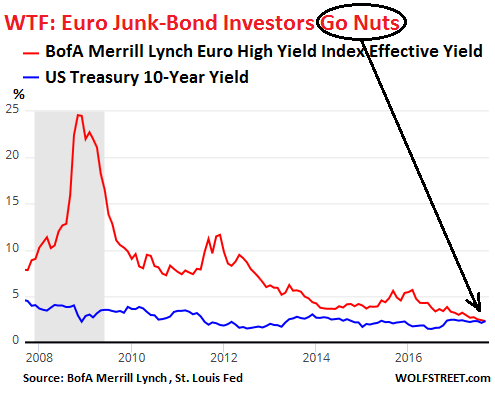

US Treasury Yield v. Euro “Junk Bond” Yield. A new record in central-bank engineered absurdity.

US Treasury Securities with longer maturities fell this morning, with the 10-year Treasury yield rising above 2.37% early on and currently trading at 2.34%. This is still low by historical standards, and it’s still in denial of the Fed’s monetary tightening: Four rate hikes since it started this cycle, and the QE unwind has commenced as of today. But it cannot hold a candle to the Draghi-engineered negative-yield absurdity still unfolding in the Eurozone.

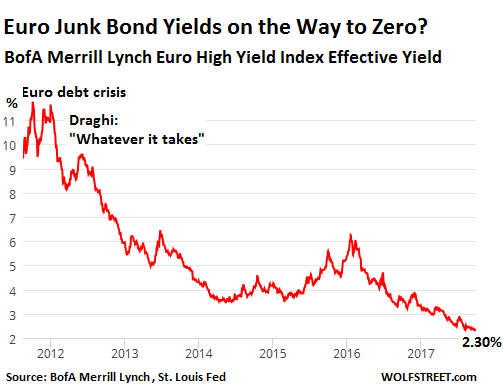

The average yield of junk bonds denominated in euros hit a new all-time record low at the close on Friday of 2.30%.

Let that sink in a moment. These euro corporate bonds are rated below investment grade. Companies, unlike the US, cannot print their own money to prevent default. There is little liquidity in the junk bond market, and selling these bonds when push comes to shove can be hard or impossible. The reason they’re called “junk” is because of their high risk of default.

And yet, prices of these junk bonds have been inflated by the ECB’s policies to such a degree that their yield, which falls as prices rise, is now lower than that of 10-year US Treasury securities that are considered the most liquid securities with the least credit risk out there.

The average yield of the euro junk bonds is based on a basket of below-investment-grade corporate bonds denominated in euros. Issuers include junk-rated American companies with European subsidiaries – in which case these bonds are called “reverse Yankees.”

They include the riskiest bonds. Plenty of them will default. Losses will be painful. Investors know this. It’s not a secret. But they don’t mind. They’re institutional investors plowing other people’s money into these bonds, and they don’t need to mind, but they have to buy these bonds because that’s their job.

This chart, based on BofA Merrill Lynch Euro High Yield Index Effective Yield via the St. Louis Fed, shows that the average euro junk bond yield is on the way to what? Zero?

During the peak of the Financial Crisis, the average junk bond yield hit 25%. During the dog days of the euro debt crisis in the summer of 2012, when Draghi pronounced the magic words that he’d do “whatever it takes,” these bonds yielded about 9%. The yield dropped below 5% in October 2013, for the first time ever.

This juxtaposition of the already low 10-year US Treasury yield and the even lower euro junk bond yield creates one of the most fascinating WTF-charts for our amusement at central-bank absurdist policies – and we’d be laughing at these bond investors gone nuts, if it weren’t so serious:

The ECB’s monetary policies include negative deposit rates and vast purchases of securities, including euro corporate bonds, as long as they’re not junk-rated, though it holds bonds that were downgraded to junk after it had acquired them, and it holds bonds that mercifully are not rated at all.

This has pushed yields on various government bonds below zero, though the Eurozone’s consumer price inflation is alive and well at an annual rate of 1.5% in September, despite the fake-deflation mantra that has long become the laughing stock of consumers who are confronted on a daily basis with rising prices.

