Ah yes, the Millennials.

If we could just get consumers to borrow more so that they spend money they don’t have on things they don’t need in order to boost GDP and corporate profits, all would be fine. That’s the current meme among economists.

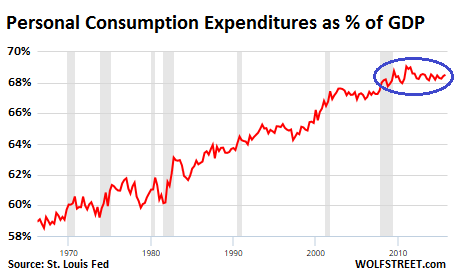

Since 68.5% of US GDP is related to personal consumption expenditures, boosting consumer spending is seen as crucial. Since wages at the lower 75% are crummy and have not been rising enough to keep up with inflation, the only other way to prod consumers into spending more is to bamboozle them into borrowing more and blowing this moolah instantly.

Cutting interest rates to zero was supposed to have helped that noble process (though consumers see those zero-rates inexplicably only on their savings and not on their debts). So that process of growing GDP by loading up consumers with debt, which worked for decades, has stalled:

Clearly, this strategy has bumped into some limits. And what is left over is debt weighing on people’s shoulders.

A lot of debt, for a lot of people: 61% of Americans say they carry at least some debt, according to a new report by Gallup that shows to just what extent carrying debt impacts consumer behavior and drags down consumer spending. As Gallup put it, “not buying things is bad for the economy.” But that’s exactly what a large portion of debt-carrying consumers are forced to do.

Consumer behavior is even more strongly impacted by the scourge of the American economy, “not having enough money to live comfortably,” as the survey found, which surprises no one. But consumers that carry debt – even people “who have enough money to live comfortably” – play a large role in the current economic quagmire.

These folks are “significantly more likely” to engage in a variety of cost cutting actions than those who’re debt-free. The most important cost-cutting actions?

- 46% put off a major purchase, such as major appliances, a vacation, or some home improvements.

- 31% put off buying a car.

- 20% sold off some of their possessions to make ends meet.

- 63% have engaged in a least one of the 10 cost-cutting behaviors in the survey.

So who are these forced cost cutters? Millennials and Gen-Xers, according to Gallup (Part 2 of the report). The survey asked whether they have engaged in 10 debt-related behaviors. Here are the top two by generation:

- Put off a major purchase (other than a car): Millennials 48%, Gen-Xers 51%, Baby Boomers 36%.

- Put off buying a car: Millennials 39 %, Gen Xers 35 %, Baby Boomers 21 %.

But GDP must be pumped up. So even the 35% of Americans who say they “do not have enough money to live comfortably” are trying to fill in the holes with debt. As a group, they carry 36% higher credit card balances – one of the most expensive forms of debt – than those who say they have enough money to live comfortably. Gallup in a separate report (emphasis added):

The difference is particularly acute among millennials, where those who say that they don’t have enough money to live comfortably carry three times more credit card debt than those who say they do have enough money.

They also carry more auto loan debt and personal loan debt. In short:

Millennials are the only generation where those who say that they don’t have enough money to live comfortably carry 8% more total consumer debt than those who say they do have enough money.

Having come of age in the era of the Fed’s zero-interest-rate schemes, these out-of-luck millennials are supplementing their income by borrowing more than their out-of-luck peers of any other generation, and in the most expensive manner.

But running up credit card balances or taking out personal loans to buy consumer items are acts that borrow from the future in order to consume in the present. That debt will have to be serviced in the future, with money that otherwise would be spent on consumption. And that “future” is now.

Because millennials are young and at the beginning of their careers and earning power, they are mortgaging more than the future by carrying debt: They are also mortgaging the present.

Millennials are putting off getting married, having children, furthering their education, and establishing their independence (by moving in with relatives) more than any other generation. This problem compounds if they have the added burden of student loan debt. Millennials’ total consumer debt load is $29,000 — but if that balance includes student loans, the total rises to over $40,000.

Consumer debt is a double-edged sword. On the one hand, it fuels the economy by giving consumers added purchasing power. On the other, it is a burden that limits individuals’ choices in the future, such as buying a home or a car. And for those with student loans, it can become a crushing burden.

That burden of debt that was incurred in the past to boost GDP is now weighing on consumer spending and on GDP. It explains in part why consumer spending is languishing, despite a growing US population – by 16 million since the Financial Crisis – and despite historically low interest rates that were designed to lure everyone into becoming debt slaves. And this too is the price to be paid today and going forward for the policies the Fed imposed on the US in 2008.

The impact is everywhere. Total business sales in the US have dropped to 2012 levels. Inventories have ballooned to crisis proportions. And as companies begin to respond by cutting costs, jobs will be next. Read… Why This Economy Is Now Running Aground

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Here is what one former central banker has to say about

the dangers of the growing global debt load that has been created by the world’s central banks. Governments, businesses and individuals have lined up at the trough, eagerly availing themselves of ultra-cheap credit without thought for the long-term ramifications of their foolishness.

I thought it would be William White.

About the only person in a position of power that seems to know what he is talking about.

It is only paper. In fact, it is only digital entries on a keyboard.

Relax. All debts can be eradicated by pressing “DELETE”.

All bankruptcy can be eradicated by a few key strokes on the key board and….press….ENTER.

Relax. Nothing is real. There is no “GOLD” or “SILVER” or other barbaric relics from the past….Japan owes 3 Trillion? Credit them…..3 Trillion. …..Detroit needs 1 Billion…credit Detroit 1 Billion

Relax.

Centurion,

The financial system(s) so perfectly summed up (pun completely unintentional).

Peace.

Well, fake or not – most people would be really upset if they took your fake credits OUT of Your account.

