These private equity firms are now waiting for a miracle.

The IPO pipeline is blocked and chock-full, after a dismal fourth quarter and an abysmal first quarter: in terms of deals, the worst since 2009; in terms of money raised, the worst since before the dotcom bubble. A fiasco with implications for the overall stock market.

So which IPOs are actually is stuck in that pipeline?

First thing you notice is that the VC-backed startups with the most dizzying valuations, such as Uber, Airbnb, Palantir, and Snapchat, are not in the IPO pipeline!

Instead, you find LBO queens. Private equity firms acquired these companies, stripped out equity, and loaded them up with debt. Now they’re trying to exit them. And there are some spin-offs too.

Of the 118 companies waiting to go public, according to Renaissance Capital’s Quarterly IPO Review, 42 are in the “active pipeline,” with new or updated filings since January 1. But everything has come to a halt.

So which major company dares to be the icebreaker, the one that allows the others to follow?

If the first major IPO this year flops like the last major IPO in October — KKR-backed First Data, buckling under $20 billion in debt — it might shut down the pipeline entirely. The first major IPO simply must be a success!

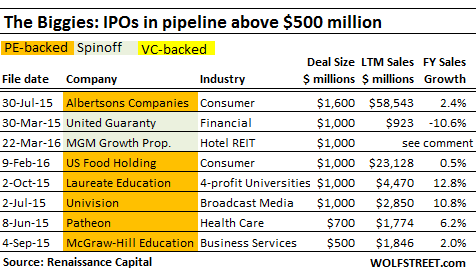

Below I discuss key IPO candidates in that pipeline, separated by size into three groups. This table shows the largest IPO candidates, with estimated deal size (amount raised) of over $500 million. The “LTM sales” column shows sales for the last twelve months. The LBO queens are orange, the spin-offs gray, and the VC-backed startups yellow. But there is no yellow:

A wild ride through LBO & Private Equity Land

Neiman Marcus is not even on the list. The owners of the LBO queen, Ares Management and the Canada Pension Plan Investment Board, were going to dump it on the unsuspecting public in October but at the last minute postponed the IPO until 2016. In December, the luxury retailer reported a sales drop of 5.6% – the first drop since 2009 – and a lot of red ink, as it is struggling with $5 billion in debt (7.1 times Ebitda!). And it scrapped its IPO for good.

Albertsons Companies: The supermarket chain was acquired in a 2005 LBO by a group of PE firms led by Cerberus. In January 2015, the company acquired Safeway to get a handle on competition. But in October, during the brick-and-mortar retail swoon, it postponed its over-priced $1.6 billion IPO. Now everyone is waiting for it to slash its price. But it’s loaded up with $12 billion in debt and needs a big price to help pay down that debt.

United Guaranty Corp, a mortgage insurer that AIG is trying to spin off. Investors got mauled in recent spin-offs, such as Oxy’s disastrous spin-off of California Resources. Spin-offs are carefully timed to occur near the cyclical peak of that industry. AIG, seeing perhaps the end of US Housing Bubble 2, decided that now is a good time to unload its mortgage insurer.

MGM Growth Properties: MGM Resorts is spinning off 10 of its hotel properties – including Mandalay Bay, The Mirage, and Luxor – with about 24,500 hotel rooms into a publicly-traded real estate investment trust (REIT). MGM Resorts will also conveniently transfer $4 billion of its debt to the REIT.

US Foods Holding: The second largest food distributor in the US was acquired in a 2007 LBO by PE firms Clayton, Dubilier & Rice (CDR) and KKR. When they tried last year to sell it to Sysco, the largest food distributor in the US, for $8.2 billion, regulators had a hissy-fit. Now they’re trying to sell it to the public.

Laureate Education, which operates for-profit universities around the world, is backed by the who-is-who of private equity, including Henry Kravis, George Soros, Steve Cohen, and Paul Allen. The company was taken private in a $3.8 billion deal, led by KKR. In 2010, Laureate hired former President Bill Clinton as honorary chancellor. He traveled all over the world to Laureate’s universities to support them with the prestige of the US Presidency still lingering around him.

