Why everyone is afraid of breaking the addiction.

Here’s another data point on the Canadian housing bubble, how immense it really is, and how utterly crucial wild housing speculation has become to the Canadian economy.

Housing starts surged to 253,720 units in March seasonally adjusted, the highest since September 2007, according to Canada Mortgage & Housing Corp. Of them, 161,000 were multi-family starts of condos and rental units in urban areas. In Toronto, one of the hot beds of Canada’s house price bubble, housing starts jumped by 16,600 units, all of them condos and apartments, defying any expectation of a slowdown.

Housing starts are an indication of construction activity, a powerful additive to the local economy with large secondary effects. Housing construction gets fired up by the promise of ever skyrocketing housing prices, and thus big payoffs for developers, lenders, real estate agents, and the entire industry.

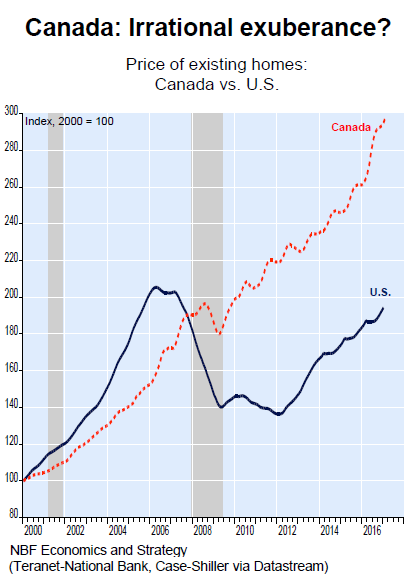

National home price data covers up the real drama in certain cities, particularly Vancouver (British Columbia) and Toronto (Ontario), but it does show by how much Canadian housing prices have overshot the already lofty US housing prices.

The chart below by Stéfane Marion, Chief Economist at Economics and Strategy, National Bank of Canada, compares US home prices per the Case-Shiller 20-City index to Canadian home prices per the Teranet-National Bank 26-market index. Both indices are based on similar methodologies of comparing pairs of sales of the same home over time. The shaded areas denote recessions in Canada. Note that during the housing crisis in the US, there was only a blip in Canada’s housing market:

Marion added in his note today:

Home price inflation has become THE hot topic of discussion in Canada. Surging prices are no longer confined to greater Toronto and Vancouver. As today’s Hot Chart shows, we estimate that close to 55% of regional markets in Canada are reporting price inflation of at least 10%.

This record proportion is very similar to that observed in the United States in 2005 at the peak of the market.

When 55% of the market is on fire, the use of interest rates to cool things down is justifiable. The Bank of Canada must change its narrative and abandon its easing bias as soon as this week.

He was referring to the Bank of Canada’s meeting this Wednesday.

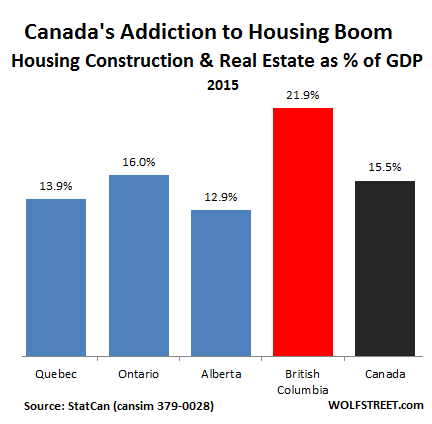

How important is real estate and housing construction to the Canadian economy? Hugely important! It accounts for an ever larger proportion of the Canadian economy. For all of Canada, according to data by Statistics Canada, housing construction and real estate activities combined account for 15.5% of GDP, up from 14.7% in 2011.

This chart shows housing construction and real estate activities in the largest four provinces as percent of the province’s GDP in 2015, and for Canada overall. StatCan data for 2016 are not yet available. Note British Columbia: 22% of its economy is based on residential construction and real estate activities – due to Canada’s number one housing hot-bed Vancouver:

This is why neither the Bank of Canada nor the governments at the provincial and federal levels are eager to step on the brakes. BC tried with its housing transfer tax aimed at foreign non-resident investors. After it was instituted last summer, it temporarily froze up the market, with sellers and buyers too far apart, and transactions plunged.

