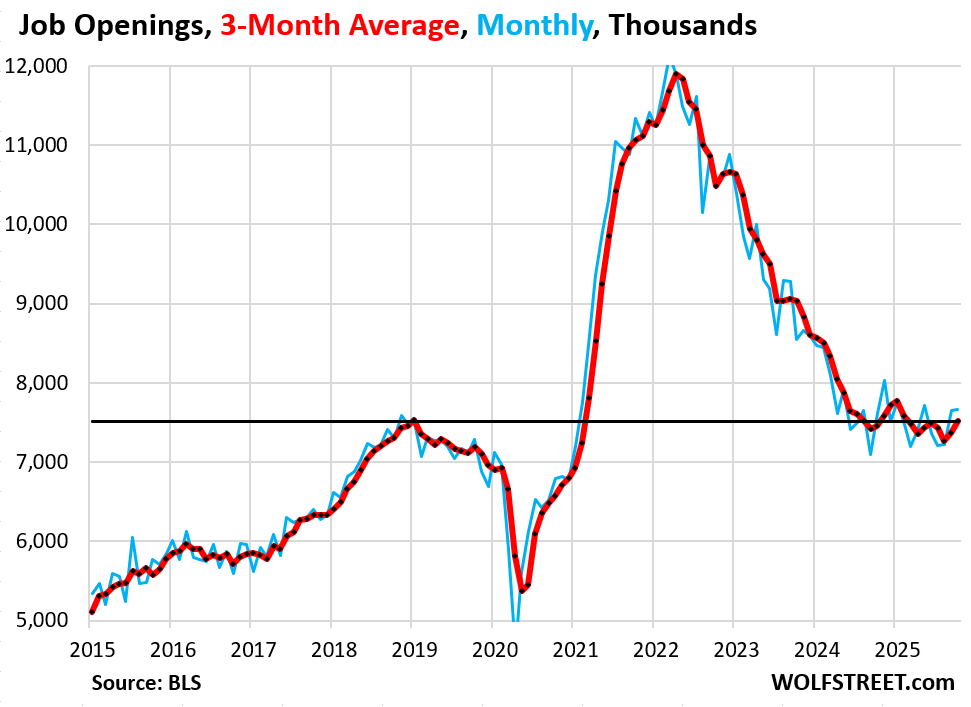

7.67 million job openings, highest since May, 2nd highest all year, and up from a year ago.

By Wolf Richter for WOLF STREET.

Due to the government shutdown, there is no good figure for job openings in September, and the September release was canceled, but “partial data that businesses self-reported electronically” were included in today’s October release, according to the Bureau of Labor Statistics. The October data were collected as normal in November. So month-to-month comparisons for October lack a solid base (September data is only partial). August was the last complete data set (7.23 million job openings), and the August-to-October comparisons are valid, and that’s how we’ll get around the September “partial data” issue.

Job openings jumped by 443,000 in October from August, seasonally adjusted, to 7.67 million. That October total of 7.67 million job openings was the highest since May, the second-highest all year, and up year-over-year by 55,000 openings.

The three-month average (red in the chart) jumped by 154,000 openings (average of the increases in August, September, and October), to 7.52 million openings in October, the highest three-month average since February, and up by 63,000 from a year ago. For over a year, the three-month average has hovered near the pre-pandemic high of January 2019, but has come down a lot from the era of the labor shortages.

All data here are from a survey of 21,000 companies; some of the data were electronically self-reported by companies, and some of the data were obtained via survey methods. This data here are not based on online job postings.

Job openings are largely the result of quits, layoffs & discharges, and other separations (retirements, deaths while employed, etc.), all of which are tracked by today’s Job Openings and Labor Market Turnover Survey (JOLTS). Only a small portion of these 7.67 million openings represent newly created jobs.

