It depends on the value of the home.

What happens to home prices during the current housing boom and the next housing bust depends to some degree on whether the home is relatively “affordable” — whatever that means at today’s prices — or more expensive.

This is an important data point in the consideration for lenders that have to worry about their collateral value and for residential property investors and for homeowners who might want to get a foretaste of what is next.

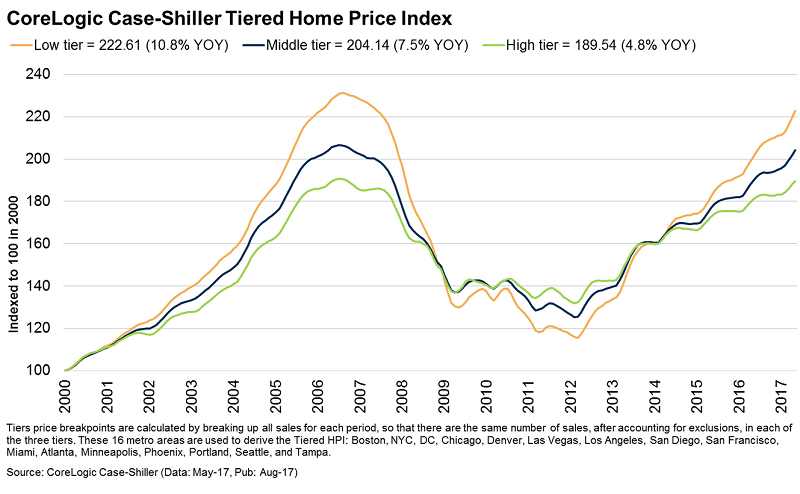

The CoreLogic Case-Shiller Home Price Index offers an index based on three tiers of prices — low tier, middle tier, and high tier. Like small-cap stocks versus large-cap stocks, the less expensive homes show much more price movements up and down and are thus far more volatile during booms and busts than their more expensive counterparts.

The Tiered Home Price Index (TPI) comprises 16 metro areas: Boston, New York City, Washington DC, Chicago, Denver, Las Vegas, Los Angeles, San Diego, San Francisco (five-county Bay Area), Miami, Atlanta, Minneapolis, Phoenix, Portland, Seattle, and Tampa.

Prices in the low tier rose 10.8% year-over-year, according to the TPI, published in August. For mid-tier homes, the index rose 7.5%. And for expensive homes prices rose 4.8%.

That principle has been true for the past 17 years of the index, covering two housing booms and one housing bust so far. The chart below shows how prices of homes in the low tier (yellow line) rise much faster than higher priced homes, but during the bust, they also plunge much faster and bottom out a lot lower (chart via John Burns Real Estate Consulting):

From 2000 through the peak of the prior bubble in 2006, prices for low-tier homes soared 131%. For mid-tier homes, prices soared 108%. And for high-end homes, the prices rose only 90%.

But during the housing bust, the low-tier plunged about 50%. By early 2012, they were only 18% above the level of 2000. The mid-tier index dropped 39% from peak to trough. But the high tier dropped only 30% and remained 34% above the 2000 level.

In the current price run-up, the same principle is at work. At the lower end, home prices have soared 88% from the trough at the beginning of 2012 to the last reading, while high-end homes have appreciated only 43% — less than half as much!

“Over the last 17 years, low-tier homes have now risen an average of 4.8% per year, while high-tier homes gained only 3.8% per year despite greater income growth at the high end,” the John Burns Real Estate Consulting newsletter says based on their US Housing Analysis and Forecast:

So what does this mean? If you focus on lower-priced homes, beware that you are investing in a more volatile section of the market from a pricing perspective and beware that lower-priced homes have appreciated the most. Remember that relatively high home prices can last for years (as they did from 2003–2007), so don’t panic.

And it has a piece of advice when things do turn around: “Just consider the risks” of lower priced homes as depicted in the chart above, “and always be ready to react when the market shifts for the better or worse.”

There is however another aspect than percentages: In dollar terms, losing 50% on a low-tier home in the $200,000 range is a loss of $100,000. Losing 30% on a high-tier home in the $2,000,000 range equates to a loss of $600,000.

But for investors with large sums at stake, that’s no consolation. Perhaps to battle this situation and have more control over the market when it tanks, the largest single-family rental firms in the US, Invitation Homes and Starwood Waypoint Homes, are merging to form one giant landlord with 82,000 single-family homes, concentrated in the low tier. But as the Burns report says, “don’t panic,” housing bubbles can last longer than seems possible, and so there may still be a little time left.