Your signature creates money. Your labor is what backs the fake currency. You don’t have to earn good credit, your labor IS credit. Just the fact that you are alive is what gives “money” value. These clowns in power know this. Use it to buy tangibles. Don’t buy into the PTB lie that you are being irresponsible by not paying back money YOU created. They are double dipping-they are the criminals.

Millennials and Gen-X are not taking on more debt, so the Boomers are still loading up on debt? Someone has to do it …

I guess Obama understands this because he seems to be ready to start forgiving student loans. Car loans are probably next to go or maybe some general refinancing at zero rates for everyone?

BTW in Netherlands student loans are not counted when you take on mortgage debt. So you can rack up loads of debt (you don’t even need to study for that, just claim that you are studying as many have discovered) and after those years of fun buy a home with zero money down, and with a little luck even get a new car loan as the lenders don’t want to know how much debt you have racked up. The bubble is still inflating, you just have to know where you can get all the ‘freebies’ (just make sure you have no money to pay back).

How can it be a real “debt” when the credit issued to you is not real money….but a “credit” to your account at that bank?

If I loan you a “credit entry”, how can you be in default when I loaned you “nothing”‘?

You take out a “loan” at my bank, but all I do is type in “$$$” in an account I just opened for you. There is no money, no value, nothing. You just have “$$$” credit.

How can you be in default of nothing? If you don’t pay me back, then what do I care since I loaned you “nothing”? Better yet, I should just type in to your accoutn…”$$$$” and you keep on going. You are consuming and paying bills and helping with the demand, aggregate demand, contributing to society, giving back to society and keeping up the velocity of “money”.

I don’t understand. Can some Ph.d. in economics explain how not paying back “nothing” can be a problem?

Almost everything is done electronically. If it’s money (a transaction of some kind, for example), it’s both a credit AND a debit, depending on which side you are. In fact, if you’re doing proper accounting like a company would (with double-entry bookkeeping), every transaction is at least a credit and a debt on your books. All done electronically. Most people get paid that way. Works just fine.

Debits and credits make the world go round. Just because it’s digital, doesn’t mean it doesn’t exist.

So if I give you some digital USD, which you claim isn’t real money, I would go ahead and take it because, real or not, you can buy stuff with it….

:-]

Yes, and as long as the Zombies continue to believe that digital is money, I accept it and then use it to purchase real money in the form of gold/silver. When people finally catch on, I’ll have to start using some of that “real money” to purchase the things that I need to survive. God help the Zombies.

If you exchange nothing for peoples labor it is called stealing not buying.

In support of your stance, I read somewhere that debt may have preceded money itself and that early writings and markings were a way of keeping track what everyone owed one another in the village. Money may have emerged later as a portable means to settle these debts.

If true, debt and credit have long been part of the human psyche and way of doing things. Dismissing money, debt and credit as mere electronic blips that are erasable would not set right with most.

I believe source is Debt: The First 5000 Years

Wolf, you invariably attract comments from the mis-informed re economics, money, debt. Invariably, they foresee the current system ultimately imploding, exploding, collapsing, etc. No one needs a “PhD” in economics to understand macroeconomics, just a willingness and an open mind to study it. Most people latch onto an idea (e.g., “fiat money”) and work backwards.

Very backwards..

It comes down to this: wishful thinking, by persons who want “justice in an unjust world”.

“I don’t understand. Can some Ph.d. in economics explain how not paying back “nothing” can be a problem?”

Well…. You my friend would be in violation of “Commercial Law” if you do not honor your debt to the bank.

Good educational video. https://www.youtube.com/watch?v=l_IgcmsqnVM

Plus, a fiat currency is backed by one thing and one thing only…. FAITH. If you do not repay your debt and all debts are just forgiven, then all Faith would be lost in the currency.

Our monetary system (Global) is so f@#ked up, it is only matter of time before this debt based system implodes.

With a discussion like this, unless terms get defined there is a lack of clarity in trying to reach understanding. To make ‘payment’ at one time meant to ‘extinguish a debt’ and this was reflected in the US Fed notes prior to 1964. Stated on the face of the Notes [1950 & 1934 Series]: “This note is legal tender for all debts, public and private, and is redeemable in lawful money at the United States Treasury, or at any Federal Reserve Bank.” These ‘Demand Notes’ “WILL PAY TO THE BEARER ON DEMAND TEN DOLLARS” .. it was the redeemable quality of the notes [evidence of debt] for the substance of ‘lawful money’ [gold or silver coin – at least during the 1928 Fed Notes that were redeemable in gold] that made “payment”. When debt instruments are said to make ‘payment’ what is actually happening is a ‘discharge of debt’ in equity. The debt has not been ‘extinguished’ as when the substance was redeemed in exchange for the paper note, rather it was passed on to another. Using debt instruments to make ‘payment’ is a misnomer that creates confusion and lack of clarity. There is more to the discussion, but enough for now.

They do create the money out of nothing but the service they really provide is to let you spend your own future income now.

They charge interest to cover their costs, for the risk involved and the service they provide.

Your repayments in the future, pay back the money they created out of nothing.

The asset bought covers them if you default, they will repossess it and sell it to recover the rest of the debt unpaid.

At the end all is back to square one.

The bank has received the interest for its service.

You have paid for the asset you have bought plus the interest to the bank for its service of letting you use your own money from the future.

Today’s massive debt load is all money borrowed from the future for things already bought.

It can also go wrong another way, when banks lend into asset bubbles that collapse very quickly. The repossessed asset doesn’t cover the outstanding debt and money gets destroyed on the banks balance sheets.

When banks are lending in large amounts on margin into stock markets the bust shreds their balance sheets (1929).

When banks are lending in large amounts on mortgages into housing markets the bust shreds their balance sheets (2008).

