China Containerized Freight Index remains near record low.

Hanjin Shipping Co. filed for the equivalent of bankruptcy protection in South Korea on August 31 and over the past two weeks in the US and dozens of other countries. Some of its ships are still idling at sea, trying to out-wait the uncertainty, and being seized by creditors. Some have made it to port and are being unloaded. Others have already been sold at fire-sale prices.

When US Bankruptcy Judge John Sherwood asked Hanjin lawyer Ilana Volkov if the carrier was liquidating, she said: “There is no clear visibility yet on what will happen with this business.”

The seventh largest container carrier in the world is not the only carrier in financial trouble. Another huge Korean carrier, HMM, was restructured and bailed out earlier this year, with creditors, including the Korean taxpayer, taking a big hit. The state-owned Korean Development Bank is now its largest shareholder.

Whatever the company-specific reasons, the entire industry has been caught up in a collapse of the rates they charge to transport containers across the seas. This started in early 2015, as a result of a shipbuilding boom of historic proportions, fueled by cheap money, endless liquidity, yield-desperate investors, and over-optimistic projections of demand. It created a vast oversupply of container ships that will continue to get worse through 2017 as a slew of new ships, ordered years ago, are being delivered.

It coincided with lackluster demand for shipping goods, particularly a decline of exports from China (-1.8% in 2015) and South Korea (-5.1% in 2015).

Having acquired these ships with borrowed money, carriers are now weighed down by enormous amounts of debt, and when cash flow curdled, the math, which had been iffy before, no longer worked at all, turning some of these carriers into zombies.

But since Hanjin’s collapse, the meme has started to circulate that container shipping rates would soar, that Hanjin’s ships would be sidelined during peak shipping season and that shippers would have to scramble to find other carriers to transport their containers, and those carriers would jack up rates and get away with it.

That optimism may have been largely based on wishful thinking.

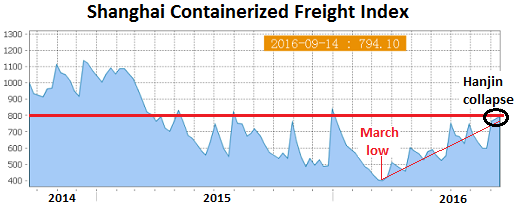

The Shanghai Containerized Freight Index (SCFI), which tracks only spot-market rates (not contractual rates) of shipping containers from Shanghai to 15 destinations around the world, had started plunging in February 2015. Carriers, desperate to get loads together, were accepting rates far below cost. Last March, there finally were rumors that some carriers quoted rates of “zero.”

At the time, we warned of Hanjin’s impending bailout or bankruptcy and, as I wrote, “the awkward side effect of stranded cargo.” The SCFI, which is very volatile, hit 415, down 62% from February 2015! But the “zero” rate rumors marked the low point of the rates.

In April, the SCFI began to zigzag higher, reaching a still unsustainably low 750 at the end of June, up 80% from the March low, before it plunged, jumped, dropped, and jumped again in its volatile spot-prices manner.

The chart of the SCFI shows this volatility. But during the first two complete reporting weeks since the Hanjin collapse, circled in black, the index has barely budged and is now at 794. It remains 28% lower than it had been in February 2015:

During the week, spot rates from Shanghai to the US West Coast dropped by $7 to $1,749 per FEU (40-foot equivalent unit container). Spot rates remained flat to the US East Coast and dropped to several other destinations, including an 8% plunge to South America. Rates increased significantly to the Mediterranean and South Africa. Rates to Europe edged up $23 to $966 per TEU (20-foot equivalent unit container). This is where the action has been. After bottoming out in March at a catastrophically low $211/TEU, rates to Europe have since soared 357%, most of it over the spring and summer, before the Hanjin collapse.

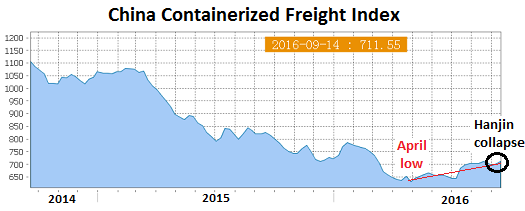

But the much broader, less volatile, and more indicative China Containerized Freight Index (CCFI), which tracks contractual and spot-market rates for shipping containers from all major ports in China to 14 regions around the world, hasn’t moved nearly as much. In April, it hit a record low of 636, down 41% from February 2015, and down 36% since its inception in 1998 when it was set at 1,000.

Then it began an upward trend. In the latest reporting week, it edged up 1.3% to 712, up only 12% from the April low, but still down 34% from February 2015, having barely budged since the Hanjin collapse, circled in black:

The fact that the CCFI failed to move vigorously since last March, despite the Hanjin collapse, shows that contractual rates are still bogged down. These rates are still way too low for carriers to survive. The collapse in oil prices in 2015 and early 2016 pushed down the price of bunker – the fuel large ships run on – a saving grace for the industry. But bunker prices have risen sharply recently, driving up costs.

