I hope the model is wrong.

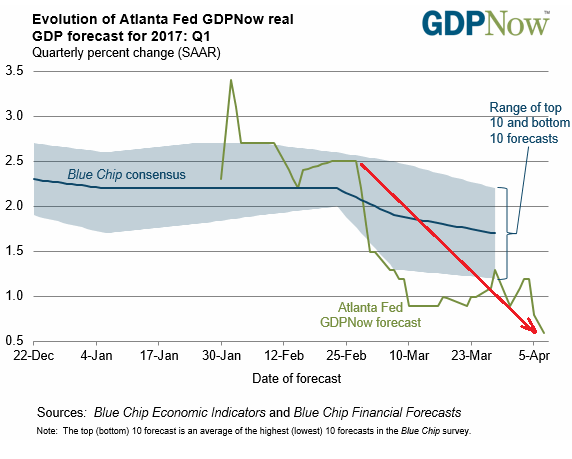

The Atlanta Fed’s GDPNow model, which forecasts GDP growth in the US, dropped to 0.6% seasonally adjusted annualized GDP growth for the first quarter. This means, if economic growth at this rate continues for an entire year, the US economy would edge up only 0.6% for the year.

As more data for the quarter is released, the model becomes a more accurate predictor of GDP growth, as measured in the first estimate for that quarter by the Bureau of Economic Analysis (BEA). So now the first quarter is over, and more data for the quarter is piling up, and the GDPNow forecast is spiraling down in direction of zero.

The forecast dropped by half from April 4, when it was still 1.2%. I added the red arrow to the chart to show just how fast and how far it fell in the past seven weeks, from 2.5% to 0.6%:

The GDPNow model aggregates forecasts of 13 sub-components of GDP. These are the factors that caused the slide since April 4:

- April 5 – Data on light vehicle sales from the Bureau of Economic Analysis: This parallels to some extent my coverage of the auto industry that is now at the cusp of sliding into a nasty quagmire or worse.

- April 5 – ISM Non-Manufacturing Report on Business, a measure of the service economy: the index dropped 2.4 percentage points to 55.2 in March (above 50 = growth, so this was still growth, but slower growth than expected).

- April 7 – Wholesales trade report by the Commerce Department on wholesales and inventories: sales up, inventories up too.

- April 7 – Employment report: only 98,000 jobs were created in March, a little over half of what economists were expecting.

The Atlanta Fed’s model found that since April 4:

- The forecast for first-quarter inflation-adjusted consumer spending growth dropped by half, from 1.2% to a miserable 0.6%.

- The forecast for first-quarter inflation-adjusted nonresidential equipment investment growth dropped from 9.7% to 5.6%.

So how bad is annualized real GDP growth of 0.6%? It’s less than half the miserable 1.6% growth rate of 2016, which had matched the lowest growth rate since the Financial Crisis. So anything near 0.6% would be the worst since the Financial Crisis.

It would also be substantially below US population growth. Hence, per-capita GDP, which is how individuals experience the economy, would actually decline.

A month ago, when the Atlanta Fed’s GDPNow model spiraled down to 1.2%, I wrote: “We hope it’s just a brief dip in the data.” But that dip wasn’t brief, and it just got deeper.

The GDPNow forecast does not at all jibe with the business and consumer sentiment surveys that have jumped to multi-year super-optimistic highs since November. Economists and Wall Street have put a lot of faith in this magnificent ebullience as driver of consumer and business spending. And stocks have soared. But the data piling up show once again that sentiments are just sentiments. Reality is another matter. And reality for now in the first quarter is a pretty dreary affair.

Venture Capital gets prudent – with consequences. Read… Startup Craziness Deflates, Hits Silicon Valley & San Francisco

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf, How do we cash in on your insightful analysis, what do you suggest we buy, not buy or hold?

Suggest you buy a ticket to Vanu Vanu.

Here is some data to help you make a decision on what industries to invest in: https://www.aar.org/Pages/Freight-Rail-Traffic-Data.aspx

Scroll down to the Monthly Rail Traffic Data. Check out the petroleum products and auto buttons. As you can see, there is some funny business going on with GDP data. Also note: The BLS revised January and February hiring data down. Best of luck!

I have heard a lot of oil pipelines have been coming online. That may be why petroleum products are not being shipped on rails.

