In War for Market Share with US shale oil.

Mayhem has crisscrossed the global oil markets since 2014: Huge losses for Big Oil, including teetering, over-indebted, state-owned giants like Mexico’s Pemex and Brazil’s Petrobras; bankruptcies among some of the smaller players; cuts in production in the US, Canada, and China where production plunged 7.3% in May from a year ago, the biggest decline since February 2001; hundreds of thousands of people losing their jobs across the globe; deep trouble in Brazil, chaos in Venezuela….

Record levels of crude oil stocks have become a global phenomenon. In the US, crude oil stocks are at 532 million barrels, a record for this time of the year in EIA’s data series going back 80 years. Even driving season has barely made a dent so far; stocks remain 63.6 million barrels above the mega-record levels a year ago. Gasoline and distillate stocks are 19.2 million and 18.6 million barrels above their levels a year ago.

Oil tankers full of crude are lined up outside the port of Singapore and others, some waiting to unload cargo, others being used for crude oil storage at sea. Across OPEC, storage levels of petroleum products rose to 3,046 million barrels in April, or 13% above the five-year average.

The world is awash in oil.

In the process, OPEC has been declared dead or dying because it was unable to agree on anything, refused to cut production, and brushed off calls to do something, for crying out loud, about the collapsed prices — which, despite the mega-rally, remain down over 50% from where they’d been before the oil bust began.