,_2017,_September_2016_and_April-September_2017-e.png){kind=link}

With the average junk bond yield at 2.30%, investors are barely able to stay ahead of inflation at the moment, and get no compensation for the large credit risks they’re taking. In other words, credit risk is not priced into these risky junk bonds. The reckoning will be painful for them.

But this is Draghi’s ultimate accomplishment in his nutty bailiwick: The total destruction of the market’s risk-pricing mechanism at the expense of other people’s money – this includes pension funds and life insurance companies that play a large role in Europe’s private pension system. They have to buy corporate bonds. Their beneficiaries that paid into the systems will have to bear the costs in future years. And then there’s the comforting thought that when markets can no longer price risks, they cannot price anything at all because the price of risk underlies all prices in the financial markets.

These central bank policies have created extraordinary asset price inflation. Read…. The US Cities with the Biggest Housing Bubbles

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Big banks around the world have trillions and trillions of dollars worth of garbage on their books, so if you’re a central banker, what’s a few trillion more when it comes to junk bonds? Protecting corrupt banks is what corrupt central bankers do.

Yet there is a trade-off and opportunity cost in everything (one of the few useful things one will actually learn studying economics before it becomes an asinine garbage heap) and it seems obvious to me Central Banks must eventually reap what they have sown. The question that’s been dogging me is how this boom cycle, despite it’s weakness, has been able to survive so long. I’ve had to concede that Central Banks can keep a ridiculous system going for a long time. You really can’t fight the Fed. The Fed is getting hawkish but what if they weren’t? How long could stupid stuff like what we see above courtesy of the ECB continue until it imploded in on itself? You can’t have junk bonds trading like this across the world indefinitely right? The Fed will probably pop the economic cyst even if it tightens slowly which will ripple through the global economy. Next time after the crash and burn phase will they turn to become perma doves or will they still even be around? I don’t know but in my view there are massive storm clouds on the horizon and they’ve been there a long time growing.

Thanks again Wolf.

The world has indeed gone nuts as you so aptly put it.

Is there no more RISK?

As I look around, all I see are risks. The world seems full of risk. Hurricanes that are larger than ever before seen. N Korea. The Tweeter and Chief and his war on things we have accepted as normal. Las Vegas. Companies that are hollow shells with huge amounts of debt that are valued in the stratosphere. Republicans who ran for office on being fiscal conservatives who now seem to accept trillion$ deficits going forward with some vague reference to monetary policy that any thinking observing human understands are false assumptions orout right lies.

Maybe I am just a paranoid that just doesn’t understand risk any longer. Because obviously there is no longer any risk.. WTF is going on in the minds of these supposedly highly educated policy makers?

The question is at equivalent rates is Euro junk as good as US treasuries, or are treasuries junk?

Great question! I was just wondering if the European junk bonds were mostly European bank bonds. But as Wolf points out many of the Euro junk bonds are bought for pension funds (both public and private) and so the bet probably is that the Euro governments will support failing issues to keep the pension funds from eating the losses. So the answer to your question may be that they are as good as US treasuries (if the Euro governments are viewed as being as creditworthy as the US government).

Also there are no federal eurobonds so company bonds are the only way to spread across the ez(company might cross euroborder, in the same way us companies can be in multiple states

Excellent point!

They both are.

Risk is a board game. The object of the game is apparently to get all the players to lose their tempers.

In finance, the absence of risk essentially amounts to division by zero, which could eventually allow prices to achieve orbit and burn up on reentry some time thereafter.

What I fear is we’ll jump from ‘RISK’ .. to ‘NUKIM’ !

“the absence of risk essentially amounts to division by zero”

Well-stated and consider that one stolen.

Globally these central bank clowns are still printing…. so this madness is going to get even more mad first.

In other news, there is a new crypto index fund called HOLD 10 and the Greyscale Bitcoin Investment Trust trades at 80% of NAV. And gun stocks went up today.

