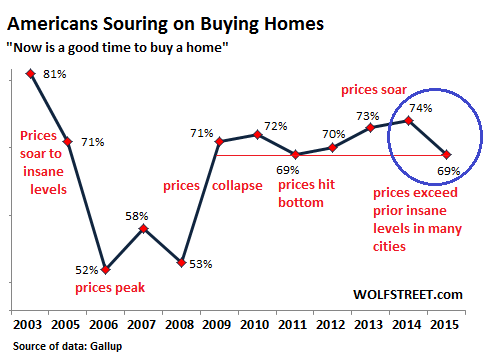

Americans are an optimistic bunch when it comes to homes. Even in April 2006, at the peak of the prior housing bubble, with prices at insanity levels but with sales stalling as the market transitioned to its epic bust, and when everyone was trying to sell, even then 52% of Americans thought it was “a good time to buy a home.” That was the moment of peak pessimism in the history of Gallup’s data series. And it was truly a terrible time to buy a home.

Peak optimism was in April 2003, when 81% thought it was a good time to buy. They were right. The Fed had kicked off the housing bubble. The second most optimistic moment, after a long climb up from peak pessimism in 2006, was in April last year when 74% thought it was a good time to buy. And they too were right. But now the honeymoon appears to be over.

In its annual April survey, Gallup asks: “For people in general, do you think that now is a good time or a bad time to buy a house?”

This time around, rather than climbing toward another peak, optimism has plunged 5 points to 69%, to the same level as in 2011. Only during the last housing bust did optimism fall below this level. It’s the steepest drop since 2008 when the housing market was tearing into the global financial system:

Gallup puts it this way:

The slightly less positive views of home buying may have been influenced by lackluster home sales earlier this year, as many parts of the country experienced unusually cold weather.

OK, let’s blame the weather. But wait….

This winter wasn’t as bad as last year. And the thing is, optimism about buying a home has plunged the most in the West, which includes my beloved and crazy state of California, where the weather has been absolutely gorgeous, sunny, warm, and way too dry for our rainy season – ringing in the fourth year of what might turn into a catastrophic drought. But in the West, optimism has plunged 11 points from 75% last year to 64% this year.

However, in the Midwest, where there actually was some winter, optimism rose 2 points to 75%. In the East, despite the heavy snow in some areas, optimism edged down only 3 points, with 72% thinking it was a good time to buy. So clearly, it wasn’t the weather. It was the West that dragged down the figures.

Then there’s another question in the survey: “Over the next year, do you think that the average price of houses in your area will increase, stay the same, or decrease?”

It’s not like Americans envision the next housing bust: 59% expect home prices to rise, the highest level of optimism since 2006, at the peak of the housing bubble, just as things were coming unglued. And only 11% think home prices will fall, same as in 2006.

At the time – in April 2006, the very moment when the housing bubble was turning into the housing bust – 60% thought home prices would rise, still believing the media and industry hype; 27% thought they would stay the same, having apparently bought into the meme that prices might be plateauing briefly before moving higher. Even as chaos was beginning to tear into the market, only 11% thought home prices would actually fall, same as now. It was this tiny minority that got it right.

The optimism concerning prices was even higher in 2005, when 70% thought prices would rise over the next year. And they were correct!

But the crux is the relationship between optimism about buying a home and optimism about rising prices.

In the West, home prices have skyrocketed from the bottom of the last crash. In many places, including the city of San Francisco, prices now far exceed the peak insanity levels of 2006/2007. And so in this environment, 76% think prices will rise further over the next year, while 17% expect prices to stay the same, and only 6% see declining prices. In terms of home prices, folks in the West are by far the most optimistic in the nation.

Yet, they’re the most pessimistic about this being a good time to buy.

In the East, only 46% think prices will increase! Another 17% think prices will decline, the most negative in the nation. Yet their optimism about this being a good time to buy (at 72%) is near the top. In the Midwest, 51% think that prices will rise, while in the South, 61% think so.

During the last housing bubble, the peak in prices occurred when Americans were totally souring on buying a home. They saw that these prices made no sense, that they were unaffordable, crazy, and artificial. And after they came to that conclusion in 2006, they stopped buying. Hence the crash.

Now a similar scenario is playing in the West. Prices have shot up to ludicrous levels in many areas. Fewer and fewer people – even with mortgage rates at rock-bottom – can afford to buy a home. And what they can afford to buy may only be a shack though both adults in the household have middle-class jobs. It appears that it’s gradually dawning on people that the party is drawing to an end, that the booze will run out soon, that it’s time to worry about a hangover. And they see the writing on the wall: now is a good time to sell instead.

