The toxic miasma of “distressed debt.”

It’s getting tougher out there for our QE and ZIRP-coddled corporate junk-bond heroes.

Unisys, whose revenues and profits decline year after year and whose stock dropped from over $400 a share during the prior tech bubble to $13 a share now, withdrew its offer to sell $350 million of bonds on Friday.

The “current terms and conditions available in the market were not attractive for the company to move forward,” it said. According to S&P Capital IQ’s LCD, the five-year senior secured notes due in 2020, rated BB/Ba2, had been guided at around 8%. But buyers were leery, and they demanded more yield. They wanted to be rewarded just a little more for the substantial risk they were taking. So the notes failed to price, and Unisys withdrew the offering.

Unisys isn’t an oil company, or a mining company, or a coal company – sectors that have been eviscerated by the commodities rout and are having trouble issuing any debt at all. Unisys is a tech company.

But Unisys wasn’t the only one: It was the 15th bond offering withdrawn so far this year, according to LCD, though two of them – Fortescue Metals and Presidio – were able to pull them off later. In total, nearly $4 billion in bond offerings were withdrawn this year.

Olin Corp., which manufactures chlor-alkali products, wasn’t that lucky. It had to have the money to fund its acquisition of the chlorine products business of Dow Chemical. Its $1.5 billion offering came in two tranches: eight-year notes and 10-year notes, guided around 6.5% and 6.75% respectively. But investors sniffed at them and lost their appetite. LCD reported on Thursday that they were pushing for yields “in the mid-to-high 7% range.”

But that wasn’t enough either. On Friday, Olin ended up selling $1.22 billion of bonds, with the eight-year notes priced to yield 9.75% and the 10-year notes 10%.

In the energy sector, the bond devastation is even worse.

California Resources – Occidental Petroleum’s spinoff of its oil-and-gas assets in California, a masterpiece of Wall Street engineering – has done nothing but burn investors in its 10 months as an independent company. When I last wrote about it ten days ago, its $2.25 billion of 6% notes due 2024, issued at par to QE-drunk investors in September last year, had plunged to 66 cents on the dollar. Now they’re at 59.5 cents on the dollar [read… A Spinoff Goes to Heck, after Just 10 Months].

Chesapeake Energy, the second largest natural gas driller in the US, is also facing the music. Two of its brethren, Quicksilver Resources and Samson Resources, have already filed for bankruptcy. When I last wrote about Chesapeake a month ago, its $1.1 billion of 5.75% notes due 2023 – that in June 2014 had been at 112 cents on the dollar – had plummeted to 70. Now they’re at 67 [read… Whose Capital Is Getting Destroyed in US Natural Gas?].

Oil and gas producer Halcon Resources, which has been demolishing its investors via serial debt exchanges that are becoming the model for distressed companies, saw its 8.875% notes due 2021 drop to 33.5 cents on the dollar. And darling Linn Energy saw its 6.5% notes due 2021 collapse to 23 cents on the dollar.

They’re in the toxic miasma of “distressed debt,” bonds that are deemed to be in so much trouble that their yields have soared to where the spread between their yields and the yield of US Treasuries has hit or surpassed 10 percentage points.

Standard & Poor’s, which tracks the “distress ratio” it its Distressed Debt Monitor, announced on September 24, that the distress ratio, after rising since late last year, hit 15.7%, the worst level since December 2011.

Oil and gas accounted for 95 of the 270 bonds in that elite club and sported the second-worst sector distress ratio of 41.9%. The metals, mining, and steel sector, with 47 bonds in the club, had the worst sector distress ratio of 53.4%. Rising distress levels are a leading indicator for defaults. And defaults have already been creeping up.

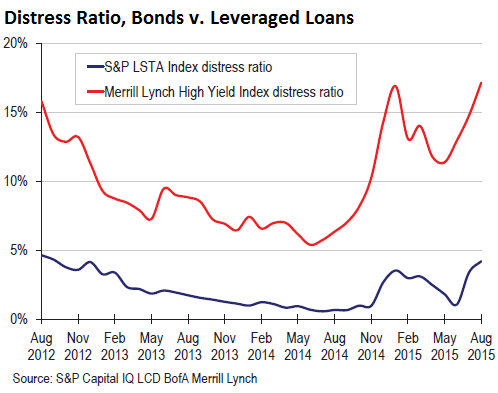

This chart from LCD HY Weekly shows the distress ratio of leveraged loans as measured by S&P Capital IQ LCD (blue line) and of junk bonds as measured by BofA Merrill Lynch (red line) which depicts reality in an even harsher light than Standard and Poor’s. Leveraged loans are generally secured and hold up better in a bankruptcy than bonds. But distress levels of both have recently begun to spike:

These yields that are rising to distressed levels drive up the spread between corporate bond yields and US Treasury yields. The spread is a measure of perceived risk. It had dropped to ludicrously low levels. This wasn’t a function of risk somehow disappearing from Planet Earth. It was a function of the Fed’s beating investors into submission with its zero-interest-rate policy so that they would eliminate risk as a factor being priced into their calculus. Now risk is re-inserting itself into the calculus. And look what happened.

