New York Fed President William Dudley is on board.

Today it was New York Fed President William Dudley’s job to hammer home the message. He’s one of the most influential members on the policy-setting Federal Open Market Committee. His New York Fed deals with the securities that are on the Fed’s balance sheet as a result of QE. And he said the Fed might start reversing QE this year.

With this call to shrink the Fed’s balance sheet, he is following in the footsteps of other Fed heads, including Cleveland Fed President Loretta Mester, San Francisco Fed President John Williams, and most notably Boston Fed President Eric Rosengren – a former “dove” who has been publicly fretting about bubbles in commercial real estate and housing and the risks they pose to “financial stability.”

So this theme unraveling QE, not in the foggy future but this year, is picking up momentum.

There is a lot to unravel: the Fed’s $4.5-trillion balance sheet holds $1.8 trillion in mortgage-backed securities and $2.4 trillion in Treasuries. As they mature, the Fed replaces them by buying more.

Dudley was talking to Bloomberg TV today. Everything was couched in the caveat that it “really depends on the data.” But it included a hue of frustration with the credit markets:

“We’ve been trying to communicate to people: if the economy stays on that trend we’re going to gradually remove monetary accommodation.”

However slow economic growth may be – it was a miserable 1.6% in 2016 – if it “stays on that trend,” the Fed will not only continue raising rates but also start reversing QE. And the markets don’t get it, that’s what he seemed to say.

So “a couple more hikes this year seems reasonable,” he said. But if the economy is stronger, “we could do a little bit more.”

The FOMC has raised its target for the federal funds rate twice over the past three meetings, to a range between 0.75% and 1.0%. This pushed the effective federal funds rate to 0.91%. The median expectation is for two more hikes this year. But Dudley and others have put a third hike on the table. Rosengren said an increase at every other meeting this year “could and should be the committee’s default.”

There’s “no huge rush to tighten policy,” Dudley said. So rate hikes of 50 basis points each are off the table for now. Whew!

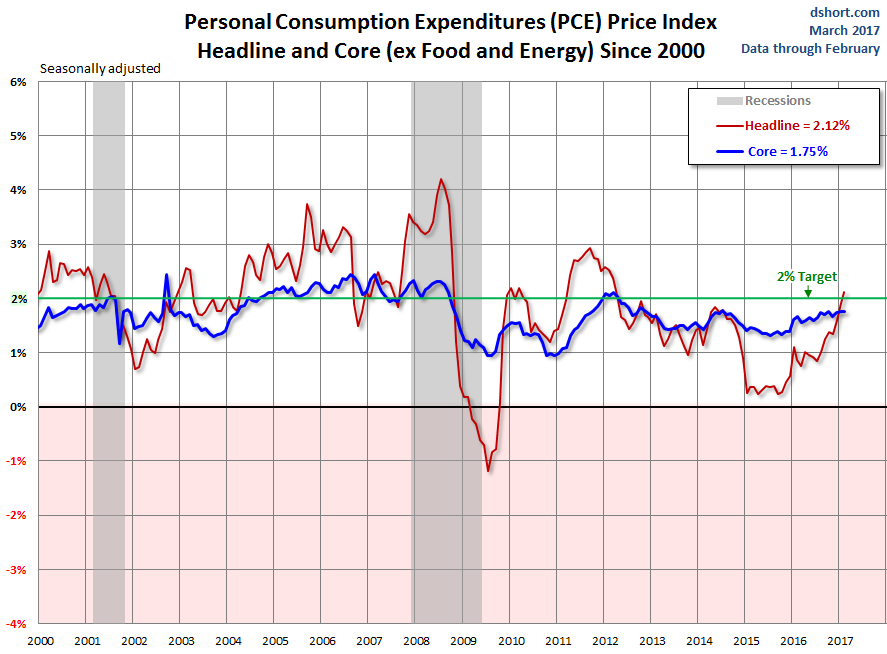

But inflation is on the radar, Dudley pointed out. The Fed’s favorite inflation gauge, the PCE core index reached 1.75%, and the headline PCE index 2.12%, according to the Commerce Department today. The CPI is already at 2.8%.

This chart by Doug Short of Advisor Perspectives shows the sharp rise of the PCE index (red line) since mid-2016 and the gradual uptick of the core PCE index (blue line). The PCE index has pierced for the first time in five years the Fed’s target (green line):

The economy “is clearly not over-heating,” Dudley said, and the PCE core index is “still under 2%.” Yet, “at the same time, policy is still accommodative and we’re pretty close to full employment, so it makes sense to very gradually take back accommodation to get monetary policy closer to neutral as we go through 2017.”

And where is neutral? The “consensus among many people is that neutral federal funds rate, adjusted for inflation, is somewhere between 0 and 1 percent,” he said. “With 2% inflation target, you’re talking somewhere in the 2 to 3 percent range.”

