It will be ignored until it’s too late.

Everyone who’s watching the stock market has their own reasons for their endless optimism, their doom-and-gloom visions, their bouts of anxiety that come with trying to sit on the fence until the very last moment, or their blasé attitude that nothing can go wrong because the Fed has their back. But there are some factors that are like a tsunami siren that should send inhabitants scrambling to higher ground.

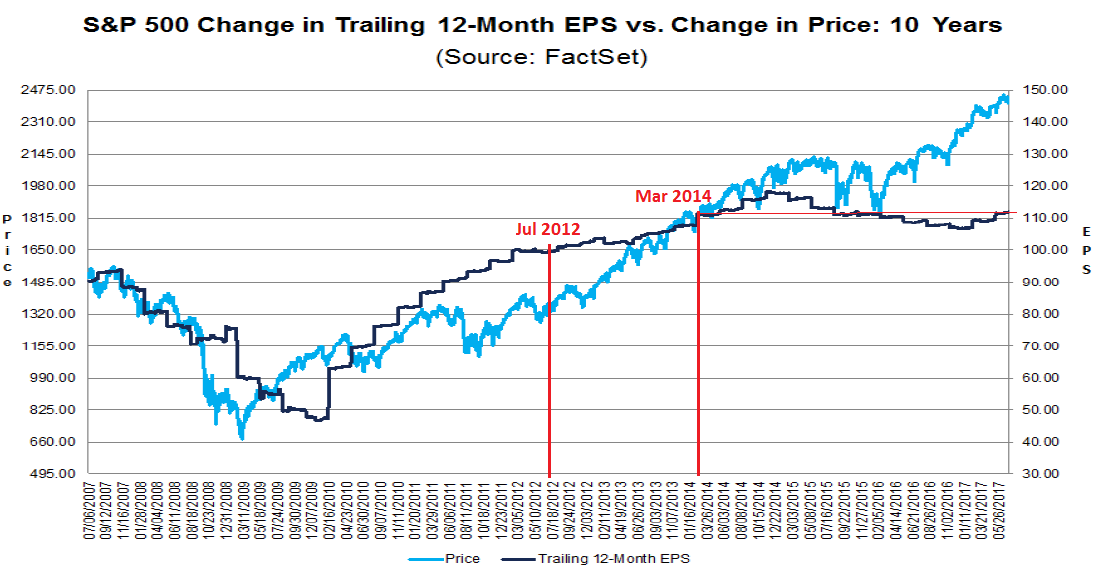

Since July 2012 – so over the past five years – the trailing 12-month earnings per share of all the companies in the S&P 500 index rose just 12% in total. Or just over 2% per year on average. Or barely at the rate of inflation – nothing more.

These are not earnings under the Generally Accepted Accounting Principles (GAAP) but “adjusted earnings” as reported by companies to make their earnings look better. Not all companies report “adjusted earnings.” Some just stick to GAAP earnings and live with the consequences. But many others also report “adjusted earnings,” and that’s what Wall Street propagates. “Adjusted earnings” are earnings with the bad stuff adjusted out of them, at the will of management. They generally display earnings in the most favorable light – hence significantly higher earnings than under GAAP.

This is the most optimistic earnings number. It’s the number that data provider FactSet uses for its analyses, and these adjusted earnings seen in the most favorable light grew only a little over 2% per year on average for the S&P 500 companies over the past five years, or 12% in total.

Yet, over the same period, the S&P 500 Index itself soared 80%.

And these adjusted earnings are now back where they’d been on March 2014, with no growth whatsoever. Total stagnation, even for adjusted earnings. And yet, over the same three-plus years, the S&P 500 index has soared 33%.

This chart shows those adjusted earnings per share for all S&P 500 companies (black line) and the S&P 500 index (blue line). I marked July 2012 and March 2014 (via FactSet, click to enlarge):

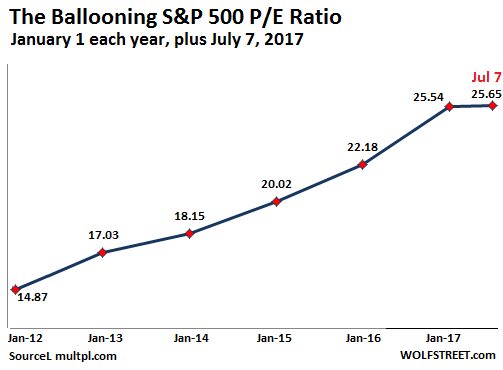

Given that there has been zero earnings growth over the past three years, even under the most optimistic “adjusted earnings” scenario, and only about 2% per year on average over the past five years, the S&P 500 companies are not high-growth companies. On average, they’re stagnating companies with stagnating earnings. And the price-earnings ratio for stagnating companies should be low. In 2012 it was around 15.5. Now, as of July 7, it is nearly 26.

In other words, earnings didn’t expand. The only thing that expanded was the multiple of those earnings to the share prices – the P/E ratio. Such periods of multiple expansion are common. They’re part of the stock market’s boom and bust cycle. And they’re invariably followed by periods of multiple contraction.

How long can this period of multiple expansion go on? That’s what everyone wants to know. Projections include “forever.” But “forever” doesn’t exist in the stock market. The next segment of the cycle is a multiple contraction.

The 10-year average P/E ratio, using once again the inflated “adjusted earnings,” not earnings under GAAP, is 16.7, according to FactSet. This includes two big stock market bubbles, the one leading up to the Financial Crisis, and the current one, but it includes only one crash. This imbalance skews the results. Two complete cycles would bring the average substantially below 16.7.