At the very high end of the housing market, where homes are listed for tens of millions of dollars, BS asking prices are now meeting the ax. Read… Whiff of Reality at Crazy Super High-End Housing Market?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Does this have to do more with the underlying land value? In run ups, more lower tier homes are being bought at higher prices for tear downs because improving the land is a better deal than buying an expensive home whereas when it is bottoming out, no one is looking to teardown anymore because demand has softened. More expensive homes therefore are driven more by people actually going to live in them and thus don’t have the extra demand for the cheaper land.

I fear the answer is sadder. It may be that in the downturn that goes with a housing crash, the owners of lower priced housing are more likely to lose their jobs and/or are generally less able to hang on for the recovery.

When I got my first mortgage at 14%, when it came up for renewal a year later it was 21%!

I was able to hang on, barely, and it recovered but I knew many who lost all.

I was at first surprised to read that lower RE suffered more. I thought it would be other way round. But if people are stretched by housing costs,

and which first time buyer isn’t, I think their higher vulnerability to downturn is part of it.

Really it makes sense. Low tier housing is cheaper so more people can afford to speculate on it. Also when prices get high, more high income people get pushed into the lower tier to buy property.

People assume that the price of a house represents all the risks associated with the home, but I don’t think it does. Do nice looking houses in Texas cost less because of continual flooding, probably not but they should.

People assume the appropriate amount of infrastructure is supported by the tax base, but I think the entire country has reached a tipping point where the infrastructure doesn’t reflect the money collected for its upkeep. If the infrastructure is deteriorating even in the expensive neighborhoods then what are these homes really worth?

The last couple of weeks have brought a lot of rain to New Orleans, even the nice areas, where it never floods have been hit hard by flooding. The infrastructure has deteriorated, pumps don’t work and were not being repaired, power generation failed and no backup systems were in place, to run the parts of the system that were working. Considering this, how much is property in the city really worth?

New Orleans is not the only place with this problem. How much is property on the New Jersey shore really worth if they can’t deal with storm surge? How much is property in Texas worth if there is a flood every time it rains?

In WW2 houses along the shore of Sydney Harbor were inexpensive because residents were afraid of the Japanese — in fact there were a couple of midget-sub attacks during the war. Today, Sydney waterfront is some of the most expensive real estate in the world.

In the early 80s when Hong Kong was in a panic about the impending 1997 handover to China, the prices of apartments on the upper floors of high-rises dropped sharply because it was assumed the Chinese wouldn’t bother to maintain the elevators when they took over.

“Today, Sydney waterfront is some of the most expensive real estate in the world.”

Maybe it is costly by Australian standards, but compared to all those multi-million dollar mansions in the Hamptons and in California, it is still ‘cheap’. Even cheaper now that the A$ has fallen from over parity to around the 80 cent area.

What is the highest priced house in Sydney? A$50 or $60 million maybe…………..and there are only a few of them.

Here in Melbourne, the record is around what, A$25 million………………

Lot’s of houses in the A$1 to $5 million area, a few in the A$10 million area, but not much above that.

The USA and maybe London make Australia look like a bunch of pikers when it comes to high priced individual houses.

I think people are more likely to react to danger that they perceive to be of the “clear and present” variety, so Japanese invasion, yes; climate change and infrastructure decay, no, since they hope and assume that those are things that will only happen after they’re dead.

And Strong Towns talks about the whole question of the real value of these houses. I’m no expert but it makes sense to me: https://www.strongtowns.org/the-growth-ponzi-scheme/

Yeah, and the Americans are a bunch of really stupid people too – I mean look at all that money they’ve spent over the years on wars and liberating people and for nothing.

Then we topped it off by forgiving war debt and then giving people MORE money to a bunch of ingrates – you know the Marshall Plan. We should have kept our money and let Europe starve to death.

Let’s see with a couple of examples: we had the Philippines and gave them independence and look what happened there.

Cuba we had that too and now they have a communist dictatorship with all its splendid lifestyle!!

Japan – yeah had that whole country as well – they have done pretty good though. Should have made it a protectorate like Guam or the Virgin Islands. Foolish giving it its independence.

