If history is the guide, you’re on your own.

The Fed has planted three separate warnings on high stock prices into its March-meeting Minutes, released last week. In the past, the Fed has warned on various occasions on high stock prices, with, let’s say mixed results. Stocks have crashed after warnings, and they have crashed without warnings, and they have soared after warnings.

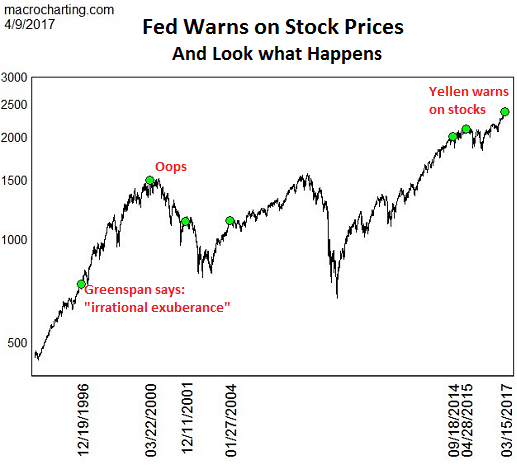

Perhaps the most infamous warning on stock prices was when Fed Chairman Alan Greenspan on December 5, 1996, said in a speech that “irrational exuberance has unduly escalated asset values.” Stocks quaked in their boots for about one breath then soared for another three years and three months before totally crashing.

So now we’re getting a slew of Fed warnings. The most recent – three of them at once – were spread across the Minutes of the March meeting:

Broad equity price indexes rose further, leaving some standard measures of valuations above historical norms.

[…]Broad U.S. equity price indexes increased over the intermeeting period, and some measures of valuations, such as price-to-earnings ratios, rose further above historical norms. A standard measure of the equity risk premium edged lower, declining into the lower quartile of its historical distribution of the previous three decades.

[…]Many participants discussed the implications of the rise in equity prices over the past few months, with several of them citing it as contributing to an easing of financial conditions. A few participants attributed the recent equity price appreciation to expectations for corporate tax cuts or to increased risk tolerance among investors rather than to expectations of stronger economic growth. Some participants viewed equity prices as quite high relative to standard valuation measures.

And here is what Greenspan said on that fateful December 5, 1996. Note the implications as he saw them for monetary policy:

But how do we know when irrational exuberance has unduly escalated asset values, which then become subject to unexpected and prolonged contractions as they have in Japan over the past decade? And how do we factor that assessment into monetary policy?

We as central bankers need not be concerned if a collapsing financial asset bubble does not threaten to impair the real economy, its production, jobs, and price stability. Indeed, the sharp stock market break of 1987 had few negative consequences for the economy.

But we should not underestimate or become complacent about the complexity of the interactions of asset markets and the economy. Thus, evaluating shifts in balance sheets generally, and in asset prices particularly, must be an integral part of the development of monetary policy.

Upon Greenspan’s warning, stocks barely wobbled long enough to notice before they skyrocketed into what would become the Dotcom Bubble … and the Dotcom Crash three years and three months later. While Greenspan might not have worried about falling stock prices per se in his speech, he still got cold feet deep into the crash and radically lowered interest rates, thus kicking off the credit bubble that also contained a housing bubble, all of which collapsed.

So how did stocks behave after warnings from the Fed? This chart by John Alexander at Macro Charting shows the S&P 500 Index going back to the early 1990s. The green dots signify Fed warnings on stock valuations:

“Sometimes it’s a sell signal, sometimes it’s a buy signal,” says John Alexander. And sometime it’s a crash signal. So how long before the stock market hits the wall? Turns out, it’s overdue…. This is Worse than Before the Last Three Crashes.

But here’s the thing: there is so much liquidity out there, supplied to this day by central banks around the world that it would take some doing to get a crash going. In recent years, market participants have forgotten the lessons of the crash and have re-learned the lesson of the bull market: just buy the effing dip. When applied with enough enthusiasm by humans, and if enough trading algos have been programmed to do so, it stops the crash, at least for a while.

Thus it’s unlikely that stocks can actually crash all in one fell swoop, as they did during the Financial Crisis. It’s more likely that, once they decide to head south, they’ll work their way down gradually, frustratingly, and nervously, spread over years, not because of the Fed’s warning, but because of the myriad reasons lurking around every corner, such as the ludicrously stretched valuations, the Fed’s tightening including the unwinding of QE starting later this year, and the bitter end of the credit cycle.

