And this, after years of being unwaveringly bullish in its housing market predictions.

By Wolf Richter for WOLF STREET.

CoreLogic, which owns the Case-Shiller Home Price Index, released its monthly “Home Price Index Forecast” this morning, based on the Case-Shiller data. After years of being bullish about home prices, CoreLogic suddenly turned bearish.

It forecast that prices of single-family houses, including distressed sales, would begin dropping on a month-to-month basis with the June reading – it just released its May reading, which was up 4.8% year-over-year – and that prices, as tracked by the national Home Price Index (HPI), would be down 6.6% year-over-year by May 2021.

“2021 will mark the first year home prices are expected to decline in more than nine years,” CoreLogic said. The last year-over-year decline in the HPI was booked in January 2012.

“Strong home purchase demand in the first quarter of 2020, coupled with tightening supply, has helped prop up home prices through the coronavirus (COVID-19) crisis. However, the anticipated impacts of the recession are beginning to appear across the housing market,” the report said.

The recent surge in pending home sales and in purchase mortgage applications to levels above June last year, supported by record-low mortgage rates, “continues to exceed expectations despite the severe recession,” CoreLogic, a property data and analytics company, said in the report (download). This was driven by pent-up buyer demand after the spring season was embroiled in the lockdowns, and spring demand moved into summer.

By the end of summer, under pressure from the unemployment crisis, “buying will slacken and we expect home prices will show declines in metro areas that have been especially hard hit by the recession.”

And by May 2021, the national Home Price Index is expected to be down 6.6% from May this year. All states are “expected to experience a decline.” The CoreLogic Market Risk Indicator predicts that 125 metro areas have at least a 75% probability of price decline by May 2021.

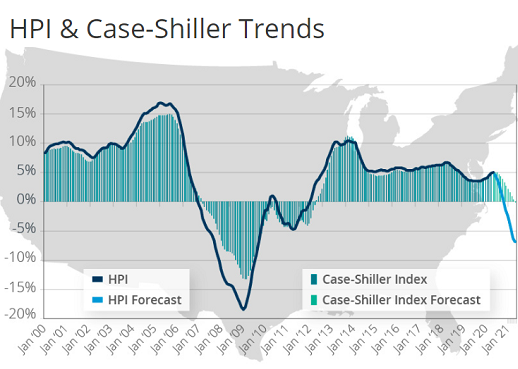

The chart below from the CoreLogic report shows two data sets: The Case-Shiller Index and its forecast through May 2021 (columns); and the CoreLogic HPI (black line) and the HPI Forecast through May 2021 (light-blue line). The Case-Shiller Index, which does not include distressed sales, sees disappearing gains in 2021, but no actual price declines. The HPI Forecast, which does include distressed sales, sees a fairly steep decline roughly in parallel with the first segment of the year-over-year price declines during the housing bust:

The impact of distressed sales becomes apparent during the Housing Bust, during which the HPI (which includes distressed sales) plunged more sharply than the Case-Shiller Index (which does not include distressed sales).

In order to analyze home price trends, the HPI incorporates the “repeat-sales” data from the Case-Shiller Index, where the prices of the same house that sold at least twice over time are tracked, going back 40 years.

CoreLogic sees some particularly bad vibes for states like Arizona and Florida that are now confronting “elevated COVID-19 cases and the subsequent collapse of the spring and summer tourism market.” This “perfect storm” will curtail home purchase demand over the coming year.

This time it’s different: Cause & Effect Are Flipped

The last housing bust occurred during an economic expansion and then became one of the triggers of the Financial Crisis and the Great Recession. This time, it’s the other way around. An economic and healthcare crisis, and the worst unemployment crisis in our lifetime, is hitting a fairly strong — and in many markets an over-inflated — housing market and triggering the downturn in the housing market.

“The forecasted decline in home prices will largely be due to elevated unemployment rates,” CoreLogic said. “This prediction is exacerbated by the recent spike in COVID-19 cases across the country.”

I’ve been on CoreLogic’s email list for years, and what stood out were the unwaveringly bullish forecasts of its HPI that turned out to be more or less on target. So this sudden shift is quite something, though it makes sense based on the economic conditions and the unemployment crisis now prevailing in the US.

Rents in San Francisco are still crazy-overpriced, but less overpriced than they were. Read… Massive Shifts Underway, Rental Market Reacts in Near-Real Time: Rents Plunge in San Francisco & Oil Patch, Drop in Expensive Cities. But Long List of Double-Digit Gainers

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Do the large price declines in urban centers skew this number?

I’m probably in for a drubbing but I’ll give it another go anyways. In the 92115 zip code there are precisely 21 sfr’s for sale (per Redfin), the majority of which are peripheral busy street junk. In what I consider my neighborhood, bounded by El Cajon Blvd, College Ave, Collwood ave and the drop-off down the hill at 54th st there is precisely 1 active listing. the other one you see is more of a town home. What’s happening nationwide and maybe in other parts of the state isn’t happening here. It just isn’t. Maybe it will and we’re late to the game but every realtor I talk to is saying the same thing, no supply, prices are out of control, no sight in end. We just lost a tenant who bought a place in a very poor part of town and paid $580k for that privilege (same house sold for $50k or so back in the late 90’s). I have my theories as to why this is happening in San Diego and I’ve stated them previously, but I’m really curious what others are thinking as to why this is happening.

A neighbor in nice, very middling hood in st pete fl pulled their house off mkt because they could not find one where they wanted to move closer to the school their child is in, about 25 miles away.

Only house left in hood now is way over priced, all others gone, with no one moving in, yet.

With owning a house as ”hedge” against the expected, likely, and majorly touted inflation, maybe most thinking best to stay put for now, versus possibility of not getting new financing due to increases of down payment and credit rate.

Lots of folks concerned with increase of virus taking out tons of income sooner and later, so not willing to venture forth until the whole shebang settles down.

With Shilling him self saying likely to see 30-40% drop in SM (stock mkt) coming in the next year or so, folks wanting to move up are not going to chance it, even if qualified at the moment…

ETC.

It’s because the realtors you’re talking to are delusional. Defaults, foreclosures, etc…These take time. It’s still premature. Realtors are literally ALWAYS optimistic. I’ve never met one realtor who is realistic. They are just like car salesman. They don’t like to believe that the market will get slow because they make less money on commission. I’m sure you know all this. Correct me if I’m wrong.

With all the houses moving in a day and sold thru the internet with buyers never stepping foot on the property why do Realtors even exist.

And when you visit redfin it talks about their 1% seller agents, where is the break for the buyers?

because when dumb people realize what they did – they’ll no longer have utilities and need people who know people that still have money

The agent who marketed and sold my house in San Jose was extremely realistic, and spot on: I wanted to list my house in the ‘hot’ months–April/May/June–but he convinced me to list in March, to beat the expected competition flooding the market. He was dead on; I had a buyer in a couple days at almost 10% above the ‘zEstimate.’ He’s an independent, did his marketing on social media and worked both ends of the deal and charged 3% commission (total). I’d use him again in a heartbeat.

He did say he was a bit of a ‘gambler,’ and would have gone through with an open house, but I had a solid offer $100K over asking and didn’t like the idea of strangers traipsing through my house with all my possessions in place. We took the offer, and spend a weekend in Yosemite instead.

ps. FWIW, the zEstimate is currently about $60K below what I sold for.

Realtors are not always optimistic. They are just lying to you. I was one for years. When they are telling customers that it’s a great time to buy a house, back at the office it’s different. They all own homes. You hear chatter about “Did you see the price on that new listing? I can’t believe that they dropped the price $50K and no takers. Where will it all end? I’ve never seen it soooo bad!”

They’re actually somewhat pessimistic about getting a listing. There are none. Not one of them is saying buy buy buy but are instead saying that there is simply no inventory. The more I research this the more I see it outside the area I usually focus on, 92115. You can’t find a listing north of the 94 for under 500k. Redfin is now pouring money into tv advertising in San Diego and the first thing they tout is that things have gone up in our region over 8% yoy. These are not normal times.

