No one knows the full magnitude, but it’s huge.

How big is margin debt really, and how much of a threat is it to the stock market and to “financial stability,” as central banks like to call their concerns about crashes? Turns out, no one really knows.

What we do know: Margin debt, as reported monthly by the New York Stock Exchange, spiked to another record high of $528 billion. But it’s only part of the total outstanding margin debt – which is when investors borrow money from their broker, pledging their portfolio as collateral.

An example of unreported margin debt: Robo-advisory Wealthfront, a so-called fintech startup overseeing nearly $6 billion, announced that it would offer its clients loans against their portfolios.

“The dream house. The dream wedding. The dream kitchen. The dream vacation.” That’s how it introduced it in a blog post this week. “We want you to have your cake and eat it too,” it said.

Instant debt “without the hassle of paperwork,” it said. “We want our clients to be able to borrow what they need, when they need it, directly from their smartphones.” Secured by “your own investments.”

It’s a great deal as long as stocks are soaring. Clients with at least $100,000 in their account can borrow up to 30% of the account value. It’s seductive: No required monthly payments and no payoff date, though interest accrues and is added to the monthly balance. The rate is as low as 3.25%. “How’s that for flexibility?” it says.

That’s how margin debt is being pushed at the end of the cycle.

This borrowed money can be drawn out of the account to fund vacations or a down-payment of a house. But when stocks spiral down, as they’re known to do in highly leveraged markets, and fall below the margin requirement, clients get a margin call. They either have to put cash into the account to make up for the losses or they have to start liquidating their portfolio at the worst possible time.

This forced selling occurs across the spectrum during a sharp market downturn and drives prices down further and begets more forced selling. Margin debt is the great accelerator on the way up, and it’s the great accelerator on the way down. Crashes feed on margin debt.

So how much margin debt is out there? We know only the $528 billion reported by NYSE. Then there are companies like Wealthfront. But it’s just small fry. Big players have been doing this for a long time. These securities-based loans (SBLs) are called “shadow margin,” and no one knows how much of it is out there. But it’s a lot.

The New York Post took a look at it:

Finra, the brokerage regulator, doesn’t track it, nor does the Securities and Exchange Commission — even though both have warned investors about the risks.

However, several advisers surveyed by The Post estimated there is between $100 billion and $250 billion in outstanding SBLs among all brokerages.

Morgan Stanley is one of the few firms that says how much in SBLs it’s sold – $36 billion, as of Dec. 31, a 26-percent increase from the year before.

Other major sellers of the loans are UBS, Bank of America, Wells Fargo, Raymond James, and Stifel Nicolaus, sources said.

If this “shadow margin” is $250 billion, it would bring total margin debt to $778 billion. That would make for a lot of forced selling.

Margin debt is in an uncanny relationship with the stock market. It soars when stocks soar, and it crashes when stocks crash. They feed on each other.

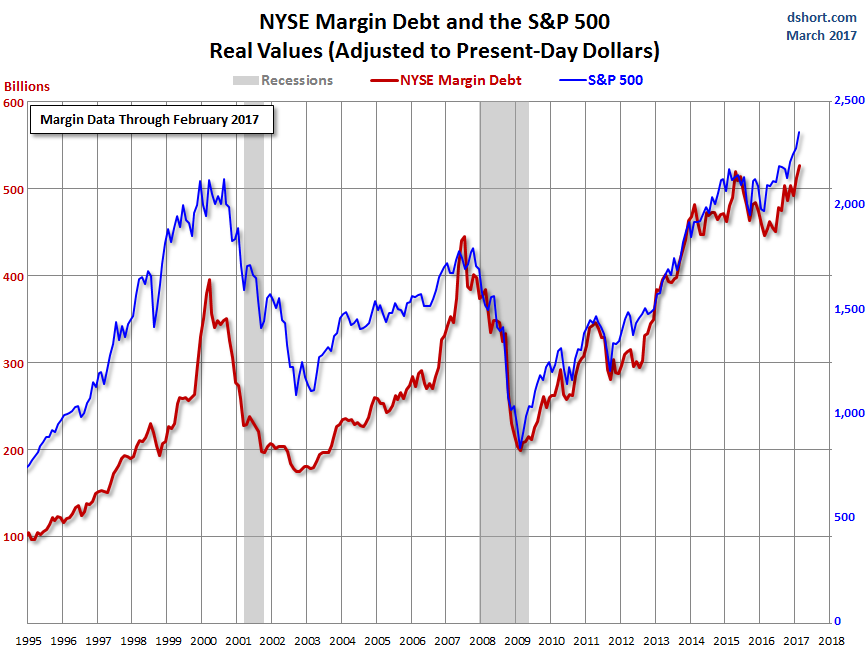

This chart by Doug Short at Advisor Perspectives overlays margin debt as reported by the NYSE (red line, left scale) and the S&P 500 (blue line), both adjusted for inflation, with margin debt expressed in current dollars. In February, the latest reporting month, margin debt surged 2.9% to a new high of $528 billion:

