Canada’s truly magnificent housing bubble, incomparably more magnificent than the housing bubble in the US that blew up with such spectacular results, is starting to worm its way into all sorts of venues. And on Tuesday, Bank of Canada Deputy Governor Agathe Côté had a special place for it in her discussions of “vulnerabilities and risks” to the “stability of the financial system.”

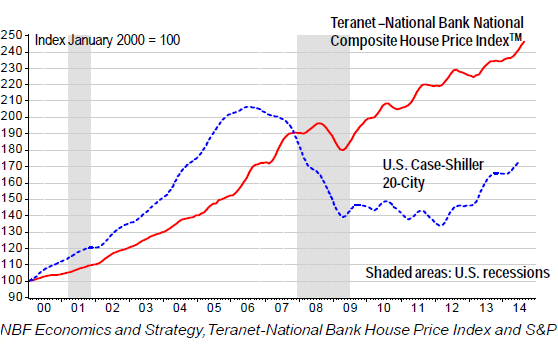

Home prices in Canada rose more moderately than in the US during the crazy go-go years from 2000 until the financial crisis: in the US they more than doubled in that period, according to the CaseShiller Index, while they rose “only” about 70% in Canada, based on the Teranet–National Bank National Composite House Price Index.

But then the hot air was let out of the housing bubble in the US between 2007 and 2011. In Canada, after a minor ripple between 2008 and 2009, home prices continued soaring – to this very day. In August, they rose another 0.8%. Over the last 14 years, prices have increased by 150%, twice as fast as in the US.

Ratings agency Fitch warned about the Canadian housing market in July. It was “20% overvalued in real terms,” based on Fitch’s own metrics, the report said. Had they looked at the above chart, they’d have come to the inescapable conclusion that it was 100% overvalued in real terms. Home-price bubbles are treacherous: “High household debt relative to disposable income has made the market more susceptible to market stresses like unemployment or interest rate increases.” That household debt to disposable income ratio has been hovering at near a record 164%.

Low interest rates have been heating up the market. Fitch’s solution? Keep interest rates near zero, obviously. Forever. Period. Because raising them would prick the bubble, and its implosion would trigger all sorts of mayhem.

Now Bank of Canada Deputy Governor Agathe Côté weighed in on the housing bubble. It’s on everyone’s mind. In a speech to the Chamber of Commerce and Industry of Saguenay, Quebec, she discussed among other things, the four key responsibilities of the BOC – monetary policy, the financial system, the currency, and funds management.

The housing bubble falls under the key responsibility of managing the financial system, or more precisely under the objective of promoting its “stability and efficiency.” As part of its Financial System Review, the BOC “assesses vulnerabilities and risks.” Among the four “important risks” in her presentation:

- A sharp correction in house prices

- A sharp increase in long-term rates

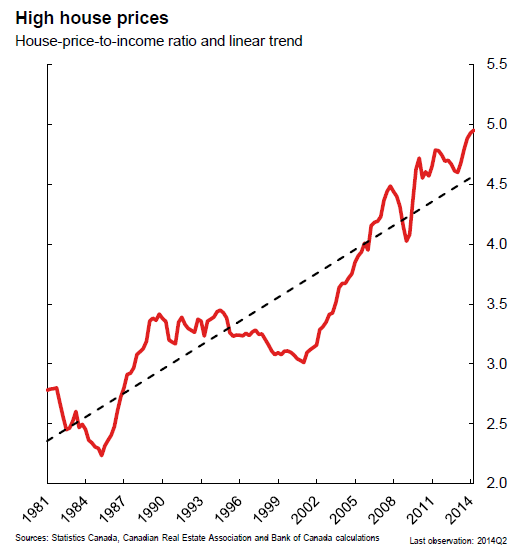

If those two occurred, all heck would break lose due to the factors Fitch had already pointed out. Home prices have skyrocketed, far outpacing household incomes. This chart from Côté’s presentation shows the very ugly growth of the house-price-to-disposable-income ratio. Since 2000, it has relentlessly soared, as home prices are placing an ever larger burden on household finances:

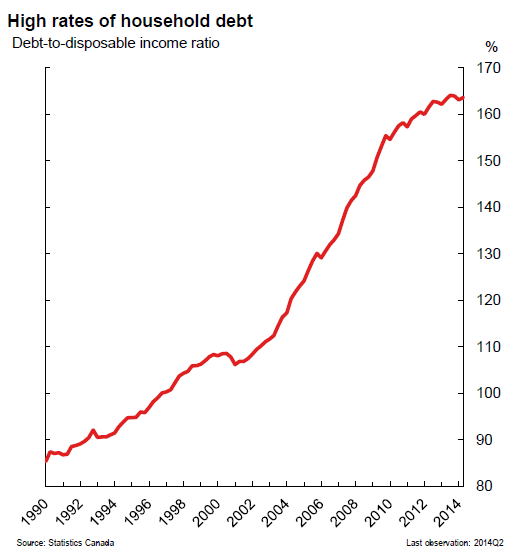

Given the lagging incomes, households have made up the difference with debt, and they’ve gone on a phenomenal borrowing binge, and their indebtedness in relation to their income has skyrocketed. The chart below shows the debt-to-disposable-income ratio, which doesn’t leave households, and by extension lenders and the entire housing industry, any room to breathe once home values begin to descend back to earth. And there’s no trace of deleveraging in sight:

Now imagine what even just slightly higher interest rates would do to households barely able to shoulder this mountain of debt, and what they would do to home prices as demand would be systematically strangled.

