Hurricanes in September & October and the Boeing strike will mess with labor market data for a few months; the Fed won’t get clear answers.

By Wolf Richter for WOLF STREET.

Three hurricanes – Francine in early September, Helene in late September and early October, and Milton in mid-October – and the heavy rains and flooding that came with them temporarily shut down work sites in a substantial part of the country, which is going to throw a lot of additional uncertainty over the labor market data for the next few months.

We’ve already seen this play out in the weekly initial unemployment insurance (UI) claims, which react the fastest: They spiked for the late September to early October period as many work sites were temporarily closed, then subsided again.

In addition, there’s the ongoing Boeing strike and the accompanying layoffs. Workers on strike are not eligible for UI and don’t show up in weekly initial UI claims. But they will show up in the employment data over the next few months. So this is going to be a mess.

Today the Bureau of Labor Statistics released the Job Openings and Labor Turnover Survey (JOLTS) for September, which is based on employer data, may have also been impacted.

And some interesting things happened:

- Hiring in September jumped for the third month in a row.

- Workers continued the trend of not quitting their jobs but sticking it out.

- Layoffs and discharges jumped, after the decline in August.

- Job openings fell, after the increase in August, and are now about where they’d been at the peak before the pandemic.

- Job openings as a percentage of total nonfarm payrolls fell but remained higher than any time before the pandemic.

- The number of job opening per unemployed persons has remained roughly stable for the third month at decent but not hot levels.

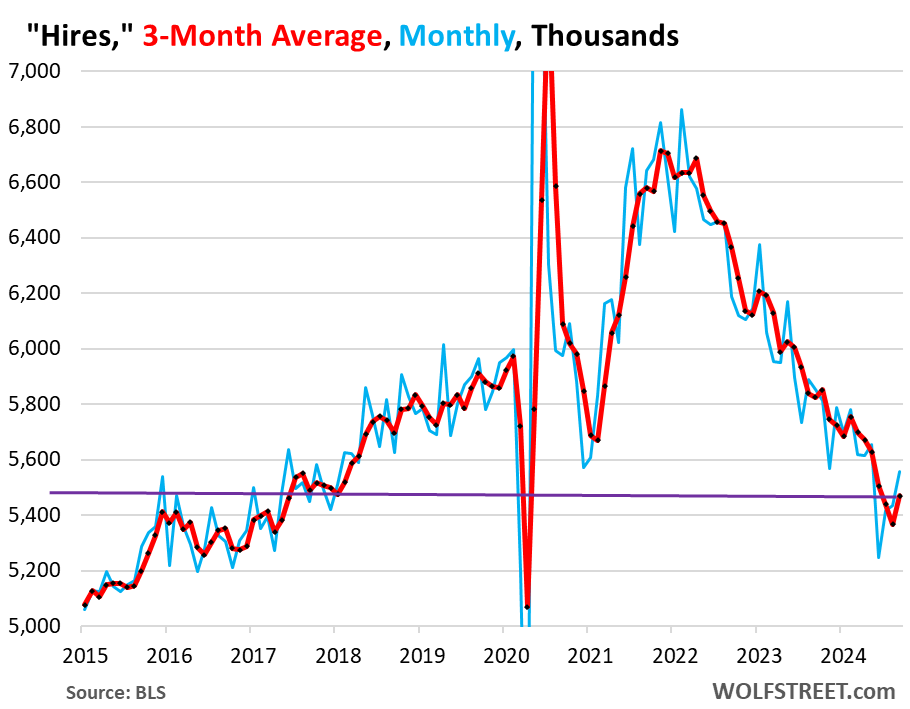

Hires jumped to 5.56 million in September, the third month in a row of increases, and August was revised higher (blue in the chart below).

The three-month average, which irons out the month-to-month squiggles and includes revisions, rose to 5.47 million hires, the first increase since February (red).

These people were hired to fill roles left behind by workers who had quit or were discharged, and to fill new roles. But the number of workers who quit their jobs has been dropping sharply as workers clung to their jobs, instead of walking out, as we’ll see in a moment. And far fewer quits means less hiring to fill the newly open positions, which explains the long down-trend in the chart below which roughly parallels the trend in quits.

But hiring has now accelerated for the third month, even as fewer workers quit, and so these hires filled newly created positions or positions left behind by workers who were discharged.