There have been big red flags about the bitter end of the credit cycle: Commercial bankruptcy filings, from corporations to sole proprietorships, soared 37% over the past 24 months. Read… Great Debt Unwind: Consumer Bankruptcies Jump, First since 2010. Commercial Bankruptcies Spike

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

It’s interesting that you’re not the first person that has put forth the idea that stocks may grind down slowly over an extended number of years.

Today, the p/s ratio of the S&P 500 is 2.07 as per multpl.com, compared to a p/s ratio of 1.58 in October 2007.

Back in 2007, the general sentiment was that real estate was in a bubble. However the S&P 500 dropped 58%.

Today it appears that the bubble is even more universal and widespread than in 2007.

So maybe you are right. Perhaps the world’s assets will slowly deflate in value just like the Nikkei did from 1990 to present.

Interestingly, Japan’s GDP grew at a 15% CAGR between 1965-90.

China’s GDP grew at a 15% CAGR between 1990-2015.

There are now numerous auto trading bots that react from programming in recognition of movement patterns rather than stock value int he traditional sense. There may never be another crash at all on account of their use.

This time it’s different. Autobots can frustrate any evaporation of liquidity. When the rats jump the autobots will catch them in nets and return them to the ship. Buy the dip.

We need to pick a day when everyone types in Stock market crash” in Google at the same time.

Couldn’t that fact make the crash even worse and far faster? “flash crash” much?

Of course it would make it ‘worse and faster’

It’s strange that anyone would imagine that computer trading programs would counter rather than amplify a big sell- off.

In ‘Flash Boys’ by Michael Lewis he describes the tech race to have the fastest possible trading platform- permitting it to ‘legally’ front run the market up or down. There are few contrarians among the bots.

The Flash Crash has been investigated. At first human action was suspected, either a ‘fat finger’ i.e. a mistake or possibly an intentional act by a pool of shorts.

It was auto- selling programs that drove the market down over a thousand points in seconds.

The event known as the Crash of 1929 took a week and one day. The first really bad day was October 21. By October 29 the bankers gave up trying to stabilize the market with ‘organized support’ and an errand boy on the exchange put in a stink bid ‘of one dollar for a share of White Sewing Machine which had been 48 a few months earlier and had closed at 11 the night before. He got it.’ (Galbraith, The Great Crash)

But it took 4 years before the result (?) we call the Depression ground away the international financial system, to the point where Britain could no longer meet its US debts.

In 2008, when Lehman declared bankruptcy, it looked like world finance would collapse that week. And it almost did.

Things happen faster these days.

I agree that the trading bots have changed the equation. The result is likely to be a different picture than it ever has been before. However, I think the chance the bots will let the bottom drop out completely in a moment is higher than the chance that we will never see another crash.

Yes – Remember Ghostbusters… don’t cross the streams. from my observation, looks like the programs create fake bid / asks that never actually execute, controlling the price. looks like the program breaks down when the phony bid and asks cross each other, creating those flash crashes. never say never… yes, the creeps will continue to print wealth for parasitic paper billionaires and their lackeys on the backs of the masses via inflation/ deflation. suppose this game will go on until finally it does not any longer. then everyone will be very sorry that they turned their backs on real capitalism real market through price discovery, but that is total BS. these creeps are parasites who only care about lining their own pockets. sure if the SHTF they will pick up like most parasites do and fly away to feast somewhere else.

Just remember these creeps don’t mind sheering the sheeple. their rigged casino works well for the melt up now but can change direction in seconds. the biggest loser in a rigged casino is real value out there but very blurred in rigged corrupt markets.

The biggest US players have been contracting their wholesale credit,

since 2011. From just under $ 500 Trillions to about half.

Commercial loans are contracting for a while.

The FED is planning a contraction of their balance sheet, when or

how is up to them.

Or, it’s another part of their campaign in building future

expectations, an attempt to cool down the market. Fake news.

The new “Real Bills” market, The market of mfg. producing their

finished product, ship to their retail customer, sell & get paid,

all of that in LESS than 90 DAYS, is showing some cracks.

In the automotive industry, inventory is piling up, beyond 90 days,

you can still find promotion of some brand new 2016 models.

Defaults are rising and that clog the lending of credit domino.

The contraction of the global, wholesale credit, affect many banks,

offshore and slow down the global trade.

