Manufacturing PMI and non-manufacturing PMI sink.

The export and manufacturing powerhouse of the world, the locomotive – along with the US – of the global economy, and an indicator of the global economy itself, disappointed economists once again. The operative word in the media today is “unexpectedly.”

China has been on an glorious debt-and-stimulus binge for the past few months. New corporate borrowing shot up to record levels as the People’s Bank of China opened all valves, and juice rushed through the state-owned megabanks to corporate borrowers and others all around.

In the first quarter, total debt ballooned by 6.2 trillion yuan (nearly $1 trillion), the largest quarterly jump ever, to a record 163 trillion yuan ($25 trillion), or 237% of GDP, up from 148% of GDP in 2007, according to some of the more benign estimates. Others peg total debt as high as 282% of GDP. Corporate debt alone is now estimated at 160% of GDP. But no one knows for sure. With the Chinese economy, everyone is groping in the dark.

It’s not the debt itself that scares observers, but the speed with which this debt has ballooned. It’s impossible to invests this sort of moolah this quickly in productive activities whose proceeds would allow for this debt to be serviced [read… China’s “Lehman Moment” or Decades of Japan-Style Stagnation?].

Economists thought that this stimulus-and-debt binge would actually perk up manufacturing, boost services, and end China’s economic malaise, the extent of which remains unknown because no one, not even the Chinese leadership, trusts the official numbers according to which the economy grew 6.7% in the first quarter. Inflated as that number may be, it’s the slowest growth since 2009.

But wherever this money went – overseas real estate and M&A come to mind – it hasn’t been invested in China in productive activities, and it isn’t helping the economy:

The official manufacturing purchasing managers index fell “unexpectedly” to 50.1 in April from 50.2 in March (above 50 = expansion). It was the second month in a row barely above 50, after seven months in a row below 50. The median forecast by economists, as polled by the Wall Street Journal, had expected it to rise to 50.4.

And that’s the official number released by the National Bureau of Statistics. The unofficial number – the Caixin Manufacturing PMI – will come in a day. It has been even crummier: 49.7 in March, 48.0 in February, 48.4 in January, 48.2 in December…. It has been in contraction mode every month since February 2015.

But the decline of manufacturing suddenly doesn’t matter in China because the government is transforming the economy into a service economy. It is transitioning the economy away from its reliance on manufacturing, which is shrinking. Services are now the new locomotive. That’s the plan.

But no.

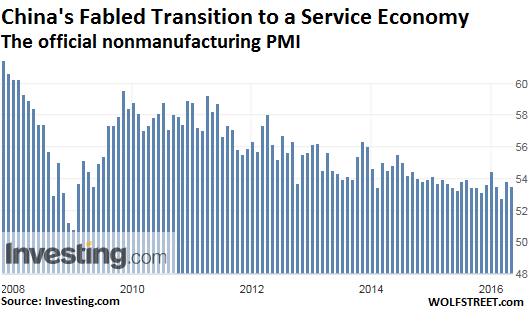

China’s official nonmanufacturing PMI, also released today, tracks not just services but also construction. And it fell from 53.8 in March to 53.5 in April.

The sub-index for services dropped from 53.1 to 52.5. Construction, which is where the stimulus money that stays in China ends up, rose from 58.0 to 59.4 in April. Construction is alive and well, and still a big engine of the Chinese economy, whether or not more ghost cities are needed.

But the sub-index for new orders plunged into contraction mode, down 2.1 points to 48.7 in April; new export orders also plunged 2.1 points to 45.7; orders in hand, though slightly higher than in March, came in at an abysmal 43.6. These are the harbingers of “growth” in the future. And they’re all in contraction!

So how well is China’s transition into services doing? This chart shows that growth of the nonmanufacturing PMI has zigzagged lower for years, from an all-time high of 62.2 in May 2007, via the big dip during the Financial Crisis, to the currently disappearing growth:

The fact that the manufacturing and the nonmanufacturing PMIs both are already weakening despite the enormous stimulus-and-debt binge that the PBoC and the government have orchestrated demonstrates that these easy-money policies have lost their effectiveness in driving economic growth.

The failure of these policies has been visible in export-dependent manufacturing for a while. But now it’s even failing in the ballyhooed transition to services that everyone had hoped would be a raving success. Instead, what do these policies succeed at? Adding to the already insurmountable mountain of debt, a good part of which is now going bad.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I had hoped that the centrally planned authoritarian PRC socioeconomy would be able to at least moderate the worst abuses, bubbles, collapses, frauds, civil unrest, etc. which seem to be symptomatic of a society/culture transitioning from a traditional agricultural to a wage based industrial/technological economy.