And Hanjin’s ships aren’t going to evaporate to knock down capacity. The oldest ships might get scrapped. But the rest will continue to ply the routes, most likely under new ownership – some have already been acquired by other carriers.

That’s the problem with a glut: Bankruptcy removes neither the assets nor the capacity. It only changes their ownership and forces investors to accept big losses.

There may be a brief period of confusion and price spikes on some routes as shippers in peak season get desperate for their merchandise. But the glut of ships, in the face of weak demand, is such that the pain for carriers is likely to continue, with many more false-hope ups followed by brutal smack-downs, and with more carriers cracking under their debt.

There’s now a new and potentially lethal problem for weaker carriers: shippers, who’d counted on a bailout of Hanjin but got caught with their pants down when it didn’t happen, don’t want to see their merchandise get stranded again. So they’re scrutinizing carriers and will try to avoid those that don’t pass the smell test, which would only hasten their demise.

And creditors, who’ve learned from the Hanjin fiasco to not count on government bailouts of even the biggest carriers, are likely to try to protect their balance sheets more carefully. So they’ll pull back at the worst possible time, just when that carrier needs it the most. This is what caused Hanjin to keel over.

Hanjin’s bankruptcy “shatters the complacency” that too-big-to-fail carriers “are immune to failure.” Read… “Zombie Apocalypse”: The Hanjin Bailout that Didn’t Happen

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

This is what deflation looks like. Spending power has tanked, thanks to neo-liberal policies, and very likely will never recover, due to energy problems. So less goods, less containers. Who knows how far it will drop?

The floor could be very low.

Little off-topic but I do persist in adressing the QE/ZIRP/NIRP policy.

Sofar QE-Trickle Down has not worked a bit.

What it really does is creating escapes for companies.

In stead off investing the cheap money QE provides in real economy, motivated by a persistend lag of demand debs are merely serving take-overs and buyback of shares, manipulating sharevalue and -in the end- creating cartels.

How come Central Banks do not adress this (mis-)use of QE ?!

Little doubt in my mind that it was anything other than a snow job. So easy to put one over our incompetent politicians and the supine media. So instead of injecting directly into the economy, they gave it to the banks, who supposedly would spend into the economy. What a joke!

Here’s Kunstler on this topic;

http://kunstler.com/clusterfuck-nation/slowly-then-all-at-once/

It is because QE amounts to nothing more than having central banks provide (to the extent that the national debt can be jacked up) virtually interest-free money to the very banks that own them! We have arrived not at a time of crisis for them, but Nirvanah: the debt has grown so great that the mere thought of a rate rise inspires terror in the markets (talk about real terrorists, not the pipe-bomb type), and they are not only looking at continuing this run for as long as they can get away with it, but those banks get a two-fer in being able to deny savers any return whatsoever on the grounds that rates are so low.

Deflation is more buying power

If you have money any to spend

Deflation sounds OK if you don’t know the bankers secret.

Money and debt are opposite sides of the same coin.

If there is no debt there is no money.

Money is created by loans and destroyed by repayments of those loans.

From the BoE:

http://www.bankofengland.co.uk/publications/Documents/quarterlybulletin/2014/qb14q1prereleasemoneycreation.pdf

When a nation has been swamped with debt, the repayments become larger than new debt and the money supply starts to contract.

This contraction of the money supply makes it even harder to pay off the existing debt and you enter debt deflation and everything starts to spiral down.

The banker’s secret means nearly everyone comes to the wrong conclusions.

The banker’s secret remains secret to mainstream economist too, which is why they are so hopeless.

That BOE article has a CB opinion slant.

Money is destroyed, in their opinion, if debt is paid down.

As they support the system based on cheap credit.

When debt is paid down. Money is only destroyed, if the item purchased with the debt. Is worth less than the purchase price, otherwise the money is simply stored in the purchased item.

Money is also destroyed, in negative asset revaluations, and created in inflation of asset values. Particularly when the asset is purchased with credit.Then sold for a higher/lower price.

Money is also destroyed by NPL’S as the bank ends up with a hole in its balance sheet, that it has to write down, or replace with what would otherwise be profit.

The CB paper, is a paper in support of the credit based system.

That the credit based system, is the problem, the CB’S, deny.

Only a few people know this on the BoE web-site, they kept it very quiet.

I think the FED have quietly put something on their web-site too, though I haven’t looked.

The vast majority still haven’t got clue how money works including all mainstream economists.

“2008 – How did that happen?”

Steve Keen uses realistic assumptions on money and debt in his models.

He saw the private debt bubble inflating in 2005.