Bob, you must be a realtor or own a few homes. Thread after thread, you keep touting home sales and hoe there is “huge demand.” I often check listings on a few sites, including RF, and I have definitley noticed dropping in prices and homes on the market for a long time. It is delusonal to believe the economic downturn created by the pandemic hasn’t or wont eventually affect home prices in a big way. I’m hearing numbers upto 35% by end of next year.

I’m seeing the same thing in Rochester, NY. No inventory. Desperate buyers are bidding up prices big time. I’m now seeing homes listed at lower prices in the most sought-after areas to attract larger pools of buyers and fuel the bidding wars.

Hi Tony,

I am a real estate broker in Sarasota Florida and agree that we’ll see prices coming down – possibly more than 6% in Florida. We won’t see anything drastic until the stimulus runs out and the election in November passes. I’m gearing up for short sales to start up by the end of this year/early 2021. I’m notifying my buyers that prices will be coming down, but not immediately. Some buyers are waiting, but others are in a position that they need to buy now. Rents are extremely high in the area I work in, making buying more attractive, due to low interest rates. Should be an interesting ride ahead! It is unfortunate that people look at realtors like they view car salesman – but remember, not all realtors behave this way.

I have several friends who are RE Brokers, all of whom are also investors and we are all salivating at the prospect of a downturn so we can scoop up more properties and increase our wealth. They will actually make more money as did we all during the last downturn. So, you are wrong to generalize about RE professionals. Optimistic yes, but realistic too, as they live and die by comps which are driven by market conditions. Green eyes will lead you down the path of despair.

Tony, not all realtors are as you describe. I have been giving youtube updates weekly stating my concern about housing that mirrors this study. We are not all like car salesmen. The low inventory situation will begin to unwind in October as the permanent lay offs begin. Core Logic is wrong to say the virus is hurting our normal summer season. We don’t have a summer season. It is too damn hot!

Denial is a very powerful emotion Or they’re just full of sheet Foregive my Greek

In NoCo, nearly the same. New neighbor bought a tear down next door after house flippers went over the place, lightly, and doubled the intrinsic value, which is the lot. Maybe worth 1/4M. There isn’t enough lipstick for all these pigs. He paid way too much. He will probably lose it, when SHTF. Who knows if the property is even worth that? I put a low ball bid at the number, and lost sleep. Now a few buckets of stucco and the place is worth double my offer. I thought about doing the trick myself but again with the sleep problems.

I am from San Diego

What you are experiencing and what realtors are all true

But at the same time housing market is like a titanic and it takes time to turn

Last time it took 4 years in San Diego to find the bottom

San Diego housing is priced to perfection and a lot of big employers are now contemplated remote work and on top of this tourism is a big business in san Diego and Airbnb as well

Unless covid19 has no impact I see san Diego housing going down in next year or two.

San Diego housing has seen many boom and bust in last few decades..and I’d never say never

This has shades of 2005/6 all over again. Except that back then folks who couldn’t afford in the first place were buying through NINJA, stated income, and other types of horrible loans. I’m not sure the exact year but things certainly were turning south by 2009. I know a lot of folks who lost places from about then until around 2012. I suspect things will rise by stupid unjustifiable amounts for a few years and then correct, but not the 35% drop in one year they did 10 years ago, but they will correct. This all assumes, of course, that builders are allowed to build, which they aren’t. As long as all they’re building is apartment type homes that won’t help either. I figure the multi-family scene will see a much sooner correction, and it will be big, than the sfr scene as there are simply too many being built. In covid times would you want to live in a box? People will remember these lockdowns for a long time to come.

SD planners have kept a lot of open land, for hiking and recreation. Remember Prop A in Carlsbad? RE is about quality of life, as well as finance.

It will be interesting to see the extent of corporate layoffs after companies start to file their Q2 10Qs. Top line growth is going to be difficult to come by so its the expense line, and jobs that are going to get trimmed. Thinking with the uptick in COVID, CEOs are going to tell their CEOs to take a bit more off the expense line do while hair stylists and waitstaff got crushed in Round 1, mid-level management may take it on the chin in Round 2.

May you live in interesting times…

RE is a lagging economic indicator. Watch what happens next.

San Diego has been an outlier so far this summer with prices and rents rising more than most of the US.

It’s happening because people are just waking up to the fact that the optimal move is remote work, move out of CA, and leave California’s tax burden to the boomers.

Give it a couple of years. Remote work fixes everything. Even for those who for any reason are stuck in California.

Don’t tell that to the perma-bears on this blog. My wife and I have been in the mar!let for a home for a while. Everything in our price range is going for 20-40 over ask with about ten offers. What people fail to realize is that most people in San Diego who own homes aren’t losing their jobs. Meant people who rent here can afford to own a home but they’ve rented. Now they don’t want to be stuck in a rental anymore with all these stay at home orders. A hard sounds much nicer when you can’t do anything. Inventory is historically low and the amount of buyers is pushing up prices. Falling home prices is not happening here. Rising.

>We just lost a tenant who bought a place in a very poor part

>of town and paid $580k for that privilege (same house sold

>for $50k or so back in the late 90’s).

How did this happen while real wages have stagnated?

Va loan and mommy and daddy stepped in

It’s the Fed’s job to supress wages and inflate assets. They are very good at their jobs.

Part one, inflation courtesy the Fed, part two, wages have not stagnated for high end tech, business, and administration types, wages have been stagnant at middle class level.

Bob,

I have my theories as well but this probably isn’t the venue to share them. This I will say, I suspect that we will be soon seeing an exodus from your near inner city location to the east end of the county in the next few months. Inside sources tell me that there are lots of folks abandoning their overprices shacks for ‘parts unknown’ as a result of the current socio-political upheaval. (ie La Mesa) Look for prices in the burbs to plummet as a result.

I walked La Mesa after what they did and got some inside scoop on what happened that evening. One of my kid’s friends had to spend the night at our house because La Mesa was literally burning. I understand that the only reason sprouts didn’t burn was because angry villagers came down off the hill armed and told them to get lost. I took gobs of pictures as I spent 45 minutes walking the village so that when the media and politicians deny it ever happened I have proof. Union Bank was still on fire two days later. I’m not so sure that the burbs will plummet in price as these homes still offer the backyard and privacy that our elected officials want so desperately to take from us. What I’m afraid more of is that the businesses are going to leave. If we learned anything at all from the mostly peaceful protests is that businesses are expendable. We had to endure pandemic shutdowns and then turndowns. There simply aren’t enough police to stop these things and the public isn’t what it used to be. If it weren’t for those unknown angry villagers more probalby wouldn’t have burnt. The police station didn’t burn, wonder why?

California is a sinking ship. Having lived in San Diego County since 1960, I left last year and now do not even have a desire to go back to visit. The property we sold in east county, topped out in value in 2008 and never regained its former value up to now. The fact is the quality of life in San Diego is no where near what it once was, and it is deteriorating, as overpopulation, and government incompetence continue to impose ever increasing regulations and living costs on the public. Now with the bankruptcies of the State, and many municipalities looming, the costs of living in CA can do nothing except rise even farther. There are reasons that CA is one of the States people are fleeing in large numbers.

Proximity to Tijuana and the collapsing Mexican economy ever more rife with crime. San Diego is an escape valve and alternate place to live and commute back to Mexico.

Jdog you always have insightful observations I enjoy. In this case, I hope you’re correct and many, many, many more “oh my California” pearl clutchers head east. I hear AZ, TX and FL are doing great right now. Luckily, people can still find that nostalgic 50’s and 60’s mentality out there in the heartland. Oh scary Mexico.

I’ll still be here in CA enjoying the “sinking ship.” Hopefully with some additional housing opportunities.