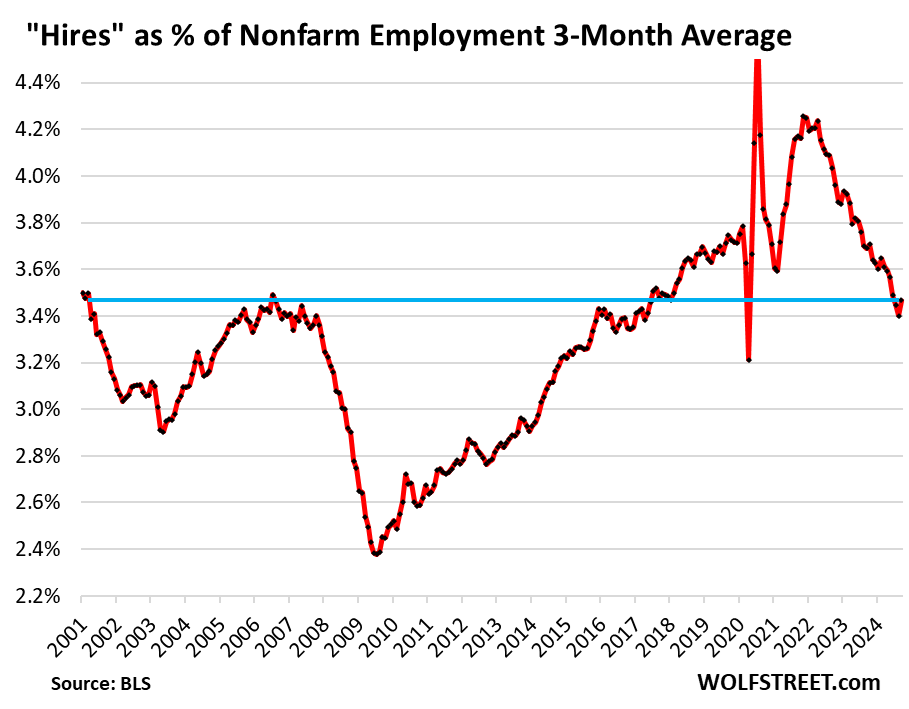

The ratio of hires to nonfarm payrolls increased to 3.47%, the highest in three months, but below where it had been in the 2017-2019 years, which were considered a tight labor market (amid Fed rate hikes and QT).

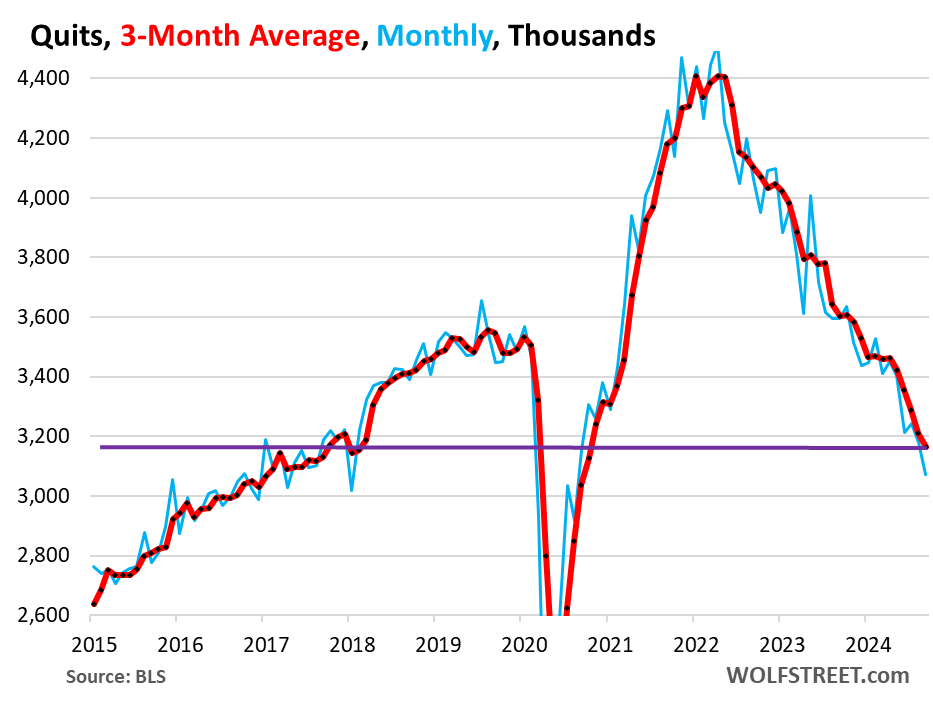

Quits: Workers cling to their jobs. Voluntary quits fell to 3.07 million in September. The three-month average fell to 3.16 million, back to March 2018 levels.

The huge churn during the pandemic, when workers jumped jobs and industries to improve their pay and working conditions, and to better match their skills and aspirations, thereby triggering the biggest pay increases in decades, has ended.

Fewer voluntary quits mean fewer newly open slots that have to be filled, so fewer job openings, as we’ll see in a moment, and fewer hires to fill those openings.

For employers, lower quits is a big improvement. Productivity rises when workers stay longer and learn the ropes. Pay increases have moderated because employers no longer have to poach each other’s employees by offering better pay. Employers are re-exerting control and they’re cleaning out the deadwood. Some are now mandating the return to the office at least for a few days a week, knowing that most people won’t quit over those policies, and if they do, fine.

