“The market is flooded with oil and everyone is desperate to sell quickly, so you have a price war,” a marine-fuel trader in Singapore, the largest ship refueling hub in the world, told Reuters as prices for bunker fuel oil are plunging.

OPEC, which produces about 40% of global oil supply, announced on June 5 to “maintain” output at 30 million barrels per day for the next six months. Six days later, the IEA’s Oil Market Report for June clarified that “Saudi Arabia, Iraq, and the United Arab Emirates pumped at record monthly rates” in May and boosted OPEC output to 31.3 million barrels per day, the highest since October 2012, and over 1 MMbpd above target for the third month in a row. OPEC will likely continue pumping at this rate “in coming months,” the IEA said.

“We have plenty of crude,” explained Ahmed Al-Subaey, Saudi Aramco’s executive director for marketing while in India to discuss with Indian oil officials supplying additional oil. “You are not going to see any cuts from Saudi Arabia,” he said. Saudi Arabia produced 10.3 MMbpd in May, its highest rate on record.

So forget the long-rumored decline of Saudi oil fields. For Saudi Arabia, it’s a matter of survival. It has cheap oil, and it won’t be pushed into the abyss by high-cost, junk-bond-funded, eternally cash-flow-negative producers in the US. It will defend its market share, and it can do so profitably.

Russia produced 10.71 MMbpd of oil and condensate in May, a hair lower than its post-Soviet record set in January, and within reach of the Soviet record of 11.48 MMbpd set in 1987. Russia is not cutting back either. It needs every foreign-exchange dime it can get. Its oil & gas sector is its economic lifeline.

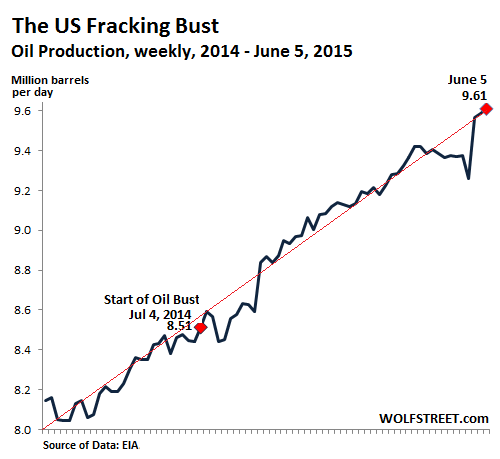

And US oil producers aren’t backing off either. They idled 60% of their drilling rigs, slashed capital expenditures, laid off tens of thousands of workers, and shut some facilities. A number of companies in the oil patch have filed for bankruptcy. But US producers are pumping more oil than before.

Despite wild gyrations in granular production data that might point at a leveling off or even a decline in one or the other oil field, overall US production, based on the weekly estimates by the EIA, soared to 9.61 MMbpd in the week ended June 5. A recent record, and up 13.6% from a year ago! Note the relentless trend line:

With the world’s top three oil producers – Saudi Arabia, the US, and Russia – pumping at record levels and with OPEC producing above target, miracles would have to happen on the demand side to bring this into balance. But miracles are rare these days.

Over the past decade, China has absorbed 48% of the increase in global oil production. But now its economic growth is slowing and its economy is becoming more energy efficient. Demand in the US and Europe is not performing any miracles either. There is some growth: 1.4 MMbpd for 2015, according to the IEA. But not nearly enough to mop up the additional production from OPEC, Russia, and the US – not to speak of Iran when it rejoins the global oil trade.

So OECD crude oil inventories rose another 12.6 million barrels in May, despite the first draws in the US in nine months. According to Bloomberg, supply has exceeded demand for five quarters in a row, the longest glut since the 1997 Asian economic crisis. Eugen Weinberg, head of commodities research at Commerzbank in Frankfurt, put it this way: “Any expectations the oversupply will be gone by 2016 don’t look justified at this stage.”

If demand grows at 1.4 MMbpd in 2015, and if production remains at current levels – two big IFs – global oversupply would still run at 1 MMbpd in the third quarter and at 600,000 bpd in the fourth quarter, which, according to Bloomberg, would be “the eighth consecutive quarterly surplus, exceeding the current record of six quarters from 1997 to 1998.”

It would be the biggest glut in recorded crude-oil history.

But no production increases in the US may be unlikely. US shale producers can’t afford to keep production level. They’re loaded up with debt that is getting more expensive, creditors are getting antsy, cash flows are negative, and so they have to produce more to get more money and stay alive.

And then there’s Iran. Bloomberg:

The glut could swell further if Iran and world powers reach an accord on the Islamic Republic’s nuclear program by their June 30 deadline, Commerzbank predicts. The country could boost exports by 1 million barrels a day within seven months of sanctions being removed, Oil Minister Bijan Namdar Zanganeh said in Vienna on June 3.