It now appears that all such transitions are inherently and profoundly destabilizing/disruptive on the individual level, and any economy with a large debt based abstract/virtual financial sector is unstable.

Anyone have some suggestions as to how the transition impact on individuals can be minimized, and how a debt based abstract/virtual financial sector can be prevented from being a “bull in a China shop?” [Unintentional pun]

Antale Fekete has discussed all the ramifications of non-barter systems. He suggests seasonal commercial paper as the systemic limit. As for individuals, Oh My! My personal best effort is to appraise the price of everything by how I would feel about growing it or making it or mining it myself(the distilled human perspiration factor–thanks Dad). I try to live by tanstaafl in my expectations. I find throwing stuff away really hard. Having prices of soft commodities at a several decade (inflation-adjusted)low really scares me because it has gone on too long. The answer to low prices is low prices :(

A big part of finding a solution to a problem is having accurate data available for analysis. By intention, the Chinese data is undependable. So, as to a solution, your dart board is as good as mine.

As an aside, I remember the big sell of the “Information Age” to come. But when it got here, it seems we really got a “Disinformation Age” instead. No matter the complexity of the model or the computing power available, garbage in is still garbage out.

Indeed. Even the “west’s” public information is suspect, but given the PRC’s highly efficient Ministry of State Security, and extensive computer science efforts, one would think that the actual data and analysis, possibly using the newer “big data” and artificial intelligence methodologies would have produced at least marginally better results. Perhaps they were more concerned with internal political dissent and external [computer] espionage than with the problems of an erratic and random economy.

FWIW: I think that it’s the socioeconomic instability that’s the basic problem, and we all need to keep an eye on the loose cannons and bulls in the China shop in our own economies. Far more damage was done to the U.S. by Lehman, Bear, AIG and GM than 9-11…

The fatal flaw with China is their lack of democracy, transparency, and accountability.

Eventually, the internal contradictions that form the basis of their economy, and entire system of government, will inevitably collapse on itself. The only solution is a transition toward democratic reforms. This is why, though India is quite a bit behind on the development spectrum, their economic growth prospects are far more rosy.

RE: Eventually, the internal contradictions that form the basis of their economy, and entire system of government, will inevitably collapse on itself.

————–

Hegel lives!!!!!

sure, buy no debt company AUD gold stocks

The economic growth needs to be organic and unforced. Debt-based currency is inherently inflationary; consequently, there must be a real demand for any improvement. The debts must be paid.

China simply went on a money printing spree to build a bunch of highways and bridges to empty cities. All this debt is coming due and much of it cannot be paid. China’s growth, and that of the US (only for a much longer time), has been artificial. Simply manipulating monetary policy does not generate growth. It only creates an excess of cheap ‘capital’ with which to invest for short term return in the bubble of the day. In short, supply side economics is bunk.

What China and the world both need and what we have sadly gotten away from are well balanced economies that develop synergies within their national boundaries as well as outside of those boundaries. These, not interest rates or money supply, are the true engines of growth.

China is the MOST liquid market in the world. And their problem is LOCALIZED, not SYSTEMIC like U.S. got with their ZOMBIE BANKS.

While you appear to be correct, the problem is we are comparing socioeconomies at different stages of development.

The U. S. is a financially dominated post-industrial economy, while the PRC is in the early to mid stages of mass production industrialization. While the PRC’s rate of development is greatly accelerated because of the import of technology/methodology, she still appears to be having problems of labor discontent and cultural disruption similar to the U. S. in the 1920s, including a spectacular real estate bubble, i.e. the Florida land boom.

It now appears, at least to me, that as any socioeconomy, no matter what it’s underlying ideology, will experience considerable stress and disruption as they transition from one economic stage to another, much as zits are a part of puberty.

” because the government is transforming the economy into a service economy. ”

I’ve been seeing this on the various business news rags for about six months. Over and over they repeat it.

What is the official policy that dictates this? Getting frugal Chinese to suddenly spend? Is that the policy?? Seems they’re spending all their money on inflated rents.

I’m not sure how any sane person can believe they can grow their way out of an over-capacity problem by stimulating the creatioon of more capacity.

More to the point, they’re attempting to solve the problem of overcapacity funded by excessive debt by creating more capacity with even more excessive debt. Finding themselves in a hole, they didn’t stop digging: they found themselves a bigger shovel.