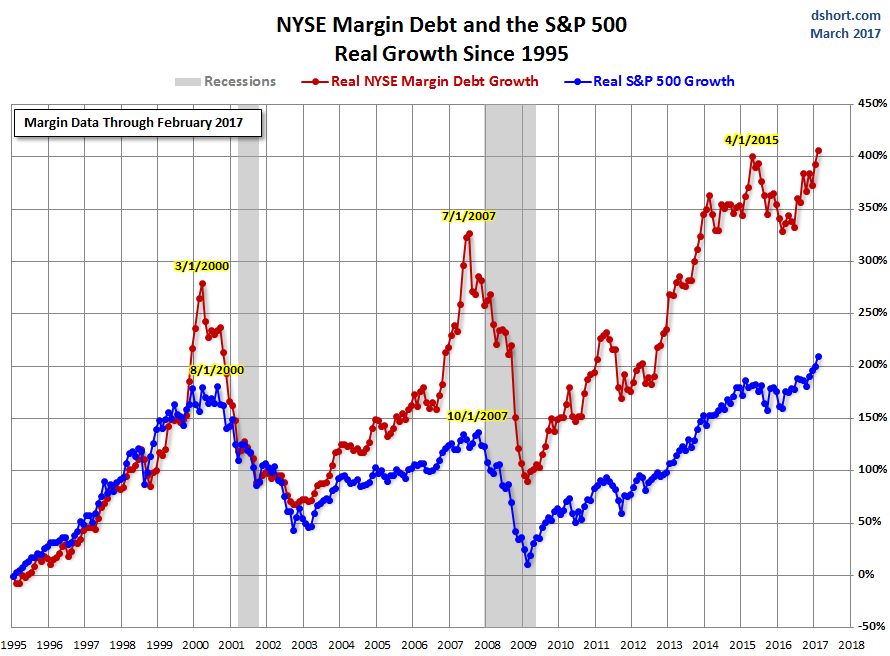

And the chart below shows growth in percentage terms of the S&P 500 (blue line) and margin debt (red line), adjusted for inflation, since 1995. Two things become brutally clear: Just how leveraged the stock market has become, and how peaks of leverage are unwound by crashes (via Doug Short at Advisor Perspectives):

But the charts only depict the $528 billion in margin debt reported by the NYSE. Now add the current spike in “shadow margin” of perhaps $250 billion in SBLs. This “shadow margin” might raise current leverage by nearly 50%!

Leverage speaks of investor confidence. A lot of leverage signifies exuberance. Borrowing money to buy stocks creates demand and drives up prices. Higher prices encourage players to borrow even more. And when prices rise for long enough, the notion that they could actually return to some prior levels disappears. That’s the beauty of leverage. It’s free money. Nothing can ever go wrong.

But margin debt, as the charts show, has the unnerving habit of peaking right around the time the bubble turns into a sell-off. While it’s a terrible predictor of a crash – no one knows if February was the peak or just another stage on the way to an even more dazzling peak – it is associated with enormous risks. And the fact that much of it occurs in the shadows, and that the total leverage of the stock market remains unknown, makes this a powerful time bomb that stock markets are sitting on in blithe spirits.

This is what companies in the S&P 500 index have become really good at: Railroads slash capital spending, but plow more money into buying back their own shares, after two years of Freight Recession. Read… This Vicious Cycle is What Bedevils the US Economy

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Looking at the second graph, it is interesting how the margin debt peaks in 2000 and 2007 were after it going nearly vertical for a year or two. The same thing appears to have happened around 2013 into 2014 with no resulting crash. It just went sideways.

Question if you know it Wolf: how often is margin debt reported? It times with the market nicely and should be a good tool for predicting sentiment.

The NYSE reports its part of the margin debt once a month, one month late (so in a few days, we’ll get March).

You can get the data here:

http://www.nyxdata.com/nysedata/asp/factbook/viewer_edition.asp?mode=tables&key=50&category=8

Margin debt will always follow the market. So it is not a good predictor.

Really? Neither was using your home as an ATM, as the ‘price appreciation’ kept pace with the borrowing.

Lets all raise our glass to the new ETF based on all ETFs.

I saw a hotrod pickup truck smashed into a tree, some kid laying on the ground with medics hovering over him. On the back window was a sticker ” No fear”. So have at it boys and girls.

Where is Petunia?

Thanks for thinking of me. I’m still out here, commenting where debate is possible.

“The same thing appears to have happened around 2013 into 2014 with no resulting crash. It just went sideways.”

This is a classical analysts mistake, that is still not viewed as a mistake, by the mainstream.

The 2013/4 event did not occur in the same NON QE market that the 00 and 07 event’s did.