Or at least Tasmania or Fiji

If you want someone to pick your stocks for you, go see Jim “Jo-Jo the Clown” Cramer over on Moneywatch. Of course, such permabull touts and shills might just cost you your life savings, as Cramer did when he told the bag holders “Bear Stearns in fine!” before it crashed from $60 to under $2 back in 2008. No ethical blogger is going to be making stock pick recommendations – do your own due diligence.

BOO-YAHHH

Laker, I don’t do financial advice as a matter of principle.

But I’m thinking about starting a new enterprise, something like “Get Rich Quick Financial Advice.” I would charge clients $1,000 a minute, billed in minimum increments of one hour. This way, clients would get their financial advice, and I would get rich quick :-)

What a 1980’s style business model this is! This approach requires recruiting customers with some wealth, getting their money, answering their probing questions, and finding assets to invest to generate returns. This is a lot of hard work! Also, those rich people are very pesky with giving up their money. In the end, you’ll get caught and end up in jail a la Maddof. If you are Twitter founder and you don’t care about reputation about how your creations die with you at the helm, this is a way to go.

An easier business model will be to recruit a ton of penniless individuals on social media, buy a thousand twitter accounts to constantly sing about how much returns you are earning them, and supply reporters from NYT, WaPo, CNN, and WSJ with wine and wo(men) or whatever tickles their fancy. They will legitimize your (worse than Ponzi) scheme and make it mainstream. All you need to do is get some VC to invest a couple of million, to which you will then add a few thousand dollars every hour until your company is a unicorn. You then go IPO or sell yourselves to Fidelity types (or anybody who has invested in Snapchat/DropBox/Uber/AirBnb or any other company whose valuation grows by a 1000$ every hour). In this model, your clients don’t get completely fleeced (Fidelity will work hard to ensure returns on the junk you left behind), you don’t become a Ponzi incarnate, the investors and you both get rich. With the stocks that you can create nilly-willy, you buy political connections and make sure you don’t end up in jail. You can even run for office someday.

Notice how both these models increase net worth by a 1000$ every hour. When you do get rich, just throw a bunch of those stocks over the transom at my place. I will be grateful like a lot of people who happen to invest privately in the right start ups in the valley at just the right time and seem to be able to read tea leaves correctly (yeah, right!).

You can do that in a way by going city-to-city putting on financial seminars to crowded rooms. Don’t forget that you will need to hire some well known retired general to help you hype your sales.

AKA CNBC. and so many other so you might need to rethink the 1 k per min rate, The market is vey crowded..

If you were really like that you would probably still be selling finance agreements and service contracts, attached to new and used cars.

Here’s the financial advice the very top levels are following: “When the chips are down distract with a small war – then, if conditions persist, escalate to a big war”.

There is a sight online that picks stocks related to a theme or an idea and is relatively inexpensive.It is called MOTIF. Check it out.

Hold onto your cash, get out of ALL debt and liquidate whatever you have to stay out of debt. You’ll thank me later.

Good advice but I would diversify with some precious metals perhaps 20 percent

“get out of ALL debt ”

facing an implosion that is no the play.

The play is to have the liquidity to eliminate all debt.

As in an implosion, lenders will settle for less than total due, to get cash NOW.

Liquidators will frequently settle for less than lender’s.

https://www.investing.com/etfs/market-vectors-junior-gold-miners

When stocks tank, gold flies.

“When stocks tank, gold flies.”

Maybe but in a deflationary cycle, everything goes down except cash.

We have yet to see a truly deflationary cycle but the opposite of a debt peak is a deflationary cycle. The PTB have been able so far to prevent this from happening with new additional debt but there will be a point where all the future profits have been spent and the only thing left will be deflation.

In deflation, there are few who actually have cash money. Most people were so enamored with the tapestry of looking wealthy, having a new car, a home, vacations and all the newest electronic toys that they don’t have much or any cash. Or all their income was spent in surviving. Also in our present environment, cash pays nothing so most is invested..

So when there is little cash around, even gold loses value because there are few with currency to purchase it with. A true deflationary cycle, which we will have eventually as it is the ONLY outcome of a debt binge, means all assets drop in value.

Not totally true If there’s fear of a dollar implosion commodities especially gold and silver could explode in value The fear of war could also factor into it

With Yellen the Felon hellbent on printing away all government and Wall Street debts and liabilities, while lavishing trillions in printing-press “stimulus” funny money on the Fed’s Wall Street partners in crime, physical precious metals are the only safe store of wealth for the 99% who are going to see the purchasing power of their dollars debased into worthlessness.

Not true at all. In the 30’s gold and gold stocks did very very well.

Much bigger bubble today and there was virtually no consumer debt then.