Borrowing is only constructive if the return can be expected to exceed the cost of the debt. Here it can only be expected to be destructive. In the absence of any valid rationale one must suspect hidden motives, but aside from feeding the financial sector I have no idea what they’re doing. They’re probably none too sure themselves, but they should probably reconsider whatever that may be before they detonate the global economy.

Is it really capitalism if it’s all credit and no capital?

“Is it really capitalism if it’s all credit and no capital?” A very good question. Another might be “Is it really communism if there are dozens of billionaires?” Confucius wrote, “Out of debt, out of danger,” and for a long time I thought this was still a guiding principle in China- to my surprise it turns out they have created new debt at a colossal rate. It is certainly true that much of it has been put to productive infrastructure: modernization of their electrical grid, greatly expanded rail system (plus mag-lev), roads and bridges, for example (as compared to crumbling infrastructure here, where fatal Amtrak derailments, including a chemical-laden train in sight of the Capitol yesterday, and rotting bridges are becoming the norm.) In fact, one thing that stands out is how much they have gotten away with. Millions of miles of copper wire and tubing, vast amounts of cement and concrete, forests of hardwood, cotton, wool and grain to feed a billion people and greatly elevate their standard of living . A Zimbabwe, or even India could not do the same by issuing debt. In China’s case, all the credit did indeed create a great deal of capital. Thje question is who is going to be stiffed, when, as with Puerto Rico just today, the debt is not paid.

“The question is who is going to be stiffed, when, as with Puerto Rico just today, the debt is not paid.”

Captain, we have spotted several groups of black swans heading north from Puerto Rican. Trajectory analysis suggests multiple potential targets. One target appears to the offices of MBIA & AGO.

They insure some of these bonds. It could be a catalyst & yes various derivative structures will be the key.

“The question is who is going to be stiffed, when, as with Puerto Rico just today, the debt is not paid.”

Captain, we have spotted several groups of black swans heading north from Puerto Rican. Trajectory analysis suggests multiple potential targets. One target appears to the offices of MBIA & AGO.

They insure some of these bonds. It could be a catalyst & yes various derivative structures will be the key.

I suspect the reason is twofold.

Despite the whole XX century under our eyes, Western media have long been fascinated by planned economies, from Stalin’s Five Year Plans to China’s infrastructural binge. More than fascinated it seems they hold these systems in awe and somehow believe they can be made to work despite a track record worse than mine in betting on sporting events.

Tied to this is the post-2000 belief that economies cannot grow without guidance from above and massive amounts of monetary stimulus. I still remember Alan Greenspan been quoted along the lines that US fiscal and monetary authorities “had” to inflate a housing/mortgage bubble at the time of Dotcom Bubble burst.

The reality is a little bit different: Chinese authorities never officially stated they want to shift towards a “service” economy. They have paid a lot of lip service to reducing overcapacity and closed a token number of steel mills, but the former workers there were not “repurposed” in the service sector. They were offered jobs in the forestry, construction and public work sectors. Just the kind of jobs that makes a service economy.

If Beijing were dead set on building a service economy, the non-manufacturing PMI (official or not) would have been manipulated to be steadily above 60, much to the amazement and admiration of our central planning-enamored media.

I think the planned shift is not from an export-based economy to a “service” economy, but rather to domestic development to provide for new employment. This includes expansion of conventional as well as high speed rail into the less-developed interior of the country , the New Silk Road development, facilitating new building and factory construction, expansion of domestic airlines and aircraft construction, modernization and development of ports, expansion of tourism and cruise industries, medical infrastructure, etc. And, of course cleaning the air and ten billion filthy windows.

The problem with the so called transition…time is not on China’s politburo side.

Well, the US ( and UK ) became ‘service economies’ essentially through ‘offshoring’ their manufacturing to places like China.

While the theory was getting rid of all those nasty, boring factory jobs would be a good thing because we would get new and better jobs in the FIRE and IT economy it would appear the bulk of the ‘new jobs’ are in the restaurant/beverage and hair and nail care industries.