If banks don’t lend prudently you are in trouble.

Then they developed securitisation …… oh dear.

Stormtrooper,

Always amusing to hear people like you referring to “real Money.”

Money is whatever people believe in enough to use as a medium of exchange to trade something they have for something they want. It matters not a whit whether it is a giant stone doughnut or a series of bits flying over the internet.

The real money that you love — gold– is basically a soft, worthless metal, good only for making trinkets and jewelry. Gold as money is only useful because of a fashion that has become embedded in the mentality of humans for a few generations. It has no inherent value outside of fashion, and fashion changes with circumstances.

Much better to have obsidian if you need to make an arrow point to put venison on the table.

Increasing credit card debt in order to “live comfortably “? What does this term really mean? It’s not a number. Food on the table? New car? Furniture? What?

And credit card debt is the most onerous form of debt. Other than owing ‘Vinnie’ and being unable to pay the vig!

The TBTF banks own and control the largest credit card companies, where they may borrow at ultra low rates as low as 1/2 %, then turn around and charge credit card consumers up to 29% interest.

Even the most credit worthy credit card customers pay 9.25% interest. Miss one payment and watch what happens to that low rate! These high morally reprehensible usury rates by the TBTF banks, are nothing more than white collar legalized theft.

Debt slaves indeed. Gold is the money of kings, silver the money of gentlemen, barter the money of peasants, debt the money of slaves.

Not seeing what the revolution is. Seems like they are forced to stop, not because they WANT to stop because of the inanity of it all or to save the environment, etc.

Nah, they are still the same creatures as their predecessors, just with less money, that’s all.

I am shedding zero tears over their “sacrifice”.

Slaves can be induced to love their chains, be they wage slaves or debt slaves, clerks and congressmen alike. The techniques have been proven to be very effective.

All in good time. Your overlords (and overladies) can well afford to be patient.

Debt?? Been there, done that. We resolved to live DEBT free before retirement, and now in retirement continue too live DEBT FREE. Do we “use” charge cards? Yes, but pay them 100% before their due date so no interest expense. Do we buy “new” cars? Frankly, we have not since 1994.

We have bought “off lease cars” a year, or two old, after the nasty depreciation hits have been taken, financed them for say 3 years, then paid the loans off early.

My niece, who works at Ford, recently advised me that now aunts & uncles can buy a NEW Ford via their A plan. I just got my PIN today, and we will check out the feasibility of a NEW car when 2017 models are available. Hey, if the price is still ‘too high’ we won’t buy. I expect a glut of off-lease cars shortly, and sellers will reduce price/value to move stock. Our oldest car is 1 1993 the newest a 2010, so we have some time to evaluate.

While cars are nice, homes need to be kept-up with new roofs, appliances renewed, and just the general cost of life.

No free lunch anywhere. You buy what you need, not always what you want. We are used to it now.

I keep waiting to see if our governing bodies will ever get any financial smarts, hope grows dim there….

Yeah…buy a ‘new’ car….that tracks you mileage, tracks your whereabouts, contains ‘software’ that can be hacked, …. to one’s detriment………be my guest…buy up!

Eight years on from the financial crisis things seem to be going from bad to worse.

Some people noticed things were going seriously wrong in 2008 and started to realise the very obvious mistakes and omissions from supply side economics.

How could economics be so wrong?

The central tenets of supply side economics are ideas the wealthy would like to be true, but in reality, aren’t.

1) Supply creates its own demand

This is useful to ensure business owners don’t have to pay their employees too much. The consumer now has no relevance as “supply creates its own demand”.

Try telling that to China!

2) Trickledown

Justifies lower taxes on the wealthy, their wealth will naturally trickle down to those lower down the scale.

No evidence for it whatsoever, all the evidence points to capitalism trickling up.

The trickle up mechanism of Capitalism is known, the trickle down mechanism is not.

a) Those with excess capital invest it and collect interest, dividends and rent.

b) Those with insufficient capital borrow money and pay interest and rent.

Just believe you suckers.

3) All wealth is earned

Again helps to justify lower taxes on the wealthy as they have earned their wealth.

Conveniently ignores inheritance, trust funds and the difference between “earned” and “unearned” income that all Classical economists were aware of. Those at the top have been maintaining themselves in luxury and leisure from “unearned” income from their land and capital for centuries and they like to keep this quiet.

4) Money exists in steady state and circulates though the economy

Useful for hoarding by the wealthy and allows debt to replace wages as wages are kept at very low rates.

A short term idea that eventually blows up when repayments reduce consumer purchasing power to zero in the long term.

An assumption that leaves economists blind to 2008 as they can’t see how money is created and destroyed on bank balance sheets and the very real danger to banks when they lend money into asset bubbles.

Supply side economics – an economics based on the ideas the wealthy want to be true but aren’t.

An economics based on fantasy, no wonder it doesn’t work.

Keith: Called Reganomics in the 80s, it was put forward that people who already had wealth knew how to invest new wealth, thereby creating new jobs and more tax payers, thus benefitting us all. So the tax cuts were made and those benefitting most from those cuts did invest. The giant fly in the ointment was that those investments were largely made outside the US, creating jobs for citizens of other countries.

It has been an epic fail. What amazes me most is that the con has been allowed to run on for so long. I am further amazed that the con still sways people to vote against their own interests. I have friends, 36 years in, who are still awaiting their trickle-down. Some people really would rather eat crap and die, than to admit that they were wrong, and even more so, that they were conned.

The financial system, whether local, national, or international has one goal: extraction of value from an economy through interest payments.

If that dries up, game over.

