Office of Financial Research slams Leveraged Loans

In its 2014 Annual Report to Congress, the US Treasury’s Office of Financial Research, which serves the Financial Stability Oversight Council, analyzed for our Representatives the “potential threats” to the US financial house of cards. Among the biggest concerns was a financial creature that has boomed in recent years. The Fed, FDIC, and OCC have warned banks about it since March 2013. But they’re just too juicy: “leveraged loans.”

Leveraged loans are issued by junk-rated corporations already burdened by a large load of debt. Banks can retain these loans on their balance sheets or sell them. They can repackage them into synthetic securities called Collateralized Loan Obligations (CLOs) before they sell them. They have “Financial Crisis” stamped all over them.

So the 160-page report laments:

The leveraged lending market provides a test case of the current approach to cyclical excesses. The response to these issues has been led by bank regulators, who regulate the largest institutions that originate leveraged loans, often for sale to asset managers through various instruments. Despite stronger supervisory guidance and other actions, excesses in this market show little evidence of easing.

How did we get here?

Relentless QE along with interest-rate repression by the Fed and other central banks – “accommodative global monetary policy,” the report calls it – caused changes in “risk sentiment,” compressed volatility, and reduced risk premiums. To get a visible yield in an environment where central banks wiped out any visible yield, investors were “encouraged” to take on more and more risk, even for their most conservative holdings, thus moving “out of money market instruments and into riskier assets such as leveraged loans….”

During the “bout of volatility” in September and October, investors sold off these creatures, but it wasn’t nearly enough to dent the vast positions they’d accumulated. “On the contrary,” the report pointed out, “the fleeting nature of the episode ultimately had the effect of reinforcing demand for duration, credit, and liquidity risk, and led many investors to reestablish such positions.”

This came at the wrong time.

The credit cycle has four phases: repair (balance-sheet cleansing), recovery (restructuring), expansion (increasing leverage, weakening lending conditions, diminishing cash buffers), and finally the downturn (funding pressures, falling asset prices, increased defaults). Now the US is “somewhere between the expansion and downturn phases.”

Nonfinancial corporate balance-sheet leverage is still rising, underwriting standards continue to weaken, and an increasing share of corporate credit risk is being distributed through market-based financing vehicles that are exposed to redemption and refinancing risk.

Financial engineering has taken over.

Early on in the credit cycle, corporations borrowed money long-term to replace short-term debt and to fund capital expenditures. Now they use the borrowed money to “increase leverage such as through stock buybacks, dividend increases, mergers and acquisitions, and leveraged buyouts, rather than to support business growth.” And ultra-low interest rates and loosey-goosey lending standards have encouraged corporations to take “on more debt than they can service.”

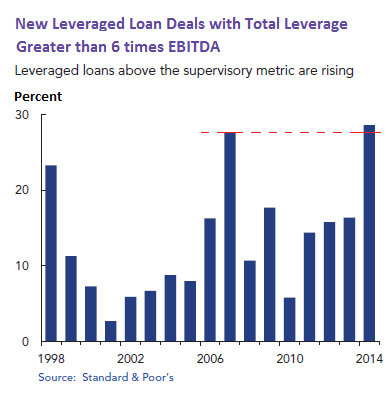

So the ratio of debt to earnings before interest, taxes, depreciation, and amortization (EBITDA) for the most highly leveraged loans reached 7.7 in October, near the peak in 2007, at the cusp of the Financial Crisis. Large corporate loans with leverage ratios above the regulatory red-line of 6 times EBITDA soared from 15% of corporate bank loans, back when regulators started warning banks about them, to nearly 30% in 2014, exceeding the record set in 2007 before it all went down the tubes:

Why would that be a problem? Because…. “Even an average rate of default could lead to outsized losses once interest rates normalize.”

And the quality of the debt sucks.

Junk debt accounts for 24% of all corporate debt issued since 2008, up from 14% in prior cycles. Over the past year, junk debt “dominated new issuance volumes.” And ominously for the holders of this debt: Two-thirds of these loans during the current credit cycle lack strict legal covenants to protect lenders, compared to one-third in previous cycles. Once the tsunami of defaults sets in during the downturn, these “covenant lite” loans will lead to lower recovery rates on defaulted debt, thus increasing the losses further.