What a marvelous world.

“trades OVER 80% NAV”

Yikes ! The value of the underlying asset has decoupled from its exchange traded price by a large margin . This is, well , I can’t think of anything rational.

So I read this book by Dr. Robert Gordon, and economist at Northwestern. He has this theory that his book provides some convincing evidence of, that we are living in an era of an extreme lack of technological change. The core idea being that a person alive in 1955 would recognize the technologies we have today. In fact, said person would likely be amazed that we haven’t progressed further (no flying cars?). However, a person alive in 1895, would think the level of technological change in 1955 would be astounding! Television, jet aircraft, nuclear reactors, computers would be unimaginable.

So suppose interest rates should represent the cost of money. With that cost being higher when demand is higher. And suppose that we actually live in an era of low technology change. Then the demand for money to invest in new technology should be low. Right? Perhaps interest rates are low because central banks can’t really push them higher. Low interest rates should spur investment in marginally profitable enterprises. Which would increase employment. But suppose those investments don’t exist at any level of interest rates?

If we lived in a world in which massive amounts of money exist, but there are actually very few places to profitably engage that money, then wouldn’t we expect interest rates to be unusually low?

Your last sentence: “If we lived in a world in which massive amounts of money exist,…”

Yes, that’s the world we live in. That has been one of the themes of this site since it started. That money comes from central banks, as a result of QE (asset purchases).

Central banks buy bonds (or other assets) with money they create. This money then starts circulating, looking for a place to go. The amount of money central banks have created since the Financial Crisis was about $11 trillion last time I checked (not including China). They also repress short-term lending rates (in some instances below zero), and thus make leverage nearly free of carrying costs. This has vastly increased leverage, which creates more buying pressure since this borrowed money is used to buy assets, such as bonds, which causes higher bond prices and lower yields (interest rates).

This has nothing to do with technology, and everything to do with central bank money creation and interest-rate repression.

All this is a standard recipe for hyperinflation.

Hendrick

You’ve nailed that one for hyperinflation.

Wolf,

I’m brought back to earth by Hemingway & “The Sun also Rises”

“How did you go bankrupt?” Bill asked.

“Two ways,” Mike said. “Gradually and then suddenly.”

Then I think of Toys R US & their bankruptcy filing. 3 weeks prior to their situation of how fast their bonds went from basically par to 19 cents on the dollar.

https://www.bloomberg.com/news/videos/2017-09-19/toys-r-us-seeks-bankruptcy-as-debt-mounts-video

In no time.

I recall September 1987 feeling very smug long of $160k of equities only to see that chopped in half by November 1st 1987. It can happen fast..

The vast bailout sum spent by the Fed between 2008 and 2010, $26 Trillion, [a lot more than the $11 t you mention] is I believe nearly all in the financial sector of the economy, insulated from the normal economy.

Some of it is asset inflation which we all have to live with, but the normal economy of goods and services etc is in deflation. The banks are siphoning off most of the money actually circulating leaving punters with insufficient funds to spend into the economy and often close to distress with debt repayments:

https://www.domain.com.au/news/alarming-sydney-households-need-to-earn-190000-a-year-to-avoid-mortgage-stress-20171001-gyloba/

It’s all a big debacle in the making. Probably it can’t come soon enough.

I agree with your statement: “The banks are siphoning off most of the money actually circulating leaving punters with insufficient funds to spend into the economy and often close to distress with debt repayments…”

This is a big problem with the US housing market too.

But let me just clarify something. The Fed’s bailout funds, such as the TALF program and many others, were huge and probably in the range you mention. The Fed acted as lender of last resort to those banks and companies (including GE, CAT, and other industrial companies) because the credit markets had frozen up and they could no longer borrow to meet day-to-day outlays, such as payroll and other obligations. But these were short-term loans that have been repaid in full.

QE was different. It wasn’t designed as bailout. It was designed as asset price inflation mechanism. It was in addition to the bailout funds you mentioned. QE wasn’t short-term loans. Instead, the QE money is still in the markets (though the Fed started today to drain some out of it).

