Fed lays out plan to unwind QE by $600 billion a year. Markets shrug. But “Painful sell-offs eventually materialize…”

Yellen sounded “surprisingly hawkish,” the experts said after the news conference today. She saw a strong labor market and downplayed slightly softer inflation as temporary. The Fed forecast economic growth at the same miserably slow rate we’ve seen for years, with the median projections of 2.2% growth in 2017, 2.1% in 2018, 1.9% in 2019, and 1.8% in the “longer run.”

So the FOMC voted eight-to-one to hike by a quarter point the target for the federal funds rate to a range between 1.0% and 1.25%. It maintained its forecast of one more hike this year. And it laid out its plan on how to unwind QE.

The Fed is no longer speculating whether or not to start unloading its $4.5-trillion balance sheet. It has a specific plan. The nuts and bolts are in place. It was agreed to by “all participants,” it said in the Addendum. And it’s going to start “this year.”

QE and the zero-interest-rate policy have driven asset prices into a frenzy, and the asset bubbles have become legendary. Now it is being reversed.

The Fed will “gradually reduce” its balance sheet by letting maturing securities roll off without replacement. For example, when the US Treasury pays off a maturing bond that the Fed holds, the Fed will take the money but not reinvest it. Just like it created the money to buy the bond, the Fed will destroy the money by not reinvesting it. This money just disappears.

The Fed specified the pace at which this money will disappear.

It will shed $6 billion of Treasury securities the first month – which could start as soon as September. It will increase the monthly rate by $6 billion every three months. After 12 months, it will unload $30 billion a month in Treasury securities.

Same principle with mortgage-backed securities, starting at $4 billion a month to be increased every three month by $4 billion until it reaches $20 billion per month.

Combined, the Fed plans to unload $10 billion the first month and raise that to $50 billion in 12 months. Then it will continue at that pace. That’s the plan. It didn’t say how far it will go with this “balance sheet normalization.” $50 billion a month or $600 billion a year will disappear. It’s the reverse of QE, with reverse effects.

How have markets taken this?

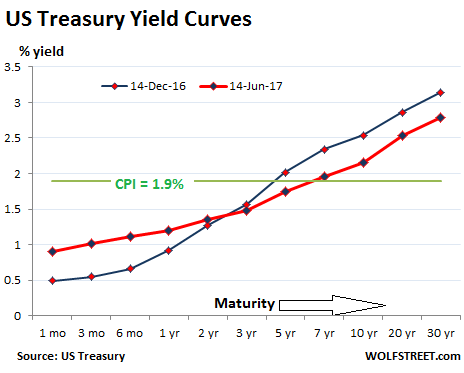

The Treasury market has responded at the short end of the yield spectrum. The 3-month yield, at 1.01%, has edged into the federal funds target range.

But longer-dated Treasuries have taken to opposite direction. Long-term yields have been falling, and thus bond prices have been rallying. The 30-year yield dropped 8 basis points today to 2.79%, and the 10-year yield dropped 6 basis points to 2.15%.

This has flattened the yield curve. The chart below shows the yield curve for today’s yields (red line) across the maturities and the yield curve on December 14 (blue line), when the Fed got serious about rate hikes. Note how the red line has flattened compared to the blue line:

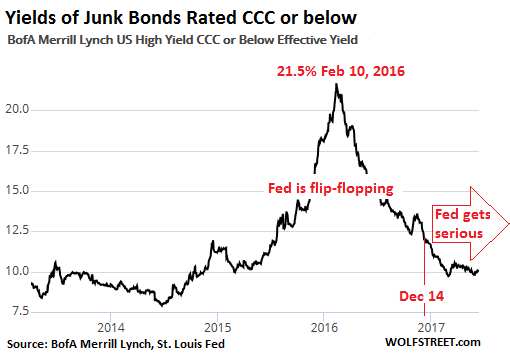

Yields of junk bonds at the riskiest end (rated CCC or below) surged in the second half of 2015 and in early 2016, peaking above 20% on average, in part due to the collapse of energy junk bonds. Riskier companies were practically locked out of the credit markets and couldn’t borrow money anymore. During this period, the Fed engaged in phenomenal flip-flopping: talking about rate hikes and then backtracking. This was carried out by the endless cacophonous appearances of Fed heads, disagreeing with each other until they became the laughing stock of the financial markets.

