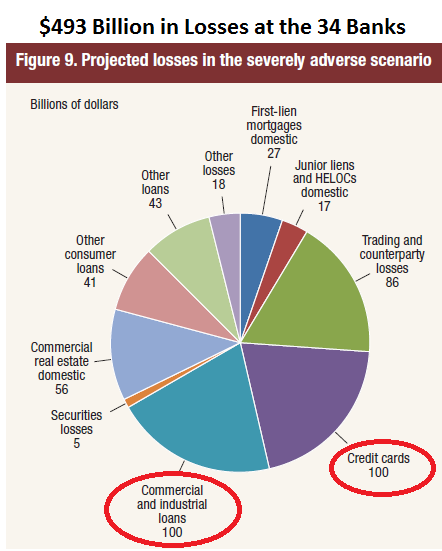

Projected losses at the top 34 banks in a “severely adverse scenario.”

The comforting news in the results from the Federal Reserve’s annual stress test is that the largest 34 bank holding companies would all survive a recession.

Based on this glorious accomplishment, the clamoring has already started for regulators to allow these banks to pay bigger dividends and to blow more money on share buybacks, and for these regulators to slash regulation on these banks and make their life easier and riskier in general. We don’t want these banks to survive a recession in too good a condition apparently.

And it would likely be better for Wall Street anyway if banks could lever up with risks so that a few of them would get bailed out during the next recession. Let’s remember, for the Fed’s no-holds-barred bailout-year 2009, Wall Street executives and employees were doused with record bonuses. The Fed’s bailouts were good for them. And it has been good for them ever since.

The less comforting news in the stress test is that credit card debt – generally the most expensive and risky debt for consumers – has now moved to the top of the Fed’s worry list in the “severely adverse scenario” of the stress test. The projected losses for the 34 largest banks – not counting the losses at the 4,997 smaller banks – are expected to hit $100 billion, up nearly 9% from the stress test a year ago.

The projected losses rose for several reasons, including that credit card balances have grown by 5.6% from a year ago to over $1 trillion. The delinquency rate has risen to 2.4%. The Fed is also blaming looser lending standards.

Sharing the top spot on the Fed’s worry list in the “severely adverse scenario” are Commercial & Industrial loans, whose balances are over twice as large, at $2.1 trillion, but whose projected losses are also pegged at $100 billion.

In total, the “severely adverse scenario” sees $493 billion in losses for these 34 banks:

Note that projected losses from all consumer categories – credit cards, first lien mortgages, junior liens and HELOCs, and other consumer loans – total $185 billion or 37% of total losses. Of all consumer loans, credit card losses are projected to account for 54%!

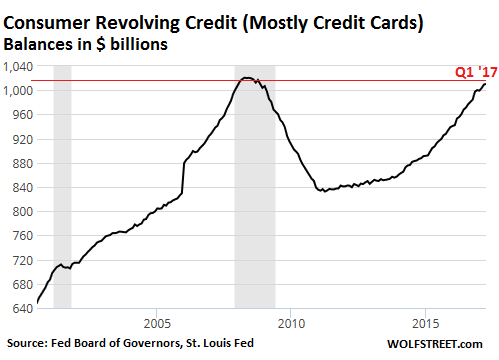

After soaring over the past two years at a rate between 5% and 6.8% year-over-year, credit card balances now exceed $1 trillion, which is about where they’d been in May 2008 just before they blew up during the Great Recession:

Credit card debt is the most expensive debt for consumers – and the most profitable for banks. The cost of funds for banks is still very low. But for credit cards, they lend out at 15% or 21% or even 25%. Even with relatively low balances, the interest and fee burden, once the consumer is falling behind in making payments, can quickly kick the consumer over the edge.

But then, as push comes to shove, the problem with credit card debt is that there is no collateral. When consumers default and seek bankruptcy protection, recovery by banks may be low, and loss ratios tend to be large. So these things are risky for banks.

Credit card delinquencies started ticking up a year ago and have reached 2.4% in Q1 2017. This is still low by historical standards, but these are the best of times, and the unemployment rate is low. Concern is that tapped out consumers, who are already struggling with this debt when the unemployment rate is low, will be pushed over the cliff when that severely adverse scenario kicks in with job losses. Then, credit card defaults and losses for banks will once again skyrocket.

For some banks, the risks are much higher because they issue credit cards to riskier customers. Some are already experiencing higher delinquency and net loss rates.

In the severely adverse scenario, CapitalOne came in with $21.7 billion in projected losses, up 20% from 2016. In real life, the company disclosed in its Q1 earnings report that it increased its provision for bad debts by 30% year-over-year to $1.9 billion, that the 30-day-plus delinquency rate rose to 2.9%, and that net charge-offs jumped 28% to $1.5 billion. Its rate of net charge-offs to total loans rose to 2.5%. Most of these delinquencies and losses occurred in its credit card and auto loan business. And these are the best of times!