By December, only four months after the transfer tax was implemented, the prospects for 22% of the provincial economy heading into a sharp decline or even a major bust motivated the BC government to step back on the accelerator to prolong the speculation – with an ingenious trick.

The province began offering a subsidy to first-time homebuyers: an interest free loan for a down payment of up to $37,500 to match the buyer’s own down payment. It was an effort to allow buyers to get around the down-payment requirements set by the federal government designed to curb wild housing speculation.

It seems the BC government has figured something out: if anything curbs this housing speculation, on which the province is so dependent, the overall economy is going to tank.

Canadian cities are desperately dependent on property taxes for their budgets. Toronto, for example, is facing major budget strains. In February, city councilors approved a 3.3% increase in the residential property tax and they raised the municipal land transfer tax. Under the new budget, property taxes would provide 38% of the revenues, and the land transfer tax 7%, for a total of 45% of the C$10.5 billion in tax revenues for this fiscal year. In other words, the city will extract a record C$4.7 billion from property owners to delay falling into a fiscal and financial sinkhole.

That kind of tax extraction is bearable for property owners only as long as the value of their property soars year after year. Once that value declines, owning this property becomes a massive liability.

This is why the housing bubble and the accompanying crazy housing speculation must be maintained and further inflated, no matter what. It has become an addictive drug for the Canadian economy. Average household indebtedness is among the highest in the world. Many households are carrying little or no debt. But many others are suffocating under a mountain of debt, and a sharp decline in house prices would wreak havoc among them.

The entire economy – including government revenues and thereby the services offered by these governments – depends on wild property speculation. And everyone is praying that it can somehow be maintained

So are these prices based on fundamentals? You gotta be kidding. Read… Toronto House Price Bubble Goes Nuts

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

This is another holy cow our politicians step around just *s they do the big banks. And hey quess whose pockets also benefit here? As for others renting….coach surfing. Good luck..

Folks,

This is an ad from Alpine home capital.

“WHEN THEY SAY NO, WE SAY YES!

USE YOUR HOME EQUITY FOR ANYTHING YOU WANT

CALL US TODAY

1.877.834.9346

• No credit check

• No income documents

• Approved in 24-48 hours

• Taking out an equity loan or line of credit can also help to: cover medical costs, fund your children’s education, buy an investment property and/or to help cover other cash flow needs”

Does this sound familiar?

Recent news:

1. 54% of Canadians DO NOT believe that prices will ever go down.

2. The Ontario Premier – whose is at 10% popularity is panicking and says help is on the way for homebuyers.

3. Just about every major bank – BMO, RBC, CIBC have chimed in that we are in a bubble…..DUH!.

I have friends in their 40s and 50s who are languishing in debt. And I mean real bad credit card or LoC debt. Some just spent on fancy cars and a second vacation home, while others helped their children with a down payment of 50k or more.

Wolf – I have lived in the Toronto and the GTA for over 30 years – and I am starting to feel something different now. That this time is very different. Its that feeling people get before the tide goes out, just before the tsunami enters the shore.

Of course, I could be wrong.

But what if I am right?

Dude, it’s all good.

Suzanne Researched it!

There’s nothin’ but blue skies and good times ahead…trust me, I’m a Realtor.

Everyone will get a big laugh when the millennials and generation x’ers finally figure it out. They got suckered into copying what the Chinese do not knowing the repercussions. When they figure it out and then realize they’re the only cog holding up the housing market bedlam will break loose. Everyone will blame it on Poloz for cutting interest rates twice in 2015.

Especially with bubbles, always be the first to panic. I’ll collect my equity and step back out of this market. Trust me when I say, too few “get it”. I ought to know. I’m a Realtor telling any who will listen that now is NOT the time to marry a big fat debt. This time around it will be more than a housing bust.

I was forced to transfer 2 1/2 years ago due to the location I was working at closing down. I sold my condo and was seriously thinking of buying again in my new location until I actually thought about it.

I retire in approx 10 years so the only way I’d make my money back selling when I retire is if the prices keep increasing. I just won’t have the equity in the home and all my mortgage payments will go to interest so after 10 years it’s a wash if the house/condo doesn’t appreciate in value. And a loss if it depreciates.

The more I thought about it the more I realized that we do indeed have a bubble in Canada and taking on a large debt load that would pretty much just line the bank’s pockets might not be advisable for me.