“When debt is paid down. Money is only destroyed, if the item purchased with the debt. Is worth less than the purchase price, otherwise the money is simply stored in the purchased item.”

True, but the money supply goes down as debt is repaid and goes up when loans are taken out.

If the asset, the loan is taken out on goes down in value enough, they can’t repossess it to get their money back. Money gets destroyed on bank balance sheets.

This is why bubbles are so dangerous, when they burst asset prices fall sharply shredding bank balance sheets.

When it’s a housing bubble, the debt is very large and is spread across the whole nation, when they burst there is hell to pay.

When the housing bubble is leveraged up with derivatives, you get 2008 type events.

From the BoE link:

“Although commercial banks create money through lending, they cannot do so freely without limit. Banks are limited in how much they can lend if they are to remain profitable in a competitive banking system.”

This statement is only true in a Glass-Steagall world.

When you can package up and sell off bad loans through the investment side of the business, banks can create money freely and without limit.

Look at the US money supply leading up to 2008 for confirmation.

NINJA mortgages only work when there is no Glass-Steagall.

Irving Fisher looked at the debt inflated asset bubble after the 1929 crash when ideas that markets reached stable equilibriums were beyond a joke.

Fisher developed a theory of economic crises called debt-deflation, which attributed the crises to the bursting of a credit bubble.

Hyman Minsky came up with “financial instability hypothesis” in 1974 and Steve Keen carries on with this work today.

Steve Keen saw the private debt bubble inflating in 2005. He had the right theory and it wasn’t a “black swan” to him.

In 2007 Ben Bernanke could see no problems ahead and his models didn’t include money and debt. He had the wrong theory.

The problems with austerity can only be understood if you know about money and what is happening to the money supply

Federal Debt injects currency into the economy. Commercial bank debts net to zero. Only the Federal Government can create money so in reality the Banks only create credit. “The Federal Reserve is the fiscal agent of the Treasury. Major outlays are paid from the Treasury’s general account at the Fed” this is from the Federal Reserve Act. It has no sovereign credit risk and there is no need for credit rating agencies to opine on the credit worthiness of sovereign debt.

Debt is future consumption denied, but no debt, no money.

The effect of Austerity is to put the Budget into surplus which drains savings in the private sphere and leads to recessions as the private sphere has to use its savings to fund the budget shortfall. An accounting identity.

Government deficits on the other hand add to non government savings, to the penny, and the economy is stimulated. Excess money in the economy is destroyed by taxes, therefore a lever against inflation.

“Commercial bank debts net to zero.”

NPL’S = LESS THAN Zero. A reduction in bank capital, and depositors fund’s.

The problem with Austerity is not, Savings, paying state debt, it is the reduction in untenable credit fueled State and Private spending. Combined with the paying back of part of the forward consumption debt. Currently estimated at a working lifetime( Which is why we have so many problems).

The problem with austerity, particularly in places like greece, is that the left will not let the process complete. So it drags on and on, then has to be repeated again, in the long term creating more distress than if the process was completed, then a new start made from that point.

The club med leftist, who claim they will undo the austerity, will simply make a bigger mess, and cause much more pain, long term.

Spaniards in particular with half a brain and a few Euros are fleeing Spain and the EU even to New Zealand, if they can get in (Those ones mostly spend some time in the UK first. As they see what the left will do and understand it can not work..

Let me repeat. Commercial bank debts net to zero. An accounting identity. I didn’t say it doesn’t have consequences. Bank loans use energy during their life. The accounting doesn’t address energy.

Here’s a video to explain it.

It comes from Richard Koo. Ben Bernanke read Richard Koo’s book and this is why the US didn’t implement austerity.

Imposing austerity in a balance sheet recession leads to debt deflation where everything just spirals down due to contraction of the money supply.

This is what happened to Greece.

https://www.youtube.com/watch?v=8YTyJzmiHGk

Ben Bernanke saved the US by understanding this.

Mr Koo’s talk is a valuable one as it explains a lot.

If only Mario Draghi would watch it before he destroys the Club-Med banking systems.

Though Richard Koo says he did give a presentation to the ECB and they just got in a huff rather than learning anything.

I found it on ZeroHedge and it filled in a lot of gaps.

I get the impression a lot of people don’t realise how significant it is ……. OR ……… just didn’t bother to watch it.

He just made one mistake that I could see. He said Governments [Federal ones!] borrow to fund their spending. They don’t – although they trick it up to look like they do, and they don’t spend their tax “revenue” either. That’s the privelege of being monetary sovereign.

” He said Governments [Federal ones!] borrow to fund their spending. They don’t – although they trick it up to look like they do….”

Haven’t finished watching the video yet.. but I’m a bit puzzeld with your remarks.

Can you elucidate what you think Governments borrow for?