JP Morgan Chase came in with $15.7 billion in projected losses, up 13% from last year, and Discover Financial with $8.7 billion in losses, up 14%.

So it’s comforting that our credit-card debt slaves, who had shown signs of unwelcome prudence after the Great Recession, are kicking that nasty habit and are once again splurging on things they can’t afford and are charging them on their credit cards to pay out of their nose for them. It’s good for GDP, which needs all the help it can get. And it’s good for the banks, which make a ton of money on credit card balances. And when push comes to shove, and the banks get hit, well then, let the Fed deal with it, no?

The Debt Slaves are beginning to buckle under their loads. Read… Great Debt Unwind: Bankruptcies by Consumers and Businesses Jump

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Debt truly is a disease.

And highly addictive.

It is a disease, isn’t it? It is a disease of spirit and values and even victimhood, sometimes.

On a lighter note of debt I know a 90 year old guy with a big car loan for his Ford Escape. His credit card is up to the max. He goes out for lunch with my 77 year old neighbour 2-3 times per week. When he was a young 88 he drove across Canada to see relatives; only made one wrong-turn mistake of 300 miles. :-) His goal is to conk out with the card maxed and a full belly and ‘fridge.

The progression with any addiction goes as follows ‘

1) You the individual make the initial volitional choice to engage in a potentially addictive behavior .

2) The longer you engage in the behavior the more difficult it becomes to extricate ones self from the behavior

3) With after a period of time depending on the addictive behavior and the personality involved the mind and /or body * becomes convinced it can no longer exist without the addictive behavior [ we are creatures of habit for the most part ]

4) With said addictive behavior then evolving into what may then and only then be considered a disease .

* Physiological and Psychological addiction are two very real independent addictions that many times do work in conjunction with one another

Yes but dobt forget about the degenerate enablers on every corner who say: you qualify, you aren’t that behind, your a great candidate, you have a good job, just sign here…..blah blah blah, these preying snakes are far more plentiful & willing that the seemingly helpful jerks who say we can help you get v those payments in control. … for this small fee.

People need to stop wanting and buying crap they don’t need which they have to borrow even to get. Simplicity is freedom- live simple!

As they say. the last check you write should be to the undertaker; and that check should bounce.

God bless him my feelings exactly.Best place to get a mortgage any company now giving mortgage’s that worked for countrywide best bunch of crooks i know they know all the tricks and can get ANYONE a loan.If anyone needs a list of companies let me know.

All to true .. but the genuine irony is ;

Much like the current opioid epidemic the folks responsible for helping to ‘ manufacture ‘ the ‘ disease ‘ are the very one’s now expressing concern and consternation [ or should that be constipation ? ] over that which they have helped create .

So whats next ? A war on debt ?

Ahh … genuine irony versus the current ‘ hipster ‘ version that passes for irony .

” the folks responsible for helping to ‘ manufacture ‘ the ‘ disease ‘ are the very one’s now expressing concern and consternation”

Exactly. The Fed through money/credit (debt) creation is the pusher of the “wealth effect”-the inflation of “assets”. In turn, borrowing becomes the only way to purchase assets as incomes are stagnant or none-existent.

The Fed’s pals get to front run asset inflation and the rest of the nation gets to try to keep up via the “poverty” effect.

The US debt is so big that’s unbelievable.

Wouldn’t it be funny if the Gov passed a law capping rates at 9 %.

Consumer credit would largely cease to exist, crashing the economy.

Quite the opposite. Prices would plunge at a rate much faster than they are currently expanding the pool of buyers.

All “money” in our system is created out of thin air when bankers issue loans. Banks charge interest for loaning people “money” that is actually just bank credit, which is created the moment the loan documents are signed. 95% of all “money” does not exist in any physical form; it exists only in the hard drives of the bank computers. The remaining 5% (paper notes and coins) are created by the US Dept. of Treasury. However, this “physical” money is sold directly to bankers for the cost of production. A $100 dollar bill costs less than twenty cents to the banker. The government requires us to use this evil money substitute under threat of imprisonment. “Legal Tender Laws” require all contracts to be settled in US Dollars. And of course they require it for paying taxes.

The money system is a legalized-counterfeiting, debt-enslavement scam. Debtors are not victims of disease; they are victims of deceptive parasites that rob decades of life and labor from each individual to pay interest. The same treacherous mechanism is used by the privately-owned, central banks (like the Federal Reserve) to keep our government buried in debt so that ruthless tax collection is required to shake down productive people.

Laughably false and totally bogus assertions. Banks NEVER create any money at all and NO BANK MAY EVER LOAN OUT MORE THAN 90% OF THE AMOUNT OF ITS CUSTOMER DEPOSITS IN THE US.

