And it’s not just oil & gas!

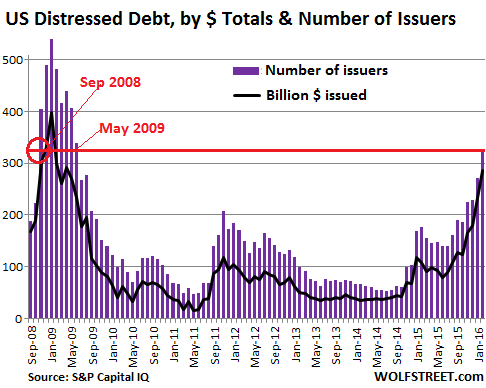

The toxic pile of distressed corporate debt in the US grew to $285 billion in January, up 22% from a month ago and up 162% from a year ago, according to S&P Capital IQ. The number of distressed issuers ballooned to 324 US corporations, up 20% from a month ago and up 84% from a year ago.

The last time the total amounts of distressed debt and the number of distressed issuers had shot up to these levels was in October 2008, just after Lehman Brothers had filed for bankruptcy.

That’s how bad it is now in the US. It’s the essential consequence of years of artificially easy credit, the Fed-inspired blind confidence of yield-desperate investors, ludicrous corporate risk-taking to take advantage of those blind investors, private-equity asset stripping and buyouts, and among other things, the collapse of commodity prices that resulted from overproduction.

During the Financial Crisis, the total amount of distressed US corporate debt maxed out at $398 billion in December 2008 and then began to drop as the Fed was dousing the land with QE and started manually bailing out corporations and banks with emergency loans. Today, there are no bailouts in sight, and no one is talking about an emergency. So the distressed debt of $285 billion today is just the beginning.

These “distressed” credits are junk-rated bonds whose yields are at least 10 percentage points above US Treasury yields, according to S&P Capital IQ’s Distressed Debt Monitor. And this is what the trend in distressed debt looks like, in terms of dollar amounts (in billions, black line) and the number of distressed issuers (purple columns – purple to give them a lugubrious nuance):

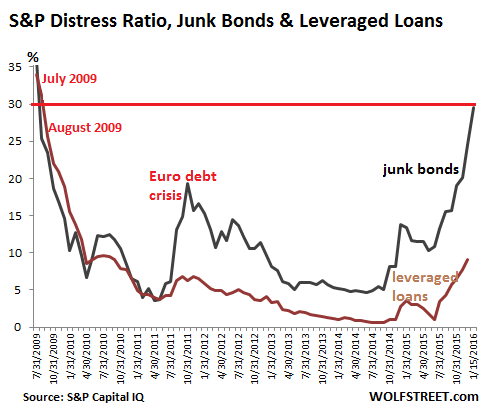

And so Standard & Poor’s US Distress Ratio for bonds soared to 29.6% in January, up from 24.5% in December, and more than double its level a year ago (13.4%).

“The ratio indicates the level of risk the market has priced into the bonds,” explains S&P Capital IQ’s Distressed Debt Monitor. “A rising distress ratio reflects an increased need for capital and is typically a precursor to more defaults when accompanied by a severe and sustained market disruption.”

In September 2008, as the Lehman Moment was evolving, the Distress Ratio was still 28.9%, below today’s level. A month later, in October, it soared to 53.5% on its way to 70%. It took until August 2009, and lots of QE and bailouts, before the Distress Ratio fell below today’s level.

The chart below shows the Phoenix-like rise of the Distress Ratio of junk bonds (blue line) and the S&P/LSTA Leveraged Loan Index distress ratio (brown line), which lags a month, jumping from 7.8% in November to 9.1% in December:

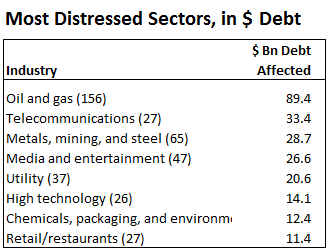

The number of distressed issues jumped 20% from December to 524 in January. Oil & gas accounted for 156 distressed issues, or 30%. With $89.4 billion in distressed debt, it accounted for 31% of the total amount of distressed debt.

It’s convenient to blame oil & gas for the tremors in the junk bond market. But the remaining 70% of the distressed issuers are spread across other sectors – the “spillover effect to the broader speculative-grade spectrum.” It’s no longer just oil & gas!

In terms of dollars, the sector with the second most distressed debt is Telecommunications with $33.4 billion in distressed debt. Metals, Mining, and Steel is in third place ($28.7 billion), followed by Media and Entertainment ($26.6 billion).

