Stockholders and junior bondholders fear a “bail-in.”

By Don Quijones, Spain & Mexico, editor at WOLF STREET.

After its most tumultuous week since the bailout days of 2012, Spain’s banking system is gripped by a climate of fear, uncertainty and distrust. Rather than allaying investor nerves, the shotgun bail-in and sale of Banco Popular to Santander on Tuesday has merely intensified them. For the first time since the Global Financial Crisis, shareholders and subordinate bondholders of a failing Spanish bank were not bailed out by taxpayers; they took risks in order to make a buck, and they bore the consequences. That’s how it should be. But bank investors don’t like not getting bailed out.

Now they’re worrying it could happen again. As Popular’s final days showed, once confidence and trust in a bank vanishes, it’s almost impossible to restore them. The fear has now spread to Spain’s eighth largest lender, Liberbank, a mini-Bankia that was spawned in 2011 from the forced marriage of three failed cajas (savings banks), Cajastur, Caja de Extremadura and Caja Cantabria.

This creature’s shares were sold to the public in May 2013 at an IPO price of €0.40. By April 2014, they were trading above €2, a massive 400% gain. But by April 2015, shares started sinking. By May 2017, they were trading at around €1.20.

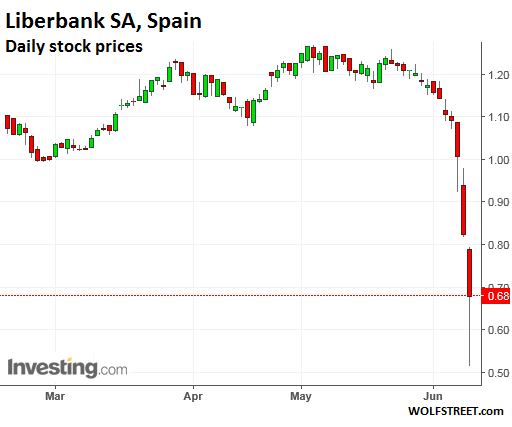

But since the bail-in of Popular, Liberbank’s shares have seriously crashed as panicked investors fled. Scenting fresh blood, short sellers were piling in. On Friday alone, shares plunged another 17%. At one point, they were down 38% before bouncing at the close of trading, much of it driven by the bank’s own share buybacks:

In the last three weeks a whole year’s worth of steadily rising gains on the stock market have been completely wiped out. The main causes of concern are the bank’s high risk profile and low coverage rate. By the close of the first quarter of 2017, Liberbank’s default rate had reached 13%, over three percentage points higher than the national average (9.8%), while its unproductive asset coverage rate was just 42.1%, compared to 47% for Banco Sabadell, 48% for Bankia, 50% for CaixaBank and 55% for Unicaja.

Worse still, the vast bulk of the bank’s unproductive assets are real estate investments. After Popular, it is the Spanish entity with most exposure to toxic real estate assets, according to the financial daily El Confidencial — a remarkable feat given the bank already had the lion’s share of its impaired real estate assets transferred onto the balance sheets of Spain’s “bad bank,” Sareb.

It’s not just the bank’s shares that are feeling the pressure. With the memory of what happened to holders of Popular’s junior, subordinate and convertible debt still fresh in their mind, investors are divesting their exposure to Liberbank’s subordinate debt. On Friday alone the bank’s most recent issuance, dating back to March 2017, generated losses of 9.8%.

Liberbank’s management has responded the only way it can — with a slew of denials. The bank is nothing like Popular, it says. It is solidly solvent and its deposits are safe, which is probably true: even the deposits of Popular’s customers are now safe despite the fact the bank had hemmorhaged €18 billion of deposits in the last few weeks of its truncated existence. It was this frantic run on deposits that ultimately sealed its fate, prompting the ECB to conclude that the bank was “failing or likely to fail.”

Banco Popular’s demise is a stark reminder that Europe’s banking woes are far from resolved, despite the trillions of euros thrown at them. “The message the market is sending is that you have to buy solvent banks and stay away from those that pose high risks,” said Rafael Alonso, an analyst at Bankinter, one of Spain’s more solvent banks.

