I get chills when insiders tell outsiders “not to panic.”

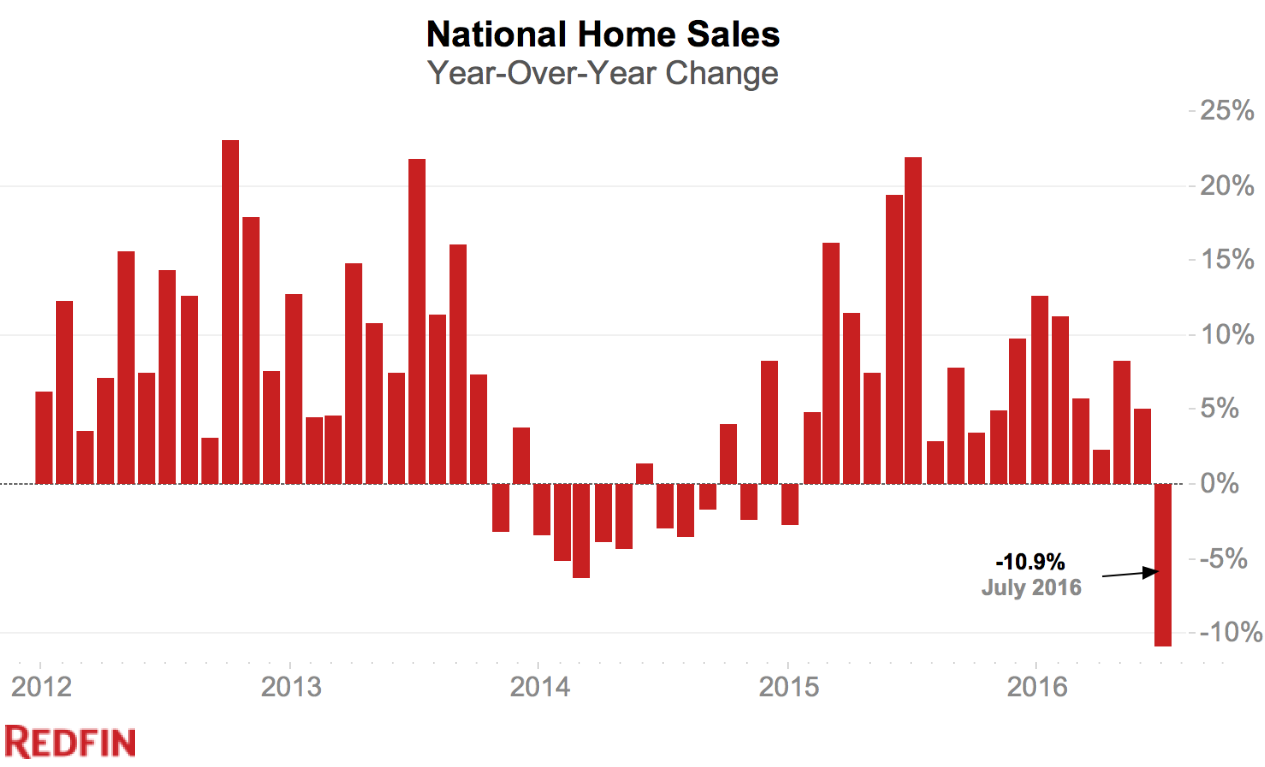

Home sales plunged 10.9% across the US in July from a year ago, “the biggest national sales decline since April 2011,” nationwide real estate broker Redfin reported, adding chillingly, “but there’s a good reason not to panic.”

When insiders tell outsiders “not to panic,” I get worried. This is what July home sales volume in the US looked like, according to Redfin:

Yet, the median home price across the US rose 5.3% from July a year ago. OK, as long as prices rise, everything is fine.

But when buyers refuse to pay inflated prices and sellers refuse to lower their prices, then volume dries up until something gives. If sellers run out of patience or are forced to sell, prices suddenly take a hit. On a nationwide average, that’s not happening yet, though it has started to happen in some cities.

All homes for sale (the “inventory”) fell 6.6% from a year ago. More on that in a moment, in the discussion about San Francisco – because there’s something important missing here.

Given the plunge in sales, supply as measured in months at the current sales rate edged up 0.1 points to 3.2 months.

