“For more than 30 years, consistently falling mortgage interest rates have helped spur more home sales. But in about a year’s time, that decades-long tailwind will likely shift to a housing headwind.” Sales will be hit hard, according to a worried analysis from Zillow.

But not yet.

Home sales have been hot, by post-Financial Crisis standards. According to the National Association of Realtors, sales of new homes rose to a seasonally adjusted annual rate of 546,000 in May, fastest pace since February 2008. The pending home sales index hit the highest level since April 2006. Existing home sales rose 9.2% from a year ago to a seasonally adjusted annual rate of 5.35 million, the fastest pace since November 2009. And the median price of existing homes jumped 7.9% to $228,700, the highest since 2006.

The median home price had hit the all-time crazy peak of $230,000 in 2006, during the insane Housing Bubble that had such dramatic consequences when it imploded. So in May, the median price was almost back where it had been during that all-time crazy peak in 2006. Just $1,300 off! Surely in June, the record will fall and a series of new all-time crazy records will be set. In a number of cities, insane records are already being set month after month, but no way that this is a housing bubble this time [read… San Francisco vs America in Housing Bubble 2].

There is nothing like a big bubble to perk up everyone’s mood. The whole industry is drooling. “It’s been a booming year for mortgage origination growth,” Equifax reported breathlessly on Monday:

Total mortgage origination balances jumped 74% year-over-year in the first quarter to $466 billion. Of them:

- First-lien mortgage balances soared 80% to $430 billion; the number of mortgages originated in Q1 jumped 55% to 1.78 million; and average loan amounts rose 12% to $232,547.

- Home equity lines of credit (HELOCs) rose 30% to $31 billion, with new accounts up 21% to 285,700, the highest since 2008; the average credit limit rose 9% in March to $108,533.

- New home equity installment loans rose 14% to $5.0 billion; new loans originated in Q1 jumped 20% to more than 142,800.

These are a huge increases.

And there’s a reason for this: mortgage rates have been near historic lows but are scheduled to rise, and now a buyer’s panic has broken out. People are desperately trying to grab the cheap mortgage rates while they’re still available and buy a home, no matter what the price.

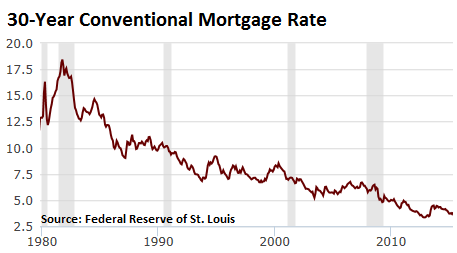

For over three decades, mortgage rates have declined, with some mini-surges in between. It boosted sales and inflated home prices. It’s been a long fun party with a disconcerting interlude back to reality. And most potential homebuyers today have only experienced rates going down:

But as the Fed approaches “liftoff,” possibly as soon as this September, “we are approaching the beginning of the end of the era of falling mortgage rates, and entering a period in which rates are likely to rise over the next several years,” Zillow said in an analysis. This is when “that decades-long tailwind will likely shift to a housing headwind.”

Rising mortgage rates would begin to be a “drag” on sales by mid-2016, Zillow figured. By 2018, it could drag down sales of existing homes by about 7% “from current levels.”

Given the recent average of the seasonally adjusted annual rate of 5.1 million home sales, a 7% drop would mean 350,000 fewer sales for the year, which would push the seasonally adjusted rate down to 4.75 million homes by 2018. A big step down from May’s seasonally adjusted rate of 5.35 million in home sales. Bye-bye long-term housing boom.

The analysis assumed that the 30-year fixed mortgage rate would reach 4.63% by December 2015, 5.63% by December 2016, 6.88% by December 2017, and 7.75% by December 2018. It also assumed a household formation rate of 1% per year, which is more optimistic than what we’ve seen in much of the post-Financial-Crisis era.

And there’s a particularly troubling problem with rising mortgage rates:

But for homeowners currently locked in at a low rate, rising mortgage rates could represent a budgetary curveball should they decide to buy another home in coming years. Homeowners used to a certain monthly mortgage payment may balk at paying a higher amount per month in financing costs for a home roughly comparable to their current residence, to say nothing of a home that is more expensive.