With the effective fed funds rate at 0.91%, “we have maybe 100 to 150 basis points of tightening ahead.” Four to six more rate hikes. If the economy (or inflation) is stronger, “we have a little more to do.”

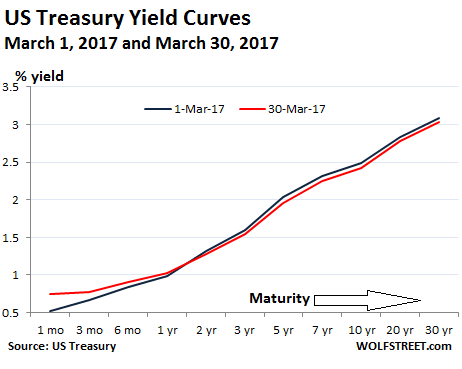

But the Fed’s target range only impacted short term yields so far. Long-term yields, though they have risen since last summer, fell recently. And the yield curve has flattened in March.

The 1-month yield rose from 0.46% on March 1 to 0.75% on March 30. But the 30-year yield edged down from 3.06% on March 1 to 3.03% on March 30, thus brushing off the Fed’s rate hike and its jawboning about QE:

Hence the warnings about unwinding QE: to nudge up long-term rates. Dudley explains timing and method:

“It wouldn’t surprise me if sometime later this year or sometime in 2018, should the economy perform in line with our expectations, that we’ll start to gradually let securities mature rather than reinvesting them.”

“If we start to normalize the balance sheet, that’s a substitute for short-term rate hikes because it would also work in the direction of tightening financial conditions.”

“If and when we decide to begin to normalize the balance sheet we might actually decide at the same time to take a little pause in terms of raising short-term interest rates.”

And he is “not that worried that the markets are going to react to the changes in our balance sheet in a violent way because it’s already factored in.”

Dudley’s statement was the clearest sign yet that the Fed is planning on letting maturing securities roll off the balance sheet without replacement, thus mopping up some of the liquidity in the markets, beginning “later this year.” This contradicts what many market participants are still betting on – that the Fed will in essence never be able to do so.

QE, boosted by ultra-low central bank policy rates, is an amazing thing. Liquidity lifts all boats. Asset prices have soared across the spectrum. That was the intent. But there are effects on the real economy, such as housing becoming a financial strain for many consumers who then cannot spend money on other things. How far can you go before this artificially inflated system collapses under its own weight? No one knows. And no one wants to find out. It would be a mess.

So with one eye on that potential mess, the Fed is getting serious about trying to back out. And if the markets brush off these efforts, the Fed will likely push ahead further and faster.

Wall Street claims surge in stocks is based on rising corporate earnings. Ha! Read… Last Two Times After Our Dear Government Reported Data Like This, Stocks Crashed

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I just don’t believe them. More excuses will come along that provide cover for more delay. The Fed Put is alive and well and only shuffling its feet a little.

Anyway, higher long rates are where savings will begin to recover. Interest income comes from savings and spending results from interest income. Bernanke ridiculed savers at one point. Why pay interest if you can depend on the Fed for capital formation at low rates? Why save when the Fed can pump asset values using QE?

Interest income begets spending, but also begets complaining people of influence who hate the idea of paying for money for money. The Fed will support financial parasites as long as theory allows it and theory is free while being endless.

I especially like the chicken and egg theory that says you can’t raise rates if inflation is low but spending remains low if interest rates are low and inflation is a function of spending. Hence, the Fed Put forever because raising rates will harm the economy. But it’s OK to borrow at low rates and load up on debt to the point of having no savings available to earn interest.

Righty–spending is a function of microeconomics, not the FFR policy. Consumers have spent money and borrowed when interest rates were well above 10%. Dudley is confident because he believes the vast interventions in various financial markets with digital dollar currency have been successful, at least in keeping financial market assets in nosebleed territory. It’s almost stupid to watch Deutsche Bank reveal bad news in the MSM and mysteriously, the equity valuation goes higher. If you believe that is the “market” buying into their stock, I have an avacado plantation in Idaho I will sell you…

The Fed put will need to go on overdrive at some point in the next 24 months. The China growth story ended a while back and so too did US earnings growth.. We could go on and on.

The only thing that will force the Fed to hike rates will be the bond vigilantes, surging inflation due to the Fed’s debasement of the currency, and/or Yellen’s Goldman Sachs organ grinders taking out a massive short position on these Ponzi markets, then ordering their creature Yellen the Felon to hike rates sharply enough to cause the financial house of cards the Fed built to come crashing down under the weight of its own fraud and fictitious valuations.

“Liquidity lifts all boats. Asset prices have soared across the spectrum.”