If that happens, we’ll be watching the most magnificent oil glut ever building up into next year.

Oil producer Canada is feeling the heat from the oil-price crash, and manufacturing is getting hit hard, but not just because of the oil bust. Read… Manufacturing in Canada Sags, Triggers Chilling References to Financial Crisis

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I expect a black swan instead of a miracle. T. Boone Pickens was recently saying that the Saudis couldn’t increase production. I don’t pay much attention to him because he is always working an angle. How long can the Saudis keep up producing at this rate? Most of us don’t have the data to answer that question. What I do know, and the Saudis know, the OPEC members always cheat on their quotas. Back in the 80s, the Saudis drove oil prices down to regain cartel discipline. This time, it is to their advantage when the other cartel members over produce their quotas. So, let it be.

At this point it’s obvious the Saudi and the Russians are digging in for the long run.

As I expected there has been no slaughter on the shale patch: layoffs, a few companies going bankrupt, but not the burst many announced. Fracking outfits are hanging on.

Two things have allowed them to survive so far.

First are unexpectedly high oil prices: everybody expected oil to stabilize in the $50-55/barrel region. It’s presently over $10 that benchmark and set to go higher short term. I wouldn’t be too surprised if, in face of all reason, it hit $75/barrel before the year is over.

Why? Oil bulls are a strange species: for them prices can only go higher. They may be right long term but they have been bloodied time and time again, often in spectacular fashion (see the 2008-9 burst). You’d expect them to be careful, but they aren’t.

Bulls are also extremely US-centric in their views: they tend to react instantly to news related to US production and consumption but to lag (or even shrug off) news from the rest of the world. This outdated view is what will ultimately do them in: taken together China, Japan and South Korea import and consume far more oil than the US. With the first too busy playing the stock market, the second struggling under Abenomics and the third dealing with a serious blow to her export-driven economy, the news there aren’t good and will continue to be so for quite a while.

But ultimately, oil is just another victim to the broken mechanism of price discovery. Prices these days are completely disconnected from fundamentals. Demand and supply are secondary concerns at best. Commodity prices crater? Retail prices increase! A glut in oil supply? The price at the pump is almost at $100/barrel levels and increasing weekly! That’s similar in nature to the what ultimately did the Soviet Union in.

Second is the crazed bond markets. All these overleveraged fracking outfits have been able to shift billions worth of junk bonds at very favorable rates because investors desperate for a scrap of yield will bid so frantically for it they will end up getting less what they originally looking for.

This may just ensure survival and not growth, but that’s all that matters now. Fracking outfit CEO’s tend to be very bullish and they expect $100/barrel oil to make a rapid comeback. The fact Iraq is pumping like crazy while mired in a bloody civil war may suggest they should be more careful.

The Saudi and the Russians know this all too well. Neither were born yesterday.

They also know 2008 changed absolutely everything: if there’s a Lehman event on the shale patch, Uncle Sam will rush in with armored cars loaded with freshly printed money and battalions of lawyers to bail in fracking outfits and protect them from further problems.

What they are betting on is US outfits will be crushed by their own debt load. One by one. Japan has taught us that, no matter how low the interest rates you pay, once debt reaches a certain size it will swallow a fifth or even a quarter of your cash flow each and every quarter. Interest rates on bonds cannot go lower than they are right now (tip: look at what’s happening in Europe) and fracking outfits are caught between the hammer of having to keep cash flow to service the debt (and hence keep oil prices at present levels) and the anvil of having to cut production to drive prices upward.

Unless Washington comes up with some nefarious scheme, fracking outfits are effectively doomed. And we all know the New Rome’s record in the field of cunning planning is not 100%.

When firms go bankrupt one by one, they tend to pass under the political radar. There may be uproar at local level, but mayors and governors have neither the power nor the resources to rush in with a bailout: most of them rule over cities and States daily flirting with insolvency and they haven’t the advantage of a printing press. The Fed lives in its own little world, far away in New York.

Comments like this is why I enjoy this site. Well thought out and expressed. If indeed the Russians and Saudis have dug in for the long haul, on which I agree, how do you see the “Red Queen” scenario with the shale operators influencing the the market “war” ? It is one thing to pump the heck out of what you already have on-line, but completing existing wells and drilling new ones are capital intensive operations. And given the drawdown curves for the shale wells, they can only pump all out so long before replacing those reserves, if that is what they intend to do, assuming that it is possible to do so. Replacing conventional reserves, of course, is much less costly than the shale plays.

Also assuming no Fed magic beans, how long do you think investors in the shale plays can hold their noses and continue pumping money into these ventures? Not trying to put you on the spot. I am just wondering how the large differential in reserve replacement costs plays into your analysis.