I would suggest you learn about the Federal Reserve at:

http://www.FederalReserve.gov

I would suggest you learn about the US Treasury at:

http://www.TreasuryDirect.gov

At least one can get away from credit card debt much easier than student loan debt. Nevertheless the Bankruptcy Abuse Prevention and Consumer Protection Act of 2005 makes much difficult for people to discharge their debt. Debt slaves or indentured servant, whatever you call it. When one is in debt, he is in bondage and bankruptcy laws always favor the creditors.

And whose fault is it for running up the debt, but for those profligate irresponsible individuals who do just that?

Favor the creditors?

Wolf: are you aware of the Illinois near-insolvency situation? What happens if they can’t pay da bills? Who is gonna bail them out? It sure as sh/t better not be me, John Q. Taxpayer.

I noted that my comment was a side note since it wasn’t relating to the article, but it removed that line—strange.

Yes, I’m aware of it. I might write about it Friday a week from now if S&P decides to downgrade it to junk on that day. It’s on my schedule :-]

It’s a huge mess. Chicago is a mess fiscally, too. Chicago’s school district even worse… I’ve already covered Chicago a few times. Illinois is next.

Good Morning Wolf,

With regard to Chicago, as a resident, and an institutional investment professional who has worked with ALL of the State, County and City of Chicago Pension funds, I am well versed in the problems they are facing. My question to you, and it is one I am seeing more reference to, is it AT ALL POSSIBLE, for the State, to file for bankruptcy protection? I have some basic familiarity with the legislative obstacles they face to do so, but is there a back door for them to do so? And if, big if, they were able to do so, would this be the opening for other States to do the same thing?

And, FYI, I find your observations and comments incredibly enlightening. You are well ahead of the curve with your commentary, and I am scared to say, I think your assessments about our domestic economic structure is spot on. I am personally scared to death.

States cannot currently file for bankruptcy protection – but there are many voices who say they should be able to in order to deal with the coming mess.

Congress cracked open the door, however, when it set up a court-supervised procedure for Puerto Rico to restructure its debts. My gut feeling is that this may be a model going forward, and that Congress might broaden it to give states a similar procedure.

If states are allowed to restructure their debts, state general obligation bonds are going to take a big hit… it changes the risk equation.

Oh, by the way, I just spent 30 min on Stocks & Jocks in Chicago (it also airs in other places). Great radio show. Drive-time in Chicago (7 AM), a little early for me on Pacific Time though :-)

I might post the interview this weekend.

States are sovereigns for which the federal government acts as their inferior agent. US territories, such as Peurto Rico, do fall under federal remit and bankruptcy laws. No comparison to states. Remember, the states gave themselves Article V in the Constitution which could be used to abolish the federal government which makes the states the sovereigns. The federal government has no such power over the states. Federal bankruptcy law does not, and cannot apply to states. States can, have in the past, and will in the future, default on their debts. Bankruptcy, no.

Read your copy of the Constitution. I can provide one if you don’t have it.

John, here’s a summary of what Congress and the Supreme Court would need to do to allow states to file for bankruptcy, via the Council of State Governments:

“To allow for state bankruptcy, Congress would need to amend the federal bankruptcy code to add state governments to the list of entities who may apply for bankruptcy. In addition, a state would need to amend its own state laws to authorize it to make application for federal bankruptcy.”

“Finally, the United States Supreme Court would need to rule on whether the contracts clause of Article I, Section 10 of the United States Constitution prohibits states from declaring bankruptcy even if authorized to do so by Congress, or imposes any restrictions on the terms, conditions or circumstances under which state governments might declare bankruptcy. If it chose to do so, Congress could require the Supreme Court to rule expeditiously on these questions.”

More detail here:

http://www.csg.org/pubs/capitolideas/enews/issue65_3.aspx

Thanks Wolf. Congress can dream all that they want about what they think they and the Supreme Court can do but that does not change the fact that any federal law that attempts to override the sovereignty of the states is null and void. States can default. They have no obligation to follow federal bankruptcy laws.

Council of State governments? You’ve got to be kidding me!

John,

bankruptcy law is not an “obligation.” It’s protection from creditors. It’s a court-controlled process that protects the entity from creditors’ seizing its assets. Argentina would have loved to file for bankruptcy protection. But there is no bankruptcy law for countries. Instead, it was hounded by hedge funds that tried to seize all kinds of property. And it eventually had to settle with them.

You’re correct. The Constitution doesn’t make it easy to offer functional bankruptcy law provisions for the states, and that’s why it hasn’t happened yet. And I’m not betting on it. But I think it would be a good idea for great minds to get together and figure out how to offer states some court protection to address their debts. I want creditors to pay, not federal taxpayers – that would be a nasty option.

