“Astronomical” default rates and losses.

The New York Fed just warned about the ticking mortgage subprime time bombs once again being amassed, and what happens to them when home prices decline. But unlike during the last housing bust, a large portion of these time bombs are now guaranteed by the government.

Subprime mortgages are what everyone still remembers about the Financial Crisis. They blew up as home prices fell. Folks who thought they were “owners with equity” found out that they were just “renters with debt.”

And they dealt with it the best they could: forget the debt and the rent and stay until kicked out. Cumulative default rates on subprime mortgages spiked to 25% in 2007, according to the report. Banks ended up with the properties and collapsed. Mortgage backed securities based on these subprime mortgages imploded. Bond funds that held them imploded. All kinds of fireworks began. While subprime mortgages didn’t cause the Financial Crisis by themselves, they were an essential cog in a crazy machinery.

Now, the machinery is even crazier, subprime mortgages are even bigger, and mortgage-backed securities, chock-full with subprime, are hotter than ever. Only this time, the taxpayer is on the hook.

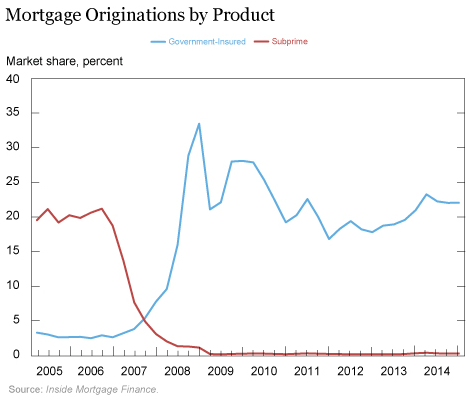

During the prior housing boom, from 2000 through 2005, government mortgage insurance programs covered less than 3% of all subprime mortgage originations, while private mortgage insurers covered over 20%.

But during the housing bust, private insurance of subprime mortgages dropped to essentially zero. And the government – through various programs by the Federal Housing Administration (FHA), the Department of Veterans Affairs (VA), and the USDA’s Rural Housing Service (RHS) – stepped in to pick up the baton, plus some, insuring subprime mortgages with a vengeance. By 2009, the government insured nearly 35% of new subprime mortgages. More recently, it still insured about 22% of new subprime mortgages.

The NY Fed’s chart below shows the plunge in privately-insured subprime mortgages (red line) during the housing bust, and how the government (blue line) piled into this business:

The thing is, according to the report:

Virtually all of these government-insured mortgages are securitized by Ginnie Mae, a government agency that guarantees the timely payment of principal and interest of these loans to investors that purchase the securities. That is, the U.S. taxpayers assume the credit risk on these mortgages.

That spike in subprime guarantees by the government in 2007 through 2009, at a time when home prices were falling, “quickly placed many of these borrowers in positions of deep negative equity.”

Many lost their jobs. Default rates and loss rates soared for these government-insured mortgages, which ultimately resulted in the FHA’s Mutual Mortgage Insurance Fund getting bailed out by the taxpayer in 2013.

By then, Housing Bubble 2 had already commenced. The good times were back. Home prices were re-soaring, and further damage to the taxpayer was put on hold. The NY Fed:

These loans are typically characterized by significant leverage, and borrowers often have checkered credit histories as evidenced by very low credit scores. For example, the FHA program allows for mortgages with an original loan-to-value (LTV) ratio of up to 96.5%; and such loans are also subject to an upfront mortgage insurance premium that is typically rolled into the loan balance, which further raises the initial LTV.

The lack of upfront equity implies that FHA mortgage borrowers are at greater risk of default than conventional mortgage borrowers.

These highly leveraged government-insured loans are also typically issued to borrowers with weak to poor credit histories, further increasing the risk of default and foreclosure. Borrowers with poor credit histories are more likely to face adverse income shocks; and the combination of negative equity and a high risk of adverse income shocks implies that these mortgages are at high risk of default.

So these subprime mortgages defaulted at an “astronomical rate during the housing bust,” and they’re going to do that again during the next housing bust.

Before the housing bust began in earnest in 2007, the median LTV for these subprime mortgages was around 98% and the median credit score was below 650. In the years since the government has taken over insuring these loans, more than 10% of government-insured loans had LTVs of over 101% and “one-quarter were made to borrowers with FICO scores in the low 600s and below.”

This combo of very high leverage and low credit score is toxic. It leads to “extremely high default rates” and extremely high loss rates.

The five-year cumulative default rate (CDR) for these subprime mortgages that were originated in 2001, the best year this millennium, was 5%. For subprime mortgages originated in 2007, it was over 25%, and for borrowers with FICO scores below 600, it was over 40%!