The Saudis will soon be joined by Iran, Pemex, and the US plan to frack off the continental shelf. Oil glut indeed. Now, if only the price of gasoline would go DOWN! I believe it is only a matter of time.

We have just been warned in Australia that the pump price for petrol and diesel is just about to shoot up by 20% due to higher refinery charges form Singapore.

The pump prices will be up to levels as were charged when the price of a barrel was over $110.00

Something screwy here.

http://ourfiniteworld.com/2014/02/25/beginning-of-the-end-oil-companies-cut-back-on-spending/

The glut may be very brief.

Great comment, MC.

Les Francis, our gas price shot up 10 cents litre overnight on Vancouver Island. Crude still around $60 and we have a local refiner in Vancouver…and nearby in Wash State US. What?? I use my MC more than car or truck. New mindset and great weather.

I predict a Black Swan to either crash the economy and Crude demand….or something will amp up big tiome in the Middle East and crude will go through the roof. One or the other…..soon.

Either way, I can’t see any steady state going forward. Things look very volatile. If I had to choose I still think the economic house of cards will collapse. I think it will be very ugly.

Hopefully, they jail Banksters this time around. Or………(I don’t want to get banned from this site so I will leave it at that).

I had heard rumors that “investors” were storing crude oil on tankers to keep the price up. Well, earlier this week, I had occasion to go across the mouth of Chesapeake Bay by boat. I saw a line of tankers stretching to the horizon, and they seemed to be riding fairly low in the water. It was the longest line of them I’ve seen there. Someone must be paying day rates on those vessels. You have to wonder how long they can keep it up.

Nobody knows how much crude -n- condensate (natural gas liquids) the world could take if there was extraction at the rate that existed prior to 1998. Demand is infinite wherever there are TVs and credit money. The world of 2015 bumps along at the threshold of recession, no doubt because of fuel constraints. Necessary ‘efficiency’ is always gained at the expense of GDP because it is a form of rationing.

Look at this another way, the countries and regions with the greatest GDP increase year over year are those with ‘catch up growth’ and stupendous inefficiencies. As these countries waste less, their GDP increase retreats, even becoming negative (most efficient of all).

Efficiency exacts a cost, at some point these exceed what can be gained by users’ borrowing. There are almost zero returns on the use of the fuel which is almost entirely non remunerative waste, for entertainment purposes, only.

Trend extraction would = 110 million barrels per day, instead of current 92 mbpd. Today’s extraction stream is partly conventional crude which peaked in 2005, the rest is non-motor fuels butane, ethane and hexane. A growing, truly inefficient world would be guzzling every bit of 110 mbpd and begging for more: countries such as Nigeria, Iran, Brazil, Indonesia, Republic of South Africa, Argentina, Kenya, etc would be China- analog ‘growth stories’ instead of basket cases.

Basket cases that include Russia, EU, Japan, oil producers such as Venezuela, including newcomers Canada and Australia, etc.

The ‘glut’ story is a public relations campaign intended to obscure the secular shortage that has pushed real costs above the returns that credit can provide to end users.

Make no mistake about it: when firms such as drillers borrow as they are now, their debts outrun their customers’ ability to retire these loans by way of their own borrowing. Every additional day these firms are propped up — either by government bailouts or credit subsidies — advances the date of reckoning, when customers throw in the towel.

I did a double take in Des Moines this morning – the QT had diesel posted 3 cents cheaper than gas. While it used to be the norm, it hasn’t been since the government forced the changeover to ultra low sulphur diesel. Go figure.

Diesel is at a 15-cent discount here in the Dallas area now at some stations, including QT’s. This tells you the demand for diesel is completely collapsing, which means the transportation industry is collapsing, which means the economy’s collapsing is close at hand. Everybody using any form of kerosene ( read: truckers and airlines ) isn’t using as much any more, and the Dow Transports have already confirmed the impending collapse of the economy.

Or… it could be that it’s driving season (which it is), and gas stations jacked up the price of gas way beyond what is warranted by the recent rise in the price of oil. And they did because they could – during driving season. But truckers might be a tougher group to raise prices on than consumers.

And it’s summer: refineries put out a different gasoline mix, varying by region of the US, to lessen smog. Prices go up a tad when the changeover occurs.

That’s certainly the case in California.

Anyone paying attention to the Saudis understand that they know that solar will ULTIMATELY win http://www.bloomberg.com/news/articles/2015-06-03/at-opec-the-saudi-oil-minister-mainly-wants-to-discuss-solar-power and have decided to sell all they can as soon as they can. They realize that not all of those “reserves” that everyone speaks of will ultimately be extracted.

Ohhh, I love the shoot out scene’s!! The best part of, The Good, the Bad, and the Ugly. And if we are being intellectually honest about it, ya know who plays the part of the Ugly.