Unfortunately for most Yanks and their families they have no boats, no assets, and no likelihood of ever getting them.

Pretty much the same for a majority of people around the world now.

Indeed. And for them, life has just gotten more expense, including or especially housing, as I mentioned. And this has real consequences.

Plus the very real increases in “health care” (i.e. “health insurance” — true care has little to do with it in the US) due to Obamacare. The newly-insured & subsidised may have benefitted, but many families are seeing significant increases in their premiums.

Some day this whole house of cards is going to collapse, possibly violently. Those who barely have $500 savings won’t do as well as those who have invested in luxury below-ground safe houses or bought a New Zealand passport.

Those who see how unsustainable the Fed’s financial house of cards is, and who have the foresight to stockpile life’s essentials before Yellen & Co. hurtle us down the road to Weimar 2.0, will be the new 1%.

Brace for impact – and for the day the Fed prints away all government and corporate debts, reducing the dollar to worthlessness. Weimar 2.0, here we come. Read Adam Fergusson’s “When Money Dies” for a preview of what’s ahead. And stock essential supplies while retailers still accept green FRNs backed by nothing.

http://survivalcache.com/37-things-you-should-stock-but-probably-arent/

Patel don’t forget real money Gold and Silver

Haven’t figured it out yet?

The FED is purposefully blowing up the economy. How convenient they decide to “Unravel their balance sheet” just as the bubbles are popping..

So, you either believe they are totally incompetent, which is what the media wants us to believe, or you believe they are doing it purposefully.

Believing they’re doing it purposefully makes a ton of sense once you throw off that naive and gullible belief that central banks are here to help us.

Does anyone actually believe that?

Then why do you have such a hard time believing they’re here to rob us and destroy our wealth?

Looks like dumping equities and real estate around now might be a plan And get some Gold and Silver while you still can at these bargain basement prices

Soon will the soon problematic bondmarket come out as ghost when FED continue raising rates,,,,,then we will have BIG problems

I’m 61, on a pension, and still save. Screw ’em.

Do people really believe there will be 4% growth in the US, and West, in general? How? In the US there is an aging population, a formal program against immigration and refugee placements, talk of countervailing duties/tariffs, pricey energy compared to traditional growth eras, and beyond hefty competiton from low-cost and off-shored reman centres. Plus, there already seems to be Peak Crap in people’s garages. This is not a recipe for growth as far as I can see.

When times toughen up it will be good to have cash. I grew up with stories of the Depression. I don’t trust any of the experts (except for Wolf, of course!!). That is why I still save. We have all we want or need.

My buddy, who has hardly worked this year and is worried about retirement, just flew out to the Carribean today for a relatives destination wedding. Nuts. Insanity. Raise those rates, yesterday.

You spoke for a lot of us. I’m seventy-seven. I was born in the last year of the Great Depression and have actual memories of WWII. I live within my means and carry no debt. Today, that is practically subversive.

Somebody is going to get a real surprise when things go South .

I guess the Fed hasn’t figured out that when you lower interest rates, people have to save more to generate the same income.

60+ – semi retired – debt free – cash flush and living comfortably small .

Typical lush promise “I’m going to stop just as soon as I finish this last drink.” The Fed should no more be independent of civilian oversight and control than the military.

As good as the U. S. Constitution is, it is a fatal flaw to have an unelected and highly secretive “CO-OP” (100% of the shares of the Federal Reserve Bank are owned by the “member” banks) controlling two of the most critical factors in the economy, namely the issuance of bank notes [money supply] and the setting of interest rates.

The Federal Reserve is certainly not part of the enumerated powers in the US Constitution, and so, many believe that it is unconstitutional.

It isn’t but the Constitution empowers the Federal government with unlimited powers over its currency. That means the government can do whatever it likes with the currency, including setting up a reserve bank.

Of course it could also act sensible instead of stupid. Stupid wins out today!

I thought just the reverse — the Constitution states that only “gold and silver” can be issued as legitimate currency? Hardly sounds like “unlimited powers”.

Its an exercise in evasion and sophistry, but the “private” Federal Reserve doesn’t issue legal tender “currency” which would indeed require gold and silver backing, as per the Constitution, but rather “bank notes” which do not. It appears that one of the major reasons the Federal Reserve Bank exists is to evade the “gold and silver” clause.

IIRC one of the rationales for this was to allow the money supply to be “adjusted” so that the Dollar had constant purchasing power rather than constant gold/silver content. One example was the farmers, in that when harvest time arrived and they sold their crops, there was a large demand for Dollars, so the Dollar value increased and the cash they received for their crops was lower, as it was higher in value than the Dollars at other times of the year. At other times, there was less demand for Dollars so it was worth less,and so the goods the farmers had to by in their “off season” cost more.

While this sounds somewhat plausible in Econ 101, the U. S. economy is no longer based on agriculture.