Another Spanish bank that could be considered to pose high risks is Unicaja, the product of another merger of failed cajas that is (or at least was) scheduled to launch its IPO some time in June or July. As things currently stand, the timing could not be worse. The greater the uncertainty over Liberbank’s future, the lower the projected valuation of Unicaja’s IPO falls. Before Popular’s forced bail-in and acquisition, the Unicaja was valued at around €2.3 billion; now, just days later, it’s valued at less than €1.9 billion. If the trend continues, the IPO will almost certainly be shelved.

As for Liberbank, if things don’t improve soon and investor nerves aren’t steadied, it too could find itself on the ECB’s Single Resolution Board’s chopping board. Perhaps it too will be sold for €1 to a much larger bank that, like Santander, is able to raise billions of euros of new funds at the drop of a hat, with other too-big-to-fail banks like UBS and Citibank more than happy to lend a helping hand. And just like that, another smaller bank would bite the dust while the biggest banks get bigger and ever more dominating in the market. By Don Quijones.

Many Banco Popular investors wiped out. Taxpayers off the hook. What it means for Italy. Read… “Bail-In” Era for Europe’s Banking Crisis Begins

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

It’s a matter of borrowing again bailouts are the way forward as money pays them anyway

ECB caused the problem do it’s up to them to solve it .

“Is Another Spanish Bank about to Bite the Dust?”

A slippery slope of 1 degree is still a slippery slope. Inconceivable has transformed into systematic. The lack of willingness to live within their means plus this has set the rest into motion and it likely will not stop. A slow but exponential increase in slope, speed, and mass can be expected and be expected to continue. Interesting times ahead.

Breaking the bank

https://oinsurgente.org/2017/06/10/breaking-the-bank/

“The crisis in Portugal’s biggest bank, Caixa Geral de Depósitos, and how it explains the crisis the country itself has faced in last few years.

“Portugal was one of those countries. In 2011, the “troika” of the IMF, the European Union and the European Central Bank came to the rescue with a €78 billion bail-out package with €12 billion for the banks to use to recapitalize themselves. They badly needed them. Not only they were the largest funders of the debt splurge the government of the day, led by then-Prime Minister José Sócrates of the Socialist Party, currently under investigation for corruption, tax fraud and money laundering, but the “austerity” prescribed by the “troika” and applied by the PSD/CDS coalition once an election threw Sócrates out of power also meant that there was no government –i.e., taxpayers’ – money for the “public-private-partnerships” in infrastructure Portuguese banks had become accustomed to invest in at almost no risk to themselves, as well as other shady deals. To further complicate things, Portuguese banks were themselves heavily indebted, both to each other and abroad, and so they to felt the noose tightening around their necks.”

Yet another shining example of why the FIC needs to be reduced to the status of a tightly-controlled public utility.

It’s also yet another shining example of why you don’t put the national or supranational financial system in the hands of the pathologically greedy and malicious. Not that the pathologically greedy and malicious persons who run such systems are at all obliged to listen to anybody about it.

They’re not going to stop until you make them stop, and if you try to make them stop they’re going to make it very clear that they’re not about to let you.

Could it have anything to do with NIRP and priced-to-fantasy, and the loss of trust in bailout?

Well, that plus the uncomfortable fact people don’t feel especially inspired to pay back their loans.

Banco Popular was ultimately done in by the modern day equivalent of a bank run: it ran out of collaterals to access the liquidity lines needed to offset the deposit outflow it was experiencing once it became apparent a bailout wasn’t forthcoming.

European banks thought they could stop bank runs by limiting the amount of cold hard cash people can withdraw (with a big assist from the ECB eliminating €500 banknotes and limiting the number of €200 in circulation) but apparently once depositors get desperate enough they find ways to get their money out nonetheless.