The table shows the biggest debt-sinner sectors, in order of the amount of distressed debt. In parenthesis is the number of distressed issues:

So which are the companies in each sector with the most distressed debt?

Oil & Gas: Linn Energy with $6.9 billion in distressed debt; Chesapeake with $6.4 billion; Transocean with $5.0 billion, and California Resources with $5.0 billion.

Telecommunications: Sprint Corp with $10.5 billion, Sprint communications with $6.1 billion, and Sprint Capital with $4.2 billion for a combined total of a juicy $20.8 billion in distressed debt, worse than the top three energy debt-sinners combined! Then there’s Frontier Communications with $5.6 billion in distressed debt. And Windstream with $3.5 billion.

Metals, Mining, and Steel: Peabody Energy (coal mining) with $4.8 billion in distressed debt, Cliffs Natural Resources (iron ore) with $2.9 billion, and US Steel with $2.6 billion.

Media and Entertainment: iHeart Communications with $8.7 billion in distressed debt, Scientific Games International with $3.0 billion, Clear Channel with $2.2 billion.

So what can bondholders expect? Not much. The report:

About 72% of the distressed issues are either unsecured or subordinated. In a default, these noteholders’ claims to the firm’s assets are secondary to the more senior debtholders’.

Distressed issues are the weakest of the speculative-grade population. Therefore, their recovery prospects are low.

Of the distressed issues with available recovery ratings, 33% sport the lowest S&P recovery rating of “6.” In case of a bankruptcy, the expected recovery of principal and pre-petition interest is 0% to 10%. Another 16% of the distressed issues have a recovery rating of “5” with an expected recovery of 10% to 20%.

What we’re witnessing is not only the end of the credit cycle, but also the festering consequences of a majestic central-bank engineered credit bubble. Cheap and easy money paved the way. For highly-leveraged corporate borrowers, those were the best times ever. Investors were blind to risks. They’d buy anything. And Wall Street knew it. And so risks were no longer priced in. But that has changed. Some risks are starting to be priced in. And creditors are finding out that they’ve been taken to the cleaners.

And how are banks that lent to the oil & gas sector dealing with it? “All of it is in the gutter.” Read… Banks Much Deeper in the Hole on Oil & Gas Collateral than they Pretend

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

This leads me to wonder what the CDS market looks like. Are the monolines still offering insurance on this junk?

Well there won’t be no government owned bailed out AIG this time to pay the banksters. Alas – who are the counterparties on the hooks for billions of losses and what will happen if there is another Lehman/BS moments?

And Hank Paulson the ex-Government Sucks buffoon will once again demand TARP II arguing TARP I saved the global banking system.

So banksters’ profits are privatized (juicy year end bonuses too) while losses are socialized borne by the taxpayers. When will this country revolt against the politicians and their bankster handlers?

PS – HELLary made cool $675k in speaking fees from Government Sucks and this came from uber liberal bankster friendly NYT.

TARP II was QE2. You know that, right? there was also a QE3, and very soon we’ll have QE4.

It isn’t just corporate bonds.

A lot of preferred stocks and exchange traded debt issues related to energy, ocean shipping or real estate are circling the drain as well. See Yuma Energy, Star Bulk Carriers or Arlington Asset Investment for examples.

Most preferred stocks and exchange traded debt issues have a par value of $25 – so it’s easy to see which of these companies are in trouble just by looking at how far below that $25 par they are trading.

My guess is that as the next crisis unfolds, there will be some notable bankruptcies in the sectors mentioned above.

After that, I think we will begin to see elevated distress in the municipal sector – City of Chicago and Chicago School Board municipal issues are the most likely candidates. And of course, without some kind of relief from the Feds, Puerto Rico is toast.

To paraphrase the Bette Davis line in the movie All About Eve, “Fasten your seat belts; it’s going to be a bumpy ride.”

If I was a business owner right now, pretty much any kind of business, I’d be selling ASAP.

There will be no bailout, no QE, no fix this time around. And anytime thinking it won’t affect them because “XYZ reason” is in for a big surprise.

Credit markets will freeze up and when that happens nothing will move, period.

All thanks to a system based on debt and credit.

ad infinitum,

…”Debts have continued to build up over the last eight years and they have reached such levels in every part of the world that they have become a potent cause for mischief…It will become obvious in the next recession that many of these debts will never be serviced or repaid, and this will be uncomfortable for a lot of people who think they own assets that are worth something. – William White, former BIS chief economist “…

Are you wearing a bathing suit? You know when the tide goes out…!

