Bond-buyback miracle-nonsense flops. Shares, CoCo bonds plunge.

Deutsche Bank – “the most important net contributor to systemic risks,” as the IMF put it last week after a lag of several years – is having a rough time. Shares dropped 4.2% today to close at a new three-decade low of €11.63, down 48% since July 31 last year, lower even than the low during the doom-and-gloom days of the euro debt crisis and the Global Financial Crisis.

It’s not the only European bank in trouble. Credit Suisse dropped 1.7% today to CHF 9.92, another multi-decade low, down 63% since July 31. Other European banks are getting mauled too. The European Stoxx 600 banking index dropped 3% today to 117.69, approaching the Financial Crisis low of March 2009.

If July 31, 2015, keeps showing up, it’s because this was the propitious day when Draghi’s harebrained experiment with negative interest rates and massive QE came unglued, when European stocks, and particularly European bank stocks began to crash.

Deutsche Bank is so shaky that German Finance Minister Wolfgang Schäuble found it necessary to stick his neck out and explain to Bloomberg in February that he has “no concerns about Deutsche Bank.” Finance ministers don’t say this sort of thing about healthy banks.

At the time, CEO John Cryan – whose main job these days is propping up Deutsche Bank with his rhetoric – explained ostensibly to frazzled employees that the bank’s position was “absolutely rock-solid, given our strong capital and risk position.”

Days later, he followed up his rhetoric with a stunning ruse: On February 12, the bank announced that it would buy back $5.4 billion of its own bonds, including some issued only a month earlier.

“The bank is using market conditions to buy back these bonds at attractive prices and to cut debt,” CFO Marcus Schenck said at the time. “By buying them back below their issuance value, the bank is making a profit. The bank is also using its financial strength to provide liquidity to bond investors in a difficult market environment.”

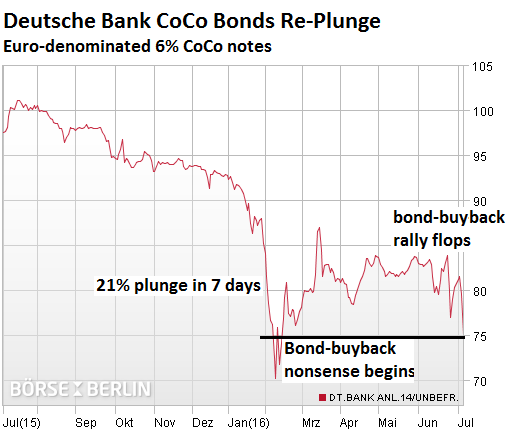

Shares soared 12% on the spot! Its bonds rocketed higher. Even its contingent convertible bonds, the infamous CoCo bonds, though they weren’t part of the buyback plan, bounced. For example, its €1.75 billion of 6% CoCo notes soared from a record low of 70 cents on the euro on February 9 to 87 cents by March – a 24% move!

The ruse had worked! During the miracle rally, short sellers got their heads handed to them.

But it was one of the silliest, most desperate ways to prop up shares and bonds. And now the bond-buyback miracle-nonsense rally has collapsed, with shares at a new multi-decade low, and with bonds swooning.

This is what these 6% CoCo notes did: they plunged 5.7% today to 75 cents on the euro. Nearly the entire bond-buy-back miracle-nonsense rally has re-collapsed…

These CoCo bonds are a gem. To prop up Tier 1 capital, Deutsche Bank raised nearly €20 billion in 2010 and 2014, by selling shares, which diluted existing shareholders, and by issuing “contingent convertible” bonds, spread over four issues in dollars, euros, and pounds.

CoCo bonds, designed to be “bailed in” so that taxpayers don’t have to foot the entire bill, are a measure of how likely investors think a bail-in is.

Cocos are perpetual: they have no maturity date, and investors may never get their money back. But the bank can redeem them, usually after five years. Annual coupon payments are contingent on the bank’s ability to keep its capital above certain thresholds. If the bank fails to make that coupon payment, investors cannot call a default; they have to sit there and get used to it. And if the bank’s capital drops below certain thresholds, CoCos get “bailed in” by getting converted into increasingly worthless shares.

In return for these risks, CoCos offer a juicy annual coupon of 6% or higher. Investors, blinded by NIRP, jumped on them at the time. For example, the 6% euro CoCo notes traded at 104 cents on the euro in early 2014 shortly after they’d been issued, and at 102 in April 2015. Investors are ruing the day they didn’t sell!