To put these numbers into perspective, the five-year CDRs associated with loans insured by Fannie Mae and Freddie Mac (the housing government-sponsored enterprises, or GSEs) are typically an order of magnitude lower. According to our calculations, the 2002 and 2009 vintages of GSE loans had five-year CDRs of approximately 2%, while Ginnie Mae’s same vintages had five-year CDRs of almost 10% and 13%, respectively.

Even subprime mortgages originated in 2010 have a five-year (into 2015) CDR of 8.4% despite the booming housing market over the period.

But “to make matters worse,” there’s a little bit of government hocus-pocus: these default rates “understate the share of borrowers who default, since loans that are refinanced within FHA are treated as a successful payoff, even if the refinanced loan that replaces it subsequently defaults.”

And these truly “astronomical” default rates and loss rates are very costly for the government programs that insure these mortgages.

But so far, so good, if Housing Bubble 2 continues forevermore – as it is widely expected to do, according to the housing industry, which has already totally forgotten the prior housing bust and what caused it. In that case, default rates and loss rates will be relatively small. Forever-soaring home prices assure that subprime mortgages with sky-high LTVs to borrowers with very low FICO scores don’t lead to sky-high losses.

The problem arises when home prices stall and begin to decline. That’s what the NY Fed is fretting about when it uses code words, like the “sustainability” of homeownership, in proposing some limits on this scheme. Clearly, they’re worried that Housing Bubble 2 will turn into Housing Bust 2.

This time, it’s the government and taxpayers that guarantee a big chunk of the subprime mortgages so that institutional investors that have gobbled up the subprime-based highly-rated mortgage-backed securities don’t have to take the inevitable losses.

But so far, the crazy machinery is still working, and renters are squeezed by the Fed’s “Wealth Effect.” Read… How the Government Hides Inflation, as Housing Costs Soar

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

How many loans were made to people with under 700 FICO scores? Data I’ve seen suggests the score is far more indicative of future problems than LTVs.

Percentages aren’t enough data to understand the severity of the situation. I have a hard time beliving the numbers are anywhere near what they were leading up to 2008.

If you haven’t experienced the crisis personally you don’t understand that fico scores and down payments don’t matter. It is all about income. We lost a house we purchased with 40% down, had a fico score in the upper 700’s, and owned it for ten years before we lost it. When we lost our income, the savings went, and then everything else. Our story was the common story among the people we knew who had lost their homes.

The press keeps feeding the narrative that people are buying houses they can’t afford, but it is not true. They can afford them when they buy them and then the income can’t keep up with the rate increases, insurance increases, tax increases, and job losses.

The entire financial crisis was an income crisis not a housing crisis, and the next one will be about the same thing, but worse because everybody is now broke.

Re: an income crisis not a housing crisis

The two are linked and the bigger the real estate bubble- the more they become linked.

The mother of all real estate bubbles was Ireland. At the height of the insanity one quarter of the work force was engaged in some aspect of real estate.

There were, obviously the builders, the suppliers of material, and lest we forget, the realtors, mortgage folks etc.

And these places have to be furnished even if only ‘staged’ for sale.

Oddly, even as prices were rising 5 % a month, there was almost no international interest, no Russian or Chinese money. The Irish were going to get rich buying and selling houses to each other.

Then almost overnight it crashed. As of 2012 ( the date of Michael Lewis book Boomerang) the new convention center in downtown Dublin, built for over 100 million US$, had never been hooked up to the water and sewer. The three big Irish banks went broke and were bailed out by the government i.e., Ireland. This busted Ireland and IT had to be bailed out by the EU.

But in addition, most of those people connected to real estate were out of job, thus the connection between a housing crash and income. And of course they could no longer afford to buy houses, feeding the negative cycle.

Ireland has since made an almost miraculous recovery, thanks in large part to a very low corporate tax that makes it desirable for US (and others) companies to headquarter there and even to manufacture there.

Ireland takes some heat for this but not as much as you might expect. It is a relatively small economy so it manages to fly under the radar.

Also, frankly, I think the English speaking world has a soft spot for Ireland and at least during the crash, felt sorry for them.

This does not always include some smaller EU members and I think that is the source of most complaints.

the Dutch have been ‘getting rich’ trading houses amongst each other for 30 years or so and this bubble is still growing (despite a slight hiccup around 2008).

