London home prices are already tanking, as demand sags.

By Don Quijones, Spain, UK, & Mexico, editor at WOLF STREET.

The symbiotic sectors of construction and real estate have been a vital engine of economic growth in the United Kingdom for decades, but that could be about to come to an end. In the words of Paul Smith, the chief executive of the UK’s largest independent lettings and real estate agency, Haart, “unaffordability in the UK’s property market is now reaching crisis point.” If drastic measures are not taken to tame prices, the UK could lose its place as a property owning democracy, he warns.

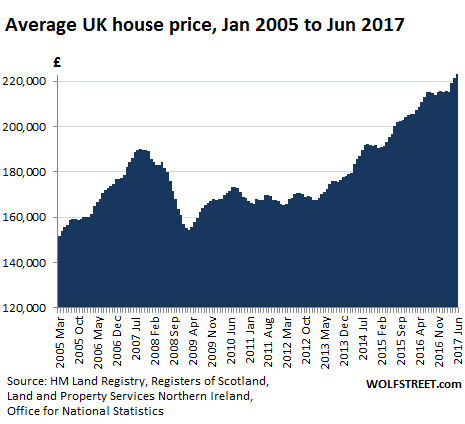

The latest figures published by the Office for National Statistics (ONS) reveal that the average cost of a home jumped by £10,000 in June from a year earlier, to £223,000. In the last eight years prices have surged by almost 50%. Its National House Price Index is now 18% higher than during the peak of the prior housing bubble (September 2007). This chart is for the UK overall. But home prices in London have now turned the other way.

Demand is already sagging. In the first six months of 2017 alone, first-time buyer registrations dropped by almost 20% across Haart branches. It seems that a trend that began in London is now going nationwide.

For well over a decade soaring property prices have priced most Londoners out of the market. The number of homeowners in London in the 25 to 29 age bracket has dropped more than 50% since 1990. Foreign buyers have virtually cornered the market, acquiring as much as three-quarters of all new-build housing in the capital in recent years.

But even foreign buyers have begun to pull back from London’s property market. In April this year values in the prime central London market were already 13% below their 2014 peak, according to Lucian Cook, head of residential research at Savills. Latest figures from the ONS suggest that things may be even worse, as average property prices in London plunged 20% in the first six months of 2017, making it the worst performing region across the country.

Now, property prices beyond London’s gilded streets appear to be catching up with the trend. According to the UK’s biggest estate agency group, Countrywide, prices will rise just 1.5% across the UK as a whole in 2017, down from 5% in 2016. Growth is expected to slow in areas such as the north of England, the Midlands, London and the south.

The main factors driving this trend include changes to UK stamp duty as well as international buyers’ increased exposure to capital gains tax and inheritance tax, leading to more reluctance in taking advantage of the weaker sterling. A recent survey by the Royal Institute of Chartered Surveyors found house price indicators at their weakest point since 2013.

There is a silver lining for the sector, though: the new builds market which, underpinned by low borrowing rates and lavish government subsidies, continues to grow at a fair clip. But even here, the shadows are looming.

The practice of selling homes with a leasehold and the government’s Help-to-Buy scheme, by which taxpayers help developers sell new-build homes to first-time buyers, are both under the spotlight. But fallout from the UK’s leasehold scandal is beginning to take a financial toll on some of the companies most implicated in it.

In the second half of the 20th century, most houses in the UK were built as freeholds, whereby a buyer would take ownership of the home itself as well as the land it sits on. Then, at the turn of the century, developers and landlords identified a lucrative new revenue stream: selling houses and flats under leasehold agreements, then selling the freeholds to the land to other investors, who can earn up to 10% of the purchase price annually.

It was a good deal for all involved, until the homeowners and the wider British public began realizing just how abusive the scheme has become. The average charge now stands at £371 a year on new-builds and £327 on other properties, according to research by Direct Line for Business. Sometimes it can be a lot higher.