Alas, for-profit education has gotten hammered by regulators, student-loan advocates, lawsuits, investigations, and judgments. Felled by these attacks, Corinthian Colleges, once the second-largest for-profit university chain in the US, went bankrupt.

Investors have taken notice. The shares of Strayer Education have plunged 67% since 2011. DeVry Education Group has plunged 73% since 2011. Capella, after considerable volatility, is about flat with 2011. Apollo Education Group has plunged 86% since early 2012.

Univision Communications: America’s big Spanish-language broadcaster was taken private in a $12.3 billion LBO in 2007 by PE firms Madison Dearborn, Saban Capital, Providence Equity, TPG Capital, and Thomas H. Lee Partners. The deal was funded by piling $10 billion of debt on the company. Moody’s rates it B2, deep into junk. Debt can kill the best company!

Patheon: The pharmaceutical services company was acquired in a 2014 LBO by Dutch healthcare multinational Koninklijke DSM and US PE firm JLL Partners.

McGraw-Hill Education was acquired by Apollo Global Management when McGraw Hill split into two, the other part being McGraw Hill Financial, which owns Standard & Poor’s.

Those are the biggies stuck in the pipeline.

Ah, the First Tech Startup

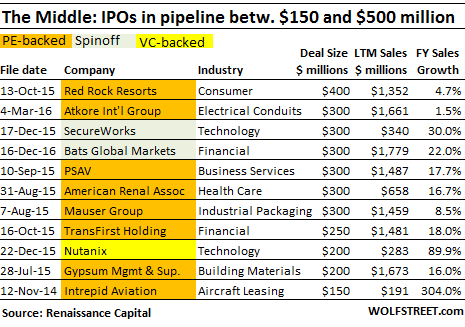

The table below lists the mid-tier IPOs stuck in the pipeline, most of them LBO queens. Two are spin-offs. And one finally is a VC-backed tech startup!

Red Rock Resorts: Formerly known as Station Casinos, it operates casinos in Nevada and Indian casinos in Northern California and Michigan. It was taken private in 2008 by PE firm Colony Capital and the founding family, led by Frank and Lorenzo Fertitta. It promptly went bankrupt in July 2009!

It emerged from bankruptcy in 2011 with $4 billion less in debt and changed ownership structure. Now Deutsche Bank owns 25%, with the option to put the company into an IPO five years after exit from bankruptcy, so as soon as June 2016, to unload some of its shares. JP Morgan Chase ended up with 15%. Some bondholders and Colony Capital still own about 5%.

The biggest owners are the Fertittas, with 45%. Red Rock Resorts pays their operating company, Fertitta Entertainment, a management fee. Proceeds from the IPO, about $460 million, are to be used to buy out the management company, according to the New York Post, “delivering a windfall for the brothers,” to be funded by the public.

Atkore International Group manufactures galvanized steel tubing, sprinkler pipe, steel and flexible non-metallic conduit, pre-wired armored and metal clad electrical cables, etc. Founded in 1959 in Illinois as Allied Tube & Conduit, it became part of Tyco International and acquired other companies. In 2010, Tyco sold a majority stake to PE firm CDR, which gave it the fancy moniker Atkore International. And it continued to grow by acquisition.

Its credit rating is deep into junk. Moody’s rates it B3 due to its “elevated leverage, weak interest coverage, low margins, sensitivity to volatile steel and copper prices, as well as its reliance on nonresidential construction activity, which drives demand for most of its electrical and tubular products.” So now would be a great time to sell it, if CDR could just line up some buyers!

SecureWorks was acquired by Dell in 2011 for $612 million. In 2013, Dell underwent an LBO by Michael Dell and Silver Lake Partners. Now it’s trying to shed assets to better deal with its mega-debts. Hence its efforts to spin off its cybersecurity business.