It appears from an examination of the historical record that ALL “mediums of exchange” are subject to some form of economic “entropy” in that they always lose value, even gold and silver, for example when the Spanish brought enormous amounts of golad and silver back from their conquests in the New World, to the explosion of gold and silver mining in the U. S. at the end of the 19th century, the bimetallism fiasco, and William Jennings Bryant’s “Cross of Gold” speech.

We are thus attempting to measure “progress” and “value” using a rubber ruler.

It’s not so much what it says, it’s what it doesn’t say. Saying gold and silver is outdated now, but not back in 1776. The lack of guidelines and laws frees the gov to decide what to do. What ever laws it wants it can pass them, like that foolish debt ceiling law, a piece of incredible nonsense. As I mentioned the government can be stupid and it can be sensible. It’s being stupid.

Score on for the Antipode . Mr Doyle is spot on . Other than the misguided rantings of the Alt Right and Freedom Caucus there is nothing inherently ‘ unconstitutional ‘ about the Federal Reserve’s existence . Fact is just the opposite is true . It is reversible [ read the article linked below ] .. but there is nothing ‘ unconstitutional ‘ about it.

Hmmm .. kind of sad that it takes an Antipode to correct a bunch of Yanks on a fundamental US issue .

Here’s an in depth article on the subject .. which assumes unlike 50% of us Americans you are capable of reading above an 8th grade level [ Good lord thats a frightening statistic ! ]

http://www.libertylawsite.org/liberty-forum/is-the-federal-reserve-constitutional/

The Federal Reserve, “the Fed”, is the central bank of the United States of America that was created in 1913 by Congress. It is a banking cartel that has a government-granted monopoly on the creation of money and credit. The Fed literally loans “money” (Federal Reserve Notes) into existence. Federal Reserve Notes are paper promises backed by nothing of intrinsic value and they are only functioning as money because the government forces them on the public through legal tender laws. Federal Reserve Notes are referred to as dollars but are not. The definition of a dollar is a weight of silver (371 grains). To put it simply, the Fed is a group of banks running a national counterfeiting operation with the protection of the government.

What is “unconstitutional” these days is whatever some unelected, appointed for life left wing or right nutter judge says is “unconstitutional’.

Just take a look at some the cases that have been decided over the recent past: peoples’ rights enumerated in The Constitution, have diminished faster than at time in in the history of the US.

Everything from privacy to protection to sanctity of assets has diminished.

No wonder the USA is in the mess it is in.

Not quite. The Supreme Court is the final arbiter. In so far as it is full of “nutters” the rest of what you say might come to pass.

In the late 80’s the UK pushed interest rates from 7.5% to 15%. What I believe we are seeing now from the Fed is a clever strategy of keeping the game going with changes which are always ‘going to happen’ and when they do are so insignificant as to hardly make a difference.

We have been led carefully to get excited over 1/10 th of a percent changes in interest rates and GDP which are little more than rounding errors. The effect however is to keep us on the edges of our seats.

Our expectations and perceptions are being managed very well!

Long-running “reality” series set in a bank to keep the “masses of asses” diverted…

So, the FED would stop re-investing matured debt. That means “someone” has to pay back the creditors. That “someone” are the US government, the banks and big companies who bought up their own shares with newly made debt at zero interest rates. Where’s the money coming from ???? This is a bullshit story, the FED, government, banks and big business cornered themselves and the truth is that 4 trillion of “new money” was created out of thin air – leading to massive inflation if the FED would “normalise” its balance sheet. It’s the little people who will suffer : pensions worth nothing anymore, savings idem dito, hard physical and liquid assets prices ( PM’s ) explode. Looks bad, people, get prepared.

Hendrik,

Although i agree with most of what you said, what you wrote could have been written verbatim 5 years ago. That’s the frustrating thing about this.

True, but doubling the outstanding debt levels every 8 years ends somewhere …. in hyperinflation. This time is NO different. The Chapwood index indicates a true inflation rate of 10+% in the USA on a yearly basis – far from the “almost 2%” reported by the FED. You think this is good for a consumer-based economy in the long run with a growth rate of 1.6%?? In addition today, it is the FIRST time in written history that the real interest rates are negative for several years – an experiment which was never tried ( or accepted by the savers ) before and now this is possible since the adoption of fiat currencies on a global scale. Each and any fiat currency has historically failed and it was always the modest little saver who got nailed.

It’s the little people who will suffer : pensions worth nothing anymore, savings idem dito, hard physical and liquid assets prices ( PM’s ) explode.

The “little people” will be ground into powder as our former Republic becomes a full-fledged neo-feudal kleptocracy presided over by a corrupt and venal .1% that has subverted our institutions of governance and concentrated all wealth and power into its own greedy hands thanks to the Fed and its political enablers in the Republicrat duopoly.