In this way, higher mortgage rates – and higher prices! – make it more difficult if not impossible for households to move to different home, which cuts housing turnover and sales and puts downward pressure on prices: the “mortgage rate lock-in” phenomenon, as it’s called.

“For decades, homeowners haven’t had to worry about that,” the analysis warns. “By this time next year, they’ll need to start.”

This is another success of the current monetary policies, and the no-holds-barred credit boom they have engendered. They’ve led to a convoluted and precarious situation where nearly all assets, including homes, are overpriced, and not just by a little. It will unwind, as these things always do over time, and for many people, a home will once again become an expense rather than that wealth-producing asset that they were promised it would be.

But the market faces another problem. Turns out, to the greatest consternation of some folks on Wall Street, millennials are smart. Read… Wall Street Frets about its Nightmare Generation

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wow Zillow said that?

In the mean time we have buffoon NAR economist Yun hyping it all up. I think mortgage rates have been low too long literally crawling the bottom and only way may be ticking up. And one gets to afford smaller house if the rates are higher. I still recall back in the late 70’s the rage in my neighborhood was “assume loan” meaning buyer can potentially assume the seller’s mortgage with much lower interest which I think at that time was like 17%.

I bought my first house at age 24, just after my daughter was born in 1979. I had saved up $7,000.00, and bought a home for $40,000. I promptly watched my mortgage rate rise at renewal time (5 years later) to 19%. My folks and my in-laws did a refi at 10% as they were only getting 8% in savings. Needless to say, the lesson I learned was to never carry mortgage debt and always live within your means. This required me to define what my needs were and develop on honest appreciation of what my ability to pay really was. At that time there were no credit cards and people actually balanced their cheque books and maintained budgets. I made a very modest wage and my wife stayed home with the kids.

When I relocated for a better job the next house was an improvement but still cost just $63,000. That was in 1988. I am just trying to use the memory bank on this, but I probably cleared (net) about $2200/month, and my mortgage payment was around $450/month. In other words, a 20% payment obligation off my net pay.

I mention this personal account only because no one lives this way anymore, it seems…..not families, individuals, or Govt.

Is it still possible to live this way in 2015? Of course it is. We seldom, if ever ate in restaurants. We are both very good cooks and like cooking so why would we? We always drove a shitty car that I kept going and never had a car payment, ever. We had crappy furniture until the kids stopped smearing and having accidents. (neither of us wanted to always be yelling at the kids about messes). What we did have is a nice little view home on 1/2 acre. We always had a great backyard and when the kids hit their teens I put in a nice swimming pool. No debt allows working people to have discretion in their purchases. When I did have a mortgage I remember when I did the last refi at the credit union. I was feeling down about things and asked the loans officer what she thought I was doing wrong? This was around 1990. She said, “are you kidding? Those people up in the new sub-divisons with the boats, trucks, and trailers in the driveways own almost nothing. They owe on everything and if they miss a months work the banks will come and take it all, one toy at a time.” And 25 years later it is even worse.

I now live on 16 acres on a beautiful river. I am retired and have been so for 3 years. My son is thirty and frets the same way I did, although he has a beautiful riverfront home .5 km away from me. His mortgage outstanding is approx. 2 years net pay for him and he plans to pay it off as soon as possible. My daughter also has a nice affordable home which she should have paid for by age 45, at the latest. She, and her husband drive older used cars and vacations are camping with friends at local lakes and rivers.

Neither have granite countertops or hot tubs. If the mortgage rates rise they both will be just fine…and this is in BC, Canada!!

When I was 24 my father-in-law said to me, “if you pay your house off it will be like getting a $1,000 a month pay raise. You will go from being broke to always having cash in your wallet.” I listened to him and my kids have listened to this same wisdom.

Have you seen those Zillow adds on tv? People’s expectations have grown to the point that everyone thinks they deserve tropical winter vacations and big new houses to live in. It is a time for crazy unrealistic people who think they should live like royalty….because they showed up to life. When did life turn into this?