Yertrippin,

Same here. I can’t wait for some of the congestion in San Francisco to ease (it already eased a lot with the tourists gone, and with people working from home). I used to live in Texas and Oklahoma, and I tell everyone around here what wonderful places they are, and housing is so much cheaper, and the summers are warm and sunny.

you guys are starting to sound exactly like the folks, many of them natives, screaming their heads off about how bad it is,, always,,, in FL

snakes all over, mosquitoes whenever ya go outside,,, gators actually coming into the house itself, not to mention hunting down dogs and cats and small children,,, etc., etc…

all true, of course, but that is just the beginning

that all went ballistic when my carrier did his fateful deed to make residential AC THE thing, and ruin the whole state for eva

Well, according to the current Covid-19 charts in AZ, TX, and FL there will likely be many buying opportunities…. AND, no mask requirements to boot. Freedom ain’t free but the discounts are coming.

Yes !!

Here .. supply is being controlled & sales are strictly channelled to in-house purchase.

And they are becoming very wary .. I rang about a unit in Preston, they pulled it off the market the next day which tell me .. “&” they are afraid of getting caught fixing sales & prices.

What a gift from God COVID-19 has been to the real estate market !!

Unfortunately the bank does not value real estate as a beloved & highly geared investor .. sweating it .. does & a realistic reduction in the property market will take place .. & soon.

That the COVID-19 miracle was able to slow down the blood bath for a time is quite fortuitous .. serendipity really.

Conspiracy theorists would have us believe it contrived .. imagine.

2 & 3/42 Kerferd Street, Essendon North, Victoria.

Now that Premier .. Our Daniel Andrews has locked down the staste of Victoria again .. auctions are on line & I have no chance for a successful bid here.

I can only wonder in earnest about here in Australia .. cause I know what our mob are like .. BUT .. what if monies .. PUBLIC & SUPER FUND / PENSION FUND MONIES .. were all heaved into the property markets .. (for who’s benefit ??) .. & now go explain who let it happen & do we have enough jail cells for the greedy perpetrators there of ??

Great stuff .. thank you all.

The forecast is interesting. The way I am seeing it society is batting around who is going to take the loss. Nobody wants to, so it’s currently being socialized as public debt. Right now prudent savers are eating the loss at about 2% per year so the Fed can keep assets inflated. Maybe MMT will steal it faster

Wouldn’t those savers adjust by cutting discretionary spending and saving even more?

I know I did, works for me. Sure, not what the Fed wants to see :-)

They have been taking about 2% per year from savers, but it hasn’t shown up yet because stock market gains have more than offset losses on fixed income. Most savers have a little of each.

It will get very interesting when stocks drop, stay low, and interest rates are remain repressed. At some point, the Fed won’t be able to prevent the stock price drop from happening.

2% Lol that you believe that! Captured by propaganda!

Savers are getting eaten at 5-10%+ annually. This year probably 20% as income plummets and costs of everything go up a lot. But at least their bank accounts and annuities and pensions have the same number of dollars in them!

Also, anyone getting paid in fiat is actually in the same boat as the savers, with the real purchasing power of their wages getting eaten at 5-10% PLUS per year. Which is basically everyone except the high exec class and the owners class who get paid in assets instead of dollars.

Interesting Corelogic is turning bearish on their analysis, they must not have talked to all the people still lining up to buy houses as I have seen many anecdotal evidence cited on here or when they say all states, they must not have included invincible markets like Southern California..

Wonder if Corelogic is the lone wolf insider now turning around the corner based on overwhelming data supporting the decline. I guess the fat lady won’t sing until Lawrence Yun turn bearish which is about as likely as when pig flys..

You realize it’s a future looking prediction right? It clearly states in the article above we are seeing pent up demand right now and things will turn South later.

There was a comment here on on HBB where someone said their corp apartment in Raleigh NC renewal was odd. Anything less than a year, rate increase. Sign for a year and 20% rate decrease. Almost unheard of, but it seems as if they had something forecast that others aren’t seeing. Which lines up with this CoreLogic data.

I heard a guy in Florida say he decided to vacate his apt because they raised the rent. When he informed the landlord, they offered to extend the lease for the current rent. The tenant says he decided to stay for another year.

I left Florida a few years ago when they raised our rent 7% on a renewal. Our income had dropped that year 15%. I expect to see a lot more of these decisions in the coming year.

I was thinking… if a huge portion of renters couldn’t pay due to job loss in the near future. Landlords start struggling… what would it take to get lots of renters that could pay to not pay in order to stress the landlords out and turn over housing inventory cheaper to the renters?

Something like a rent strike at the worst time possible.

That would be a popcorn moment.

There is nothing invincible about the Southern California market. I have seen its housing market crash several times. Anyone who thinks it will not happen again is foolish.

Lawrence Yun is the realty equivalent of Baghdad Bob.

I think the suburbs will experience an influx due to white flight, covid, and

low gas prices. We will see.

I live in Georgia, one of the top 3 or 4 states for unemployment claims. House sales are on fire in the middle class suburbs. Even in the face of tighter loan underwriting requirements. The sales are closing not pending.

Low housing costs are such a BEAUTIFUL thing!

Why on earth did this take so long? Wondering when the roughly 10% of mortgage debtors will resume their payments. Only after those who cannot foreclose we’ll see what fair housing pricing will really looks like.

Yeah. Just think. Once Covid eventually blows over, if housing costs are still low we might actually be able to afford American made cars, taxis, medical bills (well- maybe not), hotels (if any are left), boat rentals- you name it. We could possibly even afford to buy American made goods. What a thought. It’s almost radical.

Ahem.

And…the Fed has stop the money spigot!

Banks have already tightened lending standards.

And Mel Watt “retired” last year as the Director of the Federal Housing Finance Agency.

“An economic and healthcare crisis, and the worst unemployment crisis in our lifetime, is hitting a fairly strong — and in many markets an over-inflated — housing market and triggering the downturn in the housing market.”

I’m so skeptical. Saying home prices will fall is in some way like saying stocks prices will go down because of earnings decline, and we all know earnings have nothing to do with soaring stock prices for the last 10 ish years. More QE and we might see institutional investors flood in. Who knows?

Forecasts down to 1/10 of 1% within 9 months probably means they really know.

The drop by next year is going to be huge. Small landlords are selling with tenants in place, just to get out, tenants probably not paying. I already see some tenant occupied listings selling at ~40% off from last year. These are all small condos. The larger homes are all on the rental market for prices nobody can afford.

It will take landlords a long time to get non paying tenants out, then who will they rent to when everybody is unemployed, or has bad credit from being in forbearance on rent, student loans, credit cards, or utilities.

How many people will be in foreclosure by the end of this year, too many. They won’t have the credit or income to qualify for another house for a long time.

Then there’s the covid dead, who also won’t be in the market.

I wouldn’t want to own a REIT anywhere in the world right now.

PETUNIA

BTW – I would like to go on record of saying I enjoy your contributions on WS – always well thought out and often backed with stats and/or logic.

On this topic, I must disagree with you. The Case-Schiller and HPI are national numbers / trends. RE is both cyclical AND local, as we know. You stated Landlords are or will be selling tenant-occ homes for cheap. Well…..maybe that is happening somewhere, but since COVID, I have investor/buyers scrambling to buy my tenant-occ homes for my asking prices. This was happening before COVID, but the interest level just seems to have increased recently. This is, IMHO, a local thing. I am in Kansas City MO and the investment return on the turn key homes I sell is 20%+ annually. It is a known commodity, tangible and fairly predictable.

Whether it is people flocking to the Midwest (KC), the fact that you can buy a remodeled home for well under $100K (mine are typically $65K to $75K), or the fact that there will just always be renters – I do maintain certain markets will NOT succumb to the pending dangers outlined in this excellent WS article….OR…..alternatively, will be affected much less.

In Cleveland – markets with strong demand but known rental markets like Lakewood Ohio have been receiving 20-30 offers when investment properties get listed.

The last duplex that got listed went for 180k 50 showings and 23 offers in a day

Victor,

What about SFH prices in nice areas East or West? Lots of larger companies sold recently in CTown like FC and AG.

20%/year profit?