The fed is slowly starting to tighten at some point the market will revert to its PRE QE Behaviours and at that point, many people will be punished for their QE induced complacency.

That reversion, could be the event that triggers the overdue correction. Which would be a nasty double whammy.

Orange isn’t the new Black, Debt up to your eyeballs is.

Wells Fargo, corporate welfare queen who got a huge bailout in 2008, has this to say:

“Some of the advantages of securities-based borrowing include:

Access to cash when you need it

Typically lower rates than other forms of credit

No set-up, non-use, or cancellation fees

Ability to borrow between 50% to 95% of your eligible assets, depending on the collateral and type of credit you receive

These lines of credit can be used for many purposes. Common uses include:

Home renovation

Real estate purchase1

Expenses such as taxes or tuition

Boat, car, or other luxury purchase

Business opportunity”

https://www.wellsfargoadvisors.com/why-wells-fargo/products-services/lending/securities-based.htm

What would be funny is if the Donald and/or his family members were to get a YUGGGEE margin call while he is office. Perhaps he’ll have Gary Cohn negotiate handing over the White House to Goldman Sachs to settle the bill.

Fingers crossed [ minus the Whitehouse part ] and entirely plausible . If it does that’d be the very pinnacle of Poetic Justice .

This has nothing to do with President Trump!!

Right. It’s all Ayn Rand’s fault.

I know what a president looks like. I know that a president can speak a coherent sentence. I know that a president should believe in science. I know that a president should have a grasp of economics. I know that the first lady should live in the White House. I know that a president should not spend every weekend at his resort golf course. This I know!

Perhaps he’ll have Gary Cohn negotiate handing over the White House to Goldman Sachs to settle the bill.

Um, I think we’re past that point already.

The number of common stocks traded on major US exchanges are the lowest since 1984, according to the University of Chicago, Center for Research in Security Prices.

Changing accounting rule FAS 157 and eliminating mark-to-market for banks, did not end the financial crisis. Far from it. Instead we have an extended topping, overvalued, overbought, overbullish peak, of what is now the third financial bubble since 2000.

Changing the rules at best, has resulted in prolonged periods of stagflation, as there is no additional marginal banking capacity. The diminishing marginal productivity of debt has reached its vanishing point.

Pretending that debts are assets rather than liabilities, has led many to believe this false construct and to lull them into a perception of perceived wealth. The very fragile global currency system, as it exists now, has become inherently unstable. When the margin call comes and come it will, just a matter of when, the coming reset will be epic.

“overvalued, overbought, over bullish peak,”

….

There is someone who writes a weekly market commentary and he says what you said… only problem is that he has been saying that since 2003.

Oh.. and he sometimes adds” rising yield spread” to his OVOBOB statement.

Not a criticism of him; Just sayin’, that’s all.

Well said. Yes Mark to Model has been one of the reasons we are in this financial mess. On April 2, 2009 the USA goes from Mark to Market accounting to Mark to Model accounting. On May 1, 2009 Canada goes from Mark to Market accounting to Mark to Model accounting. The elimination of Glass Steagall was another great financial error.

Not to worry though; I believe the powers that be are working on another financial ponzi scheme for all of us.

My business was DESTROYED in the tech wreck of 2000-01. This should be even more breathtaking. I can’t wait, this time my powder is dry, i’m long puts everywhere and I’m ready!

what is it called when companies like IBM borrow at 1% to buy back stock.

just another form of leverage with a double hit coming when rates head up and stocks go down-

Yes, and guaranteed not to end well.

If I was a betting man, I’d put my money on that being the foundation of the next financial crisis.

Rates are not going to head up.

Fed would decrease the rates the moment they see any weakness in the stock/asset market…

If they wanted to increase the rates, they’d have done long back..

Totally agree. Japan here we come.

the feds have backed themselves into a corner, they can’t “normalize” rates; the economy is too weak. Asset inflation,money supply increases and fed deficit funding is the only game available in sustaining a moribund economy. The amount of margin debt is alarming however the amount of liquidity still being injected globally (e.g. BOJ and EU added another $1 trillion to date,2017) may keep the balls in the air.

Capitalism does not work for the majority of people. Credit is stressed out to the Maxx. Our health and well-being has been superceded by profits and greed. Our tax dollars are wasted on wars for profit that result in failure while making more enemies in a never ending cycle. Our healthcare system is collapsing. Oh…And Climate Change is real!

Now we have a government that has no clue about the real world.

They need to increase rates to stop this crazy debt leveraging. I live in fly over land and houses are selling in 2 days. I have ever seen them sell this fast before. Yes there is low inventory but credit or shadow credit must be getting flowing and easy to get. I know FHA is giving out a lot of 3.5% down loans.

My credit union is offering a Hybrid HELOC. They will allow me to borrow up to …….100% of my homes value. From 2009 until 2012 they would only let you borrow up to 60% of my homes value. What changed?