And how do I understand ” they don’t spend their tax “revenue” either “

I doubt if he has got the data wrong on US bank balance sheets around the great depression.

Central Banks are a mystery and I think deliberately kept that way.

Someone else, who I also trust, said the ECB could have bailed out the Irish banking system but let taxpayers pick up the tab.

Here is a good basic video on US money:

https://www.hiddensecretsofmoney.com/videos/episode-4

Jim Rickards endorses it and he is pretty good.

Not 100% on the Ponzi collapse scenario ……. but maybe.

You are one of the few with some real idea about money, but Mike Malone is out of date. CB’s are deliberately obtuse and obscure, by design and yes, the ECB could have bailed out the Irish, and the Greeks, banking system, although they have made doing so tricky. The ECB is not fully sovereign.

What governments do is put projects out to tender and tenderers use commercial banks to fund them, sometimes in public/private partnerships.

So instead of buying the debt interest free the government lets the private sector do it all, and this adds enormously to the final tally, as Ellen Brown points out.

““Although commercial banks create money through lending, they cannot do so freely without limit. Banks are limited in how much they can lend if they are to remain profitable in a competitive banking system.”

This statement is only true in a Glass-Steagall world.”

\

Yes and it is also an ambiguous, pro bank’s, we are responsible people, banking statement.

Many Banks will create as much as they can get away with in a fractional reserve system as thats where they get their rent from the money they create as loans. It only becomes an issue when the economy tanks or their NPL level becomes to high, AK Italy.

The recapitalization of the EU banks, was, and still is needed, as the EU banks, created way to much money to garner rent from. Making them unstable.

Glass has to come back in some form, to bring any degree of safety to the private citicens banking system. In a big hit, FDIC will simply not be big enough, unless massive hyper inflation occurs afterwards, to inflate away the money printed to fund the FDIC payouts . Which makes FDIC effectively worthless medium and long term.

In the current environment the last place to have savings is a bank, as the second you give them your savings you become nothing but a small unsecured creditor. Even with national FDIC’S of various types, if your country still has one, ours no longer does…

There is no longer a Fractional Reserve System in banking. It’s pure Credit Creation now. Banks have no need for your deposits. They just have to show they are solvent.

And when you can buy from bankruptcy ships for cents on the dollar and incorporate the costs across your fleet, it often means that your break even over the medium term plunges and you can then push costs lower to force the next stinking pile of over leveraged crap onto the market through bankruptcy and pick up even more cents on the dollar ship.

rinse and repeat. He who dares wins

As it ever was, last man standing takes the biscuit.

You do know who the last men (not man) standing will be? They are called the Feds and their crony banks. Eventually they’ll just own everything.

This poster has it right.

The (simple, exponential debt based on renting a currency and never issuing the interest except as new loans) maths says that eventually the central banks will own _everything_.

They already own rather a lot of government (via bonds), companies (via shares and bonds) and real estate (via simple banking).

china intends to be the last man standing in this shipping glut.

It is why they are still supplying COSCO a chinese state owned shipping company with free super container carriers.

he who controlls the ships controls the trade.

Guarantee you ,the west dosent wake up until it is to late.

Bankruptcy only changes owners and forces investors to take losses.

It also means the new owners with low debt can offer lower prices than the old owners could, pushing prices lower and upping the squeeze on all other owners until the next indebted operator buckles.

Lower shipping volume also squeezes, but probably not as significant as the flood of new, more efficient ships, some of which are maximized for the increases Panama.

All the older companies without gov backing are going under.

Zero interest rates are deflationary because it has increases capital spending, oddly exactly what gov wanted. But higher rates cut real residential and auto spending… They’re in a box until they figure out people have to have money in their pocket before they can spend.

“They’re in a box until they figure out people have to have money in their pocket before they can spend”

and that’s the ussie right there, i know i don’t have anything to spend.

i heard some jackass talking head say that the reason for no demand was that Americans aren’t borrowing enough……what a f’ing moron.

not one mention of income.

This is what Henry Flagler and J. D. Rockefeller did so well.

Standard Oil did not have a choice in forming a monopoly, Neither did J.P. Morgan when he created US Steel. They had to.

When separate companies, in the same business, do their “own thing”, capacity will increase, profits decrease and the newer firms have lower overhead (everything they bought, steel, rail, freight cars, etc are cheaper than the previous firm). Thus, competitive capitalism can only kill itself.

“Competition is a Crime”…John Davidson Rockefeller.

So, their are only 2 solutions:

1) is Monopoly,……….either Private Capitalist Monopoly (Standard Oil) or Private State Permited Monopoly (fascism) or State Owned Monopoly, Capitalism.

