“Let markets clear.” It’ll be just “a financial engineering shock.”

Stock and bond markets are in denial about the effects of the Fed’s forthcoming QE unwind, whose kick-off is getting closer by the day, according to the minutes of the Fed’s July meeting.

“Several participants” were fretting how financial conditions had eased since the rate hikes began in earnest last December, instead of tightening. “Further increases in equity prices, together with continued low longer-term interest rates, had led to an easing of financial conditions,” they said. So something needs to be done about it.

And “several participants were prepared to announce a starting date for the program at the current meeting” – so the meeting in July – “most preferred to defer that decision until an upcoming meeting.” So the September meeting. And markets are now expecting the QE unwind to be announced in September.

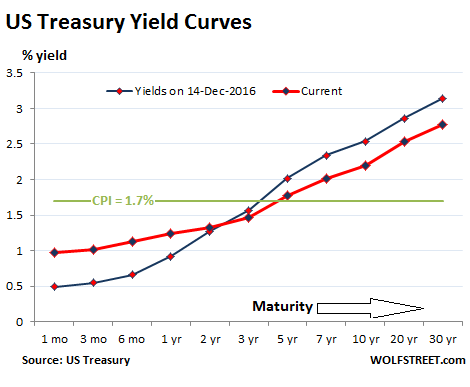

Since then, short-term Treasury yields have remained relatively stable, reflecting the Fed’s current target range for the federal funds rate of 1% to 1.25%. But long-term rates, which the Fed intends to push up with the QE unwind, have come down further. As a consequence, the yield curve has flattened further, which is the opposite of what the Fed wants to accomplish.

The chart shows how the yield curve for current yields (red line) across the maturities has flattened against the yield curve on December 14 (blue line), when the Fed got serious about tightening:

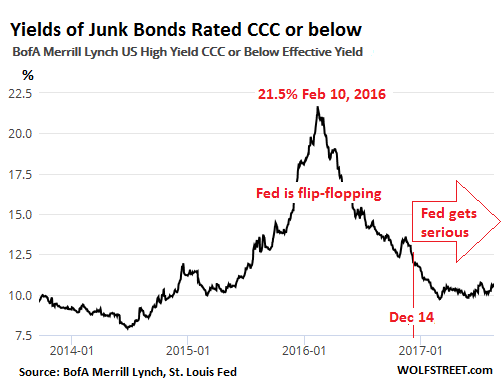

Yields of junk bonds at the riskiest end (rated CCC or below) surged in the second half of 2015 and in early 2016, peaking above 20% on average, as bond prices have plunged (they move in opposite directions) in part due to the collapse of energy junk bonds, which caused a phenomenal bout of Fed flip-flopping. But by rate-hike-day December 14, the average yield was 12%. And since the tightening moves and the planning for the QE unwind, the yield has dropped to 10.7% currently:

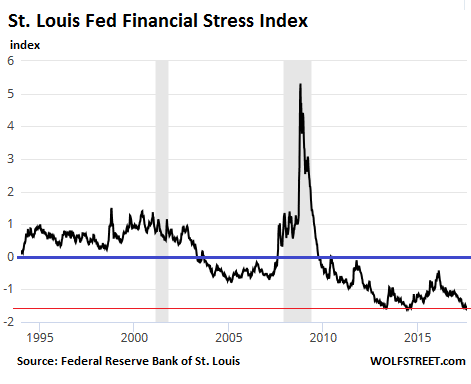

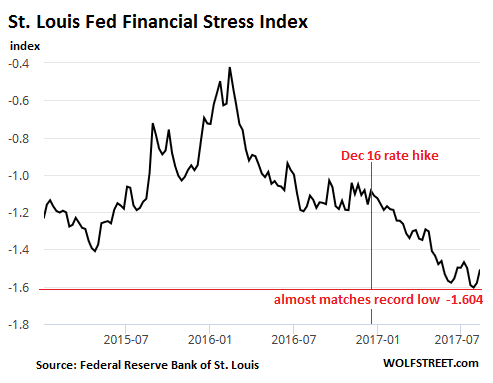

So markets are loosening “financial conditions” for companies, thus making capital cheaper and easier, rather than tightening financial conditions. The St. Louis Fed tracks these financial conditions with its “Financial Stress Index.” In this chart of the Financial Stress Index, the blue line (=zero) represents “normal financial market conditions.” Values below zero indicate below-average financial market stress. The record low was -1.609 on June 27, 2014. Currently, the index is at -1.604, just barely above the record low:

In other words, financial conditions have almost never been easier despite the current series of tightening moves. And this is what it looks like in more granular detail:

Stocks are still near all-time highs, though they’ve come down a tad. Interest rates for conforming 30-year mortgages are still quoted below 4%, thus propping up the housing market, despite the Fed’s plan to begin shedding its portfolio of mortgage-backed securities, which it acquired over the years specifically to push down mortgage rates.