The “little people” voted for this by voting for the co-opted Establishment status quo, and now they are going to get exactly what they have coming.

I think that is mostly wrong. The Fed has zero trouble paying back the bonds etc to the investors. The Fed never spends the money, it’s like a deposit account, earning interest. The Fed has no use for your money. Just as it has no need to borrow or save. It’s empowered to buy whatever it chooses [i.e., Treasury chooses] ad hoc. So its all just credited back to investors at maturity.

What inflation are you talking about? Massive?? All that QE money was hardly spent into the main economy.

What is “Normalise it’s [FED’s] balance sheet? Remember the Fed has NO money of its own. [it’s in Treasury] It does park a lot of other people’s money.

You’re right about the little people suffering. That’s deliberate of course.

It is my understanding the FED has nothing to repay ( they PRINT the money ), that is correct – but it’s the other way around. If say a big Cy borrows billions at zero interest rate through a bank indirectly from the FED, maturity of say 5 years, to buy back its own shares, after 5 years that Cy has to settle its debt through the bank back to the FED who then writes it off from its balance sheet. Same for the government Treasuries or bankers debt. If not so, the FED is just forging money for private Cies and the government and yes, then the sky is the limit – but that is completely illegal. It is of course possible, but forgery of money is a criminal offense and if true, we are being governed by criminals.

I remember being in NYC back in the ’90s. I was reading a NYT

article about the garbage in the streets, too many foreigners, traffic being awful, rampant crime, con games on street corners etc etc etc

The article I was reading was taken from a NYT article from the 1890’s.

The same commentators I read here remind me of that article. Everybody predicting collapse, the sky is falling and money being worthless. Folks, get a LIFE. It ain’t gonna happen. You have been reading too much Harry Dent and other wackos who have made tons of money making predictions of things that have never happened.

Go convince your other family members and your neighbors that you are right. They, too, will think you are still smoking

“Funny cigarettes.”

I don’t think the point of the article was that the “sky was falling.” The Fed opted for levitating asset prices and this is creating some hardships for younger people. Inequality has never been greater and that’s obviously fine with you. You’ve had a nice run in the stock market and are certain it will continue. Once the Fed removes accommodation the “earnings” multipliers may reverse.

I take it you sailed through the last couple bubbles unscathed.

The Fed opted for levitating asset prices and this is creating some hardships for younger people.

The Fed exists for one purpose only: to serve as the oligarchy’s chief instrument of plunder against the 99%. They didn’t just “levitate” asset prices: they’ve massively debased the currency – and our purchasing power – by printing countless trillions in “stimulus” to lavish on their Wall Street cohorts, benefiting a corrupt and venal .1% in the financial sector at the expense of everyone else. This isn’t just creating “hardships for young people”: it is setting up the conditions for a systemic financial crisis and economic collapse that is going to push tens of millions into insolvency, while gifting the Fed’s oligarch accomplices with new trillions in FedBux funny money to buy up the distressed assets of the vanishing middle class for pennies on the dollar.

The Wall Street-Federal Reserve Looting Syndicate is precisely the “monied interests” Thomas Jefferson warned would pose a mortal threat to the American Republic. We should’ve heeded his warnings while there was still time.

Jack,

You make very good points. Some of the commentators here are conservative, frugal, risk averse people. That is a good thing. My opinion – as are many others on this board – is that almost all global asset markets are artificially overvalued because of, among other things, an unprecedented flood of cheap money.

If people do not need to touch their invested money for AT LEAST 5 years and they are not overly leveraged relative to their current household income (middle income families), then they may do just fine… but there will be pain. It’s baked in the cake.

Why ? Bubble valuations almost everywhere caused by unprecedented globally cheap money.

Let me know what you disagree with as i am trying to learn as much as possible. Seriously.

My opinion to understand FED is that they are NOT changing interest rates to creat bubbles or kill bubbles.

Their job is to make things easy for who ever pointing a gun at their heads.

So why are they raising rates? Because they know shit will hit the fan regardless they raise rates or NOT.

They want to be able to cut it when it hits so that to make who ever pointing a gun at their heads happy.

Jack, i am with you on this. Harry Dent is just Harry Dent, never mind.

I guess there are many honest people here that actually do create wealth and their purpose is to figure out how NOT to get their wealth transferred to other people.

Of course there are folks in DC and Wall street who think about how to transfer other people’s wealth into their hands 24/7 with the brain power of ph.d.

My point is that folks here are trying to figure out how the transfer works and at the heart of the transfer is FED.

This is not scare mongering or selling other emotions.

what you said has certain truth in it but please understand why folks are here trying to figure the transfer out.