Are you renting ~$70k homes for $14,000/year?

Petunia has it right for most cases in most places IMO after 60+ years in RE in FL,CA,OR,TN, and having made profit in all those.

Some places will do relatively well with short and small declines, others longer and deeper, depending on many factors.

Last time, 08-11, a friend was buying many houses on the steps of the courthouse, fixing what was needed, and selling or renting and refi within a month or so for approx ten times the initial price… obviously, very low rent district, eh?

And for dyno, it’s ROI, not return on price of the house, huh

Yes

20% return is why everyone is leaving the stock market. /sarc

Beardawg,

I know KC, spent way too much time there years ago, in the Overland Park area.

Your price point is protected because you service a low rent, probably subsidized tenant. Welfare and section 8 tenants can afford to rent from you regardless of employment situation. You know this is not possible everywhere, which is why you invest there.

PETUNIA

You are correct in that a good number of the tenants are HUD tenants in metro KC and other similar Midwest markets. This locks in 20%+ annual returns which is especially helpful during pandemic times. In my case, about 1/3 of the tenants are HUD. Other tenants with solid pandemic-protected employment make up the rest.

Lower end SFH rentals are a viable high return investment, but I do understand they are not for everyone. I do believe, however, this class of real estate is pretty bullet-proof against the fears and realities of the price drops cited in this article.

The only logic I see is prices dropping in the cities with massive inventories while rising in the burbs as there would be a shortage with people leaving.

I rather wait for the end of the 4th qtr before I can discern what’s going on in the housing mkt. Feed back mechanism remains distorted due to Fed’s pouring Trillions and suppressing the price discovery of assets, all over including housing mkt!

30M have lost the jbo and more to come in the coming months! Wait and see!

Where I live in Boston area, inventory is low and I’m seeing properties list and go contingent sometimes immediately. I’m in a diverse suburban area and the properties have always moved and still are so far. Still say we won’t see a real estate fall until we see stocks fall, and the Fed has outlawed stocks going down.

Here in the North Bay (Marin and Sonoma) inventory is down and pending sales are up substantially from last year at this time.

A co worker listed two homes last Friday, one a suburban ranch and one a country property with a few acres.

The country property needed about $125K in work, both were priced in line with Comps.

Both in escrow, both with 9 offers, both sold for more than asking, all cash.

Will this last?

No, and I think Corelogic is optimistic, 10% down by next may sounds about right.

Those 9 offers, either they are the smartest people in the room in hindsight or they suffer the worst FOMO ever or just have so much money to burn that job security in the near future is not a thing for them. I guess only time will tell which camp they belong.

Phoenix-Ikki,

The people who have been doing well the last few years have been doing very well indeed.

If you are concerned about increasing social unrest moving to what you consider to be a more stable area makes good sense and if you are moving from the more Southern Bay Area Counties prices here may seem cheap.

That said I’m seeing the typical signs of a top, some people paying way the heck more than they should for some properties while some pretty nice places I consider reasonably priced based on comps sit.

The Economy here in Sonoma County already took a heavy hit and we reopened too soon, the next shutdown will hurt even more…unemployment is already at an 80 year high according to the local paper.

Reality can be obtrusive and very rude indeed when it shows up, and it always does.

It’s gonna hurt, starting this fall.

Don’t worry. More free money coming. Reality will hurt, one day. Based on what we’ve been doing, we are making sure that day will be REALLY, REALLY painful.

Bacon at 50 bucks a slice will hurt no matter how you look at it ;)

As they say, all RE is local. Like Tom Stone mentioned in Napa, my little piece of paradise in Naples, Fl has seen a surge in prices and a decrease in inventory. There were 3 homes listed on my street in the last 30 days between $1.7 million and $3.5 million. All have either closed or are pending. There are no other listings.

I think 2020-ish is peak Baby Boomer retirement. I know two who are selling high equity Charleston SFRs for Naples townhomes/condos.

Naples is disconnected from the rest of the market. I know a couple who bought a waterfront house in Naples for $1.8 million and tore it down to build an 8500 sq. ft. monstrosity for two people. Rarified air on that street.

Disgusting excess.

@Zantetsu – I can’t necessarily disagree; however, I have a question:

Is it also “disgusting excess” when LeBron James purchases a 2.5 ACRE, $39MM mansion in Beverly Hills?

Or is that okay?

Yes, that is even more disgusting. I’m not sure what brand of logic you think I’d be following to answer differently.

AAAH yeah tmj,,, ”Naples on the Cuff!”

Moved there in late 1950 era, when gulf front dirt was $100 per front foot! Left there mid sixties when same was $1,000 pff…

Glen Sample ruined the place when he came down, dredged most of the best oyster beds to make Port Royal, and it never the same ”paradise” since then, and now pretty close to the worst example of ”developers gone wild” ever…

Glad to hear somebody still thinks of it as paradise, in spite of the facts of the extensive pollution from the disgusting outflows working down the coast from the big O via the Caloosahatchee, etc., and almost constant red tides, gulf dead and worse from oil spill still there, not to mention the dirty and dangerous beaches now every weekend,,,,

Just a couple questions re naples on the cuff, and then i will let it go once again:

Do the cops still stop every car they don’t know and for no reason?

Do all the black folks have to be off the streets and back in the quarters after dark, or get the ”shyte” beat out of them, unless some white kids are driving them to Nick’s to buy booze for them, etc?

Do all the ”cheaters” from Miami still arrive at the Beach Club every weekend?

Do all the (white ) kids still get drunk every Friday and Saturday because there is nothing else to do to pass the time?

Does Mr. Briggs and most of his cohort still leave at the end of March or early April?

Is the majority of the area still well below the 12 feet above the dirt that the surge from Donna established as the very lowest ”safer” building limit, and does anyone pay any attention to that?

Can one still run from Doctor’s Pass to Gordon Pass on the beach without getting shot at?

Is shark fishing still illegal on the pier because a tourist might get scared to see what is just off shore ALL THE TIME?

Look people. There’s a couple of truths:

1. Rich people will always be afford things. So certain zip codes will always do well. The housing market at Atherton, CA will always be hot for example.

2. CoreLogic looks at many zip codes, not just rich people’s zipcodes. Wait till the expiry of all sorts of forbearance, and the party will get started. The government will try to extend and pretend, but forbearance is NOT forgiveness.

Florida? Don’t worry by the time the virus is done over there, there will be plenty of inventory.

I’m definitely seeing pent up demand in Solano County being met. I’m sitting on a good down payment and ready to pull the trigger if an opportunity presents itself but truth be told it’s scary as shit so I think I’ll have to wait way longer than next May.

I live in Benicia which is on the edge of Solano County North of Contra Costa. I’m 45 mins/hour away from SF. Either by Ferry or Bart. 40 mins or so from wine country. Beautiful area. Unlike our surrounding counties, our confirming loan limit is around $510K. Most other counties are $700k+. So to my surprise a hand full of homes in the $750-$910k range are on the market and sale pending and eventually sell within a month of being listed.

Not sure if these are techies fleeing the city to the suburbs but I thought jumbo loans were hard to come by nowadays. What gives?

I am not sure about that. It’s very easy to build a lifestyle that is extremely expensive. Depending on how you figure it we are somewhere between the 90% and 100% percentile on stock valuations. If we fall to the other extreme which is usually what happens even a lot of the rich will not be able to hang on.

Valuations are the highest or most extreme ever on record, maybe of all time looking at the next million or so years. Even in 1873 valuations weren’t as stretched as today.

Rich people have plenty of assets but little or no money. This became evident during the last downturn. There were some hella bargains in the pawn shops of Beverly Hills area, enough so that the LA Times did an article on the phenomena.

Cause and effect are flipped? Rising housing bubble led to false sense of personal wealth, which led to increased travel and goods movements, which led to greater spread of the nasty bug, which toppled the over-hyped economies. Land is always at the core of collapses, and excessive speculation is the driver, pure and simple. As long as this problem is not dealt with, there will always be another crash coming. It’s like handing out driver’s licenses to people not even qualified to tie their own damn shoelaces.