So we’ll just have to see what happens.

I do have my stash of gold and silver.

Gold is set to take off. Keep in mind that both stocks and bonds are at secular tops, and that moneyprinting is inflationary.

Just because stocks tank doesn’t mean we are in a deflationary environment YET.. It will take the collapse of the debts and much increase in BK before that starts. One could easily cause the other or the fact that stocks start their decline could be a leading indicator that we are heading in that direction.. As far as I know, the linkage is tenuous.

I still think that in a truly deflationary cycle, which is what is the result and consequence of debt binging, money will get wiped out as in this system money = debt = money… So as debt contracts are defaulted upon with enough frequency and velocity, the money supply will shrink and the actual dollar value of gold and silver and every other asset will also shrink.

And in the end, cash will be king.. IF you can get your hands on it.. as it may be tied up in an institution that has gone under and we may have to wait to get the FDIC insurance paid.

No guarantees about anything except death and taxes and getting older.

IMO, the Federal Reserve will buy baseball trading cards and drop money from helicopters before a true deflation sets in.

Deflation will always be the outcome of a debt binge. The FED will be unable to stop it when it starts. Debt = money and it takes profits to service debts. More debts require more profits and companies aren’t making more profits. Just look at what is happening to retail sales and commercial mortgages. Just look at the P/E ratios.. Even with historic buy backs.. http://www.mauldineconomics.com/frontlinethoughts/stock-market-valuations-and-hamburgers2

When to much debt has been created to fund unproductive enterprises and consumption, there will come a time when there just isn’t enough income to service the debts. At that time defaults will be great enough to cause more defaults and the dominos fall. It is inevitable when everything is bubbled.

The only two possible cures would be a debt jubilee or actual printed money spread through out the populous. Not money created by the FED because they can only create money thru more debt but actual money created by Congress out of nothing with no backing. And I do not believe either could happen with our Congress due to denial and uncooperative nature that they show. Besides the FED is authorized by Constitutional Amendment. Not that easy to change.

“The only two possible cures would be a debt jubilee or actual printed money spread through out the populous.”

This is rubbish

Debt jubilees:

Reward;

Criminals, Fraudsters, Professional Bankrupts, Fiscally irresponsible citicens, and nonworking/producing takers, taking Government handouts.

At the expense of;

Savers,Workers, Taxpayers, Fiscally responsible citicens, and producers.

Debt Jubilees are untenable.

As at topic they are almost forbidden on this site.

Helicopter money.

Does nothing in the medium or long term, except further debase the currency.

++

In 1929 the FED sat on its hand’s, and was blamed for all the evil that happened thereafter.

In 08 the FED did something and was agin blamed for all the evil that happened thereafter.

No matter what it does, its actions will always displease many, as it is not clairvoyant, therefore it is always reactionary, in any crisis event.

The FED is unusual, the chinese who want to get their money out of CNY in particular, who understand the FED, love the FED. As the US Govt can go broke(Default), leaving the FED, and the FED US dollars, perfectly stable.

There is another cure other than your two options, which the FED is trying, a gradual reduction of its grossly inflated balance sheet. This will put more Treasuries, and MBS theFED would buy (which means they may be vaguely stable if held to maturity) back in the Retail Market.

People/Entitys who have been forced to buy junk stocks and bonds will buy those Treasuries and MBS, The FED is not buying, if they can get them.

Which will reduce the capital fuelling various bubbles. Which is only there as it has nowhere else to go.

There have been DOOM to America articles. That state, nobody want US treasuries any more, as the yields on various Euro and Asian Items that were negative are turning positive again, and are a better buying than treasuries.

GOOD. Go and buy Euro trash with you Euro toilet paper. Then more US $ Treasuries and quality notes will be around, for investors/Pension fund’s Etc with US $ who are in Junk stock and Junk Bonds and don’t want to be.

And more of the Great balls of Euro and chinese trash money, that are helping to hold US stock and junk bonds at untenable levels, will go away, slowly draining the stock and bond bubbles.

Once the FED has reduced its balance sheet to levels it thinks appropriate and interest rates are at levels it thinks appropriate barring new catastrophes, upsetting it’s plans.

The next step would be a further increase in bank cash reserve ratios. which would be a good thing. That is at least 7 to 10 years away as that is how long it will take the FED to unwind unless demand for $ Treasuries and MBS becomes huge. Then the fed could possibly sell some of its holdings before Maturity.

d,

I was writing about true deflationary collapse, not just a normal pull back.