My wife and I have been debt free for years. We use credit cards for convenience and pay them off every month. An interesting thing happens when you stop using credit. You value purchases differently. In the past I’d finance or lease (same thing) a new car. I was focused on whether I had the cash flow to cover the payment. I thought nothing of leasing a high end BMW. Now I look at the price tag and ask myself, “Would I seriously consider writing a check for $90,000 for that?”.

A good question to ask before making a purchase is ” What problem am I solving?”. “Broken refrigerator” is a real problem. Buying a Ferrari is more of a Freudian compensation problem. Buying a bigger TV with bells and whistles is a “too much time watching TV” problem.

Interesting approach but the examples you give are subjective.

Seemingly not for you but it is possible to manage without a refrigerator. Similarly not being able to afford a Ferrari or not wanting to watch a lot of TV is no reason to project your opinions about the merits of either onto those that can afford.

“My wife and I have been debt free for years. We use credit cards for convenience and pay them off every month. ”

And another thing. Using credit cards for buying something is borrowing so actually you are only debt free after you have paid the amount owing. The interest you are not paying on the loan is one reason why interest rates are so high for everyone that doesn’t pay the whole amount in one go.

This is all about managing down climate change caused by excess human consumption, all of it must be minimized.

I’ve been boycotting the economy for years now — particularly since C+Augustus was appointed to the presidency by the conservative nutbags on the SCOTUS.

And then there was the accountability moment in ’08 that we needed but weren’t allowed to have.

I can afford to play, but the game is rigged. The only way to win is not to play.

I take care of my/family needs, as local as possible and that’s it.

Eff them! Guillotines can’t come too soon…

Vern

I too, have cut way back from what I could produce and earn in this economy. But with the system rigged in favor of government employees, corrupt politicians and criminal financiers, I have elected to downsize everything since 2008. I could employ a lot more employees, I could produce more taxable income, but I want the predators and parasites to shrink down to a manageable size.

And I don’t care how long it takes. I can live without them.

I agree with you. I have my own “businesses” and REFUSE to hire. I work 3 nights a week doing stuff I could hire out, but why? Deal with more paper work is far better than the horrific paperwork when you hire somebody. F the worker. They vote for aholes like Bernie?…then stay unemployed.

No way. I have stopped growing my business since it is NOT worth it to me. Why should I run a larger operation and feed the PIGS that run this country. F them.

I run my company for ME. F you.

Hey Wolf

Is this kind of small business you were talking about.s

Bunch of agree owners.

Backbone of economy??? Not likely.

The French Revolution was a disaster from which the country never really recovered. The 70,000 executed during the Terror included many with no particular connection to the King, and of course at the end the original revolutionaries met the same fate.

In the early 1950’s France was so unstable that an approach was made to Britain to adopt their monarchy. (The movie Day of the Jackal is based on fact- the French secret service did try to assassinate De Gaulle)

France today is by a wide margin the least equal of the Western democracies. There has never been an equivalent of someone rising to the head of the executive from humble origins- one Brit PM had a circus performer father! Thatcher was raised above a grocery store.

But as bad as the French Terror was- it would be exceeded by the Russian under its revolutionaries- it never ended for one thing.

Be careful what you wish for.

Hey Vern: What makes you think you will be operating a guillotine and not enjoying the view below as the blade falls? If there is indeed excess capacity in whatever it is you and the commenter below do, others will step in to meet the demand. So, really don’t know exactly what you are accomplishing. But carry on.

OK, Zulu poles on Pennsylvania Ave then — with satellite locations on Wall Street and the Hamptons . Longer and more painful…

And BTW, IF I were collateral damage, it would be totally worth it.

JP and Michael nailed it, as far as I’m concerned.

Except for a modest mortgage when I was younger, I have been debt free my entire life, even when I have had spotty employment. How is such a thing possible? (By following the list in the article!!) I put off buying a new car and always paid cash when I did buy something. Always have. I paid for university by working and saving up. Our vacations were modest and involved camping. We stayed away from restaurants except for very special occasions, or when we had no choice. At home we lived like kings, eating quality food/meals not usually found in restaurants. Guess what? We cook our food and enjoy the process as a couple; usually with a nice glass of wine and music playing. My kids went to post secondary with visible goals, and not ‘to find themselves’, or as part of a life stage. They do not have big student loans because they also worked while they studied.

I think they call it, “living within your means.”

People need to think about priorities and accept that they are not part of the ‘jet-set’ when they draw a pay cheque.

About 3-4 years ago I bought a small tv. Our tv room is quite small, and I felt a 27″ would do us well, and also would not over power the room when we were not watching it. Well, the clerk just about had a fit and wouldn’t hear of me buying anything smaller than a 32″. I felt it would look stupid in our room and held out for the smaller model screen size. He thought I was stupid, and I remained polite but firm. It was also $150 cheaper. It works just great. Everyone else I know have these giant screen tvs that cost upwards of $1,000 (or more). The point is quite trite, but over time the $500 savings here and there add up to serious coin.

My newly restored 30 year old truck is better than brand new. I just got it back from the auto-body shop where they cut out all the rust and welded in new steel. It sports new fenders and I also made a new box for it. It is painted racing green….looks primo. Bodyshop bill $2500. My costs for steel and parts….about $700. $3200 for a ‘new’ truck isn’t too bad as far as I’m concerned. No use buying a depreciating asset…especially with ‘borrowed money’.

regards

Paulo: so you know, my comment above referring to “the commenter below” was not meant for you. I didn’t allow for where my comment would fall when posted.

Regards

Night-train

Right on, Paulo.

I live debt free. I don’t even own a house (have had 4, they’re nothing but work), nor do I rent. I spend most of my time camping in a small camp trailer with everything I need, including all solar powered. It cost me about 15k to outfit myself, excluding my vehicle, which I bought in 2007 w/ 7k miles and thereby with a good price reduction (paid 27k cash). It now has 200k miles on it and is going strong.