What the article describes for subprime mortgages in the US has been the normal situation in the Netherlands for many years. LTV is now officially down to 103%, from 110% or more in the previous bubble phase around 2000. Downpayment, are you joking? Nobody needs a downpayment in the Netherlands … And 90% of new mortgages come with a free government-backed mortgage insurance which means that you can never lose money when you have to sell the home (due to loss of work, divorce, etc.).

The Dutch bubble has been building for much longer than the Irish one. In in my home town prices for many properties have increased by 15-20x over the last 25 years, a total disconnect from incomes. All this with very little participation from foreigners (by design, because the extremely generous Dutch mortgage tax deduction and the free government put option would not apply for foreigners).

The big difference with the US (and Irish?) situation is that defaults are still very low in Netherlands. Of course they are, because rates are ridiculously low (below 1% now, and mortgage payment is fully deductible from income tax which means about 50% taxpayer subsidy for people with a big mortgage). And even if you haven’t paid the mortgage for one year, that still doesn’t qualify as ‘behind’. Renting is several times more expensive than ‘owning’, unless you are on social security.

The result: the biggest private debt bubble worldwide, and almost the biggest total debt (public + private) in the world, just behind Greece. But nobody talks about it, and the Netherlands happily presents itself as a financially and fiscally responsible country (also known for the ‘Double Dutch Sandwich’ that they don’t want to talk about).

It seems in 2013, SNS Reaal collapsed due to real estate loans and was bailed out by the government and some bondholder bail-ins. I don’t remember all the details, but were those loans a financial crisis leftover, or why did this bank collapse?

@ Wolf Richter June 22, 2016 at 7:27 am

SNS Real collapsed primarily due to bad commercial real estate loans in Spain, not because of private mortgages. There was fraud involved, but this was more of a sideline of the housing bubble (banks make crazy loans for expensive vacation properties etc. because ‘housing can only go up’).

Neither the big Dutch banks nor the mortgage insurance fund went bust when home prices declined about 20% after 2008, mostly due to political meddling (keep in mind almost everyone starts out with negative equity over here). Most banks were forced to take huge loans/guarantees from the government, and had to be friendly towards homeowners with problematic mortgages. Many mortgages were forgiven, e.g. a politician with a loan of 1 million euros for a 800K home paid just 100K and then stopped paying; he now owns his home free. Effectively, most homeowners who should have been in trouble due to negative equity were bailed out by the taxpayers, through the ‘temporarily’ more-or-less nationalized banks. In the big cities the prices are almost tack to 2008 levels, sometimes even higher; in other areas prices are still 10-15% down from 2008.

Thanks.

Wolf, I fully agree with you buffet is part of them. But it does not make his statement any untrue. Most people are bad at analyzing assets and deal with future uncertainties.

Most people think I will consume and transfer the bill to somebody else through the bank. The bank let them because the bailout is part of the calculation and it comes back to the tax payers/consumers.

The facilitate and profit and let the consumers consume each other into oblivion and debt slavery.

America was founded on the principle of freedom, which has been corrupted into debt slavery because of the 2 weakness of most people.

My take is that the state of economy and actions of banks, government is a direct result of moral corruption. But as Joker says, corruption is like gravity, all you need is a little push, and all of loans and debt are just that little push.

“income crisis not a housing crisis”

That’s a great insight Petunia. Although it’s easy to see how a real estate bust leads to job losses in the real estate industry (and others), I think your comment reflects a deeper issue. You are calling into question the structure of the rest of the entire economy, with RE being just one very visible part of the issue.

Sorry to hear about losing your home.

There are two things that makes people different.

1. Do you choose stuff over freedom? If you want stuff, borrow and consume. If you choose freedom, you do not borrow to consume.

2. How good are you at estimating future uncertainty in terms income whether it is earned or investment income out of asset. Warren buffet says most people are born bad at this game because they make decisions based on immediate past.

My take is most people are born to be bad at estimating future uncertainties. And most people choose stuff over freedom. And most people think they can use the government/insurance to transfer the consumption bill to somebody else.

In the end, you do not get what you want…

Buffett gets what he wants: his finance and insurance empire got BAILED OUT during the Financial Crisis, and he got insider information about these bailouts the NY Fed was planning, and he invested in Goldman, GE, Wells Fargo, etc. based on this insider information. And he didn’t invest in Washington Mutual, which was allowed to collapse.

He is the single greatest beneficiary of the Fed’s largess.

But folks like Petunia might not get what they want….

If you quote Buffett, you’re quoting one of the best market manipulators out there, and one of the most Wall-Street-connected individuals with massive influence on regulators and the Fed. You’re quoting the beloved avuncular face of the banking cabal.

“They can afford them when they buy them and then the income can’t keep up with the rate increases,”

Why would the rate increase if they have good credit? If you have good credit, you normally don’t buy into shady loans.