And you are correct in that a jubilee is not an answer because it would hurt those who were not speculators and bail out the speculators.

As for all the remedies you write about, in my opinion they are going to be to little to late. When this current Ponzi speculative bubble bursts, there won’t be any pension funds and little private equity to purchase the bonds the FED is trying to unload because as debt collapses, so does the money.

As for the FED in the 30’s they did to little, and the FED in this latest collapse they did to much to long. But it isn’t the FED’s fault that government couldn’t function to come up with policies to counteract the speculation and Ponzi finance. The bail outs should have been more focused on Main Street to keep up the demand rather than Wall Street which could only put the newly created money/debt to work by making loans and that is what got us back to where we are. To much consumer and corporate debt.

I didn’t put in my last that the 08 FED stimulus went to the wrong place, but you are correct.

IMHO the fed should have forced the Govt to launch Govt guaranteed infrastructure bonds and brought truckloads of them which they could have easily sold after the projects were started.

Thats all history.

Europe and china are still building their “Ponzi’s” as you term them.

It is when they implode, and which one implodes first. As the underpinnings of both are far worse than Americas.

The question is will the FED have levered itself into the situation where it has truckloads of cash to buy up enough of America, to keep it safe without another round of QE cash generation. When the other two ponzi’s implode. No matter which one goes first it will take the other with it.

I believe this is the situation they are trying to put themselves in. Will they be in time and Successful?? At least they are trying

And at least they are trying something other than, Roll the printing press which long term solves nothing. A conclusion they and the BOJ have reached, Although the BOJ is in, much much deeper than the FED

Something the PBOC and ECB still will not admit.

Well, think of the bright side. Even if we have a recession, the stock market won’t fall. It marches to a different drummer.

It doesn’t until it does and then watch out below at least in real terms anyway

Infinite Growth? Not likely.

Does any species increase forever? No.

I live in a pretty quiet and rural place. Just 200 air miles away there lies an over-priced gridlocked hellhole called Vancouver. We spent one year there when I was a kid. I remember just 50 years ago taking a crab trap on the city bus to the bottom of Lonsdale and caught crabs off the docks in Burrard Inlet. We could fish in the north shore creeks.

Before the Vancouver move my parents lived in Walnut Creek, CA. We used to dove hunt on the fields and ranch called Marsh Banks. Our house was surrounded by walnut orchards. In fact, we had walnuts, almonds, a fruit orchard and small olive grove. By 1970, 3 years after we moved, where we lived and played was a giant subdivison and golf course. My nephew lives down in Novato and has to commute 1.5 hours each way, bumper to bumper, to earn a living. His starter home on a postage stamp lot cost $750,000 2 years ago.

Is everywhere supposed to turn into Atlanta or LA in the name of progress.? There are limits, as anyone who ever owned an ant farm or aquarium will tell you. Perhaps we’ve reached them and this .6% forecast is just another indicator.

A little off-topic but I’ve lived in Brevard County Florida (think Kennedy Space Center) most of my life. KSC was built where it was because there is a lagoon separating Merritt Island where the rockets launch and the mainland. Allows for control.

My father moved there in 1954. At the time the Indian River Lagoon was crystal clear. He would fish at night for trout based on the luminescence in the water created by the fish.

When I was kid (early ’70’s) the lagoon wasn’t crystal clear anymore, but we would dive for oysters, net shrimp at night, and still catch plenty of trout.

Today, the lagoon is a dark brown. The oysters and trout are long gone. And you are advised not to eat anything you catch from our stretch. The cause? Overpopulation, destruction of shoreline mangroves for housing, fertilizer runoff from grass, and oils from roadways.

Progress towards what, exactly? I never knew the lagoon my father knew, and my son has no reason to ever get in a boat and get out on it.

maine has clean water.

as to the economy, i am unconcerned until it smacks me in the head.

i don’t think it is following me…….

yes, things are slow and pokey.

Ed Abbey: Growth for growth’s sake is the ideology of cancer.

The Fed’s models are always wrong. We just don’t know which direction.

You could say that for any forecast :-]

So the fed is tightening by raising rates and unwinding QE to the tune of trillions of dollars? While former GS bankers are advocating the elimination of TBTF?

Either there are a lot of clueless economists or they see something far worse on the horizon.

I don’t know why anyone would question this. The economy is like a boat. When everything is evenly distributed the boat floats quite nicely. But when all the weight is at the top and there is very little at the keel, the boat tips over.

