It has a history of tripping the stock market.

Revenues in the current quarter – Q3 of its fiscal year – would drop 4% to 6% year-over-year, Cisco said after hours today. Shares plunged 8% to around $31 in late trading. Timing of the announcement was impeccable: Minutes after the Dow finished its 372-point plunge.

It also announced 1,100 layoffs on top of the 5,500 layoffs it revealed last August (7% of its workforce at the time), and it added $814 million in charges related to those restructuring efforts, spread over Q3 and Q4.

Cisco has a history of tripping up the markets.

In an earnings call in November 2007, then CEO John Chambers famously used “very lumpy” to describe growth in the US. The S&P 500 and the Dow had just edged down from all-time highs. The market was still blissfully ignoring the hissing from the housing bubble and the stench from the banks. Cisco’s quarter had been phenomenal, with revenues up 17%. But after some gushing, Chambers said revenue growth in the US would be “very lumpy.” The Financial Crisis was next.

So Cisco’s revenue “growth” – in quotes because it’s a decline – no longer compares to the heady days of that time. Revenue in its fiscal Q3 fell 0.5%% to $11.94 billion, with product revenue flat and service revenue down 2%. For the three quarters combined, revenues are down 2%.

But cost cutting has been effective: operating expenses fell 8%, particularly in the wrong places for a company with declining sales: In research and development, and in sales and marketing. So net income rose 7%.

But instead of continuing down this path of revenue stagnation, Cisco indicated that it would go down a path of sharper revenue declines, and expected its Q4 revenues to fall by 4% to 6% year-over-year.

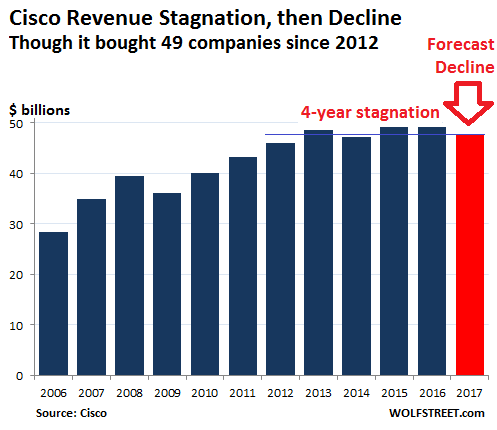

With Q4 2016 revenues at $12.6 billion, a 6% decline would bring Q4 2017 to $11.8 billion, which would bring fiscal 2017 annual revenues down to $47.7 billion, the lowest since 2014, and barely above 2012 revenues.

This chart includes estimated annual revenues for 2017 as per Cisco’s lowered Q4 forecast. In other words, after four years of stagnation comes the decline:

“I am pleased with the progress we are making on the multi-year transformation of our business,” said CEO Chuck Robbins in the statement.

In the conference call, Robbins blamed federal government spending for about a quarter of that decline (1 point of the 4% to 6% decline). The rest of that decline was just plain lumpy demand, as Chambers might have put it.

This revenue decline is occurring despite Cisco’s permanent acquisition binge. Since 2012, Cisco has acquired 49 companies, from tiny startups to not so small companies, in order to boost its revenues and technologies and stay relevant and change its future. So far this year, it has made four deals, including the $3.7 billion acquisition of AppDynamics.

Cisco has not disclosed how much it spent on 28 of those 49 companies. But for the 21 acquisitions for which it disclosed the terms, including AppDynamics, Cisco spent $18 billion! And yet, during those five years, revenues have gone nowhere!

It also blew $27 billion on buying back its own shares over those five years. Between acquisitions and share buybacks, that’s at least $45 billion out the window with nothing to show for.

Many of Cisco’s problems are company specific. For example, it’s hard for a tech company to design new and better mousetraps when it’s busy cutting in-house R&D, axing its people, and buying back its own shares.