It’s so easy to get caught up in the hype and think that the ride will never end. But a person has to ask themselves, like I did what happens if it does end. Instead I’m now totally debt free and have invested for my upcoming retirement while I rent a modest 2 bd apartment.

Sure if the bubble doesn’t burst before I retire I might miss out on potential profits. But I’m just not willing to gamble my future on an unknown outcome like this. Especially when I consider the fact that all bubbles eventually burst, it’s not an if but a when…

Of course this is also a very bad for the economy, when the population has to spend an obscene amount of money on shelter there is little left to spend on other things like autos, restaurants, shopping, etc. This speculation in properties is what helped sink the amazing boom in Japan 25-30 years ago.

You’re on to something and what everyone misses except me is think about it the millennials and generation x’ers have copied what the Chinese do (only in Canada). Basically the Chinese all do the same thing. The same is true of the Japanese race. Everything the Chinese touch no matter what it is becomes a pure 100 percent ponzi. Now that so many Canadians have copied the Chinese the flip side of the ponzi when everyone sells should result in the largest real estate crash in Canadian history.

Millennials are the ones getting the shaft. They don’t own houses right now, and if things continue they never will. When the economy breaks their restaurant industry and other service jobs will evaporate quickly. Why don’t Millennials seem to care about this? I haven’t seen much fight out of that group, unfortunately. They should have a respectable voting block by now. They could coordinate and vote out the bums who are causing this.

The majority of the buying I am sure is by immigrants and wealthy foreigners; which may be why we are not in a defined recession at the moment. Many new neighborhoods here resemble the United Nations, and millennials won’t take a stand because it’s not politically correct to.. (in the land of extreme politically correctness)

I can’t speak for other millennials, but the reason we don’t speak up is because we know it for the con it is, and we can’t see any way to “fix” it. Never mind that it’s our moms and dads that our going to be the worst hit. Maybe we secretly want everything to be OK. Some of the more cynical of us, frankly, are just waiting for the boomers to take the hit so we can rush in.

Add the fact that we’re a plurality – there’s conservatives and lefties among us, just like like you – just scrambling to find and keep jobs at all, and maybe you’ll see why we don’t really care about something that we have no control over, anyway, because boomers are still the biggest voting bloc out there, and they’re not budging a bit.

When wages don’t keep up with inflation and when immigration is high, millennials don’t have much bargaining power. The only ones who can save money in big cities are those without large mortgages.

http://www.cnbc.com/2017/02/23/uk-and-canada-closing-the-door-on-millennial-home-ownership-hsbc-study.html

Not sure on Canada, but in the US, I know a lot of active millennial trying to organize around local elections. However, we don’t have a lot of power as a whole – the same people who want to organize work 2+ jobs to barely make ends meet or a desk job where they are expected to put in a lot of time.

A lot of us went for Sanders but we saw how they played out. It’s tough to find candidates to rally around and we have so much information to fracture our party easily.

http://www.reddit.com/r/lostgeneration is one of the places they post a little. I think I got banned from it though.

I think they know what is going on but know there is really not much they can do?

The Millennials in Canada are their own worst enemy. They basically hung themselves due to their lack on knowledge not only on financial matters but in essence all walks of life. If they had of looked beyond the borders of Canada they’d notice Millennials in other countries don’t pay 3 to 5 times what a house is worth. When prices rises beyond a certain point sane people stop buying. The Canadian Millennials are in serious need of education.

How to end it?

1. Tax foreign purchases. These purchases do not have to be huge to have a huge impact on prices. Even if they are only 5%, they have a large impact because this is NEW money entering the system. This is not just upsizing, it is new money into the housing pool. There are times when this can be useful, but now is not the time. 20% sounds about right until things cool off.

2. Reduce immigration. Immigration is the big underlying driver. With close to 1,000 people a week coming and needing homes you have a guaranteed demand, again this is NEW money entering the system. With an over heated housing market, we do not need rapid immigration, especially as its side effect is a destabilizing of the stability of the economy (making everything too housing focused).

3. 20% down payment requirement. No ifs ands or buts. This alone would take the kettle off the boil, but would have additional impacts. Demand would drop and prices would drop and voila more affordable housing and easier to save a down payment for.

4. Mandatory disclosure on real owners of properties. No hiding behind shells or front buyers, with forfeiture for lying.