And the hifh housing prices were due to low interest rates due to Central Bank intervention due to private banks running our economy due to the banker class being overrepresented in politics due to the Axis losing WWII.

Where does one stop?

Boise, Id breakdown.

Tons of out of state plates from WA, OR, CA, IL, TX, AZ, CO, FL, NY.

Multiple offers on almost anything priced in-line with market.

New homes are being bought 4 months before they’re finished.

Word on the street is not nearly enough inventory coupled with extreme demand.

And this is annoying. Because when the healthcare system collapses in this state, where are these homeowners going to flee back to? Many of these out of staters are trying to escape to some imaginary land of freedum, unaware of the pending decline. Idaho is dead last in Covid testing and is now spiking up. It’s terrible for education. And there is little infrastructure.

There are also “older” homes here that are not moving at all. For example, I can think of four homes in my immediate area on the market, each less than two years old. No one is interested for some reason. Maybe because they were purchased by idiot Californians who do not see past their nose. I imagine the same types are heading here now.

Similar in Denver at the moment. No one selling, homes that are going quickly.

But it feels very much like Wile E Coyote spinning his legs a few feet past cliff. People are losing jobs on the low end mostly, this will filter up through the economy to the home buyer demographic unless C19 vanishes. Not likely. Prices will come down.

That said, all RE is local and always will be. Not everything is lock step in sync. Denver didn’t run up in the early 2000s, then did starting around 2015. Things go up and down everywhere. But with Fed money and artificial supersession of interest rates and limits on homebuilding, it’s a pretty good bet that prices will rise long term in places that people are moving to.

Places people are moving from, like IL, CT, NJ, totally different story, I would not make long term bets on appreciation in those states.

Some of you citing the recent surge in home prices due to low supply didn’t read the analysis. They noted that. Yes, we are experiencing a temporary bubble due to low supply / people afraid to sell due to COVID and high demand / people wanting to leave their apartment.

The question is whether you think this is a long term trend. I think that’s almost impossible. This short term market shock will lead to home appreciation stagnation at best and home price values correcting at worst.

Here in SLC, we have seen many homes being raised 100k their original price. However, the homes above 550k are NOT being picked up by pretty much anyone. Prices are hitting a literal wall. Wages have not grown to account for it and unemployment certainly isn’t helping new buyers enter the fray. There is more bad news ahead than good.

San Diego has failed for decades to produce enough sfr’s for what is actually needed. Thousands of houses unbuilt for years and years has led to this problem. Lots of multi family cubes with fancy flat roofs and shiny letters on the front are being built but not sfr’s. SFR housing prices in the greater San Diego area will rise for a while, a long while.

When houses arent built, they are just telling the young to leave to non-NIMBY areas.

Long-term, it’s the optimal move for the young anyway. NIMBYsm turns places into 3rd world countries by fabricating homeless and ruining schools because teachers cannot afford housing.

Teachers, nurses, firefighters, police…..you’ve got now idea how many of them live in Temecula. Or just move.

Why do buyers need jobs? They just need the stocks to go up. And the Fed is doing that. If price hits a wall it just means the Fed needs to do more QE to make the stocks go up more.

At an open house in Newport Beach today, I saw a long line of buyers with their agents waiting in a line to see a property. There were about 15 buyers waiting in line while others were searching for a parking spot just so they could get in line. The home needed work and was nothing special. I have never seen that before.

If people are truly educated about the coming stagflation, then perhaps they want to get out of the dollar right away and into tangible assets. That is what I am attempting to do but have been in awe of the buying frenzy both in real estate and the stock market (i.e. only gold mining stocks). So, my theory is we are seeing smart people with funds front running what is coming.

Mid Vancouver Island.

Listed 30 year old rancher July 1st. Advertsing started on July 3rd, as did showings. Basically, 2 showings per day.

First offer day 2. No counter offer made by us on lowball, basically told them to pound sand.

2nd offer day 3, same prospective buyer.

Day 4 (today) they accepted our counter offer slightly less than a 1% reduction from asking.

We could have held out for full price, but we live 1 hour away and it has been a hassle in many ways. Plus, we are paying for yard maintenance and we wanted it to be gone just in case Covid hammers activity.

Sold in 4 days. The advantage we had was that the house was empty, so easier to show. Plus, we have no active Covid cases on Vancouver Island. RE agents wear masks, prospective buyers had to keep their hands in their pockets and also wear masks, and any touched surfaces wiped down with disinfectant after each showing.

I think prices will be dropping around here this fall. Our Covid infection/rate is less than Europe and on par with S Korea, but it is a World economy and the US is closing in on disaster. It can’t be good for anyone, or anywhere as knock on consequences are sure to follow.

regards

Update:

Young family bought the house which really pleased us. The neighbourhood is either young families, or retired folk with a few bucks. Nice quiet street for road hockey.

The reality is probably at least double. In the Commercial, people are telling clients hotel values will “likely” drop 10-20% but when we model things out the reality is more like 30-40%. Gotta give people a soft landing, otherwise no one believes it. This crash will be hard. Housing values are highly correlated with unemployment and unemployment will be unbelievably high for a long while.

Making money on the way down. Selling over and over at a new discount each time nudged by drops in prices so they can bleed more suckers before the bottom. As for employment, it could go up later, but at lowered wages across the board once things get bad enough to cut in to those who thought they were secure. Such a change could force a re-design of the type of housing mix being built in the future. The big question is who the heck is going to keep paying for a stream of high tech toys if they aren’t making money from owning them in a dead economy? Maybe Ma Bell and her ugly black handsets might return along with the one car family.

Ma Bell returned long ago under a collection of pseudonyms, except Western Electric and Bell Labs that were moved to Europe and then to China.

I remember the frantic froth just before the last RE bubble popped!

Home were selling a day or two after they went on the market.

Offers over asking price were common.

The busboy is flipping condos pre-construction.

I’ve seen this before. The last crash felt and looked just like “this”.

Yep, it sure does look the same to me too.

However, now that I have more experience, I also see some similarities to high frequency trading(HFT) strategies being played out in some of the described real estate markets.

The comment about multiple houses on one street being sold almost simultaneously with multiple offers, mirrors a common HFT strategy. It creates the illusion of demand, allowing prices to rise, to generate a profit. The stink factor went hyper to me.

Yea, I remember people were flipping homes for $100K profit days after purchase, before they could even close escrow.. Then a multitude lost their shirts….. in a crash the RE brokers said would never happen…….

Anyone still drinking Odwalla?

They’ve just been shutdown. Another 300 jobs lost.

But don’t worry, the BLS will create millions of jobs for next month no doubt. What’s 300?

re: “Anyone still drinking Odwalla? ”

I rolled the dice a couple years ago–there isn’t a lot of choice in a hospital cafeteria–and survived. No COVID, either (yet). Coincidence? Maybe not.

Brooks Brothers just went bust too. But who needs work clothes anyway. Not going out either.

One fact you can take to the bank. In a few years Blackrock will own a greater percentage of the housing stock than they do today.

Correct bt,

When we ”had” to return to tpa bay area summer15 to take care of very elderly in laws, we found most good props already in contract to PE and hedgies, and those less good kept close by banks waiting to sell to them.

Clearly, those entities, buoyed and benefited all the way by free money, could and did drive the local RE mkt for SFR much higher than it should have been, and was just a few months earlier, before the free money was available. ( I was watching every day when the mandated move was imminent. )

This time, literally, ”gods/great spirits only know” for now, until and unless some sort of restrictions are placed and placed very clearly and communicated equally clearly, on the folks with the current Trillions of free money..

Time and enough to stop all this free money malarky ASAP. And let the chips fall where they do.

Now the PE firms buy portfolios of homes straight from the banks, hundreds at a time. The homes never come on the market where real buyers can bid on them. This needs to be stopped by legislation.