As many as 100,000 UK households are now trapped in unsellable leasehold properties with sharply escalating ground rents. In recent weeks, the UK’s biggest selling tabloid newspaper, The Sun, joined the backlash, attacking the “fat-cat” CEOs of builders that have racked up huge profits by selling freeholds on new houses to investment firms without properly informing the new homeowners. Many of the senior executives are living in substantial houses built by the companies they manage — all of them freehold!

In the face of growing public pressure, the UK government has vowed that it will outlaw leaseholds on new-build houses while drastically restricting ground rents for apartments to a “peppercorn” value, thus wiping out their financial appeal for speculative buyers. Even before that happens, lenders such as Nationwide and Santander have already announced they are not going to lend on “toxic” leasehold properties. Others, such as Barclays, will not lend on leasehold houses at all.

If the government follows through on its pledge to outlaw leaseholds, without leaving a trail of gaping loopholes for developers and investors to exploit as it did in a 1987 law ostensibly aimed at protecting homeowner, developers and investors are almost certain to lose an important source of revenue, just at a time that the UK’s property market is showing signs of strain.

Sliding prices are good news for aspiring homeowners that might eventually get the chance they’ve been waiting for to buy their first house. But for the UK economy, which has grown both rich and dependent on the false promise of ever-rising house prices fueled by ever-larger amounts of debt, the current trends are most definitely not its friend. By Don Quijones.

Even “significant economic damage” is a “price worth paying” for many Britons. Businesses are not so sure. Read… Support for Hard Brexit in the UK Hardens

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I hear there is affordable housing in Aleppo

Don’t be fooled, other than in Switzerland and Monaco there is affordable housing in literally *EVERY* Western economy.

Sure, you ability to “LIKE OMFG WALK TO DA’ BARS ‘ND DA’ KLUBS” will be materially limited, but if you don’t mind plopping your behind in a car seat for an hour there and an hour back a day — you can live in a commutable distance to most major cities for little denaro.

1) Add to that list Luxembourg , Liechtenstein , the Netherlands etc

2) Ahh … sorry Hans but … in major western cities such as SF NYC London Paris DC Berlin etc the truth is you’d damn well better be willing to accept the fact that you’ll be living dead center in the middle of a crime zone with little if any adequate police protection in order to find affordable housing .

3) Commutable being a relative term . Do you consider a daily four hour minimum round trip ( by train ) commute to and from DC from one of the barely affordable VA MD suburbs to be .. reasonable ? Or how about a minimum 60 minute drive each way ( more like 90 – 120 minute by bus ) to commute to Denver from one of our barely and rapidly disappearing affordable ex-urbs ? And then there’s the SF and greater Bay Area . Wolf can be more accurate but suffice it to say there’s nary an affordable area to live in that can be considered even so much as reasonably commutable

Which is to say your claim good sir is either uninformed ( my first assumption ) or verging on magical thinking

But commute costs go up, and you spend more of your short life on poor quality UK roads.

Many outlying areas were cheap, but even an hour out are now more expensive all in.

The only ‘cheap’ houses left are horrible and likely to become completely worthless in a proper price correction.

I look forward to normalcy returning.

Land values and builder overheads (or stupendous profit margin) aside, homes should be cheap as chips.

If you’ve built a house and seen what actually goes into one, especially a contemporary new build (even £500,000 examples in the North) you’d think they’re at best ‘worth’ £100,000.

Someone somewhere is making a killing!

You are not spanish, that is for sure.

Haus-Targaryen,

You clearly don’t live in the Bay Area. A one-hour commute (one way) by car into central San Francisco during rush hour means that you still live pretty close – and likely in a still expensive area.

Plenty of great properties in Warsaw which is a very affordable and liveable city A lot of young Israelis are buying I’ve been told Much less of a refugee problem as well Gypsies are kept in check as opposed to places like Barcelona where they are out of freaking control

50 kliks from Sydney(Penrith) the median house price is $710 thousand.

Similar situation even in Perth, WA. But the silver lining is the rent. I’m in a house ostensibly worth $900K and I’m paying $500pw. That’s a 2.9% gross yield to the owner. Throw on rates, property management fees, repairs, periods vacant. Then there’s the capital depreciation as prices fall here. Renting can be a real short-medium term winner.

But, my dear Ambrose, how may one put it?…….. the neighbours!