But don’t panic, the report said. Part of the sales plunge was due to the calendar. The number of selling days can impact monthly sales by a lot. This is true in auto sales and in a number other categories. So Redfin did its own calculus:

Because the month started on a Friday, there were five full weekends plus one national holiday, leaving only 20 days available for home closings.

Redfin data shows that the lion’s share of closings happen on Fridays. Homes very rarely close on Saturdays or Sundays. This July contained a below-average number of business days (2.3% lower than average) while July 2015 had the most favorable day-of-week setup for closings of any month on record (5.3% higher than average).

These calendar day differences only explain part of the volume fiasco. Redfin director of analytics Pete Ziemkiewicz:

“All else equal, we’d expect the number of homes sold throughout the U.S. to be 7.5% lower in July 2016 than it was in July 2015, simply because of the way the days laid out on the calendar.”

That leaves the remaining 3.4% drop in sales unexplained by the calendar. So Redfin found other reasons that dented sales:

Election anxiety, stock market queasiness, and general economic malaise combined with the lack of available homes on the market to drive sales lower as well.

“Stock market queasiness” is particularly intriguing because stocks in the US kept bounding to all-time highs in July. If anyone should get queasy, it’s from being perched on top of these dizzying valuations, even as corporate sales and profits have been declining since 2014.

And there’s more to it. The report cites Luis Vasquez, a Redfin broker in Chicago:

“Recently, I’ve been getting calls from listing agents asking if my clients are still interested in homes they saw several days or weeks ago, letting me know they’ve dropped the price. It’s been about two years since I’ve gotten those kinds of calls.

“There’s a sense of anxiety among both buyers and sellers, which I think can be attributed to the uncertainty around the upcoming election and to the perceived health of the economy. Some buyers are concerned that home prices are topping out and don’t want to get caught in a market that’s getting ready to tumble back down.”