The crashing shares and CoCos have a gloomy importance. Deutsche Bank will need to raise more capital to rebuild its buffer, fund more bad-loan losses, and pay more legal settlements for wrong-doing that keeps oozing from the woodwork. To raise capital, it will need to sell more shares and CoCos. With both crashing, it’s going to be tough. It’ll dilute existing shareholders, who are going to dump these shares in anticipation, which will sink them…. And issuing 6% CoCos when their brethren trade at 75 cents on the euro, or below, is going to be very expensive or perhaps impossible.

Italy is in the middle of a white-hot banking crisis. Risk of contagion in Italy and far beyond is huge. Read… Investor Fears Spike as Italy (and the EU) Inch Closer to Doomsday Scenario

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf,

You have been great at documenting this mess. What the heck is the endgame in this thing? Why the heck would any sane individual buy these instruments?

I don’t really understand this market, but I can hazard a guess as to why a sane individual would buy. I’ll bet the answer has to do with brokers who are peddling this stuff to the average uninformed investor with some brilliant lies about how this represents a great opportunity because this is all gonna come out fine. The governments can’t let the banks fail. The longer the game can go on the longer it will be before the situation crumbles.

I just finished watching The Big Short, based on Michael Lewis’s brilliant book. This seems to be the same stuff going on. People who don’t know and don’t care sell to people who don’t know and the sellers pocket the commissions.

I have tried to tell some of my well educated friends how dangerous the world’s economic situation is today and what the effect of the disastrous CB policies will be. They all look at me like I am a charming but harmless old sheepdog.

DB will be bailed out. They are too big to fail. They will use the Fed TARP example for Bank of America, Citibank, AIG, etc?

Deutsche Bank today remains by far the largest German bank, with assets of 1.7 trillion euros in April 2016. The second-ranked German bank, Commerzbank, has assets that are about a third of those of Deutsche Bank. At one time DB was the largest bank in the worlds measured. By 2012 it ranked third in the world by assets. As of April 16th it is 7th.

Agree!

But who will get bailed in? These days, that’s the question.

Uninsured depositors will not get bailed in, I’m pretty sure (?) of that.

Insured depositors will CERTAINLY NOT get bailed in.

Stockholders, CoCo holders, and some junior bondholders will likely take a (more or less big) loss. Then taxpayers will be forced to do the heavy lifting.

The problem is not merely that Deutsche Bank may be too large to be effectively bailed out. The problem is that if DB needs that fateful bailout, so will have many other banks, starting from Italy’s Unicredit. The bill may be simply too massive to be paid.

And it also raises another big big problem. A non-binding referendum already descending into farce has been enough to cause the EU to be rattled to the bones: yet another bank bailout at European level would have catastrophic consequences.

Switzerland has legally binding referenda: if people vote against bailing out Credit Suisse, that’s it. This system is the relief valve which has so far prevented even more mayhem in the already fractious and tribal Swiss politics.

But Germany, Italy, Spain, France and Austria have no such relief valves and their present governments have already shown time and time again they struggle to understand why their approval ratings are in the gutters.

To get back to Deutsche Bank and its brethren if the past couple years have shown us something is that any action, no matter how “extreme” by the ECB can at most create a short-term minibubble in stock and bonds values. This is great if you simply care about trading, provided you sell before air hisses out of the bubble.

The main problem I have with DB CoCo’s is the yield. It simply does not remotely reflect the risks these bonds carry. 6% may seem like a lot in the present climate, until one remembers CoCo holders would probably the very first to be forced to eat their losses.

I get the same feeling. I work with people who are primarily in the late twenties through forties and most have families. In auto sales, you can make a fairly large amount of money regardless of education level. However, they spend it as fast as they make it. Some are starting to get a little concerned about the economy. When asked, I recommend at least a bit of survival equipment and some cash set aside at home. They do laugh if I mention gold or silver. When the banks close down for a few days when the balloon goes up, they will have nothing but useless pieces of plastic.

Maybe I am the crazy one but I don’t think so…

You most certainly are NOT and your friends wont be laughed soon Bookdoc believe that

Not to be a party pooper, but what would people do with gold and silver? I never get a good answer on that one. Most people don’t own gold and silver (save for small amounts in jewelry). 99.99999% of people have never transacted a single thing in gold and silver, and never will. Even if they personally do own gold or silver, the idea of doing anything with it other than putting it in a lockbox or selling it for paper currency is totally foreign and archaic to them. You’re not walking into the local saloon with your six shooter and a couple nuggets of gold looking for some whiskey. Think someone will sell you a loaf of bread for a shiny piece of metal any faster than they would for a shiny piece of plastic?