We have been watching and documenting how our economy has become more and more unbalanced with huge inflation at the top and deflation of wages at the bottom. Without income for the middle class, there is no consumer economy. Just a pyramid Ponzi economy with all the cash at the top and none at the bottom. The government has no trouble selling Treasuries because those at the top have so much they have no where to put all the cash..

A recent survey report said that 50% of the people responding, and we know those with little or nothing don’t respond, 50% couldn’t come up with $500 for an emergency..

I don’t know when but this boat is not only being washed out to sea by the receding tide right before the tsunami washes ashore but it is going to capsize first.

Retail is slowing way down. Stores are closing everywhere. Car lots full and loans for free. Houses cost way to much and so does everything else. Seen your last insurance bill? Things are coming unglued.

Economicminor My homeowners policy premium went from 2k to 4K a year in 2014 without a claim in 40 years so I sold and left the country Best move I ever made

” Seen your last insurance bill ? ”

I like that !

Are you referring to a specific insurance bill or just insurance in general ?

All insurance seems to be going through the roof lately

6 months ago I paid $440 for car insurance. Now vehicle is older, no wrecks or tickets, and my next 6 month premium is $508. That’s what happens when Insurance companies can’t get squat in the markets thanks to ZIRP.

I wouldn’t complain about those rates I was paying more than that in 1980 in NY

Insurance in general.. my last property bill was up 10% yoy.. Auto similar..

Seems to me the bottom is getting hollowed out while the top keeps getting heavier…

I agree with you.

To add to what you said :

FICO lets us know that ONLY 38% of Americans have good credit, i.e. a score above 750.

Keep in mind, that to obtain or keep good credit requires an ability to pay one’s bills on time for an extended period of time. That is it. Nothing more than that.

Ah yes insurance , here in N. central florida my auto rate went up 25 % in 2 years. No tickets , no accidents. I reported this blatant increase to the insurance commission here in florida . They opened a case for me and asked me to send supporting documentation of which i complied. After some time they sent me a letter of closure that stated they contacted the issuer . The insurer responded to the commission that they had reviewed my policy and everything was legit. The insurance commission recommended I shop around for a better rate.

IS insurance outlays a GDP Component and/or property/sales taxes/rent ?

The Insurance Industrial Complex is a far greater problem for Americans than the Military Industrial Complex ever has been or will be.

Have you watched enough gieco, all state and progressive commercials? It’s no secret who has all the money.

I joined AARP the day I turned 50. Car insurance bill cut in half.

Wolf! I am an old man ( well not THAT old (76) )but I am still of the belief that we are in a Depression that began 10 years ago- or maybe beginning with the Dot-Com explosion. Everyone is skirting around the issue calling it whatever term of the day happens to be. Great Recession, etc.

I am not a scholar like you or Ben Bernanke but something is fishy and just does not ” feel” right. Yes, cars and homes are selling, restaurants are full and the highways are packed with new cars, but everywhere I look I see stores closing, people being more careful with spending. Etc etc etc.

But, we have been treading water for so long now I sense we as a world are going nowhere. Now we have Social Security, Medicare and other support systems that we did not have 80 years ago but the debt for all of this is staggering.

Please give me your sense of all this please. Love your blog. Thanks.

The economy has split in two: some people are doing really well (which explains many of the things you noted), and others have been in a depression for 10 years, which is why some things seems “fishy” to you.

And yes, the economy has debt out the wazoo, on all levels, federal, state, corporate, household … plus over-promised and under-funded liabilities … you name it, we have it.

“Staggering,” as you say, is the correct technical description for this situation :-)

Wolf,

No different here in Australia: some are doing very, very well and others are barely getting by.

Even the government here is bent on shafting the lower income groups and people that have saved for retirement for the past forty years by changing the rules and rates.

The latest scheme under discussion is to go after work expense deductions for workers. You know things like steel tipped boots for construction workers.

(Those people are really not a good example of ‘poor’ as it was estimated a year or so ago that the average wage of an unskilled worker in the construction industry here in Melbourne was A$140,000 a year, but that shows what kind of items they are going to go after………….).

Medical deductions have been eliminated (Tough if you get really sick now.) The amount of assets you can own and still get the age pension here has been cut by some 30%, etc, etc, etc.

Take that good ole topic of Real Estate. Supposedly prices in Melbourne are up by double digits (16%) in the past year………….

Well, maybe they are for people in the tony, ritzy areas and areas near the CBD, but I can tell you that out in the sticks prices of many house have barely moved and some places have gone down.