Bats Global Markets, which operates exchanges and provides services for financial markets, counts among its owners: Bank of America Merrill Lynch, Citadel, Citigroup, Credit Suisse, Deutsche Bank, Goldman Sachs, Instinet, JP Morgan, KCG Holdings, Lime Brokerage, Morgan Stanley, Spectrum Equity, TA Associates, Tradebot Systems, and Wedbush. They’ll make it fly!

But wait…. In 2012, Bats had to scrap its IPO after a “botched trading debut,” as Renaissance Capital put it mildly. So now it will try again, listing its shares on its own Bats BZX Exchange.

PSAV: The audiovisual and events company serving the hotel markets was acquired by Goldman Sachs and Olympus Partners in January 2014 for $878 million.

American Renal Associates: In 2010, PE firm Centerbridge Partners acquired a majority stake in what is now the largest provider of kidney dialysis services in the US. The IPO, delayed since August, has some wrinkles. The Wall Street Journal:

But first, the Beverly, Mass., company said it plans to split its stock, pay a yet-to-be-set dividend to current shareholders and enter into an agreement to share its tax benefits with the current shareholders after going public.

The so-called tax-receivable agreements have become increasingly common in initial public offerings – dubbed supercharged IPOs.

American Renal Associates, much like Shake Shack Inc., would pay 85% of tax benefits it receives to private-equity owners.

Mauser Group B.V.: The Netherlands-based company manufactures plastic, metal, and fiber drums and intermediate bulk containers that it also reconditions and resells as used. It was acquired by CDR in 2014 for $1.2 billion, funded by a pile of debt, and now sports Moody’s deep-junk credit rating of B3.

TransFirst: The payment processing services provider started out in 1995 as ACS Merchant Services. In 2000, it was acquired by GTCR Golder Rauner and changed its name. In 2007, the PE firm sold it to Welsh, Carson, Anderson & Stowe, which sold it to Vista Equity Partners in 2014. Now, after each PE firm has stripped out what it could, it will be sold to the public.

Nutanix: Voila, the first tech startup on the list! The “cloud” storage provider is backed by a gaggle of VC firms. Cloud storage is a tough business, dominated by Amazon, Google, Apple, and the like. New entrants have a hard time. Box, which went public early last year, saw its shares crash from $25 on the first day to $8.82 in February, before rising to $12.35 now.

Gypsum Management & Supply, America’s largest independent distributor of drywall and acoustical building materials, was acquired in February 2014 by PE firm AEA Investors. With the enormous construction booms in some cities, including Houston and San Francisco, looking increasingly precarious, it’s time to unload.

Intrepid Aviation owns Airbus and Boeing passenger jets that it leases to airlines. Among its owners are PE firms Reservoir Capital and Centerbridge Partners. It filed for an IPO in November 2014 but has since failed to take off. In its S-1 filing at the time, it disclosed that it had long-term debts of $1.6 billion and $4.8 million in losses for the six months through June 30, 2014.

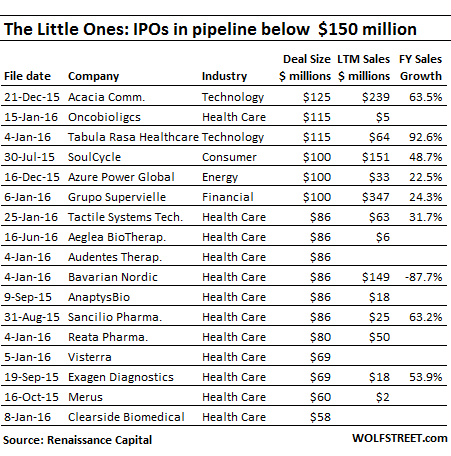

The Little Ones: no product, no revenues, no problem

The table below shows highlights of the smallest offerings, many of them biotechs without product or sales.

The standout in this group? A San Francisco startup that makes money.

SoulCycle “doesn’t just change bodies, it changes lives,” it says on its website. “With inspirational instructors, candlelight, epic spaces, and rocking music, riders can let loose, clear their heads and empower themselves with strength that lasts beyond the studio walls.” You get the idea.