The fact is, people were getting served these crap loans from unethical banks. The banks preyed upon these people.

“I have a hard time believing the numbers are anywhere near what they were leading up to 2008”

i think they might be worse, a lot of people get on the “subprime” is the only blame band wagon but down here in the trenches i saw a much different picture. The dreaded “real-estate investor” and back then they were everywhere, I remember having some truly bizarre conversations with people that “owned” multiple properties (like i am now) with no way out in a downturn.

i think we are rapidly coming back to that. One person in particular stands out in that he had great credit and 3 houses and 1 condo, talking with this guy sounded like like an infomercial…needless to say he lost it all.

when the tide goes out we’re going to see whats really been going on.

side note: this is even worse in Canada where i read one realtor “investor” had “interest” in 18 properties.

and I suspect when the smoke clears the big players will get bailed out yet again….playing by the rules is for suckers.

Your friend with the 3 houses and 1 condo lost it all when somebody in the chain lost their job and stopped paying. Like I said, the entire housing industry is built on income. Even if we had owned our house outright, we would have lost it to the tax man.

There is now an entire market in the bonds of these big corporate renters. When the employment numbers get worse, especially where they own houses, watch out. There will be no one paying rent and no one to buy the houses.

McAffee of the virus protection software was a fairly big fish and he lost most of it. He’d spent millions on an estate with its own airstrip etc. Sold for about 10 cents on the dollar.

I personally knew a guy who lost everything in a multi- million dollar subdivision. I bought two of the lots from the bank for about 30K (this was in the 80’s) he’d spent about a hundred apiece on them.

I think the big fish swim free is a bit of a cliche.

There’s a story on the Miami Herald webpage of a rapper guy who just sold his Miami penthouse. The price started at $16M, a couple of years ago, and he finally sold it for $9.5M, a $3M loss from the $12.5 purchase price. That’s about a 25% loss in a luxury property in Miami.

Qualifying since 2010 has been as tough as it gets. Rates have been at low levels never seen before. Cash purchases also higher than ever. And volume way below the years leading on 2008. This is very conservative, nothing like what happened from 2005 to 2008. A correction is due, and a recession will probably due as well, but I don’t see it as nearly as crazy as it was back then.

The powers that be (the credit bureau) makes it very hard to have a good credit score. Even if you do everything right it takes a quite a long time in most cases to have A1 credit. Dont get me started on identity theft. Your screwed if it meased your credit up!!. Takes forever to fix problem. Credit bureau dosent cooperate as they should. Oh well its all rigged for most middle class people to pay high interest and make the rich richer!

Dumb question,

What happens during the next recession when defaults pileup?

The usual. Punish success, reward failure, and blame everyone else.

To clarify,

How are things going to be this time with the govt holding alot of the subprime.

When I lived in oakland California during the 07/08 crash, home prices dropped as much as 75% from their highs…

No one knows. I don’t see a very pretty outcome of your scenario. But -75% sounds steep in the current situation.

We’ve got to factor in the construction boom now going on in the Bay Area (and other places). There’s a huge amount of multi-family supply coming on the market over the next few years (mostly high-end). When the tech boom fizzles and the hiring boom turns into a layoff boom, these recent arrivals will go back home or head to Detroit, where life is cheaper, and there won’t be enough people around to buy or rent this supply. So high vacancy rates. Developments defaulting. Forced sales….

At least that’s how every boom here has ended so far.

The drop in prices on our street, in West Palm Beach, during the financial crisis was 65-70%. The highest priced house on the street belonged to a very young couple who put all their money into their house and it was a beauty. When the crisis hit he lost his business and the house went into foreclosure. The house eventually went in a short sale for $150K from originally over $500K, it took over a year to sell, and it was sad to see the marriage fall apart as well.

Yes, the tragedy, as you also pointed out a number of times before, is that it is NOT just financial – but real damage to real people.

I remember reading that in/after the 1929 depression, the more expensive homes in California often sold for 10 cents on the dollar just a few years after construction.

In my country home prices have gone up on average 5-6x from 1990, but in reality the gains are many times bigger because these averages have many problems (many cheap ex-rental properties entering the market when the bubble grows, big canal homes split up into 4-6 expensive apartments etc.). The more expensive properties are often 10-20x more expensive than in 1990, only most apartments have lagged seriously in many areas at maybe 5x gains, because there is an obvious oversupply of them. I have no trouble imagining huge price drops when central banks lose control and the government-backed mortgage insurance fund goes bust.