Nevertheless, even getting back to a P/E ratio of 16.7 for the S&P 500, when the current PE ratio is 25.6, would signify either miraculously skyrocketing earnings or a sharp contraction of the market. The first option is a near impossibility. And the second option?

Markets overshoot, which is what reversion to the mean entails: the average isn’t going to be the floor! And that’s why this type of unsustainably high earnings-multiple is like a tsunami siren where the arrival time of the tsunami remains unknown – and that’s why it is ignored until it’s too late.

Already, bankruptcies are surging as the “credit cycle” exacts its pound of flesh. Read… Consumers and Businesses Buckle under their Debts

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Fundamentals do not matter to most. Buy the dip. Perhaps we’re on the path of Zimbabwe’s stock market. $1 Trillion Zims means nothing more than toilet paper.

The ‘zim’ has collapsed. No one took the latest addition of a zero seriously and no one would trade anything for them.

Zimbabwe has been dollarized for some time, like Panama.

The hundred billion zim ( I forget what they were called) can be purchased as a curio at some coin dealers.

I’d like to comment on this (much needed) market correction happening.

First, the powers that be (central banks, politicians, globalists, etc., etc.,) have a problem on their hands re; stock valuations. First, due to NIRP and ZIRP Babyboomers (12,000 per day retiring JUST in the U.S.) have shoved a ton of cash into equities seeking a return. The NIRP and ZIRP have blown massive bubbles in the housing market as well (typically a Boomer’s largest asset). In order for the Boomers to realize their paper/digital (fictitious) gains on these assets, they need to sell them. A sale requires a buyer. A buyer, in order to purchase these assets at these prices requires money. Money in a fiat system is a derivative of credit expansion and an increasing velocity of money.

When equities correct, the Boomers (who have worked their way through many’o recessions and contractions) will do what they always do — shut off the spending, save as much as they can and wait for things to return to normal. The boomers favoring cash over other “assets” will starve equities markets of much needed liquidity to “rebound”. Further, many like in 2008 will elect to stay in their jobs, preventing Gen X people from promoting and preventing the hiring of Millennials … exactly the same people they need to purchase their homes (to realize their gains) to retire.

However, this deflation of multiple bubbles at the same time (I am just speaking of equities and single-family residential housing — the bond market is a whole’nother story) will turn into a self-feeding cycle.

Leveraged asset valuation shrinks –> collateral calls –> sell other assets to meet collateral calls –> leveraged asset valuation shrinks

This cycle and the over-leverage of the system is going to act as a steam-roller at an egg-farm as boomers scramble to preserve their ability to retire at some-point before being put 6′ under.

Second, the above assumes the solvency of the banking and financial markets, and most importantly the survival of all of the half-dozen “material” fiat currencies the world over (the failure of only one of which would wipe out the entire world).

If any material bank, government, fund or any other organization starts wiping out loads of “cash or cash equivalent” collateral … all bets are off. The only thing to stop the runaway downhill steamroller at that point is money printing like the world has never seen. Add a zero to all central banks balance sheets to just stabilize things.

We live in interesting times gentlemen. We are all just biding our time, waiting for that one spinning plate to quit spinning and wipe out the clown’s entire show.

YES…makes sense. However, Emerging Markets will continue to grow for decades. Diversification is the key to success.

Nicko2, Emerging Markets as far as I know, rely pretty exclusively on the western civilization to sell their products and resources to.. When the western bubbles pop, and they will, everything goes Kaboom! Emerging markets will go to hell just because they are like China, the consumer isn’t much of their own base. For the most part, their workers do not get paid enough to purchase what they make but also there are so many people and such lousy living standards that there is no place to put that western washer and dryer or double door refrigerator or that 55″ TV, and the power is to intermittent or of poor quality to make them work very long.

To be honest as I’ve stated in earlier posts this is becoming all too reminiscent of the late 1920’s leading up to the Great Depression .

As for Nicko2’s assumptions … sorry mate but all the ‘ so called ‘Emerging Markets especially the BRIC’s across the board have stalled at best with many heading into a severe death spiral … all having become just another Potemkin Village about to be exposed

e.g. They aint no real and viable growth anywhere on the horizon nor even the very distant future …. cause you can’t diversify where there’s no substance to be had … and you can’t squeeze blood outta a rock

@ Economicminor

Private consumption as a share of global GDP:

https://www.bcgperspectives.com/Images/Emerging_Markets_Strategy_ex06_large_tcm80-199117.png

Long India, Mexico, Indonesia, Malaysia, Turkey, South Korea. These countries have huge domestic markets

Some of those emerging market countries will cease to exist in their currents forms… in decades to come.

@QQQ

“Some of those emerging market countries will cease to exist in their currents forms… in decades to come.”

Remember 1998? The Asian debt crisis? The U.S. and Europe, through their flying monkeys at the IMF and World Bank got on their pedestals, imposing “austerity measures”, strict conditions on borrowing on many countries in South and south east Asia.

via IMF

“On the surface, the numbers speak for themselves. In 1998, during the depths of the Asian crisis, aggregate output in the so-called ASEAN-5 – Indonesia, Malaysia, the Philippines, Thailand and Vietnam – plunged by 8.3 per cent. Real GDP in South Korea – long considered the darling of Asia’s newly industrialised economies – contracted by 5.7 per cent that year. But then the tough conditionality of IMF bailouts and adjustment programmes – Asia’s own dose of austerity – kicked in.

In response, current-account balances – the Achilles’ heel of the so-called East Asian growth miracle – went from deficit to surplus. For the ASEAN-5, current-account deficits averaging four per cent of GDP in 1996-97 swung dramatically into average surpluses of 6.8 per cent of GDP in 1998-99. A similar transformation occurred in South Korea, where a 2.8 per cent current-account deficit in 1996-1997 became an 8.6 per cent surplus in 1998-1999.”