But “lumpy” demand for a company as large as Cisco that sells primarily to corporate customers has broader implications, especially if there is a sudden and unexpected shift. Why is corporate demand suddenly drying up? Is it like November 2007, when stocks were just barely down from super-inflated all-time highs, but corporate customers were spooked by the real problems and uncertainties they saw in the economy that could no longer be brushed under the rug?

In 2007, Cisco was a key thermometer for corporate demand. Today, its revenues are 37% larger. Cisco may be on the path to irrelevance, but it cannot be ignored when it comes to corporate demand. It might be an indication that corporate investment in tech has taken as sudden and sharp turn lower, as Cisco’s customers are closing their wallets and battening down their hatches, spooked by whatever they see coming over the horizon.

But there remains a sign of our crazy times: Despite Cisco’s five years of revenue stagnation, serial layoffs, and $18-billion acquisition binge to nowhere, its shares have actually doubled!

And it’s not the only company riding up miraculous asset bubbles. But pressures are building on these bubbles – and some of them are already deflating. What the slow crash of classic car prices says about the future of other asset classes. Read… This Is How an Asset Bubble Gets Unwound these Days

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I remember the four horsemen of the 2000 bubble – Cisco, EMC, Sun Microsystems, and Oracle. Those businesses seem like commodities now. Things can change a lot in 10 years.

Indeed with EMC bought by Dell (leveraged to hilt buyout using NIRP debts) and Sun (on its death spiral) acquired by Oracle. And old darlings Bay Network and Ascend Comm all disappeared into oblivion along with its acquirer once stalwart Lucent who in turn merged with another sick puppy Alcatel. HP on its deathbed…

Cisco is facing challenges by IP thieves it helped along the way in China – was only way to get into the Chinese market but alas it came to take big chunk of its business.

And SillyCON valley is run amok by software purveyors in last 10 yrs and maybe it ought to be called InternetAD valley…

The CLOUD is happening.

Companies are moving their data centers to the cloud and not buying any new hardware or network devices.

And Facebook, Amazon, Google, etc all make their own servers and network devices these days.

I live in Northern Virginia and work in the data center space. While AWS is huge, it’s crazy how many new data center buildings are going up that are standard rentable space. The cloud providers aren’t ruling it all (Not that AWS doesn’t have a ton.)

Cisco has fallen out of favor to Juniper for routing and Arista for switches. Cisco had some software bugs and their newer Nexus hardware that replaced the older series seems to not get as much love.

– This reminds me of something else. In the 1st quarter one analyst said that the revenue/profit growth of the S&P 500 (or was it the DOW ?) was “very disappointing” and actually slightly down.

– Yes, some companies were able to grow but that growth came from acquisitions ONLY.

(Don’t know where I heard it).

– Correction: Corporate earnings in the 4th quarter of 2017 are/were not growing. Only a few companies were able to show a growth in revenues. And even most of that revenue growth came from acquisitions, not from growing business.

Source:

https://mcalvanyweeklycommentary.com/trump-trumps-obamas-global-apology-tour/

Listen from 00:04:00 to 00:06:00.

I worked as an equity analyst at the time of Chambers 2007 comments (but didn’t cover his sector)….and frankly, I though he was the most upfront of the major tech sector corp CEO’s in calling a spade a spade. His comments were the best tech barometer at the time imo and I was not in the least surprised to see him put to pasture immediately when he started to reveal that Cisco’s [revenue] ‘growth’ was stopping….which in fact what was occurring….though stock buybacks (and minor acquisitions) have provided earnings growth (until the current quarter if the new warning is taken seriously).

Shrinkage is not a pretty picture, but adding share buybacks and acquisitions to the reduced revenue is not a winning formula.

– Did Cisco buy back its shares in the last few years ?

– What happened to the dividends ? Sometime (rising) dividends are very appealing to shareholders.

In Q3, Cisco paid a cash dividend of $0.29 per share = $1.5 billion and repurchased $0.5 billion in shares.

And directly from the horse’s mouth: “As of April 29, 2017, Cisco had repurchased and retired 4.7 billion shares of Cisco common stock at an average price of $21.21 per share for an aggregate purchase price of approximately $99.1 billion since the inception of the stock repurchase program.”