KentQ:

I am one of the 1955 baby boomer(median) individuals. Growing up, The Jetson’s was one of my favorite TV shows. I knew it was not real. Reality was 1963, 1968, 1973 and 1980. Take your pick or add some years.

Kentq, That argument is true on the surface and there is lots of money in the system. The technology has advanced quite dramatically with nano technology and micro robotics. The stuff of science fiction from the 1950’s is alive and thriving today.

IMO why there are low interest rates is that there has been falling demand for products in relationship to the growth of the money supply. Just look at the FED’s own Velocity of Money charts and you will understand what has happened. Those with the revolutionary ideas and their sponsors are not putting their money back into society so that society can purchase their innovations. Those with the money are playing Monopoly and not sharing.

And YES, they have all that money and no where to make a real ROI. All they can do is manipulate the stock prices, manipulate the taxes, off shore what ever labor they can for more return. We are in an era of manipulation and obfuscation, not of the kind of growth that needs or is willing to pay for human labor. Oh, there is lots of work that needs to be done but those with the money do not want *their* money to be used to do it.

Interesting times.

My personal curse is noticing things such as this and then trying to figure out “Now, what’s next?”

Systems go from somewhere to somewhere.

The QE loop will exist until it can’t exist any longer. The Fed appears to be ending it (wait and see after a couple of years). The ECB and Japan have discovered printing money can go on for a long time as long as nobody important complains. Central bank money is unicorn money. The only people who hurt from it have no power to hurt anyone who benefits from it. Populism is their enemy.

The real challenge is trying to imagine, realistically, what will toss a monkey wrench into the unicorn works. When will it happen? What will cause it? Then, what’s next?

cdr, In history I think that the monkey wrench came from a Rogue Wave, a ten sigma event or out of the blue. Meaning that almost no one saw it coming. The last one (2008) was easier to see as it was mostly housing.. Today it is housing, stocks, bonds, company debt and art too. This time PR and VC groups have hollowed out so many companies and the managers of our systems have totally ignored the real threats. Equifax is only one of many security breaches. The airports were all shut down last week. They say our power grids are at high risk.. Then there are the crazies like in Las Vegas and our Twitter Chief and N Korea. It could even come from a solar flare of the sun or and earthquake or…

I was just talking to my wife on our walk about this and lamenting that I had no idea how to protect us from so many potential threats.

You just can’t help yourself can you economicminor? Twice in one article. Did you come up with “tweeter in chief” all by yourself? Please save your liberal propaganda for other outlets.

If you read “Common Stocks and Uncommon Profits” by Phil Fisher written in 1957, he describes the craziness in the 1920s (pre-Glass Steagall) when banks and their investment arms with huge conflicts of interest would push fraudulent investments to the public .

He describes the ’50s when the gap between the rich and the poor is dramatically narrower because of the growing middle class.

He cautions against the kind of company managements that you should watch out for.

Today feels like the 1920s and the trends are the exact opposite of the 1950s.

The main tool for the transfer of wealth is the fincialization of the economy.

Speaking of Glass-Steagall, the Federal Reserve Act of 1913 began as H.R. 7837, or the Glass-Owen bill. Carter Glass was a Democrat in the House from Virginia, and Robert L Owen was a Democrat in the Senate from Oklahoma.

As Wolf comments above, “Central banks buy bonds (or other assets) with money they create.” And, “… central bank money creation and interest-rate repression.” So yes indeed, we have a very skewed pricing of risk, and since TARP and QE 1 etc, the transfer of wealth has gone from the middle and lower classes to the Uber-elite.

Robert Solow won the 1987 Nobel Prize in economics for his work showing that technology is the source of long term economic growth. Based on my experiences, I support this idea.