Oh, the neighbours are now in London, Berlin, or around Vancouver, and Toronto.

” All in all its just another brick in the wall ”

Question is in this age of cognitive distortion and magical thinking .. will it make a damn bit of difference ?

meanwhile in Canada. How is delegating duti es over to sros like iiroc and obsi. Not defacto privatization of investor consumers issues back to the very industries they have filed complaints about?

And why has there been no public deb*te over how effective such entities are in protecting consumers rights and ensuring fair to the investor redress rather than a way to stonewall *nd sandb*g issues the government should be address but won’t because it means confronting a very powerful lobby group? Why are entities like the Ont Securities commission a-ding and a!erting this process especially a4 even their own audits have red circles serious deficiencies with how the SRO handle consumer complaints compared to the expect*tions of the law and industry codes of conduct

There equally was no public deba(e prior to the previous government’s billion dollar b*ilout of the big banks but plenty of denial

Coincidentally or not the big five are the majority shareholders of eac others companies….

The liberals who rode to power on * support the middle class platform seem to be in denial that middle class consumers who typically uses the financial industry’s services are having their wallets drained by the same industry despite legal red lights and much empty talk about fees

However we did have a deba(e about privatization of the postal service. Maybe because of the cost on the government’s wallet post 2008 financial crisis. But silence on what is a stealth privatization process ongoing now long *fter Harper has exited. Another issue not discuss is the fate of survivors and loss of ccp and oas upon death of a spouse. Which again is why maybe the government needs to address the problems in consumer protection when the industry takes over the duties from the government. And the government pushes work that direction but no one discusses the quality of subsequent service

Housing affordability I think is the no 1 reason for alt left and alt right politicians to get traction. They have totally failed with their economic model in so many countries

This^^

The total infeasibility for the vast majority of people of owning their own home, unless it’s a rabbit hutch, or is located in the middle of sh*tsville (or both), allied to the lack of decent jobs, plus the permanent neurosis attached to having any job, is what’s causing people to slide down the slippery slope of mental illness, at the end of which ugly things happen to them, and they do ugly things to other people.

“There is no longer any excuse for making the same mistake with economic theory. For more than a century, the public has been warned, and the way forward is clear. It’s time to stop wasting our money and recognise the high priests for what they really are: gifted social scientists who excel at producing mathematical explanations of economies, but who fail, like astrologers before them, at prophecy.”

By fetishising mathematical models, economists turned economics into a highly paid pseudoscience

The new astrology

https://aeon.co/essays/how-economists-rode-maths-to-become-our-era-s-astrologers

Same goes for something like Technical Analysis in the markets. People using Fibonacci numbers, Elliot Wave Theory, Gann charts, etc. etc. It’s just numerology. The basic problem with this and economics is that the past is a different country, as they say. Regulations, production methods, population demographics; everything changes and trying to extrapolate results from previous events is like predicting the speed of mayonnaise in a wind tunnel (I have no idea where i got that analogy from..)

Just good ol’ fashioned usury TBH. One of the features of decadence is saturation of a populace with debt.

It used to be reigned in by regulation but that was swept away in the 80s miracle of the big bang and the releasing of the ‘animal spirits’ in the name of (avert your eyes and genuflect) economic growth.

Of course this miracle of the magic credit money tree meant that politicians came to believe that it’s no longer necessary to design, produce and export goods to build wealth.

A falsehood which is going to cost dear in the very near future.

Best tell your kids to learn Mandarin – they’re going to need it when the Chinese outsource their low-pay, low-skill jobs to us.

So is the City of London dispersing? I mean a lot of money is going to leave the country if that happens.

Which central bank asset bubble will be the first to crater, and which will implode in the most spectacular fashion?

Britain: The first but not the most spectacular.

Maybe having to raise interest rates to protect the Pound.

UK has twice the population density of China which may be surprising to some. Scotland, about 1/3 of UK territory, has a population of only over five million. Sure, geography plays a role, but still. The population also continues climb rapidly due to well known factors. Sadly, you can discuss cannibalism more openly in a polite society than population control.

