Record moneys suddenly pile into the material of debt crises.

The Institute of International Finance opined last week that “the ‘low for long’ interest rate outlook now looks more like ‘low forever’ – an outcome that has unleashed a powerful renewed search for yield.”

They’re all doing it.

Japanese investors, such as pension funds and insurance companies, are swarming into US Treasuries now more than ever.

According to the Ministry of Finance, for the week ended July 16, Japanese investors bought a net ¥1.718 trillion ($16.2 billion) of foreign “long-term” debt (everything except “short-term” debt). The week before, they’d bought a net ¥2.55 trillion, the highest on record. And according to the MOF, they were mostly buying US Treasuries.

For them it makes sense: the 10-year punishment yield of the Japanese Government Bond is a negative -0.22%. But the 10-year Treasury yield is still a positive 1.57%. And with the Bank of Japan being outspoken about wanting to crush the yen, the hapless Japanese have even more reason to seek refuge in US paper. We can’t blame them.

Europeans are doing the same thing, buying US Treasuries, but also US corporate bonds, and even US junk bonds.

“NIRP refugees” we’ve come to call them. They’re trying to escape their central bank’s iron-fisted financial repression where bond buyers are guaranteed to lose money if they hold bonds to maturity, which many institutional investors need to do – such as pension funds and insurance companies. It impacts everyone since they’re managing the money of regular folks.

Over $12 trillion of bonds are trading with punishment yields these days. So investors are chasing positive yield where they can, thereby transferring the effects of central-bank policies from their bailiwicks to the US, and in turn pushing down yields in the US.

But where do American investors go to chase yield, now that Treasury yields are disappearing before their very eyes?

Junk bonds. And they have soared, and yields have plunged over the past few months.

And dividend stocks. Even classic bond buyers are switching to stocks that pay a dividend, to get a little extra yield. But companies can eliminate dividends in no time, and the yield goes to zero while the stock dives. A bond would be in default if the issuer were to stop paying the coupon. By that time, bankruptcy lawyers are circling. But cutting a dividend is routinely done during market downturns, and yield investors who switched from bonds to dividend stocks have a rude awakening.

And now everyone has rediscovered another source of yield. The Financial Times, about what happened over the past two weeks:

Investors are piling into emerging market bond funds at the fastest pace on record as pension funds, sovereign wealth funds, and other big institutions follow more seasoned specialists into riskier asset classes in search of yield.

“This is capitulation,” Sergio Trigo Paz, head of EM fixed income portfolio management at BlackRock, told the Financial Times. “The big, big investors are starting to move.”

More comprehensive data from the Institute of International Finance show that last week, cross-border flows to EM stocks and bonds hit their highest level since the US Federal Reserve shocked markets by pulling back from a rise in interest rates in September 2013.

The governments of these emerging markets have obliged, issuing, according to Dealogic, nearly $100 billion in foreign-currency-denominated bonds so far this year, the most on record and well ahead of the prior record for this time of the year, of €80 billion in 2014.

Foreign-currency denominated EM bonds are the material that debt crises are made of, including the 1994 Tequila Crisis in Mexico, the 1997 Asian Financial Crisis, which then triggered the Samba Effect in Brazil and the 1998 Russian Financial Crisis, followed by Argentina’s default…. But people forget.

Foreign-currency denominated EM bonds are devilishly risky, for issuers and investors. Why do governments issue them? Because these bonds are much cheaper than bonds in their own wobbly currencies. Why do investors buy them? Because they’re chasing yield, a tiny bit of extra yield, in exchange for a lot of extra risk. It’s a match made in heaven.

And now they’re hotter than ever.

“Especially eye-catching are recent flows into exchange traded funds,” the Financial Times explained. So far this year, $8.3 billion have been shuffled into EM bond ETFs, “more than two and a half times the amount at the same time last year.” In just the first two weeks of July, BlackRock’s EM bond ETFs pulled in $1.5 billion!