Yes, Wolf. It might be a good potential amendment to propose at the Convention of States. Except that the standardized wording for all current calls for a Convention require the reigning in of power from the federal government in order to be a proposed amendment to the state legislatures for ratification. Allowing the federal government to oversee state bankruptcies would add power to the federal government and would be shelved. If you would like to see an example of how the Convention might work, go to ConventionofStates.com and watch the simulated Convention held in Williamsburg, VA. One of the proposals there was to give the President line item veto power but that was considered an addition of power and was shelved.

I believe that once the Convention is convened, the delegates must go thru a systematic process to determine steps forward:

1) Do the states still need the federal government as their agent? The answer will likely be yes, but if it is no one amendment could be proposed to abolish the three branches of federal government and all departments created under them.

2) Should the form of the branches be modified. For the Supreme Court, absolutely yes. Since the purpose of the Supreme Court is to protect the Constitutional rights of the states (their citizens), the justices should be selected by the states with some form of recall available. Term limits are a must. The President: perhaps an executive committee such as that in Switzerland. Congress: I leave that to the poor delegates to determine.

3) What changes should be made to the individual powers of the federal government. This is where bankruptcy might be considered if states really want to give up their sovereignty at states (pseudo-nations) to the federal government. So far, allowing the federal government to usurp powers has been a disaster. And, again it would go against the entire philosophy of calling a Convention to reign in the powers of D.C.

So, again, legally the states have the same status as Argentina as a nation and can default on their debts but not declare bankruptcy, regardless of actions by the federal government. And, they would pay the same price as Argentina has paid for its past defaults.

And, yes, if I sound like a strict Constitutionalist, I am. I even have some of those dreaded black rifles to be used in defending the Constitution should it get to that point. But, I prefer promoting the states use the Article V power that they already have to bring the feds under control (or in the nuclear option, eliminate them) peacefully.

That’s also the last day for road construction projects if Illinois doesn’t pass a budget.

If our country bails out the mess that is Illinois, I will be furious. I am in no way responsible for their lavish government spending—I don’t live in their state. Their local officials did this—not mine. They had a vote—I didn’t.

Their property tax went up $1100 per household this year. Average 100-year old house in a rural area pays $5500 tax bill—more than the mortgage! Did I mention this is ILLINOIS?! They’re already vacating the state in droves (#1 in population loss)—this is gonna be yuuuuge!

Assuming Congress creates a path toward restructuring debt for PR and debt ridden states, one hopes the burden will be shared. Pension plans need to take a haircut if federal tax payers are ponying up.

Restructuring debt in bankruptcy court “normally” doesn’t involve the taxpayer (though there were exceptions). It’s when equity holders (if any) are forced to give up their equity, and when creditors lose part or all of their investments. In Muni bankruptcies, there are no equity holders. So who gives up what becomes very complex – but it shouldn’t involve the federal taxpayer, imho.

However, there should be plenty of state and local taxpayers that voted for and benefited over the years from this borrowing binge that has turned into a mess…

Hi Wolf,

Thank you for the explanation. It sounds like it will be interesting given all the pension funds “chasing yield” via junk bonds supporting similarly underfunded pension funds.

THANK YOU, WOLF! MAY THE WHOLE COUNTRY READ YOUR COMMENT!

Why would I share in their burden when they weren’t willing to share in my burden living debt-free (doing without) in a fiscally conservative state having a balanced budget? Why would I collectively share in their burden when I’m not a part of their state? STATES’ RIGHTS??? DIDN’T WE GO THROUGH THIS ONCE BEFORE?????????????????

No, the Civil War was about slavery. Back thirty years before that, Andrew Jackson’s era, the issue of “state’s rights” was in play.

What started out as thirteen independent “states” realized they could not survive against European powers as independent little governments. They had to face reality, and give up some “rights” in order to survive. The realities of 1788 and the defeat of the British, was replaced by the Napoleonic Era and a different world.

Coaster Noster — get real. It was a fiscal war. A War of Northern Aggression. States’ Rights. Same sh/t California is trying to do right now with their banning of employees spending state money in certain conservative states.

How can you not bail out Illinois after the FED, in 2009, bailed out 100s of banks, Goldman Sachs, Bank of America, AIG , GM, Chrysler, the big home builders (Toll, LEN,), and etc. They also bailed out some big foreign banks too.

Maybe those ‘in power’ in Illinois were counting on the witch to win the White House and with the zero’s buddy as the Mayor of Chicago everything would have been set up to to do a sneaky play and bail out Chicago first and then the State of Illinois next…………..

Who cares about laws and the Constitution when you are the ‘elite’?

Why in the world do people buy bonds from cities like Chicago, states like Illinois, and countries like Argentina and Venezuela?

IMO it is a dumb investment and they should lose everything once those places go belly up. Others should not have to pay for all the crap going on there that led to the mess in the first place.

The general obligation bondholders will simply have to take the losses on their bonds, and then Illinois will be cut off from any further borrowing, and they’ll have to negotiate their $15 billion in arrears with their creditors who will also likely totally cut them off from getting any further services without payment up front. That should help put a damper on the reckless, irresponsible, and profligate spending in Illinois.