Many credit Reagan’s tax policy for the economic boom but I believe it was really the new biotech and electronic industries that provided the boom. I worked in the electronic’s industry and watched companies such as Compaq Computer grow from a few hundred people occupying a couple rented floors, to a campus of buildings. Remember, we all went from no one having a personal computer to where we now have computers at work and home. There was no such thing as an IT department and now folks have life long careers in this area.

I remember the economic dull-drums before the dot com boom. The internet and cell phone technologies created a lot of jobs. I worked in the cell phone industry and watched as we boomed as people went from few having a cell phone, to where now folks often have several wireless devices. Every company now needs a website and larger companies have an internal web team. Most recently the social media and smart phone app technologies created additional positions as companies now need people to handle their social media websites and applications.

My last work was in electric cars. There will be a lot of new permanent positions created in the coming years due to the new technologies associated with batteries, sensor systems, aluminum vehicle structures, and various self driving technologies. However, this technological change is likely to be one where there is not a huge net increase in jobs. Jobs working on gasoline vehicles will be shifted to electric. Though the auto industry is a huge player in economies of many countries, this electric technology change won’t result in positions being created in non auto industry companies, such as what happened with the computer, internet and social media industries. So this technology change will be a boom for some but unlikely to boost the entire economy.

Gordon and Solow are probably correct and we’ll be in the dull-drums until a new technology comes along where everyone must have it.

Expanding technology was indeed a major contributor but there were many factors that came into alignment to create that era of growth.

The other major cycle with the Reagan Presidency was the peak in interest rates which have declined to today’s extremely low rates.

This was also the beginnings of fewer people protected by unions and the beginnings of the globalization of the work force.

Suppose this is a period of low technological change, then interest rates should be low? I thinks that’s correct, we might be looking at this thing from the wrong angle, perhaps we have peak technology right now?

And the DOW, Nasdaq and S&P are in record territory. Big gains today. Could it be that the rest of us got it wrong and that what we see now is the new normal. This may never end because as I have previously stated the heads of the various CBs have staked their reputations on this printing money theory and don’t want to be proven wrong.

Around the world house prices are at ridiculous levels, stocks and bonds are at never before seen values and, as some one who travels overseas regularly, I see plenty of spare money in lots of peoples pockets.

It appears that even with unsettling events happening eg N Korea, huge hurricanes, terror continuing in Europe and Canada and now the tragedy in Las Vegas the markets keep marching forward.

My questions are: 1 how much daily trading is done automatically by computers – what is the percentage.?

2 What will it take to bring about a real correction in the markets.?

3 Are mum and pop investors still involved in the markets or is it now just rabo trading.?

4 What is happening to gold and silver!!!?

5 Has China really put the brakes on the supply of money heading offshore or that just a rumour?

And here is an observation. As stated I travel overseas regularly and have recently had 7 weeks in Europe and 6 weeks in Canada. My previous experience was that people were jovial and courteous. My latest experience is that many people are wound up and nervous. I think caused by financial stress and fear of the future because of all the terrible things happening in the world.

I am from NZ so am not a trump fan but I have to admit that maybe if he causes everything to come to a head eg N Korea, Perto Rico, the issues around racial equality etc (and all the things that have been kicked down the road for many years and not dealt with) perhaps we will go through a period of turmoil then be able to start again.

Wolf I read your column every day and hope you are able to answer the 5 above questions.

My wife and I are in our mid 60s (not quite able to claim old age pension yet though) and are so concerned with what we see that we have sold everything, stocks, land, business. (Just keep vehicle and trailer home.) We have banked it all and can easily live off the interest, even as low as it is. However we have 3 children aged 36 to 40 and 7 grandchildren what is their future!!! We do all we can to financially support them.

How many other parents are in the same situation. House prices 9 times medium income!!! Rent 55 to 60% of income!!! Something has to give

Should have kept land at the very least. That’s the easiest thing to transfer, and the value should stay stable. Just keep an eye on the taxes.

“That’s the easiest thing to transfer,”

And the easiest thing to confiscate.