They have their reasons. The bedrock of a healthy sustainable housing market has been undermined. And it’s dragging down the economy. Read… Here’s What’s Killing the American Dream

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I am never buying again. I lost my home in the financial crisis when we lost our income. The house was purchased with a 40% down payment and with a prime loan. That experience made me realize that even if I had paid all cash for the house I would have lost it anyway, because there is no such thing as private property in America. We are all just renters.

Now I rent a house, smaller, cheaper, and with no repair risks. I miss not being able to decorate anyway I want but I don’t have to come up with money when things break. Overall the mobility and lack of surprises makes up for not owning. I was tired of being an ATM for local govt and their endless demands for money.

If you can buy in cash and you know you can afford the property taxes no matter what, it’s often worth it. That’s a strictly-for-the-1% thing, though.

“San Francisco, prices now far exceed the peak insanity levels of 2006/2007. And so in this environment, 76% think prices will rise further over the next year”

I live in upper middle class SF “East Bay” where the residents of the city proudly show rear license plate with the city name. Its pretty prevalent and haven’t seen other town/city residents do that and I find it tasteless. Anyway the price has gone thru the roof and now priced above the 2007 prices as most of my neighbors bought when development began to sell new homes in 2006.

Interesting stat as I thought 76% in SF think price will decline after halcyon rise from the low of 2010/2011 to price above 2006/2007. Back then the “fuel” was sub-prime and no down neg amortization interest only adjustable loans AKA liar loans given to anyone with a pulse but we’re talking more about cash deals, minimum 20% down payments to hard to get approved jumbo loans (pushing people to put big chunk of cash down). Except this time the inevitable bubble will burst and there will be lot of people with loss of their downpayment and ahem here we go again with another cycle of short sales and even foreclosures in SF bay area?

Yep we learn history so as to rinse and repeat it.

But they’re not optimistic about “buying a house”. Most of them are optimistic about borrowing to “buy” one.

The hoi polloi are confident of two things: government/Fed manipulated “interest rates” will be maintained at low levels and that they will keep their jobs.

Some lessons in life need to be learned twice.

The lessons will never truly be learned. Any caution is always temporary. Caution and prudence are eventually overwhelmed by the age-old desire for wealth without work.

You know, I am not quite convinced about that reasoning. IMHO, it’s mostly people think that they are special i.e. good things will happen as long as they are involved. As a programmer, I call it the BIG IF STATEMENT syndrome i.e. they think there’s some code in the universe that says: if name == myself, then good things will happen. Can’t blame them though, with 7 billion people, it’s hard to acknowledge that you are totally not unique.

I remember back in 2005 an economics professor in my state being asked about the ever rising seemingly-never-to-end housing prices. He made the point that people who were doing the old “buy as much house as you can possibly afford” realtor meme were betting that nothing bad was ever going to happen to them. Betting that all the things that happen to people every day, like divorce, illness, and job loss, were never going to happen to them. I would definitely call that the Big If Statement.

My first solid clue that all was not right was in 1999. I was working in another city and my wife was considering transferring there. I called a popular realtor in the area, gave her our financials and asked how much house we could afford. The amount she told me was about a third more than the upper end of my comfort zone. The kicker was, but if we really fell in love with something more pricey, there were ways to get around that. I decided right then that it was time for me to get a job back where we already had a comfortable home with an affordable mortgage payment. Something had to give with a loosey-goosey housing market like that and I didn’t want to get caught up in it.

52%, interesting… So over half the population are pathological optimists. No wonder it’s so easy to run scams on humans.

I’m going to comment on this, but I don’t think my comment will be very popular. Here goes.

I graduated college in 2008, when the economic collapse was in progress. During that time, I watched my parents’ friends lose their jobs and retirements…but most notably, their homes. These were working class to upper middle class people who had borrowed responsibly, but who lost jobs in the downturn and struggled to pay their bills. These were not irresponsible borrowers.

Flash forward nearly 10 years and many people my age (around 30-35) remember not being able to find a job in 2008-2011 quite well. This feeling has stuck with me and after trying to buy last year in Denver, I’m glad we’re thinking twice. A lot of people my age saw our parents’ generation lose a lot in the last collapse, and a pretty good chunk of it had to do with housing.

Now everyone is shocked and shaken that some thirty-somethings are not enthralled about buying a home. It’s not just student loan debt….it’s the lingering feeling of panic that we saw in the last crisis.

It is unfortunate that people have such short memories.

Thank you, Natalie, for your thoughts. I think many WOLF STREET readers can identify with your experience or know people who’ve gone through a similar situation.

Current college students and recent graduates also provide some insight about economic sentiments. Many are seeking entrepreneurial careers where they may be somewhat more in control of their destiny, instead of buying into the organization man/gray flannel suit track that saw so such carnage starting in the 1990s and repeated a few times in crashes since 2000.