After a 12-month phase-in period, the Fed will reduce its balance sheet by up to $50 billion a month in Treasuries and mortgage-backed securities, every month, with clock-work regularity. That’s the plan. By $600 billion a year or $1.2 trillion in two years. QE was designed to bring yields down and inflate asset prices. Now the opposite is being planned, and markets are just blowing it off.

No one knows how this will turn out. The Fed has never done a QE-unwind before. But folks are concerned. A committee of investors and banks – the Treasury Borrowing Advisory Committee or TBAC – pointed out some of those risks in its presentation to Treasury Department earlier this month.

They pointed out, for example, that the corporate and government borrowing costs are likely to rise. At the riskier end, borrowing costs could rise significantly. In addition, the federal government’s borrowing needs is also expected rise, Jason Cummins, TBAC chairman, wrote in the letter to Treasury Secretary Steven Mnuchin. So just when the Fed is cutting its balance sheet and the cost of borrowing rises, the amounts to be borrowed by the government are expected to increase.

“The private sector piggy-backed on the Fed’s large-scale asset purchases, a move that promoted a surge in corporate borrowing and tighter risk spreads,” Cummins wrote. “In an adverse scenario, there’s the possibility of a meaningful, but not systemically risky, decline in both credit and equities.”

It would be a “tail risk” the presentation said. It could entail accelerating “risk premium decompression,” where “small increases in yields can potentially lead to large changes in risk premium.” Which means large-scale declines in the prices of riskier bonds, and thus far higher borrowing costs for those issuers, and a big hit to stocks. The presentation:

Pro-cyclical behavior of investors who ‘piggy backed’ central bank purchases and ECB tapering are possible accelerators to the rise in US risk premium in a tail risk event.

“There may be a “meaningful decline in risk assets.” But it’s not going to be “systemic,” it said. “Banks and households have not leveraged to higher asset prices.” They can withstand the shock. So “Let markets clear.” It’s just “a financial engineering shock.”

Given how corporate bonds are now largely held by exchange-traded funds and mutual funds, this could get even more interesting. When bond prices decline, investors in those funds – painfully aware of the first-mover advantage experienced in prior bond-fund collapses – will be getting out of these funds, and funds have to sell bonds to meet the redemptions. At that point, bond market liquidity dries up, and this selling by funds will accelerate the pressures. And yet, bond and stock markets are still euphoric.

What happens to prices when the biggest, reckless buyer walks away? Read… US Asset Bubbles Crack as Frantic China “Restricts” Outbound Investments

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf have you seen this on Srsocco reports about advertising. Thought it might be something of interest to you or some of your readers.

The question that continually crosses my mind every time we broach this subject is ;

Is this a case of the markets being in denial …

.. or the fact that the Bots are running the ‘ show . and that regardless of how sophisticated their creators claim them to be … they are chasing perceived bargains rather than looking at the underlying facts behind the perception ?

Remembering it was a whole host of algorithms etc coming out of MIT that helped create the 2008 crisis . Cause an algorithm/bot is only as good as its human creator … and we all know how throughly flawed we all are

If the Fed starts to telegraph faster rate hikes then real money will go to cash as the opportunity cost of missing yield will go down. When that happens long only has to sell.

Fed is a long long way behind the curve as well as per wage inflation.

http://strategicmacro.blogspot.co.uk/2017/08/employers-paying-up-for-workers-while.html

The Fed will NOT raise rates anymore. They should be apoplectic after reading this article. You can expect a 15 to 20-minute line of bull$hit at the next staged FOMC reading and then…The markets will crash due to ridiculous overvaluations and a recession; they will lower rates; the pension funds will cry bloody murder and collapse; and then, Janet will nut up and print more useless, green, paper rectangles. BUT!! There’s always a bull market somewhere. (here’s a little secret–there is a bull market in the cryptos…)

Agreed, Spanky. Yellen will keep up her incessant jawboning about mythical pending rate hikes, but she knows it’s Game Over for the Fed’s asset bubbles and Ponzi markets if she hikes for real. More importantly, bilking savers out of interest income and forcing them to seek yield in Wall Street’s rigged casino is too lucrative a racket for Yellen’s oligarch patrons for her to raise rates unless her hand is forced.

You cannot “taper” a Ponzi.

Signficant reduction in Fed balance sheet from QE will not happen. They are talking it up to make it appear that this was certainty all along. Sure, they may start a mild reduction, but nothing significant.