If things really fall apart in some utter collapse doomsday scenario, here’s a short list of things that are more valuable as a currency in 2016 than gold and silver: food, water, clothing, weapons, and drugs.

In the developed world, precious metals are nothing more than a legacy asset to be traded; it’s near impossible to envision any scenario where they revert to currency status ever again.

Survival equipment like you mentioned is smart (even just for natural disaster situations) and would be worth more than its weight in gold, pardon the pun. Cash on hand is smart as well.

“what would people do with gold and silver?” Things can change quickly. You know the citizens in Zimbabwe learned quick when their currency collapsed. So when faith in currency, stocks and bonds is lost and investors scramble to gold and silver raising prices by 4 or 5 or more times, and every bullion dealer is sold out and everyone wants some but cannot get it then everyone will become familiar with it very quickly.

I run a business and accept bullion as payment now and will accept it then.

Who is buying? My bet is on politically well connected hedge funds; they pre-paid for it.

They’re buying ANYTHING to get some yield. And the yield is huge. DB did make the last coupon payment….

If DB survives without getting bailed in and out, those CoCos will be a good deal, just like DB’s shares. But you better have a stomach for this sort of risk.

So far, with DB shares and CoCos, the principle has been: buy high, sell low – or buy low, sell lower.

DB will be excellent buy shortly.

I have my eye on them for the past six months.

There is always dead cat bounce before total collapse.

Happy investing.

Perhaps, but I wonder. DB is the issuer for an obscene amount of derivatives. The figures I’ve heard are so large as to

defy any attempt at paying out. and if they default, no government including ours has enough money to bail them out.

I realize full well that the amounts in question are “notional values” but lets be serious, the holders of those derivatives are going to demand full settlement, not some token payment. They will appeal to whichever courts they can and DB may not be worth much when the lawyers get done.

Speculating.

Marking a rare bright spot among gloomy emerging markets, Argentina sold $16.5 billion of sovereign debt on Tuesday in its first international bond issue since its record 2002 default.

Most proceeds from the auction, which was four times oversubscribed, will go to finally settling Argentina’s messy legal dispute with investors over unpaid debt that emerged from the $100 billion default that plunged millions of middle class Argentines into poverty.

http://www.reuters.com/article/us-argentina-bonds-bids-idUSKCN0XG2W0

Lined up around the block to buy trash…. that’s what happens when ‘safety’ = ZIRP or NIRP….

Hi Wolf,

Does DB still have access to the FED window as they did during the melt down? Open windows invite thieves.

I remember quite well how they got a staggering heap of cash from the FED ( which they lent to Blackstone to buy 40,000 houses from Americans that played on the wrong side of the street and offered to do the tranches on the rents ). To bad those home owners didn’t get the help instead of a GERMAN bank.

That was DB’s US operation. In theory. In practice, money is fungible and can go anywhere.

:-]

DB isn’t facing a liquidity crisis (not yet). It’s facing a crisis of not enough capital to digest potential losses. So a bailout would require a capital injection of some sort, not a short-term loan.

Another option would be for a central bank or government to take some of these potential losses off the bank’s book, like the Fed did when it bought rotting MBS.

Let us call them “DoDo Bonds”

Sane individuals don’t buy these instruments, flash computers buy these instruments and then quickly they are quickly pump and dumped to insane investors coming in too late.

I’ll start the line waiting for Wolf’s response!

Well if they are all screwed I don’t see how anyone can complain if the good Doctor Draghi dispenses his medicine: a bunch of euros.

At least no one in the euro zone.

As to the US or UK reaction if the euro were to lose 20-30 % that is another matter.

Nick,

I just waiting for the currency devaluation to take place. I can buy a Dacia Sandero and spare parts with a 25% discount.

More like Dr Frankenstein or is it Frankensteen?

Taxpayers will pay for something like a TARP.

Bet on it.

This is so AWEful!

Deutsche Bank and the rest of the European banking system is inching closer and closer to collapse, yet US stocks soar. Are we back to “bad news is good news”?

Since when hasn’t bad news been good news….

It’s not exactly soaring. Year on year the S&P 500 has barely moved.

But compared to stock markets worldwide it’s doing great… for the simple reason investors are pouring into less risky assets. Which right now means move away from Europe. Even the usually reliable ChF has seen some pretty wild swings in the last month or so while the “thrashed” yen has been going from strength to strength in the same timeframe.