Kiwi

Realist below has a point. I have someone who lived thru Argentina between 1998 and 2002. Hard assets was the secret for the rich folks at the time. The bank accounts got cleared out. I recall Victor Sperandeo suggesting in 2013 to have a Canadian bank account to wire funds from the US to Canada (at the appropriate moment in the crisis) only to now discover that Vancouver and Toronto’s property markets have been on fire. When they collapse any funds in Canadian banks will go into the kitty of bankrupt banks.

Hard assets can help..

The last place to receive financial advice is from anyone on the Internet …. but ……please, please, DO NOT leave every last penny in your Bank! Store some in Bullion in a non-banking environment. I’m a Canadian, so thus i can be completely trusted …. i fully expect a catastrophic failure of 90% of the worlds financial systems. Revisit the history of bank failures in the past to remind yourself how honest hard working savers were rewarded. Good luck to us all.

Problem is those who should will not listen to such good advice.

I give it regularly.

they Laugh back.

Sorry but forgot to add one point. Is all the money I see people spending in restaurants, amusement parks, on holidays, buying new vehicles etc coming from income or HELOC loans or credit cards?

Maybe. In my case, they come from my budget. Having wasted 50% of my career on “hand-to-mouth” earning and spending, wife and I finally “saw the light” after a particularly shitty year when we had the choice to take a big loss on selling the house Now or go bankrupt in 2-3 years. We took the loss and restarted.

After that we got very aggressive about paying debts and savings, the new house is much cheaper, cheaper car … and Budgeting.

Now, If we go to a restaurant and spend decent money on a meal (I don’t buy junk food), then is because we planned it, the money is there, allocated, it is already spent in a sense. We just have to decide where and when to go out.

The effect is very surprising, the budgeting removes scarcity – I don’t get the old feeling that I *have to* spend this money on a restaurant, or whatever, before it “disappears”, so, I only spend when I really want to. The result is that the money sort-of piles up on it’s own and I don’t think about spending it so much, it feels like I am earning 3 times the money that I do earn (Same happens with Wife, the recording of expenses in the budget even shows that she is the frugal one, which is one less thing to argue about).

The surplus we used to crush the mortgage, so in terms of “income available for discretionary spending” we are quite well off, kinda like being young again.

Maybe there are many more people who actually do this? Doing well on the same money, generally only going out occasionally and spending on quality?

Budgeting and paying off debt is Revolutionary Acts :)

fa Jensen You described my situation to a “t” so yes there are others like you and your wife Feels great to be off the ” hampster wheel”

Surely far more than at the height of the last bubble.

Italian business newspaper La Repubblica-Affari & Finanza published some very interesting data on the matter.

For example until 2014 only about 40% of all vehicles bought in Italy (new and used, cars, vans, light trucks etc) were financed. By August 2017 the percentage had increased to 63%, and this is despite EAPR having increased by a whooping 30% on average. No money down offers and more lax lending standards seem to be the cause.

Also Southern Europe seems to be embracing “consumer credit” far more enthusiastically than in the past. The same publication noted by September 2017 loans for vacations had for the first time broken the €30 million barrier in both France and Italy. While relatively common in the US and some Northern European countries, these loans are a completely new development in these two countries as they just didn’t exist until 2015 or so. If you wanted to go on vacation and had no money for it, you either stayed home or took out a personal loan.

I often joke US franchising chains come to Europe when they are near the end to buy a few extra years due to the higher margins. See Blockbuster and Roadhouse Grill (the latter still survives in Italy) just to name a couple.

It seems US financial alchemy is migrating to the Europe when it’s near the end as well.

I’m sure that someday someone will recieve a Nobel prize for explaining the current monetary and market madness …

I have more and more begun wondering who will finally end up holding the shittiest end of the stick, will it be frugal people who try to manage their finances in a sane way ?

At least I’m convinced that my possible retirement will depend on what I’ll be able to stuff into my matress or else the basic retirement plan will end up as to be carried out boots first ….

I’m happy that I have adhered to what my old folks taught me, ie if you can’t pay cash on the barrelhead for something, then you don’t need it. Call me old fashioned and a misfit in today’s brave new world….