And Europe – we had most of that as well and left – we should have kept it and did like the Soviets did to Eastern Europe.

Panama – another example that had under control and gave it up too.

Iraq – well, we did occupy most of the country, but that was a mistake the second time around and we didn’t get squat fort that either.

Nope, we wasted our money on a bunch of foolish ideas and people that really don’t deserve it.

I believe it, the factors are implied, people buy low tier housing because they need it, they buy high tier with discretionary income, often second or third homes. There is also the Zillow factor, which tends to commoditize homes in the same area with the same value. Its widely said that housing is not a national market, but when corporations get involved it has to be.

If mortgage credit shrinks or rates rise, and more sellers carry the paper, then prices should return to more intrinsic valuations, which means if you overpaid for a low tier property you might suffer more.

I have a vacant lot I would like to sell, and would carry the paper at a lower rate, if I could get my price. (That leaves the buyer an opening to buy it on spec) My reasoning is that chasing yield you can lose principal, in a land sale the collateral comes back to you.

The way my father has always worked. He has purchased a number of property’s over the years, always after a market crash or out of foreclosure. He will clean up the property, sell it and always holds the mortgage.

He bought a single-family house out of foreclosure for $45K in 2007, in an old, but decent neighborhood. Sold the house, but held the mortgage for a young family. They bailed after the young man lost his job. Dad just sold the house for $145k to a new mortgagee and he continues to hold the new mortgage.

Wolf, while I would welcome a west coast property crash – What is the reason that it would happen?

Many pundits have been predicting this for a few years now but the prices are not taking a breather (SF bay area esp. South bay and near East bay – Fremont).

Maybe the house prices would just plateau?

The only reason for crash would be a massive killing of 1000s of startups in the bay area and ensuing layoffs. Failing which, why would houses owned by either:

1. Overseas Chinese (who are laundering money and presumably don’t care a drop of a safe haven asset)

2. 2-income households

3. Long time owners with low property taxes

have no reason to drop in value. I only speak for the SF bay area where I have lived for a long long time; seen the 2004 recession; 2007 crash and have never seen the enthusiasm in house buying and corresponding prices.

Summary is: What would precipitate a price drop in SF bay area?

One uncited reason is that home ownership does not mean as much to this generation. They would rather rent. And so the corporate takeover of private property is in part due to corporations adapting to personal needs. That in enough will bring prices down, the problem with being a landlord is you can raise the rent but if your vacancy rate is too high it undercuts the business, you can only raise as much as the market will absorb. (Same thing in groceries which is one reason there is no real inflation) And sure grocers and landlords have the power to charge what they want, but hungry homeless people will have the last word.

“one reason there is no real inflation”

I wish I could live on your planet, a #6, medium, at Carl’s Jr is now over $8 bucks. My salmon special that was $9.99 two years ago is now $14

And a house in a so so hood is over $600K…….based on your metric if we get real inflation i’m bankrupt……..I can’t afford to live in the USA as it is and I make decent money……..for 1997

As long as lenders are willing to lend against overpriced property, the market won’t go down.

So the question is what will cause lenders to be too scared to lend against the properties?

In 2007, it was the freezing up of the private MBS market due to fear of mortgage fraud.

>So the question is what will cause lenders to be too scared to

>lend against the properties?

Your government guarantees the mortgages.

Remember when John McCain said the Fannie’s balance sheet was not backed by taxpayers dollars, uh huh, and there are a lot of you now who assume the Fed is an independent bank and ITS balance sheet IS NOT backed by US taxpayers, but you would be wrong. Unlike the first housing bubble there are not marginal originators who are feeding bad loans into the system. Sure values are extreme and assessments are 125% to pad the subprime buyer with a down payment, or cash back if you want. Corporations and hot Chinese money lead the way. It’s not like ARMS or interest only loans are everywhere. We cut out the subprime buyers, and affordable housing is getting scarce.

No one would be able to predict for sure the exact factor that will cause a crash. Some of the factors you mentioned are contradictory. Would Oversease Chinese be considered long term owners with low property taxes? Also the world economy is interrelated, a big crash in China will cause a big crash in the world. China now counts for 15% of the world’s economy. The powers that be in China will surely call some capital home, there’s already rumblings that groups such as HNA are being pressured to sell US assets.

2 income households. If you think this is a sign of strength, you must be joking right? What happens if one of them loses their job? Also if you’ve been following this blog, lots of startups and even big tech companies are not making any profit whatsoever. Uber, Twitter, etc, etc.