Cheers.

“You know when the tide goes out…!”

If it is as big a tsunami as I think it will be, you may not be seen naked but that won’t keep you from being dead when that 500′ mountain of water comes sweeping back in.

And I have no ideas as to how to get to high ground either. Utilities, transportation, communications, energy and who knows what else all overly leveraged.

Here you go…check the color! Hint, hint. The lady is nice too.

http://www.amazon.com/Monokini-Metallic-Swimsuit-Plunging-Neckline/dp/B012E5Z1FW/ref=sr_1_20?s=apparel&ie=UTF8&qid=1453994621&sr=1-20&nodeID=1046622&refinements=p_n_size_browse-vebin%3A2343353011

Lugubrious Wolf?

Bravo.

I’m an independent oil guy Wolf and the unholy alliance of Wall Street and the shale guys is killing us man.

In the future, any observations on shale oil production declines would be greatly appreciated. They’re operating as if they have an unlimited source of funding and drilling new wells in this market?

Many thanks for the website compadre.

Per my read, the whole “glut” is US Shale oil driven by ZIRP/QE policies. The money HAD to find a place to go and the oil patch was smart enough to craft business plans to attract the capital – they just never had a chance to make money.

Robert Rapier had a post late last year on BP’s Stats Review that showed global product was flat-ish, but US production ramped like mad over the same few years, so global production, without ZIRP/QE would have “caught down” to demand and not burned the F**KING HOUSE DOWN. Instead, the wise morons at the Fed invested in overcapacity – a sure fire way to resurrect a dead/dying economy – or is that how the zombie apocalypse starts – I forget.

If they turn the spigots back on, it will just flow to SOMEWHERE and do just as much (or more) damage.

The world is awash in overcapacity – the free money has to stop – interest rates need to find their place in this chaos – and someone will survive it and grow on the other side – let’s just hope govvy doesn’t pick those winners.

Regards,

Cooter

My thinking is always evolving … and I really like the community and quality of comments here, which is why I visit and contribute often … and with that notion here is an almost 2 year old post I did on this subject without the benefit of watching the future blow up in real time. Judge for yourself with respect to time and content:

http://www.zerohedge.com/news/2014-07-14/150-years-real-oil-prices#comment-4957574

I specifically linked to RR’s article on US oil production (that I cited above). The specific bit I intended to quote is thus (at the time of original posting – almost 1.5 years ago). From RR’s article:

“Just to put the current US oil boom into further perspective, over the past five years global oil production has increased by 3.85 million bpd. During that same time span, US production increased by 3.22 million bpd — 83.6 percent of the total global increase. Had the US shale oil boom never happened and US production continued to decline as it had for nearly 40 years prior to 2008, the global price of oil might easily be at $150 to $200 a barrel by now. Without those additional barrels on the market from (primarily) North Dakota and Texas, the price of crude would have risen until supply and demand were in balance.”

So, a bit of crow pie for me. I will have to go dig, but I recall looking at this along the way and seeing flat-ish global production curve with the huge ramp in US production (all shale). To be clear, I recall global NON-US production was down about 3 MBBL while US production was up 3 MBBL (where the US production was uneconomic, free money finding a hole in which to die as we are now seeing). RR is saying global is up by the net gain in US production, if I read it right, so supply and demand both went up, according to RR, but supply outstripped demand and now demand is cratering (e.g. price collapse and huge inventory builds).

Please factor this into my supply-demand argument from the previous Wolf thread on the subject. US frack oil HAS TO COME OFF THE MARKET to balance global markets, but we have a global recession setting in (not counting mounting storage) so the goal post for balancing the two is heading for deeper water.

MAKE NOTE: More QE/ZIRP and protection of banks with bad energy loans is going to make the PAIN a lot WORSE (if you are anyone but the bank with the bad loan).

I don’t pretend to be perfect or get all the details right – but I feel pretty good about what I wrote 1.5 years ago on the subject. I found this attempting to source the actual link to the article I remember reading.

If you are really bored, one can always search, via google, only the contnet on a specific website for phrases by using “site:zerohedge.com” and then whatever you are looking for … so give “site:zerohedge.com crazycooter” a go and hopefully that keeps y’all busy for a few weeks until I am back in the US.

I found this article, which I recall posting to ZH, by googling “site:zerohedge.com crazycooter energytrendsinsider” and it was right at the top.

I am still packing and getting ready to travel soon, so I can’t dig further, but I hope this provides a bit of additional color to my comments here on WS.