Liberbank apparently still has enough collaterals to get the liquidity to buy back its own shares but this could come back to haunt them down the road: every euro in eligible assets that is used as collateral now is one euro that won’t be available to lend against when the deposit outflow will start in its earnest (educated guess: unless something changes next Thursday or Friday). Unless of course Europe adopted the same standards as China, where the same collateral can be pledged multiple times to multiple creditors. Before disappearing from “bonded warehouses” and “traceable accounts”, of course.

To completely change tune, the big difference between Spanish and Italian banks right now is all in media treatment. Silence has descended upon Italian banks: apart from a few truly independent news websites and some bloggers close to M5S you don’t hear a peep after Intesa dodged the bullet of a highly questionable merger and the government assured everybody MPS would be back on the Milan stock exchange by July. This was almost three weeks ago. Since then to quote Simon and Garfunkel “the sound of silence”.

Smaller banks have been roughed up in the meantime, despite a concerted PR campaign to sooth their shareholders’ and bondholders’ nerves: fast-talking will only get you so far if you cannot get buyers to open their wallets.

And this is all despite record liquidity injections by the ECB: turns out even supposedly omnipotent central banks have to bow down to the law of diminishing returns. All the ECB has to show for such a gargantuan effort (seemingly coordinated with the BNS and the BOJ) has been to prevent a general rout in bank bonds and stocks.

Limiting the options to withdraw deposits (i.e. removing €500 note), and keeping silent (i.e. starting the rumour mill) will cause panic? Who would have thought?

The retirement of large denomination notes began in Holland long before the EU. Canada followed suit more than twenty years ago with the retirement of the thousand dollar bill. At least in Canada, this had nothing to do with bank runs. It was done on the advice of Tax authorities and the RCMP.

In Holland it was noted that a large note (can’t remember if it was the 100 guilder note) was known to exist in large quantities but hardly ever seen.

Law enforcement in both countries were convinced the notes played a big part in illegal transactions.

I’ve heard this angle a lot of times. While I am personally convinced those launching these crusades on savers genuinely believe their angle, I am yet to hear somebody explain why the illicit drug trade keeps on growing in dollar value every year, completely unimpeded by these measures. Are Mexican cocaine cartels and Middle Eastern heroin middlemen stashing their ill gotten gains in €1 coins in their basements? Do they dive into that sea of metal like Scrooge McDuck?

Sorry for the sarcasm, but illicit activities of all kinds, even innocent ones like hiring some teenager to mown your lawn, have long been used to hit savers on the head a bit more, to make bank runs harder and to tighten the bureaucratic grip on society. While criminals laugh all the way to the bank.

“the bulk of the bank’s unproductive assets are real estate investments”

This is the case across the board – most real estate properties are not even realizing profit from rent paid –

I can’t understand why the genius that investment mind set is purported to be, does not realize that real estate profit is not gained from property sales – but from rent collected – actual cash in the hand & reinvested wisely.

A bird in the hand is worth two in the bush, man.

Newtons Law of Motion is in play here – the population of planet earth is – still – steadily decreasing – there are way to many banks on planet earth – it’s the most lucrative business to be in – thus goes the fairy story – a correction must take place for healthy blood to flow.

Today – the only place for a punter to stash his few meager dollars in under the bed & for the duration.

“https://wolfstreet.com/author/don-quijones/”

“And just like that, another smaller bank would bite the dust while the biggest banks get bigger and ever more dominating in the market.”

Yes Mr Quijones.

However Spain and Italy both have far to many “Trading Houses”. That became Banks as a secondary line of income then closed or hived off their other activity’s over time.

5 or so majors and a (very)few minnows is all Spain and Italy need each.

Yet they have between them ?? close to 100?

Simply far to many.

Consolidation is required, in both those States and others in Europe.

Otherwise as the age of taxpayer funded bailouts in Europe ends, the other option will be forced closures some of which will be very mess.

In the age of electronic banking and 24/7/365 cash machines.

small limited service outlets working with major branch Hub’s, in a big area are all that is required.

A Nationwide major bank in our country does this, they share their small outlets with postal service, and stationery/book chains, Nationwide.

They pay slightly higher interest and they charge slightly less interest as they have lower overhead’s. The have good housing loan portfolio.