Personally, I support any debtors to the major banks of this nation to tell said banks to go F themselves. And I’m pretty much debt-free myself. I don’t want the irresponsible to gain, don’t get me wrong. Put in some kind of boon to those who live within their means.

I wish we’d have a national labor strike and unanimous action to simply stop paying debts. Crash this whole monster monopolistic / oligarchic monster away..

Sounds like a good business.

Credit card Balances: 1000 Tr

interest Revenue @ 18%: 0,180 TR

Bad debt: 0.100 Tr

Profit: 80 billion

When your cost of good sold it practically zero, it is still a great business.

whoops to many zeros! 1 Tr not 1000!

Debt is also an instrument of control. Always keeping the debtor in a permanent state of indebtedness is the ultimate goal. Extend and pretend. Extend the payback period and pretend that all debts will be paid.

Has Very true Stay away from the intoxicating drug called debt and your life will be so much easier and better in the long run That’s what I’ve done

Indentured servitude to the bankers. New Massa same as the old Massa.

At the moment with the banks (especially US one’s) there’s a sense of we’re all okay.

It feels like pre 2008 all over again.

Whilst I like Donald Trump from a pro business point of view and what’s he trying to do on that, deregulation of banking rules which were put there for a reason makes me feel uneasy.

At some point there will be another correction on auto loans, credit card debt whatever it is and the banks should have the liquid assets in place to cover that, not relying on Joe Public again.

Maybe Illinois can get some Trumper advice on bankruptcy procedures and strategies. :-) Watch, when it happens he’ll castigate and mock, but really…the whole darn Country is in debt to its eyeballs.!!! Can Illinois have a debt ceiling, too?

Talk about the pot calling the kettle black.

Debt is the accepted normal. (Not in my house, though).

“Mom, these new runners are only $150.00. Everybody has ’em”…(Reply) “Oh, okay, you’ve been a good boy”, and pulls out the plastic.

“These new F-35s are down to 95 million per, now. What a deal! Come on Congress, pass the debt ceiling extension, already. ”

“No health care for you, we can’t afford it. Get rid of medicaid, we can’t afford it. No….”

The heyday of America was in the ’50’s and ’60’s. They didn’t have a lot of business regulations then with the exception of banks. Basic things like inter-state banking was not allowed, and usury laws were strictly enforced. Not to mention federal laws like Glass-Steagal. There are reasons for this. Deregulating banks is NOT being pro-business. Just the opposite in fact.

Great Post!

Kent,

There was also a big government that gave out tons of free college educations… and taxes the wealthiest at a 90% top marginal tax rate. There was major investment in infrastructure.

There’s a Norwegian bank, Komplett, that has a quite interesting business idea:

They offer blanco loans without any security and yearly interest rates towards 20% plus additional expenses and the victim doesn’t have to payback the loan as long as the victim pays the interest and expenses.

When the victim turns 65, then he/she has to start paying back the loan itself. Nice, considering that if your economy was crappy when being working, then in what shape is it when you are about to retire ??

I bet this thought is from the old school…..that by retiring age, most should have cars/home/education taken care of –wrong in today’s economy.

Especially with that awful disease going around…’house lust’.

Thanks Realist for your message.

Even though this Norwegian idea is different, I can sort of see this idea happening more and more in the banking sector.

If the wigs that run those banks only had their salaries and bonuses depend on the bank making a profit, things might be done differently.

They do. It’s just that it is not clawed-back when the bank fails. So they don’t care if the bank fails, they get fired and walk away with millions in their pocket. There is no downside for failure, and massive reward for the actions that eventually lead to failure.

It’s an issue of corporate governance which the government wants to leave to the Free Market

Oh, like Marissa Mayer at Yahoo? Fail miserably and walk away with hundreds of millions. As you said, “no downside for failure.”

Wolf, how is the credit card “debt” of those of us who pay off our entire balances each billing cycle treated by the Fed?

Does anyone know the relative magnitude of this C.C. “debt”?

If you pay off your entire balance every month, it doesn’t enter into the “installment loan” numbers since you’re not paying interest. So these charges that are promptly paid off are not part of the $1 trillion. A lot of people are doing that. I don’t know if anyone is tracking these amounts. From the Fed’s point of view, these amounts that are paid in full every month are not a risk to the banks. So it just ignores them.

Visa and MC are publishing their respective numbers on credit card spending. These amounts are flows of money, not balances. And so they don’t answer your questions either. It might be possible to back into it and figure out how much of total credit card spending never becomes an interest-bearing debt. But I don’t have that answer.

thanks, Wolf.

Wolf

Vert recent changes at the 3 major credit bureaus may soon make these numbers easily available.