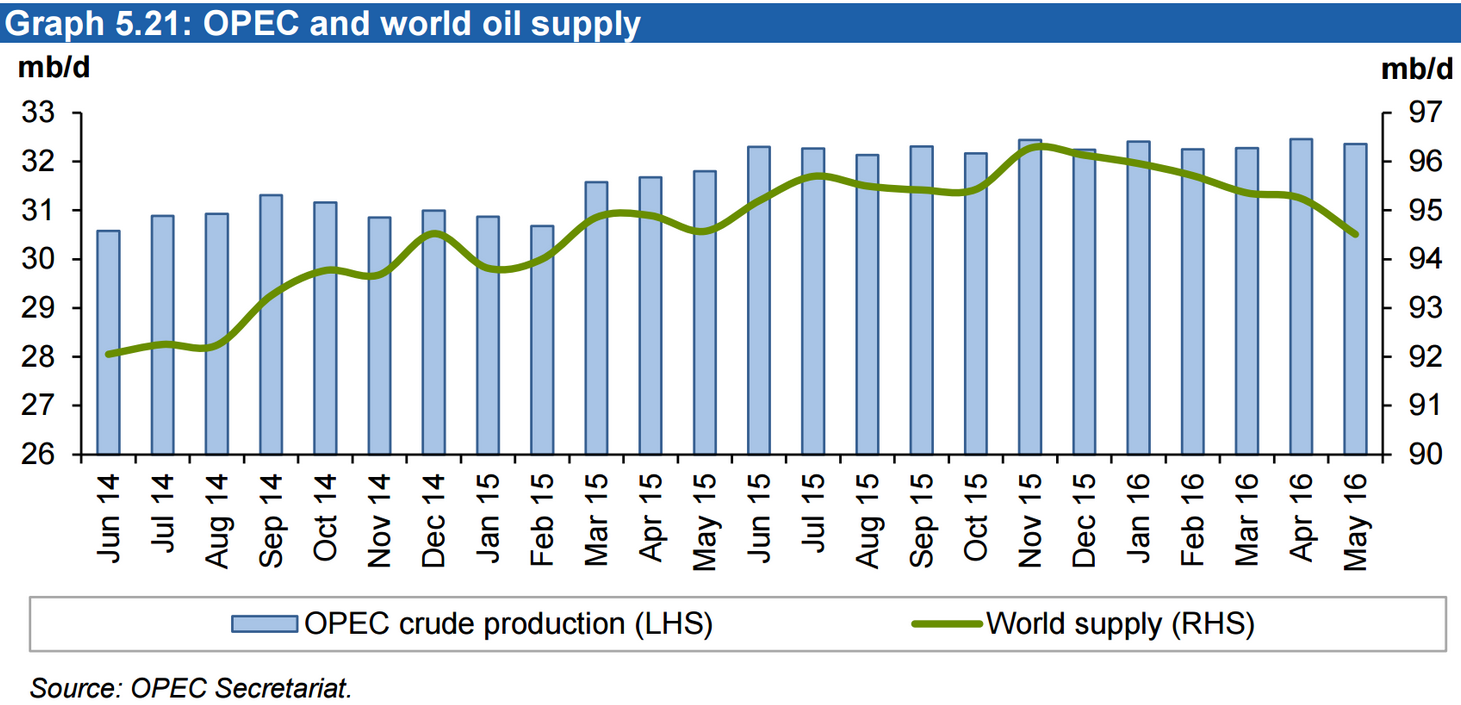

But there was one thing OPEC was able to accomplish by not agreeing to buckle under pressure and cut production: it increased its market share.

This chart shows how OPEC production (blue columns) has edged up year-over-year, while global production (green line) has started to decline. Hence, the increase in OPEC’s market share at the expense of non-OPEC producers, particularly in the US shale patch.

According to ISA Intel, Oil & Energy Insider:

As of May 2016, OPEC captured 34.2% of the global oil market, up 1.8 percentage points from the 32.4% that it held in November 2014 when it first embarked on this strategy. And that rising share comes even as the global market has grown by nearly 2 million barrels per day over that time frame.

OPEC may have inflicted damage on its own members, but it dealt a bigger blow to the shale boom.

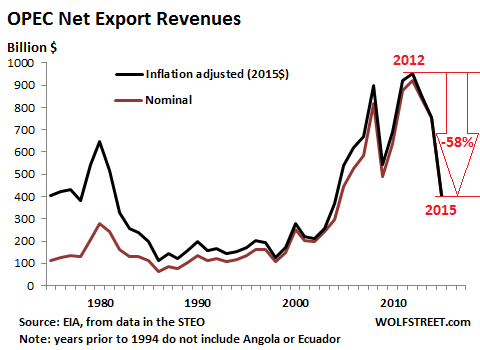

But OPEC paid a big price, leaving members with massive sinkholes in their oil-dependent budgets. The US EIA estimated that OPEC oil export revenues plunged 46% in 2015 to $404 billion, the lowest since 2004, down 58% from the glory days of 2012.

This chart shows that plunge and the history of OPEC’s export revenues going back to 1975. Saudi Arabia accounted for $130 billion in 2015, or about 32% of the total. In nominal dollars (brown line) and inflation adjusted dollars (black line):

And according to the EIA, the situation is likely to get worse this year:

EIA projects that OPEC net oil export revenues could fall further to about $341 billion dollars (unadjusted for inflation) in 2016, based on projections of global oil prices and OPEC production levels in EIA’s June 2016 Short-Term Energy Outlook (STEO).

The expected decline in OPEC’s net export earnings is attributed to lower forecast annual crude oil prices in 2016 compared with 2015. The price declines are expected to more than offset OPEC’s increased production and exports in 2016.

So just about everyone survives to fight another day. OPEC is clawing back market share. Even the dozens of energy companies that have gone bankrupt in the US are surviving in restructured form. Some stockholders have gotten wiped out, and some bondholders have lost their shirts and are licking their wounds, and in some places, taxpayers are asked to chip in to bail out big oil, as in Mexico. Local economies in the American oil patch are showing serious signs of strain. Among some OPEC members, Venezuela’s situation has turned into chaos. But the fight for market share goes on. And the US shale patch isn’t about to throw in the towel.

But the US coal industry – “king coal,” as it was once called – is in an existential struggle. Read… Why US Coal Production Collapsed to Lowest Level since 1981

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Guess it was just a flesh wound.

This is still a cheap war for Saudi. No missiles and bomb’s are landing on Saudi soil

And they are winning currently.

US Shale is simply collateral damage, and a gain in Market share, is a collateral benefit.

Some years ago I looked up crude production costs in various parts of the world.

From memory, and I have to rely on memory, because that data seems to have disappeared from the EIA website.

The cheapest oil to produce was Persian Gulf oil, about $12 a barrel.