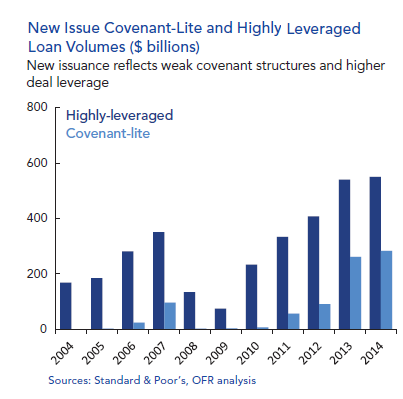

This chart (2014 data through September, annualized) shows how volume of “highly leveraged loans” (those with a spread of 225 basis points above LIBOR), at nearly $600 billion this year, is about 50% higher than it was at the cusp of the Financial Crisis. And the dreaded covenant-lite loans, oh my:

Now enter CLOs.

The combined issuance of CLOs and leveraged loans has exceeded the peak levels of the last credit cycle, whose downturn phase turned into the Financial Crisis. This buildup in credit risk has frazzled bank regulators, and they have responded harshly, the OFR reported, um, “with guidance and exhortations.”

It may be too little, too late. As the credit cycle enters the downturn phase with the deterioration in corporate credit fundamentals and rising debt levels, “the buildup of past excesses will eventually lead to future defaults and losses.”

But we’re not there, yet.

Yields on leveraged loans and junk bonds, and spreads per unit of leverage, are still at historic lows, the OFR found (though some of it has very recently gone to heck, especially in the energy sector). And “investors are not being compensated for the incremental increase in corporate leverage.”

The increased credit, liquidity, and volatility risks – that “tend to rise simultaneously during periods of stress” – have led to these junk loans being wildly “mispriced.” When they’re repriced during the downturn, investors will lose their shirts.

And “product innovation” has soared, another “hallmark of late-stage credit cycles.” They led to “broader, cheaper access to credit such as exchange-traded, high-yield, and leveraged loan funds; total return swaps on leveraged loans; and synthetic collateralized debt obligations (CDOs).”

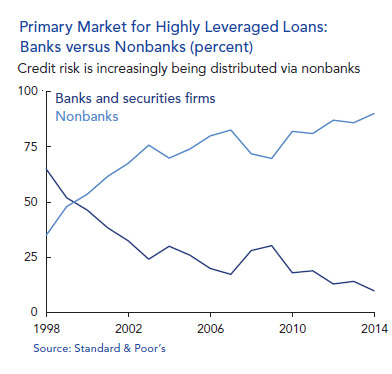

Banks, after originating these leveraged loans and repackaging them, increasingly sell them to nonbank lenders, such as institutional investors, pension funds, insurance companies, finance companies, mutual funds, ETF, etc. This process started long before the Financial Crisis – manifested by the collapse and occasional bailout of nonbanks, such as AIG. This chart (data through June 2014) shows this trend of risk being sloughed off to others:

The problem with nonbanks?

They’re not regulated by banking regulators. Even if the Fed, the FDIC, and the OCC crack down on banks with regards to leveraged loans, there is little they can do about nonbanks. And pushed to desperation by the Fed’s near-zero interest rates, nonbanks “engage in riskier deals than banks….”

Short-duration funds, which invest in leveraged loans, have shown the most significant growth. Assets under management have increased ten-fold over the last five years, driven by a search for yield and a hedge against an eventual rise in interest rates.

But banks can still be at risk when “a sudden stop in the leveraged lending market” – for example, when investors in ETFs and mutual funds get spooked – forces banks that originated these leveraged loans to hang on to them.

Yet a “significant amount of this risk continues to migrate to asset management products,” including mutual funds and ETFs that people have in their retirement funds. And investors in these products are largely on their own. When redemptions and fire sales start cascading thorough the system – the dreaded “structural vulnerabilities” – all heck could once again break loose. And that “adds urgency to the discussion” of how “a poorly underwritten leveraged loan that is pooled with other loans or is participated with other institutions may generate risks for the financial system.” Not to mention how it will savage the retirement portfolios of unsuspecting retail investors.

And some of this has already started happening in the energy sector. Revenues are plunging. Earnings will get hit. Liquidity is drying up. And stocks got eviscerated. Read… Oil and Gas Bloodbath Spreads to Junk Bonds, Leveraged Loans. Defaults Next

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“they have responded harshly, the OFR reported, um, “with guidance and exhortations.””

Too funny!

Tick tock tick tock

The book 1984: Only making up 2% of the population, the Inner Party, the oligarchical political class, is the ruler of Oceania. They make policies, decisions and govern. (And ,,, they never lose.)