“An individual investor might not realize it – but by buying these funds, he’s risking his life’s earnings on the governments of Brazil and Russia, among others,” wrote Steve Sjuggerud, at Daily Wealth:

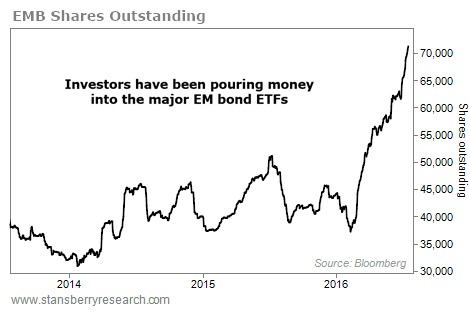

The benefit is dubious. The largest emerging market bond ETF pays less than 5% interest. Five percent! Meanwhile, the price of this ETF could easily fall 5% in less than a week – wiping out a whole year’s worth of interest.

He added this chart of the largest EM bond ETF, the iShares JPMorgan USD Emerging Markets Bond Fund (EMB), whose shares outstanding have skyrocketed as investors chased after EM-bond bliss by buying its shares:

These kinds of exponential spikes cannot go on. They will end. And they will reverse. When funds begin flowing out of emerging markets, as the risks become apparent once again, that’s when crisis-talk suddenly graces the headlines, while the IMF begins circling these countries.

And investors who chased yield this far and got in late, especially in bond mutual funds and ETFs, are going to pay the price. Chasing yield, especially late in the game, is one of the more costly forms of excitement.

In the US, many companies are buckling under their debts in an environment of slack demand and declining sales, as the noose tightens one by one. Read… US Credit Conditions Drop to Worst Level since Q3 2009, Markets Soar

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I haven’t reinvested any bond principal or interest since last October.

My guess is that I’m just going to keep any extra cash in an ultra low-yield short-term US government securities fund.

At age 64, I’m probably not going to get a second chance if my principal is annihilated by bond defaults or stock market crashes.

The problem with central-banker-created asset inflation is that when asset prices plunge, the corresponding debt that underpins those asset prices is still payable in full.

As far as I’m concerned, the world’s central bankers can go perform some anatomically impossible sex acts upon themselves.

I was wondering why the South African Rand was strengthening the last few weeks against the US$ and the €.

The “experts” on financial web sites have all kinds of reasons. These are btw the same “experts” who did not see the financial crisis coming and don’t know how to solve it.

But now I understand. Thanks.

Good job, Wolf! This makes sense.

A G20 IMF staff note:

Role of the SDR – Initial Considerations. (BullionStar)

Jim Rickards (via a tweet) said, “the IMF just fired a cruise missile at the dollar”.

Just announced by China that it will accelerate, borrowing in SDR-denominated bonds. This is in advance of the Yuan being accepted into the SDR basket of currencies this October.

1998 – Wall street banks backstop the derivative market which was in the process of meltdown because of the failure of LTCM.

2008 – Washington and the US taxpayer bailout Wall street banks and backstop many with liquidity lines.

2016? – 17? Who’s left with a clear balance sheet to bail out the underwater ($17 trillion of negative rate bonds) global governments?

Looks like ONE MORE TIME, only this time with gusto! The IMF with the SDR seems to be the new show in town, to prop up and continue the same old, same old. And the band played on….

Google Tuna Bonds from Mozambique

I’ll give people a quick roundup.

In 2013 Ematum, the Mozambique State-owned tuna fishing company, issued US $850 million worth 2020 maturing bonds yielding 6.3%. On paper it looked like a good deal and foreign investors, driven to insanity by the quest for yield, scooped it up: after all tuna is a white commodity and until captive breeding will become commercially feasible prices will remian high.

Small problem: it transpired this was actually a disguised sovereign bond issue. Maputo pocketed half billion and only $350 million arrived on Ematum’s books.

Earlier this year the government offered to swap Ematum bonds for US dollar denominated treasuries, finally dropping the charade. I hope investors have noticed since the beginning of the year the metical has lost over 30% against the US dollar…

Ah, the old ‘bait and switch’ sales job. In a non-regulated environment no less. What could go wrong?

It actually gets better, if this is possible.

After being caught red-handed Maputo stated they used that cool half billion to buy “maritime surveillance equipment”, like this is an excuse people would somehow buy.

The PR genius behind this probably forgot those buying high yield bonds don’t care if the money raised goes towards building orphanages or turning orphans into dog food: they just want the yield to appear on their bank account when it comes due.