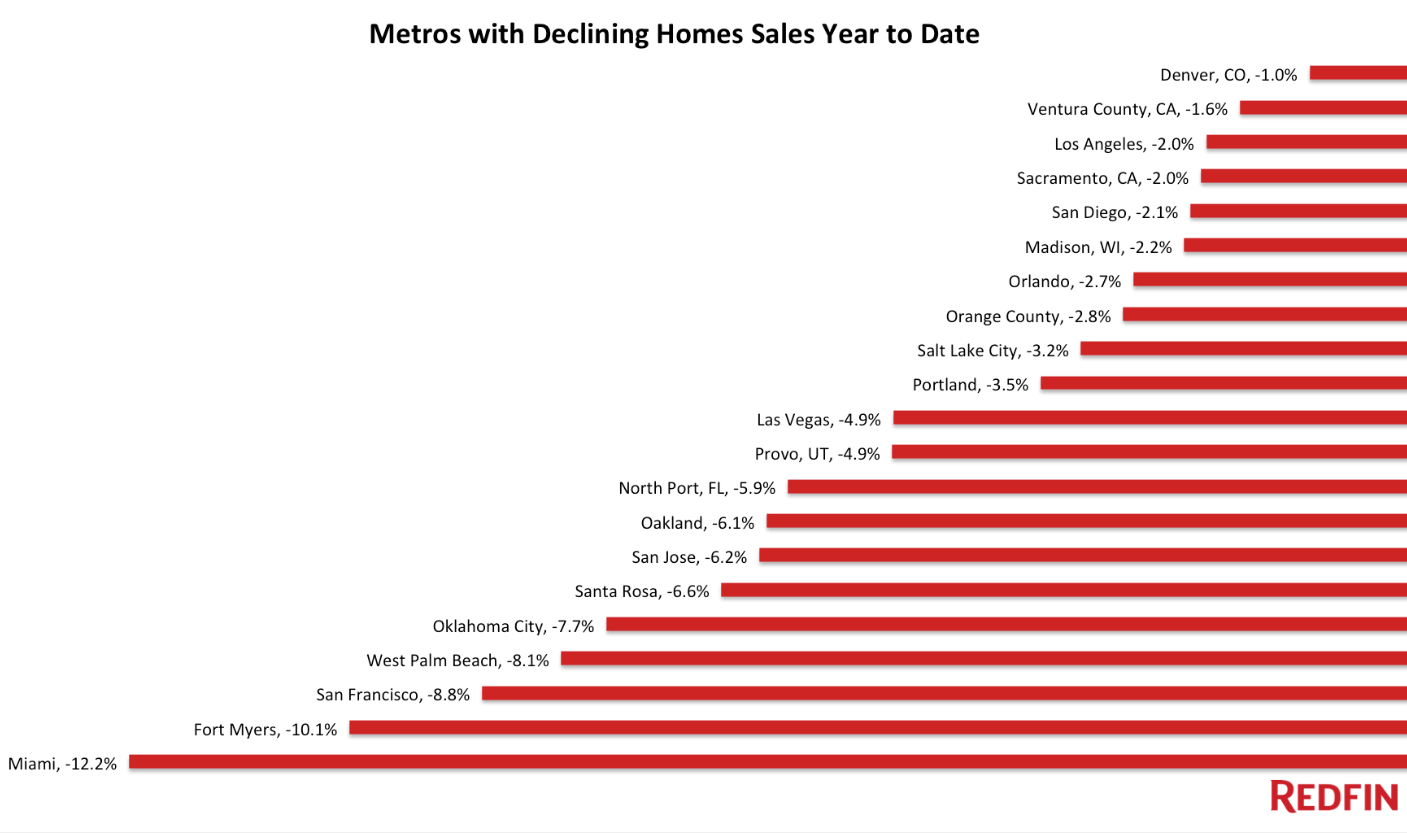

Despite the July sales fiasco, for the first seven months, sales were still up 4.8%. But that’s the national average. Some markets have started to crater, with the worst year-to-date plunges in markets whose difficulties we’ve pointed out for months: Miami year-to-date sales -12.2%, Fort Myers -10.1%, and San Francisco -8.8%. Even in Denver, once one of the hottest housing markets in the country, year-to-date sales are down 1%: Redfin’s chart shows the major housing markets with the biggest year-to-date sales declines (click to enlarge):

The above chart depicts the first seven months of the year, compared to the same period last year. But in July, compared to July last year, sales in Las Vegas, NV, plummeted 46%, even as prices jumped 7.5%. In Allentown, PA, sales plunged 32%, and in Pittsburgh, PA, 30%. Only a fraction is due to the 3 fewer selling days. The rest is due to market conditions.

Real estate is local – until enough markets hit the skids. Then it’s no longer local.

According to Redfin, there were four cities with year-over-year price declines of more than 1% in July: Washington, DC (-3.8%), Hampton Roads, VA (-2.2%), Albany, NY (-2.2%), and St. Louis, MO (-1.4%).

Home price changes are apparently the hardest thing to measure. A number of entities attempt it, each with its own methodologies, tricks, and devices, among them: the Census Bureau, the S&P/Case-Shiller, the National Association of Realtors, CoreLogic, local and state indices based on Multiple Listing Service (MLS) data, or brokers like Redfin that rely on data from their own brokers. They never agree on the median price and the magnitude of the price changes. But eventually, they tend to agree on the direction.