Stopped by legislation, or by organized militant squatting of vacant PE owned homes by disenfrachised homeless citizens :-\\

Any way to build indexes online of PE owned homes? That dataset being visible might help put some negative pressure on the practice.

Step one… how to find all the homes owned by Blackrock or American homes 4 rent.

Neo-feudalism for thee.

Not much sales activity in my area. One house wildly overpriced on the market for a few months. Two houses came up this week reasonably priced so I should get some idea of the current market in this area soon. But as to the general housing market, to me, CoreLogics’ numbers make no sense. The Fed/Gov can no more let the housing market crash then they could let the stock market crash. We are going to see a blizzard of money printing this year and next, and no significant fall in housing or stocks in my view.

RickV,

“We are going to see a blizzard of money printing this year and next,…”

The money printing started reversing three weeks ago:

https://wolfstreet.com/2020/07/03/qe-unwinds-feds-assets-drop-for-3rd-week-another-76-billion-3-week-total-163-billion/

The fed has been doling out massive amounts of money to folks to stay home and not work. A lot of people are making a lot more than they were working. Those folks are probably not the home buyer demo but it’s still money flooding the market. As for all this corporate money, that’s another story. There’s gobs and gobs of money being sent out to businesses left and right. Money is being granted to business for ppe stuff and there’s no oversight as to how it’s spent. Tremendous amounts of money is going into the PPP and as long as you structure your payroll correctly you don’t have to pay it back. I’ve got SBA guys pushing no interest (for one year) loans of $150k on me and if you have more than one business you can get more than one loan, again, with no restrictions or oversight; the eventual interest is in the 3’s. Home loan refi’s are dropping payments all over freeing up money and all the forbearance stuff will also free up money. I called for one and got it by simply pressing a few buttons on the phone. We’ve continued to stay current but I could have stopped paying and pocketed the rental income money for several months. I’m certain some folks are doing just that. There’s no doubt there will be some fire sales on properties but probably mostly commercial stuff. Anyone waiting for foreclosures to make a buck is going to be in for a long wait. With forbearances of a year and all the time it takes to finalize a foreclosure Trump will have landed on Mars first. This is assuming a foreclosure will actually happen, which it won’t, considering you can sell you place for more than the note instead. These are times of free to practically free money combined with blessings to not pay your bills. Get yours while you can because we’re in for big time inflation sooner than later. Look at food, it’s already begun. All this printing of money and subsidy money flowing into society will catch up with us all and it won’t end well.

Good summary B,,, thank you,,, please keep commenting on here, especially about your local situation in place and time!

Also, as an aside, you may want to add to your ”handle” to ensure we wolverines are able to differentiate

VintageVNvet,

I’m somewhat new to posting on forums so guaranteed this will sound like a stupid question…do I simply no longer put “Bob” and put some sort of funny or identifiable name?

Bob,

There are other “Bobs” here, so it’s helpful if you add something to Bob, such as Bob01, or whatever. This way, people know that this Bob is not that Bob.

Also, it’s helpful putting the name of the commenter you reply to at the beginning of your comment, just like you did with VintageVNvet. Otherwise, it can get very confusing.

Well, it was either that or Chicken Little.

thank you all, I enjoy posting here and will now be known as “The Bob who cried Wolf”

Pretty good article on the hedge a week ago by a respected analyst saying the next time asset prices drop the Fed is going to have to print some more. He had a a reasoned argument.

Who knows if he is correct? Does anyone doubt now that if the Fed feels like it is needed they will buy stocks? Some say the current leveraged vehicle the Fed is using is technically illegal because the taxpayer can suffer a loss under the program which makes it fiscal policy. I guess they haven’t started the leverage yet, but will be interesting if they get sued.

Quoting a friend of an acquaintance;

“Real Estate is HOT HOT HOT!! right now!! If you have any properties you have been thinking of selling… do it NOW!!”

In other news, while RE agents may always be optimistic in public, some of them are now privately training for deflation. As mentioned privately by a agent friend of mine.

Markets against people, people against markets.

I saw a whole lot of great answers to the question I asked earlier and want to also thank Wolf for having this forum for us to exchange ideas. I recently posted this on another site but it really warrants repeating here. This is why I think things are out of control with regards to sfr’s in San Diego. Maybe it holds true elsewhere but this is what I think is happening here:

In the 92115 zip code in San Diego there are very few sfr’s for sale. Every realtor I know is saying the same thing, there’s no inventory. This has a huge affect on the total sales. This isn’t to say things are rosy as they are anything but rosy. People aren’t selling and builders spent the last 10 years building COVID cubes with nice gyms for the millennial crowd. Now that they got stuck in a box for 2 months and had the spouse chirping in their ear the whole time they’re desperate for the white picket fence and swing in the tree. The tards running the cities and states could only think two things, small cubes of people stacked on top of each other and public transit. Once the little millennial misses starts popping out the rug rats she ain’t gonna want to be downtown anymore, too. Of course houses are in demand. No building of them, no existing inventory coming onto the market, inner cities being burnt, and locked up in boxes for two months, what did you think was going to happen?

Bob, any comment on vacant apts in that massive upscale complex next to I15 by Mira Mesa Blvd, maybe 500 units, little stacked cubes, built about 8 years ago. I always considered I would prefer to be in jail then live there.

Also 92115 is SDSU area, what is going to happen to all the rental housing if college does not reopen?

I know the place as I drive by it every now and then. It seems it was or still is in a state of eternal construction and must have at least the 500 units you figure. I would use that as the poster child of covid cube construction and, likewise, would prefer jail. I’m not surprised there are vacant apartments there but don’t know a whole lot about it other than what I’ve seen.

As for SDSU, we’ve been pretty fortunate with getting our stuff rented but it is trickier now SDSU is floundering on whether they want folks on campus or not. My boys go there and are pretty pissed about paying full tuition for online studies. If all I had was online I wouldn’t pay rent to live close-by. That being said, the market here is flooded with available rental listings and it seems that every street has at least one ADU under construction. ADU’s are basically what we used to call granny flats. When they build these near the university they typically cram 3 bedrooms and 2-3 baths into a 1200 sf footprint. This is in addition to the existing house which, for student rentals, typically has at least 5 bedrooms already. Basically, the market is soft and supply is growing. That’s about to change, though, as Trumps policy of revoking visas for all online foreign students seems to have thrown all schools into a frenzy. If I could include the email sent by the school in this post I would. They’re concerned. The bigger worry is that the college area is basically a college town in its own right. All the business that falter over summer then thrive when school begins. Even with store openings everything is empty. The typical student hordes you see this time of year aren’t materializing. We’ve frozen our rents and are actively making our places nicer to attract what’s out there. Fortunately, all of our stuff is more family oriented which I think will be easier to rent than a 5 bed house with a 3 bed in back. If I was a student I’d look for the smaller place first.

Following your post here’s one of many items which spells doom for San Francisco, or at least until some serious political and social reversals occur there:

“San Francisco, population 865,000, has roughly the same number of dogs as children: 120,000. In many areas of the city, pet grooming shops seem more common than schools. In an interview last year, Peter Thiel, the billionaire Silicon Valley investor and a co-founder of PayPal, described San Francisco as “structurally hostile to families.”

https://www.nytimes.com/2017/01/21/us/san-francisco-children.html

Note, that story is over a thousand days old. Schools and the streets are now far worse crimewise and relative to state funding, plus the virus. Marin County sure is looking good to families that can afford it.

As house prices start to quiver, had a look at the price of gold in the UK today (8th July)…its £1440 an ounce, as high as it has ever been………somebody, somewhere feels a tad scared…..

i always thought that rising real estate pricing

was driven by new demand.Now that foreigners are

being locked out of America that has to effect prices

to the downside.

Up in Canada its 100 percent driven by the Chinese. Nothing else matters.

Top immigrant group to Canada are Indians, not Chinese.

Although, given what is happening in Hong Kong, I’m sure there will be a surge to Canada soon.

