junk bond yield is 2.16%, so this spread is 1.76 percentage points.

The 10-year US Treasury yield today is 2.33% and the average BB-yield is 4.1%, so this spread is 1.77 percentage points.

BUT… the insanity + absurdity + bubble are:

1. The very narrow yield spreads on BOTH sides of the Atlantic.

2. The very low yields in the US.

3. And the ludicrously low yields in the Eurozone.

To claim that this isn’t a bubble is sheer propaganda.

I wasn’t disputing the spreads, but rather the rational. Is currency hedging even a justifiable reason for buying this euro junk?

The risks of these junks bonds are huge, the rewards very limited at this point. Currency hedges are undertaken to lower exchange rate risk, but if you try to lower exchange rate risk by cranking up credit risk, the whole equation falls apart.

Very interesting. Thanks Pl’n’l

Can the ECB buy USA debt bonds?

The ECB doesn’t buy anything denominated in dollars.

It buys only bonds denominated in euros, and issued by European entities, which can be subsidiaries of US companies (“Reverse Yankees”).

“Draghi’s only hope is that he can keep this scheme together until his term expires in 2019, and that someone else will have to deal with and get blamed for the consequences.”

There was talk here the other day ( I think it was here) that his hat is in the ring for another term.

Heaven forbid.

This ECB mafiosi mess, intended to prop up, Italy, Spain, and greece, has the potential to plunge the world into a depression.

The likes of which have never been seen before.

There is talk that 40 – 70 % of these “Reverse Yankees” are unhedged and that hedging them which is becoming a necessity a the Eur has stopped dropping v $ will cause an even greater resurgence in the Eur price (Note I said Price. Not Value) which is an even greater negative for the whole EU.

This whole global situation reminds me of the conditions required for nuclear strike assessment (in The Bears Tears). Except that

The global financial situation, is much much closer to the strike point that the soviets ever got.

If this thing goes off the three ugliest, china russia and the US, will be left standing but none of them will be very well. Or happy. Which bodes ill for their next moves.

Unless someone who intents to normalize rates and keep them normalized takes charge of the Fed soon, this will not be just an ECB story.

Bernanke got the ball rolling with low rates and QE. The other central banks got in on the act for various reasons, all of which involved printing money and lowering rates. Governments benefit from monetized debt and lowered borrowing costs. Normal expenses are now covered by printed money. Negative rates serve as a tax on savings. Low rates and excessive available cash provide wealth for people who know how to skim cash from asset values that continually rise in price due to bubbles.

The game was to beat the system by having each major world governmental unit print almost unlimited money. Competitive devaluation would not result if everyone was doing the same thing. Everyone could live off of artificially low rates and central bank printed money. Savers would bear the cost by seeing their earned capital evaporate by negative rates or by spending it out of necessity. The wealthiest would prosper even more by skimming cash from artificially rising asset prices. It was in effect institutionalize class warfare started and maintained by governmental entities for the benefit of a small minority of rich people. Almost a pre- Hunger games environment. Dystopia rising. Low wages and open borders for flexible labor and resource movement close the loop.

This may still happen. If anyone else had won in 2016, negative rates in the US would be a strong possibility by now. After all, somehow everyone decided we need inflation to raise rates, yet excessive money printing with artificially low interest rates is deflationary. The Fed is on a snipe hunt. The inflation excuse is a farce. Printing money was seen as manna from heaven and the entire game could be scammed if everyone did it. Only people who didn’t matter and would believe anything they were told (savers) would pay the cost.

The game may continue if rates don’t normalize in the US. Negative rates in the US are still a possibility down the road.

FYI. Your interest expense is my interest income. I spend interest income. You will borrow only for good reason. Many people borrow for capital investment. If rates are high, this capital investment will create jobs as a by product. This cycle creates economic growth and has existed for thousands of years – ever since someone saved the first money and someone else needed to borrow some.

If rates are low, it will be to flip paper assets to others who will flip them later just to gather the skim from money printing. Unless the Fed is stocked with traditionalists, the dystopia scenario is a definite eventual possibility.

If the US ever got negative rates, here’s a long shot way to end them (low probability of success but worth a try in desperate times):

Negative interest rates are a tax on savings. The Fed is not legally authorized to impose taxes on the general public, or possibly anyone for any reason. Only bills introduced in the House and approved by both houses of Congress and the President may raise revenue. Thus, unless the Supreme Court is in on it, negative rates might be ruled illegal here. Not that a willing group of governmental flunkies wouldn’t try.