Unfortunately the low C$ is making real estate more affordable for foreign buyers. There is not much we can do about that other than taxing them to make up the difference.

Personally I prefer the Swiss approach to the problem . You cannot buy or own real estate / property , commercial residential or otherwise unless you are a citizen [ even inheritance is a but tricky if you’re not a citizen ] And it takes ten years of living in CH consistently to become a citizen .

I know people who own property in Switzerland but are not (that I know of) Swiss citizens. I think if you come in with enough money (“investment”), doors just open.

I don’t believe you. That is not true and you know it. Only possibility for foreigner to own in Swiss is after getting permit to own and that is restricted to tourist resorts, something similar to owning cottage out of town here in Canada. Foreigners are not allowed to own residential property in urban areas (cities, towns), regardless of how rich they are or how much money they might bring in.

I didn’t say it’s easy. But it’s possible, and plenty of people do it, including people I know:

“You can buy property if:

– you are an EU or EFTA national with a Swiss residence permit who resides in Switzerland; or

– you hold a Swiss C Permit.

In both cases, you will have the same rights as a Swiss citizen to purchase property, so you can buy business premises, investment properties or a holiday home, in addition to a primary residence.”

“Those who fall outside these categories, such as non-resident foreigners wishing to purchase property, foreign residents without a Swiss work permit (including those working for diplomatic missions, UN agencies and CERN) or workers on short term or seasonal work permits, may not be allowed to purchase property or may have to apply for a license to purchase. Licensing criteria vary from canton to canton but will typically favour applicants purchasing a primary residence who have been settled in the canton for five years or more.

http://www.expatica.com/ch/housing/Buying-a-house-in-Switzerland_100026.html

Millennials are the ones getting the shaft. They don’t own houses right now, and if things continue they never will.

Millennials look set to unseat the Boomers as the Most Worthless Generation in Human History. They voted lemming-like for “Hope n’ change Goldman Sachs can believe in” in 2008 and 2012, and got exactly what they voted for, i.e. shafted. You can’t fix stupid – they are going to have to learn everything the hard way.

Yeah, sure. I forgot what a no-brainer that McCain/Palin ticket was. lol

Oh yeah … a no-brainer alright . The brainless wonder Palin and McCain not using his brains by allowing the RNC to force Palin on the ticket .. especially in light of the fact that had he chosen an intelligent running mate rather than the idiot Palin he probably would of won . So yup … a no – brainer all around .

What, exactly, does who they voted for in Presidential elections have to do with housing markets being unaffordable?

Do you think McCain/Palin or Romney/Ryan would have magically waved their wands and *poof* housing is magically affordable and without any negative repercussions elsewhere?

You were right about exactly one thing in your post… you can’t fix stupid.

I agree Smingles. The president has nothing to do with housing. I keep hearing how useless millennials are. My kids are millennials as are their friends. They’re hugely successfull. It’s not uncommon for me to call them on Friday nights and they’re at work.

The housing boom is a result of free trade. I realize no one understands this but it’s not my job to teach people economics. Continually harping on young people is just plain ignorant.

it was once predicted oil would never come down from the triple digits. And some even predicted $200-300/barrel oil. Oil is now $50ish. Gold similarly suffered a similar fate.

What did we learn?? When prices are in the troposphere there will be a race to OVERsupply more of whatever people have decided to pay gravity defying prices.

Buy some popcorn and sour patch kids. This is gonna be a fun movie. The glut hasn’t even materialized yet. I speculate that to come in the late 20s. Then it will be a massive collapse as supply outstrips demand by 10x

Unemployed people in our Obama-Fed-Goldman Sachs “recovery” aren’t doing much driving.

Aren’t we already in the late 20s? I doubt prices will fall more than 30%…and a 30% decrease from these prices still makes things affordable. I am one of those that prices will not fall, or fall all that substantially. The government will support these prices, just like they support the stock market. The perfect example is what BC did re: helping with a down payment. They have many tricks up their sleeves that we aren’t thinking of. I have given up hope.

Heres what we know(US);

-Current housing prices are 300% higher than long term trend

-Current resale housing prices are double construction cost(lot, labor, materials and profit)

-Housing Demand is at 1997 levels

-Rental rates falling

-Rental rates 50% lower than mortgage, insurance, taxes and depreciation

The fundamentals are much much worse in Canada.