It works.

Agreed D there needs to be more consolidation of the smaller banks to take some of the weak one’s out of the system.

I think the shock in the last week is that Popular whilst not being a big bank (No 6 in Spain) its sent a shock that a 109 year old bank has gone.

Saying that Monte De Paschi isn’t from 1492 lol.

“Saying that Monte De Paschi isn’t from 1492 lol.”

.MDP has been bailed out indirectly that many times its like saying the British royal family, is over a thousand years old, it is, but it isnt.

Great article and good comments. To have an unproductive asset coverage of 42% they deserve to go under. Monday should be interesting reference Liberbank’s share price. Similar to Popular, if the confidence of the people has been hit in the two banks mentioned then a bank run will occur and thus that one euro coin will come out again. The Spanish Press are using words like contagion and share collapse that isn’t going to help the situation.

How much of bad loans was transferred into Sareb at the time?

Agree things in Italy have been far too quiet.

I’ve been trying to find out the exact breakup of the Sareb “assets” by originating bank for quite a while but never got anywhere. All I know is the bulk of Sareb business is to sell real estate, most of it in “new” or “unfinished” conditions, hinting it didn’t come from evictions but was taken over by the bank from a construction or real estate company, possibly after being pledged as collateral.

Personally I am holding on until Thursday or Friday before declaring Liberbank either dead and gone or out of immediate danger: dip buyers have had a pretty rough 2017 so far and even something as dubious as Liberbank shares may attract them. The dust needs to settle a bit to see if deposit outflow is accelerating or the bank is in suspended animation.

One thing is for certain: unless something radically changes at macroeconomic level Liberbank, and a host of other similar banks throughout Europe, will be in serious troubles again very soon, possibly at the beginning of the next ECB President’s tenure.

The “problem” with Italy is the sound of silence is not fooling nervous shareholders. One of Italy’s lesser stock exchanges, Hi-MTF, trades only the stock of a small number of those local banks which are teetering on the brink of collapse. At least one of those banks floated the idea of an IPO on the Milan Stock Exchange (FTSE-MIB) and was shot down immediately.

These banks bounced back thanks to ECB largesse early in 2017 but have already lost all those gains, and some, over the past month: just to give an example Banca Valsabbina stocks had bounced all the way from €4.95 last August to €7 this May. On Friday they were trading at €5.7, having lost 10% in just a week.

Valsabbina has engaged in a costly and elaborated charm offensive to keep shareholders (which include several of my relatives; now you know where my Italian part comes from) from selling but it only managed to fool the most gullible. The rest are lining up for the exit.

MC – All I’ve picked up was that 100 billion euro’s of Property Assets has gone into this sareb scheme – government backed. You’ll never find out which banks valuewise benefited, too political.

Aside of all the smaller banks like Monte De P and the Veneto Banks which are dead in the water, is there any stories reference the bigger Italian players like Unicredit?

MPS is not small: it’s the third Italian bank after Unicredit and Intesa.

Like Unicredit the big problem with MPS is nobody wants to touch their NPL’s with a very long pole, yet getting rid of those toxic assets somehow is the requisite for the EU greenlightning the State aids MPS desperately needs, not unlike it was done in Spain with Sareb.

Part of the reason nobody wants those toxic assets is banks flat out lied about them: Unicredit’s share of toxic assets to be spun off has grown for €10 billion to €20 billion in just a year and it’s likely to grow again. To this must be added collateral quality. If China has a problem with collaterals being pledged multiple times to multiple creditors, Italy has a problem of collateral quality.

To cut a long story short assets backing loans have routinely been inflated in value by the banks themselves, which have used every dirty trick in the book to keep real estate, the chief collateral by a huge margin, artificially inflated. As real estate values started to weaken at the end of 2014 in several areas and have been softening (but not crashing) ever since, NPL’s started to pile up as banks were forced to renegotiate loan terms.

To this it must be added the usual rascality, such as pretending a dilapidated warehouse in the middle of an abandoned industrial zone is as good as a freshly refurbished attic in the most fashionable area of Milan.