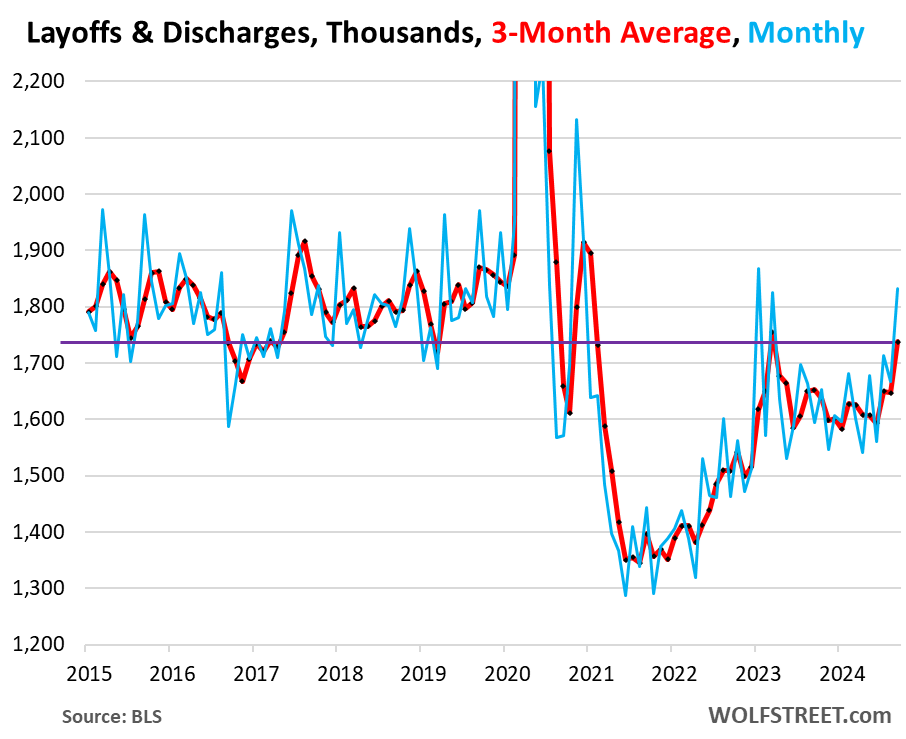

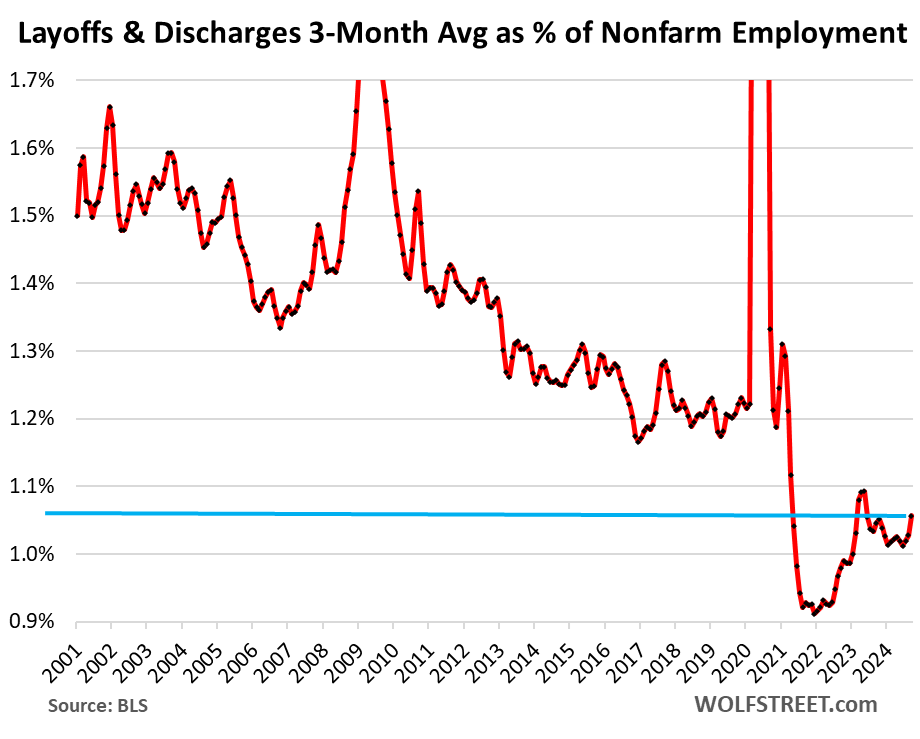

Layoffs and discharges rose to 1.83 million in September, after having declined in August. This could be one place where Hurricane Francine, which hit the Gulf Coast and especially Louisiana in the first half of September, showed up. The much bigger effects of Hurricane Helene will likely show up in the October data. The three-month average rose to 1.74 million.