I’m always surprised at how fast I get shutdown by people online when I suggest over-population is the root cause to whatever issue is being discussed like pollution, warming, environmental destruction, poverty, etc. etc. What’s their game plan? Wait till we hit 12 Billion and THEN address the issue? Madness.

Hear, Hear! Western citizens may not reproducing like animals anymore, but plenty of places in the world are still reproducing like animals, and these very people come to Western countries and reproduce like animals, and thus more than compensate for lack of birth rates in Western countries.

All countries should be given a quota for reproduction; if they go over that reproduction quota, impose gradually harsher sanctions on them. Do that and see how many of these governments get their acts together and stop their people from reproducing like animals.

I don’t call it madness; I call it Gaussian or bell curve of intelligence distribution. A lot of things make more sense if you look at it that way.

The population growth in the UK is also mostly in the lowest social strata, people who will never be capable of earning much in an advanced economy.

These groups reproduce at will, whereas others now ponder deeply as to whether they can afford one child.

All good for those who require semi-skilled labour for dumb poorly-paid jobs.

Lots of cheap housing in Japan away from the big cities.

You can buy a nice house on 1/4 acre block for around $250,000 an hour to an hour 1/2 from Tokyo. And you can bet that the trains there will run on time.

Even much cheaper if you go to other parts of the country.

Kyushu is really cheap especially for land.

Big cities in Japan are ridiculous and even there condos are high priced.

Condos in resort areas vary and can run from really, really cheap to ridiculous as in the big cities.

I was looking at a really nice 100 sq meter condo in a high rise in a famous resort area and the cost was very reasonable – about US$80,000, but the monthly condo and sinking fund fees were way too high. You also have to worry about high repair bills as the condo ages for unexpected repairs.

Other resort areas have condos as low as US$10,000 for a small condo!!!

IMO that is the next crisis in Japan: high fees for condos. When owners die and the heirs don’t want the condos and refuse to pay the fees the building will have big trouble.

The above US$80,000 condo had a monthly common/management fee of around US$500, sinking fund fee of around US$250, water use fee of about $US40 and an ‘onsen’ fee of around the same.

Plus you never know who your neighbours are and all the other problems with living in a condo.

RE taxes in Japan are a ‘mystery’ most of the time as well. IIRC the taxes are based on when the house /condo is built and rarely go down even if the price of the dwelling has fallen. So if the dwelling you are interested in was built during the bubble and had a high initial price your RE taxes will be quite high.

IMO houses are a better buy.

Thank you for your post. I’ve always wondered why housing in Japan has not exploded upwards with interest rates being at zero.

My internet searches have suggested that the Japanese like outsiders to visit, but not ‘reside’. Given that the population growth in Japan is stagnant, any purchase from an investment perspective would be nill given the ‘apparent’ , no doubt very polite, dismissive attitude toward new foreign investment.

If you have any thoughts as to why housing in Japan is a dead investment, please share them

Thank You

Commercial RE in Japan in the big cities including hotels, office buildings, and such have been big winners over the recent past. One reason is the huge influx of tourists to Japan.

New or almost new condos in certain parts of Tokyo have gone up as well.

Other big cities – I’m not sure. Nagoya, for example has a a large number of expensive condos built in huge high rises over the past ten years or so, but I have no idea what the after sale pricing has been like and not interested in finding out.

IIRC between 15 to 20% of houses in Japan are vacant, yet they build around 1 million new houses/dwellings a year!!

Go figure.

As for the reason why housing is dead outside of the big cities is as you state: Japan is dying. There is also a big problem with heirs not wanting property as the houses are in bad shape and the plot is small or the property is located away from big urban areas.

In regards to ‘abandoned’ property there is something like 4.1 million hectares of land with unknown owners now in the country.

Finally, as I have posted before, out of the big cities RE is cheap and in fact cheaper to buy than rent. If you buy in a regional city within good commuting distance of a bigger city you probably won’t make any money, but you will be able to sell the place when you ‘leave’ for whatever reason. Better than throwing you money away on rent and all the problems with renting in Japan.