2) Permit private free enterprise bankruptcy. This will teach business owners, investors, etc., to NOT USE DEBT in creating or expanding their chosen industry. Use your own capital and that of your partners. Re-invest your profits and thus never fear bankruptcy (as in Andrew Carnegie’s method. His partners HATED this, but since he owned 51%, he had control and was smart enough to keep driving costs down and don’t borrow). Borrow prudently.

YOU Are so wrong. In a capitalistic free market economy. It works best when their are MANY buyers and sellers. This leads to stable prices and the variable is quality and service. When other companies move in to take over competitors they achieve an economy of scale for a while. This leads to a lower price, only through economies of scale. But when the companies use debt to acquire competitors to reduce competition and lower prices, it is only temporary. We have seen this in last 10yrs with cable tv, cell phone service, health care insurers, pharmaciticals. And many others. The Sherman Anti-trust law is now being reviewed for dozens of “oligapoly” and “monopoly” style mergers we are seeing in the current period. The massive “Monsanto” is the 1st to come to mind but their are dozens of multi-national combinations currently under federal anti-trust review.

“That’s the problem with a glut: Bankruptcy removes neither the assets nor the capacity.”

Not necessarily. It depends on the nature of the firm, the nature of the assets, and the terms of the bankruptcy. In some cases the assets are merely scrapped. A lot of horses went to the glue factory when autos became affordable. Container ships are not horses, of course, but ships sometimes do get beached in India to get broken up, although maybe not Hanjin’s.

‘Hanjin’s bankruptcy “shatters the complacency” that too-big-to-fail carriers “are immune to failure.”’

Shumpeter might quite naturally surmise that this is a good thing, even a necessary thing. But no enterprise should be TBTF, which allows such firms to blackmail governments into protecting their economies by resorting to unShumpeterian bailouts, externalizing their risks and socializing their losses. Such situations amount to a corruption of the capitalist system and are piratical, enable gross moral hazards, and force unnecessary economic destruction.

It would seem Hanjin rode the bubble up and are now following the bubble down because the greed of its leaders too far exceeded their wisdom. Let Hanjin go down, I say, and serve as a warning to the others.

Walter – I agree.

What is needed is some good old fashioned “creative destruction” throughout the global economy.

The economic deadwood left over from the dot com bust, is mostly still floating around in one form or other. Unable to wash out of the system because of Greenspan’s ultra low rate adjustments. Which only blew an even bigger real estate bubble!

Again, because of the too big to fail mentality, TPTB let the deadwood drift around in the economy infecting all levels credit. What is drastically needed is an economic washout (or enema) of the system if it is to survive.

Hanjin is discovering the first rule of economics, which states that; ‘All debt will be paid. Either with dollars worth pennies, or with pennies worth dollars’. Some of their ships being sold for pennies on the dollar? So be it!

” What is needed is some good old fashioned “creative destruction” throughout the global economy. ”

BE CAREFUL WHAT YOU WISH FOR. This time, the next or coming time will be beyond your comprehension thanks to globalism. A category 7 or 8 might be close.

Too many companies are kept a float with cheap CB money. No incentive to reinvent eventhough their market is stalling if not downright dead.

To survive they turn to buyback and takeovers.

M I

Not a matter of “wishing” in the least.

Economic Mother Nature will have her way.

As to comprehending malinvestment, hubris, corruption and criminality, in the global market place – what is to comprehend?

The storm still rages with the intensity rising.

When you can buy ships for cents on the dollar the old ships of the fleet get retired. You get scrap money for them. The newer Hanjin ships replace the old scrapers. They’ll be volatility sure. If there is still too much capacity in the worldwide fleet, we’ll rinse and repeat until the fleet shrinks in capacity until stable shipping rates return.

We’ve seen this across so many industries that its comical that we all don’t see what’s going on. Coal companies have gone BK as have gold companies. The cheap low cost QE loans have caused a deflationary epoch. We are now working through that over supply across many commodities/ industries. Not unlike the over supply in the gold market where prices fell from $1900 to $1050. We are now on the inflationary bust rebound, Yellen frets about jacking up rates, yet the US bond market is going to help out (LOL). The long end is going to raise rates up so fast that when Fed try to roll over maturing debt, the new higher interest rates will be crippling (higher) interest rates for governments. It is then that the denouement of the clothe-less emperors will be revealed with Venezuelan style inflation rates. This is going to get ugly across the board..

Hanjin’s container carriers constitute about 3% of the capacity available worldwide.

Presently 5.3% of the worldwide container capacity is idled. Here I must make a difference: idled ships are merely taken off trade routes and moored at a convenient location with a crew tasked with maintaining the ship ready to sail on a 24 hours notice. Mothballed ships are moored indefinitely, often have no crew on board and may take months to be put back in service: more often than not mothballing a ship is just a convenient way to delay sending her to be broken up in Pakistan.

In short it would take about 24 hours to undo the loss of capacity brought about by the Hanjin bankruptcy, if need be.