Low rates have fueled massive capital investment and jobs. But in a globalized economy, none of that has benefited the US. But China has seen massive capital investment and job growth. At the expense of American savers.

On the upside, at least for the American capital-owning class, their control of wealth is no longer threatened by the whims of the the American working class.

“… (savers) would pay the cost.”

That depends on what’s being saved.

U.S. dollars in a bank savings account, yes.

Savings elsewhere (land, precious metals, other so-called “stores of value”) contemporary fiat money pricing doesn’t matter.

“The fact that the world, as a result of quantitative easing, has seen an asset inflation that benefited the uber-rich, and that nothing has been cured. One cannot cure debt with debt, by transferring from private to public sectors. The markets will ultimately crash again, although this time it will hurt a lot more people.”

–Nassim Taleb

Can we say that there will be a Bastille day, again?

Wolf

Inflation is higher that 2.3%. So those who hold bonds will lose money- in the real world.

How do you think this tax bill will affect bond prices?

We know about stocks and the wealthy.

It is well to remember that economics, the [stock market] “economy” and “money” are all human intellectual constructions with no physical basis. As [financial] “risk” is an internal logical result of these constructs, it also has no physical basis.

In many ways we are fighting over moon beams, smoke and mirrors.

IIUC the Kirchner/Fernandez government in Argentina avoided the pension fund investment [bond] trap and placed most of the assets in their governmental pension funds beyond the reach of the bureaucrats/politicians by investing the bulk of the pension funds in affordable housing. The assets of the pension funds are thus real houses/condos on real property, and the retiree income stream is the [adjustable rate] mortgage payments the owner/residents of the affordable housing make. Not a perfect solution but seems to have solved several problems including providing employment and domestic development.

Interesting. Imagine, investing in citizens’ standard of living as a path to future security, whodathunkit?

And partly explains neo-liberal animus towards Kirchner/Fernandez. Chicago-boyish Macri must be trying to roll all this back, no?

RE: Chicago-boyish Macri must be trying to roll all this back, no?

—–

Indeed. He appears to be honest in convictions/ideology [reactionary neo-liberalism] and is imposing massive spending cuts and austerity in education, research, infrastructure investment, etc.

Many of the protective tariffs have been removed, and the imported goods are indeed now cheaper than the domestically produced goods, but the resulting massive unemployment means increasing numbers of people can’t afford the cheaper goods. Massive [+400%] increases have also been made in the electric. distillate fuel, and natgas rates triggering the bankruptcy of many small to medium businesses.

This appears to be a rerun of the conditions/policies that drove Argentina back to barter in 2002.

Europe Junk Bonds rate is x5 times more expensive than the

German Government 10 years Bond rate @ 0.4%.

Europe Junk cannot go even lower because of the US Government

10 years rate.

Since Jan 2015 $WTIC, for almost 3 years, is in a triangle.

The downtrend will resume. That will put the energy sector junk

bonds, or 1/2 a Trillions ($) of junk, at risk.

There will be an outflow from junk and stocks into US Government

and German Government 10 years Bonds.

That will happen after the Fed will raise the short end of the curve,

flattening the curve further.

If the purpose of bond buying is to lower rates, presumably to create the “wealth effect,” how are those low rates going to help the economy? Credit card rates are still usurious, so that rules out any benefit to the consumer economy. But it’s good for banks. Housing bubbles draw money out of the economy, as more income has to be used to make mortgage payments. Not surprisingly, this also helps banks mightily. Can anyone get the “economists” at the Fed to explain why they keep doing what they do despite the utter failure of their actions? Or is saying “it’s good for the banks” too politically incorrect?

Negative rates are tax on saving, but pension funds can earn

their annual 7% when the stock market rise from $SPX = 667 in

March 2009 to 2,571 now. Or, when junk fall from 20% to 2.16%.

The point is different.

The “experts” claim that the top 1% own 90% of all assets.

The reality is that the middle class send their saved money to the pension funds and they own a big chunk of all assets.

These two statements contradict themselves, providing logic to

people anger and protests.

But soon everybody will be so happy, when the poor, the middle class

and the rich will have equal assets.

So, why would anyone ever buy a European junk bond when they could buy a US 10-year? Fears of FX fluctuations?

1) rising us rates decrease value of bond = capital loss

2) opm is easier to spend than your own money

3) decreasing rates cause bond values to rise … possibly hoping to sell for gain if rates really drop a lot more

if big US stock market crash, flight to safety into bonds would allow people to sell euro-junk and profit from rising US bond prices.