You would want to avoid areas that are dying which can be found as easily as looking at the Japanese language Wikipedia site for the train station in that area and seeing how the number of people using the train has changed over the past thirty years.

I remember looking at some places data and the number of people using that station have gone from 1500 a day to around 300 a day over that time period. A place like that is dying and will soon be gone.

So here is another “Brexit did it.” for the UK. Doesn’t change the fact that the Euro zone is a slow sinking ship and long term, leaving it is likely to favor the UK. Just not in the next few years, maybe not in the next decade and a half. But when Spain and or Italy crash, the UK won’t be helping since it won’t be part of the European Union.

The Euro currency might be Europe biggest mistake in decades, if Italy and Spain still had their own currencies, they would have a way out their crisis.

It seems that real estate is starting to crack all over the globe. Property prices in China itself is plunging, in Canada is plunging, now London. US and Australia will follow the same path.

Could this have anything to do with the Chinese government crackdown on transferring money out of China? Could it be that the biggest and dumbest gamblers have no funny money to buy anymore?

Wait till the Feds in US keep raising rates and start to unwind their QE at the rate of $50 billion per month; then the show will get really interesting. 3-4 years after they crash the prices, then bankers will come in, and start to purchase the same properties they sold to the public at extremely high prices for pennies on the dollar.

As most people are oing to end up on minimum wage in the UK, it makes sense to buy where property is affordable.

Burnley, Blackburn you can buy a freehold two up two down terrace house for £30,000 ( US$39,000) and easily afford the mortgage on minimum wage doing a 35 hour week if you live realistically.

At £30,000 (US$39,000), you couldn’t even buy the materials to build that property let alone the labour for the hosue and the freehold land and utilities put in it. With the UK rapid population increase due to immigrants arriving at 400,000 per year, the muslims breeding at rabbit production rate.

Why people live in London nowadays I’ll never know.

A truly overrated city with its crimes and immigration issues.

Time for a house price correction down there…the price of houses in the capital is crazy.

The crime was very much worse in the 1980’s and 70’s with the muggers.

Now gun and knife crime seem to be rising, but the street mugging stopped when credit cards came in – no cash to steal.

My mother was mugged while pushing me in a pram.

What is terrible now in central London is the over-crowding, it’s just insufferable to be on the main streets or the underground.

The only way to move on foot is by the back-streets, which can be quite interesting architecturally.

One also finds empty streets in the uber-wealthy zones, for obvious reasons .

Yes the mantra of “you can’t lose with property, it doubles every 10 years” is about to be severely tested in the UK…

Sadly, it’s that “you can’t lose…” myth which has been propagated for – well, forever – which sees desperate/greedy people (take your pick) dive into daft arrangements such as leasehold wherein you don’t even own the ground the building (sorry – ‘property’) stands on.

Ironically, therefore – it’s never really your ‘property’ at all.

As for the “it’s different – it’s London, a global financial center” line, well we’ll see how that holds up now there are no quick gains to be made and the foreign speculators stay away.

After all, it wasn’t ‘different’ for Tokyo at the end of the 80s. And a bubble is a bubble is a bubble.

A (wo)man’s view of the economic future largely depends on the amount of debt (s)he has, after all.

In the long term, you can’t lose on property unless you are a short-term speculator. British house prices always had a slump on an approximately 11 year cycle in the 20th century, the last being in the late 80s/early 90s, but they always rose again. So, if the property you own is solely your residence, price rises and slumps don’t really matter unless you find yourself in negative equity and need to move.

The reason that the historical slump didn’t occur in the early 2000s was the increasing popularity of Buy to Let lending and it was seen as a fashionable investment. A slump didn’t occur until 2008 due to the global crash. The problem is that Buy to Let ate up a great deal of first-time buyer properties, and we are still left with the situation where many cannot afford to buy, yet have cripplingly high rents. Britain is now the 2nd most populated country in Europe thanks to Blair’s open door immigration policy, with much of its population in England’s lowlands. Yes, Scotland and Wales have much lower population density but if you’ve ever been there, much is mountainous and not suitable for building. England’s construction industry is picking up again but I fear that much of my country will end up being concreted over as there is still too much housing demand.