Wolf, longtime reader/lurker here. Thought I would let you know that the Ameritrade ad is blowing me out of your website today. Ad pops up and there is no way to close it. Keeps popping up regardless what I do. Just FYI.

I love your work. Keep it up!

Thanks. Yes, big problem with my ad agency. I took off their ad code for now and run Google ads only. That fixed it. This is the second time it happened in five months.

Rhetorical question: Don’t techies these days do any kind of quality control anymore? Rhetorical because I know the answer. It’s NO.

What I was told a decade ago about Microsoft quality control operation.

Set up a couple of sites with several dozen users/coders to test a new product. Create a task list to do. Push “start” and have these people work, produce an error rate per day or week. Set a goal to reduce this rate to some value. When this value is reached, release the product.

There is precious little other risk management involved from what I know, e.g. not just rate, but impact of the failure, and other risk management concepts (risk management is a very thorough, complex and productive activity when properly applied).

I don’t know if this was/is true, but was told to me by a spouse of a Microsoft employee many years ago.

So, a piece of ad software acting badly? Par for the course in the tech world….

It’s cool, though, right?

Pros: might start deflating the asset bubble

Cons: job-killing, demand reducing policy when the economy still isn’t great; might pop the asset bubble and start a recession

Jack,

Be afraid be very afraid. While optimism should always be the first option, when they go out of their way to warn you, take heed.

Here’s why, the fed’s unwinding on the surface may look like a mere monetary contraction. They take back their cash and the money supply tightens, this assumes the securities will be paid back in full. If they need to take losses as the securities mature, their write offs will need to be addressed somewhere. While they don’t discuss the possibility of not getting all their money back outright, they do tell you they have no intention of raising rates. This is because they know that if they don’t get all their money back, the market will consider the missing cash, a condition to raise its rates. The spread between the quoted rates and the market rates will widen.

How bad this can get, depends on how much crap is on their balance sheet and how much they can squeeze the banks to take the crap back. So while I hope its all sugar and spice and everything nice. I can read the tea leaves they are telling me to read.

I don’t believe the Fed has any intention of actually selling its assets. If those assets were going to create inflation, it would have happened already. So we are at a new point of equilibrium where $4.5T needs to be on the Fed’s balance sheet to maintain current status. The balance sheet will only reduced if inflation picks up convincingly, and that ain’t happening.

This bubble will pop not because the Fed alters its balance sheet. The bubble will pop when people understand the Fed is sustaining a permanent condition of wealth disparity, which is fundamentally unfair. When Trump goes down in flames with nothing accomplished, that’s when people will get really angry. Trump is Stage 1 of a generational revolt.

The Fed’s asset bubbles and Ponzi markets will not pop until Goldman Sachs goes massively short, then orders its “former” employee Janet Yellen to hike interest rates enough to implode the bubbles created through 14.5 trillion in created-out-of-thin-air “stimulus” gambling money gifted on Wall Street banksters.

“Trump is Stage 1 of a generational revolt.”

Although i avoid reading economic/political conspiracy theory articles like the plague, that thought has crossed my mind.

I have not come across your posts before. I hope you keep them coming Bobber.

You can trust the corporate media and its oligarch owners to tell you everything you need to know. Don’t be confused by those alt-media sites and their “conspiracy theories.”

Baaaaaah! Baaaaah! Now trot along into the incorporated globalist plantation like a good little sheep….

” “Trump is Stage 1 of a generational revolt.” ”

This implies organisation.

To date there is no organisation.

However P45 is the symptom of something, that could become “Organised” into some thing. The centre left and the globalised Vampire Corporate oligarchy allied with china, that control the US Duopoly, do not want to see.

I wasn’t referring to the fed selling their assets. The article was saying they intended to let the securities mature without rolling them over. My comment was centered on this operation.

Again, if the value is there, they will get their money back. If the value is nonexistent then they will have no choice but to write off the “mark to fantasy” value. This will contract the money supply and be deflationary. The market will have to increase rates to attract dollars. So it becomes a backdoor way for the rates to go up without the fed doing it directly.

“Again, if the value is there, they will get their money back. If the value is nonexistent then they will have no choice but to write off the “mark to fantasy” value.”

The FED brought most of those securities, with a REPO price guarantee.

Losses will be eaten, but not by the FED.

The overall effect will be as you say.

More dissembling by Yellen the Felon’s flying monkeys. The Fed since its surreptitious 1913 creation by the robber barons of the era has had just one purpose: to serve as the oligarchy’s instrument of plunder against the 99%. There is no more efficacious means to loot and asset-strip the productive middle and working classes than the Wall Street-Federal Reserve Looting Syndicate’s engineered boom-bust cycles every eight years or so. Despite the incessant jawboning by these Fed mouthpieces, this criminal banking cartel will never of its own volition give up its most lucrative rackets: NIRP or near-NIRP interest rates, which bilks savers out of $500 billion a year in interest income, and gifting free printing-press trillions in “stimulus” on a corrupt and venal .1$ in the financial sector so they can gamble with abandon in our rigged stock markets, with all losses covered by the taxpayers, and buy up the distressed assets of the increasingly pauperized American middle class.