It has 58 fitness clubs equipped with stationary bikes. You book bike and class on your smartphone. If you’re fast enough, you can reserve a bike in front of a fan. The company expects to have 250 clubs in the US. One more national fitness chain. For the nine months ended September 30, 2015, revenue rose 50% to $118 million. It’s said to be profitable. It’s not exactly a tech startup. But hey!

These are key companies in the “public pipeline.” Renaissance Capital also has a Private Company Watchlist of 258 companies that it believes could go public in 2016 – if they can. Because there’s a problem:

The IPO window may only be open to some of the largest and best-run companies, which may still face valuation pushback as weak public valuations and overheated private valuations converge.

And companies that can’t make it out the IPO window? For many of them, particularly the over-indebted deep-junk-rated LBO queens, it’s going to be tough out there.

Despite the booming stock market that is just below its all-time high, which would normally entail a booming IPO market, IPOs are in the worst shape since 2009. And something has to give. Read… The Fretting Among Wall Street Gurus Has Begun

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Billions in debt! Amazing!

I apologize for being off topic, but I was wondering if anyone read the story in the “Washington Post” about Trump predicting a major recession? The author stated that, regarding a coming recession, no mainstream economists agreed with him. That only a few economists on the fringe held the view of the recession threat.

I guess the mainstream economists would be those who missed the 2008 dust-up until after the economy was nearly destroyed. And I guess those in on the game are in up to the hilt, or are they being willfully ignorant?

Which only goes to show that Trumpf, for all the vast scope of his personal deficiencies, still isn’t nearly so deeply corrupt and wilfully stupid as your garden-variety Wall St. economist.

Trump Wars: The Farce Awakens.

That is Drumpf, not Trumpf.

Maybe his Atlantic City experiences give him insight

This is what the Fed’s (and other CB’s) ZIRP policies have brought us. The PE backed IPOs have tons of debt on their books, and they want investors to buy stock at very over valued numbers.

I love the quote on Neiman Marcus, ” …a lot of red ink, as it is struggling with $5 billion in debt (7.1 times Ebitda!). And it scrapped its IPO for good.” People buy IPOs thinking they’re getting in on the ground floor, but the IPOs Wolf listed look more like getting in on the septic tank!

Personally, I prefer to own stock in companies that have revenue growth, and operate in the black – not the red, but that’s just me. Ten days ago, I did sell off half of my equities (a week too soon, darn it) because I do not see any fundamental reason that the markets will continue to climb. Though, as others have opined, where else do you put your money?

Pay off ALL YOUR DEBTS and invest in yourself or invest in your children.

OR, buy a nice commercial building and open the hottest sports bar in town. I have many a “retired” doctor friends who have quit the pathetic “health care” business (it is not even a business anymore and you can forget the “health” care part) and have opened entertainment type businesses: Bars, Sports bars, Marinas, Mini-Golf…..anything to get out of the target sight of Government and Insurance companies.

Sell entertainment, booze, burgers, fun, youth. Not a single one of them advises their own children to enter “health care” but have done what they are doing so their kids can have a business that they can run.

One guy I know is telling me the BIGGEST mistake he ever did was go to Medical school and waste 25 years of his life. He, and his family, have the best sports bar in town.

They tell me America’s future Docs are coming from India, Pakistan, Taiwan, and get this, even Vietnam. Imagine, the son of the guy you killed in the Mekong is going to be your doctor, G.I.

Vietnamese are some of the finest people I have ever met. Very gentle and kind. They don’t hold grudges like Americans.

Just don’t invade their country.

My wife is VN. When I first visited I thought they might hate me – but I had a really, really great experience pretty much everywhere I went (and we traveled a lot on the first visit).

Eventually I asked her about it and she said “Well, they think they won.”

Truth is, many … most really … have a really hard time making ends meet, but their perception is what matters and American’s (who always pay more for everything – a sport I engage in regularly with merchants) are almost always welcome.