Russia was about $20 I think?

I can’t remember US onshore costs, but US offshore production is $60 a barrel.

How long can the oil companies bleed, before they bleed out ?

A lot of US offshore costs went, down and can go. further if adjustments are made.

Just as shale costs went down as technology’s improved.

US and European companies are still developing and bringing on all the new oil tech. The chinese and Russian then steal it, so are always behind. But they avoid the R & D costs.

“How long can the oil companies bleed, before they bleed out ?”

More a question of will the shareholders allow them, to go to a very reduced, or no Guaranteed dividend policy, and will the management accept huge Bonus, Salary, Share option, and “Other Associated ” cuts.

The oil industry, just like mining, is very, cost, top heavy, VERY.

Like, if work on a job for BHP, they pay 3 times, or more, what the retail customer in the nearest city pays, for the same job. But the contractor I work with, pays a “Commission” to the Contract Broker. This ” Broker” spends a lot of time, and money, attending to. Oil and Mining Executives: Wives, Family’s, and their Trusts, you know.

Oil and Mining, is very Expensive, for some reason’s, you Know.

Yes, Russia is a low cost producer and with a relatively low paid work force that just got even cheaper with the ruble crashing to half its dollar value- Russia sells in dollars and pays in rubles.

With Russia and oil I think you are looking at something like China and steel. Half joking, I like to say that the Chinese will run a steel mill for the fun of it. When factory production first got rolling in China, a big part of the pay was a place to sleep and supper. They might not be too happy about it but these are tough regimes that actively discourage strikes etc.

Russia is not a basket case like Venezuela where production is actually dropping as the country begins to starve.

I just hope Mexico is not the next Venezuela.

‘Even the dozens of energy companies that have gone bankrupt in the US are surviving in restructured form’

Then there would be no loss of shale output. The above sounds like the old airline bankruptcy or a Trump casino bankruptcy, where the bond holders and share holders get a haircut, but the gambling rolls on.

I thought most shale energy bankruptcies ended production on their field.

“I thought most shale energy bankruptcies ended production on their field.”

No The licenses are what is worth the money.

People like buffet buy them for pennies (cash) in these bankruptcy’s, Just like any other rBankruptcy.

Then restart the rigs, as soon as it is profitable form them. Which is a much lower Per barrel figure than the last bankrupt operator had to work on as the “buffet” has no or very little debt on that field /Play.

Hence the Average production cost Per Barrel of US Shale. Drops again. As teh Buffet probably only needs 10% over lift cost to run the operation and lift cost on shale is close to Kuwait with, no debt around $5.00 Per Barrel.

One of the reasons for the reluctance of banks to foreclose on shale outfits is that apart from trucks etc. there is nothing to foreclose on- the acreage is worthless at prices below 50.

As for the ‘lift price’ (a term from a traditional vertical well were the oil is already down there and does not need to be fracked, just lifted) being anything like the Kuwait price, if this was true there would be no problem in the shale fields at all.

You are the only person in the world quoting a shale break- even of 5. Your regulatory and office costs alone might be that, then there are fracking fluids, special sand etc. that have to be brought to site. Then there is depreciation of the equipment, which has higher wear than the slow back and forth rocking pump on a legacy well.

Some traditional wells in the ME have been pumping for a hundred years, likewise stripper wells in Texas- a fracked horizontal well might produce for 2 or 3 years. Then you have to do it all over again. The labor cost for a Kuwait legacy well is practically nothing

compared to fracking.

According to most experts in the field- at a sustained price much below 40 there is no hope for shale. If a few guys want to be owner- operators and work like those gold field guys- that’s up to them. But you couldn’t afford employees or interest on loans, etc.

Above 50 there is hope. No one would have lent the industry money if they’d known the price was going to be 50 but it can muddle along, with lenders taking a haircut. Shareholders? Don’t ask.

Above 60 an gutty lender, one who hadn’t been too badly beat up, just might advance new money ( NOT an extend and pretend) to the

right operator.

But we’re more likely to see 30 before 60.

“You are the only person in the world quoting a shale break- even of 5. ”

I didnt say break even is said lift cost.