But late last year, everything changed. The flip-flopping stopped. The Fed went on a mission. It has been one rate hike every other FOMC meeting since. And QE is going to get unwound.

Yet stocks have surged since December and the average yield of junk bonds rated CCC or below fell from 12% on rate-hike-day in December to 10% currently:

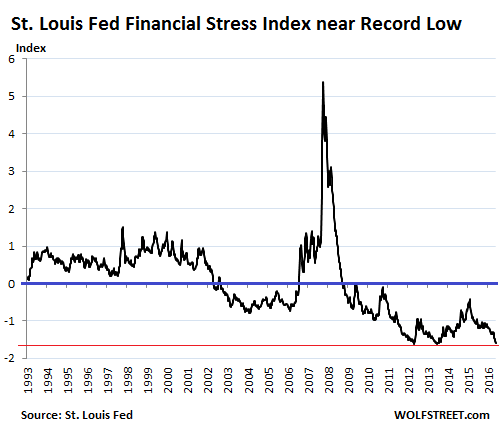

This is a sign that markets are loosening “financial conditions” rather than tightening them. The St. Louis Fed’s index that tracks these financial conditions, the “Financial Stress Index,” has dropped to near record lows.

In this chart of the Financial Stress Index, the blue line (=zero) represents “normal financial market conditions.” Values below zero indicate below-average financial market stress. Financial conditions have almost never been easier despite the current series of rate hikes:

And the stock market is hovering near all-time highs. So markets – except the short-term corner of the bond market – have blown off the Fed. But…

“There is absolutely nothing unusual about financial market conditions easing amid Fed rate hikes,” wrote John Lonski, Chief Economist at Moody’s Capital Markets Research. This is what happened the last two times.

The Fed started raising the federal funds rate in June 1999, taking it from 4.75% to 6.5% by May 2000. From June 1999 through March 2000, stocks surged; it had taken about 9 months before financial markets began to react.

When they did, they reacted with a “financial event,” the dotcom crash. From March 2000 through October 2002, the market value of US stocks plunged by a cumulative 43%.

Similar scenario when the Fed started hiking rates in January 2004, taking the federal funds rate from 1% to 5.25% by July 2006. Throughout that period of tightening, the stock market surged and the housing market became a mega-bubble. This scenario ended with another financial event: the Financial Crisis.

Corporate borrowing too can balloon when the Fed raises rates. This is the case right now, and it was the case during the past two episodes. Companies across the bond rating spectrum go out and borrow in record amounts to take advantage of the low interest rates while they still last. (And home buyers do the same thing).

“In summary, markets often prosper during episodes of Fed tightening,” writes Moody’s Lonski. “However, painful sell-offs eventually materialize….”

The Fed has set its sights on the asset bubbles that can, when they blow up, take down the lenders or worse. It is trying to engineer some kind of soft landing, by deflating them gently. And it will continue with a dual policy of unwinding QE and raising rates until markets react sufficiently. But as the last two financial events have shown, this can get very messy and may turn into anything but a soft landing for asset prices.

So is the Fed still bound to economic data? The data has been weak for years. But the Fed has started on its mission. Read… What Would Yellen Do, with these Retail Sales?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Reduce the balance sheet? pfffffffftttttttt No way.

I decided to comment right away instead of at the end because I wanted to predict that in the comments would be ‘tightening deniers’.

And sure enough the first one is!

I resemble that. With the yield curve inching closer every day to inverting, as China’s already has, you think momma Yellen will sell off the balance sheet into that? And all the other data that stinks?

She’d unwind the balance sheet to bring up long-term yields, which would steepen the yield curve. So if they stop raising after the next hike and start massively unloading the balance sheet, you’d have 10-year yields in 3%-4% range and the short-term yields in the 1.5% range, which would make a much steeper curve.

Given how the Fed has been pushing balance sheet “normalization,” that’s what they might have in mind.

“It was agreed to by “all participants,” it said in the Addendum.”

Including Neel Cash-and-Carry? Ok, then.

Neel Kashkari voted against interest rate increase. Apparently he voted FOR the reverse QE.

Anyone hazard a guess as to why crude crashed today? The 0.25% rise should have been priced in via the currency markets.

No one seems to be commenting on this.

OPEC hasn’t really cut production or exports. USA production is still increasing. Gasoline inventories are high.