Layoffs and involuntary discharges include people getting fired for cause. Getting fired is a standard feature of working in America, and it occurs a lot even during the best times.

These numbers are still relatively low in comparison to the prior two decades, as employers are shedding people at a rate that is lower than during the Good Times before the pandemic, and they’re hanging on to the workers they’ve got.

Layoffs and discharges as percentage of nonfarm payrolls – which accounts for growing employment over the years – rose to 1.09%. The three-month average rose to 1.06%, both far below any time during the pre-pandemic years in the data going back to 2001. This shows just how employers are hanging on to their workers.

Why employers are hanging on to their workers has been subject to a lot of speculation, including that employers may have learned a lesson after getting burned by the labor shortages in 2021 and 2022, when they couldn’t rehire the masses of people that they’d let go, and had to poach employees from each other and thereby drove up their labor costs.

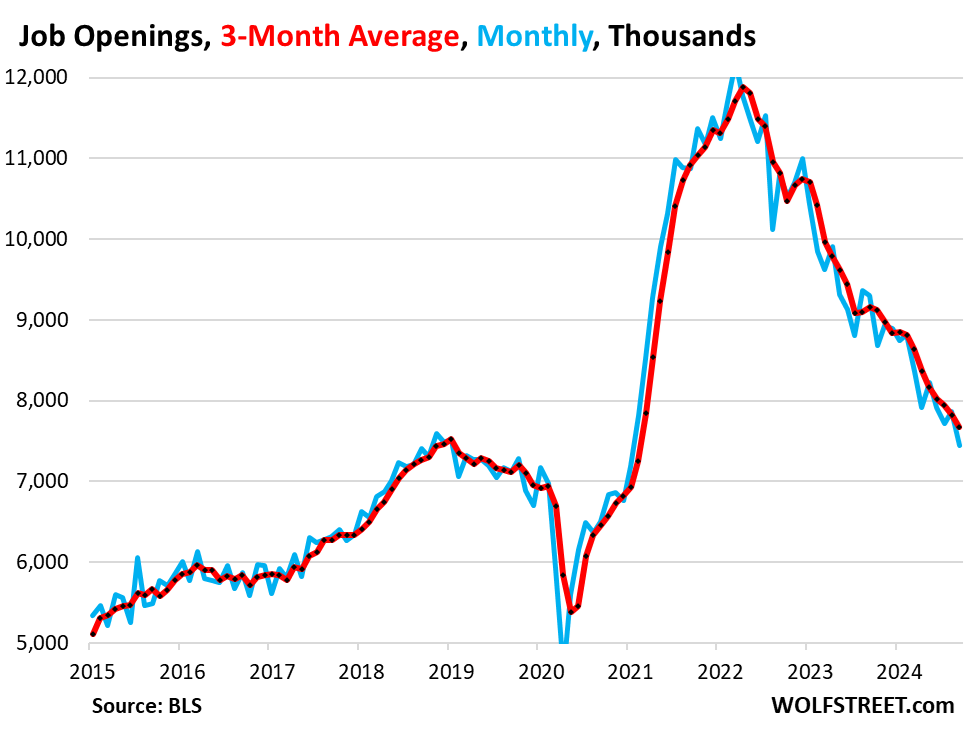

Job openings fell to 7.44 million, roughly where they’d been at the peak before the pandemic. With fewer people quitting – see above – there are fewer job openings to fill. The massive churn of the labor force in 2021 and 2022 has ended.

The three-month average fell to 7.67 million job openings, and that’s still above the prepandemic record of job openings.