Too many weak players in the game.

The Bay Area is unique. It’s so expensive, people leave. When people lose their jobs, they leave in droves. They go where they can afford to live. Companies move because employees get too expensive. Or, like Schwab, they stay, but move more and more of their people to cheaper parts (Texas, Idaho…). This is already happening. Still new people are coming in, but the numbers are smaller.

In my last employment report on the Bay Area, I covered some of this. I will keep my eyes on it. Once employment flat-lines or shrinks, while the new supply from a historic building boom comes on the market, you’ll see a lot of pressure from the top down.

Also there may not be a “crash” in that sense – the last “crash” in SF took four years to play out. It hit bottom in Jan 2012, three years after QE began. The next one will be different … maybe even slower and even longer, which is my current guess.

But this is not how things play out in most other parts of the country. Every area has its own dynamics.

At least in the SF bay area; we are missing the obvious:

A massive addition of foreign born workers on H1-B and their spouses. These folks generally have children too.

So while the natives may move to cheaper pastures as Wolf points out; my experience on the ground is that net-net foreign immigration inflow exceeds the outflow of natives in the SF bay area.

If you ever visit Silicon Valley you would be surprised on how Chindian it is – mostly Asian and Indian and whites are even lower in % compared to overall in CA. (I am not White!). There are lot of whites though in management but not in engineering ranks where Chindians are the majority.

As to others asking what happens if 1of the 2 income households loses their job – how is that different from most of the country where 1 of the 1 income household loses its job?

As to San Andreas; it will happen once it happens – nobody loses sleep over it. Whether wise or not; that has not detracted hordes to move here.

Again, my analysis is local to SF bay area and the population pressure here is growing and adding to house prices (I agree lots of folks are stretching themselves).

Tesla, Snap etc. are not making money is no news. News will be when VCs stop bankrolling them.

I suspect since there NO FUNDAMENTAL ideas to put money into, the VCs are forced to plough money into all these hypeware creator in the hope that one of them will be the next Google. Since the cost of borrowing money is almost next to nothing; this cycle can go on for a long time.

Is there an expiry date to the VCs doing it? Please tell me.

History only teaches us to learn from mistakes in the past. Most are unequipped to learn on AVOIDING new mistakes. So until this party crashes (and I am rooting for it to crash) SF bay area is going to be immune to pressures relevant elsewhere.

Truth Always – the correct answer is: Very, very Chindianspanic. Everyone seems to get along pretty well, but keep in mind that if any group gets into power through money, political power, sheer numbers, or a little of each, well, it’s not fun to not be in that group.

2 conditions.

1. shelter buyers must be leveraged weak hands and a large scale event like recessions or stock market crash (source of their w2 income and RSU) hit the house out of the hands because they made a 30year promise without even a 3 year visibility of their income stream and assumes maximum borrowed money NOT at their 3x of income but 5,6,7 times.

2. Even first condition is met and weak shelter buyers become forced sellers, the 2nd line of defense in housing price is rent seekers. To remove them, you have to have rent/price lower than interest rate. Now the bay area’s rent/price is about 3 to 4%, still larger than short term rates, which are 1%. If this persists, houses will flow into rent seeker’s hands when weak hands in shelter buyer group taps out and you will NOT see significant price drop. My suggestion is that, in stead of rooting for a price drop, you better wait till

first condition happen, and then you start a “occupy central bank” movement and while you influence interest rate control out of their hands, you better pray you will NOT get stoned/egged by fellow leveraged home owners.

The reasons are always different and not so obvious otherwise smart people would have made a killing..

The housing has busted many time before even in bay area and it would

We just don’t know how and when

Two income households are lumped in with Chinese money laundering?

A majority of res mortgages are taken out by two incomes i.e., by couples.

What would affect SF RE?

Not necessarily a crash but a big correction would be caused by something that has to happen: regression to the mean by interest rates.

A UK bank economist said the other day that real interest rates are the lowest in 5000 years.

I don’t know about that but they are the lowest in a century.

If they merely go back to the average rate since WWII, many people’s mortgage payments would double.

There is a piece of data needed to accurately judge the risks: sure, long time owners who haven’t loaded up on Helocs are OK.

But we need to know how many mortgages require the support of rents, ranging from suites legal and illegal all the way to roomers.