The $99.1 billion in share buybacks includes the $27 billion in buybacks over the past 5 years that I mentioned in the article.

“It also blew $27 billion on buying back its own shares over those five years. Between acquisitions and share buybacks, that’s at least $45 billion out the window with nothing to show for.”

Just curious, how were those share repurchases funded? Through debt or cash?

As long as they take on debt to fund repurchases, and save their cash for dividends, they’ll remain in favor of the sell side folks.

– One way is issueing debt and that makes sense with these low rates. Then the interest on that (short term) debt is lower than the dividend yield.

– In that regard rising interest rates would be very helpful to eliminate this kind of “financial enginering”. But it also will tank CISCO’s profits.

– Oooooops. I only now found that info in the article.

In the past the clarion call was, get big or die.

Going forward that will prove in most cases, to be a losing stratagem.

As a winning corporate structure will prove to be one that is nimble, lean, and financially quick footed, with a small amount of leverage that is beneficial. Mega corporates like Cisco will fall as outmoded corporate models, slow to react and burdened by debt.

Looks like Cisco didn’t get the memo!

Tech is maturing out. Commoditized. There is little growth left.

I can’t keep up with the tech we already have. Further advancements seem like overkill. Who wants to sit in a chair and let a computer do everything for you? Most people go crazy when they don’t have repetitive mundane tasks to focus on. Not everyone is wired to be a Plato or Einstein.

I get enjoyment from collecting and riding motorcycles. Driverless vehicles will take away much enjoyment.

I’m with you Bobber. Fifteen years ago I purchased a new Kawasaki ZRX12 sport bike, and it’s great to drive as well as being inexpensive to insure and operate.

I can’t imagine we’ll ever have driverless motor bikes let alone AI driven cars???

At least Cisco is a tech company. Unlike Uber, which is a big taxi service, calling itself a tech company.

I get Internet connectivity from my local cable company: Sprectrum. They called the other day and told me for just $15 more per month I could upgrade my paltry 10Mb connection to 65Mb. Speedtests show I actually get closer to 13 Mb on average. Bandwidth testing shows I never, ever use more than 4Mb, usually while watching something on Netflix, while my wife is watching a YouTube video.

My wifi router is 10 years old and works great. My Mac is 8 years old and works great. At work we have 100 Mb to the desktop, 10 Gb between sites and 500 Mb to the Internet. All of this is overkill.

The days of overpriced Cisco hardware are done.

“…$45 billion out the door with nothing to show for.”

Except the stock price is at a sixteen year high. Isn’t that all that really matters these days?

We had 10BaseT then we all upgraded to 100meg connections then we got 1gig connections. All to the desktop. I say when the Scotty on the Starship Enterprise can beam us up to the transporter room because they can geo-locate our co-ordinates via the desktop technology then that’s a new and worthwhile tech upgrade reason. Until then I’ll continue to use the 12 year old Cisco hardware that can support a gig connection to my ISP.

Ford laying off 10,000 ( in the US alone )

Harley Davidson’s laying off in the hundreds

Brick & Mortar closing doors across the US

FCA about to announce major layoffs

GM no doubt about to follow suit

And now tech … Cisco specifically laying off an additional 1100 on top of the 5500 already let got

And yet … the cronyism continues in the vain pursuit of making America … something again … though what god only knows

But hey … in this current Land of Nod where fair is foul and foul is fair .. debt is the new wealth and loss is the new gain ..

.. sigh .. who’ll notice ?

No, no, no, you are wrong. The labor market is so tight that we can give everyone 2.856012 jobs.

You’ve got to love their ability to keep everything looking rosy; they are absolutely geniuses at that.

Cisco has been historically very good at beating analysts estimates for quarterly earnings by a penny. It was almost a joke.

Something must be amiss if their methods can no longer bring in a ‘beat the street report’ earnings report.

“Something must be amiss if their methods can no longer bring in a ‘beat the street report’ earnings report.”

As is popular today, we just need to rejigger our lingo.