I have a rental house. I thought about putting new siding on the house on year ago. The cost was $7800. Now one year later I got a bid from the same company. This new bid is $8600. That is over a 10% increase in one year.

Things are too hot right now. If the Fed lets this go on much longer we will see a big housing crash again. They need to increase rates at least 1%.

Fed don’t do anything

The increased in asset pricing is helping the elite and Fed is indentured to them

Not enough trades people around for what is going on. A lot left following 2008 and didn’t come back. A fellow landlord just got a bid that made me choke. I hope and pray I don’t have a major repair before this thing pops.

“Not enough trades people around for what is going on. A lot left following 2008 and didn’t come back.”

Plenty of tradies around, look at the regulations and regulation compliance costs.

With all those extra compliance cost and the time wasted dealing with them. Most small tradies cant comply and put it a winning bid, so they go elsewhere to earn.

Only the operations that are corrupt, or can afford to keep compliance departments the consumer funds, and run on small after compliance cost margins can stay around.

And that clown at the Boston Fed has promised to expand the balance sheet again to keep the asset prices high (also known as printing money). It appears the margin marvels have the Fed-approved right idea. The moralists are appalled and will continue to be appalled.

If I remember my Brealey and Myers Principles of Corporate Finance textbook correctly, such an action would be considered… a really dumb idea.

I don’t know, but somebody had better telling those poor souls lending IBM money Big Blue has been bleeding sales for twenty consecutive quarters and under GAAP rules their revenues have been steadily falling since Q2 2012.

For once reality came back and the news wiped all the undeserved gains IBM stocks had in January and February.

IBM is to Apple as Sears is to Amazon.

So is there an investment strategy I would follow re any of the four?

Yep – desist. Any appraisal I can devise looks like an inflated valuation, just as with everything else the Fed is funding.

You have to keep in mind a minor detail, the IBM of today isn’t the IBM everyone has in mind when speaking of IBM. They have sold off their traditional hardware business to the Chinese and today IBM is a slowly withering software Company. Mr Spencer if he was alive today would probably bring out a carbine of his own manufacture and go after the management of the company he once did found if he saw what they are doing nowadays with IBM …

Realist should read https://en.wikipedia.org/wiki/IBM_and_the_Holocaust

If ever there was a US company that deserved to die, it is IBM.

Its death can not come soon enough.

IBM German subsidiary Hollerith made Tabulators to count Nazi Concentration Victims as they were being Gassed and Burned. The Germans paid the costs into Swiss Bank Accounts which were transferred to the IBM (USA) after the 2nd World War.

IBM and Hollerith, also did a HUGE number of things for the general German war effort, that among other things after the war became JIT, industrial supply theory.

Their Assistance to the German war effort, also helped kill, a LOT of American’s.

https://en.wikipedia.org/wiki/IBM_and_the_Holocaust

should be required High-school reading.

Along with the Fact, everything IBM knew. J Edgar and FDR knew.

When I was at college taking Chemistry a Fellow Student told me that in his Biology Coursework his Textbooks detailed German Nazi Research conducted by Dr. Mengele and others in Experiments conducted on Concentration Camp Victims. Like trying to Replicate Gangrene on Inmates Shot and Deliberate Broken Limbs in Freezing Conditions. Injections of various Chemicals like Anti-freeze and Compounds supplied by Bayer and other German Chemical Companies.

Put it this way.

Amazon can make profits when they want them: they generally choose not to do so for purely fiscal reasons. Bezos’ machine is more about fiscal than financial engineering.

Apple is all about profits. Problem is how long they will be able to have those margins now that their business is iPhone-dependant and that smartphones are becoming commoditized. The ongoing iTunes fiasco is, in my opinion, a warning they are becoming too complacent. If Jobs were still alive, heads would have already rolled.

Sears is a relic of a bygone era. In a way it’s like the Giant Panda: everybody’s sorry to see it go, but it reached an evolutionary dead-end.

IBM… I honestly don’t know what the management was thinking when they decided to become a software company with no truly exclusive technology.

Nah, MC, you’ve got it wrong. IBM itself says that everything’s going to plan as IBM “confidently reinvents” itself. It’s a “high value” business. You obviously don’t understand financials. ;)

Want some laughs? Go here:

https://www.theregister.co.uk/2017/04/19/ibm_q1_fy2017/

The question is not margin debt and its relation to stock valuations.

A lot of investment in paper flipping involves other people’s money. Realistically, if I were investing your money and had no conscience, I would let it run until your losses were so large they might affect me. If I couldn’t get hurt, it’s your problem not mine. If I could get hurt then it would be a time for concern. My first impulse would be to find someone who would cover my losses to you … of course that person would not realize that was their job. They would be saving the world or making a killing. Whatever worked as a sales pitch.

If that didn’t work, then I would take my actual investment and head for the hills. At that point the markets would really fall.