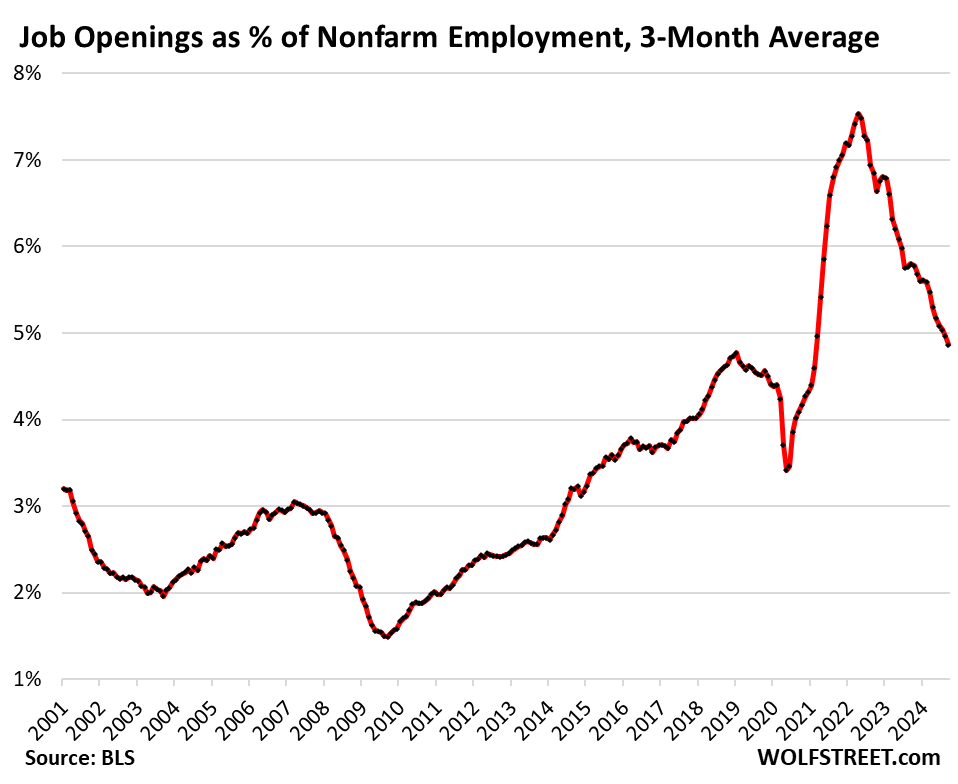

The ratio of job openings to nonfarm payrolls, which accounts for rising employment, dipped to 4.7%, but is still higher than the pre-pandemic records in late 2018 and early 2019. The three-month average of job openings dipped to 4.9% of nonfarm payrolls, still above the prepandemic record.

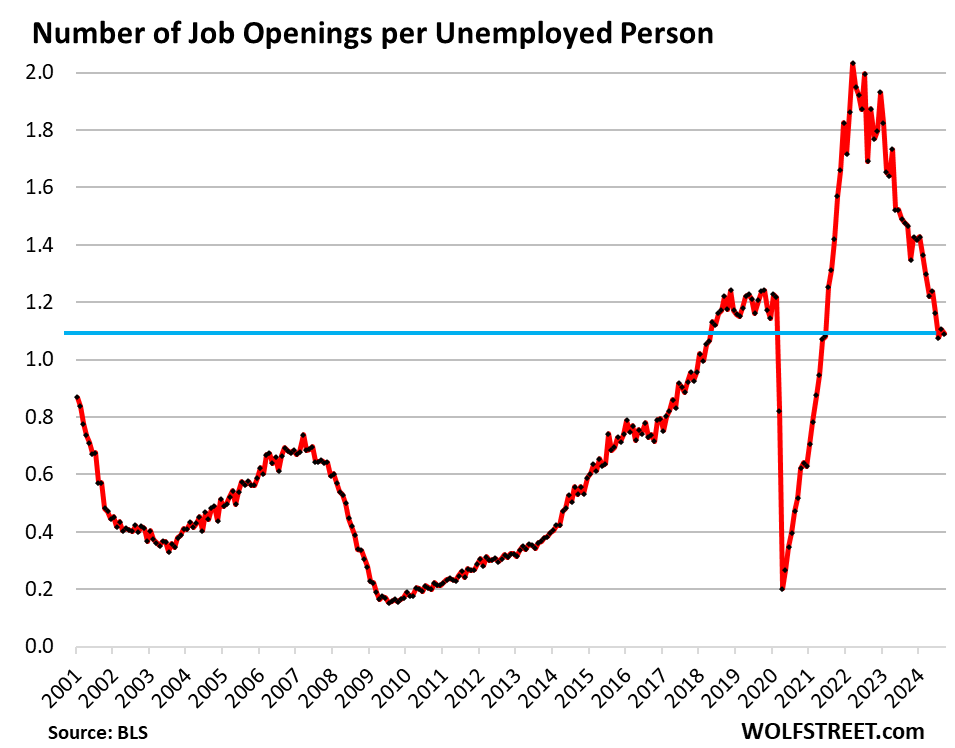

The number of job openings per unemployed person – a Powell favorite – has remained at about 1.1 for the third month in a row, meaning that there are still slightly more job openings (7.74 million three-month average) than unemployed people looking for work (6.83 million).

This ratio – now lower than it had been during the hot labor market in late 2018 through February 2020 – was one of the reasons Powell cited for the 50 basis-point cut; the metric was a sign that the labor market has cooled enough that doesn’t need to cool further:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I wonder how many of these jobs are government jobs? Everywhere I go here I see a shortage of workers actually working. Lines everywhere at checkout counters.

In the US economy, government jobs don’t play as much of a role as in other economies:

Federal government job openings: 114,000 = 1.5% of total job openings (7.44 million).

State and local government job openings (most teachers and healthcare): 703,000 = 9.4% of total openings (7.44 million).

There are still industries with worker shortages — including some teacher shortages at some local governments. But also there are companies that refuse to staff up enough in order to keep their costs down, and customer services, quality, etc. suffers because of that — and that may be what you’re seeing at the checkout.