And there’s another twist in the story: most shipping companies right now have adopted the practice of “slow steaming” to keep their ships moving (and hence the customers paying) as long as possible.

Officially the practice is used to “save fuel” but the three largest manufacturers of large displacement marine two stroke diesel engines (Wartsila of Finland, MAN of Germany and Mitsubishi of Japan) have issued a number of joint statements warning against the practice as their engines are designed to work very specific speeds. Slow steaming may save a tiny bit of fuel but this is more than offset by accelerated engine wear: as these enormous two stroke diesels are designed and built to last the life of the ship, saving a few tons of bunker fuel a day is just not worth it. Yet it’s a risk shipping companies feel worth taking: that’s beyond desperate.

Informative- coincidentally or not. even the two stroke outboard is not happy at low RPM.

These are slow speed diesel two stroke engines which… work in pretty different fashion from both Otto cycle two stroke’s and Diesel cycle four stroke’s.

While each engine is pretty much taylored to the ship class it’s installed on, we can generally say that a slow speed two stroke diesel achieves maximum efficiency around 80% of load, with said efficiency dramatically dropping off over 85% and under 70%.

The chief problems caused by slow steaming are improper combustion due to reduced air flow from turbochargers (leading to more deposits) and increased cylinder liner wear (these huge engines use hydrodynamic, not boundary lubrication, meaning there always need to be a thick film of lubricant between moving parts).

All of this is perfectly known in the industry, of course. MAN has attempted introducing some technical features to reduce the damages of slow steaming, but as good as their engineers are, they are still constrained by the laws of physics.

Re: ‘slow steaming to keep customer paying’

Surely the customer is paying a fixed amount?

My only experience with an international 20 footer it was fixed, not variable re: time.

However once unloaded it was a daily charge to have your container on the dock, so we hurried get it unloaded.

It really depends on how big you are.

For most of us fixed rates on a given route (Yokohama-Hamburg, Shanghai-Oakland etc) are the normal because we think and work in terms of under a dozen containers a pop but some contracts, especially very large ones, are day-based. Beforehand it’s negotiated how long a ship will spend in transit: generally speaking due to the aforementioned engine efficiency speed tends to be more or less the same but some lines may offer some discounts or special conditions if the customer accepts slow steaming. Always remember ships degrade more rapidly by staying moored than moving around.

MC

It matters little as to how large the size of #Hanjin ‘s fleet. No one will be able to put Humpty Dumpty back on the wall.

See this insightful piece of scrapping ships because of obsolescence. All the Panamax fleet is doomed no matter its current age..

http://gcaptain.com/10-year-old-panamax-becomes-youngest-containership-ever-sold-for-scrap/

10 Year Old Panamax is being sent to the scrappers!

There will be more ships sent to the scrappers (or whole companies) that go bust .. Rinse and repeat Hanjin till the market is in balance..

The above is factual. This process of “Creative destruction” will continue until the entire commodity sector is purged of its low cost loan excesses..

And Maersk I believe has ordered a bunch of even bigger container ships.

I wonder if they would have done that if they’d known that Hanjin’s would be available for pennies on the dollar?

Just yesterday I was reading how cargo airlines have started mothballing parts of their fleets, starting obviously from the older aircraft (less efficient engines) such as the old Boeing 747-200F. Recently 26 of these four engine aircraft were parked at the Oscoda Airport, raising planewatchers’ curiosity.

This is odd behavior as we are getting close to Christmas shopping season, when cargo airlines are usually the busiest shipping consumer goods from the Far East to the US and Europe.

That worldwide trade has slowed down is now obvious to most, albeit this is of the “slow and barely noticeable but steady” nature instead of the “the sky is falling in on me” variety. In short the slowdown in trade alone is nowhere near enough to explain the mothballing of such large numbers of cargo aircraft.

Overcapacity is surely part of the problem: not only has Boeing (Airbus plays second fiddle in the cargo market) flooded the market with cargo versions of their fuel efficient airliners such as the 777, but conversions of older passenger aircraft are cheap enough to make them worthwhile and former Soviet manufacturers are back on the market.

As many readers here have at least some corporate experience, it won’t surprise anybody saying cargo airlines, just like container and bulk lines, have been obsessed with the growth of the Asian trade for years now, so much CEO’s have lived in fear of being “left behind”.

Thanks to financial repression this meant many carriers, both air and sea, heavily invested in capacity, especially long range, high capacity ones such as the New Panamax container ships and Boeing 747-400F cargo aircraft. Let’s talk money now.

A Maersk Triple E container carrier cost the Danish company US $185 million a piece.

A Boeing 747-400F cost about US $300 million when new. It has now been replaced by the 747-8F which is far more fuel efficient but also far more expensive at US $360 million a piece.

And those are just the naked costs, which do not include hiring, training and qualifying personnel, maintenance, fees, debt servicing etc.