I live in the West where there are lots of good free camping spots. When I get tired of camping, I rent a motel room for a night or two, but I rarely get tired of camping. I don’t watch TV and rarely eat out. I buy virtually nothing but a bit of gas, my food, and the occasional pair of hiking boots or necessities.

I spend my time hiking, star gazing, exploring, doing photography and video, and reading and writing. I have two rescued dogs for company. When I get tired of a place, I move on. Usually I spend the summers in BC, the Yukon, and Alaska, and the winters in AZ, then the spring and fall in Colorado and Utah.

I’m 65 and in good health. I live on income from past investments and have enough saved to live for years, even if I needed to rent. I have one grown daughter and a grandkid and go see them when I want. I donate liberally to animal shelters and people in need. I retired at 48 when my last employer laid me off, decided to never work for anyone but myself again. It was an easy choice, though it involved reducing my wants and needs. No regrets. Anyone can live like I do if they’re willing to forego all the crap they don’t need.

Until bank capital requirements and borrower liar-loan down-payments go negative, just as interest rates, how many [employed/income earning] debt slaves are there remaining that could actually “qualify” for additional credit lines? Gut the productive element of an economy by transferring the mfrg off-shore while dumbing-down, debilitating and drugging the “work-force”, what’s to be expected? Duh!

Ooops! Probably stated something not “PC” again.

Censored!

We have been in collapse mode ever since 1971. We peaked as a civilization with the moon shot. Then we went straight away into resource unsustainability, and Nixon took finance off the gold standard. It’s been downhill ever since. We are past the wealth creation cycle and are now in the wealth recycle system all supported by credit. Credit is tomorrow’s resources spent today. It is mathematically impossible for this to end well.

Centurion ‘s idea above of hitting the DELETE key on debt is what will happen. Debts which cannot be repaid, especially en masse, will not be repaid. The Delete key is what a Jubilee will do in part.

It won’t save us but we might get some breathing space.

This “delete key” will instantly impoverish everyone who holds this debt as an asset, including pension funds, 401ks, banks, IRAs, corporations… Stocks will crash to next to nothing….

OK, so you say, no, let’s get the central bank to print this money instead and cover those holes. This is what you mean by “debt jubilee,” according to your many prior comments on this topic.

So here is a story: My dad (who was middle-aged when I came along) lived through the Weimar Republic as a teen. He told me all about it. The Weimar Republic had the same kind of money-printing program you’re espousing, and for which you’re spreading propaganda far and wide. I tell you, the Weimar Republic was not nearly as much fun as you make it out to be. Look it up!

In fact, it was terrible. And we all know how it ended! And that was more than TERRIBLE.

So I wish you kept your crazy ideas (wherever you picked them up makes no difference) to yourself. Your pro-money printing propaganda, however you dress it up, is not welcome here. Start your own blog and post your crazy ideas there. It’s really painful for me to read them.

My Mother and maternal grandmother told me the same stories about living in the Weimar Republic. My grandmother would wait at the shop where my grandfather worked with a suitcase. He got paid several times a day and when he got paid she would put the money into the suitcase and run down to the bakery or butcher shop to buy what she could before the price went up again.

“My dad (who was middle-aged when I came along) lived through the Weimar Republic as a teen. ”

Your writing this somewhat dark blog is beginning to make sense. The Schadenfreud is like a thick layer of jam.

But as to your other comment:

“The Weimar Republic had the same kind of money-printing program you’re espousing, and for which you’re spreading propaganda far and wide.”

“When money dies” gives a fair (I don’t know how accurate) description of what transpired in the Weimar republic.

One thing I took from that book ( quite boring actually) is that the Allies demanded reperations to be paid in gold! Historically the ratio of gold to script was fixed in Germany, until they had to export the gold to pay for the reparations.

Hyperinflation followed the devaluation of the currency (less gold, script worth less) and then down the line Hitler.

Hitler was a by-product of Ally greed, just as the terrorists of today are the byproducts of our foreign policy.

No Schadenfreude on my side. Just checking out the rust perforation of the structural parts of our beautifully inflated construct.

“Hitler was a by-product of Ally greed, just as the terrorists of today are the byproducts of our foreign policy.”

Get it wright or leave it alone Hitler was a byproduct of, Malicious, Vindictive, leftist, French, Arrogance, Cowardice, and Ego.

That document Guarantees another major war in Europe Woodrow Wilson

On the Versailles Diktat, before france, forced Germany to sign it. All the allies told france back off ,the french would not listen. England received no reparations of note from Germany neither did the US france gobbled it all.

What made it worse was that in 1936 when Hitler marched into the Rhineland he was terrified. France had the largest land army and the most Tank’s in Europe they were simply as usual to GUTLESS to use them. So a little war to remove Hitler in 1936, which france should have been able to accomplish became WW II.

China proved long before Weimar, money printing, is Catastrophic.

“No Schadenfreude on my side. Just checking out the rust perforation of the INTERNAL structural parts of our beautifully inflated construct.”

You left out the Ironic bit, the descendants of Guillotine operators and their bureaucrats, are today’s rich, the street mobs of france want to “Guillotine”.

Seems to be a cycle of around 250/300 years, and after every Kill the rich event. The people at the bottom, are worse off.

Leftists, never learn. They always want to smash everything, kill the rich, and build some new leftist utopia, with the money they stole from the rich they murdered.

Instead of resolve the issues in the current system and try to make it better.

Perhaps it is the curse of ill gotten gains, that ruins their dream time, leftist utopias..

The fact that those in charge can not even admit there is a problem seems to be the total problem. We know that nature abhors such an obvious imbalance and we all know that this imbalance can not last much longer. What none of us know and nobody knows is how this imbalance will be rectified!