In 2008, when it came to their own economies, the U.S. and Europe did the exact opposite. TARP, QE, credit flowing like water.

In a few years from now, it is the U.S. and Europe that will be tottering. Not vice versa. I am investing accordingly.

Haus, “…waiting for that one spinning plate to quit spinning and wipe out the clown’s entire show.” Lol… I like that analogy, like the good ol’ days of The Ed Sullivan show, right?

Idaho Potato You are correct The developed world will be where the majority of the pain will be felt no doubt about that This aggression will not stand man quoting Mr Lebowski( the poor one)

Wanna hear something funny about the BRICS ?

One is South Africa, where Zuma is firing a Minster of Finance every month or so. This is looking sadly like the next Rhodesia, which turned into Zimbabwe

When you think what it could be, the next is as bad: Russia. The state, i.e. Vlad and the 1000 or so ‘made’ men now have their tentacles in most of the economy.

In case anyone disagrees that the situation is dire, the current head of the Russian Central Bank has joined former minister of finance Alexei Kudrin in stating: ‘there is no alternative to painful fundamental reform’

Both should get food tasters.

economicminor – Not only that, but consider the large and growing “internal third world” in the US itself.

I don’t have running water, do have “the electric” and after 4 years without internet, my employer finally sprang for that – I could not justify spending 10% of my gross income for internet access. I have a half-size fridge with a little “frost free” freezer in the top part, I love my little Frigidaire. I have two radios – a Sony “survival” radio that can go almost year on a load of C batteries, and a Sangean radio that eats batteries like a kid eats candy but can plug in also, and mainly, can blast – it gets loud around here and sometimes I have to crank it way up to hear it.

I don’t have a TV if for no other reason than I don’t want the electricity consumption a TV would entail. Same reason A/C is an open window or a small fan.

I am going to be 55 in a couple of months. I should have a typical suburban-ish house, a car, all that stuff. Instead I live like a poorish person in, say, Greece or Poland.

There is a pretty large chance I’ll never own a car again. And although I live pretty humbly, there are literally thousands here living on less than I do. Probably 10% of working-age people here in San Jose don’t make the thousand a month I do.

There are more people falling down to my level than there are ascending to the upper middle class. Or even rising from working class to middle class. This is why the homeless camps are growing. This is why the car manufacturers are in trouble. This is why public transit use and bicycle ridership are up.

Expecting to be able to lean on the US middle class is pretty foolish considering the US middle class is becoming an anemic 98-lb weakling.

HT, glad to see you posting here. You put up with too much BS at ZH – but tend to have better framed arguments than most (not agreeing with all them per se – but I do prefer to consider well structured arguments different from my own as an opportunity to learn).

Regards,

Cooter

I was there in 2003 before hyperinflation took hold. I was driven about 150 miles to get to my destination and there was constant evidence of ‘panning’, people digging holes in the ground looking for gold. Petrol queues could be dangerous I was told but the people I met were wonderful to me even though they were struggling.

Back then if the Zim dollar had been physically larger and had good wicking properties it would have been cheaper to wipe your arse with, on a Zim dollar to bog roll sheet ratio!

Won’t be Zimbabwe but definitely will be worse off than Europe or parts of Asia. Don’t worry stocks will be up another 1% tomorrow as the automated funny machines are programmed to deliver 10-15% returns to infinity. pay no mind to the doom and gloom misinfo idiots. this will continue to ride until they decide to sheer the sheeple.

Excellent comments so far. I enjoy reading every bit of it! This will be a great blog document in the future after the next big crash. We have to keep it and review it for the next post-crash crisis blog. When is that? Who knows, perhaps sooner than later. However, make sure you don’t have to panic with the crowd! Have a great week-end and summer. All the best from Switzerland.

Yes the day of reconning will come sooner or later and it will come. Nothing goes up or down forever

Makes Japanese stocks look cheap even with their funny accounting!

Yes, the PE will revert to the mean as usual.

But this time it’s different, in two major ways.

First: there’s pretty much no chance the Fed is going to ride to the rescue.

It’s shot off its powder and a lot of its credibility.

Second: we will soon find out what the HFT robo- programs do in a major correction. My guess is they aren’t contrarians and turn it into a tidal wave, and over correct the PE ratio in the other direction.

Nick,

I’ve been wondering the same thing.

Now that 90% of trading on Wall St. is done by computer programs, what happens in a true sell off?

For me, it’s hard to say. For one thing, the NYSE will simply turn the market off after an hour. But what about the next day? In a major sell off, will the NYSE be open for only one hour per day?

different this time because the auto trade machines don’t use real market bid and ask to determine price. instead they set the price and let the auto bid ask funny machines play out a ridiculous fake trade scenario throughout the day. most ridiculous moment is watching those clowns ring the morning bell. watching the markets use to be exciting and interesting. now it is like watching a bunch of old farts play bingo at a rigged game – dividing their skimmed profits.

In all the crashes since 87 there was still a significant number of Boomers that bought into the buy-and-hold philosophy.

Even in 2008 the oldest boomers were just 62 and could hope to extend their work years and recover.

However starting in 2011 the oldest Boomers started hitting 65.

https://www.census.gov/prod/2014pubs/p25-1141.pdf

When the selling starts, how much extra panic will be generated by Baby Boomers trying to save some vestige of their retirement fantasy?

In 2008, my parents were not terribly concerned, as you said, they had bought and were holding. Ten years later, they’re very concerned. My mother is especially high anxiety and I’ve had to reassure her I will support them if it comes to that.