They do have crime in some areas, so, as always, be thoughtful and cautious. That said, if you stick to the main tourist areas it is fine – we have taken the bus on many, many occasions and are almost always accompanied by the weird backpack/hostel living europeans.

Regards,

Cooter

I saved them money, I went to VN to get my medical physicals (and dental and glasses) in February because the US costs were so high. Didn’t break even but got to visit the wife’s family.

Came pretty damn close to even though.

You are correct though that medical costs will destroy what is left of the middle class. However, this is by design.

Regards,

Cooter

It is all value proposition and ingenuity. Here is a classic example.

When I lived down south, I had this buddy of mine (really sharp engineer type – grew up on a ranch) that had a place SW of the urban sprawl I had to suffer with (he had a hell of a commute). Anyway, on his place, he had a few cows and a nice garden – but the land was very sparse with no tree or anything – fairly barren really.

So I asked him one day how his garden looked so nice. Turns out the “grey” water from his septic fed into his “stinklers” that watered his garden!

I LOL’ed so hard – I had never heard of anyone doing it that way before (we always planted over and downhill of the septic drainage).

There is probably a modern day investment axiom in here somewhere …

Regards,

Cooter

Nice list. One of the companies that stood out to me was Bats Global Markets. Looking at the partial ownership list of this company & then what they do as a business has me just shaking my head. How wonderful for them to list their shares on their own exchange. Big WOW!

I guess this means you won’t be an early mover in BZX 500 index futures. I can’t wait to short it myself.

How exactly do they figure out what to put on the balance sheet of a company with no product and no revenues? Or is that what random-number generators are for?

GOODWILL?

Past Performance of the Partners?

Estimated Projected Earnings?

Historical Comps?

Reminds me of the old joke (very off color) …

Gal comes home and tell her mom, I found out today I got a case of the herpes.

Traditional response: Give it to your dad, he will drink anything.

New response: That is all right hon, stack it with the other cases of goodwill.

Regards,

Cooter

P.S. In my recent accounting classes, goodwill was one of the hardest things for me to really get my head around, until I realized it was almost always another case of the herp. Do I have it wrong?

can’t help but notice the KKR kiss of death on a number of the companies discussed……….

O ye of little faith. RJR Nabisco worked out, didn’t it? So long as Jonathan Pryce is still running the show you have nothing to worry about.

“The IPOs Stuck in the Pipeline? Not What You Think!”

Financial constipation? A little liquidity should loosen it up.

Why should people go in for these new ways to lose money when the old ways are working so well?

Love the lists. Here’s my take on a couple of them:

Neiman Marcus:

I use to love it, now I only like it, and only because it is still better than Macys. It is either junk or jewels with them now. Not much that appeals to the affluent middle class woman. Saks is already ahead of them as a premium shopping destination. If they go public I expect they will disappear between Macys and Saks.

Univison:

They picked a fight with Trump and he will make them pay for it, if and when he gets to the WH. Aside from that, the shows are tired, the same ones from 10 years ago. They also switched production of their soap operas to the states and the quality of the content is not as good as before. Many of the soaps are now about the narco wars in Mexico and Columbia, boring, but they seem to know a lot about the subject. I would stay away.

Bats Global Markets:

My favorite of the bunch. If they can’t make money skimming and scamming then nobody can.

Dell:

Not on the list but will be eventually. If you fall for it again, you deserve everything that happens to you.

UNIVISION needs to go back to what their market really wants: Hot looking blondes with nice (you know whats) that speak Spanish and lots and lots of glitz. Their target audience does NOT want contemporary stories….they left Central and South America to have the materialistic good life with the White folk and don’t want ANYTHING to remind them of the “old country”.

They want images of money, cars, houses, parties and light-skinned women. (Isn’t that what we all want).

Oh, and every single soccer game being played anywhere in the world…. GOOOOOOOOAL.

Borrowing money you can never pay back? At time honored tradition. The IPO market is all about confidence. So I guess they can tell confidence is not good right now.