Same with more raising of short term rates. Not going to happen.

Reminds me of funny quote: Big hat, no cattle. = Big talk, no room to manuever.

I agree with you completely. There is so much outstanding debt the FED is scared to death to make any significant (read meaningful) increase in interest rates. Any increases will be very small and intended for media consumption. At some time something beyond the FED’s control may happen to cause QE to unwind but it would probably be so catastrophic as to render the QE moot.

Except, Old Engine, if they keep interest rates low, pension funds and insurance companies will blow up. They have painted themselves into a corner and we will pay the price. :-(

Yeah, the Fed is in the so-called optimal position–the position that is not GOOD, but from which any deviation will only lead to a worse position.

When all is said and done.

When the dust had settled from the 2008 financial collapse, 5 trillion dollars in pension money, real estate value, 401K retirements, savings and bonds had been vaporized.

8 million people lost their jobs.

6 million people lost their homes.

Compared to what is coming, 2008 was just the warm up.

Yeah but all those dollars have been regained, albeit different people now own those dollars.

In other words, a crisis is just another opportunity to get richer. So yes I agree, 2008 is just another warm up. For the 0.01% it’s a chance to own everything.

The Federal Reserve cue card:

Step 1: Create fake money stealing value from everyone

Step 2: Loan the fake money to people with interest

Step 3: Take people’s stuff when they can’t repay the debt

Step 4: Get government to enforce our fraud

Step 5: Plunder humanity

No, it’s not that complicated. It’s support the people who pull the strings. BS the rest.

The people who pull the strings are not you and me or some abstract vision of ‘the public good’.

It’s grown into a complex framework, which includes experts who offer theoretical support that is taught in major universities, of innovative financial engineering that happens to trickle down from the 1% to you and me.

Gershon, that sounds about right.

How much real money do you have? 90% of all American’s money is electronically created and has no monetary/intrinsic value, it is a digital record of wealth. How many of you are comfortable with this, and what are you going to do to safeguard your assets?

Mike, if your money has ‘no intrinsic value’ just mail it to me. I’ll even send you postage and the envelope.

Do you ‘work for food’ like some of those people at highway exits put on their cardboard signs? Barter economies are cool.

Mike,

Gold has no intrinsic value either. It conducts electricity fairly well.

Food has some intrinsic value but decays rather quickly.

Gershon, you get it. 99.9%er!!!

Rates are going to rise eventually (unless the old globalists take charge again, then negative rates are coming in a couple of years).

I believe the greatest odds favor higher rates sooner than later. The actual rate of rise is uncertain.

The 1% favor low rates, low wages, and flexible labor sources. The 1% supports professionals and experts who support this goal. These ‘supported experts’ receive career advantages, financial gain, and public support for assisting the 1%. Those who disagree are treated as kooks and marginalized.

Goofy theories about the need for inflation motivated QE and large balance sheets and low rates are rarely questioned, even though they make no sense and are actually immensely stupid. Many people believe in the need for inflation without question. It’s almost Pavlovian. QE does, however, benefit the 1% quite well. The claimed need for inflation makes a great excuse. This is raw class warfare. Nothing less.

In Europe, rates will never rise. The ECB needs them low to keep the Eurozone in existence. The Fed is mindful of this and, I suspect, with globalist urging, will put the ECB needs for low rares ahead of the US need for higher rates.

Really, all we can do is wait and hope rates normalize. The FOMC does not support the 99% and therefore can not be counted on to follow through just because they said they might.

However, if rates rise and the balance sheet is reduced to a small fraction of what it is today, magic will happen. While the 1% will scream and the ECB will shriek and print even more, the 99% will prosper and so will the general economy. Higher rates will create interest income which will be spent. Higher rates will end junk investment in favor of investment that creates jobs.

A falling stock market is a non-event except for a few true believers who confuse the DOW with the economy.

It’s still too early to expect any good will occur.

Amen. Preachc cdr.

Thanks.

Me to the moon: “Bark”.

Reminds me of this …

https://www.youtube.com/watch?v=4D-456BT0A8

Regards,

Cooter

Rates will not rise in the US as there is no inflation, and there will be no inflation for the foreseeable future. This economy has now pushed unemployment below 5% – down to levels where the Phillips curve would predict we would see wage increases and inflation, but it is not happening.

In my view, massive deflationary forces will continue to affect the US economy for years to come: Boomers leaving the workforce and downsizing, Millenials unable to spend due student loan debt loads/inflated housing costs, and technology eliminating the need for low and middle skilled labor while also reducing inefficiencies/redundancies. And that’s the short list.