So, this is the scale to use to figure out the hits to the public markets. When the cost actually hurts the big players, then the markets will react. Until then, it just a paper flip.

“The question is not margin debt and its relation to stock valuations”.

The correlation of margin debt and stock price are intertwined.

Where systemic deleveraging happens, a depression usually occurs.

Assets are sold, often for pennies on the dollar. The result being that asset prices collapse. Equity levels drastically decline. This triggers more selling of assets. Credit levels shrink as the value of underlying collateral vanishes. Cash flow dries up and debt service stops, generating more asset sales and bankruptcies become common. This now becomes a self-reinforcing cycle of economic negativity. A vicious circle.

Yes, but it requires the equivalent of a few atomic bombs to get the ball rolling downhill. At least today considering all the players who each have a different game … some to prop the markets and some to exploit them. Even then, a Bullard save can be worth trillions and nullify everything bad. I’m not holding my breath, although I would be ecstatic if the equity markets fell 20% – 30%. The upper 1% and their flunkies are in charge and no depression is in the near future .. unless a big profit can be made from one and a ‘depression’ is a part of the plan.

My great uncle on my fathers side became VERY wealthy buying up prime real estate in Nassau County NY during the Great Depression He was an MD and not a great humanitarian to put it mildly If your wife was dying and needed his help and you couldn’t pay he would gladly take the deed to your home And yes he looked exactly like Mr Potter

Most of the top 5% or more, double up, or more, in a real depression event.

Which is why we need a wind down not a fall down. As in a wind down. The little guys don’t all get those “pay today” notices on the same day, which create opportunities for the top 5 % with cash waiting, like they do in a fall event.

All those wish PAIN on the top 5 %, are wishing much worse on the rest, as whatever pain the top 5 % suffer, is always magnified by 100’s of %. On the other 95 %, getting worse the further down the scale one travels.

In the old adage “S t gathers speed and volume, as it rolls down hill”.

Also, let us not forget what happened from October 2008 until early March 2009. To wit, the major global Financial Institutions and their counter parties wanted their money back….. all at the same time.

I have learnt one thing by observing USA in general.

The system rewards the reckless and punishes the diligent and conservative people.

A lot of people have been crying for the last 5 years that housing prices in CA is bubblicious but people who bought houses in last few years are enjoying great appreciation.

People who were over risk averse and conservative are now regretting and waiting for the bubble to burst.

Same thing with stock market. I have friends who pulled their money out of stock market 4 years back and now they are regretting big time.

We need to remember that these are not normal times and this can sustain for few decades…..

Jon

I am like one of your friends, convinced the insane lack of fundamentals meant there was no foundation to invest upon. I have also missed out on this increasing wealth casino. However, my wife and I live as well as we wish and both of us sleep at night knowing we have no debt and a decent savings account if/when things go sideways.

One more thing, we are at that age with sick and ailing parents to attend to. While they are okay financially, we are watching them slide into their end of days and must do all the organizing for them; taxes, medical appointments, keeping them engaged, house maint. etc. If we had to worry about losing our nest egg or carrying debt, well, it would be just too much. Life is short and there is more about living than making money.

regards

A zillion comments were posted on the internets today and this is one of the most thoughtful. Thank you.

Your “sleep” comment reminded me of something an Algerian or Moroccan taxi driver told me one evening in Montreal: “it’s better to sleep in the gutter at night at peace with oneself than in a mansion with blood on one’s hands” (paraphrasing the original in French).

I have quite elderly parents — currently in good health but at the age when any slip on the floor could be a disaster. As you say, life is (too) short.

Regards to the great Wolf Street community.

I AM an elderly parent, staying as independent as I can and arranging my affairs as best I can to leave the kids a worthwhile inheritance without unduly burdening them now, or as time goes on.

They deserve it – I have not financially subsidized their lives much.

We just brought them up with emphasis on self-reliance and decent ethics.

Paulo,

Your safe haven is cash?

Land and cash. The land is a woodlot with an orchard and large garden site…yet zoned residential so it can be sold if needed. (I bought it in case relatives ever needed a landing pad). It is 16 acres, and the taxes are very low here. Our home site is across the road from the land, and is on a river with good salmon runs, etc. Our cash is in term deposits at a local but well established Credit Union. Our pension is fully funded at I believe 105%, and free from interference (raiding) by either Govt. or corporations, instead, is managed by a Board of professionals and actuaries. We are set up that we could survive without the pensions, but if the whole thing blows up we are in the same boat with everyone else. :-)

We also live in a tight community and have very good relationships. (Rural)

This has all been deliberate and very fun to plan and carry out over the last 15 years. (Like RD)

Jon – Maybe we’re in what will be known as “the roaring teens”.

I know back in the late 90’s, even I could have bought something, some sort of land, in a small Arizona town and I’d have been OK even through the last two crashes. Lost some but then gained back a lot more.