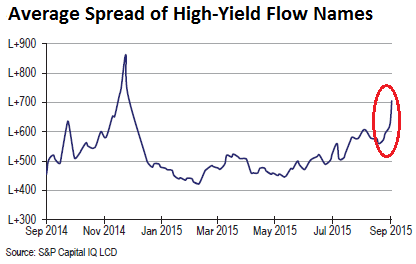

Investors are suddenly discovering an idea – the very one the Fed in its infinite wisdom has beaten out them: they want to be compensated at least a tiny bit for taking on huge risks. And now spreads have begun tentative efforts to spike, “tentative” because history shows that they can blow through the roof:

The chart by S&P Capital IQ LCD is based on LCD’s “high-yield flow names,” junk-rated companies whose bond issues are large and frequently traded. They include in alphabetical order: California Resources, Charter Communications, Chrysler, Community Health… and so on, all the way down to Sprint and Valeant Pharmaceuticals.

Rising spreads make raising money more expensive to get, and for the biggest sinners – the very companies that must get new money or fail – impossible to get. Investors will try to stay out of harm’s way. In this manner, spiking spreads lead to rising distress, and rising distress leads to rising defaults. And that’s when these bonds go kaboom.

But the $40-trillion US bond market is not an entity by itself. Many of these companies are publicly traded, and stockholders are at the low end of the capital totem pole. Even the lowliest, most kicked-around unsecured bondholders come ahead of them. That’s how problems in bond land tear into stocks. To get an idea where Chesapeake’s and Olin’s stocks are headed, watch their bonds.

These rising spreads – regardless of what the Fed will do in terms of flip-flopping on interest rates – is a very bearish signal for stocks. But according to our soothsayers, there should have been a big rally. Read… What the Heck’s Happening to the Global Stock Markets?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Completely agree with premise of article. Great supporting data, thanks Wolf! I track the ratio of HYG / TLT to get a real time approximation of this distress. It really tanked on 8/24 and started looking ugly again on Friday. Anyone know of a better way to track this measure intraday?

When McClendon was CEO:

“Persistent investigative reporters at Reuters traced a chain of shell (fake) companies in Michigan — companies which are now rejecting 97% of the gas drilling leases they signed with hundreds of farmers, many elderly — back to Chesapeake Energy corporation and its CEO, billionaire Aubrey McClendon.”

“The Republican State Leadership Committee, a newly-formed PAC that raised more than $9 million over the previous three years – the bulk of it from corporations, prohibited by state law from contributing to Pennsylvania candidates – said that most of the Corbett money came from McClendon, who had donated $450,000 to the RSLC in separate donations, around the date it was sending money to Corbett. As of last month, Chesapeake had obtained 839 Marcellus drilling permits in Pennsylvania, more than any other company, and had drilled at 126 sites, making it the second-biggest operator after Talisman Energy of Alberta, Canada, according to the state’s Department of Environmental Protection”

Flash forward to 2015:

“Fadel Gheit of Oppenheimer suggested that Chesapeake Energy will report losses of $544 million this year, only to worsen to $833 million next year. In addition, the company is expected to realize a free cash flow deficit of $2.1 billion this year and $2.7 billion next year.”

“”Shares of Chesapeake Energy have the third largest short interest among all companies in the S&P 500.”

And now McClendon is taking his questionable practices to Mexico. I am sure it will all work out just fine. Unless of course, he crosses the wrong people. And if he does, they usually don’t spend a lot of time and legal fees to get satisfaction. A more direct approach is often employed.

Here’s how it plays out for these distressed zombie companies.

First, there will be an ongoing series of desperate attempts, such as mass layoffs and capex cancellations, to try to keep the zombie alive. Next, the zombie puts itself up for sale in a last ditch effort to stay alive. When that fails, the bonds and stock of the zombie company go kaboom. The final step is when the vultures swoop in to pick up any of the zombie’s remaining assets at fire sale prices, usually at 1 to 8 cents on the dollar.