Huge inventories are still sitting around the world.

Japan is restarting its reactors and China has cut back its demand for diesel. Also huge imports into China for seasonal/inventory buildup will not be repeated in the next few months.

So I guess we’ll see gasoline prices here in Oz continue to be higher than they should be by some 30 cents a litre.

Finally watch the spread between WTI and Brent. A big difference will mean US exports more oil.

And now just out despite falling world energy prices:

“EnergyAustralia has hit NSW and South Australian customers with price increases of up to $1000 for power and gas.

The company’s average small business customer in NSW will pay an extra 19.9 per cent – $915 a year – for electricity and an extra 10.7 per cent – $1042 over a year – for gas from 1 July. Residential customers are also being hit with price rises of nearly 20 per cent for electricity – an extra $320 a year- and 6.6 per cent for gas, an extra $49.40 a year.

SA customers are also paying an extra 19.9 per cent for power, which adds $390 to the average residential bill and $967 to the average small business bill. Gas is up 13.3 per cent for small business – an extra $936 a year – for small business. Queensland small business will pay an extra 13.3 per cent – $559 – for power.”

More money out of pocket.

Can hardly wait to see what happens in Victoria – looks like the wood fireplace will be going in sooner than we thought.

Too bad that a decent built in would cost around A$10,000……………….

Lee,

I’m pretty sure you can cut that installation bill in half without too much effort. Australia produces some excellent stoves, including the Bakers Choice wood cook stove with a glass door. I looked at purchasing one for our Canadian home, but instead bought one from here at a modest savings. Insulated stainless chimneys are excellent and a fraction of the price of masonry. Plus, they draw much better thus are more efficient.

Obviously, here on the BC west coast we have very easy access to wood supplies. However, in southern locales close to major centres wood is very expensive. (I get my wood virtually free if I cut on our woodlot, but it is easier to cut logging cull). I understand you folks have gumwood, etc.

Burning stove oil, NG, or fossil fueled produced electricty for heat is just like tossing cash into the fire place. Good luck with your heating, etc. (I have installed 2′ of insulation in our attic, R20 walls, and new windows….+ LED lighting, etc. ) 61 and been using wood heat for 40 years. Passsive solar and watching the bills represent the new reality of getting by.

regards

“Markets” have been wrong before. No, really, I seen it myself. The “smartest guys in the world” leaping off the plane without a parachute. Jumping to conclusions, as it were.

Now if I could just set this up right, I could cash in. Let’s see, where’s the gravy? Oh, there it is.

The Fed is only doing this to try to get ahead of the meltdown, you know.

reduce their balance sheet in fed speak aka we’re gonna print 4.6 tril and hand it to straw buyer and they’re gonna buy the worthless paper,been goin on for 9 years,why stop now

Looks like the Fed is actually getting something right this time. Take your profits now and buy gold folks.

The coming financial collapse is going to disabuse even the most slack-jawed dullard of any notion that the Keynesian fraudsters at the Fed were responsible central bankers or knew what they were doing.

Gershon — you mean Friedman, not Keynes. Pro-cyclic Fed policy is the antithesis of counter-cyclic Keynesianism, just as you are the antithesis of logic. Are you this wrong in the rest of your life? Good god, man, are you even able to operate a toaster?

two beers – alcohol makes you stupid and cranky. Go back to your safe space and sleep the sleep of the angry snowflakes. We will all have the last laugh as you will still have to pay back the school loans from your fast food paycheck. Perhaps your living standard will be higher if you go to jail after you graduate.

Gershon,

While I deplore two beers insults, he is correct. Keynes had little use for central bank monetary policy. He was all about fiscal policy which, other than Obama’s one-time $700 billion stimulus, was rejected by the federal government for the rest of the downturn.

Milton Friedman is the father of the current Federal Reserve’s thinking and actions. Friedman was a Libertarian who didn’t want Americans looking to the government for help during economic crises. So he came up with the idea of using interest rates to manage the economy. This would give the great unwashed a belief that our benevolent bankers were behind prosperity while the government was the cause of all problems.

Kent, Gershon:

I somewhat disagree with both of you. I think the Fed devises theory to support actions they decide upon. If one already exists, they will say it applied or applied somewhat or will let you make assumptions about their reasoning. By ‘theory’, I mean the gobbledygook used to justify their actions.