This is an economy for hucksters and gamblers, and reasonable, prudent people tend to buckle down and do the right things and that’s no longer rewarded much.

Alex, I know you from Dr housing bubble website.. good to see you.

I know that website is crying wolf about prices being too high in bay Area and Socal for last 6 years..

we know what happened so far…

Jon I finally got tired of that site. At least 50% of the posters there don’t live in California, it’s a big Trump love-fest, and it’s just …. well, hanging out with the “slow kids” gets old.

Let the depression happen. Everybody would lose their job and foreclose on the mortgages. Those who think they can retire find reality other wise.

But the good thing is, while u r dying, the rock become poor or die with you.

Want to go that way? I do.

Most will not. That’s how they own you. You are playing the game and so deep in the situation you depend on them to survive.

Periodic economic crashes are necessary to purge the speculative excesses from the system and restore true price discovery, as well as punishing the reckless and greedy.

“Periodic economic crashes are necessary to purge the speculative excesses from the system and restore true price discovery, as well as punishing the reckless and greedy.”

Or, you can just avoid government and Fed policy that leads to the asset bubbles that cause crashes to begin with.

Naw, that would be big gummint innervention in the fwee market! It’s much better to give Wall St a fwee wide down easy street and make working people suffer, right? Cuz, we gotta have our crashes, to teach poor brown people the value of hard work, right?

It is all talk guys.

When the voters go to the voting machines, they do not care about any condominium principle. They vote for politicians that promises food stamps, artificially created jobs, and of course those who promises to “solve” the sinking houses and economic problems.

Nobody cares if those were money taken from Paul to give Joe, nobody cares when those “fixes” were done by money pritining.

I remember when Wall street started to buy houses to convert into rent in 2012, i heard it on local radio that people cheers because that will lift their underwater mortgages..

In the end, viters do not get what they want, biters get what they deserve which is to let GOV and 1% take them for a ride.

These ‘Security Based Loans’ seem to me to be a cute way to avoid paying capital gains tax. I wonder if the IRS might want to take a look at this practice since, as I understand it, the lender can liquidate your shares for non payment. Isn’t that transferring ownership?

“Liquidate” in this context means “to sell” at whatever price the market is trading at that moment. Whether it results in a capital gain or loss to the hapless client at that time is of no concern to the brokerage firm. Its only interest is in protecting the capital of the firm. The investor will owe taxes on the transaction if they are due.

So can your broker, when you get a margin call, which happens every time there is a market crash, and if you do not liquidate shares quick enough to satisfy it, he will. But I don’t believe the sales price, when the broker generates the sale, reflects any change in ownership other than you’re not owning the shares any more. The loss on those shares, if any, is yours.

I would say the big hedge funds are placing massive bets but are also shorting at the same time and probably the big banks so they win on the margin either way but don’t worry uncle Sam will come to the rescue if it all goes wrong just print some more money bingo problem solved. But it’s not free money it’s debt with artificially low interest rates.fast rising debt and slow rising growth which in the long run is not sustainable is legal theft by stealth through woefully inadequate regulation such as the repeal of the glass stegal act. It was put there in 1933 for a reason .maybe we will find out the hard way AGAIN.

Its free money for big people.. they have the freedom to play and if they lose, the middle class would pay up for them..

I must admit that I’ve never heard of Security Based Loans before reading the article. I need to do more research before forming an opinion, but they seem to be a product which has the potential to benefit to a small category of investors whose principal (or only) assets are stocks/ETFs but are marketed towards a much wider potential consumer base.

SBLs used to be the domain of high-net-worth investors. Normal folks had to make do with regular margin loans, which can do pretty much the same thing (fund a vacation, for example). Looks to me like fintech is trying to democratize SBLs.

There is a reason for the “Used to be”.

Both Fintech and its new non HNW Investor clients, will live to regret violating that reasoning.

If we could hook up a turbine to the revolving door between the Fed and Wall Street, we could generate enough power to light up the whole East Coast.

http://www.businessinsider.com/stanley-fischer-on-revolving-door-between-wall-street-and-fed-2017-4

OK, I’m back from a six-hour blackout in my part of San Francisco. Beautiful day, sunny, calm… and then at a little after 9 am, everything stops. And forget the internet.

As we were trying to monger some rumors, we suspected Russian hackers, and then North Koreans hackers, but turns out, according to my battery-powered radio, it was a substation that experienced a “catastrophic failure” and apparently caught fire.

Stuff happens.

The server for this site is somewhere else. So that’s good, and WS remained up for those not tangled up in the blackout.

These blackouts should be cautionary tales for all those pushing the “cashless society” on the one hand and bitcoins as a store of one’s wealth on the other.

A reminder to one and all to stock up on the essentials and have a wad of cash on hand for when the lights do go out for more than a day or two.