We have seen house prices up in my little area, but maybe 5% if we are lucky. If they had gone up 16% the developers around here would be knocking on the door asking us to sell the place for land value…………..

Well maybe next year as they knocking down houses and putting up those stinky little townhouses on 250 square meters blocks just down the road from us.

Only 400 meters away now……..

Cutting work expense deductions is a time honored tradition among governments. Countries like Italy, Portugal and Spain have all been doing it with a passion over the past decade and Italy is presently considering cutting them again.

The only effect it achieved in these countries is to drive an even bigger part of the economy underground, which is basically what has so far saved a good part of Europe from a monster recession.

Well I’m staying long US treasuries. Everyone and their mother is on the side of interest rates rising though due to the Trump reflation trade continuing, the Fed raising a puny quarter point 2-3x more this year, and the Fed starting to unwind its balance sheet. When hard economic data continues in the direction it’s going, eventually the Fed will be seen to be raising into economic weakness – it will take back those raises and suspend whatever asset sales it’s making. We’re overdue for a recession, and the Fed can certainly change tack.

In my experience, when everyone’s on one side of the boat, it’s often best to cross over to the other side.

strikes me the yield curve will flatten, and then rates will drop across the board.

but, not a bet i need to make.

Meanwhile, ‘Muricans are still whipping out the plastic to buy crap they don’t need with money they don’t have.

http://www.marketwatch.com/story/consumer-credit-reaccelerates-in-february-2017-04-07

Dr. Pangloss,

If you followed professional cycling over the last decade or so, it may help you understand the corruption in the global financial system.

There is a British cycling commentator called Phil Liggett. He said on record that he was unaware of any top cyclists using steroids in all the decades he was covering the sport.

Phil Liggett or Alan Greenspan. There are no differences.

keep in mind, there were bull headed guys like Paul Kimmage banging the table for years about the rampant use of steroids in the sport. His admonitions fell on deaf ears for a long time.

Professional cycling and global central banks are both rotten from head to toe.

From the SEC across to the New York Fed to the stock peddlers at the bottom. They all have one thing in common. They all “play pretend”.

The two biggest problems we all face are too much global debt and slowing (peak) global demand. We’re in a very tough spot.

Or as Phil Liggett calls it – a spot of bother.

Good analogy.

Let’s pretend we don’t want to hang them.

Wolf can you do a post on how to profit from such negligence?

Of course the model is wrong…its really below zero

“sentiments are just sentiments”.

Exactly right. Economic models are NEVER correct. After all, what they attempt to do is predict human behavior. Impossible. When speaking of the GDP future growth improvement, as being one half of one percent, is nothing more than a “rounding error” for a statistician. To say nothing of the data used that they base their model on! Just too many variables to cut such a small fine line, between expansion and contraction.

yet most of the data is computerized and readily available to them so it isn’t like witch craft or magic. They do see the data as it comes in and an anomaly would be for a big spike either way because of some unforeseen event.

“most of the data available”

“some unforeseen event”

nuff said

You should check some papers about actual GDP calculations. They employ so many random or conventional variables (like deflators) that the end result may vary in very broad ranges.

Tim….INDEED…and their propensity to report forecast results in decimal point percentage values is an absolute joke.

I wonder if it’s because they actually have a sense of humor, which is doubtful, or because they are trying to deceive the public by making it look scientific and accurate to the nearest thousandth, which is likely IMO…

It’s really unbelievable how these forecasts can move the markets at all. It’s really just noise and all economic forecasts are B.S.

Are you trying to say that the government GDP numbers are fake news?

If they use the same flawed formula each month, they should come up with the same flawed outcome shouldn’t they?

You don’t think politics enters into the numbers do you?

Oh my!

Why do we bother with them?

The first numbers that come out are per data and the revisions are per politics?

:-)

In Wolf’s terms…”BIG LIKE” on your comments!

I guess, as an older American who remembers boom and bust, I fear getting back into the market right now. The success and profit results meant something at one time. We now have a market with high values to companies that haven’t produced anything profitable so trying to guess what the algorithms and whiz kids rigging prices are going to do that someone like me hasn’t got a prayer to be anything but an additional profit source. I know I missed a lot but got out of the market last fall. I have most of my assets in gold, silver, and CDs (1.5% APY for 24 months is better than nothing!).