Vacancy rates in the inner city where I live, with many ‘trophy homes’ are around 10%. Many of these homes are owned by small and large speculators who simply hold on for the price gains (and sometimes probably because just like in the US, homes are an easy way to park black money), rents are irrelevant …

For many years politicians have made sure that too few homes were built, driving up prices and government land revenues. They are now starting to build more for the migrants, who knows what could happen if in a few years the economy craters and the migrants suddenly decide to head for greener pastures …

Janet needs to print more money and keep these balls in the air. There could be real trouble if the balls drop and consumption falters. Pump that wealth effect lever faster and faster. There are no limits in Japan, no limits in Europe and the only limit in the U.S. is our imagination according to the genius Bernanke. Asset prices can keep up with debt or even speed on past. Bring in new buyers from around the world. Pensions are counting on the gains.

I have already seen some interesting discussions on TV between boomers who feel entitled to their gold-plated pensions (which are beginning to be threatened with cuts because the pension funds are in trouble thanks to NIRP/ZIRP), other boomers who feel entitled to ever lower rates to keep their trophy homes appreciating even more, and at the same time younger people who are totally shut out from the housing market (even POS homes are unaffordable on a normal salary despite the lowest rates in 400 years), self-employed people and small business owners who are killed by mandatory insurance/pension/healthcare premiums to keep the current ponzi’s going. I’m not even counting the people (especially boomers, again) who feel entitled to free million-dollar medical treatments every year because ‘it was promised to them’.

No limits on the greed that is on display. Something has to give …

Boomers are the new Bankers.,… the new most hated demographic

My understanding is that when subprime borrowers defaulted during the global financial crisis, the banks that insured the loans had to pay out not just the holders of the debt but also everyone who held credit default swaps on the loans.

My knowledge is only from the movie the big short but apparently banks had issued as much as 1 billion dollars of swaps on capitalises debt obligations (bundled mortgages) of 50 million or so. It was the credit default swaps that broke the financial system not the defaults.

Surely the US government is on the hook for only the face value of the loans they have insured?

That seems like a good point. Surely the USG did not underwrite any CDS!

“Astronomical”

Trillions? How about a Quadrillion Plus?

The Depository Trust and Clearing Corporation (DTCC)

In 2011 the DTCC settled close to $1.7 quadrillion of securities transactions.

On Wednesday February 10, 2010 the Federal Reserve Board approved the DTCC application to form a subsidiary of the Federal Reserve System, that would be responsible for the clearing of derivatives. The new entity would be known as the Warehouse Trust Company operating under the Trade Information Warehouse, which is itself a subsidiary of the DTCC.

What all that means is the American tax payer is on the hook for not only sour sub-prime mortgages, but for all derivatives that default in any future financial meltdown.

Did you really think that the wall street bankers would be the bag holders? The public has been thrown under the bus and is now just waiting to be kicked down the cellar stairs.

God forbid that wealthy gamblers should be forced to eat the losses on their bad bets…

Precisely. Keep in mind that when the former US Treasury Secretary was the head of Goldman Sachs, the company not only made large sums of money bundling mortgages into MBS and also creating and selling other bundled real and imaginary debt, the company also took out tons of “insurance”, i.e., credit default swaps on these derivatives. In fact, many companies and individuals that did not hold the underlying derivatives bought CDS on the derivatives, which is gambling. When the issuer of the CDS, AIG, poisoned by all of the toxic Goldman Sachs derivatives went belly up, guess who was forced by the former CEO of Goldman Sachs to have taxpayers bailout AIG?

I hadn’t seen much lately about the DTCC, but I understood they were hopelessly behind in their accounts due to the high speed trading in securities, something like 99%, according to Bix Weir.

Any way these are debts “which cannot be repaid, so will not be repaid”

The obvious question is – why are such mortgages being permitted.

What does the Fed fear so much that they would allow this to happen – when they knew how it ended last time.

Ends of Days is imminent

such mortgages are totally normal in the Netherlands, and have been for many years ;-(

As the politicians say: it works, still very low default rates! Similar to the guy who jumps off a high building and when falling past the second floor reports “no problem so far!”.

Can you provide evidence of any country that has permitted subprime lending — Liar Loans — 0 money down financing on property ….

That has not run into a major crisis?

You do understand what a subprime mortgage loan is?

It is a loan to someone with a very poor credit rating — someone who is very likely to default on that loan.

Throughout history this sort of think has been anathema to the banking industry …. bankers have generally been in the business of loaning money to people who are likely to pay them back.

Obviously things have changed in the past 15 years. We’ve had one gigantic explosion because of these policies — and we are setting the system up for an exponentially bigger bomb detonation.