Bureaus have recently separated credit card users into “transactors” (pay in full each month -1/3rd of total card accounts); “revolvers” (carry a balance- 40%), and “inactive (no balance & unused – 1/3rd).

The changes are very recent and will soon begin to trickle into credit scores. Because risk profiles are materially different, “transactors” will see increases, “revolvers” will not.

Thanks!

so the “revolvers” are carrying the float for us “transactors”. Thank you revolvers’ ! /sarc . I am surprised at the percentages.

Wolf,

My understanding is that the banks report the statement balances. And as Chip Javert mentions, this will hopefully change soon. I get annoyed with the fact that I look like I keep more revolving credit card debt than I actually do… given the fact that I pay the bill in full every month. And also, I believe that people who live this way should be deemed highly credit-worthy as opposed to, “He has no debt! Give him a bad credit score! We need people to have debt to prove they’re worthy of it!!!”

I would be surprised if there’s data that factors in and distinguishes those who pay-in-full.

This is exactly the change that is coming.

Previously (all things being equal), person X, having a credit limit of $10,000 and a never paying off monthly balance of $2,000 would have exactly the same credit score as person Y, having a credit limit of $10,000 and charging & paying in full a balance of $2,000 per month.

Wolf – what are your thoughts on loss severity for P2P /unsecured consumer credit? Originations were >$20B in 2016, so proverbial ‘drop in the bucket’ relative to $1T credit card debt. But P2P loans have built up cachet amongst yield starved investors seeking “alternatives.” I know many persons myself who have had modest success with P2P but not sure if it’s Auction Rate Securities 2.0 or whatever analog product leading up to 2008-9 financial crisis. Cheers.

They’re riskier than credit cards. So you should make a big-fat yield to compensate you for the risk. If you are, and if you can handle the risk, go with it.

My credit is still not repaired from my foreclosure and I regularly get offers for personal loans. One offer was a sign here and we will send you a check for 35K at over ~30%. I don’t remember exact rate, but I could never afford that, not even when I worked on Wall St. These are local lenders. It’s crazy.

I have some department store cards that were never cancelled when my credit got really bad and I don’t use them because the rates are ~30%.

“I have some department store cards that were never cancelled when my credit got really bad and I don’t use them because the rates are ~30%.”

These predators would encourage people who have a spotty credit history to keep their cards, but Chase wanted to charge hundreds of Amazon Chase cards (including mine) a fee ‘cos we were paying on time at the end of each billing cycle. When I called to cancel, they didn’t push back at all.

They don’t want customers who pay back on time. They are not here to provide a service, but to prey on people.

For what ever reason, my experience has been different.

I too have a Chase AMZN Visa card, and auto-pay the full balance each month (for the past few years). Have not had an attempt to charge me extra for paying in full.

I only use my Amazon card for purchases on their site. I use another for all restaurants and another for travel. Based on rebates you can generally save 3% or more. Just never carry a balance!

Here in Oz the big banks co-issued branded American Express cards that had a frequent flyer miles as rewards.

They used to offer 2.5 miles per each dollar spent, then it went down to 2, and finally the last adjustment was down to to .75 miles.

Used in junction with the grocery stores frequent flyer miles programs you could really rack up some serious points. Put everything on the card, pay it off every month, and get lots of ‘free’ flights.

Alas, many of the big banks are cancelling the Amex cards (including the black cards) as they don’t want to give away the miles anymore.

It is going to be much harder to accumulate miles now.

The banks get their first skim when you buy something with your credit card- from 1/2% to 5% of the selling price.

Even if you pay off your balances, the banks are still make obscene money.

“It’s good for GDP, which needs all the help it can get.”

When I go to any store almost everything is made in China. As GDP only covers products made in the USA, how does spending on Chinese goods stimulate US GDP??

-and I’m not talk about products partially made in the USA.

In the most boiled-down version: The amount you spend adds to “consumption expenditures.” But the amount that the importer pays for it to get it from China is part of “imports” which are subtracted from GDP. The difference between the imported cost and the price you paid is the net amount added to GDP.

Of course it goes without saying, the remainder of this division (presented in the form of imaginary numbers) excludes the government offshoring subsidies.

huh?

Almost all info describes the 08 crash and aftermath, as being something in the past tense. As something that came and then was over. Maybe for the 1% of major wealth holders, however the 90% of Main street not so much.

So, this is the first recovery that has been worse than the recession!

One hundred grand used to be a lot of money. To be a millionaire meant something. Government debt in the hundreds of millions was a deep concern. Then it seems overnight, millions became billions, and just as soon as this was acceptable, billions became trillions. Quadrillions?

To be in debt used to have a very negative social connotation. It was where one did not want to be. This has now been turned on its head. Acclimating the public to debt acceptance, and higher numbers of debt has been very successful. That which a short time ago was considered aberrant, is now seen to be normal.