Some suggest a jubilee and others massive defaulting. We know it can’t be repaid or even paid down to any extent because when you borrow against future earnings so far out, it just will never get paid without massive austerity which then adds to less economic activity which adds to more austerity or a deflationary cycle that ends in depression.

Many of us have our own plans in place to try and weather the coming storm but none of us know if our plans will actually work because no one knows the severity or the speed or the direction of the impending storm. So all we can do is blog to each other and hope that we can get a glimpse of it in time to rearrange our plan or at least batten down the hatches.. Good luck to all of us.

All debts are repaid in blood.

This one will be paid in the same way, sadly.

For those of you contemplating social security it looks like the are starting to tinker with the rules.

Here in Australia they have already started the squeeze and pensions, amounts, and rules which impact those in retirement and those that will retire shortly. I expect that the next budget to be announced In May will included even more taxes/rules changes/cuts in the retirement spectrum.

Social Security has announced changes to the “file and suspend” so it no longer makes any real reason to put off getting your social security as soon as you qualify:

“A popular tool families use to help boost retirement income known as “file and suspend” will be taken away after April 29th of this year, courtesy of the Bipartisan Budget Act of 2015.

File and suspend is essentially a way for one person who is eligible to file for his/her retirement benefits to file, but delay getting them until age 70 (in return for an 8% per annum credit). Once the benefits are filed for, however, that person’s spouse can file for spousal benefits and begin to receive those right away, thus increasing income to the couple.

One final element of this strategy is that if the higher income earner dies, the spouse can now receive the full benefit including that 8% per year credit amount earned by delaying, which significantly increases the income of the surviving partner.

The point of cutting out this “loophole” as the government so proudly calls it, is to save money. ”

http://www.zerohedge.com/news/2016-04-14/government-breaks-through-deficit-reduction-will-lower-social-security-payments

After all there are lots of ‘you’ out there and few of ‘them’ so it is better to to pay ‘you’ less so ‘them’ can keep or get more.

What is very interesting in the age we live in seems to be a lack of responsibility for ones actions. Lets delete the the mistakes of the irresponsible while the responsible carry the burden. Sorry, I do not buy it and my responsible children do not buy it.

What you consider the responsible, I consider the just lucky. Doing all the right things doesn’t guarantee success and failure doesn’t mean irresponsibility. In fact the most irresponsible people I have ever met are the ones doing the best these days.

They had us basking in this false since of security.

You guys are “rugged individualists” to the point of being a little bit sociopathic about it. They found the fossil of a leopard in South Africa that was about 2 million years old. It was buried under a ton and a half of what were obviously thrown rocks. Our ancestors survived what was a hard and dangerous world by cooperating and working together. If you had decided back in Ice Age times to be a free spirit and go marching off into the wilderness by yourself it wouldn’t have taken you long to end up as lunch for some predator. When the big crunch comes you need to provide leadership and not try running off to some hidey hole. You won’t last that long if you do. Nor can you live high on the hog because of your clever foresight when the others in your community are starving. They will soon be hunting you down. What would really make sense to me would be to revive some of that good old fashioned 19th/early 20th Century technology. how to farm the land with animals and forged iron tools. how to smelt and forge iron and basic metals for that matter, and many other things. Revive earlier forms of medicine so doctors could save lives without access to high tech and so on and so on. We might need to revive methods of social organization from Pioneer times too. When the big crunch comes down and people are panicked and desperate, get them together and organize the basic kind of society we had before. Most people would go along with that and serious troublemakers could be dealt with firmly. If you can realistically offer hope then people will come to you. Collect old tools and books on how to do things.

My ancestry is overwhelmingly Texan and we Texans could easily resurrect the Republic of Texas again if the united States falls apart. Do you guys catch my drift and see where I am heading with this? Be real Americans and not just isolated escapist hermits. Have some faith in what America was founded on!

You might be right. The obvious fly in the ointment is that the current populations cannot be sustained with iron tools and draught animals and while the developed nations populations are shrinking towards 19th century levels, the Islamic world and Africa are speeding towards the Malthusian limits of the land they occupy. Italy and Spain, e.g. could gently shed half their current population by ‘attrition’ but it is likely they will just be inundated by the surplus population of Africa.

As for medicine, we need to be honest. Clean water and antibiotics account for most of the ‘increase’ in human lifespans. Despite all the hoopla and expense, high tech medical care has only allowed the elderly to hang on for a few extra years.”Useful” lifespans have not increased. Our biological clocks still tick and we grow old and frail, useless organisms beyond 75 years except for the medical, legal and financial industries which feed on the shrunken bodies of the elderly. Unless and until the aging process can be stopped we do ourselves no great favor by allowing more to live into their eighties and beyond.

The ageing process can be slowed by eating healthily. Not starting to junk the junk food when you realise you’ve left it too late but throughout your life.

Most illnesses and ailments are self-inflicted. If you age prematurely then you only have yourself to blame.

While you’re doing that, I will be melting down aluminum cans to build the largest f*****g computer chip you have ever seen. All this back to the land bs is more than I can take. All the people touting this bs would rather die than give up their giant Ford pickups.

I can’t argue with your general premise that community (as opposed to hoarding canned goods and ammo) is the best means of dealing with socio-economic problems. But a return to 19th century social organizations and technology? Drive into the future with eyes firmly fixed on the rear view mirror?

Forgive me for making an assumption, but that nostalgia for a supposedly rosey past sounds so pale male. For the rest of us–women, minorities, gays–the past is the last place we want to go. This increasingly vociferous embrace of an idealized, undefined past moment sounds a lot like Trump’s battle cry.

You mean the ‘community’ that lives in the Melbourne CBD?