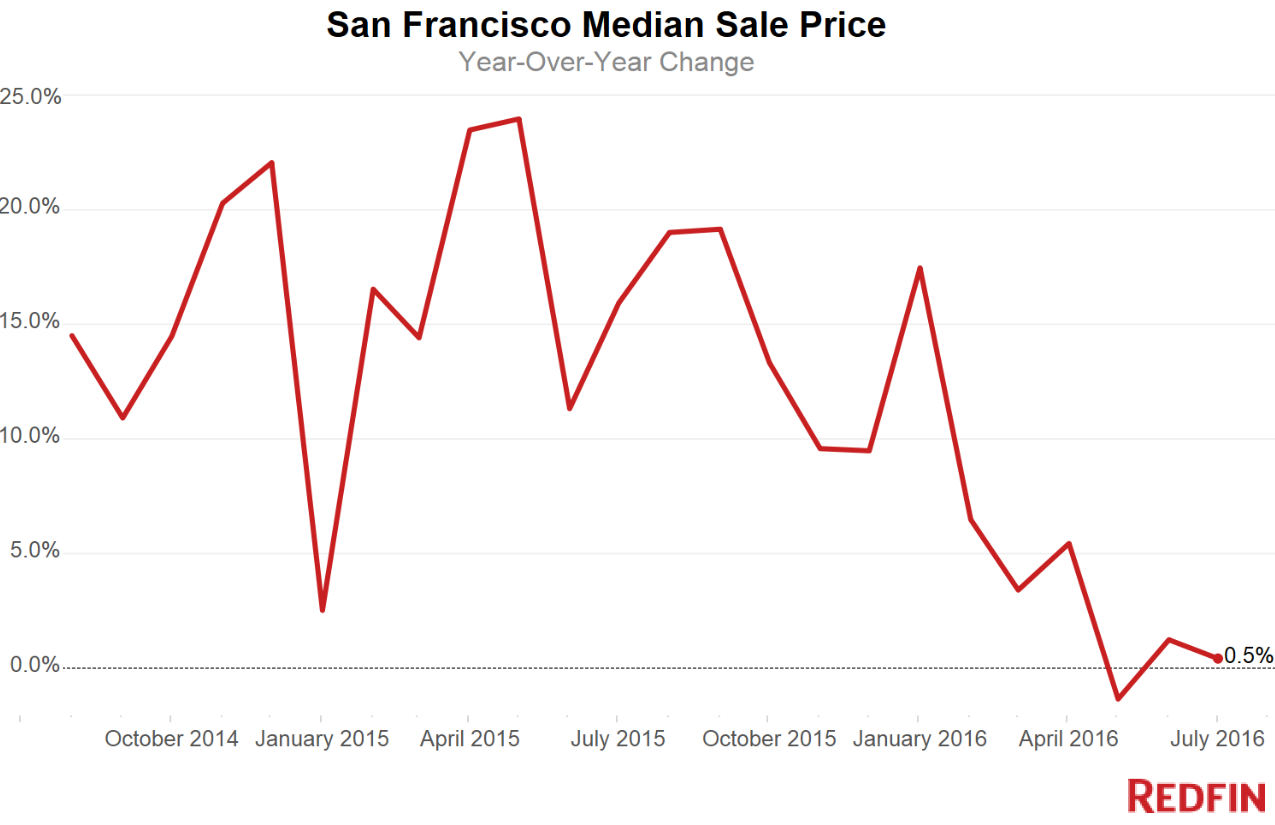

So in San Francisco, one of the formerly hottest housing markets in the US, home sales in July plunged 13.6% from July last year. And according to Redfin, the median price, after soaring in the double digits for four years in a row, inched up “less than” 0.5% to $1.2 million:

CoreLogic, in reporting on the nine-county San Francisco Bay Area, also noted a 13.5% plunge in home sales in July, but was somewhat less benign about prices: across the Bay Area, the median price dropped 6.3% from July last year.

This comes as homes for sale in San Francisco have shot up to more than a two-months supply, according to Redfin, “a rarity in a city known for its tight housing inventory.” Inventory has been rising every month since December, with single-family inventory now up 39% from a year ago, while condo inventory “has nearly doubled.”

Thousands of new condos are being completed every year in a historic construction boom. These units started hitting the market two years ago and will continue to do so for years to come.

But here’s the problem with the condo inventory: the numerous condo towers being completed have their own sales offices. Their units are not listed in the MLS. Redfin doesn’t get to sell them. So they don’t show up in Redfin’s data, or anyone else’s data. They only show up once the new owner tries to resell the unit.

This massive supply of new condos is murky, on purpose. No one needs to know if they’re hundreds or perhaps thousands of units either on the market or soon to be on the market. But that inventory is real. And trying to keep it in the shadow is part of the game.

In that respect, Miami is ahead of San Francisco. It too has a phenomenal condo construction boom, but condo resales are plunging, inventory is soaring, and developers are just “sitting” on their units, in a market that “could get scary.” Read… The Pooh-Poohed Doom-and-Gloom Scenario for Miami’s Condo Bubble and its Lenders Has Arrived

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf,

That is just terrible news for investors. Seems like housing bubble 2.0 is out of runway.

In some markets, it sure looks like it.