But, those of us who refuse to behave “new normally” will be OK when the “new normal” fails.

Fail it will.

Not a question of if, but of when. It will be spectacularly ruinous for the debt slaves and for those rent seekers, that depend on their “investments” from those “assets”.

Debt as an asset is another “new normal” perversion.

Maxed out auto loans. Maxed out credit cards. Extremely high housing prices all while incomes for most of these people remained relatively flat.. Just makes me wonder if the mentality is that people feel they have nothing so nothing to lose.. Where as people like me have money and just don’t spend more than my income.. Many months we spend less and still save the difference.

I was in my local bank this week putting some money in and the teller and I were chatting. I told her I was a squirrel. She said that at one time she was over her head in debts and as she got out of debt and started a little savings account that saving also became an addiction with her and her husband and now they love to watch their savings grow.

The country is divided in so many things. It seems that we are divided in this also.. There are the conservative savers and the addicted spenders. I wonder if there are many who live in the middle, neither saving nor spending more than they make?

Personally I think savers are stupid

It is time to leverage yourself to the hilt..

Take as much debt as possible and enjoy life..

America punishes savers

I am thinking about cashing out cc and not paying them

Troll ! *chuckle*

Jon the problem with your suggestion is that those of us that are responsible would be miserable and would NOT enjoy life by acting irresponsibly like you advise That’s why we’re not called snowflakes That’s your department bud

There’s someone down the street who owns a house that is valued about the same as mine. This person got a 0% down mortgage in 2005 with the closing costs rolled in and stopped making payments.

Then the housing market crashed and they renegotiated the mortgage with BoA 2% below the original rate and went on to live in that house until 2011 for next to nothing. Now they have moved close by and rented out this place to another family. Their credit was shot, but they seemed to be doing fine.

We’re the suckers, I guess.

History says a default would kill your short-term credit rating, but they will be lending to you again in another 5 years. The greedy bankers can’t stay away.

It is so good to see common sense prevail once again.

56% of American adults have less than $10,000 in savings.

http://time.com/money/4258451/retirement-savings-survey/

It’s not that they are all spendthrifts. 40% have nothing leftover at the end of the month to save. This just boggles my mind.

I come from India – not a wealthy country by any means – where the household savings is 31% of GDP (down from 37% of GDP from a decade ago, but still good).

I am not a troll and I come from India as well.

I am a long time poster here..

Living in States for last 20 years…

I think savers are stupid here.. and they are punished..

Poor country you guy.s have more gold then russia and china.

Even though i am fiscally ultra conservative, I tend to agree that savers are now stupid.

Hindsight being 20/20 if I could go back to 2010 I would have multiple properties at 5% down rather than hoarding cash.

Even the stock market has been rigged with PE ratios of the high flyers to be super high.

Maybe the savers will inherit the kingdom of heaven for they are meek?

I’m the same economicminor as the bank teller.

Since 2008 I’ve just paid off on any debts like loans-credit cards. Just gone back to good old fashioned cash, try to save a bit each month.

There must be a lot of people out there who’ve realised they’re happier having no debt and paid off like myself.

Not at all buy buy buy.

Your capacity and tenacity to live without debt will be rewarded as this financialization of the Western world collapses.

You can rob from the future- it looks like for decades- but eventually the future is broke too.

“The comforting news in the results from the Federal Reserve’s annual stress test is that the largest 34 bank holding companies would all survive a recession.”

In summary: These 34 are the host, we are the bacteria.

As an old retired CFO, it has always amazed me how much credit is granted to people. Credit agencies & their scores are primitive and only slowly evolve (example: recent differentiation between credit card transactors and revolvers). Only in the past few years have new lines of credit needed to take into account the total of existing lines of credit (I think that was a Federally imposed requirement) .

Unsophisticated credit users (50% of the population?) who are given credit probably think some complex analytical process was used to determine how much credit was “safe” for them. Just like home mortgages are supposed to be calculated, I’d support only granting a certain portion of income as total credit (unless other assets, trust fund, etc, are available). Lenders and the population in general would riot in the streets before accepting anything like that.

I suspect you are familiar with this phrase, wrote in the runup to the 1997-1998 Asian Crisis “Banks borrow abroad and lend at home with complete abandon”.

I’ve seen it happen both in Spain and Italy between 2000 and 2008 and I’ve seen it start again in 2014. Banks are lending with near complete abandon again, especially to the two sectors which caused Spanish banks to require a massive bailout and which will most likely break Italy’s budget for years to come: construction and real estate. Yes, those making up over 60% of Italy’s ever growing NPL mountain.

I keep on wondering at the bank officials who merely rubberstamp some harebrained speculative scheme instead of saying “Let’s first look at vacancy rates in that area and then if people there can actually afford to buy these houses”. Or those extending credit to municipalities which would have already been taken to bankruptcy court if they were privately-owned firms. Or those not wondering “Four supermarkets for 2000 people? Which one is going bankrupt first?”.