How about saying “Cisco Beat the Analysts on the downside?

Just like earnings descriptions just a few years ago that were “worsening at a lesser rate”.

What P/E does CSCO deserve given its growth prospects?

Probably closer to 10 rather than 15

That would bring the stock down to ~ 25 or even lower

One financial metric which is becoming more common is the increasing amount of goodwill on a companies balance sheet.Goodwill is an intangible asset largely arising from acquisitions.Increasing amounts of goodwill are not necessarily a bad thing provided they are accompanied by increasing free cash flow.But often this is not the case and companies need to write down some of this goodwill.This is nothing more than an admission that they threw money out of the window . Investors often ignore any of this goodwill impairment because they incorrectly focus on a companies reported earnings and not their GAAP earnings. CSCO is a company with a large amount of goodwill on its books

Demand was “lumpy” too back in 2013: http://www.zerohedge.com/contributed/2013-08-16/cisco-ceo-chamber%E2%80%99s-warning-record-sales-and-%E2%80%9Clumpy%E2%80%9D-demand-just-november-200

Sorry guys, just a bump in the road. Still not seeing problems.

“Demand was “lumpy” too back in 2013

Sorry guys, just a bump in the road. Still not seeing problems.”

…………..

Fair enough.

As long as declining retail traffic to stores and malls has minimal impact on economic activity.

As long as the decline in auto sales is only a blip.

As long as the decline in condo prices in Manhattan, Miami and Vegas is a non event.

As long as there has not been overbuilding in Commercial RE in major cities.

As long as oil companies can make a profit at $50 a barrel, ………..

then yes, it will be just a bump in the road.

Yeah, but back in 2013 no doubt there were other economic numbers that were not exactly hot either. In fact given our so called “tepid” expansion for the last few years, it can be argued that economic numbers have at best been so so.

All I am saying is that the case for the economy remains at stall speed, which means no change.

Our local Winn Dixie is letting 10 people go at the end of this month, according to one of their own. It’s definitely lumpy out here.

It’s really interesting…

If you come to this website, it seems like the world is falling…

But when you look at the real estate prices, stock market, people spending money… everything looks awesome..

Wondering when these two would converge

USA is driven by 70% consumer spending.. the wages are declining, people are losing jobs… costs are increasing.. then where the hell people are getting money to spend… debt ?

Won’t this make things unsustainable..

I am a saver and my bank pays 0.01% per year interest… people like us are really screwed big time..

time to take on big debt and enjoy life…

After doing all the right things in my youth, I have nothing to show for it, except my family. We lost our home, our savings, and even had to sell our wedding rings after 20 years of marriage.

My father went to sea at 15, to care for his mother, and after working 50 years, my parents died broke. My in laws worked their whole lives and lost everything to medicare and illness, they too died broke.

It’s the new normal, a parasitic system. Spend it, enjoy it, help your children, because the plan is to take it from you.

Stock prices and real estate prices have been propelled higher by the flood of money created out of thin air by the world’s central banks.It has been estimated that these central banks created over 1 trillion in the first quarter of 2017.This and other monies created in the last 5 years have had relatively little affect on the real economy,especially those consumers who are not in the top 10% of income earners.

I was looking at Ascena Corp. this morning. Stock down 35%. It’s trading at $2.00. They own 6000 ladies retail stores nationwide employing 16000 people. Same store sales declined 8% last Quarter. Both it’s income statement and balance sheet look scary.

I suppose Ascena may have to take a number and get in line behind Sears.

Let’s hope it’s done in an orderly fashion.

Ascena Corp. owns Ann Taylor and Loft, both of these were in my local mall, until recently. Ann Taylor is now gone, it was the more expensive professional brand. Several other stores have also closed since my last trip there some weeks ago. The contraction in retail is extremely evident, you can see even the open stores have cut back staff and inventories.

Petunia

I live two streets away from a main thru way shopping area. Stores are becoming vacant all the time. There seems to be a backlog of them if you will. It is becoming worse out there..