Due to stiff competition, many carriers have pretty much operated at cost for years now. This left them particularly vulnerable to any turbulence in the market.

In the container and bulk business, this was the meteoric rise of COSCO, the State-owned Chinese shipping company, which is geared to operate at a loss as its goal is not to make money, but to promote China’s exports and provide work for her shipyards.

In the cargo airline business this was, ironically enough, the downward pressure on ticket prices on the European and Asian markets, which pushed airlines such as Lufthansa to invest heavily more in the (then) lucrative cargo business.

In such conditions we are bound to see a whole lot more Hanjin’s happen: despite the mad scramble for yield and Draghi and Kuroda threatening lower interest rates, today is as good as it’s going to get. Plainly put if bond yields, investment grade or junk, go any lower the whole security markets worldwide will roll over and die like they are doing in Europe.

The Boeing 747 is truly a work engineering genius! It has been in operation for 47 years, and is testament to making machines properly that stand the test of time. Porsche 911 is also an example of this.

Ironically enough the 747 was designed as a widebody because it was felt to be an interim type: at the type SST was still all the rage and it was felt the 747 would eventually be relegated to the air freighter role.

The distinctive “hump” was part of this, as Boeing felt there was need for a tilt up nose for cargo loading and Pan Am suggested a hump could be added to provide a dedicated first class area.

While there was a lot of interest for a 747 freighter right away, the original engines used on the -100 series were simply not up to the task and hence airlines had to wait a few years formore powerful engines to be introduced on the -200 series.

While the 747 has a well deserved reputation as an airliner, Boeing showed incredible prescience in designing it right away for the freighter role. It’s as a cargo that the 747 won its wings and made Boeing a nice profit.

While many outfits offer passenger to freighter conversions, those offered directly by Boeing are intriguingly enough performed by two “partners”, one in Taiwan and the other in mainland China.

The bittersweet irony…

Is there any news on car containers?

These are the huge floating multi-storey car-parks that trawl the trade routes moving cars from country to country.

I.e. like the Hoegh Shanghai etc.

As inequality rises demand collapses.

The majority are impoverished and a few become fabulously wealthy.

It was obvious really, if anyone thought about it.

How can creditors seize ships and others sold when under US, international and maritime law it is prohibitive when in bankruptcy?

US law does not apply outside the US.

There is no ‘international law’ in business- the only international laws are like those regarding conduct in war etc. e.g. the Hague Conventions, which many including the US violate. (Under the Hague Convention an occupying power is responsible for law and order; the US failed to do this in Iraq, and its unique museum of early artifacts was among the many looted)

There is no ‘maritime law’ that would apply to ship seizure. There is no extra-national authority that would make or enforce such law. Note the multiple claims of sovereignty in the China sea- whose law applies?

The so-called Law of the Sea is happily a widely respected code of conduct about helping a ship in distress. It is not a law for which you could be brought before an international court, but you might be brought before a national court.

The Hanjin mess is being cleared up by an injection of money- the SK government has said publicly it is very unhappy with Hanjin Group for letting the shipping subsidiary go bust in mid-ocean. We can only imagine what it said privately. One result apart from money is an apology from Hanjin Group.

It sounds like you yearn for a sort of supra-national governance- at least in matters concerning all things maritime. That is a laudable sentiment but it can only be achieved by international treaty, which would have the power to overrule local courts.

You won’t have to look far for opposition.

If you read the book “The Box” by Marc Levinson it will give you the entire rundown on the history of the industry. Interestingly enough I have asked most of the top management of liner companies if they have read it and I almost always get a blank stare back. Container shipping has been a boom and bust business since its inception. The father of container shipping, Malcolm McLean went bust with US Lines in the 80’s. Todays liner shipping companies are run by managers who have no clue about running a business and in many cases no knowledge of the history of their industry. The industry is corrupted by a “Herd Mentality”. Despite years and years of literally having the ability to print money vis a vis conferences, talking groups, legalized price fixing, collusion, and the ability to tack on accessorial charges (that may or may not reflect real costs…read the old RRS “Revenue Recovery Surcharge” of the 80’s) they can’t make a go of it. Something is seriously wrong and its not going to get any better anytime soon. The Baltic Dry, The SCFI, all show that we are in a deep trough for the business. Yet liner companies go on and on ordering bigger and bigger ships. Most likely Maersk will come out as the clear winner (as they usually do). The rest are like ducks following the Maersk mother. NVOCCs have long take the lions share of revenues while owning no assets. Liner companies have created adversarial relationships with customers, NVOCCS, and everyone else with their hubris. Most of these carriers have sold off their offices, port operations, intermodal companies, trucking companies, logistics companies, and etc. just to stay alive. The well is almost dry for most. It will be interesting to see who survives.