Again —- why do this knowing how it is going to end?

I have put my theory out there and supported it with facts — this is a situation of acute desperation.

No one loses money as long as home prices continue to go up. Even liar loans (false info on the application) don’t lose a lot when the bank forecloses on the property … as long as home prices rise endlessly, and by a lot.

That would be the case in every country – and there are many countries – including the Netherlands, as nhz has pointed out many times – that subsidize home ownership with these policies.

But when home prices run into resistance or sag, all bets are off.

it’s as Wolf says: people keep paying as long as prices go up, I have no doubt they will walk away without any moral hesitation when the market craters.

Really, most of the home loans in the Netherlands would be considered subprime elsewhere, they would not be possible in a normal market but loaning to homeowners is considered ‘zero risk’ because of the National Mortgage Guarantee, an even bigger ponzi than Fanny & Freddy in the US. This mortgage insurance fund has about 0.1% of the mortgage value it insures as a buffer; and why not, home prices always go up so no ‘insurance is needed’. Nobody knows what happens if they go bust, because officially the taxpayers are on the hook then (which includes most of the people with such a ‘subprime’ mortgage).

BTW, Australia is starting to sound a bit similar as Netherlands, piling all kinds of crazy subsidies and incentives for homeowners on top of each other.

For convenience, our politicians and realtors always start the home price statistics around 1985, prices only went up from then except for a small hiccup in 2008. But in 1981 there was a 60% price drop in the Netherlands within 1.5 years, after a prior runup of about 100% within five years. The amount of mortgage debt was many times lower then, but there must have been quite some tragedies. Everyone seems to have forgotten this episode, just like the tulip mania and many other examples of speculative excess before it. My own city already had a serious RE bust in the 18th century, due to speculation with stocks of the Dutch East India company (VOC, first multinational ever). Everyone in the higher classes thought they were going to retire early and build an estate outside the city thanks to the stock market – that didn’t really work out ;-(

Just imagine what can happen after a home price runup of over 1000% …

Government related mortgages, FHA, VA, Fanny, etc., which have some guarantee somehow, all had the provision that NO LENDER involved in fraud, convicted or fined in lieu of prosecution could originate any home loans. Our president, using an executive order, had that clause removed at the beckoning of our to big to fail banks, and Congress as well as other government agencies never made so much as a whimper about it.

As for the Fed, they can only survive by blowing the bubble over and over. It is no accident anymore.

Actually nothing is an ‘accident’ anymore.

The ultimate question for everyone is, what ever happened to honor, integrity, conscience, and the soul of the country?

I remember when the mere hint of scandal could close down a financial institution, Salomon Brothers comes to mind, and there were others too. But that was sooo last century.

The bubble phase started around the time that oil went from $12 to $35+….

Because that ends growth.

And when growth ends you either collapse into a very primitive state — or you fight with whatever tools you can find in the tool box…

Of course there will be toxic side effects when you do that….

As we are experiencing….

Bubble after bubble after bubble….

We lost our house to foreclosure in 2010 after my job loss and half of our income wiped out. I still remember that BO smelling real estate agent who sold us that subprime interest only 40 year loan telling us to join the party like everyone else. So we did. Refinanced it 1 year later and put in a pool. Life was good on 2 six figure incomes and then it all came crashing down.

During early 2009 after my job loss I negotiated for over 9 months with the bank to save the house from foreclosure. We had excellent credit, my wife’s great nursing job, and had never been late on a payment. But we could no longer afford the payment and the value had dropped 60%. It was a big time loser. In the end, the bank decided to kick us to the curb rather than renegotiate a loan they would have made more money on than reselling the house in foreclosure. But no, those bastards weren’t about to set a nasty precedent by helping us out – even in a win situation for the bank. No. What they did was jerk us around for 9 months deceiving us into believing they would work with us. Tried to sell us on that BS HARP program after they continued to lie to us. So in Dec. of 2009 know what we did? We bought a 55″ flat screen tv for Christmas and told them to kiss our a..es. Rented for 3 years and bought again in 2013. A smaller single story house my wife and I can now afford on a “fixed 30 year” FHA loan qualifying with her job and a 720 credit score. So my thanks to the government for allowing us an option to own again. Life is pretty good and we have our health and family. But you never know with the current state of global affairs. Good thing we have that tent and camping gear for backup.

Good to hear you’re back on your feet again, but 0 sympathy for having to deal with a hardball bank.

I mean seriously.

I still remember that BO smelling real estate agent who sold us that subprime interest only 40 year loan telling us to join the party like everyone else. So we did. Refinanced it 1 year later and put in a pool.