West Vancouver never had even a hiccup in 2007-08 nor did the rest of Canada, but I don’t take that as proof it can’t have one.

Back when illegal suites were an issue ( they no longer are) it was estimated that without the income a third would lose their houses.

My niece’s former condo was sold twice in 4 months this year then she was evicted. Final price 470K for 540 square feet. Nothing fancy. West Van alright but noisy.

I think the last guys bought near the top.

Have you heard of the San Andreas Fault?

Right!!!!

There may not be an imminent crash but bad things could happen for all of use with out a crash.

For instance what happens if banks are finally forced to raise mortgage interest rates or lose money?

With today’s hard lending cutoffs in theory some people will be cut off from buying many homes because the new monthly cost will push them over 40-50% DTI.

Once this happens I assume the first thing we will see is lenders attempt to prop up prices still by loosening standards, faking incomes and getting the majority back into ARM loans. Because a 5/1 will be the only way to afford continued rising prices and “high” interest on 30 year fixed loans. That will inevitably create a massive bubble just like before though the trigger for the true start of the bubble hasn’t gone off yet.

Another alternative is interest rates go up and lending stays tight. In which cases prices will have to come down. To keep aligned with carrying cost. In this case recent buyers will get trapped in starter homes, and some may sell out of fear of losing value as interest rates creep up.

Further I suppose it is still possible, against all odds, banks find a way to suppress interest rates on mortgages for longer than anyone expects.

It does appear hard to pinpoint though what exactly will lead to a glut of homes being sold. But I see many scenarios where housing prices face harsh realities even if the result isn’t a rapid crash like 2008.

>What would precipitate a price drop in SF bay area?

The end of taxpayer guaranteed easy credit.

Falling rents, skyrocketing inventory, dead demand all of which are occuring.

Demographics. Play a BIG part.

A population chart from 1946 – 1956 shows 3 distinct birth waves, the first wave being the largest and each successive wave smaller.

These are the three Baby Boomer Waves.

First waver’s are now over seventy years old.

Second wavers are just now starting to collect pensions

Third wavers have just turned sixty years old, ready to retire.

Hand in glove with retirement goes life style change – downsizing.

The Boomer’s are selling off their big houses and moving to traditional retirement areas (warm climate) where they buy small houses, town homes, or condos. Often near large centers that offer complete, in depth health care facilities. These parts of the country are experiencing a real estate construction boom and have a demand for the product.

As for the parts of the country that the Boomer’s have fled from, the outlook does not look promising.

“The Boomer’s are selling off their big houses and moving to traditional retirement areas (warm climate) where they buy small houses, town homes, or condos.”

How do you reconcile the above statement with the below article titled “Baby Boomers Keep Tight Hold on Their Homes”?

http://finance-commerce.com/2017/08/baby-boomers-keep-tight-hold-on-their-homes/

One article with limited research does not make it so.

Total owner-occupied by household is 65% of that only 18% are in the +65 year old range and has been decreasing.

http://www.nmhc.org/Content.aspx?d=4708

OutLookingIn – that is exactly what has happened to my city on Vancouver Island. Boomers in Vancouver and Calgary sold their homes at a nice profit and have bought comparable or better ones for less money in Nanaimo. Many have not downsized, just moved to a lovely part of the world for a quieter life and relatively good climate.

The average price of a detached house here has risen 19% over the past year and developers are scrambling to find land.

In Denver regardless of price its Condo’s that fall first and the hardest with Townhouses and Patio Homes bringing up the rear rapidly following suit .

Strongly recommend that you get hold of a copy of Homer Hoyt’s One-Hundred Years of Land Values in Chicago: The Growth of Chicago to the Rise in it’s land values, 1830-1933.

Written in 1933. It was a very interesting early effort at looking at cyclical pricing within the economy. It also shows the same pattern of greater price swings in the periphery (less valuable) areas of Chicago. So your trend goes back a lot farther than you state.

They call it Chiraqu because of the murder rate. People are fleeing the crime, the mismanagement, the weather, and still the price of real estate increases.

If you have the land already, cement igloo houses (also know as bubble houses but that name sucks) are a cheap and lasting way to get a house.

But back on topic, is the 500.000 $ dollar or under houses the ones that can be considered “affordable”. Don’t expect the prize of those to sink any time soon unless dragged down by other crisis.