Loved your comments about having old cars, old furniture, getting by, eating at home, etc. My parents did this when I was young and they’re now millionaires, but you’d never know it. My dad still drives a 15 year old truck. House is paid off and most of the rooms are empty because they HATE moving furniture.

They didn’t get to this point in their lives by obsessing over hot tubs and granite counters, fancy vacations, or expensive home furnishings. They got by and appreciated what they did have, instead of always wanting more, more, more as we’re conditioned to do by the media.

i don’t want more and more, i just want a job that provides an income where i can survive in California, sadly that ins’t in the cards.

i bought my first house in 1991 for $176K @9.25% interest…….and i was upside down until 2000..

sadly i still earn the same wages as then and now that home is $500K…(well not that particular house it’s still at about $200K cause no one wants to live in that hood)

HELOC’s up, what possibly go wrong…………..

But its our sweet little house honey.

In thirty years dear.

Pending if I read the article correctly in ZH today is homes that have been contractually signed. Existing means homes that have been sold ? O K I got this. Problem here is the rate last month actually fell over 2 pct for existing homes as contracts have been falling through due to credit being denied and other circumstances such as people losing jobs before settlement which is usually a 3 to 6 month lag. This could be a bad sign for already a bad and anemic housing market that is already cooking the books to begin with

Did millennials suddenly jump into the housing market? Did tons of student debt disappear? Has real income started to significantly rise? Credit card debt per household significantly lower? From whence comes the famously necessary “first time buyers”? And lastly, can the numbers be trusted? Is the mine being salted?

Or does Matt have a point? Could a lot of these sales depend on first timers and sellers wishing to move up (possibly two of those) all being able to get financing? One link in the chain fails and the whole deal falls apart? Color me cynical.

I wouldn’t buy a house today even with a zero interest rate. The houses in Florida are so overpriced and need so much work that it doesn’t make economic sense. The corporate owners have inflated the prices of homes by withholding inventory but the valuations are bad. The house I currently rent was renovated before I rented it and it still needs so much work that the first year’s rent will not cover all the repairs. If I add in the fines against the house the second and third year’s rent won’t cover it either. They value the house at 60% above what I think it is worth. I think this is a very typical rental.

The last house I rented was put on the market and sold in several months but the inspection revealed all the problems and the sold sign is still out front. If the buyers take the house as is, it is a gut job even thought cosmetically it looks ok.

The house I lost to foreclosure had the same problems it was built in 2002 and by the time I lost it it needed a new roof, new AC – two zone, pool resurfacing, and driveway resurfacing. It wasn’t even worth modifying the mortgage because I would have had to add at least 50K to the mortgage I couldn’t afford. The taxes and insurance never went down, they went up. Buyers beware.

Wasn’t the global crash caused by people buying houses they couldn’t afford?

nope, it was caused by mortgage lenders lending people money who had no business getting loans….AND THE LENDERS KNEW IT!!!! BIG difference.

“People are desperately trying to grab the cheap mortgage rates while they’re still available and buy a home, no matter what the price”

and why not? here in California nobody cares what the price is because when the price drops you just stop making payments and get to live in a house payment free for up to 48 months…i HAVE SEEN this happen.

this will ONLY end badly for tax payers and those that (were fucking stupid) played by the rules.

Yes, this will become part of our culture now. Many people are reluctant to tell others they live without paying mortgage payments. But I’ve seen people slip and reveal their no-payment lifestyle. There’s still shame in this practice… for now.

The stock market crash will get us all before the housing bubble. Starting with the Black Monday1987, August of 1990 invasion Iraq invasion of Kuwait market crash, Dot.com market cash 2000 and mortgage and lending financial crisis 2008, these market corrections all occurred in the presidential campaigning year before a new face took over the white house. We are due for our current one any time now. THIS IS THE WAY THE FEDERAL RESERVE HAS TIMED THESE CORRECTIONS THAT USUALLY OCCUR IN A LAST QUARTER! !!