Lift is no BE.

America has a lot of Exensive post lift costs Kuwait does not have.

The next interesting point in the cycle will be how long oil stays over 60 when it get there, for more than a spike, which will probably be years if no a decade away.

Something that will be a lot harder on the Muslim states and Venezuela, than it will on the US.

Bankruptcy doesn’t stop the oil from flowing. What it (the low price of oil) does though, and this effect goes way beyond the already bankrupted companies, is to massively reduce investment in future oil production. The full effects of the oil price carnage of 2015 and 2016, won’t be really felt until 2018 and beyond. If the oil price does not pick up soon, then we are looking at serious shortages before the end of the decade.

Customers — who have to pay for everything including their petroleum products — are broke. Not just in the US, around the world.

So much attention is paid to the drillers, not much said about customers, ripped off by years of QE, who cannot pay for their fuel by using it.

Stagnating or even contracting demand from Asia and Europe is one of the main drivers in this oil glut.

Starting in 2008 France lost 480,000bbl/d refining capacity, Germany 300,000 and Italy 400,000. No new capacity has been added to offset this.

This year Shell started closing a few of their Asian operations, like Lutong in Malaysia.

In spite of this Gulf oil producers have huge plans for expansion, and not merely for crude: Kuwait is building a colossal oil refinery (al-Zour) with an astonishing 600,000bbl/d capacity. Iran has big plans to further expand the 450,000bbl/d Abadan monster.

These refineries are not meant to supply domestic markets (which are oversupplied already), but export markets in Asia and Europe. Asia has a massive refining glut and Europe is reducing capacity because even the rosiest scenarios say demand will be down.

Plainly put demand for oil has peaked and is now contracting under the two pronged assault of what promises to be a long stagnation (if China stagnates, the world stagnates, that’s as easy as that) and shifting trends in energy generation, from the growing use of natural gas for energy generation and heating to higher solar panel efficiency. Not even all those SUV’s carmakers are shifting now are enough to change this.

“(if China stagnates, the world stagnates, that’s as easy as that)”

Dont get to wedded to that it will not apply as a truism for much longer.

Much of chinas “work” is leaving for other homes.

Apple will have to move some production to India apart from Foxcon, if it is to get apple store access to India.

Apple has also already brought some manufacturing (Robot) back to the US.

Nike, Adidas, also have moved some manufacturing from china. They set the trend going into china, and they are already leaving.

The EU as well as the US are complaining, their companies are finding china an increasingly hostile and closing, not friendly and opening, environment.

MSCI again, china stock-markets not open enough, to opaque, to much state interference in price discovery, to many trading halts when prices are falling, to hard to repatriate fund’s quickly.

Costs are rising in china, when costs rise the globalized Vampire Corporate’s move on.

Why should china be treated any different, than the country’s whose industry’s it stole, by the Globalized Vampire Corporate’s it attracted as allies, with huge state subsidy’s.

china even stole textile work, from Bangladesh, now that work is slowly returning. .

Veterans Today has a great story on Saudi involvement in the 911 attacks as well as the Fort lee NJ connection VERY professionally done piece that everyone who is interested in justice for our fallen countrymen should read

One thing that the opec countries have to do is to sell oil to pay their debts. They’re kinda stuck as this is their only real revenue generator. At the same time their domestic consumption is rising. More developed countries have more options.

http://oilprice.com/Energy/Crude-Oil/Iranian-Oil-Is-Disguising-A-Significant-Decline-In-Global-Production.html

According to this article a big drop in oil production relatively recently. Supply has dropped since. Iraq and Iran can’t continue increasing production very much these days. Canada and Nigeria have had their production drop. Rather than being awash in oil these days, it’s likely you have a defecit at this point.

On a somewhat related note, we bought a tank of gas for the grill less than a month ago, for $50 on sale. After 6 or 7 uses it is empty. We are pretty sure we were short changed on the amount of gas in the tank. Usually a tank last us almost an entire summer.

Weigh your tanks empty and full, many people mistakenly fall into the belief they were shorted. In my case I’ve always traced the issue to forgetting to turn off the tank valve, forgetting to shut down the grill or worse, a leak.