Nothing to do with president Trump.The Fed was planning a

contraction since 2011. They had repeated to announce loudly of

their intention in 2014.

But the stock market, in contrast to all experts and Mr. know all,

moved up, way up.

To sum it up :

the Fed printing of money do not affect the economy. Banks

expanding / contracting balance sheet does.

The Fed talk like monkeys in a cage. The markets ignore them.

Remember when markets moved based on fundamentals, not on central banker bloviating?

Neither do I.

I’ve never understood the concept of financial market fundamentals. Financial markets are just speculating on asset prices. It is just trading. Financial markets aren’t a wealth creation engine, like actually building a product somebody needs.

How does one apply a fundamental value to speculating?

Kent,

I think you’d have to go way back to find a US market based on fundamentals………….maybe in the early 70s was the last time you’d find such a market for US stocks.

Ever remember going to the public library and spending a day looking at the financials in the old hard cover Moody’s? Book value? Cash vs debt? Finding those companies with land valued at cost, but worth a fortune?

And as far as ” Financial markets aren’t a wealth creation engine” I guess it really depends on who you are – more specifically – how much you own.

For those that lots of stocks or a large chunk of a so called ‘public’ listed company the stock market has been a wonderful tool for you. You know the 1%.

For others that don’t have a stake in the system anymore for one reason or another it means nothing.

Instant billionaires based on some kind of pie-in-the-sky new fad technology that gives those people an idea that they have something intelligent to say about other facets of life or politics in the country.

Another area where ‘fundamentals’ and real value are lacking.

It’s worse than being “on our own.” The Keynesian fraudsters at the central banks are actively complicit in helping their insider .1% pals rig and manipulate these broken markets to bilk retail investors.

http://www.marketwatch.com/story/bank-of-england-pressured-banks-to-rig-libor-secret-bbc-tape-reveals-2017-04-10

It IS being on your own since the government has been corrupted by corporatists cronies. So Keynesian? Not really.

The Fed cannot sell, because there are no buyers.

Negative rates are on the way up.

Investors of the buy & hold type got squeezed out of the markets.

$ 3 Trillions in government bonds moved from negative rates, to

above zero.

The Fed cannot swim against the trend.

Dr. Zanet is not an Iron man.

Their best option is to allow their assets to expire in maturity.

You may have noticed

“Their best option is to allow their assets to expire in maturity.”

is what they are slowly doing.

And its also has the same effect a small incremental rate rises lits just not a publicly noticeable.

There are three huge balls of printed money rolling around the planet. from bubble to bubble causing mayhem. 1 CNY, 1 EUR and 1 US $.

only the US $ one is even shrinking in a minor way. global trade and teh global economy can not pick up until these balls of money are eliminated by, 1 deflation, 2 inflation or 3 central bank tightening.

The fed is trying for gentle 2 and 3 in combination. So that when the bubbles go bang, it and the US $ will still be strong.

I am a buy and hold type and I have not sold a share of my major oil company in forty (40) years. The dividends fund my retirement…thank you. What is talked about on this site and every other one is trading….a form of gambling. Might as well buy lotto tickets or SNAP.

Karl,

Your post reminded me of a long time ago when I first started buying stocks.

There was a broker at Piper, Jaffray, and Hopwood who was always pushing Exxon……………..

Wish I had listened to him!!!

The Fed is planning to reduce debt.

That a reduction of UST and mortgage debt. Great.

When Us government debt is going down, it’s a sign of a good

economy. No budget problems of raising debt ceiling.

Friendly talks with the austriporosis on the other side.

No problems to finance defense, infrastructure and existing

obligations….

Budget talks will be smooth. No risk of government shut down.

No RISK on the horison. Nothing as far as you can see.

Yet, risk future for the next 10 days, that include some major

holidays, is higher than the risk future for the next 40 days and

only slightly below the risk future of the next 75 days.

But there is absolutely no tension on the horizon.

Shake hands cured all friction, globally.

The market plateau at high level. No tremors sounds.

The only tension that some could detect was between the first

lady and prime minister Iva.

And One Bullard Save outweighs 100 comments in Fed statements. Just wait for it. The markets expect it as soon as the number start to go bad. Too many friends of bankers depend on the status quo remaining this way. The Fed is a creation of banker intended for bankers and run by bankers. Bankers want a fair game only if they can benefit from it more than from a fixed one. Everything else is theater.