The current market situation is crazy. I feel that MANY stocks are way overpriced for what the organizations are worth. I’ve seen it attributed to several economists but the dictum “a thing which cannot go on forever will not go on forever” or something like that is the sentiment that comes to mind. I do wonder when the market will hit the “not go on” part. I know a lot of business commentators have predicted it an incredible amount of times and, eventually, one of them will be right!

“This means, if economic growth at this rate continues for an entire year, the US economy would edge up only 0.6% for the year.”

Suggests the Fed Funds rate will be cut (maybe after another rise).

There is no doubt that now is the time to pile into US residential real estate. America is the new Canada and we can count on several more years of FED inspired price appreciation. This site has shown that compared to Australia or New Zealand, the US residential market is only just starting.

I mean folks, this is the most obvious easy money trade of the 21st century. Do you think the easy money central bankers of Australia are any different that our denziens of the US Fed Reserve?

You Yanks need to increase the number of foreigners buying real estate if you want to have a real bubble.

So for you to get a real bubble you have to:

1. Increase the number of people moving into an area by around 100,000 a year or in % terms at least by 2%. Make sure that those coming in have lots of money to buy those nice houses and cars – you know BMW’s, Mercs, Porsches……..

2. Restrict the amount of land being developed for housing.

3. Make sure any land being developed is far, far away from the center the city so that increased demand is reflected in the higher priced real near the city which go up by multiples compared to other real estate in the sticks.

4. As the lower classes will have to buy out in the sticks make sure that there are no new highways or train lines being built so as to increase the amount of time wasted getting to and from work. This helps increase the value of the real estate near the CBD and surrounding suburbs.

5. Allow banks to keep mortgage rates higher and not pass on decreases in interest rates. Also allow them to increase rates more when rates go up. This will allow those with money to buy those nice nifty multi-million dollar properties, but make it hard for the lower classes to buy in those areas. It also helps the banks’ share prices go up and as the lower classes don’t directly own many bank shares it helps keep the money where it belongs………

Got it?

Lee, your summary of the plight of those less-fortunate here in urban America sounds pretty accurate to me.

Wolf…what do you think about SF? #1 (?), #2 (Check), #3 (Check), #4 (Check. I remember traffic in The City and the failure to upgrade for increased population)

#5 (Check. Why would they ever lower rates if it doesn’t benefit them? I’ve often wondered…how much of the interest being charged is actually used to cover losses from defaults and how much is pure profit?

#1 check. Until now… inflow slowed to a crawl.

#2 and #3: Not really. Lots of land being developed in SF, including the nuclear and otherwise contaminated Navy Shipyards at Hunters Point and the even more contaminated Treasure Island.

Here’s one of my stories on Treasure Island from 2012…

https://wolfstreet.com/2012/08/17/nuclear-radiation-on-san-franciscos-treasure-island-we-dont-need-to-know-apparently/

Some of these issues in the article have now been resolved and cleaned up (largely federal government, which owned them), and development is moving forward.

Tens of thousands of housing units will be built in these locations over time. Also lots of new construction in SOMA and the Van Ness Corridor (all VERY central).

#4: Check. Most of the new development is EXPENSIVE housing with some artificially “affordable” (subsidized) housing thrown in.

But… the onslaught of supply in SF should put pressures on prices (already is).

#5: This appears to be an Australian thing. Mortgage rates in the US have been very low, though they’re creeping up.

Are you saying that this program has been successfully implemented in Sydney and Melbourne?

Wolf,

Well if not intentionally, by default.

RE near the CBD and tony suburbs has increased by huge amounts. Some of the places going under auction beat the reserve by hundreds of thousands of dollars – more than the cost of house out in the sticks.

And as far as transport is concerned, there hasn’t been one new rail line built in Melbourne for something like……………100 years.

Some highways have been upgraded and there has been one ‘new’ toll way built here in the last 20 years which just happens to feed into the Monash Freeway which itself is nothing more than a carpark during peak hours. Really helps.

And I have harped on the banks and interest rates for a long time. There really is no competition here in that area. Banks have made a fortune off of the increased margins changed to people on ARM’s.

The latest estimate is the out of cycle increases just announced will add another A$1 BILLION in profit to their bottom line.

Finally, all those cheap imports from the rest of the world are going to get slugged with our GST (Value added tax) of 10% as of 1 July.

I don’t know how it will affect many businesses: if they will stop selling to Australia or how they will implement the program. (ie Ebay, Amazon).