Of course next year or even December will be another deal. And junk/trash investment is called that way for a reason.

I read at a different site that there is no way this is a new “bubble” in housing. And they used inflation metrics to prove that.

I don’t give two shits about their inflation metrics, I couldn’t afford a house in 2006 and I can’t afford one now because their inflation metrics don’t seem to apply to my income and it drives me nuts.

real-estate is so completely out of wack. There is no way i’ll ever be able to afford a home again unless my income triples or home prices crash “again” by 60% minimum…..based on that article I mentioned, if their views hold true, homes in socal will be $1,000,000 for a crap shack in 2020 …..in an area with an average household (that’s household not individual) income of ~$65K….this is insanity.

Your patience would be rewarded

Socal is over frothy… just don’t know how and when itd burst

The last bubble wasn’t a bubble either until afterwards. Now the last bubble is no longer a bubble. Did you notice how “bubble” disappeared a couple of years ago as descriptor of the last bubble? The reason being that this bubble is bigger than the last one in many markets, and calling the last one a bubble would require you to call this one a bubble too, and everyone resists that.

Ah…youth. You forget that if everything never crashes (or just went down a bit) then 100 x 75 a building lot in Miami beach would be somewhere around 2 billion dollars now. In the 1920’s a building lot was $100,000. Well didn’t 1929 fix all that.

Now, Wolf, can tell you about SF in the late 1960’s, in 1988/1973 period, fear, fear that ‘I am stuck with an overpriced property”.

if you buy into ‘this time is different’ , chances are you will be buying the boat at high tide, not low tide and end up getting stuck on the shoal.

Save and have patience, when those around you have none.

One of my co-workers, mid 50’s married with two children under the age of 10, just bought a house on the SF bay peninsula. He indicated he will be paying more than $20,000 a year in property taxes. Now that is frothy.

“paying more than $20,000 a year in property taxes”

that alone is more than my rent.

About ten years ago a friend of a friend visited from East Orange New Jersey. Her taxes on a quite basic house, valued roughly the same as ours were 4 times ours for same services. 2500 versus 10, 000.

Thats nuts considering California tax rates for homes are pretty damn low. 1% with maybe 0.1-0.3% correction for local fees. But yeah you hit crazy tax numbers quick when you own a $1.5 million dollar or so home 0.o.

Scary to think that even if I bough a $1.5 mil place cash, the taxes alone cost me about as much as my current rent. Forever.

A man can live for a year on that amount of money in many parts of the world and have a decent life to boot.

Think of it this way – someone probably is, as its likely going directly to someone on welfare.

Waste is the issue.

“But as the Burns report says, “don’t panic,” housing bubbles can last longer than seems possible, and so there may still be a little time left.”

No, the trend will persist so long as the FED maintains low rates.

Corporate rental firms with access to cheap money are at the wheel this time (instead of NINJA homeowners living off doritos), so you can expect this to continue for at least another 5-10 years.

The FED is about done raising rates (no price pressures, too much money coming in from bubble land) and will soon begin cutting.

Most US states are hopeless junkies dependent on the easy money from stock advances to fund pensions. California is the welfare queen of this lot- barely even to keep its head up know, much less after a market crash.

There will be no reversion to the mean with housing for a long while.

Prices collapsed 40% here in the Bay area from 2007-2012 and the fed did nothing because they’re powerless.. I anticipate a much larger correction this time. It’s already started with falling rents.

People who believe in the omnipotence of the Fed belong to a secular religion, or a cargo cult.

Are low interest rates a good? Is it nice to have mortgage money below the rate of inflation? Then what is the source of this good or valuable thing? Is it a horn of plenty that will never empty?

In addition to all the private mortgages, the US has slowly mortgaged the country itself. That is the source.

There is a reason the patent office will no longer consider perpetual motion machines, but endless cheap money is one.

The Fed has also mortgaged itself and has had enough.

There could be another act or two to this play however.

Populist politicians, unhappy with the Fed’s attempt to take away the punch bowl, may abolish the Fed or at least its independence and print money directly.

This will postpone the final acts.

I think house market is an important but still just another way using people in debt to increase control and gain power.

War/external tension is just diversion of financial crashes.

Citizen behavour is key. Easy lending deeper in dept they become an easy prey. Set up by Deep state moving positions forward yet another step. Or finally?

Where will it all end….. In the long run we are all dead