“I’m sure that someday someone will recieve a Nobel prize for explaining the current monetary and market madness …”

I accept, as I have explained it numerous times. In the US, it’s basically the robber barons of the 19th century, now called Globalists, have taken over the country. Low interest, low wages, open boarders. They have met a little headwinds as of late. Too soon to see if they matter. Globalists put hired hands and flunkies into important jobs, such as the FOMC. Those who disagree with them are marginalized and suffer from bad careers. Their only serious enemies are populists.

The ECB provides printed money to lower rates in the Eurozone, pay for socialism, and open boarders for who know what reason. Ditto with Japan, except for the open boarders. China does it to prevent social unrest, which would end the world if it occurred on the scale that scares the Chinese government. The Swiss do it to buy shares of stock and pump asset prices, making a profit for the Swiss people.

The resulting deflation is just an excuse to print more so the inflation central banks claim they want will appear, according to their models.

Central banks are unicorns. Really, just without the skittles.

Keep the medal. Just send a check.

I’m sure that someday someone will receive a Nobel prize for explaining the current monetary and market madness …

The second coming of Hyman Minsky?

Nah – No Nobel Prize in Economics was ever awarded to someone that does not fully support and reinforces mainstream economic thinking!

The blow-up of LTCM didn’t change this rule :).

Australian government 10 year bonds are trading at 2.83%…………….

Wonder which one is safer?

On Sept-30-2017

10-year Treasury yield = 2.39%

BofA Euro Junk bond = 2.39%

Could this be the inflection point?

Today 10-year treasury closed at 2.337%. Will money flow out of Euro junk to 10-year treasury when the latter goes above the former? If that happens to be the case then we may have seen the cap on 10-year treasury for a while.

Interest rates are low because the financial world is saturated in credit / debt. We are living through the end of a financial cycle. The financial crash of 2008 / 2009 derivative (estimated 1.4 quadrillion dollar) failure is too big to bail out. The BIS, Federal Reserve, World Bank, IMF, ECB, BOJ large International Corporations, Investment Houses and other Primary Dealers decided to offload their bad debts and bets on to the worlds 99 percent worker bees.

If interest rates go back to pre 2008 levels the financial system crashes quickly. If the interest rates stay at present or are raised a little at a time, the same financial system crashes over a slower period of time.

Most of this debt is odious and needs to be written off. We need a new Monopoly game that all of us can play.

That new game is called ‘JUBILEE’.

Lets look at junk European junk bonds and 10 year treasuries separately

Any bond in the Eurozone is priced NOT according to its risk,i.e. junk bonds or Italian bonds,NOT according to its real yield i.e. negative yields when inflation is running ~1.5% ,not according to its duration,i.e Austrian 100 year bonds yielding %2, but JUST according to the perception that the ECB will never stop its government and corporate bond buying program and probably will expand it to lower quality corporate bonds.

10 year treasuries are priced to yield very low but positive real yields with the current probability that the Fed will be only an increasingly large seller in the future

Add in the consensus ,which is probably wrong, that the dollar will continue declining vs the Euro and it might actually be profitable to continue buying junk bonds and selling Treasuries

Off course nothing can wrong with this trade!!!

Woke up this morning to the terrible news from Las Vegas. More and more people are going off the rails as the socioeconomic fabric rips apart. While Wall Street and global markets hit new Ponzi-like highs, thanks to a criminal cabal of central bankers and their printing press “stimulus,” a worsening economic malaise is settling over the people who have to make their way in our oligarch-ravaged economic wasteland. But it’s all good – as long as these rigged, broken, manipulated markets keep hitting new highs, it doesn’t matter that “quiet desperation” is turning into something much uglier and more dangerous.

I know many people who have extensive cash balances in their

account.These are modest people who won’t buy because

they see value.So if this is true of the rest of the world ,

how can interest rates rise.There is more cash lying around than needed.