Regards,

Cooter

HR: Retired conventional guy here. Been telling folks the shale promise defied economics, geology and engineering. Even the lease signing bonuses were whacked. The hype was too strong. No one wants to listen to the guy who points out the Emperor’s new garments don’t exist. Before I retired in 2010, we were good with $60-70 bbl for Gulf Coast prospects (Smackover/Norphlet), $60 bbl on in-field wells. So, no I couldn’t make the numbers for most shale plays work. Best of luck to you and turn to the right when you can.

What is your take on secondary recovery in shale reservoirs?

I don’t know about the secondary recovery methods. I only know what I’ve read about the whole shale deal really. I do know they brag about the results and then don’t publish actual figures to back up the claims. I also know that their quarterly balance sheets are some of the most horrible things that I’ve ever seen. This whole financialization of everything is a disaster. It’s as if the big bankers move from one industry to another destroying everything they touch in an effort to carve out an income for themselves. And they’re immune from any laws and prosecutions. They steal fifty billion and pay a five billion dollar fine. Then they look for the next score.

I also know that this isn’t going to end well. The obvious double standards that are flaunted in this country undermine the core of everything. The massive debts of all the governments will cause the current system to collapse.

Yeah, have a happy Thursday. I have to go help repair some tanks because I need the storage. Nothing like a twenty thousand gallon tank full of oil that springs a leak.

…secondary recovery for Chinese and Russian oil companies? I doubt if you’ll be able to invest in them except as slave labor. Maybe you’ll get a bowl of rice at the end of each day. Doubt it, though.

Don’t worry, oil investments are “asset backed,” you know, like subprime was.

To say nothing of the private equity loan sector, or the “shadow banking” that has taken place on a company-to-company basis. As in a peer-to-peer loan obligation in search of some positive yield.

There is no way of judging just how big this sector is, or just how much in total the loan obligations are. This hidden from view financial time bomb has the potential to set the dominoes into motion.

The PE lending/shadow banking presence is big in the low income world. We had a car loan funded by PE money and charging 24%. I know it’s crazy but we needed a car at the time. Now they are pushing credit cards from no name banks with low credit lines and 29% interest rates.

good list. very useful. 20b for sprint, huh?

wasn’t son on top of the world a little while ago?

softbank-yahoo-alibaba. hmmmmmm.

China just forbid banks etc to buy US Treasury Bonds and the government is selling them like Hell.

Junk bonds, debts leveraged to hilt, pending defaults and maybe collaterals pledged multiple times (i.e, China), and bowl of derivatives spaghetti – what can go wrong?

Alas the banksters will deny, extend and pretend on defaulted loans and play hide the weenie galore on non-performing loans.

Debt is either paid off or defaulted and kicking the non-performing debt can down the road is akin to inevitable default.

More QE? Why not. The Fed provides a do-over for the most fouled up debt markets and the govt. Is there a level at which the Feds imbalance sheet is too big?

Debt destruction is the major factor to deflation and they know it. A situation , I believe, they find intolerable. They’re essentially giving debt jubilee to special sectors of the economy in order to keep the debt economy rolling. Imagine the price of most things without the ability to borrow money to purchase them…expand or start a business, etc…

That’s why we are going back to 1980 prices. Since all the job creation in this country is based on $15 wages and cash will be king…….

Everything since Reagan and his asterisk economics (guns and butter and no corporate taxes) all is debt inflation and financialization/rehypothecation, there is no price discovery.

Top it with hyper-efficiencies from robotics, we have pulled demand forward not from just the next decade, but the next quarter century…..

Looks like the next crash will take us back to 1980,… if not 1580…..

except if we go feral, those glowing fires in the distance, will be the big cities…..

And those nuclear volcanoes

This site has overtaken Zero Hedge for quality content. Well done!

All that I can say after reading stuff like this is BWAHAHAHA, see you later, Chumps!! You all get what you deserve when you decide to play in the game of unjust weights and measures! You get involved in a scam of trying to get over on others, and you wind up getting burned too! You get played by the REAL confidence men of the world and you wind up losing nearly everything that you worked so hard for all of your life! Get a clue sometime and learn the REAL lesson being taught here, that ONLY the ones who run the game ever get to win at it, just like the scam Three Card Monte or the pea and shell game. The shills in the crowd make it look like someone is winning, but they are in on the scam too! I have been trying to teach people this important life lesson since 1996, but have yet to meet an apt pupil who will also divorce themselves from the system and cut their losses while they still can.

good write-up, wolf.