Of course Miami is off, the Federal anti-money laundering campaign now includes Miami [and also San Francisco and LA, among other places]. It will take a while for that to play out, and reach a new equilibrium.

Nobody cares about the Feds in Miami. They would find your comment amusing.

Last summer, in Florida, I saw houses in my development sell for record prices. Most of these households could afford to pay more because they had multiple adults (2+) working to pay the bills.

This consolidation would explain why you would get record sales last year, followed by a deep drop in demand this year. People have doubled and tripled up in households and cannot afford to form new ones.

We couldn’t doubled up, we had to downsize to a smaller cheaper house. House sales are dependent on income which has trended down for years. Anyway you look at the trend, demand is going to be down. Eventually, you hit the brick wall of not having that extra dollar.

It would be helpful if the number of listings was included in the data dump as well. A drop in volume sold co-occurring with an increase in price could also suggest that the supply curve has shifted – for whatever reason – and that there were fewer listings. Not saying that that what has happened – just hard to evaluate otherwise.

In the article:

“All homes for sale (the “inventory”) fell 6.6% from a year ago.”

“Given the plunge in sales, supply as measured in months at the current sales rate edged up 0.1 points to 3.2 months.”

What I also pointed out at the end of the article is that big developments, such as condo towers in San Francisco, have their own sales offices and don’t list the new units for sale with the MLS. These new condos don’t show up in the numbers, nor are they sold through brokers. So this very large supply in some of the biggest markets remains in the shadows.

They only show up in the listings when the original buyers try to re-sell them.

Thanks for the reply Wolf. I know supply is a difficult thing to measure since, as you point out, there is a business timing aspect to listing.

Wolf, I am a Broker Associate in Sonoma County and a few months ago I started getting invitations to “Broker’s Open Houses” at some of the new Condo towers in SF.

Free food, free booze and in some cases live bands.

These invites go out to every MLS member in the 9 SF Bay Area Counties…When it comes to analyzing the Sonoma County market you have to get very granular, it’s always about the money. Where the money is coming from says a great deal about the quality of the demand.

Tom, have you ever gotten those invites before?

I seem to remember reading about Chinese and Russian oligarchs laundering money through high end real estate and that both the home countries and the Feds are working to stop it-each for their own reasons. I wonder if the loss of this buyer group is affecting prices and inventory.

I’m wondering if rising tension between the US and Russia in Syria and the US and China in the South China sea have anything to do with the US government clamping down on Chinese and Russian money into the country.

I dug up a statistic of 7.6% drop for Texas in July. One month is not enough data. May 2015 was a month of dropped home sales in Texas, too. My next investment home purchase will be this winter, in a market crash or not. The current real estate market in the U.S. has benefited from rising rents, which is worth tracking. With minimum wage hikes happening across the U.S., I suspect rents will stay high. I was in Seattle recently where locals explained everything is expensive there but my bartender said her pay is up and she can afford to pay $200 for a parking spot (in a city where a car is not needed.)

A bartender earning minimum wage and dependent on tips for most of their income paying $200 for a parking space? That has to be the definition of shortsighted.

Maybe she’s afraid to ride the buses home from work at night. When I was doing that, it wasn’t comfortable.

Symptom to the bigger problem: I’m new at his kind of thinking but I’ve been looking at articles here and over the ZH for over a year now and it seems we have a philosophical/academic (?) problem.

Companies are set up to make profits. That is the only reason in a capitalist system is to make profits. But what if you no longer have to do any meaningful work as a corporation to make profits. In the old days you had to borrow somebody else’s expensive capital at a high rate (4-7%). This meant that you had to work really hard, hire the best people, to get a return on your investment to cover the cost of the expensive capital which you borrowed. Or you went bankrupt and somebody else came in a liquidated your assets to pay off your hungry creditors.

But with the price of money being so low, the incentive to make a significant rate of return is not there. What if, despite the fact that you are going bankrupt, there was still somebody out there who was willing to give you money? What if your creditors didn’t give a rats ass if you went bankrupt or not? With so much free money there is no need to take risk, no need to hire the best people. No need to invest in the future because all the money you need is at your fingertips now? There for a company/corporation to hire people to make profits is gone. The need for risk takers to make a company/corporation in order to make profits is no longer there. That is why your housing markets are tanking.