Look, if the universe can be modeled by using 1 and 0, then Fed theory should be able to be broken down to elements that everyone can understand at some level. It should appeal to common sense, not priestly level nonsense that appeals to the superstitious. If you have to guess at what they mean, but believe in them as magnificent people, then it’s a con and makes perfect sense at that level.

We are more in agreement than you think.

Kent:

I respectfully disagree that Keynes was “all about” fiscal policy. Keynes was “all about” counter-cyclical policy, which employs variously (and sometimes simultaneously) fiscal policy and monetary policy. Each has their functions and limitations. Monetary policy is the domain of the Fed. Fiscal policy is in the hands of the gummint, but I’ve seen it argued that some of the Fed’s vehicles function as fiscal policy, although more indirectly and inefficiently than the gummint.

There’s also the problem of treating the economy as a monolithic GDP. If the gains to productivity are vastly unequal (i.e. high Gini coefficient), than a simplistic metric like GDP is extremely misleading. The Fed doesn’t do “equality” or “lifting all boats, ” and only focuses on the aggregate GDP that means bowcoo bux for the .01%.

Criticism of the Fed is most warranted, but confused gibberish like Gershon’s garble only works to marginalize intelligent discussion on the subject (…which may be his actual intent, after all).

“This would give the great unwashed a belief that our benevolent bankers were behind prosperity while the government was the cause of all problems.”

That is a nice summation of neo-liberalism.

Two beers,

It’s great to discuss things and disagree. But attacking other commenters personally is not appropriate here. Thank you for your understanding.

Sure, Wolf, sorry.

The key contribution of Keynes was a re-definition of money ( money= monetary)

In the depth of the Depression no one had any money, unless they had gold. The only real money was gold before Keynes. He famously called gold ‘a barbaric relic’ and said that the government could and should issue a medium of exchange with no connection to gold.

The abuse of his theory by politicians buying votes is a whole other story.

BTW: some of the original ideas behind money creation were tried in Alberta in the 30’s, where the collapse of the price of the main crop, wheat. led to desperate thinking. This led to a political party called Social Credit which did try to issue a provincial currency.

However this was ruled as ‘ultra vires’ or outside Alberta’s power by the Supreme Court of Canada,

Amen Kent, along with Ann Rand thinking the ship is sinking without government leaders. U.S. Government spending always creates growth and need not be paid back, unlike Fed policy and private banking.

This comment misrepresents Prof. Friedman’s approach to the Fed. He had a lot of profound insight, that indeed the Fed does use – and abuse – to this day. However, he is also famous for the statement that “…the Fed could be replaced by a computer…”. So he wasn’t a fan of fine tuning/abusing policy as they do today.

I have seen many hours of Friedman’s lectures and seen him in person. He was a very humble man when it was all said and done. I believe a fault of his was that he did not want to get his hands dirty with too much practical, detailed advice- was happy to stay an academic.

See Taleb’s description of people with “no skin in the game”. For better or worse, that describes academics such as Prof. Friedman.

The responsibility of what is happening now in Fed policy is squarely on the current Fed office holders, not somebody who passed away over a decade ago.

Hasn’t it occurred to anyone that these Fed people are simply insane? They are simply Ponzi Dr. Strangeloves, and they are intoxicated by the notion they have been able to get every individual in the world to sign off on the Ponzi. We live in a mad world.

Sooner or later market participants will realize that the Fed was never data dependent. It was just an excuse. The Fed has one goal and one goal only -> “wealth effect” code word for asset value increases. The idea is to make the wealthy class wealthier. But this wealth effect is getting out of control and so the Fed thinks it can bring it under control and also make room for the next downturn. In order to do that it’s telling the wealthy that it will be taking the so called punch bowl away later this year. But the wealthy is intoxicated and do not believe the Fed would actually do that until it’s too late. And they figure even if the Fed is serious then it’ll bring it back when needed. Fantasy!

Too true, camerons. I really hope the fed hikes, as a crash in asset values would help the working class … as long as we don’t lose our jobs. Even if we do, the status quo has gotta change as too many people working in cities can’t afford to live in them.

Food and shelter are too much considered “strategic investment assets” rather than “basic human rights”.