This year the election cycle is “trumpeting” an end to globalization and the exodus of jobs and industries. It had to happen. The consumer in the West is so tapped out that they can’t afford Chinese exports. Chinese exports are down 25% in the past year. The is how the whole debt-fueled process comes to a crashing end. Great Depression ahead.

dont worry people will be learning to cook their own food and do their own nails very soon as the wealth is drying up like you know what through a tin horn assuming the EBT cards still function

I think measuring China, perhaps the world’s second largest economy, by the usual western standards – if it hasn’t turned around and is making money in a year it must be a failure is not a valid analysis. I suggest that a decade is a better time frame in which to begin to seek the answer the question of success or failure of the Chinese conversion. I recommend reading Stephen Roach for an expert’s view of how things are going.

http://www.marketwatch.com/story/chinas-economy-is-not-melting-down-stephen-roach-says-2016-01-26

In attempting a sea change of this magnitude, one should expect setbacks and failures, problems, successes and a lot of unhappy people who have had their entire lives changed along with the happy people who have benefitted from the changes.

‘Ponzi lending? In China, 45% of new company debt is raised to pay interest on existing debt’

Banks are lending more money to insolvent companies… so that they can make interest payments on debts they will never repay….

http://www.marketwatch.com/story/chinas-giant-bonfire-of-debt-needs-one-spark-to-become-an-inferno-2016-04-14

A piece by Bloomberg a while back, written by one of their underpaid twinkies (I guess) opined that the transition to a service sector was well underway as industrial jobs were replaced with ‘baristas, hair dressers and, (get this), baby sitters.

If this appeared on Wolf Street I would assume it was satire, but as far as I could see, the statement was meant seriously.

İ try to avoid anything Bloomberg like the plague same with Goldman Sachs Gartman and other paid shills for the banksters but thats just me İ guess

I am still betting the US and/or Europe will be the trigger for the next global depression.

In a race between China and Deutsche Bank, it’s the later that will be naked first.

And that strange meeting between the Fed and Obama is probably a prelude to some kind of Summer Blockbuster. One day you wake up and it’s either: there’s no more cash or some kind of negative interest rate has been imposed on you.

At the moment Italian banks are the financial equivalent of the Siachen Glacier: nobody pays attention to them, but they could be the flashpoint of the next “big one”.

Leaving aside the question of NPL’s, chiefly because nobody has a clue how big the problem is, Italian banks are right now trading at enormous discounts to book value. Unicredit, Italy’s #2 bank has a market cap 40% of its book equities. MPS, which has already been bailed out twice since 2010, has a market cap 25% of its book equities.

This means even those speculators cheering wildly for any scrap of monetary lunacy originating from Frankfurt know the situation is rotten beyond repair.

To this it must be added most smaller Italian banks are effectively insolvent and only kept afloat by yield repression. If yields went back to pre-2009 levels, it would be goodnight Irene.

Capital flight has resumed to other EMU countries (chiefly France), so these smaller semi-bankrupt banks are also sitting on a dwindling pile of hard assets.

The Italian government is fiddling while Rome burns: late last year four of these minor banks defaulted on their obligations and its only concern has been on how to bail out bondholders (these are well-known “Red Banks”, meaning close to the ruling party, a mutation of the Cold War era Communist Party) without infuriating the Germans and the Dutch and how to hush the fact a minister’s family sits squat in the middle of the scandal. For the rest they have no contingency plans of any kind bar distracting people with irrelevancies.

One can add Spain and Portugal to the list of countries whose banks are in major trouble. If one adds in the Landesbanks in Germany, their banking system is flat out broke also. It looks to me that every country that one looks at in the world is in the same shape, debt overwhelming the ability to ever repay it and soon, the ability to pay the carried interest charges also. The only thing that is keeping these places afloat is ever more convoluted financial engineering and an iron determination by the governments to turn a blind eye to the situation.

Yes, it’s seems apparent that the entire global financial system is one huge sinkhole of debt. All entities keep adding more debt to fix the problem of more debt. It doesn’t seem to matter what country, state, or city you examine, it’s pretty much the same just shaded in different colors of gray. I guess the big question is how will this be rectified on a global basis? There are lots of theories out there & it’s hard to grasp what the implications will be for any given area, mine included. What will be the fuse that sparks a global financial conflagration & will it be lit on purpose to obscure the true nature of things to the sleepwalkers?

The Landesbanken are “different”. To say they are poorly run would be a mild understatement, but most of them have a huge advantage over Italian and Spanish banks: the main shareholders are the Landers and munis.

This means troubled assets can be simply transfered from the bank to the muni’s or Lander’s books. It has already been done and the mechanism has been approved by the appropriate EU commission because it’s technically a bail-in, with the main shareholders footing the bill. The fact taxpayers in Hamburg or Fulda are technically the shareholders and hence footing the bill despite often having not a single pfenning in deposits, shares or bonds doesn’t seem to faze the EU.