Now where do you think prices are headed?

With the exception of your post, there is a who lot of gloom and doom here.

What is so fearful about a booming economy as a result of falling prices? We all grossly inflated prices are the problem and the solution is falling prices to dramatically lower and more affordable levels.

Do any of you really believe wages(inflation) will magically triple or quadruple to meet grossly inflated prices?

Of course not.

Prices will continue falling to dramatically lower and more affordable levels meeting current wages.

“The glut hasn’t even materialized yet. I speculate that to come in the late 20s.”

Are you talking about late 2020’s? Are you for real? The weight of the high prices is about to snap so hard that Canadian and Australian housing prices will become a legend like the Dutch Tulip Mania, and you are suggesting that we have another 7-8 years to go? This is gonna snap like a wooden lever that is used to try to move a massive stone, and when it does, it is gonna hit Canadian and Australian a**** so hard, they won’t be able to sit for at least a decade.

I agree with you. The Canadian, Australian and Swedish housing bubbles are reminiscent of the Spanish, Irish and Cypriot housing bubbles of the previous decade. They will implode big time.

For supply to outstrip demand by 10X, oil companies would have to produce 900 million barrels per day. Given the fact that a “huge” find is 1/20th of ehat it was in the 60’s, that’s unlikely.

The current glut is due to more effecient fracking, something literally EVERYBODY, even the frackers got wrong. That said, all they did was add a year on a well that would deplete in 3 years. Hardly an earthshaking event.

The gold price downtrend had nothing to do with oversupply.

And do you really thing this housing bubble can run another 10 years?

Only 35 million people in Canada in a country the size of the USA. Plenty of room to run up housing prices.

The explosion in Canada’s beaver population has also kept housing inventory down, the nibbled down older buildings requiring immediate replacement with bear proof concrete bunkers.

I knew the collapse of the fur industry was bad news.

Beaver still costs dinner and a movie in Canada.

Actually have fond memories of Canadian Beaver,never forget that Bar in Vancouver ….ahh,never mind

When I built a house in 2006 in Germany it cost me about 200000 Euro to build it. 85 per cent of all the work was being done myself and with the help of relatives. That was the only way I could afford to build the house in the first place. Also I was one of the first in my community to ditch the basement. Simply could not afford it. I went back to Germany a few weeks ago and was told by my cousins, who are in various stages of just to have built a house or about to build one, that now one requires at least 300000 Euro to build the same kind of house. Thats what low interest rates will bring you.

Despite the fact that construction cost has ballooned enourmously my taxes on the property just got up 100 Euro at the most, in the last 11 years. Here in Canada it is different though. Everybody but the potential buyer profits from higher prices for housing. The municipalities, banks, realtors and insurance companies all want the prices to go up. There is also no real competition, since the realtors control the market. Just today a known realtor, that had adds plastered all over Edmonton got fined $96000 for misleading advertising and practice http://www.cbc.ca/news/canada/edmonton/real-estate-council-suspends-licence-of-edmonton-s-terry-paranych-1.4065086. Given the fact, that there are a lot of black sheep in the realtor business, no wonder prices are going trough the roof.

Terry would be better off collecting welfare. Edmonton real estate must be among the worst in the entire world the past ten years. Average resale condos and resale townhouses are down 50 to 60 percent from the peak way back in 2007 to the present time today. Resale houses have fared a lot better only down about 30 percent from the peak way back in 2007. The Edmonton housing bust from 2007 to 2009 was one of the worse in the entire world, now prices have fallen an additional 10 to 15 percent since then.

Immigration into Canada is well below the record set in 1913, when two of my relatives arrived, as part of the 400,000+ that came that year. In those days, immigrants settling in cities tended to settle in poor neighborhoods like “The Ward” in Toronto (comparable to the lower East Side of New York). These days many of the immigrants are wealthier than their Canadian born neighbors; the cities and the province of Ontario have imposed restrictive zoning and Toronto is saddled with rent control.

I suspect there is massive under reporting of worldwide income in Canada among the wealthy immigrants who still maintain business interests abroad while their wives and children live in multi-million $ homes in Vancouver or Toronto and report little or no income.