A 40 year subprime interest only loan! How could anyone with half a brain cell think that could possibly be a good idea.

“like everyone else”. A poor excuse if ever I heard one. Very similar to the “following orders” tripe.

The thing is…

People see the likes of Paris Hilton and her ilk … someone who has done nothing of note in her life other than be born to money and perform in a hard core porn movie…

They also are bombarded with images of people who live very large — images that celebrate hedonism.

Recall ‘Lifestyles of the Rich and Famous’ for instance.

Of course it is not easy to be born to wealth — and most people who made a porn movie would be laughing stock — earning big money is increasingly difficult

Yet everyone wants to Live Large!

When the real estate agent and the mortgage broker urge people to buy that big fat house they have a very receptive audience.

Go on man — just sign on the line — and all this can be yours!

You might have second thoughts but then you think about your cousin Bobby and his wife Jenny — who bought the mega house (no money down) and now they make snide jokes about your ‘bungalow’

So you grab the pen — and you get on board — it makes you feel a bit like a movie star… a sports hero … a tycoon….

Gotta keep up with the Pitts… and the Hiltons….. — even if it means you end up bankrupt.

Then what you are implying is ‘everyone’ has no self control. I think not.

Based on the popularity of idiots like Paris Hilton … Justin Bieber …. and American Idol…

I would suggest that the majority of Americans have bought completely into the picture I painted earlier…

I do not engage in discussions about US politics because the Fed runs the show and the rest is all infotainment…

But when at complete and utter braggart/wanker/loudmouth asshole like Donald Trump is the leading candidate for president…. i.e. he is actually admired!!!!

Well that pretty much says it all.

America is like a diseased old whore whose body parts are rotting….

Not everyone admires Trump. He’s the presidential candidate with the highest negative ratings ever. Hilary is bad enough, but he’s practically reviled by a large chunk of the electorate.

I have no clue how we’ve gotten to the point where these two characters are our top two presidential candidates.

Understood – a lot of people also no doubt dislike Paris Bieber as well (hmmm wonder what the result would be of breeding those two…) — and feel they represent all that is wrong with the country…

Let’s add a the weekly mass murder — and regular cops killing anything that moves and is black….

These are all symptoms of an unraveling situation – in some respects as the biggest economic power the US is the epicentre…

My take on this is that we have reached The Limits to Growth … the famous study released in the 70’s suggested we would hit the wall in about 50 years….

And here we are ….

Tens of trillions of dollars pumped out — ZIRP – NIRP – Lair Loans – subprime auto loans – a few kitchen sinks….

And yet no green shoots.

We have shot the old nag with speed, coke, smack, HGH, roids — he moaned and staggered to his feet for a few years but now he is barely twitching.

Let’s face it — the system is finished. Growth is over.

The fat lady is warming up

This is an interesting article that looks at the bigger picture… the only part I disagree with is the totalitarian nightmare — I prefer the word apocalypse….

Why is this happening at this point in history?

As the world explodes in violence, war, riots, and uprisings, it is challenging to step back and examine the bigger picture.

With airliners being shot down over the Ukraine, missiles flying between Israel and Gaza, ongoing civil war in Syria, Iraq falling apart as ISIS gains ground, dictatorship crackdown in Egypt, Turkey on the verge of revolution, Iran gaining control of Iraq, Saudi Arabia fomenting violence, Africa dissolving into chaos, South America imploding and sending their children across our purposely porous southern border, Mexico under the control of drug lords, China experiencing a slow motion real estate collapse, Japan experiencing their third decade of Keynesian failure, facing a demographic nightmare scenario while being slowly poisoned by radiation, and Chinese-Japanese relations moving towards World War II levels, it is easy to get lost in the day to day minutia of history in the making.

Is There a Limit?

“At the rate of increase prevailing between the birth of Christ and the death of Queen Elizabeth I, it took sixteen centuries for the population of the earth to double.

At the present rate it will double in less than half a century. And this fantastically rapid doubling of our numbers will be taking place on a planet whose most desirable and productive areas are already densely populated, whose soils are being eroded by the frantic efforts of bad farmers to raise more food, and whose easily available mineral capital is being squandered with the reckless extravagance of a drunken sailor getting rid of his accumulated pay.”

Aldous Huxley – Brave New World Revisited – 1958

Read More:

http://www.theburningplatform.com/2014/07/28/our-totalitarian-future-part-one/

http://www.theburningplatform.com/2014/07/29/our-totalitarian-future-part-two/

I just read some highlights of this article to my wife. (Canadian here). Her comment, ” Considering this is a country supposedly so opposed to socialism, including helping people out with an affordable medical system, it sounds pretty socialist to me. At least for some it is”.