I’ve never found my tank to be short but watch them refill the tank and many will vent till the tanks burps liquid, a good indicator there’s no air in the tank and it’s at capacity.

$50 seems pricy FWIW, but then nearly everything seems to have gone nuts. Probably nothing to do with the producer unfortunately, mostly lengthy line of gougers handling the products.

I’m no economist but shale oil will always hang above like the sword of Damocles. Anytime the price goes up making it profitable, the US will start pumping shale again. Doesn’t that prevent crude oil price from going up too high? Yes, Saudi is winning market share but the price will remain depressed. In a way they will be forced to supply cheap oil.

“Anytime the price goes up making it profitable, the US will start pumping shale again. Doesn’t that prevent crude oil price from going up too high? Yes, Saudi is winning market share but the price will remain depressed. In a way they will be forced to supply cheap oil.”

That is what it does and is going to do for quiet some time, it effectively neutralizes the Iranian fear factor and prevents the muslim oil as a weapon, oil price extortion of the west, for quiet some time in the future.

Once the major muslim oil states re budget, on less than 60 $ oil, the must have 100 $ + oil fairy story, will simply fade away.

The conventional oil production has been on a production plateau since 2005 at 82 million b/d.

The non OPEC production has been declining by 1million b/d annually since 2010.

OPEC has been filling up that decline.

The increase in production since 2005 has come from unconventional oil.

Saudi Arabia has been producing 10 million b/d and exporting 7 million b/d during this time, with ups and downs.

The giant oil fields (some 500) count for 60 percent of the global conventional oil production. Most of them are over 50 years old and 80 percent depleted. They are today being horizontally drilled, fractured, water injected and co2 injected to keep them on a production plateau.

Saudi does fracking?

Conventional oil reservoirs continue production through secondary and tertiary recovery techniques, usually called enhanced recovery. The lifting costs are increased when compared to primary recovery, but still much cheaper than drilling and developing a new field. The rapid decline US shale wells may not be candidates for enhanced recovery due to geological characteristics controlling reservoir dynamics. Shale fields may only stay productive through drilling new wells, which even with cost cuts, are still expensive compared to onshore and shallow water conventional wells.

Or put another way, shale plays require high oil prices to justify expensive wells which have to be replaced in a short time frame to maintain production levels. In shale plays, geology is not your friend.

Excellent comment.

Many people miss this aspect of the equation (i.e. how much oil comes from very few fields which are very large and are old).

Robert Rapier had a chart a while back that showed the US filling the void (with unconventional oil) as global production rolled over.

The year we discovered the most oil was in the 60’s … discoveries have been getting smaller and more numerous, but in total we discovered the most oil in one year in the 60’s and it has been downhill since. Just lag before it catches up.

Regards,

Cooter

Thanks for keeping our eyes on the ball Yoshua.

NK: Most conventional oil and gas wells are fracked in the completion process. The frack jobs are typically smaller and therefore cheaper. It really comes down to reservoir geology and reservoir characteristics. Fracking is a process, not a play description. A typical Saudi carbonate reservoir is very different from a shale reservoir. Shale is a high porosity/low permeability. A good carbonate, or even a good sandstone conventional reservoir is typically a good-high porosity/good-high permeability reservoir. But a good quality reservoir rock’s production may be increased through acidizing and/or fracking.

They’ve won the battle but will surely lose the war. Who cares about market share if it doesn’t give you pricing power?

Current shale oil tech puts a lid on prices @60/barrel. As tech improves, that number will go down. Already at 50, rig counts in the shale patch are starting to go up. Even if it stays at 60, OPEC is toast. Not a single country within OPEC can survive long-term on $60 oil. They got used to $100, and any effort to cut domestic spending will be met with revolution, likely of the bloody kind. Even Saudi Arabia, the one country who’s banking on surviving the carnage, is burning through foreign exchange reserves while figuring out how to wean its citizens from their oil-subsidized lifestyle.

Couple that with drastically declining renewable energy costs and OPEC faces capped prices and declining demand. Not a good long-term outlook.