Traders who started hitting the “panic buy” button with Italy’s Unicredit about three weeks ago have got crushed time and time and time again. Not even the massive LTRO extension on Black Friday saved them and the Italian government’s press releases this week have failed to drag Unicredit above the €2 mark.

Unless one is able to play on the short timeframes these minirallies last he’s bound to get bloodied time and time again.

Compared to earlier this year it is soaring, yes it probably has (finally) topped again, but for some reason the bad news from Europe didn’t send them plunging like it was earlier this year. Maybe it’s still too early.

İve read that we should all watch for DB to hit single digits and at that point the true collapse is here More QE Janet? GOT GOLD?

Perhaps Deutsche Bank should hire some Greek auditors ;-)

“Perhaps Deutsche Bank should hire some Greek auditors ;-)”

Goldman Sachs?

The demand for investment instruments went up and up as the Boomers were socking away savings for retirement(demand).

Now they are retiring and they are withdrawing that demand….

Decrease in demand>>>>>increase in supply>>>>a lowering of prices

I forget which analyst pointed this out shortly after Y2K, but it was stunningly correct.

Dan Amerman. The guy is brilliant, btw.

Ultimately, the taxpayer is the one getting bailed in as more private debt becomes socialized through Tarp-like measures. German national debt will grow just as American debt has grown from these measures. I think we are going to see massive sovereign default on a global scale in the coming years (perhaps months?). Get ready for wide scale economic re-trenching when this happens. Let’s hope that’s all that happens. After all, this is the stuff of revolution and war.

The German taxpayer has already contributed, generously I may add, to saving a few of the Landesbanken, with BayernLB and HSH Nordbank standing out.

As Landesbanken are owned by local governments, these bailouts are “local” in nature and involve the Lander not as white knights but as owners: under present rules if owners eat their losses it’s technically not a bailout, even if taxpayers are ultimately on the hook.

Part of these problems were caused by the little talked about bust of Austrian bank Hypo-Alpe-Adria, one of those financial disasters not many like speaking about.

There’s still an ongoing shouting match, with lawsuits flying in both directions, about who’s ultimately responsible for this fiasco. It will take years to decide and by then there will probably be much bigger fish to fry.

I had a brief chat yesterday with a friend of mine who is a conservative and successful investment advisor. “Nick, how long can we go at zero interest and in some cases negative yields?” I asked.

His answer, without hesitation, “Forever; this thing is going to be at least a generation. There is no growth anywhere in the world, and nothing but debt. There’s no way interest can go up!”

I reckon he speaks the truth, and the Central Banks have changed the rules from capital having cost to capital being issued to borrowers at no cost, or in some cases, borrowers paying back less capital!

The natural order of free market capitalism has been “Shaken, not stirred”.

I share your friend’s opinion, Dan, but I disagree that this ZIRP and NIRP can go on “forever” or for a generation. The reason being that this destroys the whole business model for pension funds and insurance companies. Pension funds are floundering right now and as they cut back on their commitments to retirees, and as big insurance companies also follow suit and get into trouble, sufficient pressures will be generated to guarantee another significant crisis.

Back in the 1960’s my aunt was high in government as a big lawyer and advisor. I remember her telling my mother that the government was very concerned about the mobility that Americans had and how to keep track of them. My mother was alarmed that one idea was to keep them poor. Poor people can’t move so easily. When you step back and look at one pension after another, sort looks like a plan to break them in half…along with unions. You ain’t going no where when you is broke and no one sees your face.

We have no idea…none… how powerful some invisible people in this world actually are or what plans hatched 50 years ago are maturing right now. Just look at what was conceived in 1913 and how that plan is playing out before our helpless eyes.

Some things are done for the next generation, not yours but theirs!

The idea that a secret financial cabal runs the world- keeping people poor- turning wars on and off for profit was a key plank in the platform of the National Socialist German Workers Party.

The key factor endangering pension plans in the private sector is demographics- not only are the baby boomers are retiring, they tended to come from larger families. They boosted the economy abnormally while working, due to the number of them. Now they are a brake on the economy due to the number of them.

This is especially true in their effect on medical costs- it’s the one thing you consume more of as you age.

The birth rate has been down everywhere in the developed world for decades. Result- there are not enough workers to support the pensions of retirees.

But where is the nest egg from their deductions, with accumulated dividends?