Thank YOU for writing this blog. I am grateful. I think that this blog kept us from making a H U G E mistake and kept us from buying a house just to buy one and fit in with the rest of our friends. Thanks for shining light on these issues.

I agree, thank you for the blog Wolf. I am 31 and graduated college in the same time frame as Natalie. I can’t imagine buying a home and being able to stay in it for 30 years with a stable job. I’m just waiting for the next bubble to pop.

As I commented before I was like your friend’s parents. I also have a twenty something son who experienced losing his home and watched his parents lose everything. He views home ownership with fear and I doubt he will every buy. I have advised him to remain mobile and liquid. This might be why home sales are down and will remain down.

I lost my home after the crash (due to divorce and moving for work – I couldn’t make it pencil out and eventually gave up and let the bank have it). I am still dealing with its financial fallout. Owning a home is a horrible liability in today’s market place where economic opportunity may require one to pack and go where the work is available.

Further, even if I have a permanent, safe gig for the rest of my years (think about that – do those REALLY exist?) then it still might be a bad idea to buy for a whole host of reasons.

I think anyone who lived through the 1999/2001/2008 blowouts and suffered job loss, home loss, and so on, will end up acting a lot like their GRANDPARENTS who lived through the 30s and save cash in the attic in trash bags. I have a very negative view of debt and am actively working that number to zero where it will remain for the rest of my life (unless I borrow to buy/invest in a cash flow positive business).

There are a lot of home owners out there (demographically speaking) who will need to sell and downsize as they get older and their needs change. Things are so screwed up now, I am wondering who they are going to sell to … because it ain’t gonna be me.

Regards,

Cooter

Good to hear from younger person like you Natalie.

I was laid-off in 2009, unemployed for a year and underemployed as consultant before I landed a job in 2011. Those 2 yrs were darkest moments of my life and my heart goes out to those still unemployed and underemployed.

Interesting to hear that your generation who graduated in last recession and faced challenges finding jobs are still remembering how the economy can sink and bring hardships to middle class and countless who lost their biggest saving tied to a house. Yet we have the “smart” money and TBTF banksters exhorting another bubble in making. Hopefully many folks won’t be fooled again.

You are refusing to buy into the American Dream? Don’t let the folks at HGTV hear this. They’ll send the Property Brothers over to smack you around!

Natalie…curious…why have you got a job NOW, but didn’t in 2008-2011? Have things magically improved?

For most of us, living standards seem to be more or less continuously declining…debt levels rising, savings being spent, education useless, jobs non-existent.

I do not think things have magically improved. I just kept working and applying for jobs and pieced things together until I landed a full-time position in my field, but it took two years of hustling. I learned a lot about myself in that time. Luckily I have a great family nearby who helped me along the way.

Generally, in my opinion, I think the division between the rich and poor in this country widens every day. Real unemployment is closer to 11-12%, not the measly 5% as proclaimed by the media. I agree with you and unfortunately I think the gap will continue to widen.

I’m a longtime resident of Denver and absurd doesn’t begin to describe the current real-estate situation. I’m not sure who’s buying all these overpriced properties but I suspect a lot of it is investors who either seek to rent or flip—the supply of houses going for $400,000+ almost certainly exceeds the number of would be homebuyers (i.e. people who actually want a place to live) that can realistically afford them.

Between adjusting for inflation and the lack of job security, I’d say it’s a lot harder to buy a home now that it was a generation ago, though I can’t say for sure as I’m well under 40. Anyone with the mindset that renters are undeserving dirtbags is out of touch with the current situation—it’s just getting to expensive to buy.

Housing prices are increasing faster than wages in many parts of the country, which isn’t sustainable. Something eventually has to give.

Louis, I agree with you. I am a Denver native and my husband and I tried to buy a home last year. We gave up! The bidding wars were stressful and being pressured to bid upwards of 20-30k over asking price just got to be too much for us — it felt too risky. I am wondering if things will ever cool off. In the meantime, my husband and I have resigned ourselves to either renting or living with family until we can come up with a plan B. It may mean relocating to another city in CO or even another state.

I love Denver in many ways and it will always be my home; however, I am questioning if it’s still the right place for us considering the prices of not only homes to buy, but rentals as well. I think the new average for a one bedroom in the metro center is close to $1.8k/mo. which is pretty high considering the salaries and median income here.

Hate to say it, but I think we have a ways to go before we see a housing correction. The Fed will not be able to raise interest rates this year and instead will likely launch another round of QE sometime in early 2016. Lower rates and a wide open money spigot, plus loose(er) lending standards, combined with neg rates, a war on cash, and worries about the long term viability of our debased fiat dollar, means folks may increasingly look to move out of cash and paper assets and into real things. Housing will likely benefit from this. Before the massive credit edifice ultimately rolls over and pukes I predict prices head even higher from here.