A huge catastrophic solar flare like the one that hit in the 19th Century could wipe out our communication satellites and knock out power systems for months. It is not foolish to make provisions for your survival.

All right thinking Americans blame Putin for the blackout. Putin is also responsible for Bumgarner’s dirtbike injury, the movies “Gigli” and “Ishtar,” and the closure of Thrift Town.

and THE CLOSURE OF THRIFT TOWN!!!!!

hilarious/brilliant.

It’s Actually Much Worse, Wolf:

You see, since the last run-up in ’07, ETFs have become enormously more popular. And guess how many leveraged ones there are: LOTS. Furthermore, it is possible to get numerous offerings of 1.5, 2 & 3X leveraged versions. While not all brokers will do it, I have gotten an added 50% margin on some 3X ETFs (i.e. 6X total).

And some of that variety (such as VIX-related) really fly, at 3X, let alone 6X. Finally, I would imagine it is infinitely easier to get ‘shadow margin’ from many lenders who are not so scrupulous about the difference between un-leveraged ETFs and 3X versions.

Thus, I would not be surprised if, considering the ETF space as well, that the total borrowed on the whole shebang is over one Trillion Dollars!

This time is different…

A major cause of the 1929 Wall Street Crash was Penny Stocks being bought “On Margin”. Is History about to repeat itself. 2017 Wall Street tries every conceivable ,illegal Scam in the book, to increase “Yield” . “Any Gain Without Any Pain”.

Just before the tech crash in 2000, I was getting offers from day-trading outfits of $20,000, $30,000 to trade with. I know enough from dealing in electronic surplus that if you don’t know at least a fair amount about something, it’s better not to mess with it – or get it for free and even then, free stuff isn’t always free (like storage charges if it’s physical, price per trade even if the stock costs you nothing originally). I even had people around me saying day trading was great (guy at the hardware store lol) just like the old saying, “when your shoeshine boy gives you stock tips…”

Margins have been tightened since 1929… somewhat.

Regulation T has put margin requirement for margin stock purchases at 50%. This was in 1974, and the FRB hasn’t deemed necessary to change said requirement since despite having the authority to do so.

Back in the 20’s the margin requirement had to be “reasonable”: this was generally accepted to be between 30 and 40%, not very far from the 50% it has been for the past 40+ years.

As it always happens as the stock mania acquired a life of its own a number of brokers emerged catering to latecomers (today known as “retail investors” and less politely as “dumb money”) who creatively interpreted the “reasonable” part as being between 10 and 20%.

There are some parallels with the Shanghai and Shenzhen stock bursts in 2015 in that the latecomers took a similar well deserved beating through extreme margin calls which were used to buy stocks at extreme valuations. As usual extreme valuations mean that even if a stock drops 4-5% the buyer loses a lot of money. We all know how much Chinese stocks, especially the Shenzhen small caps which did not benefit from the plunge protection team and where most latecomers dabbled due to double digit weekly gains, truly lost that year.

The short of a lifetime, I am glad I didn’t miss that out as it’s most likely the last one I’ll see in my life.

Margin is important but so is the breath of the market move up. Last year (2016) only five stocks were said to have contributed to 81% of the Dow’s move up.

Anyone know where the margin debt is invested? Big vs small cap?

https://www.wsj.com/articles/the-five-stocks-that-are-driving-the-dow-dow-1478103925

Two of those companies (IBM and Caterpillar) have had declining sales and revenues for half a decade now, mostly due to being unable/unwilling to meet the challenges posed by more aggressive competitors, mostly, albeit not exclusively, from Eastern Asia.

If I look at brand new escavators, I see three Komatsu’s, four Kubota’s and two Doosan’s for every CAT. And honestly I cannot remember the last time somebody pitched to me an IBM product, hardware or software.

Speaking of where margin debt is used. I suspect the thing is cyclical.

The spurt in growth on the graphic for the last months of 2016 coincided with a boom in the Russell 2000, which far outpaced the S&P500.

In 2017 what even Nasdaq called “exorbitant valuations” in small caps, not to mention a marked decline in earnings for Russell 2000 companies (which wasn’t supposed to happen), drove enthusiasm back to big caps and this year the S&P500 is back on top of the game.

As margin debt has continued to soar even as attention shifted from small caps, I suspect small cap vs big cap is more rhetorical than anything.

“Earnings per Share” are very low across the board. but Share Prices are sky high. Companies buying their own shares is inflating the prices. This Price Rigging is passing the Regulators.

We are still in the Depression that began in 2000. All the rest is BS. “They” will keep juggling balls. The end is NOT near. This will go on and on and on. When the total debt is in the Quadrillion’s it will still be going on and the same folks will be calling the “end is nigh.”

It can’t continue forever. Pensions and SS have to be paid. Medicare has to be paid. Military has to be paid. There are tons of promises out there. Thus, there are clear time limits in place. The reckoning may not happen this year, but it surely will happen. Current status of ever-increasing debt is unsustainable.