Excuse my ignorance, but the plethora of acronyms gets dizzying at times. I’ve got PE, IPO, but not LBO. Could someone set me straight please?

Leveraged Buy Out: the acquisition of another company usign significant amounts of borrowed money, either loans or bonds.

The assets of the company being acquired are often used as collaterals for the loans, and normal practice is to “dump” upon the newly acquired company the costs of servicing the loans and/or bonds issued for its purchase.

As leverage ratios of around 90% are not rare, this means that a very considerable part of the newly acquired company’s revenues will go into servicing the debt incurred.

Sounds reasonable to me…………………………………

And, as I was explaining to my wife earlier, when a company defaults/BKs/etc, all creditors ARE NOT the same. Being first in line to get paid, have control of assets, etc, is very, very key – particularly when things are really out of balance.

So it isn’t uncommon for lots of debt to fly around and the folks who lose may not be who you would expect.

Do. Your. Homework.

P.S. (before I sign) If you don’t have your own hot shot legal bond team – you will probably lose. If you are Joe Bond Investor, find another hobby – racetracks, pull tabs, blackjack, poker are all pretty attractive by comparison.

Personally, I am getting out of debt, saving some dough, and looking at what things look like after the sun hits the earth.

Regards,

Cooter

leveraged buy out

Investopedia is a great tool.

A leveraged buyout (LBO) is the acquisition of another company using a significant amount of borrowed money (bonds or loans) to meet the cost of acquisition. Often, the assets of the company being acquired are used as collateral for the loans in addition to the assets of the acquiring company. The purpose of leveraged buyouts is to allow companies to make large acquisitions without having to commit a lot of capital.

This Debt theme/meme is amazing isn’t it?

Or, the purpose of LBOs is so that the arrangers of the deal and new ‘owners’/controllers can pull out huge fees and pay for performance, effectively strip out whatever equity is left in the company.

Your questions is a good one, and I should have explained it better in the text.

Thanks to our commenters for stepping in and helping out. Good explanations!

I just re-read the headline. I had three acronyms in it. Terrible! So I changed it.

HI Petunia. I remember when Neiman Marcus opened it’s store in Houston in 1970 at the Galleria. It was a destination shopping experience which was like no other. One could see Stanley Marcus on the floor from time to time. So sad to see how far they have fallen. Your assessment of their fate is dead on.

Macy’s: How in the heck are they still in business? The sad thing about the Macy’s back story is that they gobbled up all of the classy, higher end, regional department stores that were on par with Nordstroms. The variety of the high middle to upper range shopping venues has been wiped out.

Macy’s = Walmart of clothing.

What will NM become?

Dona, a soul mate. As for NM, I remember when Henri Bendels was the coolest store in New York City. Now it is a shadow of its former self. I expect NM to follow the same fate, unfortunately.

I trace the decline of high end retailers to the decline in the quality of their staffs. I remember when the sales people of every store on Fifth Ave. knew the names of all their regular customers. Now they can’t even add.

DONA,

I was there in 1977, and even though a guy, I was fascinated with NM. Their catalogs, their image, their history, their culture…….even though I was a student and had no money, it was like walking into American Heaven…..what used to be…..what working was for……the dream.

My unsolicited, un-trained, marketing mind says SOMEBODY needs to have the kind of store NM used to be. Stop trying to appeal the the masses. Stop trying to have “affordable luxury”. Be retail Heaven on Earth with the finest staff than is even polite to a young broke student. Because someday that student, me, becomes the Doctor who wants to shop there.

I felt unworthy whenever I walked through the NM at the Galleria and I loved that feeling. It gave me drive, ambition and something materialistic to long for when it comes to materialism. Beats having the “desire” to shop Wal-Mart, know what I mean?

Sharper Image was a catalog that made no bones about the superlativeness (and prices) of its goods. I remember the day I saw Sharper Image guy on television with his little girl telling how proud he was to introduce a container that discouraged bacterial growth. He, unfortunately, mentioned the word “silver” in the ad. He was ahead of his time and paid the price.