I agree with your views with some additional comments.

1) Some of the latest movement in house sales and prices is being driven by boomers near retirement and looking for that last home; sometimes in other cities/venues. These people have money and assets and basically have been waiting since the first housing crash to move forward. This housing pop is not unlimited but it has further legs probably.

2) The moral hazard set by the Fed bailing banks and banks ignoring foreclosures for 6-7 years leaves many with the impression that this could happen again if there is a bust. And it probably could. Doesn’t mean people are shooting for the sky, but maybe a little less afraid to buy if they have money and assets; thinking there might be some grace if things get tough. Don’t know.

3) The Fed is in a tight spot. But it will do another QE (even if it has to be stealth) if the economy is on the brink. No question. Nobody in these power positions wants the crash to happen on their watch. That’s how we got to where we are now and why it will continue until it can’t. With QE, the economy can muddle a long for years with one caveat. That is that we hold onto reserve currency status (i.e., people the world over still trust the dollar). When that changes, all bets are off and the US is screwed.

I am not sure your opinion is actually “contrarian”

QE will not be coming back. Quite the contrary the federal reserve will be making a margin call on the over-leveraged. That is where the banks will really make out by seizing the collateral. Think of it as a pool with alligators.

Michael – I’m not suggesting now is the time to buy … it is not. I sold my house last year and sold off ALL my equity exposure two years ago. I’m suggesting irrationality and insanity will continue, and unprecedented levels of manipulation driven by increasing levels of central bank desperation will drive housing (and equities) higher from here.

It is politically unpalatable for banks to seize homes en-mass, in fact, the more likely scenario is mass debt forgiveness and lowering lending standards back to 2006 levels in a misguided effort to juice the weakening economy.

And because the economy is weak and getting weaker, the Fed will kick the can and not raise rates. As the economy falters further we should expect QE4, 5, 6, etc.

Sheep graze, sheep dogs heard, sheep herders get’s rich.

For thousands of years.

Historically, house prices run about 3.3 times household income. When they exceed this, they are in a bubble and ALWAYS come back down. Check your local household income and average house price. Now IS NOT the time to buy. Also, household income is down, household debt is up, unemployment is up. Time to hunker down in a cheap rental and get debts paid off and save cash.

“house prices run about 3.3 times household income”

i was cruising thru a friends neighborhood last year and noticed a house for sale with a ‘please take one’ flyer……it was priced at 10X the area income….nope, no bubble there.

We built our house in 1985, have always enjoyed our house and yard but what owning real estate does is allow every municipal, country, and state taxing body’s employees to get their hands in our pockets for as long as we own it. It’s a delusion that a house is as good as a saving account, and many times we wish we never had built it.

I like to tell people I will buy a house if I can get me an allodial title. That usually shuts them up one way or the other. :-D

And yes, they are out there, but it is extremely uncommon to be sold or transferred. These are usually properties/lands that belong to old money.

Regards,

Cooter

Not a good time to be buying houses, stocks, or bonds. Everything is over priced and over valued . I think it’s time for another reset. Sell now or pay later.

I wonder if optimism about homebuying in California isn’t tanking BECAUSE of the drought.

Like you Wolf I live in California (Pasadena), and we’ve seen our crappy 70s built condo edge towards a million dollars in value. But how much will it be worth when the state’s spigot runs dry?

The disconnect between our home’s absurd market value and the impending crisis over water supply is literally driving me crazy. Should we sell, take the money and run? Or should I adopt the view held by most of my neighbors, that somehow God and technology will take care of us?

@Mary.

SELL your quote crappy unquote condo asap Madame!

Without enough water, to live the american dream lifestyle is quite

impossible.

Have the Californians ever thought of using their grey water to flush

their toilets and watering their lawns?

Even I have converted our home ( in the Mid West ) to collect rainwater,

laundry and shower drains into three each 315 gallon tanks.

Look at your water reduction amounts when you receive your utility bill.

If southern California does not change their water consumption behavior,

they wil learn the hard way, for sure.

Look how Israel is doing….!

Welcome to the Long Porch, Natalie. I don’t know why you felt the need to preface your remarks by saying they might not be popular, as they are your opinions formed by experience. I found them quite refreshing with a level of maturity beyond your years. I almost feel inordinately lucky NOT to have lost my house or job in the recent unpleasantness. I hope that you, like Mary, will stay and regale us with your “unpopular” notions.

I am, Madame, Your Humble Servant,

Julian

Articles like this make me miss your Housing Bubble 2.0 section, Wolf.

Shoeguy, I’m not sure what you mean … you don’t like the post?

BTW, Housing Bubble 2 is in transition. Different forces are pulling it in different directions. So now there’s conflicting data. That’s often what you get at a turning point. I’m keeping my eyes on it.