The only way out is to re-balance wealth, which can be done through significantly higher taxes on wealthy or lowering of financial asset prices via higher interest rates. It’s clear that the other option – backdoor financial repression via ZIRP – isn’t going to work, because they’ve been trying that for many years without success. The wealthy folk and savers simply batten down the hatches spend less.

Everybody will suffer to some degree, but we would climb out of the hole eventually. Hopefully central bankers won’t be dragged by an F150 as part of this healing process.

One thing I keep wondering about is what the actual consequences of the central bankers’ doings will turn out to be. After all, the Fed, ECB, BoJ, PBOC et all have been doings things that were unhearad off before the first stage of the crisis and thus they apprently have managed to ( at least for some time on the surface) to neuter certain central rules of the economy. What happens when the CBs do not any longer manage to manipulate the economy and the genie escapes the bottle ? There will probably be awarded some future Nobel Awards in economy for explaining what really did happen … I don’t know what (or when) will happen, but my gut feeling is that it will be surprising, nasty and long lasting. One of the things that does cause me nasty foreboding is that most of the people handling trades haven’t any other experience than BTFD and add the algos into that soup, too …. Another thing I do wonder about is wether the pension systems in western Europe ( forget about the South and the UK ) will survive or wether the future will be similar to the US, ie a decent pension will be available for only the selected few, others will retire with their boots on …

“What happens when the CBs do not any longer manage to manipulate the economy and the genie escapes the bottle ?”

Currently watch Europe, Venezuela, and china for the eventual answer to that .

The FED is trying to shrink its balance sheet, and trying to reduce printing. So reducing excess printed cash in the system. So that America does not end up there.

Lets see if it will be allowed to complete the process. Or if the Socialists will demand more free free free for the masses of sanders supporting takers, and be bowed to.

d, please stop hating the poor. They are not the cause of the problems we are having now. Most of them work too. They give a great deal and take remarkably little. They are not the real takers.

“d, please stop hating the poor.”

You confuse reality.

With your own bias against of those who succeed and have.

Simple reality.

Socialism always fails, when it runs out of rich peoples money to steal.

Look at Venezuela. Classic corrupt Socialist failure.

Another “shoeshine boy” moment. These Millennial bagholders-to-be are going to be a cautionary tale.

http://www.businessinsider.com/snapchat-stock-td-ameritrade-trading-2017-4

The Keynesian fraudsters at the central banks have embarked on a “liquidity supernova” to keep their Ponzi markets levitated and defer the inevitable financial reckoning day. True price discovery, when it finally asserts itself, is going to be cataclysmic for all these central banker-blown asset bubbles.

http://www.reuters.com/article/markets-flows-baml-idUSL3N1HT3E0

“The American economy increasingly serves only a narrow part of society, and America’s national politics has failed to put the country back on track through honest, open, and transparent problem solving. Too many of America’s elites-among the super-rich, the CEOs, and many of my colleagues in academia-have abandoned a commitment to social responsibility. They chase wealth and power, the rest of society be damned.”

Jeffrey Sachs, The Price of Civilization, January 2012

Bobber. I am not picking a fight with your argument. However, people have been arguing about debt since the beginning of this country. WWII they worried about debt. The Korean War was off- balance sheet debt. Ergo, Nam. Ergo Iraq. This is never going away and the debt will keep on growing. There is NO other choice. The FeD will just keep adding to their ” balance sheet” ad infinitum. If we made it thru the Great Recession we will continue on and on. There is NO other choice. We will be arguing about this for the rest of our lives.

Real interest rates are key?

Once the Fed stops remitting excess liquidity premium from its bond operations to the treasury and instead has to defend said balance sheet, stuff might change?

Borrowing money to buy E.T.F.? (Another financial product which is open ended like a central bank balance sheet?)

The only thing closed in this set-up is the fire escapes?

The store can’t have burned down- I still own some shares!/sarc

I would collect those 3.25% interests and invest them in the stock market to drive prices ever higher. It is a perfect circular virtuous cycle that only ends in absolute infinity. 1/2 sarc

Bay Area jobs up 12000 month of March. Party keeps going.

You have to look at year-over-year changes to avoid the big seasonal effects. That said, employment is up YOY as well, just not nearly as much as before. In San Francisco, for example, the YOY change for March in employment look like this:

2012: +20,900

2013: +17,300

2014: +16,700

2015: +19,800

2016: +17,000

2017: +4,300

In other words, the YOY increase in employment in March plunged from something near 20,000 in the prior years to just 4,300. In fact, the March employment level is now below that of July last year!

I think a similar pattern is playing further south in Silicon Valley.

um, margin debt is useful if properly used.

but 50% leverage and air pockets don’t mix.

yes, arithmetic is important.