Boomers have tried to convince subsequent generations of “buy and hold” but this seems to benefit only boomers. If you buy right now, how long will you be holding until after the next crash just to be made whole again? Sorry, no thanks, this Millennial remembers 2008 vividly.

Millennials should stop contributing to social security yesterday. We are each ultimately responsible for our own retirements (or our kids are), and I don’t trust SS to be solvent when I retire. What happens when Millennials start coming to this conclusion en masse?

I remember people saying the same thing about social security back in the 70s. I know I felt that way back then.

The government will just print to keep SS solvent. Millions of people leaving employment and living off meager SS earnings is deflationary enough. SS becoming insolvent would be catastrophic. Makes far more sense for the government to print the meager earnings.

Yeah right print of course you are correct but as we all know that’s nothing but a stealthy default Better get your vegetable gardens cranking at full capacity now and beat the rush all you retirees

Clash of the generations is what will happen, and it will be ugly. Here we have the most spoiled generation in history meeting the most horrific future in history. There will be blood.

It’s just algos testing what happens when they divide by zero.

Max

Algos are written by people, even algos that write algos are written by people. And that is the inherent flaw.

And why can’t you divide by zero? Well, because the rules of Math say it is not possible. The mini-flash crashes are the precursors to what happens when an algo meets a conundrum.

At age 70.5 anyone with a retirement portfolio must being to take a minimum annual disbursement. The more you have socked away the more you must redeem each year.

The baby boom in the US really took off in 1951 and peaked in the early sixties. As people near retirement age they reduce the proportion of equities in their portfolios and this is happening now. In a few years the minimum annual disbursements will kick in with a vengeance on those with the largest retirement accounts. This also applies to any inherited IRA type accounts at the time the account is transferred.

Against this demographic bulge there was a baby bust that began in the late 60’s and continued until the baby boom ‘echo’ in the mid eighties so there are millions of fewer people in this cohort to buy the shares of their parents and grandparents.

Demographics and population distributions may have more to do with stock prices than any chart Wall St. analysts create.

I wouldn’t worry about the 70.5 disbursement rule. They’ll “temporarily suspend it” when they ban selling equities (nvm ban shorts) when this finally turns around.

Who needs retail purchases of shares when the Fed buys from Goldman who buys from J.P.Morgan who buys from BlackRock who buys from the Fed.

All that matters is the appearance of a market and the churning and skimming for the players at the top.

Also the 70.5 rule is an IRS rule. It means that people have to move the money from one account into another and add it to their yearly taxable incomes.. It does not mean the money is spent nor does it mean it has to be removed from the system.. Just taxed. Many people will not pay anything as they won’t have enough to be taxed. For me it is an insignificant pain in the ass. I am not going to change my lifestyle because I have to move this money from one account to another.

Anyone who is 70 at this stage of life and isn’t in a rolling, short term, treasury direct (personal account) – is an idiot.

https://www.treasurydirect.gov/

When the dollar tanks – you can’t avoid the pain that comes with it – particularly at 70. TreasuryDirect is as close as you can get to cash safety and liquid funds (assuming you can manage your cash flow).

Personally, I invest in beer (they can’t confiscate that) and knowledge (can’t confiscate that either). I will take a horribly over taxed job rather than nothing any day of the week.

Regards,

Cooter

A good beer is great. But it’s hardly a “long-lived asset.” But knowledge is.

Factset also review share buybacks. Wolf you present EPS. Shares in issue have been shrinking about 2% a year. If you adjust for that the earnings dynamic shows substantial margin compression. Does Bloomberg have a margin chart that anyone can post?

Rob

There is another complication with this data that makes it look “less bad” than it is: There has been a wave of M&A over the past few years.

Each time two S&P 500 companies combine, a new company and its earnings (and shares) are brought into the index to keep it at 500.

If an S&P 500 company acquires one that is not, it also brings those earnings into the S&P 500 earnings.

If the acquisition is structured as a (debt-funded) cash deal, the acquired company’s shares will disappear from the share count. So the total number of shares in the index goes down as a result of this transaction. And the new company will add its shares and earnings to the index.

The share count stays flat if the acquired company was outside the index. But their earnings are brought into the index. So it boots earnings per share in the index though overall corporate earnings have not changed.

Retail investors dont hold that much control on prices from a sell off its the institutional side, right? So is this market rise from QE money borrowed on the corporate side as individuals have to jump moore hoops after the GDepression? .Ps Wolf, I’m new to your blog and lovinging it. Great input and knowledge from the community too! Glad I found it even though I live in Shanghai, China.

Scott, we would love to have some of your insights abut China. What you are actually seeing versus what we are told by MSM.

Its like an office fire alarm, but everyone prefers to stay at their desk even though the building is on fire.

History shows that this can continue for a while before everyone rushes for the exits.

Question is whether we will have a hyperbolic phase first and once the markdown phase begins, how much of a markdown there will be. Jeff Gundlach says to raise cash now, let’s see if he is right again.

“everyone prefers to stay at their desk even though the building is on fire.”

Like the plastic wrapped burning apartment tower in London, “everyone is TOLD to stay at their desks”. Because our “betters” have everything under control (as they rush to the exits).

Oh, the NY Fed tells us everything is just fantabulous.

https://www.msn.com/en-us/money/markets/us-households-see-spending-up-job-prospects-improving-new-york-fed-survey/ar-BBE9gh5

The thing is, this is all based on “sentiment”, not actual economic activity.