Stop the Oligopoly’s financial warfare against the 99%. End the Fed!

“If the American people ever allow private banks to control the issue of their currency, first by inflation, then by deflation, the banks…will deprive the people of all property until their children wake-up homeless on the continent their fathers conquered…. The issuing power should be taken from the banks and restored to the people, to whom it properly belongs.” – Thomas Jefferson in the debate over the Re-charter of the Bank Bill (1809)

That’s you, Janet Yellen. You and your accomplices at this criminal private banking cartel called the Federal Reserve are exactly what the Founding Fathers warned us against.

Thank you for the last several comments. I/ we have been truly blessed. I have an amazing wife and several great kids and g’kids. We made most of our savings in the mid- eighties til August 18, 1999. Put everything we had into money market funds ( then paying 6%+.) have kept it there ever since.The market started crashing on August 26, I believe.

Now we are not even close to getting those returns but we sleep very nicely and have done so for 18 years always adding to the amount.

Now, long retired we have enough to last the rest of our lives but not so much that we have to worry about.

I am not afraid of the future. I am not afraid of a Trump presidency. I am not afraid of ” them” coming to take any of my stuff away.

Yes, really upset that the perps that created the financial crises weren’t sent to jail but so be it.

I’m seeing “Hiring” signs all over New Mexico and AZ. Granted, most are low wage jobs. But construction of homes is also taking off. If the stock market continues to trend up and this hiring trend continues, the Fed will probably follow through.

The genuine irony is that despite those jobs wages being on the rise in order to fill all the vacancies … the Righty Tighty voted for Trump don’t want those or any other jobs requiring manual labor across the Nation .. and especially in CA’s agricultural industry

“History records that the money changers have used every form of abuse, intrigue, deceit, and violent means possible to maintain their control over governments by controlling money and its issuance.” -James Madison

Restore the Republic. End the Fed.

http://endthefed.org

“There is a lot to unravel: the Fed’s $4.5-trillion balance sheet holds $1.8 trillion in mortgage-backed securities and $2.4 trillion in Treasuries. As they mature, the Fed replaces them by buying more.”

I don’t understand. I thought the FED was given a mandate by the 2008 crisis to make one time purchases of distressed debt. What program is this occuring under?

Are these purchases ‘new’ junk from the recent housing bubble?

They did buy a lot of distressed debt, starting with $29 billion Bear Stearns refuse. This was not part of QE but part of the bailouts. On their balance sheet, some of this stuff ended up in segregated funds, called “Maiden Lane,” that have now mostly been sold or written off, and have thus disappeared from the balance sheet. The bonds on the balance sheet today are mostly Treasuries and Agency (gov guaranteed) mortgage-backed securities.

“The Sun Also Sets”

I’ve said time and time again that Janet’s computer (money machine) has a magic zero key which she holds down for longer and longer periods of time in order to, when eventually necessary, “buy up” literally everything on the planet, as well as, most importantly, pay for the MSIC that is the enforcement mechanism of the drone-standard fiat-USD. (You don’t want to accept fiat USD as payment-in-full for your REAL products, resources, etc.? Whether you ask for it or not, “democracy” is going to be delivered ASAP to your country via very-expedited air service.)

Back on track. Janet also has on her keyboard that similarly-magical little “delete” key. Never underestimate the power of smoke, mirrors and Fed-controlled zero and delete keys.

In short, never underestimate the power of the human imagination (greed).

The question is, what breed is the NEXT rabbit to be dragged by the ears out of the Fed’s (BoJ, BoE, BoC, etc.) top hat? Only the Group of 30 knows for sure, along with the “systemically important” VIPs they “leak” to. (Don’t you wish you were one of the “leakees”? Then we, too, could enjoy the “shower”. Now, THAT would be a “trickle down” economic system that I could live with!)

Depending on one’s particular definition of “collapse”, one could easily argue (and win) that the “traditional” US economy ALREADY collapsed with the bailout of TBTF banks, TARP, Dodd-Frank, etc.

Of course all of that very unwise rescue stuff was necessitated by the previous repeal of all of the very wise post-1929-depression legislation and the very predictable return by the TBTF banks to doing what caused the Great Depression 1.0.

At the very least, one would have to say that what the Elite’s governments and central-bank slaves have be doing since “the Financial Crisis” a few short years ago is “flying by the seat of their pants”. Or, as one Lord Rothschild recently said ….

http://sputniknews.com/politics/20160819/1044443930/rothschild-gold-dollar.html

“The six months under review have seen central bankers continuing what is surely the greatest experiment in monetary policy in the history of the world”.