Thanks for the heads up about that book.

As usual reading suggestions by people are here are extremely useful.

Yes this is an excellent work. Its funny how most folks are not aware of how the business started. By that I mean folks in the business.

At least Retail’s Q4 earnings call reports can scapegoat Hanjin as a factor for declining sales. “We didn’t get our merchandise in time.”

The Weather excuse was getting old. “Too cold for people to shop or too warm for them to buy coats.”

I am betting we will see Hanjin mentioned (or at least “supply disruption”) in at least 60% of earnings calls. Can’t wait to read them.

I perused an upscale boutique liquidation sale last week. They had plenty of merchandise to liquidate. The sale had been ongoing for a week before I gave in and took a look. The place was busy but it was easy to see why they were closing. How many pairs of expensive jeans and white tee shirts can you buy?

A few days before, I had stopped at a thrift shop and there was a big sign out front that they were not accepting clothing donations. This place has a lot of clothing a family on a budget would buy, lots of kids clothes, jeans, and tee shirts, as well as nicer stuff. Looks like demand is dead all over the place.

Inequality killed demand.

Debt papered over the cracks for a while but now everyone is just making repayments on that debt.

You are so right.

My daughter loves this “Justice” brand…..BUT, my wife has realized the local consignment shops are loaded with this brand. Luckily for me, my daughter has no problem with consignment clothes since the Wife and I have tricked her…….shop here and you get “tons” of Justice jeans and shirts OR you get one, or two, at that boring Mall………….(I’m going to hate this when she gets a little older and she realizes the “consignment” store is NOT the Mall…..Dad will have hell to pay……………)

Give her a set amount to spend on shopping and you will be surprised how cheap these kids get when its their money they have to spend.

No Debt

No Bankruptcy

Not really. You still have no protection from predatory pricing of necessities, like food and utilities.

I read of story on Drudge yesterday about a condo in Maryland where the paying owners are being put into foreclosure by the ones that are already defaulting.

Condos from the 60s and 70s that should have been demolished already. Those common area fees were what I would expect from a new posh condo with a doorman….not a rundown leaking, rat hole. How can they pay $550 for common area fees???

The condo model can only work in Manhattan, DC, and SF. Here in Dallas area some of these upscale condos already have Section 8 living in them. Boy, would I be pissed.

DO NOT BUY CONDOS unless you can buy 51% of the complex to control the HOA and at 10%-30% of market value.

As an investment, Condos suck.

In good times you have to compete with brand new complexes with FULL-TIME PROFESSIONAL sales staffs, all the latest bells and whistles and artificially low HOA dues.

In bad times there is really very little difference between units and the most desperate owner(s) set the market price.

In between you run the risk of losing FHA financing if the percentage of renters gets above 50% , AND YOU CAN LOSE YOUR ABILITY TO RENT YOUR UNIT if the condo board decides UNILATERALLY to restrict rentals.

In addition to all of the financial problems, you lose a LOT of freedom.

In contrast, if you are renting, you can move relatively easily and inexpensively to a better complex, a better area, better schools, closer to a new job, or even to a new city for a new relationship or a better job.

IN MOST CITIES CONDOS ARE A TRAP. DON’T BE THE SUCKER.

ONLY a fool buys a condo. These condo owners are getting what they deserve since they entered a “communist”/ “socialist”/”we are all equal” BS deal when they bought the “communal” BS called a CONDO.

NEVER BUY A CONDO. EVER.

I agree with you, but in Florida almost all houses are in some HOA, so you can’t get away from it. These associations are one of the biggest wealth extractors in existence. The insiders take over the HOA and give all the contracts to their buddies.

“our incompetent politicians and the supine media.”

So many people still cannot comprehend how wrong this assumption is, which is why we’re still where we are today..

I assume you mean the politicians know what they do?

If that is a correct assumption, then it is positively evil. See also my link to Kunstler above.

Typo to be corrected: Rates to the US West Coast are per 40′ container, not per TEU/20′ container.

Ooops. Thanks. Fixed.

Wolf’s article is very timely. Headline from the JOC which is the best known source of shipping news.

“Overcapacity expected to plague container lines for years”

On a positive note…..seems there will plenty of empty Hanjin containers available for those who support the Tiny House and recycling movement. Hooverville here we come.

http://fortune.com/2016/09/14/hanjin-shipping-trailer-shortage/

Good article. Well done. There are several factors which have lead to this over capacity in the container shipping industry. The top 3 carriers control 40% of global capacity. In addition, once the new alliances are in place next year the two largest alliances made up of seven carriers will control 70%. It has been years in the making. Maersk and MSC the No. 1 and No. 2 carriers have been growing services and market share for years. Others had to follow to keep up. The ultra large container ships are the problem. Only the fittest will survive, and global shipping will become an oligopoly.