Interest rate “normalization”? Don’t hold your breath…the long end of the curve is going to be pinned to the floor for the foreseeable future. I’d expect to see the 10 year at 1% before we’ll see 3% again. When the Chinese economy is exposed for what it is, tensions in Korea or Iran boil over, or a black swan event occurs – we’ll be below 1% on the 10 year before you know it.

“Rates will not rise in the US as there is no inflation, and there will be no inflation for the foreseeable future. ”

Mark, when did it become ‘common knowledge’ that you can’t charge interest if inflation is low? This a completely bogus.

If the money being lent originates from a printing press, it has less value, as compared to cash that resulted from the savings of someone who worked hard to accumulate it. Asset prices will inflate in price from printed money. Everyday items won’t because there’s less actual income (from interest payments to you and me) floating around. Everyday items do not rise in price quickly because of a lack of liquidity. Most of the printed money supports asset prices that the 1% swap back and forth in order to get the skim off the printed money, plus anything the 99% volunteers into the scam out of their actual savings.

Cash retains value because the 1% have an unequal distribution. It’s is more scarce to the 99% from this scheme. The Fed would see it’s precious inflation if everyone got an equal cut of the printed money.

This is an example of a fraudulent concept as ‘common knowledge’. It’s class warfare where the 1% control the central banks by putting people in place who believe goofy theories, or at least claim to. This is the scam, commonly called QE, which the Fed purports to be thinking about possibly ending someday a long time from now.

Whats the hubbub? The market is providing liquidity, which gives the Fed the chance to normalize rates without draining liquidity. Allowing bonds to mature, reduces supply, puts more downward pressure on rates. (maybe the market is pricing this in?) The downshot is another hit to the energy sector, and perhaps we are getting into deflation country again, which the Fed does fear. And so raising rates incrementally doesn’t work, time for the Paul Volcker moment. Raise raise and keep raising. Only Volcker was a hired gun, and there is a leadership vacuum in D.C. Left to its own devices this Fed (global CB cartel) will return to QE, and kick the can down the road. For those crying about their fecklessness, a bit of deflation is good for working class Americans and is also part of the Presidents weak dollar policy. Trying to figure out what’s wrong here, and I keep coming up with nothing.

Wolf,

Perhaps our corporate overlords have bought back all the shares they feel is necessary?

It’s not like any lending is going to industry anyway, right? Isn’t most to mortgage and buybacks? There is no productive lending. So, does the lending rate even matter at this point vis-a-vis the real economy and current debts?

I think the rate doesn’t matter (directly) as much as it normally would. I agree with you.

I suspect the real, productive economy wouldn’t directly suffer much from one percent higher. The stock market would, though. Especially indebted companies but also any company that has been engineering their price through buy backs. The Fed thinks “trickle down” asset inflation saved the economy. That makes the Fed and many people worry about removing the prop. Include me among the people who wonder just how bad financial markets will suffer. I could imagine a wide range. Unknown territory.

whats the buyback endgame, eventually you have all your own stock and you go private? that means maybe splitting up your company into a series of new IPOs, rinse and repeat.

The FEDsters have squandered their credibility many times over. That’s what low Financial stress index reflects. They could avail themselves of a useful mental faculty called self-reflection.

“No one knows how this will turn out.”

No one knows, but basic economics will give you a pretty good idea.

So far all the market has seen in regards to reducing the Balance Sheet is, well, BS.

Once that supply of debt instruments starts showing up in the market that old law of supply and demand will start to take effect just as it did when the Fed was pumping ‘money’ into the system: that increased supply reduced rates.

Once the supply is too great for the demand at a price point, yields on debt instruments will increase.

There are going to be some huge losses across the asset spectrum from bonds to real estate. The question is who are going to be the bagholders this time.

My SWAG is that the market finally wakes up (In my dreams??) and whacks some of pie-in-the-sky companies peddling crapola without any profits. Those companies will no longer have access to funds needed to continue the hype and join the long list of failed companies.

Real cash flow from operations will be the key. No real cash flow and watch out below.

One particular high tech car company that as of the other day was the 4th largest car company in the world by market cap comes to mind.

The market is in denial and that makes for nasty surprises.

On a related topic to see how a central bank can control a bond market all you have to do is look at Japan. A while back I posted that the rate on the 10 year bond had soared and was around the 0.1% level. It didn’t take long for the BOJ to jumped on the market and now the rates on that instrument are back down to 0.02% – a huge move.

Good points; rising yields will result in higher mortgage rates. Stalling housing market, the lifeblood of the economy, will hit government revenue, so no more subsidies for pie-in-the-sky companies. And soon, there will be a fast reversal.