To change tune, Intesa dodged a massive bullet in form of a merger with insurance company Generali. Now: the Intesa board had very little appetite for this merger. But it was politically driven and Generali was all for it.

Intesa already tried their hand at the insurance business and didn’t like it. Not one bit. And they also know that, despite Intesa being the financial heavyweight, Generali would end up dominating the new board of directors thanks to their political clout.

Another reason so many Italian banks are kept running by any means is that nobody wants to see an evaluation of the NPL’s by anybody. Not 200% owned by the Mafia.

As the collateral for so many of those NPL’S If it even actually exists was never worth 10% of the loan in the first place.

I read of one loan that was secured against a multiple Hectare farm when the investigation took place the farm was found to be under 5 Meters of Sea Water, at low tide. No it was not a Mussel or Fish Farm.

In another, a “Fleet” of 4 Axel trucks and trailers, tuned out to be a “Model Fleet” of 4 Axel trucks and trailers, all of which had been road registered.

Italian banks are Loaded with NPL’S against this sort of “Collateral”.

Great comments D.

There’s an article on Bloomberg today about a small Greek Bank having 61% of its loan book being non-performing.

You couldn’t make this stuff up.

Correct.

Unless Eurozone NPLs are all cleaned up and there is huge consolidation in Eurozone Banking.

It will always be a when Euro zone banking implodes and does it take the whole global financial system with it.

The Global system cam withstand an imp[losino in 1 of its three legs EuroZone, US, china.

Not 2.

china is a when so if the EuroZone does not clean up and consolidate, when china does everybody does. As china and the EuroZone are getting very friendly and so.

Very financially interconnected.

EuroZone and china,2 Huge economies together, who both bend the rules much farther than the US ever does.

And both print money like there is no tomorrow with, can only end with a BIG bang. Unless 1 of them has a very stable base.

Remember it was a banking collapse in Europe, that triggered the wall-street crash in 1929. Although wall street, was an accident, looking for a partner, and a place to happen, then.

Crime syndicates in both Spain and Italy (often the same things) have no interest in loans: in fact their business model in both countries and, to a lesser extent, Germany is built around using money-losing ventures to launder their ill-gotten gains.

The same applies to Asian immigrants (the only ones with any money): if they need a loan they don’t go to their local bank but to their community leader.

No, the problem is twofold: collaterals are massively overvalued and at the same time lending standards have been (and in many cases still are) incredibly loose.

The latter has obviously political overtones, but one should remember Italy’s governments, regardless of their composition, have been obsessed with GDP growth at any cost, even after the country has long run out of steam.

“Crime syndicates in both Spain and Italy (often the same things) have no interest in loans: in fact their business model in both countries and, to a lesser extent, Germany is built around using money-losing ventures to launder their ill-gotten gains.

The same applies to Asian immigrants (the only ones with any money): if they need a loan they don’t go to their local bank but to their community leader.”

Depends on what level you criminal is at.

If we take a long step away from ….

“Oh, God, the banks are closing down around us.”

Is it possible that Banking is seen to be the most lucrative business on planet earth ….

“Ma, I know he is short & ugly, but ma, he works in the bank.”

And that over time, the banking system has grown – & – grown – & grown – & – grown – grown out of all proportions according to clientele & real profit realization.

Shouldn’t we appreciate these bank closures as A CORRECTION to improvement.

“Shouldn’t we appreciate these bank closures as A CORRECTION to improvement.”

In the case of the entire Eurozone MOST Defiantly.

Q:

If the poppy fields – legal & illegal were to experience difficult is producing a successful crop – due to soil degradation & an overrun of damaging pesticide resistant insects – how would this affect the market share of the pharmaceutical industry – if their capacity to deliver to the market place adequate supply of painkiller products was inhibited ?

I didn’t need to look but I did anyway, another Abengoa bag holder http://cadenaser.com/ser/2015/11/26/economia/1448544006_588588.html

They are Abengoa heavy, anybody holding Abengoa paper is gonna eat shit, it’s a fraud.