Cash is a commodity.Demand and supply rules

And another thing.Why can’t we know what banks and insurance co. and

sovereigns

have in exposure to derivatives. I’m talking the whole thing.Whats in

the packages etc.

“You can fool all the people some of the time, and some of the people all the time, but you cannot fool all the people all the time.” – Abraham Lincoln

“You can fool all the people some of the time, and some of the people all the time, and that’s how you become rich!” – Guess who?

So, to wonder the Eurozone is a slow sinking ship with this going on.

Got me thinking. My bank thinks I should raise my exposure to stocks in my pension plan.

In response to that advice, just last week I was thinking that: “It would be very typical of me to come into stocks right before The Market dumps so I picked a 70/30 split (Bonds/Stocks) instead.

However, maybe it *is* different this time? Maybe the bond markets are actually much junkier and riskier than the stock market. Maybe this time, the flight for safety from price discovery will be from bonds and into the stock market, not the other way around as usual?

So, I think, I probably should go 50/50 as the bank suggested!?

In the very bottom of the line, Western capital has nowhere to rest. It has to recycle in whatever way.

I was in the commodities business for 31 years. Timber. Very simple to understand. So much to buy the marked trees ,which I did as the consultant to the private landowners. So much to extract the timber plus clean up costs, versus what you could get at the mill, and what the mill could make sawing and veneering the timber. Likewise, the current financial situation is very simple to understand if you look at Shiller SP 500 data, his book to sales ratio, etc. Fundamentally ,corporate values are only as good as their revenues, accounting antics aside. If his SP chart doesn’t give you pause, I don’t know what will.

Toys R US. Toys used to be papa and mama shop business in my country.

Then T R U came with thunder and more thunder. Suddenly they were everywhere. Kids knew the name just like McDonalds. Then suddenly it happened. But they lasted several years.

More interestingly of late another business model variation. This time also a kind of small retail operations before. Renting of bicycles.

Of course there must be catch phases in the business model. Call it Bicycles Sharing Scheme. Use technology. Build an app for the hand-phone. Allow customers to book them any time any where. Allow customers to leave them anywhere after use. The next nearby customer can easily pick them. Track them and manage them using Internet and satellites. Where they are and the wear and tear? Not important as they are cheap and dispensable. The more paying users the better as the inventory of bicycles are all scattered and hardly any maintenance needed for months. And the longer the bicycles are booked the cheaper the rates as the users are in effect looking after those bicycles.

Much more important. Just like the dot com days. A website and ecommerce features attracts ‘angel investors’ like the Softbanks who seemingly see the attractiveness of the business. Of course it is the IPO in time that they are after. Who cares about profitability? Who cares about long term? Business is about leveraging. More lyrics in the new song to attract investors. Like Gangnam style the more people dance and sing to your tune the better.

Heard of Ofo? Just like Toys R US catchy name for a company.

Like Zuckberg, the CEO of Ofo was reported to be a multi-millionaire still in his thirties. Company still to go IPO. Life goes on…

So the deterioration of pricing risk in the market is one negative consequence of your negative interest rates. Can you guys help me sort out what other consequences and side effects negative interest rates have that are severe but usually overlooked by many people.

Thank you for your help

Super article Wolf. Short, easy to understand and demonstrates the madness. Imagine seeing this in the FT.

TBTF has only grown in the last decade and the gov has shown a distinct bias towards saving them at any cost. Rational observation says this is trend that will continue. Hence, risk off for these organizations. All others are subject to more normal risks.

Looks like we’re all being forced to become financial/real estate speculators in order to achieve the return we need to retire.

Which is what happens when you turn your back on manufacturing and export, and put your country’s economy in the hands of financiers who create their wealth from our debt.

The only surprise for me is that people are surprised.

It would now be very appropriate if the Fed’s, and Mr. Draghi’s and Mr. Kuroda’s and Mr. Carney’s and Mr. de Galhau’s and Mr. Visco’s and Mr. Poloz’s Elite-written, Top-Secret, one-page Bible were revealed to the world.