Yeah. Check your investments for net debt v cash flow!

“Given how corporate bonds are now largely held by exchange-traded funds and mutual funds, this could get even more interesting.” – Statement by Wolf.

Is there any data, article or other evidence backing this?

Thanks for your answer

Total in US bond funds: $20.6 trillion:

Bond mutual funds, June 2017: $17.43 trillion

https://www.ici.org/research/stats/trends/trends_06_17

Bond ETFs, June 2017: $2.94 trillion

https://www.ici.org/research/stats/etf/etfs_06_17

Closed-End Bond Funds $270 billion

https://www.ici.org/research/stats/closedend/cef_q2_17

Dear Wolf

Thanks for the links. Unfortunately, the first two do not work anymore..

There is a paywall, but you can probably get there by googling it.

And the numbers are not right…

17.43 trillion is for all the assets.. but I am looking only for the assets in bonds held by ETF and mutual funds..

The numbers are correct. If you don’t believe me, why don’t you check the sources I linked? It’s really pretty simple…

Of if you can’t get past the paywall, google it.

OK, I’m going to help you with Googling it. You may not get the same results as I do if you Google outside the US. But try these key words – for me in the US, they generate the ICI reports:

total assets in us bond mutual funds

If you still can’t get the data, email me, and I’ll send you the PDF report from ICI.

wonderman, bond funds are a BIG DEAL. They’re the modern day equivalent of a savings account. Many pay interest monthly. Even the high yield bond funds are not especially risky. Some possibly most, spread the risk among 100 or more issues with an average maturity of a few years. If one goes bust you would not notice.

If rates rise and liquidity is seriously impacted in a bad way, share prices will fall and capital losses are possible for anyone who want to sell shares. While I am waiting for this day to buy in, many others will scream a little if their shares fall 15% – 20%.

Data, check. pokerface, check. no crash, check. Print money ad infinitum whee… everything looks fabulous.

The treasury sec. Might be James Bond but he respectfully isn’t Tron!

Bigger cans and a larger cake pan, desserts for everyone! I rubbed by naughty bits on every bar- Steve to Donald 10-4.

Buying at the peak of the biggest mania in history, thanks to the central bankers. Pure genius. Norwegian pensioners are going to rue the day they let a gang of fools and grifters manage their retirement money.

http://www.marketwatch.com/story/norways-sovereign-wealth-fund-has-50-billion-in-shares-on-its-shopping-list-2017-08-23

But the EU countries, Norway, and yes the US banks, still have to put that 100 billion plus a month somewhere….cutting back reminds me of the politicians when they say “we cut spending by 10%” which means in Washington speak they are only increasing spending on whatever to a 9 billion dollar increase in spending instead of a 10 billion dollar increase…. That’s why we kept going higher with Fed cuts….its hard o pinpoint when the cuts will cause real bleeding.

“hey pointed out, for example, that the corporate and government borrowing costs are likely to rise. At the riskier end, borrowing costs could rise significantly. In addition, the federal government’s borrowing needs is also expected rise, Jason Cummins, TBAC chairman, wrote in the letter to Treasury Secretary Steven Mnuchin. So just when the Fed is cutting its balance sheet and the cost of borrowing rises, the amounts to be borrowed by the government are expected to increase.”

= Riskier bond rise in Yields.

So lower risk Govt debt with lower yield looks more attractive safer and are available. Overall liquidity is still reducing as the FED is shrinking its sheet even if it does not raise rates. As the state increase its Borrowing.

IMHO the FED will keep raising, at 50 to 75, BP, PA, it may even raise 75 and drop 25 to freshen the market, but it will keep on dumping it sheet. Which will eventually force the risk to be savagely re-assessed in some bond’s as excess liquidity finally starts to recede.

This exerciser isn’t about interest rates (IMHO the FED interest rate game is a smoke screen), it is about reducing excess liquidity, that stayed in the wrong place. Reducing it very quietly.

Everybody needs to reflect, the FED never did QE like this before.

It is a learning curve for the entire American financial sector. Good Hindsight analysis, is still 15 plus years out.

My prediction is that in the final analysis. It will be determined “The medicine was correct but given to the wrong patient” (Wall street got what main street should have) as profits move, upstream and sideways, long before they move down, and asset profit only seems to move, up..

Or the operation was a success but the patient died

NO the patient lived.

However, the patient is now suffering sever side effects from the medication, that kept it alive.

Rather like a patient whose Gonorrhea is cured, who now has a case of Mercury poisoning, as Mercury was the medication used, to cure the Gonorrhea.

The Patient may recover from the mercury poisoning in time, but will bear the marks of both afflictions, for ever..