I forgot to add: Shortage of school bus drivers, Police Officers etc.

No shortage of panhandlers at nearly every major intersection.

I love economics by anecdote. Vibes beat data. Like the fact that the employment to population ratio for 25-54 year olds is close to it’s all time high. But I saw a panhandler who could have been working so everyone’s a lazy bum

The Federal Reserve Bank of St Louis website shows the Employment-Population Ratio at 60.2%.

It was 61.1% in February 2020, and its all time high is 64.7% in April 2000.

Its lowest since April 2000 was at 58.3% in January 2011.

A.D.

“…the Employment-Population Ratio at 60.2%.”

Boomers retiring. Many of them don’t want to work anymore. They’ve had enough of the rat race. And those that want to work run into age discrimination, and that’s not fun, and so they stop looking and enjoy retirement instead. Boomers are still a big generation. They move the needle. I thought you’d know that by now.

numbers,

You might be trying to be cute, but there is absolutely no shortage of bums, panhandlers, or druggies. It’s disgusting and should be illegal.

SC,

Agree with Wolf that companies are just being cheap by not hiring enough workers. Will add that it’s almost like they’re still blaming covid. Anecdotally, having been to nearly 70 countries, I’d say the US has about the worst customer service in the world (except for in Utah, where you get great service by young people with nothing behind their eyes) and it’s only getting worse.

I was never some hippie activist, but it becomes ever more clear that everything is run by greed.

Yes, I specified prime age for the exact reason Wolf outlines, there’s a ton of boomers who have retired.

The percentage of the population over 65 has increased by over 5%, more than enough to explain the for in the overall employment to population ratio.

If you’re asking who is sitting around the house while other people work, it ain’t 25-54 year olds.

Panhandlers are a nuisance, but they are not economically meaningful. Different problem.

You either work for the government or you work for a company that contracts from the government. The government is the biggest employer in this country. Where do you get your delusional facts Wolf? Whether you are directly employed by the government or work for a company that contracts for the government is the same thing. You got city, county, state and federal government hiring the vast majority of people in this country. Get your facts right.

The federal government has 2.25 million civilian employees = 1.4% of all 160 million nonfarm employees in the US.

Closely behind the federal government are Walmart and Amazon. And then there are millions of smaller employers, including my company.

Government employment as percent of total employment (the spikes = census taking). Adios.

SC:

“I wonder how many of these jobs are government jobs?”

You self-select into the DC area and complain about your life, endlessly.

Your point is….

OutWest

You don’t know what I do. I work in the private sector. Stop stereotyping. My point is that a major portion of the new jobs are government jobs or government funded jobs.

I had recent tenant(retired) who took contract job at Raytheon(think making missiles for ukraine)

he got $22,000 sign on bonus before making $5k week

Pretty wild that you insist on that despite being wrong. The percentage of all jobs that are government jobs is under 15% (less than one in 6) and has been steadily dropping for 50 years straight. Looks like propaganda is working well.

Not sure why some people have their replies locked, but this is for “numbers”

13.8% of all BLS jobs are government workers, literally NO OTHER SECTOR IS HIGHER!

But they only make up one in six people so who cares?

HAHA

Jobsnumbersarefake,

Federal government jobs = 1.9% of total jobs

State and local government jobs = 12.8% of total jobs.

State and local government jobs are mostly teachers, college instructors and professors, administrators in education, and first responders (police, highway patrol, fire fighters etc.).

Duh

Youarefake.

I’ll thank Wolf for doing it for me. If you want to fire all teachers and cops, be explicit about it. It’s only a single category because you lumped together all layers of government and because you probably forgot all those people are government employees.

Government employees by occupation:

Education (teachers and professors): 6.7%

Public safety (cops, prisons, fire): 1.6%

Health (hospitals and health care): 1%

Post office: 0.4%

Federal: 1.4%

Health and hospitals: 1%

All others: 1.6%

Almost all of these numbers haven’t changed since 1998.

Gotta love the anti government blowhards who don’t have a clue who does what for them. Something out there is rotting their brains.

LOL, I just got his name now.

Swamp Creature at a self checkout:

yelling “Could some employee come press these damn buttons for me?!”

Hehe jk 😉

May a commentator condense and explain?

Wolf manytimes, details how this Keynes Special Theory has roots and is intelligible — i give him credit for that — what about the revisions?

The revisions are included in the data. In this particular data set, revisions were up AND down. For example, hires was revised up a lot, and job openings was revised down a lot. But those revisions are included in the data and you’re looking at them.

HR packages are good to go. Those who quit got the money. Those who

didn’t might be unemployed. Layoffs and discharges might rise above

2023 high, in thousands. Layoff claims and payments end after 26 weeks.

The next administration might start with a major correction or recession.