“Like the plastic wrapped burning apartment tower in London, “everyone is TOLD to stay at their desks”. Because our “betters” have everything under control (as they rush to the exits).”

In the UK the recommendation for tenants to remain in their flats in case of fire elsewhere in the building, has been in operation many years with the object of avoiding risk and saving lives. It has worked well in buildings of traditional construction.

A proper enquiry should establish the part played in this tragedy by new construction techniques and forms of property management.

Good call Rob. It would be interesting to see how much has been spent on share buybacks with reference to S&P 500 companies. For some companies that’s the only thing left in the locker as this article states growth isn’t going up anywhere soon.

Aside of share buybacks it would be interesting to see what the debt levels are of the S&P 500 companies.

It would be equally interesting to compare share buybacks to actual operating earnings from these very same corporations.

http://blog.yardeni.com/2017/07/us-corporate-finance-show-me-money.html

Buybacks, profits, cash flow.

Comparing the U.S. to other markets

https://www.ofwealth.com/us-stock-markets-unique-problem/

Thanks Idaho for the figures.

Really interesting American companies spend so much of their cash on dividends and buybacks.

Paying ever more currency for the same thing has a name, it’s called inflation, which is what they want. Same as every other item not included, or low weighted, in the inflation basket.

Here in Florida, I know lots of people with boats and yachts…some really big yachts. I always ask if there are enough life preservers onboard. 90% of the time I get a blank stare or I don’t know. I never get a worried look.

Stock market, bond market, commodities market…same thing.

Why in the world would you get a worried look?? Who did you ask about the life preserver situation? Chances are the owner who is not also the captain might not know. However, the captain (owner or employee) and crew of ANY vessel sailing ANYWHERE under USCG jurisdiction will know that one life preserver is required for each passenger- in addition to life rings, buoyant cushions and whatnot, and must be easily accessible.

I’m afraid you’ve chosen a very poor analogy here.

rx

Yep, the owner is generally not the captain. The Captain will be in deep shit if they don’t comply with the safety rules and they can get checked by the coasties at any time day or night.

“People of privilege will always risk their complete destruction, rather than

surrender any material portion of their advantage”

John Kenneth Galbraith

“Thru out the ages People and Entities of power and influence during an era/age of transition * when recognizing they are about to lose at least some of their power and influence are faced with one of two choices ; Either chose to lose gracefully accepting less power and influence ** while still being able to maintain a fair amount of power and influence albeit at a diminished level : or fighting it out to the bitter end making stupid , desperate , illogical , irrational and self destructive decisions leading to their ultimate demise with most peoples and entities of power and influence choosing the later ”

John Lukacs ; ” At the End of An Age ”

And errr … taking a look pretty much around the world today .. stupid , desperate , illogical , irrational and self destructive has pretty much become the norm

* We are now deeply embedded in a time of transition having exited the Industrial Age with no new nameable age on the horizon ..

** The two best historical examples of accepting loss gracefully while maintaining a fair amount of power and influence are the British Empire post WWII and the Etruscan Empire

Good comment TJ. (and all the rest of you thinking folks!!)

I remember listening to a historian speak in 2006. He said that the US was beginning the state of a collapsing empire due to over-expansion in all facets and that in our lifetime we would all see the same stair steps down mirroring what befell the British Empire. (He was British).

His advice, ” Relax, you’ll get over it….Life goes on and there is no reason why individuals who are prepared will not continue to do well. Life doesn’t end”.

What will be the story we tell ourselves going forward, and I speak as a Canadian who was born in the US. This applies to all of us inhabitating never never land. Will it be, “4…even 5% growth is possible and we will be great again and all debt and obligations will be irrelevent. Perpetual adolescence is possible”!! Or, “Well, we thought something was amiss, so we prepared to the best of our ability. At least our family is debt free and we own our home”.

Alas, I fear a big war looming over N Korea and the nightmare will continue until the clock breaks. Best to be at least used to living within means when it happens. Life does indicate change, and a whole lot of surprises are possible. Unicorns under the Christmas tree, and unlimited opportunities have not been part of the human condition as far as I know. It doesn’t matter whether it is wrapped up in the Flag, or wishful thinking, either, it just doesn’t change the laws of reality and common sense. Individuals have to take responsibility…right now, even if our so-called leaders don’t.

That historian sounds like Niall Ferguson.

I think you’re the one who mentioned the documentary comparing the propaganda leading up to the Great Depression with that of today. Do you have the title or link to that? Thanks.

Remember, buyers buy companies’ futures. Take TSLA. When will they declare their first quarterly profit, if EVER?

How is the 2nd hand market? Are folks aware that these batteries won’t last longer than 1000 deep cycles or 7-8 years? Then: it will be time to spend about 25 grand on a new battery!

Central Banks try to con every body into turning low profits and low yields into “the new normal”. CNBC shills touting “AAPL to be worth a trillion” etc. need to be ignored by serious investors.

Those 3,000 sales jobs shed by MSFT ain’t coming back. Keep watching actual payroll hours and tax deductions. “Job reports” are b.s. when the total hours worked 7 total income haven’t increased!!

Tesla Batteries are made up of 6800 or so 16850 batteries. It should be possible to refurbish the battery packs for much less than $25,000

Tesla is about the most exciting thing to happen to the automotive industry in a long time.

Yeah, I’m sure that when everyone wakes up from the FANG MATRIX, looks around, and starts applying some fundamental analysis Tesla will will be one of the first stocks that gets hit.

Maybe the problem is that nobody knows what ‘fundamentals’ are anymore.

Tesla have a big battery project that is going to start in South Australia.

Musk said that it will be up and working in 100 days from when the contract is signed or it is free. IIRC it is a 100 megawatt battery complex to be powered by some solar farm in the vicinity of the battery.