The Buy to let brigade of landlords have had it too good too long. Low interest rates also have been a big benefit to them when borrowing for mortgages.

The banks haven’t helped either with their interest only repayment mortgages which the landlords have lapped up.

Add to the fact a lot of these landlords aren’t registered for self assessment taxes then if there was a housing slump in prices I wouldn’t be losing any sleep if a few of these went bankrupt.

An example recently Newham Council in London found out 13,500 landlords in that one borough alone weren’t registered for taxes.

Good news they’ve supplied the names to the Inland Revenue so hopefully they will all have to pay backtaxes and interest.

In Newnham they will mostly be Indian Asians – they just love property.

Turks stick to small retail properties for money-laundering: restaurants, barbershops and hairdressers, cafes, small shops.

“After all, it wasn’t ‘different’ for Tokyo at the end of the 80s. And a bubble is a bubble is a bubble.”

FYI:

“The highest roadside value nationwide is 40,320,000 Yen per square meter in front of the store “Kyukyodo” on Ginza Chuo-Dori Street in Chuo ward, Tokyo. This has been the highest priced space in Tokyo for 32 consecutive years and has gone up over the past highest 3,650,000Yen per square meter in 1992 right after the bubble economy. The rate of rise in Ginza has marked 26.0% which is the highest rise in Tokyo compared with the previous year. ”

(I think what they are trying to say is that the price for this property is now 3.6 million yen per square meter higher than during the bubble and the price increased by some 26% over last year….)

SEE:

http://www.realestate-tokyo.com/news/official-average-roadside-land-price-2017/

“US and Australia will follow the same path. ”

Well I guess you’ll have to put off that action for Australia or at least Melbourne for a while. We had our weekly residential auctions and had a clearance rate of 75%.

True that stamp duty is affecting house price demand, but mortage lending criteria has also been tightened which is ruling out many buyers. Buy to let investors have been hit by taxation changes. Property prices are falling only because the costs involved in buying has risen disproportionately. With buy to let most landlords pay cash so it is not the price of the property that is the issue but the investment benefit.

The bulk of the market in UK is for owner-occupation. There have often been times when demand has fallen or remained static. Currently as I understand there is a shortage of the type of property that buyers want to buy. But since the cost of moving house has risen sellers owning the type of property that is in demand are not interested in selling. No point in wanting to cash in on demand and supply imbalance if should you feel like selling you can’t find anything you’d want to buy.

Tough maybe on thisr that would love to get on the housing ladder or would like to trade uo but property ownership is a private sector industry, not an extensionof social services.

In the meantime, thanks to national planning policy, every scrap of undeveloped land in rural towns is getting planning permission for another street of cardboard boxes. Which is adding to local population regardless of local infrastructure.

The main reason for overcrowding in UK is that too many people want to live in towns and cities that lend themselves to overcrowding and suit the sort of people for whom overcrowding is second-nature. As for London, I was born there and lived there until I moved out over 20 years ago. Would’t go back. We whites are now in the minority there!

There are many excellent posts here.

The problem of high property prices inevitably creeps throughout most of the country but the greatest distortion is in England, and mainly in the south of England. Kofi Anand thinks we should take more refugees (because some of us are rich) and when the cost of London property is mentioned he says there are plenty of other towns in the United Kingdom. Somebody should have explained to him that when refugees are sent to cities in the midlands and the north, many immediately return to London.

The government has funnelled the cheap money sloshing around into a bubble instead of into consumer spending, or best of all into investment in industry and commerce. The planning system is an absolute disaster which supports a handful of established house builders which have accumulated massive land banks. Maximum profit for them is clearly not to satisfy demand because that would lead to lower prices. Sadiq Khan, Mayor of London was elected on promises of a grand house building programme. Figures show no construction began for homes at social rent levels in 2016/17 and none has been built since the beginning of the financial year for 2017/18.

What is happening in London has happened in many parts of the world where wealthier people ease out the indigenous population, sometimes buying whole islands. When children grow up and need their own homes they are forced to move away from where they grew up, often only to commute back to their jobs. Commuting is not a solution to anything, but I had better not start on that.