This takes nothing away from the monumental incompetence of Landesbank management, such as falling into the Hypo-Alpe-Adria trap not once but twice. Yes, this should open a chapter about Austrian banks as well, but let’s not go there for the moment.

Thank you for bringing up the Landesbanken!

There are people around me that keep haranguing me about “pubic banks” that are owned by cities or the state. They keep citing the Bank of North Dakota. These banks would somehow cut out the profit-taking mania of banks and lead to better lending. “The money stays in the community,” they like to say.

But as you pointed out, public banks are a magnet for incompetence and/or corruption, political lending, and the like, and in the end – not at first, but after decades of operations when it’s clear that its loan book has fallen apart – it’s always the taxpayer that foots the bill.

It is well to remember that the “great global depression” can be dated from the collapse of Creditanstalt in Austria in 1933. This was after the bursting of two major domestic [US] asset bubbles, the Florida land boom, and in ’29 the stock bubble, when the U. S. was beginning to recover.

yes indeedie they most certainly have morsel of fun planned for us No doubt about that GOT GOLD?

“government is transforming the economy into a service economy.”

Code phrase for a contracting economy, just as “I’m an independent contractor” is code for being on the edge of unemployed or underemployed.

I think I hear war drums: The political class’ last refuge from the consequences of their stupidity, incompetence, and corruption.

I read somewhere that when a country is 250% in debt relative to its GDP the debt will not, cannot, be paid back, so there is nothing left to do but WAR. China and Japan are both in that territory.

İ would agree except alot of the japanese debt is held internally by their loyal population who are much more willing to “sacrifice” for the cause Therein lies the difference in my opinion

It’s a 20 year project that is only about 3 years old, but some people have declared it a failure. It’s amusing to see “experts” pontificating from the other side of the planet about China’s demise when their own economy is failing.

China’s “demise?” What are you reading? We’re not talking about a “demise” of any kind. We’re talking about the economy and debt. Don’t react so allergically if someone questions the for you sacred Chinese government statistics.

This blog constantly uses words like “collapse” and “crash” to describe small incremental changes, constantly painting a negative picture. Anybody who spends a lot of time in China and doesn’t have an foregone agenda knows otherwise.

On this site, we’re talking about a “hard landing” for China. We’re talking about a huge debt problem that you personally cannot see when you look out the window wherever you live in China. And because you cannot see it when you look out the window, you think it isn’t there.

Or the Chinese government pays you to troll Western websites to spread the word that there is no problem in China, least of all a debt problem.

But others see it, including the largest organizations in the world that track those kinds of things, and everyone is worried about it, even the Chinese government.

roddy6667: And how has the 20 year plan worked out for Japan? The lost decade is now the lost decades. Yes the US economy is stagnant, or at least we will admit it on this website. With globalization, it means all of our economies are screwed. And you think China is immune…how?

Japan is not China

Ain’t that the truth! Japan has established a reputation for quality- China’s is pretty much the opposite. Do you see a bunch of Japanese stuff in Wally?

Personal anecdote: I love those big cheap box or window fans- known in the biz as the 20 inch fan. After owning a Taiwanese version I ordered another: when the Made in China ( not ROC- Taiwan) version arrived I noticed it was different. It was 20 inches square alright ( lulling unsuspecting wholesale buyer) but instead of being almost 6 inches deep (thick) it was only 4 inches.

To achieve this the blades had been drastically flattened- they were paddles instead of cups. The motor was smaller and the visible windings were of copper wire closer to human hair than the ones in the Taiwanese version. To save less than $10 the unit would push at most half the air until its windings burnt out.

I still search garage sales for the old version, but the cheapos have driven them from the new market.

This fooling the buyer is a constant theme from the mainland

BTW: the CCP has publicly castigated industry for its low quality

so I’m not the only one

While Japan has very considerable economic problems, e. g. grossly excessive governmental debt and huge amounts of non-performing loans, i.e. zombie/vampire corporations, the foundational problem appears to be demographic in that the birth rate is far below the death rate, and the ratio of retirees to active workers continues to increase.

Immigration of selected and skilled individuals from neighboring countries, such as China, Taiwan, and Korea, could offer some relief, but this is not culturally acceptable.

Little difference in scale: about 300:1

A lot of people seem to be confusing the finances of the Japanese government with its overall economy. For starters the debt is mostly held internally.

By comparison with Japanese cities much of the US looks like a (lost) war zone. The infrastructure looks new. You can leave a purse on a bench and a hour later it’ll still be there. Violence from a stranger is almost unheard of – whereas after dark many US cites have no-go zones.

