The quintessential ingredient in the stew that makes up a thriving housing market has been evaporating in America. And a recent phenomenon has taken over: private equity firms, REITs, and other Wall-Street funded institutional investors have plowed the nearly free money the Fed has graciously made available to them since 2008 into tens of thousands of vacant single-family homes to rent them out. And an apartment building boom has offered alternatives too.

Since the Fed has done its handiwork, institutional investors have driven up home prices and pushed them out of reach for many first-time buyers, and these potential first-time buyers are now renting homes from investors instead. Given the high home prices, in many cases it may be a better deal. And apartments are often centrally located, rather than in some distant suburb, cutting transportation time and expenses, and allowing people to live where the urban excitement is. Millennials have figured it out too, as America is gradually converting to a country of renters.

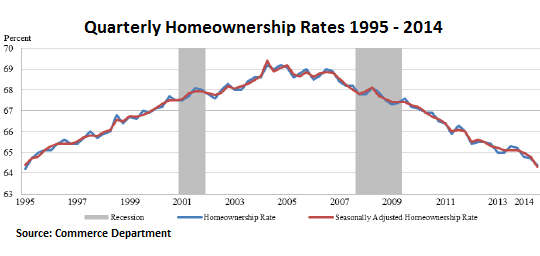

So in its inexorable manner, homeownership has continued to slide in the third quarter, according to the Commerce Department. Seasonally adjusted, the rate dropped to 64.3% from 64.7 in the prior quarter. It was the lowest rate since Q4 1994 (not seasonally adjusted, the rate dropped to 64.4%, the lowest since Q1 1995).

This is what that relentless slide looks like:

Homeownership since 2008 dropped across all age groups. But the largest drops occurred in the youngest age groups. In the under-35 age group, where first-time buyers are typically concentrated, home ownership has plunged from 41.3% in 2008 to 36.0%; and in the 35-44 age group, from 66.7% to 59.1%, with a drop of over a full percentage point just in the last quarter – by far the steepest.

Homeownership, however, didn’t peak at the end of the last housing bubble just before the financial crisis, but in 2004 when it reached 69.2%. Already during the housing bubble, speculative buying drove prices beyond the reach of many potential buyers who were still clinging by their fingernails to the status of the American middle class … unless lenders pushed them into liar loans, a convenient solution many lenders perfected to an art.

It was during these early stages of the housing bubble that the concept of “home” transitioned from a place where people lived and thrived or fought with each other and dealt with onerous expenses and responsibilities to a highly leveraged asset for speculators inebriated with optimism, an asset to be flipped willy-nilly and laddered ad infinitum with endless amounts of cheaply borrowed money. And for some, including the Fed it seems, that has become the next American dream.

Despite low and skidding homeownership rates, home prices have been skyrocketing in recent years, and new home prices have reached ever more unaffordable all-time highs. Housing Bubble 2 came into full bloom, but now it too popped. Mess ensues. Read… New Home Prices Plunge the Worst EVER (in One Ugly Chart)

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Keep up the good work, Wolf.

I noticed that Bloomberg is reporting that mortgage purchase applications have plunged to 1995 levels, a 19-year low.

My view is that this whole recovery meme may very well be derailing and that the US economy is flatlining at best or falling back into recession at worst, not that we’ve ever actually left recession since 2008.

Even one of my favorite whipping boys, Alan “Mr. Magoo” Greenspan (or is that Greedscam?) remarked today to the Council on Foreign Relations that “effective demand is dead in the water.”

I guess that means we should all go out and buy stocks and wait for the next round of money-printing so our stocks will shoot to the moon. Not!

Between 2008 and 2014 90% of the foreclosures and short sales went to US and foreign (Chinese) institutional investors and of course the banks helped them self as well. Most of those homes are rentals today.

Welcome to the USSA.

The hedge funds own tens of thousands of houses in Florida. There are still thousands of homes in the foreclosure process. The banks have slowed down the process in order not to dump too many houses on the market at once. But, the supply is still in the pipeline and the demand is not there. Prices look like they will eventually be going down.

Charts like this one are why the FED has to end QE. GDP growth per $1 of printed fiat is now zero, and increasing the asset bubble only makes it more difficult for people to buy houses and big ticket items.

The FED has boxed itself in a corner and has no options left but to watch the economy crash by a deflationary collapse or by an inflationary collapse. They’ve chosen the deflationary collapse because that has less chance of being blamed on them.

Don’t expect QE4, like everyone’s saying, it’s not coming. The realization of this will sink into the collective consciousness over the next few months, that’s when the real fun begins.