Relentless deterioration meets stunning overcapacity.

The amount it costs to ship containers from China to ports around the world, a function of the quantity of goods to be shipped and the supply of vessels to ship them, just dropped to a new historic low.

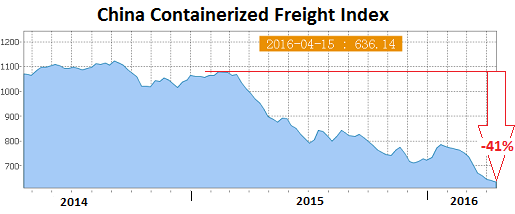

The China Containerized Freight Index (CCFI) tracks contractual and spot-market rates for shipping containers from major ports in China to 14 regions around the world. It reflects the unpolished and ugly reality of the shipping industry in an environment of deteriorating global trade.

For the latest reporting week, the index dropped 0.6% to 636.14, its lowest level ever. It has plunged 41% from the already low levels in February last year, and 36% since its inception in 1998 when it was set at 1,000. This chart shows the continuing collapse of containerized freight rates from China to the rest of the world:

The Shanghai Containerized Freight Index (SCFI), which tracks spot-market rates (not contractual rates) of shipping containers from Shanghai to 15 destinations around the world, dropped 3.6% for the latest reporting week to 472, after another failed price recovery. It’s down 58% from February last year.

Rates to Europe plunged $20 per twenty-foot equivalent unit container (TEU) to $271; to the Mediterranean, rates plunged $29 to $409 per TEU. To the US West Coast, rates plunged 9.3% or $79 to $770 per forty-foot equivalent unit (FEU).

A year ago, the spot rates to the West Coast had already fallen 10% year-over-year, and there had been a lot of hand-wringing about them. At the time, they were $1,932 per FEU. Now they’re at $770 per FEU. In one year, these spot rates have collapsed by 60%!

During the big plunge last year and earlier this year, the saving grace was the price of bunker fuel, which was plunging along with the price of oil. For example, according to Platts, bunker of the grade IFO380 in Los Angeles had hit a low of $118 per metric ton in mid-January. But it has since soared 91% to $225!

Bunker prices differ, depending on grade and location around the world, and not all made this sort of break-neck snap-back price reversal. For example, IFO380 in Rotterdam soared “only” 61% from $109/mt in mid-January to $176/mt. Other locations and grades experienced lower price increases. But all bunker prices everywhere have risen sharply.

So the ballyhooed notion that carriers, under pressure from competition, are simply passing on their fuel savings to their customers has now died an ignominious death. Instead, their margins are getting crushed.

But there are some real reasons for the collapse in freight rates from China to destinations around the world: China’s exports have plunged. For the January through March period – to iron out the monthly volatility associated with the Lunar New Year holiday – exports are down 9.6% year-over year. Specifically:

- To the US -8.8%

- To Hong Kong -6.5%

- To Japan -5.5%

- To South Korea -11.2%

- To Taiwan -3.7%

- To the countries in the ASEAN -13.7%

- To the EU -6.9%

- To South Africa -29.6% (!)

- To Brazil -47.2% (!!)

- To Australia -1.9%

- To New Zealand -12.4%.

Exports ticked up just a tiny bit to only two major countries: India (+0.2%) and Russia (+0.2%).

So demand for transporting containers from China to other parts of the world has withered, just when the supply of container ships has reached catastrophic levels of overcapacity.

Last year, what had already been an overcapacity problem turned into a self-inflicted nightmare for carriers. They’d assumed ever since the bouts of QE and zero-interest-rate policies started that central banks had their back. They’d smelled the lure of cheap money. And they’d fallen for the central-bank propaganda that “bold” monetary policies could actually stimulate the real economy, the goods-consuming economy. And so, imagining years of big-fat growth, they ordered ships, including the newest mega-sized container ships. And as these new ships were delivered over the past couple of years, carriers embarked on a fight for market share by cutting prices.

This culminated in 2015 with the delivery of new ships that added a record 1.7 million TEU of capacity to the global fleet, just when growth in global trade was grinding down. At the same time, according to Drewry, the amount of capacity scrapped in the year plunged by nearly half, with only 195,000 TEU of global capacity taken out.

Why? “Because demolition prices were less attractive….”

Like so many things in this world where free money created overcapacity, the rates paid for ships to be scrapped has plunged from around $475 per ldt (light displacement tonnage, the weight of the vessel including hull, machinery, and equipment) in 2012 to around $290/ldt recently.

So far this year, scrapping activity has picked up. And everyone is hoping that this will alleviate the problem. But it’s not going to help much, according to Drewry:

As we have highlighted before scrapping alone does very little to redress the supply-demand imbalance – last year’s scrapping total was equivalent to just 1% of the cellular fleet….

Now carriers are hoping that the huge general rate increases they announced for May 1 – in some cases more than doubling current rates – will stick. But they tried that last spring, when overcapacity wasn’t nearly as bad, and it didn’t work. So will they have more luck this year? The Journal of Commerce put it this way: “Conditions are hardly optimal for raising rates.”