Overall, it is a more stable society than the US. In fact

at the present rate of deterioration in what we call civil society, I would not be surprised to see a state try to secede.

How has the last 20 years worked for Japan’s exports? While 2 of the 3 US automakers went bankrupt Japan increased its share and entered the luxury market.

No matter how many ads the big three buy, all consumer reports name them as (some) of the worst values and Toyota as the most reliable.

This does not look like changing- in fact back out trucks from GM and what’s left. Escalade?

China? What about Puerto Rico?

Yeah, and a little more off topic, what about the Chicago School System? I think these will get really interesting in the near future and may serve as catalysts to get the ever complacent bond buyers off the dime.

Indeed! And you raise an interesting question. There appears to be no reason why Puerto Rico with its climate, location, cheap airfares, no visa/passport requirements for US citizens and abundant labor is not a tourist and retirement destination.

Some browsing on the web shows the appeal of the coastal Italian villages with their quaint building, and superlative food, and many Brits have retired to the Costa de Sol area in Spain, showing language is not a significant problem. Lan

While these would be isolated/gated type communities, something on the order of Disneyland attractions, it would appear that a combination of constructing “quaint” villages on the Italian model, but with reinforced concrete construction for storm protection internet access, etc., and a training program for the island residents that wished to become involved in the hospitality/retirement industry, would have a large return. Not only the waitstaff, but other individuals such as bakers, pasta makers, barristas, gellato makers, etc. would require training.

Indeed!! Looks like that particular house of cards collapsed first in Detroit. Looks like the teachers have had enough of being asked to do the impossible for the ungrateful while being loudly blamed for the ills of society.

Go away Troll. You and “V” are so top secret important that you can’t reveal your real identities. Looked at your pathetic websites…no thanks. We “Schmucks” will stick with Wolf.

Your website is all cut and paste from other websites and recordings from other websites as well. Probably a good thing since your grammar is so terrible. Your method of trolling for readers will not work on this site.

You sound like the serial troller that appears on the FT comments attacking anyone who points out the obvious – which is that China is a powder keg ready to explode.

The thing is … you are not even a very good troller – anyone can see right through what you are and where you are coming from.

Your government is going to collapse. The dream is over. Hard landing buddy. Crash landing.

How do you like that?

Can you add the name of who you were replying to? I know this system limits placing too many replies because the column gets too skinny. But just add the name. Thanks.

Wolf: I made 2 comments to the below Trolls comment….an then all 3 comments disappeared off of the site.

L the Different Observer commented on China’s Furious Stimulus-and-Debt Binge Backfires.

in response to wolf4ws:

Fabled transition to a service economy? Forget it.

I don’t even got slight worry on China, unlike some SCHMUCKS here.

And unlike U.S. economy, China is willing to pop their bubble, because in order for them to have stable economy and highly valuable GOLD-based currency, China NEED to pop those bubble and they got balls, I mean guts to do it.

Folks, V the Guerrilla Economist can provide you all a better and bigger picture of China’s problem.

Thanks. I deleted a troll comment that I thought went over the line. But it wasn’t posted under this article. It was posted under another article. If you replied to that one as I was deleting it, the system deleted your replies with it. I don’t see your two replies anywhere now. I don’t know where they went.

Do you remember who you replied to and under which article?

Hi Wolf! Yes it was: L the Different Observer commented on China’s Furious Stimulus-and-Debt Binge Backfires.

He was promoting a hideous website. I called him out on it. Reread my post above which is his original post I found in the “New comment” email. I responded to it and saw it on this tread for a minute and then they all disappeared. I have to assume Thomas Malthus replied to the new comment email by “L” but by that time is was deleted. Along with my pithy replies to “L.” ;-)

I just found the comment (with that website) in the trash. Actually now I vaguely remember reading your reply, but it’s gone now. Thanks for that reply, even if it’s gone.

TM, Mystery resolved. I deleted that comment. Thank you for responding to it.

And thanks to The Dona for solving the mystery

RE: …which is that China is a powder keg ready to explode.

Most unfortunately the PRC is not unique. All of the major economies and many of the minor ones [e.g. commodity exporters] are in the same condition. All of the central banking “arrows” have been fired, but the basic banking/finance problems have not been corrected, and indeed in many ways become even more dangerous.

It is highly unlikely that a credit event in one major economy will not propagate to all economies other than the ones which are isolated [North Korea] and/or already in ruins, e. g. Somalia and Sudan.