Don’t know when the contract will be signed, but one project to watch and see what happens.

The entire company cycle these days has been turned on its head.

Way back in the good ole days a company had an idea, floated some shares at a cheap price, made progress, floated some more cheap shares and then started production, and and finally made some earnings with the share price going up.

Now companies get huge valuations for pie-in-sky crap, no earnings, and no real production.

If and when I ever go back into the share market, it won’t be to buy companies in the USA or Australia.

I’ll stick with what I know and that is Japan.

I’ve never owned an electric or hybrid, but wonder how their re-sale value holds up compared to, say an Accord or a Corolla, especially considering the above. Anyone know? It also amazed me when Mercedes bragged in an ad I saw that one of their models had 40 computers. Frankly, I would be in the market for a car that had none- three dozen more headaches when the warranty expires, IMHO.

If adjusted earning look that bad, how about GAAP earnings? And even worse considering the massive stock buy backs.

I really don’t understand the psychology of buying at historic highs, especially with interest rates trying to work their way up.

“…economic fundamentals and the stock market. They have been surgically separated a long time ago. Keep your eyes focused on the stock market, and you have no clue what is happening with the economy, corporate earnings, corporate revenues, consumers, business in general…. You’re just betting on the greater-fool theory. Which works great, until it doesn’t.” – Wolf Richter

https://wolfstreet.com/2017/06/25/the-economy-is-suffocating-major-adjustment-period-coming/#comments

I hope my counter-culture point of view isn’t entirely remiss on your blog.

There is nothing more economically fundamental than producing your own goods and services, as best you can. Certainly most folks don’t do that, for all kinds of reasons.

But it’s worth saying that it’s possible, IMO.

He who marches to his own drummer that way and does something foolish is in far greater control of the damage than the fool who bets on stock prices rising for too long, IMO.

” I hope my counter-culture point of view isn’t entirely remiss on your blog.”

In case you hadn’t noticed … you’re not alone . And lets face it RD .. though we made a hell of a lot of mistakes back in the good ole counter- culture days … overall … we were dead on right about the majority of things we stood our ground on … with our being proven right with each and every day and action .

Rock On – Remain Calm ( despite it all ) and do Carry On

TJ

As for emerging markets continuing to grow, where has the money to date come from to bring the growth?

Developed countries.

So when the boomers pull out of emerging markets on mass for their retirement earnings, how will emerging markets continue to grow?

T

Great comment, however, I think the boomers (retail investors) account for 30% of market buy in even if they are in a fund, right? if true, we need to watch out for institutional investors, right? but clearly Wolf has arduously documented smoke in the building so how long to wait?

Scott

The entire market since 2009 has been Central Bank money/credit creation.

A quick look at the big institutional banks shows about a 100% growth in their balance sheets. And GDP has barely moved.

To know what Central Bankers are going to do, think about a drug dealer that is also a user.

The ” Black Swan ” never comes when expected .. nor can its arrival be clearly anticipated … what will happen is one morning we’ll all wake up to the news that its finally landed and here to stay for quite awhile … with all bets being this Black Swan will be bringing an entire bevy of fellow black swans with him.. some as bad .. many potentially worse .. from politics to economics and all places in between

Sigh .. this … is gonna be ugly .

People in general are not really expecting black swan…

the proof is.. the ever rising stock market…

people holding the view that market is too high and prone to fall are quite limited… otherwise asset markets won’t keep rising..

I don’t know if the bubble crashes or not but everyone knows for sure that bubble is becoming bigger and it is only possible when majority of the people believe that prices won’t go down

The reality is as stated above is that the BRIC’s have already started falling out of ” The Wall ” with nothing on the horizon to replace them . Fact is they were all nothing more than Potemkin Villages to begin with

The number of listed companies on the NYSE is about half from the peak in the 90’s. The stock market is now a crowded trade, too much demand not enough supply. All the mergers and buyouts have hollowed out the exchanges. Oh well, who knew?

Petunia, et al,

If I might ask a question;

There is a company, whose stock I used to own, called Immunocellular…IMUC. It was found to be manipulating test data, and now have multiple shareholder lawsuits pending…. Stock dropped to under 90 cents a share, and then they received a notice from the NYSE for non-compliance…share value aggregate too low. The NEXT DAY the stock jumped to $2.00+ a share, with virtually 90% volume trade. thus avoiding delisting.

I’m not a stock guy, but I expect that there was a less-than-arms-length transaction within the company…probably last ditch, and illegal…not to mention a taxable event.

What actually happened?

thelocalpragmatist, you missed that class action lawsuit whose deadline was June 30th for stock promotion schemes.

Two possibilities.

The first is the activity of dip buyers who, to quote Mr Richter, “try picking up pennies in front of the steamroller”. Typical dip buyer strategy is to single out some penny stock who’s getting hammered and send it soaring but at least 15% day on day, thus attracting the attention of quant funds, who in turn will send the stock soaring a whole lot more, as they are pretty much all set up the same way.

Dip buyers do not care about the company itself: their temporal horizons are pretty narrow and are only interested in avoiding delisting for long enough to make their profit and dump their whole holdings upon both quant funds and reatil investors.

Second is that IMUC may have run into a vulture fund. There are several types of vulture funds, including some which specialize into lending money to distressed entities in return for shares obtained directly from owners. The loans often come with clauses that a large part of them should be used for share buyback programs, and we all know quant funds love buybacks. At that point a scenario similar to dip buying play out: buyback sends shares soaring, the software pick it up and start buying a penny stock quickly doubles or triples in value, again enough for those involved to turn a profit and abandon ship and leave the usual suspects holding the bag of their own greed.