Everyone already knows that I think this so-called ‘economic recovery’ is an abject fraud. There are over 9 million more people in the US living in poverty than there were in 2007. That’s not the definition of economic recovery. Rather, it’s a cruel hoax.

It would be really interesting if it were possible to conduct a study to determine the true extent of unproductive economic activity that is enabled as a result of QE and ZIRP. Unfortunately, it’s not possible.

I suspect but can’t demonstrate that, if and when ZIRP is finally ended, a huge chunk of unproductive economic activity will quickly disappear, such as the zombie businesses Wolf has listed, plunging the US and the world economy into outright economic depression.

VB, I appreciate your analyses and I believe, on this one, you are spot on. May be a squadron of black swans heading in and little we regular folks can do about it. It is also proper to use the collective noun “lamentation of swans”. Lamentations will certainly abound across the land.

NT

Just take a look at the mansions on Long Island if you want to see unproductive economic activity coming out of Wall St. One hundred million dollar plus apartments in New York City. No one in their right mind would make these kinds of purchases except people who have money to burn.

What credit giveth, credit taketh away.

Stay safe! Stay liquid!

Regards,

Cooter

We now know about the famous VW computer program algorithm that sweeps away any undesirable results which an official analyzing unit is supposed to look for.

Obviously this algorithm can be used for any statistical situation.

I was surprised to see that Chrysler’s bonds were junk rated. The quick look I took at the S&P rundown didn’t seem too negative- I guess they don’t use the word ‘junk’

Does this mean that a pension fund can’t have Chryco bonds?

Re: Olin. This sounds like their bonds might be a buy- they had to have the money, true but they’re buying ie eliminating a competitor. I would have thought that this was not an easy business to get into and even I have heard of them.

I was surprised to see that Chrysler’s bonds were junk rated. The quick look I took at the S&P rundown didn’t seem too negative- I guess they don’t use the word ‘junk’

Does this mean that a pension fund can’t have Chryco bonds?

Re: Olin. This sounds like their bonds might be a buy- they had to have the money, true but they’re buying ie eliminating a competitor. I would have thought that this was not an easy business to get into and even I have heard of them.

Olin is caught up in the commodities rout. They’re now praying for higher prices but might not get them soon enough.

I haven’t seen Unisys mentioned anywhere for twenty years and I’m a techie. A blast from the past for sure. They are still probably supporting systems installed decades ago, a scary thought.

I had the same reaction… I remember the name, and the logo, but can’t remember what the hell they ever did!

They are a merger of two big mainframe companies, Sperry and Burroughs, that had a big installed base in banking and govt. What is scary is that the govt machines are probably still running.

I worked on a project at an auto insurance company (the third assigned to the project – the previous two employees quit and their projects scrapped – I was the first to succeed) which involved building a web site backed by a mainframe. The business problem was that the insurance company, their actuaries, etc, had *EVERYTHING* on mainframe and their competition was selling policies via online pricing tools. They had to be in the game.

Earlier attempts involved duplicating mainframe logic in .NET which sort of worked, but had discrepancies (i.e. folks bought based on one price and got another – creating arbitrage opportunities for agents/re-sellers and lower revenue/increased risk).

The only solution was to have a single rating engine/etc, which I implemented by mimicking a COBOL data structure in memory, wrapping it in .NET, and mapping the data in/out to the website (and rebuilding their website so it worked). All I ever sent to the mainframe was the copybook and a request to perform an operation. The data structure was 100+k and the mainframe was IBM Z series IIRC.

I got thrown under the bus by incompetent management, despite a total and complete homerun. Very common in my experience (failure is someone else’s fault / success is their work). I literally got in shouting matches with my manager despite my success as they needed to keep up appearances and expected me to play along. No opportunity there (and their health insurance was UNGODLY expensive – in ~2006).

My point is, many, many companies just can’t afford to walk away from the decades of capital spent on their processes/formulates/engines/etc because migrations to new technology DO NOT WORK.

To this day I do NOT advocate any company migrating technology unless they do it because their vendor is literally out of business (e.g. DEC) and there is no other choice. It is expensive, very high risk, and the last, last last option.

So, these companies will milk it … but everyone wants to be on “the cloud” these days, so everything old is new again. :-)

Regards,

Cooter

The 10 year T is at ~2% and these bonds are getting sketchy. Hunker down mode may be the trend for awhile.

Thanks, Wolf, great commentary