If I were doing business like that I would have gone to almshouse long ago.

Wondering if someone out there has advise for someone that lost his income, has 20 grand in 0% APR credit card debt, with no other debts.

Other than shares in an llc that owns his home and a couple acres he has virtually nothing to his name. Has little qualms about loosing his credit score ie. is ready to be done spinning the hamster wheel.

Should he just forget about paying once they come due? Talk with a lawyer or with a debt negotiating outfit?

Transfer to another 0% offer or two when they come due. 20k is nothing.

Use it quick before they catch on. And never never never pay it back.

farmboy

You are in great shape. You just don’t know it.

I have been through this on three accounts totaling $35K, eliminated two through court or FTC action, settled 3rd for 20%. They have to wait six months before taking action after default. Since amount is $20K they will most likely retain the loan rather than sell it and use collection agency “on assignment” to collect. Since they are retaining ownership, they will have the necessary proof to prevail in court. (Loans under $10K are usually sold and evidence in court is robosigned and easy to beat, although I have seen a loan of $36K sold also.) If they win a court judgment they will put a lien on your house, which will be at state assigned simple interest of about 10%. The lien will be paid off when house is sold. If you can live with that default might be the best option. If they do sell the loan, a competent lawyer could beat them.

An economic calamity

and debt collapse, give a opportunity to “retire” opponents.

The other side constantly attack your goal line, force you to commit

stupid mistakes.

They smell victory. The tramp is set to commit another felony.

They salivate, because very soon you will get a red card, be evicted from the game.

They know it’s a surefire. Soon, it’s just a matter of time !!!

You can see it on their face : they are laughing, they enjoy themselves. becoming complacent.

But soon, they will be subjected to quick counter attacks.

The first score against them, still will not diminish hope and a chance.

They will press harder, in a desperate way. There is still hope.

They commit to the attack, exposing themselves to another

counter attack.

The strong hand, the better knowledge side, will survive.

That’s what too much credit cards debt is doing

Are you perchance a descendant of Johann Jakob Engel?

Call them up, tell them you need to work out a payment plan that’s viable in your current situation. if they don’t cooperate, default and never pick up the phone because it will be a debt collector. I wouldn’t feel bad about it. They offered you the credit cards and expect a high default level as people lose jobs, get divorced, etc.

No need to worry about the phone block out # or get a new phone #.You guys are getting me all excited again this feels like 1988 again let the good charge times roll. We did before and we can do it again.

Since 2014 I get a credit card offer in the mail every month. At least 6 times a year I get sent an actual credit card ready to activate. I’m not surprised by this. They are handing out cc like candy.

Use them all let none go to waste.

I wish it happens but reality is it’d never happen

Pedophile satanists oppression? Wolf, maybe it’s time to pull the plug on this day’s comments section.

The DNC showed their true colors, we endured 8 horrible years of bailing out TBTF at taxpayer expense and opportunity costs. So much for change, fool me once.

As payment, now we’re dismissing the never-ending barrage of anonymous sources inside the CIA who leak to the Washington Post. et-all

They blew it, DNC needs to get a clue.

Trouble with pulling the plug is decent folks are shut silenced along with the miscreant.

t would be best if Wolf could just delete offensive posts, I think.

Meanwhile, the rest of us can object to such hateful ad hominem stuff here – put a little pressure on the haters, anyway.

Wolf,

I have to dispute your notion that credit card purchases are “good for gdp”.

1) Credit card transactions are more unnecessary overhead for society. Don’t forget that the bank makes money from interchange, merchant processing fees. There’s profit on all transactions. Why do you think we have so many gift cards out there?

2) This means that merchants have to charge more than they would if consumers weren’t operating through debt instruments all the time.

3) Some people might say, “Yeah, but I get points!” No, you don’t. Prices would be lower without all the merchant fees. In effect, you’re paying yourself the points. If anything, it’s people who are paying without a good rewards card that are going negative more than anyone with them is going positive.

Personally, I would like all of these insolvent bank institutions around the word to go belly up and disappear forever. I want the stress test to show what failures they are.

I want the state to provide money creation, not the banks, (cough), the Fed. Same thing.

That was sarcasm. Credit card borrowing actually does add to GDP, but it’s a terrible way of adding to GDP.

It takes 7-10 years for the newly arrived adults to due the same as previous adults. Bankers know this. Its a racket.

The 2008 peak in CC debt was in large part done on healthcare spending, (BOC, Before Obamacare). Should Congress repeal, or impair guaranteed coverage (but not limit costs) we face the second shoe to drop. Too bad, a CC with robust limits will barely cover a broken leg. If anything limits have lagged consumer prices in all categories, and if banks are worried about consumer debt limits will continue to fall, and that in simple terms equals a tightening in credit, which is not something the Fed wants to see.