MC,

Thank you for the reply. Might have been, as you suggest, a dip buyer…stock opened today at $1.50…a 25% loss from the bump. I expect that would pencil out somewhere considering the volume and timing of the trades?

The company has almost no assets, other than the intellectual variety…and that in a failed attempt at a medical/pharmacological treatment for rare brain tumors.

This is above my pay grade….

Somebody obviously bought the stock and there could be multiple suspects. There are bottom feeders in the market who buy into distressed companies because they know some of the assets are valuable. It doesn’t take much money to control a company in distress and a still listed company is more valuable. Sometimes these bottom feeders are insiders trying to hijack the company.

Another possibility is that the “market maker” used ANY market volume to readjust the price upward. They don’t want to lose the company at the exchange because the company pays a lot of fees to be listed, and that’s what generates their income. This could motivate some people.

Petunia,

It seemed as if 90% of their cap was traded immediately after the notification by NYSE…3.1M shares. I don’t understand the “market maker” model you describe.

It seems suggested that someone purchased the stock to control a company with multiple fraud lawsuits pending from seven or eight separate law firms…as well as a delisting threat from the NYSE, and the company with little value to loot.? What is the value of a shell corp. these days? I know this company began as a shell.

thelocalpragmatist, it has a lot of patents, has received licensing from companies on their particular patented testing methods, and it also has orphan drug status. Possible that one of the major Pharma players has manipulated it so that they end up with it, and like Petunia said – hits the ground running. Or possibly they shelve it because it hurts too much of their drug portfolio. Big Pharma is not in business to make friends or cure people.

thelocalpragmatist,

Looks like it was short covering that increase the volume and price.

Off the shelf listed shell companies can be worth a lot of money to someone who wants to hit the road running and it buys a history too.

the number of companies listed on the nyse probably has decreased ( can’t find any data ) . But the total number of shares outstanding is still high per this chart , look at the drop after dec 31,2015 and then subsequent rebound. Still plenty of supply .

https://ycharts.com/companies/TOT/shares_outstanding

Here’s an article on the subject. CNBC was discussing this maybe on Friday last.

https://www.bloomberg.com/view/articles/2015-06-24/where-have-all-the-publicly-traded-companies-gone-

petunia :wow , thanks . almost 50 % drop in delistings due to M &A activity. that ychart i posted maybe represents total number shares TRADED that day. here is a corrected post of historical number of shares outstanding via NYSE data base . still quite a supply. but this supply might represent derivative type shares also (i.e etf’s , etn, short etf’s , bond etfs). Issuance of these types of instruments /shares have burgeoned .

http://www.nyxdata.com/nysedata/asp/factbook/viewer_edition.asp?mode=table&key=3152&category=3

I too have many concerns over central bank induced malinvested capital. However, I think the issue on adjusted earnings has more to do with the base of earnings than the growth of earnings. If I adjusted earnings last year and now compare my adjusted earnings this year, growth is not enhanced, as the adjustments cancel out. However, due to adjustments, the earnings base is likely flattered making a stock look cheaper than it is in reality.

I’m beginning to think that the stock market isn’t an economic indicator but a wealth inequality indicator. Since the wealthy own the vast majority of stocks, the economy will only be deemed “bad” when stocks fall. That is when corporate media will ask the question “what is wrong with the US economy?” Until then everything is fine, why bother trying to understand it all.

Of course. The economy is always good for some and bad for others. Since the rich fund Congress and buy advertising in the media, how they fair is what counts.

That’s a great insight, Duane… sincerely.

I’ve been saying for years that the market has absolutely no relationship to the real economy. Yet, it’s reported as though it is.

In reality, you’re correct. It’s a wealth and/or wealth inequality indicator… disguised in the media as having some sort of relationship with people’s retirements. They need the latter in order to blackmail people into thinking we need high asset prices.

After the 29 stock crash, a huge amount of ink and spoken word, emanating largely from government and industry, tried to tell everyone the ‘real’ economy had little to do with the stock market.

The words ‘fundamentally sound’ became a mantra, best repeated several times a day.

For its part Wall Street dwelt on the bargain opportunities that the crash had created.

Because government reaction to the downturn is now universally believed to have made it worse ( the gov began cutting back, as left and right insisted on balanced budgets) we can’t take it as proof that the stock crash caused the 30’s Depression.

But nor can we entirely dismiss the theory that it was at least the big nudge that pushed an unstable system into the downturn.

Debt is keeping this all alive. But consider the many levels of debt that have piled up but ultimately rely on a shrinking workforce and maxed out consumers to repay it all. Consumer debt, mortgage debt, corporate debt, public debt (local, county, state and federal levels), unfunded public pensions at every level of government plus the rising payouts for Social Security/Medicare. The debt bubble burst will be pretty painful.

Wolf’s earnings analysis is accurate but does it matter? The government is buying bonds and stocks. They understand the social risk of a steep market decline and what will happen if many pension funds go bankrupt. It can’t be allowed to happen. They’ll convince people that a market PE of 26 is ok. They’ll keep rates low and the PE high until the Boomer cohort exits the system – 20 more years of ‘new normal’.

This is EXACTLY correct. The stock market was taken over after the 08/09 crash. It has been manipulated UP and will not be allowed to correct significantly. ONLY a true black swan event that scares EVERYONE into selling will sink the market. Otherwise, chill.

I’m not saying it’s right. But it is obvious to me that the stock market has strong behind the scenes players keeping it aloft.