And Australia is even worse than Canada: https://www.youtube.com/watch?v=AUFn3LFsdQ8 (Fitch puts Australia housing on ‘alert’ — could Canada be next? )

Australia has two major problems which caused Fitch to balk.

First is the massive imbalance between the Western and Eastern parts of the country. The housing bubbles in Perth, Port Headland, Geraldton etc is gone and will deflate for years to come reagrdless of how commodities behave. At the same time Sydney, Brisbane, Melbourne etc are still in full bubble mode.

Second is the fact despite warnings to the contrary going back a decade, RE transaction and accessory services are exempt from the 2006 Anti-Money Laundering Act, meaning the whole Australian housing market is effectively at the mercy of what Australians call “Hot Asian Money”. If said money is barred from entrance by a change in legislature or, more likely, either Beijing finally starts getting serious about capital flight or Chinese nationals discover some new fancy investment, it won’t be pretty.

All it takes for a market to change is for 5% of the buyers to radically alter their buying patterns. Hot Asian Money means paying in cash and often full price, if not above it: we’ve all read stories about Chinese buyers in Vancouver trying to outbid each other. Apparently it’s some sort of sports among these people.

It works the other way: if that same 5% paying cash disappears or starts demanding big discounts, the market will change the oher way.

There doesn’t need to be a big burst: after all the craziest RE market in history (Japan) is still deflating outside the primest Tokyo and Osaka areas 27 years after the burst. There may not be much air left inside, but it’s still hissing out.

Friend of mine brought a nice 3 storey with garage In higashi Osaka in the late 80’s.

It went underwater a few year’s later and still is, ever since it went underwater he make’s the minimum payments and deliberately misses 1 or more each year Because he can. Nobody at the bank says a thing.

I quizzed him about this recently, its nearly 30 Years?? he said he financed it with a lifetime loan and the payments are still cheaper than renting the house.

In a continually deflating market, the last thing the bank wants, is more underwater properties on its hands.

In the US I believe the banks and reits brought up all that property to defeat the Japanese Deflation scenario.

long term I am unsure if they have won. Unless they can unload all the reits onto stupid “investors” at obscene overvaluations. But that simply moves the problem into the hands of said stupid “investors”

“At the same time Sydney, Brisbane, Melbourne etc are still in full bubble mode.”

Sydney is nuts; Melbourne is in bubble in certain areas – others are not.

And Melbourne’s population is booming.

Read all about it:

“In the year to last June, the Bureau of Statistics estimates that almost a third of Australia’s population growth crowded into this city – 108,000 more people – with another 16,000 settling in the regional towns and cities within commuting distance.

No Australian city has experienced growth on this scale before.”

SEE:

http://www.theage.com.au/victoria/bursting-at-the-seams-what-you-dont-know-about-melbournes-runaway-growth-20170406-gvewbk.html

Any wonder there is a huge demand for housing?

And in Japan areas outside of the big cities also has to do more with demographics than anything else: falling population in those areas.

A quick question: why is Melbourne growing at that crazed pace? What is that attracts immigrants there in such numbers, especially immigrants from China and India?

Lee is a real estate agent; so, I’d take the info he provides with a grain of salt. I’m not interested in Australian housing market; so, I wouldn’t waste my time on it. But if anyone is interested in his data, you should do your own research.

Good to know. Thanks.

What attracts immigrants from China and India? There is an element of market and corruption to it, but let’s not forget there are 7 1/2 billion poople on the planet and growing. Some places simple outgrew the natural environment. I could not say it better than sir David Attenborough.

“Three and a half million years separate the individual who left these footprints in the sands of Africa from the one who left them on the moon. A mere blink in the eye of evolution. Using his burgeoning intelligence, this most successful of all mammals has exploited the environment to produce food for an ever-increasing population. In spite of disasters when civilisations have over-reached themselves, that process has continued, indeed accelerated, even today. Now mankind is looking for food, not just on this planet but on others. Perhaps the time has now come to put that process into reverse. Instead of controlling the environment for the benefit of the population, perhaps it’s time we control the population to allow the survival of the environment.”

– D.Attenborough: Life of mamals

I dont see why people are so upset with prices going up 300% in Canada.

If you can build a shoebox for 200k and sell it to a chinese investor for 800k then I say go for it. Canada has lots of land and ressources, so lets build houses for foreigners,sell them at a steep profit and increase the property taxes. This is a win win for Canada and canadains. The local governments should be flush with money and full employment everywhere. Drill baby drill.

have you looked anywhere else they have let hosing bubbles burst?