Stocks won’t drop until liquidity falls significantly and rate management ends. I wish it were different and, in a textbooks world, equities would be lower and rates would be higher. This is not a textbook world.

Actually we are in a textbook world. One of the Potemkin village and debasing the coinage variety.

The game is the same as always- how to tax, tithe, or steal goods and labor from the working class.

First part ; Exactly ! Potemkin Village / ” Emperors New Cloths ” sums it up quite nicely . But err .. tis more literary fiction verging on fantasy than ‘ text book ‘

Second part ; Close but no banana . You’re assuming there’s a strategy or motivation of any kind behind it all … when in truth they believe they’re in control … playing by the seat of their pants according to the Gospel of Ayn Rand with every move they and their tradebots make hoping beyond delusion to keep all the balls floating in mid-air not crashing to to ground in order to maintain their place in this very Class oriented world all while ignoring the fact that twas ( and still is ) the upper middle , middle and working class buying the goods and services they offer that created their wealth .

And in the end what can we do about it ? Other than hunkering down … and attaining a sense of Zen ” Wisdom of Insecurity ” ( by Alan Watts ) Not a goram thing . Cause the fact is as little ( if any ) control that ‘ they ‘ have … we have even less .

I just looked up ‘Potemkin village’. Good analogy. An effective substitute for reality. The media with their Trump hatred has proven, quite obviously, that fantasy outweighs fact if managed and marketed correctly. Loud pervasive repetitive blanketing noise becomes fact and the status quo. Hence the reason a Bullard Save is so effective. The stock market level combined with media whitewash equals a strong economy.

“There have been [and are] Big Red Flags”…

Fundamentals:

Since 2008 the national debt has doubled.

Student debt has surpassed one trillion dollars, with more than one in four student loans in default.

Auto loan debt has also surpassed one trillion dollars, with over one million loans now delinquent.

Residential real estate loans have now topped 14 trillion dollars.

Average total debt per household has topped $100,000

Bubbles are everywhere, with the largest being the global bond bubble which is the largest in the history of the world! When bonds are bought for capital appreciation, then they are going to trade like a commodity.

The stock markets are shrinking. The number of common stocks traded on major exchanges are the lowest since 1984, this according to the University of Chicago, Center for Research in Security Prices.

There are only five, largest stocks traded by capital weight that are all tech stocks and account for the largest portion of value. This market has been the fourth narrowest stock trading range since 1928, with the range smaller only in 1958, 1964, and 1965.

These financial “casinos” that insist on calling themselves “markets” are nothing more than houses of chance. Where the odds are always tilted in favor of the house. The coming crash will be epic.

Now that kind of talk gives me goosebumps. I think more debt will be taken on by consumers. I read HELOCS are increasing… why….because the increase in home prices have created free money again. M credit union is offering HELOCS up to 100% of my home. 3years ago they would only do 60%.

Also….houses are selling in two days after being listed. Realtors are telling clients to give their best offer 24 hours after the house 1st day on the market. 3,houses on my street sold like that. Price 15% over peak 2000s prices. This is in flyover land in the mid west that is not a technology hub.

“It’s more likely that, once they decide to head south, they’ll work their way down gradually, frustratingly, and nervously, spread over years,”

The only time that I am aware of this happening in the US was in the late ’60’s and into the ’70’s. But that was a period of extraordinary economic issues: inflation, the end of Bretton-Wood, and peak US oil production to name a few.

I tend to believe people need the stock market to go up and it does so based on that desire. Not to mention it is more difficult and risky to short stocks over the long term than to buy and hold.

So my guess is it will hang on until something out of the blue happens. And that will have to be something that puts the banking system in danger again. It will likely be some overly-leveraged, stinky asset class goes tits up and nobody knew that it was worth $10 trillion and all the big banks were in it way deep.

“The only time that I am aware of this happening in the US was in the late ’60’s and into the ’70’s. But that was a period of extraordinary economic issues: inflation, the end of Bretton-Wood, and peak US oil production to name a few.”

And before the huge piles of consumer debt including student loans and autos.. and record high house prices… hard to have inflation in this kind of atmosphere with out tipping over the apple cart.

Cyclical activity is not always a bubble. Today’s cycle peaks are not in the realm of previous bubbles. And they are not aligning with each other as in the past.

