The American public is astute about a lot of things, but the stock market – despite all the hoopla in the media and even on NPR – apparently isn’t one of them. That’s what the Wells Fargo/Gallup Investor and Retirement Optimism Index survey found.

And it raises some thorny issues about the Fed’s strategy to print a few trillion dollars and force interest rates down to near zero in order, as it said, to inflate stocks and other financial assets, thereby triggering the “wealth effect,” which would stimulate the Main Street economy. This is, of course, precisely what has not happened. And the American investing public just told us why.

The survey asked American investors with $10,000 or more in stocks, bonds, mutual funds, or in a self-directed IRA or 401(k) – so not the entire American public but only those who have a stake in the markets – to comment on a number of basic topics, but here’s the one that stuck out the most:

As far as you know, how did US stocks perform on average in 2013 – did they increase in value, stay about the same, or decrease?

(If increased): Which of the following do you think comes closest to the overall increase in the US stock market in 2013 – was it up 10%, 20%, 30%, 40%, or 50%?

It so happened that in 2013, the S&P 500 chalked up a total return, including dividends, of over 32%. It was the most phenomenal year since 1997, when it had zoomed up 33%. So it’s not exactly a common event. And it should have entered into the consciousness of the investing public who’d presumably benefitted from it. But it didn’t.

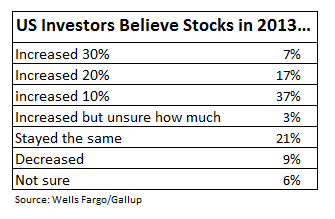

A mere 7% of the investors got it right.

One can only imagine how the overall American public, including the tens of millions of folks who’re just scraping by and have zero stake in the financial markets, would have performed on the pop quiz.

To their credit, 64% of the investing public believed that there had been at least some gains, even if way below the actual gains, with the bulge bracket (37%) figuring that stocks had gained 10% in 2013. But 21% thought stocks had remained flat, and 9% of the investors thought stocks had declined!

The survey made clear to the respondents that it was about the stock market, not their personal portfolio. But could people really distinguish? Wouldn’t it impact their judgment about the overall market if their 401(k) had been whittled away by fees and bad decisions whose holes weren’t papered over with new contributions? Maybe. But in the statistics, they would have been overpowered by the other investors who watched their statements gain weight during the course of the year.

So then the survey asked directly how knowledgeable they were about investing in the market. Thankfully, only 11% described themselves as “highly knowledgeable,” but 56% thought they were “somewhat knowledgeable” though almost none of them could pinpoint one of the most basic facts of investing, namely how much stocks had soared last year. And 33% were honest, considering themselves “not knowledgeable.”

Whatever this survey says about American investors with more than $10,000 in the financial markets, it speaks volumes about the Fed’s favorite policy goal, the “wealth effect.”

The Fed claimed that by inflating asset prices, it would make Americans feel wealthier, and thus induce them to spend more money, which would crank up the Main Street economy and solve all problems. OK, sales of luxury goods, expensive cars, corporate jets, yachts, and the like responded very well. Sales of other goods not so much.

Why? Because the majority of Americans didn’t benefit at all from rising stock and bond prices because they had no stake in the markets; they were busy trying to find jobs and make ends meet. And even most of those who benefited from the rising stock prices by having a stake in the markets weren’t sufficiently aware of it, or weren’t aware of it at all, according to the survey. Maybe they simply didn’t have enough money in the markets to make a real difference in their lives.

The Fed has known about this all along. It knew that the wealth effect would do nothing or very little for most Americans who were much more impacted by the concomitant reduction in real wages. It knew that that the wealth effect would do nothing to crank up the Main Street economy. For the Fed, it was just a pretext for engineering the greatest wealth transfer of all times and for whatever other goals it wanted to accomplish. And America’s investing public just pointed that out again.

And the fact that most investors are in the fog about the markets they invest in, the risks and rewards they face, the rip-offs they encounter, the fees they pay… is the reason Wall Street gets away with its game for as long as it does.

And the game has been honed to perfection. Everyone is playing along. And it performs miracles. Or it did. Because just now, it inexplicably conked out. With major consequences. Read…. The Wall Street Hype Machine Suddenly Breaks Down

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Actually, the market peaked in 2000 at 11,722. Adjusted for the loss of purchasing power since 2000, the market isn’t up, it’s down. It may be “up” compared to the previous year, but that doesn’t buy you much. In addition, many, many people have either lost their jobs or experience no wage increase for many years. What money they have goes for food and housing, not discretionary purchases. Wealth effect ? Surely you are joking.

As to the stock market, it is tiny by comparison with the bond market. In recent years, the political manipulation of the interest rates on bonds has driven a flood of money out of the bond market and into the stock market in a desperate search for yield. That flood was far in excess of what the stock market could reasonably absorb, and the result was asset price inflation, not growth. When it was clear that earnings were anemic and couldn’t justify the valuations, companies began cooking their books to make things appear more reasonable. The government and Wall Street analysts are fully aware of this but are terrified of pricking the balloon.

In addition, many old timers like me have gone to the margins because we are convinced that the market is a Three Card Monte table. You don’t put money you can’t afford to lose in the stock market, you put it into bonds – well you did in the years B.G. (before Greenspan), now you put it under the mattress. Among the most serious problems is the widespread use of machine trading which has distorted the entire concept of stock investing. Machine algorithms don’t select stocks based upon classical guidelines. They are geared to detecting momentum in price movements. Purchases and sales are made without human intervention of any sort. Trying to actually implement Warren Buffett’s principles in today’s market is like picking up nickels on the railroad tracks. It is worth mentioning that Buffett himself doesn’t adhere to all of his theories anymore. Ask him about derivatives and tax strategies.

Average Americans have no investments. The majority cannot scrape together a paltry $400 to cover the cost of a moderate economic emergency. What Americans have is crushing debt, whether that debt be credit card debt, student loans, car loans that exceed the value of the car, or mortgage debt on vastly overvalued property.

I was born toward the end of the Truman Administration, so I’ve been around for awhile. This so-called economic recovery is the greatest hoax ever perpetrated in my lifetime.

If you believe in a “Main Street” economic recovery, take a good look at Atlantic City, New Jersey. As of the end of September 2014, 4 of the city’s 12 casinos will have closed – The Atlantic Club, Showboat, Revel, and Trump Plaza, taking down $75 million in city tax revenues, or 30% of the city’s annual budget.

While it is true that competition from Philadelphia-area casinos since 2006 has eroded Atlantic City casino revenue, the unpleasant little fact is that erosion of casino revenue since 2006 is now around 50%.

This level of decline is not solely the result of competition from Philadelphia-area casinos. It is also the result of drastic declines in the discretionary income of average Americans since 2008. Ordinary Americans can’t even afford a day trip to Atlantic City any more.

Atlantic City is in an economic death spiral, and could soon be a miniature Detroit.

Recovery? You’ve got to be kidding me!

It seems like every city has its own peculiar economic issues.

The financial crisis and the housing bust hit Las Vegas hard too, but the casino industry there has been recovering nicely and housing has been re-pumped up by private equity firms playing the buy-to-rent game.

Why would LV be so different from Atlantic City?

It could be that primary gambling locations like LV get foreign visitors along with the portion of Americans who can afford a plane ticket, while casinos relying on regional visitors get shafted. Would be interesting to get some data on this.

VegasBob, if you live near Atlantic City and have your own photos of shut-down casinos, boarded-up stores, closed hotels, etc., I’d be interested in posting something on it. If interested, contact me via the contact tab.