Japan 1989 – never recovered

US 2008 – took out the global economy (derivative leveraging)

It never ends well, debt deflation is the problem.

hosing should have been housing as you may have guessed.

Catch 22.

To stop it now, causes a huge problem now.

To let it carry on, creates an even bigger problem later.

Let’s take the easy option and pray I am no longer in office when it blows up.

So where does the money come from to pay for the mortgages? If housing is in that kind of bubble than wages must be keeping pace or people are just racking up debt. So what collapses the house of cards? Anything that triggers the slightest tick up in unemployment

I hear that Justin just boasted that Canada will receive 30,000 “Syrian refugees”. In fact, this is resettlement of wealthy Armenian families from Aleppo, arranged by the local diaspora. So what you have is another wave of wealthy buyers. Locals will continue to be priced out.

Have you looked at Syria and Syrian refugees? Even if someone sells all his assets in Syria, all he can muster would be probably $50K. Assuming this is a rich guy. Ordinary Syrian refugees will need support for 5 years before they can have any income. Where do you people come up with these ideas?

Hamilton, Ontario, a small city about an hour from Toronto, received several thousand. It’s changed the character of downtown noticably and it was shabby enough before. Social services there are swamped. And they pull up to food banks in a car load of family and swamp the front give aways. I’ve seen them loading garbage bags with loaves of bread before being told to stop. Then they come back the next day and just do it again.

Syria is a war-torn country. There is no expectation of its people to be rich. Even if you had huge properties there, now they are practically worthless. So, even the richest people in Syria would at best be average if they exchange their money for a currency like the dollar.

This really reminds me a lot of what happened in Spain before 2008. The Brits were cashing out from their wildly inflated flats to buy Spanish retirement homes. Something like 1 million British emigrated there and they had similar statistics (something like 25% of their entire economy) around construction and real estate. I remember being on the ground there in 2008 when things were falling apart and the folks were telling me that everything was fine. We know how that turned out.

Canada looks very similar to the Swedish real estate bubble (for internet users you can find data at valueguard.se and bloomberg users can find data using ticker “SWRLPRIC Index”). Since year 2000 prices are up by 186%.

Swedish banks tend to be mentioned whenever “well-capitalised banks” are mentioned in Europe. However, looking at Equity / Assets the ratio is between 4% – 5% (so approx 20 times leveraged). This ratio has not changed last 20 years. The reason Swedish banks are supposed to be “well-capitalised” is that most of the lending goes towards real estate that has got low risk weights (no politician wants to pop a nice real estate bubble). The four biggest Swedish (SEB, Nordea, Swedbank and SHB) banks have got balance sheets that are approximately 400% of Swedish GDP. Consumer indebtness is growing approx 2 – 3 times faster than growth in income. The central bank has got the rate pegged at negative 0.5%….

If you are looking for an attractive short position for when the “everything bubble” pops you might want to consider shorting Swedish banks if / when swedish real estate prices start to flat line or decrease.

I’ve read quite a few comments about the Swedish banking system, from “it’s not gold all that glitters” to “Potemkin village”. However one thing that struck me is just four banks have balance sheets worth 400% of the GDP… by comparison the whole Chinese shadow banking system is worth between 90 and 95% of their GDP.

Children playing with fire is an apt metaphor.

Canada and Sweden has something else in common: a great advertised image for the outsiders. Let’s put it another way, a life boat in a sinking world worth any money.

Now Canada wants to “house” its radioactive waste in a pit one mile from Lake Huron. What is there about housing bubbles that makes nations greedy and stupid?

Human nature. It never changes.