The Chinese have among the highest savings rates in the world. But 75% of their wealth is in real estate. They’ve overinvested in one illiquid and bubbly asset that they wrongly believe can only go higher. But when prices break down, it will devastate consumer demand and reverberate around the world. Read… This Will Be Largest Evaporation of Wealth in Modern History

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

World population and the need for an increased supply of manufactured goods will not be rising forever. Furthermore, if the political stirrings throughout the western world accurately reflects impending change, the rule of Globalism might be fading. Nationalism certainly seems to be on the increase as well as calls for tariffs to ‘fix’ the economy.

I know in our house we just don’t need anymore plastic crap from China. Instead, for the past few years we have been trying hard to buy North American made products. Multiply this by many, throw in container ship over-capacity, and it is easy enough to understand the decline in shipping rates.

Buy local…buy quality…repair, don’t toss.

regards

This insane system is dépendent upon continual unnatural rates of growth to feed this debt creation based system. The planet is finite and while the pie can be expanded by incorporating best practices into how things are done, there are still limits to everything, even printing money out of thin air. We are soon to hit those limits where the TPTB will find out the hard way along with their brainwashed and bought off citizenry that you have to pay the piper at some point. This system is all about quantity, more profit, more power, but has little to do with quality of life issues including having a government that represents the interests of its public instead of the monied and power lusting interests. Quality is not necessarily about having more of everything including the problems that continual, excessive rates of expansion bring on, but of having the right amount of something and then either moving on in a different direction or just being reasonably satisfied with the present state of things until something more is required or available. This system does not allow the natural transition into different areas cause that may be a threat to the status quo who do not want to lose their positons of power and profit. And to do that it tries to manage the public as if they were their own personal livestock, only there to serve the agenda of ruling elite. The endgame is here now with peak debt situations everywhere and within every major government and hollowed out economies that would collapse immediately if not for the artificial life support of funny money and financial engineering. This excellent article points out another example of the egregious malinvestment that takes place in these funny money generated bubbles just like in real estate, shale oïl, and retail space in the U.S. For market analysis, http://marketscope.ca/

Superb summation and analysis.

Unfortunately, US made goods do not have a high reputation internationally if attitudes in Australia are typical. Your deregulation has made us wary of purchasing things which have been produced or even packaged in the US such as maple syrup due to fears of adulteration. Only Made in Canada is acceptable according to people I speak to.

I struggle to think of anything the US makes which is considered premium value.

This sort of reputational damage may be very difficult to overcome.

Boeing?

Canadians were big shoppers in Florida when the dollar wasn’t as strong. In New York they would cross the border to shop on a regular basis.

The current crisis (and renewed obsession with nationalism) will pass. Post-nationalism is the future, whether people like it or not. I’m based in Africa, a continent still seeing impressive growth and development rates, where countries are working to lower national barriers to trade and population movement.

Paulo

I really believe you have hit the etheral nail on the head. In many Western countries I believe your point is getting traction and beginning to have an effect on container use. Certainly the low end of trade ie fresh local food produce has been a big deal for years in here in Australia and in the US.

This attitude eventually morphs into processed local food products which then migrates rather more slowly to manufactured goods eg Old Navy US made clothing rather than imported stuff.

Poor old Aussie of course doesn’t make much of its own so referring mainly to the great USA machine.

Always amazed at the doomsayers in the USA as you guys are the greatest critics of your own country.

The USA is far from loosing any powerhouse status. Admittedly you folks need to do penance for the ignorance of your foreign policy and for the slaying of your middle class but things get sorted.

The USA is still the world’s most fabulous country by a country mile.

Closely followed by Australia of course.

Ian Qld

I realize they aren’t the same measurements, but BDI has rallied over the past few weeks. One would think they would move together.

BDI is for dry bulk commodities, such as iron ore, grains, etc. It has rallied before only to collapse again. Dry bulk carriers have gone bankrupt already. They’re in worse shape than container carriers.

The 1920’s Shipping glut preceded the 1930’s depression.

Although the drivers are a little different ,the projection’s look very simular. All that is needed is a Sept 29 trigger. china’s situation today Vis housing and population movements, is eerily similar to the US pre Sept 1929.

chinaused draconian methods to prevent the Mainland markets imploding recently, for how much longer can they keep this up??

TEU FEU rates, what is even more frustrating, is comparing the subsidized rates out of china, against the conference rates out of Japan. Which receive no state subsidy to Japanese carries, unlike the aid given to COSCO, CSCL, Et al by the chinese state.

Japanese shipowners can maybe borrow with negative interest rates. is this not a subsidy ?

Get used to the fact that NOBODUY but the state and The CB’S.

Will ever be Borrowing with Negative Rates.

So the answer to you deflection of unfair competition by chinese company’s due to chinese state subsidy’s, is NO.

What conference do you refer to? Thats been over for some time.

Japanese conference line out of Japann on the southwest Pacific run Mitsui OSK Etal still maintain their cartel.

Which is why you can move 3 heavy TEU’s from NE china for less than the cost of 1 Light from Kobe/Yokohama to Sydney or Auckland.