I understand that you can’t encourage a class of entitled non-workers, but trust me when I say we’re nowhere near that extreme. We need to think about the concept of “living wages” again, so that even the lower middle class worker can afford decent food and shelter.

Too many of the wealthy ruling elites see their paper wealth as a “high score” in their game. We need a game-changer… someone interested in something other than their own net worth (aka total dominance), even if that is regional or cultural dominance.

I don’t mean to support racism or genocide, only to point out that the “game” of financial dominance has run its course and will lead only to instability and war.

Story about the 29 Crash. Guy’s dad had a hardware store. When the stock market crashed he said ‘good, now those Wall Street parasites can get a job’

Six months later he lost the store.

The falling tide leaves no boats afloat.

There used to be a social and legislative counter-weight to offset income disparities. Then, propaganda machines convinced people Unions were no longer needed, that 401k or RRSPs would replace decent pensions, that trickle down would help wage earners, and that if you just ‘went along’ you might one day be just as rich as the Donald.

The decline started with Reagan and has only increased in velocity. The rate of gun purchases seems to be a match, too. Looks like a nasty speed bump coming up. Really nasty.

When the Bank of Japan started hiking rates in 1989, both the Nikkei 225 and the Tokyo and Osaka real estate markets shrugged it off and shrugged it off for months and for several consecutive rate hikes.

There was so much liquidity sloshing around in the Japanese financial system it wasn’t a problem: banks like DKB kept on lending with complete abandon.

Right now there isn’t merely an incredible amount of liquidity sloshing around in the US financial system, but the world is far more interconnected than it was back in 1989: the US stock and bond markets are not the exclusive preserves of US investors and a lucky few foreigners anymore.

NIRP refugees from Europe and Japan are scouring the whole world for any discernible scrap of yield. Just to give an example purchases of FAANG stocks, especially AAPL, by European funds are the stuff of legend.

Personally I am waiting to see how bond markets in Europe and Japan will react. Despite a lot of fast-talking by Draghi and Kuroda, both the ECB and the BoJ have inserted a near-record quantity of liquidity into financial markets so far in 2017. Both central banks’ balance sheets, despite pledges to the contrary, have grown considerably this year, meaning they are buying something, and that something is usually securities.

Both the EU (and by extension Switzerland and Sweden) and Japan are still fairly convinced they can “win” the ongoing currency war with China by keeping interest rates repressed and central bank balance sheets bloated. But it looks like the Fed has just made their task a little bit harder.

The Eurozone is not in a currency war with anyone. I doubt it even crosses anyone’s mind ever. News writers who don’t understand economics care about exchange rates in that capacity. It like the Russian Conspiracy, just different.

They only matter a little when central banks go on a debasement binge. Think of it as a sale on money instead of as a sale on underwear at Sears. Only central banks sometimes think a permanently lower price is best so they print out the wazoo. For some reason, it doesn’t seem to work over the long run except in bad cases such as Venezuela. Instead, they generally end up monetizing sovereign debt. The public views it as a free ride.

ECB QE is all about debt monetization intended to keep the Eurozone project alive. The Eurozone will end when ECB QE ends. However, as a distraction from this, I can certainly see Draghi mouthing something about exchange rates in the context of “ECB QE must continue until exchange rates are fair and balanced and all in the project benefit from them being applied by other nations honestly and fairly.” (Try to make sense of that … but I have no doubt he will say something like it if needed.)

Modern day currency wars are not about exchange rates.

Modern day currency wars are all about “sophisticated financial instruments” to give one’s economy a hedge over the competitors, usually by making the cost of debt far cheaper than it would normally be.

Marc Faber explained this very well in his newsletter already back in 2009: he rightly predicted the Chinese shadow banking system would give that country a “very definite hedge” over the rest of the world for “years to come” by effectively giving the Chinese economy, especially its least productive and financially sound part, what is effectively unlimited access to credit, ultimately backed by the government in Beijing.

The EU has so far struggled in this modern day currency war. Germany has benefited from easy access to cheap credit but Italy and France haven’t. All the ECB could do was help as many of these two countries’ big players to stay afloat by buying their securities and hope in the “trickledown effect”.

Japan is a different case. The keiretsu are flushed with almost unlimited liquidity from the BoJ. Most are doing well on export markets with some doing exceedingly well, not unlike their Chinese and German competitors.