Better question might be: Why would anyone who doesn’t need to live on a 2% yield buy any such bonds?

And why not buy gold?

If ultra low interest rates are largely a symptom of money printing in its various forms, and with bond markets thus ultra over priced, might

gold at just ~$400/oz over the 1980 high of $800/oz, be a screaming good value for those with some patience and foresight?

Exactly But why not do both and some silver and rental property in a good location as well Diversification I’d say Bitcoin but I’ve yet to fully understand it

Of course, if you can buy a sound, money making rental property, that isn’t price to perfection at the time of purchase, Then I guess by all means do it. However, I don’t think there were too many of those around at this point in the cycle.

With respect to bitcoin, have you read/know about Nassim Talibs anti-fragile book? When the sh@t hits the fan, you gonna want to be in stuff that goes up in price with volatility/bad times. I’m not so sure at that point bitcoin is going to be a Safehaven. At this point in time crypto currency‘s r simply way too risky with respect to scam possibilities.

Simply holding physical gold is a pain in the but enough. Crypto currencies? Oy vey !! :)

With respect to the other post talking about getting the Price / timing right for gold?

Well sure, that holds for everything, no?

Buy anything going the wrong direction, and you gonna lose money, at least for a while. But my point is given that gold is only 50% over where it was in 1980, And given the phenomenal amount of money printing that has occurred since then, does that not make gold / silver the best values out there? What is else is only just 50% over its 1980 high?

You pick the 1980- high which is a little self serving.

better at least to start from the 30 at the end of bretton woods.

When silver had a 20 multiple roughly to gold.

So even with overpriced silver today there is a $ 950.00 Divergence due to upward manipulation of gold price.

The 20 multiple is and old old relationship that predates written history.

Nobody suppress the price of a commodity (Silver) in favour of poor buyers. Which is what the Gold Bugs claim, is in fact happening.

No matter how the divergence came about, that divergence is a HUGE problem. For current buyers.

Gold at a 1000 (APP) over browns bottom is much better.

Particularly if you shorted it down from 2 K to 1200 in the next cycle. which I did.

Gold is only money if you buy at or near the correct price.

Spme how I do not think I will live to see it at 300 again.

Surging 10-year bond rate is going to make it harder for Yellen to pull off her patented “Lucy-and-the-Football” punting routine on rate hikes next FOMC meeting.

https://www.marketwatch.com/investing/bond/tmubmusd10y?countrycode=bx

Why is buying corporate debt by central banks allowed ? All big central banks are doing this. FED BOJ PBOC BOE EU etc Is this not against WTO rules ? I don’t understand this. Are we not already in a trade war via central banks supporting their companies. It looks like you not need tariffs to final kill your competitor in country x. as long as your central banks just keeps rolling over your debt at zero pct you will finally win if you have access the reserve currency ?

The environment for TIPs should improve, since inflation is a constant, and is fueled indirectly by accommodative monetary policy.

Inflation is a manufactured constant, not in the sense of physics constants like the gravitational constant.

Per Lee X comment:

I have never seen a universal definition of “money”,

Here goes (my definition):

Money is a token of value in an accounting system that tracks the exchange of promises for goods and services.

In short, the financial system is an accounting system. Printing money is creating fraudulent bookkeeping entries. We are in trouble because the accounting system is fraudulent. Think Enron.

Good money is a token which cannot be easily counterfeited. If we discover a mountain of gold somewhere, even gold won’t be good money anymore. Money is only valuable as a token in the accounting system. By itself, gold is good for jewelry, electronics and filling teeth.

“By itself, gold is good for jewelry, electronics and filling teeth.”

Tell that to the Cambodians and Vietnamese (Mostly Ethnic Chinese, Vietnamese and Cambodians). Who had to pay with it, to be allowed to board those boats, as refugees, post the end of the Vietnam war.

They will laugh and tell you when TSHTF. US $ are F F worthless.

I think the easiest way to view this obvious paradox (10 -yr vs. Euro Junk) is to just realize it is all junk rated. We know the US pensions are way out of whack, we know there is little ability to pay off the US debt, we know there is no US taxation system that will work to make these US issues (pension + debt) go away.

So it is all junk, all of it. So the real question is if it is all junk, it must be amazing buying by EU to get the corporate junk down to the US 10-yr rate.

Interesting times.

Ha Ha ! That’s the market sentiment – eversince Alan Greenspan showed the way Central Bankers have written a put option to the market and that too ‘free’ so the pricing of risk has gone haywire. Why to only blame Draghi? Hes just following the available precedent albeit an agressive one!