Of course the irony is that if large investors were to start selling stocks, bonds, etc. and started buying PHYSICAL gold and silver (or homes in Toronto, London, Vancouver, etc.) in large quantities, this would not only cause the price of physical gold and silver to skyrocket, but might very well force the Fed, etc. to prevent the DJIA — the too-big-to-drop (TBTD) ulitimate symbol of “capitalism” — from crashing by becoming the share-buyer of last resort. That is, if the Fed, etc. take their “whatever it takes” experiment to the extreme in order to prevent a stock market crash, the private Fed, etc. might end up “owning” or effectively controlling some or all of the corporations that are listed on the stock markets. (And what could possibly go wrong with that?!)

So lots and lots of astronomically-priced gold would be owned by all of the stock/bond-sellers, and the central banks would effectively own or control lots and lots of shares of corporations. Now, THAT would be what I would call experimental, because if you think corporations are buying back their own shares to the extreme now, can you imagine how high Janet’s computer’s number-pad could boost the prices of ITS VERY OWN corporations’ shares “on the stock market”? To infinity and beyond!!

Dear Janet, what you’ve been doing so far has worked great, so you just keep spouting gibberish and using those zero and delete keys wisely and we’ll all enjoy another great sunset this evening.

(Now, how’s THAT for squeezing another shot out of a 1913 Fed musket that was “out of dry powder”, Mr. Stockman?)

If I was a betting man I would put odds of the Fed balance sheet hitting 10 Trillion before it hits 3 Trillion. Well, I do bet, but only food :)

“Dudley’s statement was the clearest sign yet that the Fed is planning on letting maturing securities roll off the balance sheet without replacement, thus mopping up some of the liquidity in the markets, beginning “later this year.” This contradicts what many market participants are still betting on – that the Fed will in essence never be able to do so.”

Inflation is not turning up to inflate away the debt.

It cant, as the Stimulus stayed in an asset loop at the top. Not what the FED wanted, but better than what Occurred in 29, when the FED sat on its hand’s.

Live and learn.

What is regarded as unconventional monetary policy, QE, applied the the way the US FED applied QE does (FA). In the real US Economy experiencing a deflationary shock.. (FA) now being known. And creates other negative side effects.

Namely. Large unsustainable asset bubbles, at the top of the economy, and general stagnation, with declining wage rates, in the rest of the economy.

So this is the only other way to slowly ease out of the situation for the FED.

As has been deduced by the logical among us, some time ago.

The fact that the FED is laking about it publicly, asserts that this is already long term FED policy.

The question is

How “long term”, are we talking here?

Those who this cant and wont happen, should put their heads back in the sand. That way they will be protected from seeing the disaster that comes, until it aggressively descends upon them, if this does not happen.

RE: It cant, as the Stimulus stayed in an asset loop at the top.

—–

Indeed! Assuming that QE was in fact required, this “skimming/loop” could have been minimized by the FED:

(1) Putting the QE money directly in the hands of the people, for example by sending a 1000$ “bonus” check to every citizen who filed a tax return the previous year, who would spend it, and it would circulate at least a few times in the local economy before being concentrated in the mega banks;

and/or

(2) Having capital allocation policies and procedures in place to divert the banks from financing non-, even counter-, productive activities such as commercial and residential asset bubbles, stock-buybacks, stock dividends, 0 down /0 APR 72/84 month vehicle loans, stock, FX and commodities speculation, etc. The FEB has the power to set margin rates, and could have issued rate/term requirements for the various classes of loans as a condition for the banks receiving the “free” money.

If banks get weak we could raise rates 17 times in three years no problemo! Maybe twenty in a month if banks get serious?

So basically the FED bails out and rewards Wall Street and the criminals that have destroyed the REAL ECONOMY by front loading a fake stock market and now that they have exited the market it is now time for some shock therapy for Joe average. I wish the masses would wake up to this criminal entity that has hijacked our government and throw the bums out. They all must go !!!!!!!!!!!!!!

The challenge is to normalize rates while providing liquidity. They have done it before, Greenspan managed the fact by opening the discount window. It’s just that RPO is like putting near beer in the punch bowl. Investors want MOAR! RRPO is the same thing, but it’s still financial repression. Fisher (resigned now) said last year the Fed could divest a third of its holdings WITHOUT affecting short term interest rates. (The longer they wait the less viable that assumption may be) What happens on the long end of the curve, stays on the long end. The old tools are too weak, the new ones too restrictive, but they can and they will achieve higher rates and keep new credit flowing. The banks are not going to do so well in that environment, so we must repeal the regulations which separate investment banking from the standard business models. Banking is an obsolete business. All you need is a credit card.