The impact of the aging Millennial generation is being underestimated in many regards. There is tremendous pent-up housing demand. Millennials are also moving into an age group of rapid wage-growth (approx 22-32). Household creation is going to grow.

Don’t you think the pent up demand for houses by millennials will be satisfied by the over-availability of Boomer houses due to moving to assisted living facilities and death?

The Boomer pull-out of housing is real but delayed as much as possible (reverse mortgages, etc) and not evenly spread across the country. Not until boomers begin hitting 80 will they be more likely to exit their homes. Plus Millennials are more urban, car-averse, and won’t snatch up rural boomer homes.

Saw a 60 Minutes piece on how the tech industry is using neurosciences to make smart phones addictive because the number of ads viewed is their income. They have, especially with the Millennials, devised an addictive quality to their phone apps. If you notice, people addicted to smart phones have one in their hands almost all the time. They get nervous and can’t concentrate if they haven’t looked at their phone in a few minutes. Thus many Millennials have a hard time working or forming close social ties. This could account for why so many live at home and why the formation of families at their age is so far behind other generations.

Interesting to think about.

Fed creates bubble. Fed warns of bubble. When it explodes, the Fed will get busy creating a new one.

The Fed since it’s clandestine 1913 creation by the robber barons of the era has had just one purpose: to serve as the oligarchy’s chosen instrument of plunder against the 99%. Engineered boom-bust cycles every few years are the most efficient means to transfer the wealth of the disappearing middle class to the Fed’s .1% accomplices.

http://endthefed.org

90% of this worlds problems because of the ” FED ” and Rothschild’s ” other ” Central Banks , IMF, UN, World Bank and the list of Parasites goes on .

My sense is that these statements are being embedded so as to inoculate the Fed if/when things head south. It’s for future purposes of misdirection.

“You see, we did issue warnings!”

Now, carry on…

“But here’s the thing: there is so much liquidity out there, supplied to this day by central banks around the world that it would take some doing to get a crash going”

Truer words were never spoken Wolf. Now, go back on TV and scream it. These people are flooding the world with money and destroying balance sheets. UPS, FDX, F, PEP… these stocks should be half their current valuations

Liquidity = debt = money

For all the liquidity there is some form of debt enabling it. We don’t have sound money backed by gold or silver. We have money that was totally created by creating debt.

As defaults occur, the debt behind them gets written off and this will reduce liquidity. Write off enough debt and there will be no liquidity. Then the defaults will accelerate. Unless the CBs are willing to put the additional debt on their balance sheets. And fast enough to stop it.

Another time, it will be interesting to watch as there isn’t a damn thing we can do about any of it.

Right now we are peaking… or close to it.. and Congress has to raise their debt ceiling very soon.. And they decided to go on vacation instead. I guess they have a plan.. hahahahahaha! ROFLOL!

p.s. what happened to the follow these comments box?

China’s financial system is being kept alive minute by minute, with the central bank supplying a dwindling supply of dollars when needed. If it should stumble, watch out. There won’t be a slow decline in stocks then, but a drop off a cliff. And the Fed won’t be able to do anything to stop it. Right now, playing the stock market isn’t just gambling, it’s a game of Russian roulette.

Yellen the Felon is getting massively trolled on Twitter after accepting questions from the general public. Oh, the humanity!

https://twitter.com/hashtag/fordschoolyellen

May looks to be shaping up for downside chances, still some upside momentum given cash on sidelines they’re gonna chase for now.

IMO

The fed anticipated the need to boost overall returns as the great recession dragged on. It realized that boomer pensions were important long before the boomers did?

Now with company pensions seeing strong gains in risk and the need to be more conservative they sell stock and buy more bonds?

Hence a possible answer for stock buybacks and corporate debt issuances on a grand scale?

If government debt becomes more attractive as the dollar falls, than corporate debt must be triple good? (until fed can prove higher rates are good for the economy?)

Beware; everyone in Europe loves Europe!

Equity markets levered way up, multi-trillion junk bond bubble, > 1/2 trillion NYSE margin debt, ECB buying corporate bonds fueling buybacks,

& revenues, earnings flat for years. No growth. C&I loans no longer growing? Looks like a bad mix, and bad signals keep turning up.

Wonder what insider information the Fed is giving to its Wall Street partners in crime behind closed doors.

http://www.businessinsider.com/federal-reserves-fischer-held-private-talk-at-brookings-2017-4