It has become very clear that the manipulated low interest rate policy of the Bank of Canada has created a housing bubble in many cities across Canada. The Bank of Canada’s Keynesian policy of targeting interest rates in order to manipulate (rig) the free market to encourage people to spend and invest beyond their means or capability is threatening the housing market and economic stability of the country. Purposely lowering interest rates has created distortions in all markets and robbed savers and pensioners of an income on their savings. This is a disgrace. Every great free market economist knows housing price inflation will lead to severe consequences for Canadians. The dream of owning a home in these cities is becoming unattainable , especially since wages have not kept up with housing inflation. See Graph. Depressed Interest rates for an extended period of time is the biggest driver in housing price inflation. See graph below. Rates have never been this low for so long in the history of Canada and the world! Real interest rates are currently negative at –1.5%. { the overnight interest rate (.5) less inflation (2%)} In addition, the Canadian dollar has fallen to .75 USD since lowering the overnight rate from 1% to .5%, or a 50% reduction in rates. This means a 25% reduction in purchasing power for all Canadians buying US products/services and anything priced in US dollars. See graphs below.

Image result for housing prices vs wages in canada Image result for Toronto home prices chartImage result for interest rates and toronto home prices

Related image Image result for interest rates over 3000 years Image result for Canadian dollar vd USD

Bank of Montreal and other financial institution also confirm the housing bubble. “Let’s drop the pretense. The Toronto housing market — and the many cities surrounding it — are in a housing bubble,” BMO Chief Economist Doug Porter wrote in a note to clients Tuesday. http://www.bnn.ca/bmo-declares-toronto-housing-bubble-amid-dangerously-hot-prices-1.672542

Clearly, The Bank of Canada’s low interest rate policy is failing and therefore must change. It must raise interest rates to free market levels to avert severe market distortions and destabilizing economic consequences. The US has started on a policy of monetary tightening and interest rate hikes. Canada should follow its lead. Don’t you agree?

P.S. The government puts out the inflation rate figure using the Canadian Price index (CPI), currently at 2%, but the everyday things most Canadians buy, like food, housing/renting, insurance, utilities have gone up substantially much, much higher that the CPI.

“It has become very clear that the manipulated low interest rate policy of the Bank of Canada has created a housing bubble in many cities across Canada. ”

Blame televison, the internet, the 24/7 news cycle and easy credit. Advertisements tell us we should have it all now, politicians need the votes now, and developers want the money now. There is no force pushing back the other way.

Prior to the 1980s the urgency to douse the economy with hot money did not exist.

The housing bubble is a crisis of fast news flow and hyper consumerism. It is a mental disorder.

I live in Canada, province of Quebec. This confirm what I thought. Canada is a empty fake economy supported only by three pillars. First and most important pillar, housing and cars loans bubble (debt bubble), followed by oil sand production and finally auto manufacturing in Ontario. These are the three man pillars of the Canadian economy. There is no creativity in Canada and no sense of entrepreneurship in Canadians.

The other day was looking for a portable cheap low end oscilloscope to troubleshoot my car. I end up buying something made by a Chinese company for the Chinese market. I still cannot believe the lack of entrepreneurship from Canadians. I was really surprise of the quality for the low price I paid. Canadian just want to sit there and drink beers.

In a real economy with no trade barrier, cannot will no survive.

“I still cannot believe the lack of entrepreneurship from Canadians.”

Walk into any start up and count the number of Canadian engineers versus foreign. The ratio might be 5 to 1 like where I work. So integrity goes straight out the window first. Second, no immigrant new to the Canadian job market is going to take a risk of failing. They invested far too much just to get here. There goes your innovation. Everything is very short term oriented. Make your nut and move on. And if it all blows up there’s always home to go back to. It’s an entirely different field from 30 years ago.

Allowing foreign capital inflows to influence real estate prices is a dangerous precedent. Seems that this is the new paradigm within many western countries. It would seem that any sovereign nation would assure affordable housing for its citizens. But such inflows bolster the nations capital account. Also it is a denial that structural/fiscal policy changes are needed . It is politically easier to rely on monetary policies for economic sustainment . In regard to the above narrative , the province of BC just made it easier for a canadian citizen to buy an inflated asset with a down payment loan . The transfer tax was not given enough time to work.

Just walk down Yonge Street from Bloor, the center of the city, and it will look like a red light district. It is really rundown all the way down to Lake Ontario. I don’t know if anyone would want to live there. https://www.youtube.com/watch?v=JMhdees45O8

I noticed that Bill Morneau didn’t do much to curtail the situation in his recent federal budget. When real estate seems to the main driving factor in our GDP, wouldn’t you think there’s something wrong here?

In the upcoming Provincial Ontario budget, Premiere Kathleen Wynne is spewing out threats but with an election on the horizon, we’ll see how far she actually goes?