The one that lives in high rise apartments and votes Green?

The ones that leach off everyone for subsidized public transport, talks about reducing energy consumption, but needs a lift to get to their 25th floor air conditioned apartment powered by coal generated electricity and one that depends on somebody else to produce their food?

They’ll be the first ones that come running and screaming when the s**t hits the fan one way or another.

Yeah, that same ‘community’ that wouldn’t know how to grow even spuds.

Some people laugh at me when tell them that I grow spuds, cukes, spinach, tomatoes, garlic, eggplants, onions, peas, beans, peaches, cherries, and mandarins.

The taste is great and much better than that store bought junk, there is nothing on them as far as chemicals. We east fresh wholesome food and even better we save hundreds, if not thousands off our grocery bill each year.

When the ‘new wave age’ nutters like Al Gore, DiCaprio and the like give up their multi-million dollar houses, jets, boats, and start living like ordinary people maybe then ‘community’ may have meaning.

Until then it is so so much PC BS.

I am talking about complete political, social and economic collapse. Most people will die anyway, especially in urban areas. Cities do not hold more than few months food supplies. In the even that civilization crashes, I think the results will be utterly horrific and the cities will be left depopulated. if we are to continue civilization, especially American civilization, it will be predominately rural areas that will be in the position for it to survive. Without practical access to high tech, late 19th/early 20thCentury technology will be a good starting point, the alternative will be basically the Stone Age. I also think that organizing society along past structures would be an effective technique in a rural based culture. As for using draft animals and old equipment to raise food, it will be either that or turning over large rocks and grabbing quick for your dinner. The most precious thing we can preserve though, would be knowledge and there should be a big emphasis on that and education the first few generations, As long as he knowledge of Modern civilization is preserved,then it can be recreated. We don’t have to sink back into barbarism and superstition if we do, though we might have to fight fierce battles against those who do.

If we succeed in recreating an American civilization on a stable basis, then we can start searching the cities and scavenging the many high tech items we no longer have the means to create for ourselves. Then we can start recreating towns and cities as our numbers increase.

I am not at all talking about “going back to the land”, i am talking about saving something after effectively total collapse. I am talking about a kind of worst case scenario.

Things do fall apart pretty quickly as the fuel tanker strike showed in the UK in 2000.

No petrol, you can’t drive, you can’t get to work.

Deliveries can’t be made, staff can’t get to hospitals ……. etc ….

Gordon Brown was preparing to put troops on the streets in 2008 in case the financial system went down and people couldn’t get cash out or use credit/debit cards.

We live in a complex world that falls apart very fast when critical areas go down.

One of the flakiest areas being one of the most important, banks and money.

Let’s hope it doesn’t happen.

I’m getting old ( 63) I guess and so remember the days when the ability to get into ‘debt’ had to be earned. Credit cards were a status symbol for the affluent. Everyone else paid cash. I was ‘proud’ when Texaco deemed me worthy to have credit card good only to buy their gasoline. Ford then decided to take a chance on my and let me buy a godawful “Pinto’ for 36 monthly payments after I didn’t default on my Texaco card. Only after I proved myself to Ford did Wells Fargo allow me to escape the ‘cash’ economy and grant me a Visa and Mastercard.

Somehow the US economy managed to thrive then even though college students couldn’t borrow tens of thousands of dollars for tuition or put their beer tab on their credit card!

I grew up before credit cards and everybody had credit everywhere, at the grocer, the furniture store, appliance store, and clothing stores. The bill collector would come to the house if you missed a payment. I don’t know where the notion that people had no credit before credit cards comes from. BTW, my parents never had credit cards or a checking account. They only got a bank account when social security forced them to.

This brings back memories… I remember when my father was granted his American Express card. He was happier than he would have been had he won the lottery. AmEx around here was the credit card for “high flyers” and if it was approved it meant you had made it big, something necessary given I have vague memories of the monster fees it came with.

Clearly next move is no down payment housing, probably pick-a-pay or interest only or whatever exotic idea brought on the 2008 mess. This is foolproof because the Fed can’t predict bubbles and the banks must be bailed out no matter what to protect us from Armagideon or the Collapse of Civilization. Rinse and repeat. Yellen insists she’s got plenty of ammo. Good old Ben is still pimping his helicopter drop. Buy stocks!

In England it feels like there are no people with money AND ideas. The money people refuse to take a risk and the people thinking of the future have no money. It also seems that we have a constant supply of cheap labour coming in from the east which drives wages down. What you find here is that they love an immigrant until he has kids and then they cost the state, so he then becomes the “typical lazy Brit” .

Also somebody else mentioned money going abroad to benefit other countries workers…snap! Same here. ALL the money goes off shore, but it’s for the companies and ruling families AND we pay for the European Union and massive payments to countries we are scared of. We are not allowed to carry arms here and we are trained from birth not to cause a fuss!! We will politely go down the drain and apologise for the noise.

“Ruling family” is so 18th century.

Will the people…really?

“In 50 short years debt has gone from being a luxury for a few to a convenience for many to an addiction for most to a disease for all ” – James Butler

Just saw this as well. RE: Debt Saturation. The economic status quo is a failed construct. How apropos.

To paraphase former President Bill Clinton “It’s the debt, stupid!”

http://www.hoisingtonmgt.com/pdf/HIM2016Q1NP.pdf

2015’s Surging Debt

The striking aspect of the U.S. economy’s

2015 performance was weaker economic growth

coinciding with a massive advance in nonfinancial

debt. Nominal GDP, the broadest and most reliable

indicator of economic performance, rose $549

billion in 2015 while U.S. nonfinancial debt surged

$1.912 trillion. Accordingly, nonfinancial debt rose

3.5 times faster than GDP last year. This means

that we can expect continued subpar growth for the

U.S. economy.