Cosco has always been a sailing Circus but a cheap one. Although out of japan it is not that much cheaper than Fesco its main non Conference/Cartel line competitor.

Even when crossing the Tasman, a most expensive piece of water to cross. Cosco does not go that much under the cartel rate.

Unless the good come from CHINA. on the same ship it is cheaper to go from mainland china via Sydney to Auckland than it is Sydney to Auckland.

Dont try and tell us there is no Cartel.

Just how many times have Maersk, CMA-CGM, Hanjin etc tried doubling their rates over the past couple of years only to be forced to backpedal furiously? That’s not only linked to fundamentals (better to ship at cost or at a loss than keeping a carrier idle) but to having to deal with COSCO and China Shipping Co., both State-owned and both not above operating at a loss for purely political reasons. The customers in Antwerp, Yokohama and Oakley don’t care which flag a carrier flies, as long as they get their goods delivered on time and at the lowest cost.

To this it must be added Chinese shipyards are now capable of building mega-carriers over 15,000 TEU of capacity and, just to make matters even worse, dry bulk carriers in the 400,000 DWT class. In short that shift towards a “consumer economy” seems to have sidestepped Chinese shipyards and their chain of supply. This capacity to build super-carriers has been added over the past five years and it’s highly unlikely it will just be quietly scrapped: part of CMA-CGM Explorer mega carrier fleet was built in Changxing and Chinese shipyards are always aggressively looking for buyers just to keep the factory doors open and the chain of supply rolling.

In short this is going to get a whole lot worse before it gets better.

But there’s probably some relief in sight for shipping company: with the Doha oil summit ending in a complete failure and Iran dead set to open the taps, fuel prices are bound to come down again, at least until October, when the next “freeze” meeting will be held.

And the Koreans are saying to china by Action.You cut a lot of the overcapacity you built after us, before we cut any, which the Japanese don’t like either.

http://davidstockmanscontracorner.com/too-many-boats-too-little-cargo-the-monumental-glut-in-global-shipping/

Pgph 10.

Cosco is a sailing circus. Its a very poorly run company with what amounts to incompetent management. Cscl is now gone. Hyundai and Hanjin will merge.

Some soft commodities were oddly active over the weekend. If this means futures contracts will be NOT rolled over, at least some container ships will have business. It will be fun to see if gold and silver are treated as “commodities” or “money” on Monday :P

CCF isn’t the only thing collapsing in China.

The New Middle Kingdom Of Concrete And The Red Depression Ahead

http://davidstockmanscontracorner.com/the-new-middle-kingdom-of-concrete-and-the-red-depression-ahead/

Supply-side economics gone berserk. Totalitarian regimes are capable of spectacular achievements, exceeded only by their spectacular human costs.

It should be very interesting to observe the catastrophe from a safe distance. No telling what that might be.

I usually live in China. I am visiting the US at present. I see the US as in worse shape, and less prepared for a world-wide downturn in business.

Customers = broke.

That’s all you need to know.

Wolf,

Are these percentage drops volume or $ weighted? For example, how much is shipped to Brazil and how much to the U.S.? Both are down, but in absolute terms I wonder which regions are being hit the most.

Another way to look at this would be to compare how much per-capita freight is Brazil importing vs. the U.S. and how much has it dropped?(population = 200m vs. U.S. = 320m).

Also, can you point me to a breakdown by port? I am especially interested in the Port of Houston. I was talking with a cousin there today about all the flooding (thankfully, he is on high ground) and he said FOR SALE signs are popping up all over and houses are sitting without offers.

P.S. My cousin is from Alberta, Canada, traveled the world as a highly skilled engineer, lived in Houston for 12 years, and works for one of the large oil-field services company. He says that the current price of oil will go back down and stay there awhile. Then, when it starts to go up it will skyrocket.

We all seem to think that you just turn the tap on and off, but he says it is a very complicated business. Once you lose engineers and highly trained people it will be difficult (and costly) to ramp up again.

C,

The percentages of Chinese export declines are based export data expressed in US dollars. Marginally different when expressed in yuan.

The US, Japan, and the EU are by far the largest destinations for Chinese merchandise. But Brazil has become a pretty big customer too. Note that transshipment through Hong Kong distorts some of the data.

I have no data about the port of Houston at my fingertips. Just a word of caution: ports are transit points. They don’t say all that much about how well the local economy is doing. If it’s cheaper to ship something to Houston and rail it to New York or Chicago, they’ll do it.

Thanks for the housing update on Houston. This confirms some other anecdotes I’ve been hearing.

I think your cousin has a good chance of being right about the price of oil. Watch hedging mania if it hits $60. That will restart the production boom in the US, with more pain to follow. But it might not even get that far for now. There is a huge amount of oil in storage. Until that glut has come down, really all bets are off.

Okay, over-optimistic buffoons will jump in and say that the problem is overcapacity in the Containerized Shipping Industry.

Right. Pull the other one.

Overcapacity plays a role, but NOT LIKE THIS.

John Little

Fk China. Boycott Walmart. We don’t need any more cheep plastic crap that breaks. 1000s of harmful chemicals in plastic kids playing with everyday for their billions.