Too many known black swans hovering over the country to predict anything. Americans have a strong normalcy bias and will disregard most bad news until it lands in their lap. Take Michigan. 21% unemployment, U3 for Pete’s sake, with the auto industry more or less back to work! What will unemployment rate be with the hospitality industry going back to work at a shrunken capacity? 15%? How can house sales thrive in this?

Look at Spain to see what will happen in the future.

Unemployment in Spain stubbornly refused to go below 14% even during the “good times” in 2018 and 2019 and hasn’t gone below 10% since the Euro Bubble imploded back in 2009. Mortgage originations have remained repressed: even during the “good times” they never exceeded 40,000/month, less than one third of their 2007 peak.

Yet real estate prices are in Cloud-Cuckoo-Land. While this is somewhat understandable for hot tourist destinations like Barcelona or posh places like Bilbao it’s completely out of whack with the situation in the rest of the country, where the double pincer movement of out of control speculation and flight from the countryside is creating a massive stock of unsold properties.

I shudder to think at what the unemployment rate in Spain must be right now (25%? More?) but I strongly suspect real estate prices won’t budge and will probably start to climb again at first occasion.

Which leads us to the vital question. Who is buying? Mortgage originations and the combination of new and existing home sales don’t exactly convey the image of a booming market full of those mythical “all cash buyers” and even more mythical “bidding wars”.

The image I see is that of a whole nation under a powerful collective delusion that’s using every trick in the book (including the return of the infamous 100% no money down mortgages) to keep said delusion going because it reminds them of a brief time frame when the sky was the limit.

Delusions are difficult to break free from, but if my fears of 25+% unemployment prove to be correct this may just be the shock needed.

Pre-2008 was the Land of Cockayne for Spain, and they long to get back there.

Well, there IS nothing else to cling on to but that delusion embodied in an absurd historic real estate valuation.

It’s very hard to wean oneself off the feeling of self-satisfaction and success that comes from contemplating those inflated numbers.

Friends say their relations in Italy are just the same.

And really one could say much the same thing about Britain, although no one quite realises what has happened yet.

People in Spain should listen to that infamous Steve Earle song, CCKMP. ;-)

The problem with Italy and Spain is exactly the same: mortgage originations and total sales (new + existing) don’t support the silly prices, especially against a background of large unsold inventories.

But the problem is another: the inflated numbers are just that, numbers. Where are the buyers? Outside AirBnB hotspots such as Barcelona and Florence there aren’t exactly those long queues of cash buyers some folks here seem convinced exist: perhaps they are like the Loch Ness Monster. You need to be a believer to see it. ;-)

Maybe I am not as successful as all the “playa” around here who sell in a few days 15% over asking price after a ferocious bidding war among all-cash buyers, but my experience in the Italian real estate market is dismal to say the very least.

And the new development those scoundrels in the town council approved (goodbye woods, hello concrete monstrosities) sits there empty and unloved. The only winner is the council who pocketed €90,000 in impact fees, a lot of money for a small town which apparently has already been squandered since there’s no money to resurface the roads…

At least Spain has great roads, I hope to be there this Fall.

TTFN

MC01,

I’ve read similar accounts of what you wrote about Spain applied to ither southern European countries, like Italy for an example. There must be some sort of compensatory mechanism like a black market. I would guess that the underground economy in Spain is thriving.

Brooks Brothers just filed for bankruptcy.

I’ve been in N. Florida for 2 years now….as a refugee from California, and SFR’s, multifamily and even warehouses, and some other types of commercial sell fast and at listed prices here. All real estate is local, as we all know, and if prices are declining, it is probably in the large metro areas…..Atlanta, Philadelphia, etc, as examples just off the top of my head. These are the areas which will probably see more rioting and other Marxist types of behavior and become less and less attractive. On top of that, taxes are no doubt going to rise faster in these metros, and in states which already are very liberal and have high tax rates, which will further encourage people to move to Arizona, Nevada, Texas and Florida.

RE: and in states which already are very liberal and have high tax rates, which will further encourage people to move to Arizona, Nevada, Texas and Florida.

Should be lots of available RE in your mentioned States as Covid continues to increase at an exponential rate. Of course over at Zerohedge many commenters still say it is a hoax. It should be an interesting summer, sad, but interesting.

I have a friend who lives on West Coast of Florida. They’re surrounded by MAGA and miserable. Not sure oceanfront RE is worth it, given the political climate.

Them MAGA folks rioting in the streets and looting the place?

Opportunity: SPV to buy homes, securitize, sell security to investors. Homes can either be liquidated to wealthy investors around the world, or can serve to generate a rental income stream. Selectivity regarding renters is a value added. Renters waive any rights to habitate without paying rent.

Where are those renters coming from when the collegearkets will be tough this year, and immigration evaporates?

Do they give market by market projections? I’m moving to Arizona and looking to buy in the next year – planning on watching to see what happens until February-ish at the earliest.

Mortgage applications to purchase a home up 33% year over year.

…….and prices are going to decline?

Not in my area. Inflation is coming. Gold is exploding.

The bean counters don’t get it. The fed will just keep pumping until the value of the dollar drops…..making everyone spend.

The reason the market is going up……insanity and as a hedge against inflation.

In this kind of situation, people may just be scrambling to bail out of where they have been and thought they were going. The economy has tanked far faster than the dollar can fall, even with money printing. The unemployed that did not run back to work are not getting rich. They may have realized that their wages have not covered their basic costs. They take on debt which allows their employer to make profits by not having to shell out the real cost of living. They are just trying to tread water..it is debt servicing, not discretionary spending. It does not automatically produce wild inflation, and down the line it could result in massive deflation along with death for those who hold no currency. Printing is not leading here. It is following and far behind what is needed just to keep afloat. Yes, some folks are getting what they shouldn’t…policy screw ups abound as usual (FUBAR).

Corelogic.

Isn’t that special. Someone actually thinks logic has something to do with Fed policy.

How qwaint. Corelogic this:

QE of 20-50 trillion, if needed, to make the stocks go up.

There’s a totalitarian government taking over Hong Kong, and people are still not panicking and fleeing the country. I’m sure there are many people with substantial equity in their real estate holdings in Hong Kong who could sell now and retire on that money. Instead, they’ll be spending the rest of their lives toiling to earn back what was given to them for free. (I don’t mean to sound like I can predict the future, but in this case, I simply can’t see a good outcome for investors in Hong Kong real estate.)

I graduated with a degree in computer engineering in May 2000. I wondered why all the engineers who had been putting money into tech stocks since the eighties didn’t just call it quits and retire on their lottery winnings. I watched them lose substantial wealth and spend the next 20 years working to earn back what they lost.

Maybe this time around price won’t go down in nominal terms, but in investing you only make headway if your net worth goes up faster than everyone else’s. You have to ask yourself, who are the suckers at whose expense you’re gonna get rich? Real estate is so safe and effective as an investment because you get to steal the paychecks of your tenants and you don’t need to use your own guns as a threat (the government will provide the threat of force when tenants don’t pay). You know exactly who the sucker is in the game (renters). Another possible answer to the question is that the people who trade their hard asset (real estate) and become holders of cash are the suckers.

At the same time, I believe it’s impossible to prevent more and more price crashes in various asset values in the coming years because when the trend is up and people pile in, at some point you always reach the point where all the money-printing has been priced in. When interest rates are guaranteed to remain at zero forever, you can’t have expected annual returns of 5% or more in other assets because it would be foolish not to bid up the assets to the point where the expected returns go to 1-2%. Investing is just a game of front-running. Once valuations reach that level, there is no mechanism for prices to plateau at that level because everyone knows the trend is your friend, so prices will inevitably overshoot and then crash. For that reason, every sound portfolio needs some cash to buy after the crash.

The wealthy in HK have other homes and passport already, there won’t be a rush to the door, this was what most thinking people thought would eventually happen post 1997

The hits just keep on coming.

Levi’s laying off 700 people from corporate jobs.

United now thinking of furloughing 36000 jobs.