Back on topic…Google managed to not do the regular ipo process, but I never expect it to happen again.

well..in my part of the world, the grocery chain Haggen, which last year acquired the only Albertsons in my little city, has choked…to be closed this month……which was re-acquired by, you guessed it, Albertsons! They are not reopening said location….sooooo our depressed burg now has TWO sucky Safeway stores……

competition??…..what’s that??

Oh…and did I say that the SEC sucks a big bag of d!cks for their part in all of this malfesence !!

I will just note that during my shopping trips at Haggen, I could sense the apprehension (and perhaps desperation) of the employees working there, while not really knowing how thinks were going to shake out…for the entire year that this whole IPO/Hedgefund scenario played out……

It’s not numbers on a ledger….it’s flesh and blood people — friends, or family. or neighbors……….

I get it. I live in a rural AK town … Walmart closed – we have Safeway, Fred Meyers, (a store recently sold/bought), and (a store recently sold/bought). And that doesn’t include Safeway in the Albertson’s buyout. If you factor that in, Fred Meyer is the only store to not roll over in the past 12 months or so.

Living has been expensive here all along, but it is getting worse, not better. I have no doubt that the new owners will need higher prices than the last.

Our household debt is fading, but costs are going up much more than I like, but thankfully not as fast.

That said, I know many who are going under the bus – on the long time line. I love this place, but it is f**ked I think.

Regards,

Cooter

Did anybody else notice that Slaveway raised prices 20% within a week of being bought out by Albertson’s in January 2015? They’ve had to come up with a lot of cash to pay the interest on all that junk debt.

After a few more grocery chain LBOs, Whole Paycheck might be the grocery chain low-price leader…

Hmmm; 20% price increase simply isn’t going to work given the largest USA grocer is Walmart (25% of market)…and they’ve only been in the grocery business 28 years.

The rest of the guys are simply sucking assets out of also-ran grocers (aka: load ’em up with debt) before the roof caves in.

Depends on local consolidation and competition. Could be workable on specific bases – see my comment up thread.

Ask for details then shop the geographic area and competition.

When our walmart closed we dropped damn near 1500 bucks at 25% to 75% off on closeout/clearance and most of it was dry good or freezer good stuff. Saving a lot a the store lately!

Regards,

Cooter

So these companies like KKR for instance can take something off the market, load it with a debt pill too large to swallow but hidden somehow, paint it with lipstick I guess, then IPO it for foolish consumption?

So what’s the logical choice to front-run these nefarious goings-on, buy KKR instead?

I mean, do even the investors get confused on how all this money shifting goes around and around? I am just a simple person making a simple income. My motto is if I dont understand what I am putting my money into then i dont put it in. I could never see myself investing in the stock market except for my pension which I do not control. Is it true that making investing and the stock market as confusing as possible the ultimate goal?

“Is it true that making investing and the stock market as confusing as possible the ultimate goal?”

No. The ultimate goal is to maximize the ROI generated by your confusion.

Lol!!! Thank you for that confirmation.

To be clear, most professionals in the investment space are paid a “vig” (google it) to make a deal.

They don’t care what deal, as long as they have a deal. Not unlike car sales (or any sales). There are many, many layers of really fancy sounding BS, certifications, industry groups, etc, but it is all a big game of skimming. But they don’t really DO anything but skim.

Learn to grow a garden instead.

The best part (after the tomatoes, onions, peppers … well) is when you tell your investment guy you blew all your free cash flow on a garden … watch him blow a gasket … and if your personality allows, throw some fuel on the fire.

It is best if you talk it up in front of other clients so they show interest.

If you can get that far, you can f**king IPO http://www.MyGarden.com and make billions!

F**k em. And yes it is more or less that simple.

Regards,

Cooter

What I look for in an IPO is scalability.

What I look for (in priority sequence):

(1) credible management team

(2) credible product & business pan

(3) something approaching profitability

Scalability is a tiny subset of “business plan”

Scalability of losses?

Regards,

Cooter