Am i seeing this right?

This system is seriously sick and in its current condition, seems doomed to fail…perhaps it’s time to make money hard to get again so that there will be something worth striving for once again.

SG: I believe there is validity to your thinking. I am philosophically predisposed to believe that too much of anything is not a plus, and may even be disastrously detrimental. At the very least, all the cheap money available is distorting the system.

fully agree, this is killing the real economy – slowly, unfortunately so that most people won’t notice until it is too late.

And no, housing markets are not tanking at all in such a situation. Housing is booming all over Europe thanks to free money from the ECB. Every deadbeat can buy a home, isn’t it great? People who are financially responsible are thrown under the bus to make it possible.

By discouraging real investment and financial responsibility (living within your means) we will end up with a population that is all about shortsighted stupidity and endless entitlement; some day the free money will run out (or will end having any value).

I don’t think money will be made ‘hard’ again, the elites and banksters will continue this policy until the bitter end because it benefits them; nobody wants to think about the longterm fallout.

You are correct that companies no longer need profits to survive. This goes all the way back to the corporate raiders of the 80’s, it was about unlocking value thru higher stock prices.

Micheal Milken made it acceptable to raise money for companies already near bankruptcy. The companies didn’t have to make a better widget, they needed to raise stock prices and cover debt service until they could roll over the debt, again.

Most of the big chains run on Wall St. money, not on profit margins. As investors pull out, you will see who is swimming naked.

I’d draw a distinction between large and small companies:

large companies (Fortune 500 – currently all have revenue over $5B) can go longer without profits than smaller companies. Example: GM failed to earn its cost of capital for 20 years before it entered bankruptcy. They can sell assets and live off cash flow (among other financial tricks).

Fortune 500 companies employ 26M, or about 1/6th of the US working population of 126M. Smaller companies do not have anywhere near the financial flexibility of large companies.

Not making a profit in a smaller company means costs have to be cut much sooner than in a large company.

The financial system is simply stacked against small business nowadays. Big business can loan money for free through the bond and stock market and hide its cash in tax heavens while small business cannot get any loan (or only at outrageous rates). And how could a company live off cash if the cash is taxed and inflated away at every increasing rate, and constantly at risk of bail-in?

“Symptom to the bigger problem:” Yes indeed!

Another negative, to add to the litany of economic negatives.

It’s the fundamentals – across the board that are negative.

People. Start connecting the dots. The picture that resolves is grim.

Yes, the economy for regular people is broken. That includes investors who are not multi-millionaires. Jim Sinclair, Jim Willie, Bill Holter, David Stockman, Peter Schiff and the rest all talk about how “free money” ruins the real economy. I am astounded that more people aren’t cluing into the sea change…including the “smart investors.” Not much in the US economy is real. The other countries don’t want our agricultural foods due to GMO & labeling issues. The US is really going 3rd world. None of the other countries will care about our problems since we caused so much trouble for them.

Recently, my rent was raised. By 20%! I live in Stockton,Ca. So I looked to buy. What I found was houses bought on auction for cash only a few months ago and being listed for double.

I understand cash discounts, but with interest rates at an all time low, how is the cash versus mortgage spread remotely justified? Yet the policy makers do nothing?

People need a place to live yet the policy makers have nothing to offer but what amounts to a lottery ticket based economy: don’t play you can’t win thought the odds are atrocious.

if money is free (not cash but debt, really) it makes a lot of sense that paying cash is rewarded. However, I see nothing like that in europe where money is free (or sometimes cheaper than free, if you buy a home).

In my country houses bought on auction often sell for strong (20-40%) discounts but this is because of collusion of the RE mob. Ordinary citizens have no chance buying at these discounted prices, in fact if you buy at auction the chance is pretty big you would overpay.

I agree with the “Don’t Panic” making one nervous sentiment. Does anyone in authority ever tell you to panic? The financial industry and its fraternal twin, the real estate industry operate like the Captain of that Italian cruise ship. They just slip quietly into a lifeboat and slide away into the night. Everyone else? You are on your own.

I’m not sure how people would actually panic, just stop buying the hugely inflated property?