Don’t worry, our waiters, etc will pick up the slack and get into a bidding war.

CARES guaranteed airline employee jobs until October, so expect those layoffs to begin in earnest shortly thereafter.

I’m currently unemployed ( 5 months to care for the Boss Lady and 5 months due to Covid) I cannot beg, borrow, or steal an interview much less a job. I’m a contract engineer. My industry (Aerospace) has been absolutely decimated. While I am desirous of a job, can someone explain how all this money printing will help me the working man?

I have cashed in my last 401k with penalty, used up my savings, consumed my tax refund, and am currently on unemployment only.

While my house is paid for as is my vehicle, I still need a bit to survive.

NOT being sarcastic at all, but I fail to see how one $1200 check since this madness has started is going to change my life. If the bright folks on here can point me to sources of all this money it would be most appreciated.

So far I see corporate America benefitting but nothing making it to main street. Please enlighten me. All I see is skyrocketing foreclosures, repossessions, and bankruptcies. WHAT am I missing?

You are not missing anything, you just do not have a vested interest in ever increasing RE value. In the real world, there is a direct relationship between unemployment and housing bubbles. Now in the real estate sales world, it is always time to buy, and you had better hurry……..

We need more of you to vote for UBI. Most jobs are useless anyway. We’d be wealthier as a society if we voted ourselves a monthly income for doing nothing.

GRANT

Keep reading Wolf Street – it will grow on you and you will become educated. As a real estate person, I will be direct with you since you did ask the question. Sell your McMansion and downsize. There’s no cap gains tax if you make less than $250K profit on the sale. Buy something else with cash and invest what you have left based upon wisdom gleaned from this site. I do not have exact stats or proof, but I suspect the majority of the people reading and posting on this forum quit their day jobs well before traditional retirement age.

Grant, I don’t think you are missing anything here. IMHO, the Oligarchs are using the COVID-19 to crush what’s left of the Middle Classes economically and turn us into something like a Brazil.

They have to be careful though in their extreme arrogance & hubris not to end up with a late 18th century France event instead of the Brazilian economic model they so desperately seek.

Grant,

Sell the house before you lose it to RE tax default. You are going to need the money. Don’t buy anything until you have a good job or maybe never again. Mobility will help you in the job market.

BTW, I lost everything because I held on to the end. Looking back, I should have sold my retirement home two years after we bought it, when it doubled in price. That was the warning I didn’t understand, it seemed normal, but it wasn’t.

The worst of the Latin American models is clearly the path the US is on.

This has been apparent for quite some time.

But take comfort, everything almost everywhere is going down too.

I know that gig workers like Uber drivers have been able to receive unemployment checks. Perhaps contract engineers would qualify as well. I’m not sure whether you need a recent track record of revenues to qualify.

Grant,

Sorry to hear about your unemployment. I just want to add this, and this is just anecdotal: I have never in my life known so many professionals (engineers, program managers, lawyers, marketing pros, etc.) who are now NOT working — they were either laid off or furloughed or their contract work has dried up.

Well I’m living near Upstate NY, North of the border, and I heard a rumor that the NFL been notified: Change the name Buffalo Bills to Buffalo Helocs, with a commitment to refinance the jerseys every 12 months as long as incremental lowering of interest rates, even if negative, and gold stays below 10,000 oz. Going to the game will be ok as long as you remain 3 seats apart and wear a mask. Full bragging rites for this ritual on par with Mexico two week vacation or Caribbean cruise, while collecting third rescue pooch.

Less than a 7% drop is nothing compared to the rising interest rate storm about to brew. The “No Inflation” lie is about to meet a brick wall called reality. The Govt won’t be able to contain the lie and the price to be paid for the bazillions in monopoly money will come home to roost. Real estate, equities and bonds all get killed which is what the Fed wants to avoid almost as much as a Fed Govt that wont be able to repay just the interest on the massive debt to keep things rich for the rich.

Elder Millenial here. Husband and I have two toddlers and live in the Bay Area. We’ve been saving every penny since we graduated with PhDs in 2015 and work as scientists in biotech. We are probably in the top 20% income bracket but started saving later than most of our peers who didn’t go to grad school. Now we’re still renting a place that’s too small for the four of us, but we do it to continue saving every penny to have a large down payment and be able to afford a house. Regardless, even with relatively safe jobs, even though we are hoarding cash and contribute to extremely risk-adverse investments, we still would not be able to buy a house that would allow us to have less than a 1.5 hour commute each way with kids in the backseat. We cannot leave because our aging parents are here and we love it here. And with schools and daycares being closed to us still, our aging parents are our only source of childcare. We’re trying to figure out the right time to enter the housing market, not for profit, but to live in long term, and feel strangled by the math of a mortgage and property taxes alone that would be higher than the rent we are paying now. We see these types of articles about decreasing sales and then in the comments alone, read and hear all the anectdotes that seem to contradict the data and feel so confused. We tried to buy a house once in 2018, but were competing with 30 offers at one point, and houses that were being sold for 500k over asking price, so we got out because we didn’t have the stomach to play that game and end up with buyer’s remorse. And now we’re afraid we’re going to end up in the same place anyway.

JENNIE

There are so many things that “can” happen in your work life and also in the RE market. A friend of mine bought a house in 2015 in Scottsdale AZ thinking it was the last home before the Nursing home (i.e. a 20 year home). 2 years later, Nazi HOA made it unbearable – she had put in $200K improvements on a $350K house. Sold it for a small loss. Could not see that one coming.

You have children and aging parents and you love it where you live. You have numerous reasons to believe you will be there at least 5-10 years. Within that time period, if you overpay for something now, it will come back to at least where you bought it (worst case), and with asset inflation on the horizon, there’s a decent chance what you buy will be worth 2X what it is now in 10 years.

In short, if you are one of the unlucky ones who cannot escape the Peoples Republic of CA (sounds like that is true), then check in to Hotel California.

Jennie,

Maybe you can house swap with your parents, they let you live in the house, and you use your down payment to buy them a nice townhouse nearby.

By May 2021? I’m watching a few 600,000 houses in a Portland drop 20 – 40 k a month as I type this. Multiple reductions – April, May, June.

By May 2021 they will be down 20 to 40 percent.

Yup, the Portland area is a great place to be from. Emphasis on ‘from’. I know, I’m one of them. I remember when it was farming country and conservative!!

I’m glad Portland is not like that any more. Much more interesting and unique now than just another sleepy farm town, which the country is absolutely full of. There is only one Portland OR though.

Many thanks to everyone for the information and apologies if my frustration came through. My home is a 1200 sq ft on 1 1/2 acres in rural Arkansas. Paid for car is 2012 Mazda 3. Not extravagant by any means.

I have spent many hours gleaning wisdom from Mr. Richter and all who post replies. VERY informative.

I can’t go mobile. I’m 57 and the Boss Lady is 62. She just finished recovering from her fourth cancer and has COPD. We are close to the VA

which is the only health care she has. Dropped my insurance when it went to $850/month.

I’m not trying to sing a sad song. We have been blessed! I give this background to illustrate that I am lower middle class. Like a few million Americans who are getting fewer. I want a job to earn my living, not handouts. That said, it seems that the trillions that have been printed to date are doing little to nothing to help me or my fellow Americans at my income level.

Thanks to Mr. Milken and his ilk, I have struggled to stay employed since graduating college in ’84. Not able to save much through the years and now that’s gone.

Again, don’t mean this to sound like sour grapes. We are very blessed!

To tie all this to the original topic, if an individual of the working class has no job then they are not able to afford taxes on a home much less the home itself. No way to buy a 50-70k pickup to go to the job they don’t have.

DOW 100k doesn’t matter to one sleeping under a bridge eating scraps.

These trillions being digitized are doing nothing for the shrinking middle class where basic survival is becoming the norm. Once this class is destroyed, there will be no one left to purchase from corporate America, much less “invest” in it.

Again, thanks to everyone for your thoughts. While my majors were physics and mathematics, I just can’t get the numbers to work.