In many cases the company failed to make its share of contribution, or went bankrupt, and in some cases the pension fund was looted. Illegal but once it is discovered, we know who is responsible. In the case of one UK media tycoon who did this, he ‘fell’ off his yacht.

Depending on where you live, the government deduction may have entered general revenue- just one pocket, not a separate one. So if the government is bankrupt (Detroit) it no longer exists. Looting of a legal kind.

And there is the lowest interest rates in centuries, which makes it hard, or impossible, for a pool of pension money to generate an adequate return.

Some of the above are criminal, and are probably under prosecuted, but none of them require a government conspiracy, or a conspiracy extending beyond a few corporate insiders.

The plan for 1913 was in play for decades. Soon after the US became a nation, moves were on for a (private) central bank.

What do you do when your favorite silver miner slips 15% at the open? Been there done that….

“DB isn’t facing a liquidity crisis (not yet). It’s facing a crisis of not enough capital to digest potential losses.”

I’m not comprehending the difference between not enough capital and lack of liquidity.

I’ll give it a shot, via a simplified example:

Say you own a home that is worth $250,000. You owe $100,000 on it. But you got a cut in pay. You can still make your mortgage payment, but you can’t pay for your kids private school because you don’t have enough cash. You have $150,000 of equity in the house. That’s part of your “capital.” But you’re short on “liquidity” to pay for your kids’ private school. So you charge your kids’ school expenses to your credit cards. When the credit cards are maxed out and you cannot borrow anymore, you have a “liquidity crisis.” But you still have the capital (equity) in the house. You don’t need to default because you can sell the house to get flush again. So with your good capital, you can solve your liquidity crisis.

Now in another example, say you owe $300,000 on your house that is worth $250,000. So you have “negative equity” of $50,000 (negative capital). You get a cut in pay. You charge up your credit cards until they’re maxed out. Now you can’t make the credit card payments and you fall behind on your mortgage. You have a liquidity crisis that you cannot solve by selling your house because you don’t have any “capital.”

FREE Hair Cuts for Everyone ! Yippee !

Got it, thanks. I owned that one @ $33 and managed to sell @ $34 right after they began selling assets that sounded fishy so barely got out by the skin of my teeth.

Seems like they should be able to borrow infinite amounts at negative rates, it’s refreshing to think they can’t.

I just read that stockholders lost $0.5 trillion on the largest 20 global banks so far this year. And probably a lot more since July 31, 2015, when the bank-bloodletting started.

If I have some time, I might run the numbers for those banks. Could be $1 trillion. The Japanese banks have totally gotten clocked too. Like Mitsubishi UFJ is down 52% in 12 months.

The EU needs a big disaster to roll up all the debt into an SDR. A DB collapse would be just the big disaster to justify it.

They have been writing about this scenario for a few years now. James Rickards wrote an entire book on it, “The Death of Money”. If you read the book, note that the entire scenario was laid out as a war game at our favorite intelligence agency. An SDR roll up is the only way to kick the giant derivatives can down the road. I expect it any time now.

1960’s: My dad kept complaining about the Millions of Dollars of Government Debt. We are all going to be ruined.

1970’s: My dad kept complaining about the Hundreds of Millions of Dollars of Government Debt…..

1980’s: My dad kept complaining about the Billions of Dollars of Gevernment Debt…………..

1990’s: My dad, who was soon to die, kept complaining about the Hundreds of Billions of Dollars of Government Debt…..

2000’s: I started reading Financial Blogs where everybody sounded like my deceased Dad. They kept complaining about Trillions of Dollars of Government Debt………….

2010’s: (Do you see where this is going?) EVERYBODY is still complaining about the Hundreds of Trillions of Dollars of Debt…..

So, how long can this go on? What comes after “Trillion”? In the 1960’s the smart people worried about a few Million, yet it is 56 years latter and it keeps on going….as it shall. When we use paper notes as “money” (which it can not be), there is really no difference between “Million, Billion, Trillion and the next word to be used”.

We’ve been a debtor nation since the 1800s. We have only been a creditor nation for– quite literally– a handful of years in our entire history. And for sure, it has gotten worse in the last three decades for a number of complicated reasons (mainly demographics, globalization), but generally speaking, the sky is not falling (yet).

How long can this go on? That depends.

Consider this… and generally I use this as a rule of thumb for whether people know what they’re talking about or are just parroting talking points:

The US has a NET worth of about $120 trillion. That is net, after accounting for the roughly $150 trillion in public and private debts.