Excellent analysis! Yet another leveraged loan cycle that will wreak havoc and impair/impale so many retail investors. This one will be the most devastating to date. It has been an easily foreseeable consequence of the Fed’s QE and ZIRP. When will the Fed learn?

The Fed cannot learn from its mistakes because it cannot admit its errors in the first place.

Some day future historians will write of the downfall of a society run by over-educated, credentialed fools who were completely devoid of common sense.

FED learn? They have boxed themselves in. IF they had allowed the asset prices to decline so would the value of the debts held against them. The system was so leveraged that any significant decline in asset values or in the value of the debts held against them just starts a deflationary spiral. The end of which is a total monetary collapse.

Since, oh maybe 2000 or maybe 1995, the US has had more debt and more expenses than could be serviced from the actual profits from value added productive enterprise. The FED believed that they had to try and inflate the monetary base so that these unproductive debts could be paid down with dollars that were inflated in value.

The FED’s QE was misdirected IMO. Rather than putting the money with the consumer so that they could fund the mis-allocated housing and auto loans with this newly created dollars, they funded the top gamblers in the system. The Private Equity, the TBTF banks, and the Hedge Funds thinking that this would some how filter down to the consumer.. ha ha..

On top of this Congress, which is just about worthless, couldn’t get around to actually jailing any of the first fraudsters, who pushed the system beyond its reasonable bounds. Thus created a worse moral hazard in that these same fraudsters were given new money to play with. With NO restraints!

This is all because everyone wants more that what they could purchase from wage income and the way to get more was to borrow against their futures. The Sheeple were an easy sell. This whole plan was nuts though. Lower the value of the worker thru inflation, then lend them the difference so that they could maintain their lifestyles. Then when that wasn’t enough they were sold the idea to get more house than you can really afford and a couple of new vehicles too all on exaggerated debts that they could no way repay. All so some fraudster/gamesters could buy their second yacht or that bigger condo on Park Ave.

We let the government do it too and lie to us about it.. Said that government debt wasn’t like family debt.. like that meant somehow it didn’t need to be paid back.

After the second big crash from these foolish policies, many of us thought that government would do what they did after the S&L debacle.. But NO, they were afraid and just paid the ransom to the financial terrorists.

And Now we are here again, except with much more debt, trouble all around the world both political and militarily. Not only can’t these guys learn, it just isn’t in their DNA to even recognize what they are doing. But at this point, it really doesn’t matter as the whole house of cards is shaking and what is going to be left is beyond anything any of us ever wanted.

Sorry about the rant.. I just an so frustrated about the idiots at the top who think they are soooooo smart and deserve all the spoils because they are soooo special…

No need to apologise. You summed it up nicely.

” ….Said that government debt wasn’t like family debt.. like that meant somehow it didn’t need to be paid back…”

Yes, I’m growing tired of that line too. To my knowledge, gravity still is a universal law. At least on this planet. So what goes up…

Bought some Chanel at Younkers in Omaha for Xmas. For the first time in my life I got a 10% discount. This scares me and I’m fearless…

“An average rate of default could lead to outsize losses.” I’m just letting that sink in. It all goes back to the crisis response of -08-09: “everybody takes the smallest losses possible, then we paper it all over with low rates and new debt, and all aboard for those who want to get on the risk-free ride.” What’s step two?” “What do you mean step two? That’s it.” Hell of a lot of foresight.

Leveraged loan excesses (as well as others) is one reason the Fed routinely talks up this nonsense about raising interest rates, perhaps next year. Never going to happen, but they have to try and bully pulpit the market down a bit.

By my figuring, the US economy requires 500-1000B in fiscal stimulus (rough range of ongoing deficits) and probably 1 T in monetary largess each year to keep from falling off the cliff. The fiscal deficit “just happens” and won’t change. No budget, no discussion anymore. Just happens.

The monetary stimulus by the Fed is actually trickier in that people know this is money printing, in spite of how the Fed and others try to spin it. So loss of faith in currency is the what they have to manage.

The deficit/debt stimulus is the easier of the two to let slide. It’s growing buts doesn’t conjure the concern that money printing does.

The ROW has already lost faith in the currency. The hapless American sheep will be the last to know how worthless it is.

Shouldn’t the treasury be honest, and point to the national debt as the real creature that will “sink the system”? These new leveraged loans may be the straw that finally breaks the camel’s back, but the camel could carry a lot, if it weren’t packing around 18 trillion buckaroos of debt.