But their equities do not seem palatable, so much the BoJ had to step in and directly buy them to prop up prices. I know of at least one Japanese company which put its IPO on standby because of this situation.

Perhaps they’ll go public after the BoJ has run out of other equities to buy.

I agree completely about sovereign level economic gaming. QE and permanently gamed rates from the Fed could have been avoided if working capital were provided – force fed if necessary – on the economy. The globalists won that round.

What nobody talks about is the payback. The other side of the equation. The check for the free lunch.

Eventually, it will arrive and the amount demanded will be immense. The game after that will be how to make someone else pay it. Anyone with actual savings will look like an easy target.

“QE and permanently gamed rates from the Fed could have been avoided if working capital were provided – force fed if necessary – on the economy”

“force fed on the economy”– hilarious, comedy gold!! So, Keynesianism for Kapitalists, but not for workers!

Yay, supply side welfare! Give the rich more free money – they’ll know what to do! God forbid you give working people better-paying jobs that would enable them to purchase goods and services without going deeper into debt, you know, a virtuous cycle…

two beers – do you even know what working capital is and how it relates to daily business operations?

Hint: it’s the lifeblood of all companies. Remove it and watch the company wither and die. QE has no effect on it. Loose and supportive retail banking does. The Fed should have forced banks to make short term working capital loans to maintain inventory or meet payroll, not bulk up idle bank reserves. The globalists won in 2009 and thereafter. Business is recovering in spite of the Fed, not because of QE.

It sounds like they want to end QE and ZIRP because most asset values do not makes sense anymore when compared to their underlying fundamentals.

Canada also hinted they were going to raise rates, most analysts/economists in Canada guest it will be late 2017 early 2018. Most of our mortgages and loans are variable, so the reaction should be quick if that really starts to happen.

But of course, we are in a state of denial right now.

Markets will not fall significantly until something bigger and stronger than the algos removes liquidity, thus reducing the velocity of paper swapping. Reduced paper asset prices caused by a reduction in paper swapping will be conflated with a ‘crash in the financial markets’.

What’s bigger and stronger than the algos?

1) People waking up one day and noticing that the Eurozone will collapse when ECB QE ends and debt monetization is all that is keeping it afloat.

2) Higher interest rates that cause the profitability of fast algo driven paper flipping to remove players on the margin. This will reduce velocity and and raise the amount on each trade that must be earned to protect margins.

3) Less likely but possible is Japan doing something responsible, such as ending it’s adventures in the ETF market and doing something to reduce BOJ QE.

4) Less likely but possible is the Swiss Central Bank ending it’s purchases of equities – they are more prone to be a buy and hold investor who will gin up the printing press to prime the pump at the bottom. Actually, if they become desperate enough, they could conceivably cause a flash crash just to play it. Lots to be made by them doing this.

5) Less likely but possible is the Chinese government running out of ideas about how to cover up several trillion dollars of bad investment, much of which is said to be a ponzi scheme or non-performing.

Basically, if you reduce liquidity, you slow the algos. If you raise the cost of money, you impact the profitability of each algo trade.

‘Yellen sounded “surprisingly hawkish,” the experts said’

Yellen is proceeding on the basis of data that are politically distorted, assumptions that are unsound, models that are invalid, over an economy that is rigged, serving policies that are destructive, under conditions that have been out of control far too long, with tools that are pathetically inadequate.

This will all end in tears.

1) I always favored the one about flapping your arms when falling off a cliff … it won’t hurt and it might help.

2) Yellen is a political animal. She would recite recipes for tomato soup and add some references to econometrics instead of teaspoons if she were told to.

3) Please explain why you can’t raise rates from the zero bound (which is abnormal past the point of bad humor) because raising rates is harmful to the economy. Zero bound rates are a disease and this argument says you need to keep the disease because removing it might make you feel bad. Only the germs have something to lose. So many pundits talk out both sides of their mouths about this. They moan “rates are way to low but you can’t raise them NOW!!!”

Yes, rates must be raised. But what happens to federal interest costs when you do? And when do those costs become unsustainable? Or have they already?

You must also tax the rich and regulate the banks, but then, you must also do ten or twelve other things, none of which are going to happen, and some of which it is already too late to do anyway.

Flap your arms if you like. I will have no objection.

Unwinding a bad idea always cost more than having not put the bad idea into play in the first place.