Well if that happens we’ll have a few questions for the Fed, because they have raised rates, said they will raise more and have published the (modest) rate at which they will be selling, not buying, bonds as they unwind QE.

Re: pension funds. They would MUCH rather be in their traditional investments, bonds, including gov bonds. No segment of the financial world has suffered more from ZIRP than pension funds and lifecos.

At 72 living in the Bay Area all my friends have there wealth in the financial markets along with RE but none of them have the slightest worry about the market given its bounce back in the last 10 years nor does it bother them that RE prices were 50% less just 4 years ago. Its all about cruise and European vacations forever….

at a PE = 25, the Earnings Yield (1/PE) of the SnP 500 is still 4%. Much better than inflation or Treasury. This can continue until inflation rises.

High inflation would balance the P/E ratio.

What does a crash the other way up look like?

It just needs salaries to go up hard too.

Some subversive kind of helicopter money would be needed.

Suppose you have a coin that is %99 weighted heads.

And also suppose that you keep on increasing the size of your bets.

What will happen

“It will be ignored until it’s too late.”

Well, it will largely be ignored in any case. The Fed has shown that it can levitate the financial markets by cannibalizing the real economy. That will end when the real economy can no longer service the accumulated debt and there isn’t enough left to cannibalize.

The rich will still be rich. They just won’t be as rich. The general population can expect to be reduced to penury.

Japan can still service its debt, but it’s getting closer. The U.S. situation is worse, and the collapse of its economy and financial markets can only be a year or two away. In the meantime the discomfiture of the general population will continue to increase because its support is based on the shrinking real economy, and not investments.

Since there is no political will to reverse or arrest these trends, disaster is inevitable. If you think the problems the Fed creates are bad, just wait until you see their solutions. And if debt is their answer, they’re asking the wrong questions. The U.S. is already a couple of years past the point where more debt increase economic growth. Now it’s merely used to forestall collapse.

The US situation is no where near as bad as Japan, where debt is 250% of GDP. The new hawkishness of the FED is largely because it doesn’t want to go down that road.

Part of Japan’s demographic problem is that its post-war older generation ate a much healthier diet than the red meat, fat, and sugar laden diet of North America. They live a long time.

A second problem is that there is, in effect, a zero immigration policy.

(The omnipresent critics of US immigration will no doubt see this as an advantage)

Trivia: years ago a young American was one of the very rare permanent hires of a foreigner by BIG newspaper Asahi.

Not on contract, as a salary man.

He went to immigration to regularize his papers and they didn’t believe him. He reported back to the manager at this BIG paper who said: You leave this to me’

Next day immigration phones: ‘Would it be convenient for you to come at 2 PM?’

A third problem is that only half the population, the male half, is really utilized by the economy. The ruthless obsession with education is focused on males. My sister as foreign admissions officer at a Canadian university has seen many transcripts from young women with things like ‘needlework’ as a credit.

Balancing all this are many positives including a fixation on quality, aka ‘zero defects’. Millions of the result can be seen in North American driveways.

Did you know that the government in Japan made a huge reduction in the deductions available for estates?

Jacked up the amount of tax that all those old people will pay when they die.

http://www.nippon.com/en/currents/d00154/

Here in Oz we have no death duty or inheritance tax………..well so far, but I think that will change in the future.

Oh, and if you are an American married to a foreigner…………watch out as the government will really rake you over the coals if you leave money to one of those nasty foreigners!!!

“The US situation is no where near as bad as Japan, where debt is 250% of GDP.”

Not likely. Numbers can be misleading, and one must be careful about self-serving national propaganda.

Japan had no bankruptcies among listed companies last year. The Japanese have higher rates of personal savings, and medical bankruptcies are uncommon. Japan has far less income inequality than the US, and it hasn’t shredded its social safety nets.

Let’s see which one falls apart first, shall we?

‘Japan can still service its debt, but it’s getting closer. The U.S. situation is worse, and the collapse of its economy and financial markets…’

Check context. Of course Japan is not going to fall apart and I suspect the US will be here when we’re not. And of course Japan has fewer medical bankruptcies. The US is the only place specializing in those.

But in terms of servicing its government DEBT, your word,there is no comparison.

Wolf…the obvious question that springs to my mind is: “so, if this is how thing look using adjusted earnings, how does it look using more conservative GAAP earnings over the same timeframe?”

Thanks

Sam

This data is out there. When I get access to it, I’ll share it, guaranteed.

:-]

I read about “the Boomers” doing this and doing that and the consequent effect on the SE, but is that true? It was my impression that individuals are a tiny percentage of the total shareholders of a given company and that the stock movements are ruled by institutional investors nowadays. Wolf, am I correct?

If so, what you or I (excepting Buffet and his ilk) do is neither here nor there in the grand scheme of things. Titanic and shifting deckchairs springs to mind…

Welcome to the “New World Order”, where monied interests control the vertical and the horizontal in the interest of doing God’s work.

But they’re showing restraint, despite full employment and wage inflation.

Enjoy the fairy dust while it lasts, perhaps commodities demand is telling us something? See this:

https://wolfstreet.com/2017/07/09/is-this-a-contrarian-buy-signal-for-the-commodities-bust/

“Yet, over the same period, the S&P 500 Index itself soared 80%.”

How evenly distributed is this rise? Are there FANG stocks in the s&p 500?

Yes, the FAANG are in the S&P 500. There are also some big losers in the S&P 500, and a lot of huge winners.

This article prompted me to do some googling to see if I could get a similar perspective on European markets (I live in Europe). I found this, which may be of interest here.

http://www.starcapital.de/research/stockmarketvaluation

– I would concentrate on cash(-flow). That’s nearly impossible to manipulate.