The ratio of nonfinancial debt-to-GDP rose

to a record year-end level of 248.6%, up from the

previous record set in 2009 of 245.5%, and well

above the average of 167.5% since the series’

origination in 1952 (Chart 1). During the four and

a half decades prior to 2000, it took about $1.70

of debt to generate $1.00 of GDP. Since 2000,

however, when the nonfinancial debt-to-GDP ratio

reached deleterious levels, it has taken on average,

$3.30 of debt to generate $1.00 of GDP.

This suggests that the type and efficiency of the new

debt is increasingly non-productive.

Most significant for future growth, however,

is that the additional layer of debt in 2015 is a

liability going forward since debt is always a shift

from future spending to the present. The negative

impact, historically, has occurred more swiftly and

more seriously as economies became extremely

over-indebted. Thus, while the debt helped to prop

up economic growth in 2015, this small plus will

be turned into a longer lasting negative that will

diminish any benefit from last year’s debt bulge.

Bruce sounds encouraging NOT

This complaint of “not having enough money to live comfortably” indicates clearly that living standards in “developed” economies must fall much further yet to reach levels commensurate with those economies’ dismal productivity levels.

As I see it, corporate debt is owed to whom? I suppose it could be argued, corporations might have a way out if currencies were devalued but it’s improbable all currencies can be devalued, so this idea doesn’t seem possible?

Another mechanism that might save corporations is by increasing prices but who has the income to pay those higher prices?

So there could be waves of defaults, the debt owners get stuck. I guess currencies could actually increase in a reverse Wiemar?

Wiemar was a result of punishment for a singular country, arranged by the financial system as far as I know, not sure how that can be translated to today’s situation? Not arguing, just I don’t see the correlation.

Some very good traders I know have been completely wrong (esp about gold) since 2009 concerning the macro picture…….

Oh, and US for one, has a huge military thus most likely strongest currency from that perspective.

No, I really wish someone was interested in the theory of purposefully slowing global growth in the name of climate change, that’s what I believe is really occurring and it’s ALWAYS the phenomenon everyone misses that comes true, I haven’t heard anyone going off on this tangent, which is one big reason it holds credence.

Why should the US care about racking up larger debt, considering the $US is one of the cleanest shirts in the hamper? And yes, I do believe they intend on confiscating wealth, for the purpose of contracting economic growth.

There are some aspects that make no sense to me though, such as why didn’t the US support Europe’s carbon tax for air transport?

April 22 is Earth day, I guess it’s cause for celebration IF they can expedite implementing regulations targeted at stopping growth in it’s tracks, so far the progress has been impressive.

Oh BTW, when does Soros buy out Peabody Energy?

“No, I really wish someone was interested in the theory of purposefully slowing global growth in the name of climate change, that’s what I believe is really occurring and it’s ALWAYS the phenomenon everyone misses that comes true, I haven’t heard anyone going off on this tangent, which is one big reason it holds credence.”

G7, G20, IMF, World Bank, cant get that organized, and the 2 biggest total polluters on the planet. India and china, will not play that game.

To slow global growth, to effect climate change, you need to REDUCE Population. Particularly in the Explosion zones, Muslim Greater ME, Indonesia, Malaya, Indian sub Continent, Africa, Brazil, Central America. Not by exporting it, but by the chinese method of not producing it.

Mainland china has moved back to ONLY 1 PLEASE, from, 1 or else. The only area the CCP have really ever done anything globally positive in.

India, the Muslims, and the Catholics (In south America, Africa, and the Philippines) are still playing the same game. World domination by majority population mass. Unless these policy’s are aggressively reversed. Humanity will become extinct, probably in a combination of global rising sea levels and epidemic Disease. The planet can be viewed simply, as a huge Farm, overstock a Livestock Farm, at your peril.

Climate change, was a factor, in what happened, to the Dinosaurs.

Climate change deniers can deny Humans are responsible, for the greater changes, all they like. I have used the Coastal waters for over 45 years, sea levels have noticeably risen, and are continuing to rise. The continuous wind speeds are rising on average, storms are more aggressive, and greater in number, global sea temperatures are rising, simple facts on the water.

If Peabody was worth buying Warren would be chasing it.

Soros makes noise, he no longer makes the big Decisions in his entity. He admitted that, some time ago.

The game with peabody may be to let it go under, then pick out the viable pieces from the Liquidators. Less labour related issues that way. In a sector that needs big consolidation.

If it goes under completely, the creditors take a bigger hit, which is good, as larger segment of debt and equity, so segment of wealth, simple evaporates.

Very interesting to read how the main story topic can go off the tracks so easy and create a chain of seemingly unrelated comments and stories.

As for the GDP and spending in general, Debt aside, suppose…just suppose that folks have reached a point where they say…I don’t need it.

As if an epidemic, I hear and see more and more ( regardless of age) saying I…Don’t…need…more, and I don’t need that.

I include myself and my family in this thinking. 2008 and the following years, wondering if the economy was really going to a 1929 style crash, taught us to…do without. That spending pattern is now broken ( think of someone who finally stopped smoking or drinking, or got off drugs). So I thank the FED and the banks for teaching us restraint and respect for cash.

I now have more cash than I have had in years, just sitting there and happy to have it do so. I hear the siren song of ‘it is loosing value and you are not getting interest”. Yet, everywhere I look I see my stash of cash as being able to buy more than it could last year or the year before ( if I spent it). And, what has a higher cost ( i.e. a share of stock) I would not touch.

“I thank the FED and the banks for teaching us restraint and respect for cash.”

You just thanked those who created the bubble (and subsequent crash) in the 1st place.

I know it was a setup in my heart, I cannot thank them and hope they go to hell.