That’s why Fitch was hoping that additional regulations by the federal government, instead of interest rate increases, would cool down the market. Some of it already happened, including shortening amortization periods to 25 years from 40 years and tightening the eligibility for government-backed mortgage insurance. In this manner, Fitch said, the government should try to “engineer a soft landing.”

Good luck.

Bubbles don’t land softly. They implode. It’s a brutal process. The longer bubbles are maintained, the more brutal their implosion. Housing bubbles are particularly vicious: they’re accompanied by a construction boom, which contributes enormously to the economy in myriad direct and indirect ways – from well-paid construction jobs to pickup truck sales. It was the collapse to the construction boom in the US that took down the Main Street economy, not the shenanigans blowing up on Wall Street. And the housing bubble in Canada puts the US housing bubble to shame. Hence the BOC’s public fretting about financial instability.

In the US, our new housing bubble has already run into trouble. Investors caused prices to balloon, but now prices are too high for investors. What’s left is a toxic mix: dropping sales, still rising prices, and ballooning inventories. Read…. After Mucking up Housing Market, Investors Flee

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

A couple of points on Canadian housing.

1. Capital gains on your main house are not taxable

2. Interest on your mortgage is not tax deductible

3. Property taxes in many locals are about 1% of assessed value

4. Much of the price rise has been driven by immigration with immigration hot spots seeing the biggest rises (Toronto, Vancouver, Calgary). Toronto now has 50% of the population born outside Canada.

5. Mortgages are not as easy to get as in the US. Many mortgages are still bank financed and held. Still the Conservatives are culpable for loosening restrictions before the financial crisis. They have very slowly come to their senses.

4. Partially correct. The prices in biggest cities also are driven by the inflow of off shore money from China, mid-east and Russia as well as speculators/owners (many step-up owners bought big homes while keeping the starter one)

5. Bank lending are very lax. Someone with passable proof of income and credit history can borrow up to 5 times of income. So if a mid class family with 150K income, with 5% down, they can buy a 800K home, 900K if they stretch it. As long as CMHC insurance is present, banks can give you up to 6 times of loans.

4. Yes, immigrants have an impact. However, most purchases are by locals.

5. Nonsense. I went through the US mortage process recently, along with four coworkers. It was MUCH harder than in Canada. Everything was scrutinized. A mortgage in Canada is far easier to obtain.

House prices in Canada are so exorbitant that they are not so far off from Japan!

House prices in England in moving in the same direction, somewhere around 19% every year. What I would like to know is what is driving the profusely high house prices in Canada? Some dilapidated, pusher, looking homes are going for as much as $1 million dollars! Who is giving all this credit to these house buyers?

Unfortunately, it looks as if the Canadian government through its bank and proxies is addicted to issuing consumer credit to procure growth based on a virtual economy.

“…the Canadian government through its bank and proxies is addicted to issuing consumer credit to procure growth based on a virtual economy.”

You just defined the economic theory that is so passionately practiced by governments around the world. And when some government dares to be a little bit prudent, it gets hammered down by all other governments.

The CMHC is the federal agency that provides mortgage insurance to the banks. If a CMHC insured home has a borrower who defaults, the government guarantees payments to the banks.

Hence, the taxpayer is on the hook for all the risk with CMHC insured homes. Of course they argue that they have a pool of funds, but we all know that insurance mechanisms do NOT work when losses are non-independent. Real estate downturns and extreme weather events are examples of correlated losses that wipe out insurers. In this case, however, the insurer can turn to the government for a bailout.

Moral hazard at its finest.

Canadians own a large percentage of the luxury ocean front condos in Florida and they actually use them. The older Canadians might just decide to move to a cheaper country, America.

Bursting bubbles don’t always lead to severely crashing property values. In many US markets, once the values dropped to a level where property becomes a profitable rental, investors step in and start purchasing. Extremely low interest rates enable the properties to be profitable rentals. Granted, exceptions occur in markets with negative demographic trends (I personally am avoiding investments in Reno because of this) or other unfavorable trends (Chicago’s taxes, social trends, etc.). I have no problem investing in a market that the media claims is overvalued, as long as I am positive cash-flow situated.

Another peculiarity of the Canadian housing market is that residential mortgages have a five-year term (and longer amortization periods, typically 25 years). So, every five years, families have to replace their mortgages with a new one at the then-current market rates. If rates go up, there is little ability to meet higher monthly payments. This is the real threat to the Canadian housing market, since Canada cannot manipulate its domestic interest rates as can the US.

Indeed. And if the value of their home has diminished over the five years, they have to make up the difference in cash because the bank will not make up the shortfall.

We know Canadian consumers do not have cash on hand because they are drowning in debt. BC is negative savings, and StatsCan has hard evidence that retirement plan contributions are not just abysmal, but people are raiding their plans.

It seems the entire globe is one, giant, inflating balloon.

I just can not wait to see the carnage left by these greedy bastards at the central banks who think they could print there way out of the cesspool of debt they created. Escape velocity? BS!

Lots of new housing in Ottawa, and far more on the way. It’s actually been slower the last 2 years, but some of the larger builders have a ton of land and some really big plans in the works.

Dealers are practically throwing new trucks away right now; and as skilled trades are pulling in around $120000.00 in this market…..keep ‘er comin!!

If they can keep this bubble blowing for just another 7 or eight years, I’ll be retired at 45 from banging tin :) :) :)

Check out the bottom line (total debt outstanding) of the latest credit market summary data table from Statistics Canada to see the extent of the debt problem in Canada:

http://www5.statcan.gc.ca/cansim/pick-choisir?lang=eng&p2=33&id=3780122

Thanks. Now I’d like to see how this compares on a per-capita basis to the US, Japan, and the UK. I guess I could do my own math, but this being Friday night, I’d rather have another IPA.