The US deficit to GDP in 2014 was just under 3% (deficit, not debt). During the Civil War, deficits ran as high as 10% of GDP… 20% in WW1, 30% in WW2, 5% for most of the Reagan administration.

And your timing is off regarding people in the 1960s worried about a few million, considering that by 1816 the national debt had already reached over $100 million… 150 years before your dad was complaining.

Throwing out large numbers when talking about debts and deficits is a scare tactic that ignores the country’s ability to pay those debts and deficits. In and of itself, there is nothing wrong with increasing debts– so long as they are used to support wise investments. Of course, I’d argue that increasing debts so you can cut taxes for the most opulent generation to ever walk the planet (baby boomers) has been a poor decision when our education and infrastructure (things that I’d consider wise investments) are lagging, but… that’s just me.

@Smingles

I agree that “Throwing out large numbers when talking about debts and deficits is a scare tactic” used. Context is important and that is what you did very well. How did you arrive at “The US has a NET worth of about $120 trillion”? Does that include stock market and RE properties? If so, then consider when the stock and property markets crash (not if but when) the net will be negative. Yes there will be defaults on debts as well but then you and I will pay for it via central banks money printing which is an indirect tax whether you and I have income or not. Debt matters a lot. This is a rentier economy not a producing economy. When we don’t produce enough we have to borrow and print money. That does not solve the problem. It only postpones it.

Millenials are age discriminators, that’s baby boomers fault as well.

Let’s move from the 1800’s and WWII a little closer to now.

When Reagan took office the accumulated debt of the US after two world wars, Korea and Vietnam was one trillion dollars.

Reagan ran on the GOP platform of smaller government, less spending, lower taxes ( what else?)

Four years later the debt accumulated since 1800 was two trillion.

It had doubled in 4 years.

The Fed thinking is quite simple, as long as the GDP grows faster than the money/ credit supply it can inflate its way out of its debt

just like the real estate believer pre-2008.

The trillions thrown at the deflationary scare of the Great Recession have failed to reach the inflation target necessary for the largest debtor in history to begin reducing the debt.

Instead, after all this stimulus, the US by any number of measures (#1. Inter- modal transportation down sharply ) is about to enter recession, followed by disinflation, if not deflation.

This era has nothing in common with the past. Stimulus like this in the 60’s or 70’s would have produced double digit inflation.

Deflation is a disaster for the debtor- all those treasuries etc. issued at rates that made the investor look stupid, would now make the government look stupid. If it sold bills paying 1.7 %, and we have 5 % deflation, the real interest rate is roughly 6.7%.

And of course, the biggest ‘debt’ of the Federal Government is future obligations, mainly social security.

This is growing rapidly as the population ages but is not included in usual debt figures.

That depends on whether you are here in the U.S. or in Europe. The European system generally goes: million, milliard, billion, trillion, quadrillian, quintillion, hextillion and so forth. In the u.S. we drop the “milliard (equals a billion here and European billion equals our trillion) and offset the ones after by three places: million, billion, trillion, quadrillion, quintillion, etc.

Also be aware that the format in which large decimal numbers is generally different in Europe and varies from place to place. The most common difference is the role of the “,” and “.” is interchanged: 349,567,908.233 will become 349.567.908,233

They use a decimal comma rather than a decimal point. Some countries separate digits into groups of three with spaces and not punctuation: 349 567 908,233 I think there are a few other variations also.

Like the drowning person at the waters surface institutions are trying every desperate thing to keep the mouth about water for the next gulp of air. Like a drowning person exhaustion overcomes and the victim succumbs. Payback for the many previous years of ripping off the working class.

Hopefully snot-nosed millenials get to be the same beneficiary of globalization as boomers faced.

Screw them, my next smart phone will be Korean or Chinese.

There are lots of dollars out there looking for a yielding home. I don’t think the US govt debt is an issue currently as it’s more than likely the mere thought of a crisis sees money flooding into ‘safer’ USD denominated assets. Notice treasury yields while slim are attractive compared to EU / JPN.

Extrapolating from there, a rising USD is poison for dollar denom debt and this should hurt EM Corp debt. Would also means Yuan peg under pressure. Probably good for US stocks though.

Great article! Of course, CoCo was sold as a way to justify NOT fixing banks. CoCo will solve all the problems!!! One useful idiot I know testified to that in Congress. Problem is that DB’s chief economist is calling for a bank bailout despite CoCo bonds.