Layoffs and discharges might reach/ breach two millions. Labor became too expensive, especially in the junk food sector. They will not be able to pay rent.

My 2005 Matrix, at 200k,, is a high clutch, a tad rusty, but i don’t want to buy a new computer machine, with its 8 year shelf life for when the software goes bad. Stick shift, you can’t get them anymore, except for sports cars.

Your 2005 Matrix almost certainly has ECM to manage engine timing, fuel trims etc. I also dislike newer cars with their bloated tech, but engine computer management is a good thing.

IIRC, Honda made a 6MT version of the Accord until 2018. Not sure how recently Toyota offered a stick.

I say I say that’s just a dressed up Corolla.

2005 was a nice year, I think the first year of a new generation but a really good generation.

The getup and go on those things is so nice.

Hmm…more data day by day until the next FOMC to oppose another rate cut. I guess if they want to do it, either the inflation number before the meeting has to look much better, or they can use below to shield them against any criticism for another rate cut. Market is probably counting on this hard judging by recent rally….interesting time.

“Layoffs and discharges rose to 1.83 million in September, after having declined in August.”

The market is rallying because the economy is the best and most healthy it’s been in years. It doesn’t need anything. A pause will cause a temporary dip at worst

Only if you leave out the LIABILITIES. There are 5 general classes of full general ledger accounting which are 1) Assets, 2) Income, 3) Expenses, 4) Capital/Equity, and 5) Liabilities. It’s way past time that we deal with both the public and private ‘economy’ using full balanced general ledger accounting. It’s not a pretty picture at all when you include the mandatory five (5) classes.

Assets and equity is at all time highs. What are you getting at?

Bonds have sold off hard in the last couple weeks.

Anonymous, it’s hard to convince the doubters here of that.

It really is like a beautiful day and a lot of wolf’s forum is carrying around umbrellas and waterproofs. You just can’t pry them out of their treasuries.

“The bank across the street is giving away 30% a year on your money. Ummm I think it’s called the S&P”

some on This forum: “I’m good with my 2025 average of 2.25% thanks”

😊

That rate cut is happening.

Labor is a creature balanced between fear and greed — the fear that getting another job at the same pay may prove harder than expected, and greed to get more out of a paycheck every 2 weeks.

M

Investors are creatures balanced between fear and greed.

The fear that they may miss out on an unearned windfall.

The greed that endlessly craves more and more lucre.

Not leaving my job as 100% telework jobs are slowly going away! Amazing how many applicants there are, many not even remotely qualified, just because of this. I even get a telework stipend, albeit small, but I would happily pay to continue to telework. All that gas and parking back into the economy plus time not spent in commute. After 4 1/2 years of it the concept of a cubicle is very strange.

Enjoy it while it lasts. I am afraid Amazon started the traction of large companies calling back employees in 5 days a week. Heard 3M doing the same for management as well. Other companies are probably holding out for now until they have even more power over worker bees if a major recession does happen..then you can bet your A$$ hybrid or remote will be as rare as wearing a mask in public.

It’s funny to me how the general public has so much good faith in companies doing the right thing and thinking hybrid or remote is the new norm…you mean reversing a 50+ years trend because of a sudden episode that lasted 2-3 years? I guess that explains a lot of why quite a few people once something goes up, it will just go up forever…

The crypto, housing, gold, and stonk bubbles certainly seem to be going up forever

yeah that’s true, I guess we finally arrived at a time to withness “This time is different….” being proven right..if we only knew in hindsight to make this time different stick, all you need is couple of trillions in very short amount of time…heck 08 probably could’ve been adverted..

phoenix_ikki it’s easy to avoid recession just by printing money. if you don’t care about your currency, that is.

They printed everything higher.

“There’s a floor under stock prices.”

~Nancy Pelosi

People leaving jobs that decide to go from remote to hybrid in favor of staying all remote is the main trend I see in the white collar world right now. We are about to pick up someone good on my team because his current job went hybrid and he doesn’t want to be in the office.

Does your firm need an excellent Systems Engineer?

Hires, quits, and job openings are plummeting in unison. The velocity of the associated trend lines suggests a rapidly cooling job market. If we see an abrupt leveling off and sideways trend in the data, Powell will have pulled off his so-called miracle. Alternatively, if this trend continues I’d expect Wall St gets its wish of more aggressive rate cuts into 2025.

Hires are NOT plunging, they JUMPED for the third month in a row.

Quits plunging is a good thing; people are actually working instead of looking for the greener grass, and they’re staying longer in their jobs and learning the ropes. This translates into productivity gains. That high rate of quits was a huge mess for companies.

As quits plunge, job openings plunge because fewer people are quitting and leaving job openings behind. So that’s logical.

The churn has ended. That’s all.

That’s what the whole article was about.