They will do that anyway soon as they are unaffordable – I think your lifeboat analogy is the correct on – his ‘don’t panic’ message is basically saying ‘give me a few days head start..’

Gravity is now in charge of property prices, but in the areas where work is plenty I’d expect a lot of price stagnation.

In the Netherlands, where the housing bubble is almost 30 years old, prices also increased about 5% compared to previous year, which was the largest increase in 12 years (the biggest surges with many years of more than 10% increases happened in the nineties and after introduction of the euro in 2001). But this was also with the largest sales volume ever (according to the realtors, don’t know how reliable that is).

Nothing cures sagging sales volume like more government intervention and free money. Why would buyers refuse to pay ridiculously high prices if they are paying with OPM?

As for murky condo supply, same story. In a nearby seaside town there are some condo towers that are 75% empty and have been empty for many years. you don’t need statistics to check, these condo’s are dark every evening. Again, nothing that NIRP/ZIRP policy cannot fix. Why would owners use or rent out a condo if it appreciates anyway thanks to central bank policy (plus ultra-generous income tax deductions as a bonus)? Even without increasing valuations the condo’s are a far more attractive investment than money in a savings account which is heavily punished.

Vacation homes near the coast same story. This year we had a 350% increase in building on the coast, most of it in protected areas where building should not be allowed at all. Most of these homes will remain empty except for maybe 2 weeks in the summer, they are primarily a tax-friendly store for easy money that the elite receives from the ECB.

Completely agree: The Netherlands is having housing bubble 2.0:

https://www.cbs.nl/en-gb/news/2016/34/largest-house-price-increase-in-almost-twelve-years

And, sales volumes seem to be up too:

http://www.kadaster.nl/web/Zakelijk/Vastgoedcijfers/Aantal-woningen.htm

Given Redfin’s statistics, I would like to know what the government will report – on a seasonally adjusted basis of course. Anyone wanna bet that the Fed’s numbers show an increase in home sales? Or that the realtors association shows a sales increase?

Just based on current events, I expect New Orleans RE to do well because of the disaster in Baton Rouge. Many of the people now in Baton Rouge originally moved there because of Katrina and never went back. Now they may have to go back because Baton Rouge has been badly and widely damage by the flooding.

The estimate is that currently 60K homes have been damaged or destroyed. I don’t think the city can restore the damage quickly.

The people of Baton Rouge were underwater, as Obama was hoping for an under par, while he was vacationing on the east coast. When asked why he wasn’t going to Baton Rouge post haste, to help hasten aid to citizens, he replied ‘that he wasn’t going anywhere until after Billie’s (Clinton) 70th birthday bash.

Meanwhile, Hillary takes a private jet to travel 20 miles, so she may attend a fund raising dinner, with a purported cost of $100,000 per plate! The east coast elite establishment entertaining their puppet choice to occupy the white house, with their dough, ray, me!

Don’t be silly. Why would he go there if the golf courses are all under water.

A little fairness please. In 2011, when a tornado cut a swath through our town of a 100,000, President Obama visited after coordinating with the local and state leaders. And we are a red state like Louisiana. And the Federal money did flow. I have heard no complaints regarding FEMA or other Fed assistance.

That night he ordered the bin laden operation to go forward. Is that multi-tasking or what?

“Redfin data shows that the lion’s share of closings happen on Fridays. Homes very rarely close on Saturdays or Sundays.”

“This July contained a below-average number of business days (2.3% lower than average) while July 2015 had the most favorable day-of-week setup for closings of any month on record (5.3% higher than average).”

However Friday July 3, 2015 was a holiday so there were only 4 closing Fridays in July of 2015. There were 5 closing Fridays in July of 2016.

http://www.marketwatch.com/story/this-is-the-best-time-in-history-to-invest-in-real-estate-2016-08-22

http://www.bloomberg.com/news/articles/2016-07-18/it-s-not-a-housing-bubble-it-s-just-expensive

hmmmm, who to believe ….. who to believe? /sarcasm/

I can’t imagine better contra-indicators than corporate media sources desperately trying to convince everyone “all is well”.

One of my favorite quotes:

“This is far and away the strongest global economy I’ve seen in my business lifetime.” – Hank Paulson July 12, 2007