With the metical in free fall against the US dollar everybody involved is looking every bit as bad as he deserves.

Anyone who doesn’t stop reading the offer after the word Mozambique does not merit the description ‘investor’

It seems you did not receive the memo.

The Party has decreed everybody who ever bought stocks, bonds, IOU’s, shares in a pyramid scheme and toilet paper is to be referred to as an “investor” henceforth.

You got wiped out during the Asian crisis or bet oil would hit $150/barrel by the end of 2008? No problem, you qualify.

You got sucked into one of the many housing bubbles fueled by shady characters originating from China? You qualify.

You bought Ferrari stocks and was sure Twitter would turn a profit as large as Apple’s by the end of 2014? Welcome aboard!

And everyone with dough in some protection racket captive bid pension fund, that will ultimately be scooped by Sam Zell or some other Wall St. raider, is an Investor! Thrown under the bus? You’re and investor! Bus tire tread marks up and down front and back are the returns.

There is too much investment capital at the top and they use NIRP to try and keep the stuff away before they are deluged with the stuff.

There is not enough money at the bottom to spur demand so there is nowhere to invest.

Inequality at work.

I think this why they used to have re-distribution through taxation.

When all these risky investments blow up, the wealthy might remember.

Anytime investors buy assets denominated in other currencies,there is a currency component to the transaction.In order to buy US Treasury bonds ,Europeans need to sell Euros and buy dollars.Buying dollars will strengthen the dollar and weaken the Euro.This in turn will make it make it more difficult for US exporters to sell their goods because their prices will go up in Euro terms.

Some years ago, before the financial crisis, I toured an old South Carolina plantation house. It was beautiful. During the tour it hit me that all that beauty and wealth was made possible by an unsustainable system of misery and oppression.

I have the same feeling today. It can’t last and it won’t. The elite political and financial system is based on criminality and fraud. The foundations are being rattled on every front. I think our grandchildren will be walking through what we consider the corridors of power and shaking their heads.

That happened a long time ago, the modern version uses children in “developing” countries and there’s the argument plantation owners were actually pretty good to the slaves. Yes of course there were those who treated them poorly, and life was much tougher back then.

The slave owners argued that they treated their workers better because they owned their workers rather than renting them.

Wage labour (renting labour) was pretty tough then too.

Firstly, slavery is an evil institution and cannot be defended, no matter the argument. It hurts my brain that I even have to defend the opposition to it.

Secondly, a system that worships profit as religion is equally evil. The people who continue to “invest” in the rigged system are perpetuating the fraud. Riding the wave is the same as endorsing the criminality and the fraud. If you don’t care, at least stop complaining about it.

Looking at the EU, Japan, emerging markets, and of course the US it would appear central bankers have tried (and failed) to ‘stimulate demand’ overall.

Except consumers in certain countries have gorged themselves on cheaper long-term debt.

How do we -CAN we – ever return interest rates to a more ‘normal’ level commensurate with risks, and inflation?

No, I am not buying any long term bonds. Just sold the last of them for a juicy near 20% gain.

Money just doesn’t have much value these days.

The calm before the storm. Was listening to the news driving into the Guitar this morning, and they were saying that the economy was finally firming up. I just burst out laughing. The read Michael Moore’s piece about how Trump is going to win. Listening to him preaching to the choir about The Last Stand of the Angry White Man reminds me of religious conservatives waxing rhapsodic about what MUST be going through an atheist. The point is Moore’s mind cannot wrap around the philosophical system that founded this country. But ignore that! The KIDS are throwing a tantrum.

I wonder what’s going through the minds of religious conservatives at Trump’s selection to bridge the gap ( canyon) to them: Paula White a prosperity preacher who will sell you a resurrection blanket for $1140

Dear Wolf,

Thank you for being one of the few lone-wolf voices out there in “finacial-mania la-la land” giving us insight into “the institutional matrix” that is gobbling up our economic reality without us knowing it. It is a wonderful breath of fresh air.

I have followed your columns on a semi-regular basis for about a year and have been quite impressed with the high intelligence level of those that comment on your published articles compared to other financial websites. This alone is a commendation and testimony to your fine work.