In this case, I think it will be not as bad as some think … although the globalists and paper flippers will scream bloody murder and the press will support hem.

Money flows. The interest someone pays is income to the lender. People spend income. If you pay higher rates, I will spend the money I earn from them via my savings being invested in debt. If rates are too low, I will make less or not invest at all in debt. This means either no income for me or income only from paper flipping. Both cause low national income overall and decrease economic activity … which would increase if I and others earned some return on savings.

The financial press and central bankers who want to please those who benefit from free money all work hard to ignore the other side of the equation. If you ask about the lack of interest income and the effect on the economy caused by lowered income, they will look at you like you farted repeatedly. Then you will be accused of a new form of Russian Conspiracy. Except for falling paper asset prices temporarily, the economy will grow if rates rise.

“Unwinding a bad idea always cost more than having not put the bad idea into play in the first place.”

Are you airborne yet?

CDR and Walter,

Excellent comments….thanks. Of course I’m just another pi**ed off saver.

In spite of very low inflation, Yellen stated that they were raising rates because of strong employment numbers – WTF??? What is wrong with people having job s? Oh, they might ask for a raise sometime? But consumer spending is 70% of the economy. Workers spending money is good! Strong employment is not an inflationary threat that requires preemptory attacks by the Fed- more people having jobs should be welcomed. But the Fed, fronting for corporate America and the banks, views strong employment as something that needs to be suppressed. The truth is that the Fed is against the workers.

“The truth is that the Fed is against the workers.”

I don’t believe that this is the truth. The Fed does believe full employment will cause large wage increases that will cause inflation. Because that was what happened in the ’70’s.

But most American workers do not have any wage bargaining power because of the loss of private sector unions, and because there is a huge pool of workers on the sidelines if wages start going up.

So the Fed leaders are lost in theory and have little feel for the reality on the ground.

This. They sit in their ivory towers with no clue about the reality on Main Street. The only feedback they get is from Wall Street.

I agree with this. The Fed still operates under the assumption that the US economy today is not fundamentally different than the manufacturing & industrial economy of yesteryear. Yellen believes in the Phillips curve. She still thinks that if she can drive unemployment low enough, inflation will increase as wages eventually creep up. I don’t think this is true anymore – the post-Recession economy is fundamentally different that the pre-Recession economy, and she’s still trying to fight the last war.

The other issue is one of confidence. When the labor market is so insecure – even for well educated, highly skilled workers – I think people tend to batten down the hatches and save, rather than buy that new car or expensive toy. Add in low rates decreasing returns for savers and very high home prices – increasingly unaffordable for the median wage worker – and the situation is exacerbated further.

Kent- so the Fed thinks because of the discredited Phillips Curve that strong (it’s not close to full- there are unemployed people everywhere) employment will cause inflation…it hasn’t yet, so why raise rates and throttle down the economy when inflation is almost nothing? That makes no sense, unless the Fed was scared of workers getting a raise.

“Because that was what happened in the ’70’s.”

Many factors went into stagflation other than just high employment, not least of which was the exogenous shock of the oil embargo. High employment as culprit was the story the Friedmanites concocted to eviscerate the unions and defenestrate Keynes from campus and Congress, and supplant him with the neo-liberal voodoo hegemony that we are suffering under today.

The big banks run the Fed and they really want to make some money now that they’re fully bailed out. Enough millennials have found jobs either brewing beer or pouring it that perhaps the time is right to help those banks out. I’m convinced politics is dead because the rubes can’t read or think so we are now in the technocratic brave new world where the stock market can go up forever. Or at least so long as there is no shooting in the South China Sea.

By raising interest rates, the Fed is signalling that the economy is healing. That is “risk off” to the financial markets. And lower long-term growth means low long-term inflation.

So I’d expect long-term interest rates to fall and the stock market to party on.

This should continue until the black swan arrives.

In the link below ,Bank of America has described the money created by OTHER central banks as a “liquidity supernova” that equaled an annual rate of 3.6 trillion.This amount of liquidity is what has driven and will continue to drive assets prices higher .But it is INEVITABLE that this money creation will stop and then there will be huge price to pay with much lower amounts of liquidity or even a decrease.

Although the bear market will not be a large as 1929-1932 ,where stocks fell~ %90,the coming bear market will the second largest .