SEE:

http://www.theage.com.au/money/tax/the-300m-gst-grab-hardly-anyone-knows-about-20170407-gvgcfb.html

https://www.ato.gov.au/Business/International-tax-for-business/In-detail/Doing-business-in-Australia/International-taxation-of-goods-and-services-supplied-to-Australia/

You still dont understand GST the only person who pays it, is the end user/consumer.

So it makes no difference to imports what % GST is, as all locally manufactured/produced goods, are subject to the same % when they leave the production point.

Dear d,

Yes it makes a difference to imports as all those things we buy from Japan via mail as of 1 July will now cost us an extra 10%.

Tea, seaweed, dried fish, books – things that we buy from Japan. These are cheaper to buy in Japan and pay the postage (some places discount the postage on orders or rebate the Japanese GST) than in Australia.

All those orders under A$1000 which were bought overseas by consumers and sent by mail and not currently subject to GST will be subject to GST.

No doubt there will now be even longer delays, more bs paying the GST, and hopefully no extra fees such as delivery fees, customs fees, or inspection fees.

It also makes a difference to people who buy collectibles such as stamps and coins from overseas as they will now cost an extra 10%.

These items were not subject to the GST. Buy some stamps from a seller in the USA and now we’ll get hit with an extra 10% or maybe people will stop selling as the old law of economics kicks in: high prices result in lower demand.

Maybe some companies with sales of over A$75,000 to Australia will not want to register and go though all the extra paperwork and refuse to sell to Australia thus reducing choice to consumers in Australia.

This is just another example of the big end of town sticking it to the lower/middle class via the exercise of influence on the government here.

No different than the banks, toll roads, utility companies, etc.

Thats how GST system, is supposed to work.

Its called a global level playing field.

Your free ride loopholes, are slowly being closed.

What they have not yet done (It appears) but will do, as it cost top much not to, is give every addressee a $ per annum, GST free, in due corse.

“Even bank robber pay GST” R D Muldoon.

Considering housing demand is at 20 year lows and falling, it seems everyone knows exactly what’s on the menu.

You do remember that huge amounts of even single residential properties are owned by PE groups which were funded by both first access to the foreclosure market and also first access to money.

Virtually all the apartments are held by large players and the large players built all the new rentals and condo units too. Thus, the TBTF and PE drive both the rental market and the rising prices.

At first this was good for all the others (private as well as FRE and FNM) who were underwater on the 2009 crash as it put a floor under the market. Now it has driven the markets to unreasonable highs. All these players looking to make a killing.

Just shows me that manipulation can work for a while but I believe in the end, the real market economy will reassert itself. Profits don’t exist in a vacuum. You can borrow from the future to a point, then the future wants to exist along with the present and at that point the future is now. Once the future profits have all been extracted, there aren’t any left to pay for today. Pay back time… Economic collapse! Winter then eventually Spring and back in business.

Well said.

You don’t earn a cent holding onto millions of excess empty housing units. To the contrary; their losses rack up rapidly.

With the Goldman plants and Keynesian fraudsters at the Fed and central banks assuring us that debt-based consumption is the key to our permanent prosperity, it is no wonder that the sheeple are willingly embracing their debt serfdom.

http://www.telegraph.co.uk/business/2017/04/08/plastic-fantastic-debt-frenzy-may-catching-us/

When “Don’t Fight the FED!” has worked over and over.. people end up believing that the FED is Omnipotent.

I believe the the FED is a Wizard behind a curtain and just an old (wo)man doing what ever to make it appear that everything is alright.

I wish you wouldn’t misuse a term like Keynesian. Keynes was a counter-cyclical economist: when economies improved, you raised taxes and cut spending. of course no one liked this part of the formula, which is why “fiscal conservatives” like Reagan and George W. could double the deficit, and then Obama could double it again. The last Keynesian was George HW, who, to counter the Reagan deficits, raised taxes and largely froze spending. This got him booted out of office, but it was the proper policy given the situation. Since then, Republican or Democrat, is has been stimulus all the way, and no counter-cyclical anything.

“I hope the model is wrong”

How about making a graph with the two projections, GDPNow and blue chip, along with the later “official” GDP figure over the duration of the availability of both projections? Maybe both are garbage. That’d be my guess.

GDPNow has nailed it before when the quarter was “unexpectedly” bad and economists totally missed it. Q1 2015 was the prime example:

https://wolfstreet.com/2015/04/29/gdp-now-atlanta-fed-model-nailed-ugly-q1-gdp-blue-chip-economists-too-optimistic/

There is data on this on the GDPNow website, comparing the final forecast to the official first GDP estimate by the BEA. No forecast is perfect :-]