So essentially, the job data for the next couple of releases are going to be less reliable than usual because of the hurricanes, where reliable means a useful indicator of the trend in long-term economic conditions. So if the data show economic conditions are worse than normal, then the hurricanes can be blamed. If the data show conditions are better than normal, then conditions are actually MUCH better than normal because of the expected negative impact of the hurricanes.

The longer-term effects of disasters on the economy are usually somewhat positive as construction work picks up to re-build, businesses modernize with new plants and equipment, and postponed purchases are eventually made. Of course, if a good chunk of the population moves out, the community’s economy will eat it.

Short term too T2! Arborist did us a favor and came to trim a couple trees yesterday, but only due to family connection.

Said he had about long term 200 clients begging him to come to their properties and will be back logged for next couple of years if not longer.

Told him he wasn’t charging enough, and proved it quickly just by showing him how much his big and needed pickup was actually costing him per mile.

Good to see such a hard working self taught 30ish guy, but he not able so far to hire any similar help.

Seems like the labor market is finally coming back into balance. Hopefully this means less wage inflation.

But… some would say more wage inflation is needed to catch up with asset (home) price inflation. Homes are still priced way too high relative to income.

How will this distortion be brough back into balance?

I look at a lot of properties. Home prices are declining. The massive increases are slowly being unwound. 10, 50, 100k reductions.

I wouldn’t offer more than pre 2020 prices for any of them. Look for empty homes with no furniture in the pics and track days on market.

Won’t be much longer until sellers will again take cash offers at reasonable prices due to forced circumstances.

Some places remain outliers, but this is middle TN. The market has been booming for years yet has cooled waaay down.

We just got back from an inspection in our favorite neighborhood which was once blocked off because the crime rate was so high. I saw a sign on one of the properties handwritten which said “Stop killing people”. The realtor, who was very helpful, said that business was dead as doornail. The only properties moving were people who were forced to sell because of job changes and investors unloading renovated properties. No one is lowering their prices and the market is frozen. This will continue until mortgage rates get back down to the low 5% range.

Love your name, Swamp Creature! Your last line – ‘This will continue until mortgage rates get back down to the low 5% range.’ That’s NOT how things worked in the past. When interest rates rose, prices came down. The low interest rates and easy money created this monster (bubble). From much of what I’m reading, we may be on the verge of a credit/bond crisis. That would be the equivalent of an atomic ‘bum’ going off in the housing market.

“That would be the equivalent of an atomic ‘bum’ going off in the housing market.”

FORGET IT! There will be no atomic bomb going off here anytime soon.

The Swamp is a unique market. Lawrence Yun would be proud. Real estate almost never goes down here. If you wait and look for a lower price, you will wind up paying more in the form of higher interest rates or higher price. I wish it weren’t that way but it IS what it IS. GET OVER IT!

You Silly Goose. You yourself said

“The realtor, who was very helpful, said that business was dead as doornail.” That says volumes. Prices are WAY TOO HIGH. Buckle up. Prepare for crash landing.

🚨

People always say they won’t lower their price until they have to. I’m not old enough but have seen it twice in my shorter life.

It’s always the same story the last one holding the bag is the one some of us enjoying buying from because it’s just amazing what you can pickup in times of distress from people who hold far too long.

Yesterday I overheard a conversation between 2 ladies, one of whom was trying to run her small health food store. She was saying that her regular job at a local department store here in Wisconsin was having trouble getting seasonal help for the Holidays, and how all of the regular department store employees where having to put in longer hours.

Customer service in these parts can suck. Especially at grocery stores, where a single clerk may be helping 8 to 20 people go thru the self checkout. Also, a lot of people stocking at the grocery store may not even be working for that store. Bread, HABA & meat vendors may not even know the current name of whatever retail store they are working in. It is just stop #6 of 8, or whatever.

OK. Where was I going with this? Oh, yeah. Here in flyover country, we haven’t been effected by all the fires and hurricanes. The economy is still based mostly on producing and distributing things. There does seem to be a lot of new condos and apartments being built. Overall, things seem normal, not the frenzy of speculation in the Sunbelt.

old g- …until the ‘Murican buying public truly acknowledges that ‘good customer service’ has costs, and is worth paying for, expect increasingly lower levels of it. Concomitantly, the necessity to actively improve one’s product knowledge&usage to purchase effectively in what is now, essentially, an ‘efficiency’-driven, self-service retail environment (at least until AI can replace those always-substandard, but still-too-expensive, organic-type service units…).

may we all find a better day.

In the last four year, since Q2 2020, GDP was rising 50% vertically, from

$20T to $30T. That cannot last.

Wait a minute…

From the low point in Q1 2020:

— “real” GDP (adjusted for inflation): +22%.

— “Current-dollar” GDP (not adjusted for inflation): +47%

So that non-inflation-adjusted growth of 47% included inflation of about 25% since Q1 2020.