Batten up the hatches we are just beginning a wild ride down.

http://www.zerohedge.com/news/2017-04-21/why-nothing-matters-central-banks-have-bought-record-1-trillion-assets-2017

For the Fed to reduce their balance, in theory there are three options,

1 – Securities go back to the market, fed get money from the market, fed lets the money disappear.

2 – Treasury loans money in the market and hands it over to the fed, the fed lets the securities roll of their balance sheet. Money and securities both disappear.

3 – Fed lets the securities roll of their balance sheet and get no money from market or treasury, now the earlier printed money becomes helicopter-money

4 – ??

That would mean in option 2, that there is a lot of money extra for the treasury to loan. In this case they better start raising the debt ceiling asap. Correct??

Hey Jon,

>>Treasury loans money in the market

The word loan is not a verb in English. The word you mean is *borrow*. In English, people lend and borrow, they do not “loan”.

But even after fixing the bad and very confusing English, what you wrote contains some major misconceptions that are even more significant.

When securities are redeemed at maturity, whoever holds them gets the money. The securities become void and disappear. This is what the Fed will be doing: When the Treasuries it holds mature, the US Treasury Department redeems them, that is it exchanges money for those securities that then become void and disappear. The Fed gets the money. If it doesn’t buy anything else with it, that money disappears too. Now both the Treasuries and the money have disappeared.

Since the Treasury Dept doesn’t have the money to pay off maturing bonds (the US government runs a big deficit), it raises this money in advance by selling bonds. So the market gives the Treasury Department the money to redeem the old bonds. By redeeming the bonds that the Fed holds, the Treasury Dept gives this money to the Fed. At the Fed, this money disappears. In this manner, the Fed drains liquidity (money) from the market.

This is the reverse of what happened during QE.

Thanks Wolf for explaining this. I do understand it better now.

A somewhat more granular question to anyone following US markets. The volume so far today. WTF??

Either my source is problematic or someone or something has got the major markets in a serious choke hold. Who’s got the Ex-lax?

Interest income on Fed securities is already transferred to the Treasury. Why not the principal payment for Treasuries? A $2T windfall for the government. Should be good for deficit funding for a couple of years.

Yes. Federal Reserve profits are distributed to the Treasury after payment of a dividend to the member banks.

By law, these proceeds do not simply disappear, but should instead be an important part of the budget once the unwind is well underway.

The market ignored because market knows the fed is on their side ..

What are they waiting for sitting on its “balance sheet reducing scheme”? The world has never been this close to wiping out the grandparents for the yield on their savings bond and the Fed is doing What? Between now and some arbitrary time the Mortgage Backed securities could lose value…. This balance sheet is a port a john!

This balance sheet is a debt collecting agency that bought securities for pennies that were worth nothing and is about to have to steal a baby from hospital or admit it wasn’t pregnant?

Can we trust Yellen to drive a hard bargain with Dimon? Yellen bought the securities for income and fees? Yellen is Hank Greenberg!

Wasn’t the whole point of QE to overpay for the securities so bank can offload them? Even for treasuries, the Fed paid top dollars to force interest rates down. The Fed will write large losses as these “investments” mature. Will be interesting to see how they hide the losses.

Regarding the Fed allowing MBS to roll off at maturity, does that include those which are backed by mortgages in default? If so, that’s a huge backdoor bailout of Fannie and Freddie, instead of the QE unwinding that’s being proposed.

Yes, it includes mortgage backed securities (MBS). When they mature, the issuers (Fannie, Freddie) pay the Fed the face value of those MBS and take back the MBS which become void. This is the normal process. It has been happening for years. What will be new is that the Fed will not reinvest that money by buying more MBS, issued by Fannie Freddie. Instead, that money that the Fed gets from Fannie and Freddie will just disappear. So this (a buyer, the Fed, stops buying) puts pressure on the MBS market and is likely to raise mortgage rates.

Buying MBS during QE, and replacing them after QE, was a bailout of the mortgage market and every entity that had anything to do with it, including Fannie and Freddie. Unwinding QE in this manner has the opposite effect, and it will put pressure on those entities.

I don’t see any speculation on the effect of this big unwind on the federal deficit. Redeeming those bonds will mean using tax money, or money borrowed from elsewhere, since the Fed won’t be rolling over their maturing binds any more.

All this will have the effect of neutralizing the Unwind, I would think…