Amen to that.

Petunia, I have often thought about your housing story. It sounds terrible, and scary. I remember back when I was 26. It was in ’81 and the Canadian recession was snowballing in lockstep to rising interest rates. My wonderful company laid me off (and many others) in a deliberate program to break our Union and de-certify. I also had very little income beyond UI and carpentry work under-the-table. It was a very lean 6 months, but we managed to scrape up the mortgage payment every month. Somehow. We had the garden, wood heat, our own eggs, and a freezer with venison and rabbit. To make a long story short I had to work away for 3 months at a time and was under-employed for many years. Despite spending thousands of dollars renovating over the next 3 years, collapsing house prices ensured I barely broke even. The sweat equity = 0% profit when I finally pulled the plug and moved away for a fresh start.

It is something I never got over, despite doing quite well in subsequent years. We always lived well below our means and still do the food preserving and sustainability lifestyle. Unless one is a damn fool, you never get over hard times and loss. I take nothing for granted and certainly will never trust politicians and/or corporate leaders with anything they say.

You are correct, it is an income story. Also, when things crash, and you see many on the losing end of things (and also being one of them), it is doubly hard to see others who have total job security living a high-on-the-hog lifestyle, who are also oblivious to what is really going on around them.

regards

75 years ago germany invaded russia, and titanic battles followed.

things aren’t so bad.

Things aren’t so bad…….yet!

“What does the Fed fear so much that they would allow this to happen – when they knew how it ended last time.”

Thomas that is a brilliant and relevant question.

Make sure you watch your money in your work 401K. READ THE FINE PRINT. That’s what I did in 2009 AFTER I was laid off and handed what was left of it. I had put the money in what was claimed by the brokerage firm that handled the accounts, to be a fairly conservative portfolio. I was stunned. It had lost 30% of its value. How was this possible?

As I read the fine print I discovered my money was invested in subprime mortgages.

Fortunately, my story had a better ending than some of the posters here. I already had a job lined up before I got let go. I took the money and plowed it into the stock market and made it all back (I had to get a 50% increase to break even).

In the meantime, I’ve gotten much much better at playing the market and don’t fear the future anymore.

Petunia always seems to hit the nail on the head. Income is the key to lock. Look around you, we are constantly seeing layoffs, downsizing, business closures. We are seeing (not me) the 401k, IRAs, etc., investing in companies whose goal is to put you out of a job. How many or you have stock in Google for example whose driverless cars and trucks will end thousands of jobs? Yes, yes, all the tech is just wonderful making everything more efficient where one machine can do the work of hundreds of people.

At some point, the unemployed will exceed the employed. Unpaid will exceed the paid. Squatters will be the norm. Perhaps then the FED will just send each of us a check to keep us happy and quiet.

It should also be noted that the Federal Reserve still purchases about $30 billion per month in Agency MBS bonds (TBA Passthroughs) through their FOMC Permanent Open Market Operations (POMO) which rounds to about 70% of everything Fannie, Freddie, and Ginnie issue in a year.

https://www.newyorkfed.org/markets/ambs

GSE’s own more of the debt this time? Aren’t the banks required to keep major skin in the mortgage game this time around?

This is the Feds taking our tax dollars and transferring it to the poor. By stealing our money they make the poor middle class and the upper middle class poor. They also destroy the capitalist basis where stronger survive better just like nature intended. Systems die if the weak elements survive and the strong elements are undermined. Socialism is a perversion of the natural order which destroys survival.

The average income of a Tesla owner is 250k….

Tesla is heavily subsidized …. http://davidstockmanscontracorner.com/tesla-bonfire-of-the-money-printers-vanities/

And big oil?

Last I looked we all use oil…. so I am good with the government doing whatever it takes to ensure a constant supply….

And of course regardless of the amount of subsidies… oil still delivers a significant return on energy …

If it did not then we’d not bother to extract it

Oil makes the world go round… the world go round… not Tesla

I quite agree with the Wolf Street analysis. We are headed down the same path as before as it concerns housing policy. Many of the loans being made under the FHA program shouldn’t be made as they contain multiple risks: minimal down payments, combined with high debt-to-income ratios, low credit scores, and lengthy 30 year terms. When the next recession occurs and the unemployment rate rises to 8% and holds for 18 months or longer, the default rate on many FHA loans will rise to 30% or better. Given that these loans are more or less concentrated in certain urban areas, entire neighborhoods will again be stripped of equity.