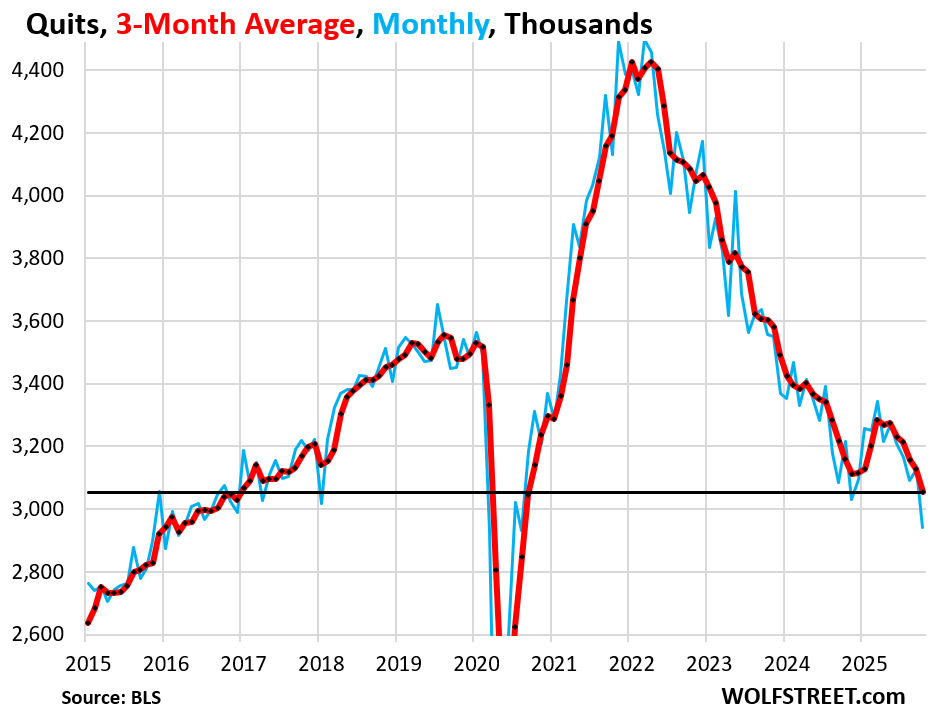

Quits fell by 150,000 in October from August to 2.94 million workers who quit their jobs voluntarily, such as to take a better job somewhere else (blue in the chart).

The three-month average fell by 75,000 to 3.05 million quits (red in the chart).

Fewer quits means fewer job openings left behind, and less hiring needed to fill those newly left-behind job openings.

The survey tracks turnover in the labor market: How many workers quit voluntarily to work somewhere else, how many were discharged for whatever reason, how many retired or died while employed, etc., and how many were hired to fill these left-behind job openings.

Turnover in the labor market had exploded in 2021 and 2022 during the labor shortages. That episode of massive churn was expensive and inefficient for employers, but ended up reshuffling where people worked, with better matches between workers’ skillsets and aspirations and companies’ needs.

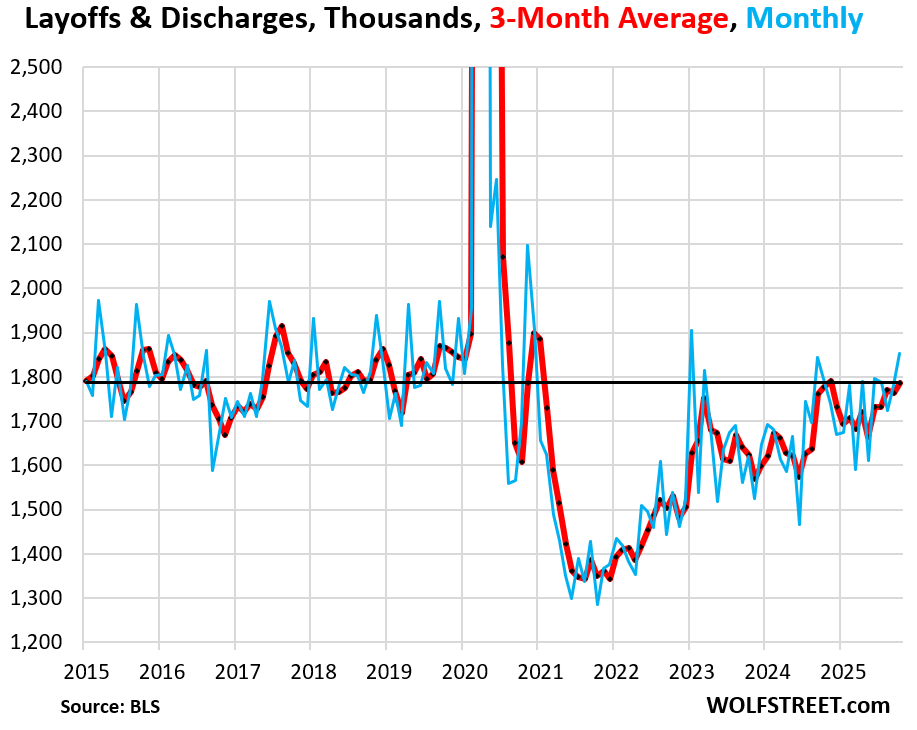

Layoffs & discharges rose by 129,000 in October from August, to 1.85 million, in the middle of the pre-pandemic range. The three-month average rose to 1.79 million, the highest since November 2024, but still at the lower portion of the pre-pandemic range.

These relatively low layoffs & discharges – though up from the era of the labor shortages – has been confirmed by other data, including very low unemployment insurance claims.

How low are the layoffs & discharges in relationship to nonfarm payrolls, which have grown over the years? The three-month average of layoffs & discharges amounted to just 1.1% of nonfarm payrolls, which would have been a record low before the pandemic in the JOLTS data, which goes back to 2001.

These relatively low layoffs and discharges translate into fewer job openings, and less hiring to fill those job openings.

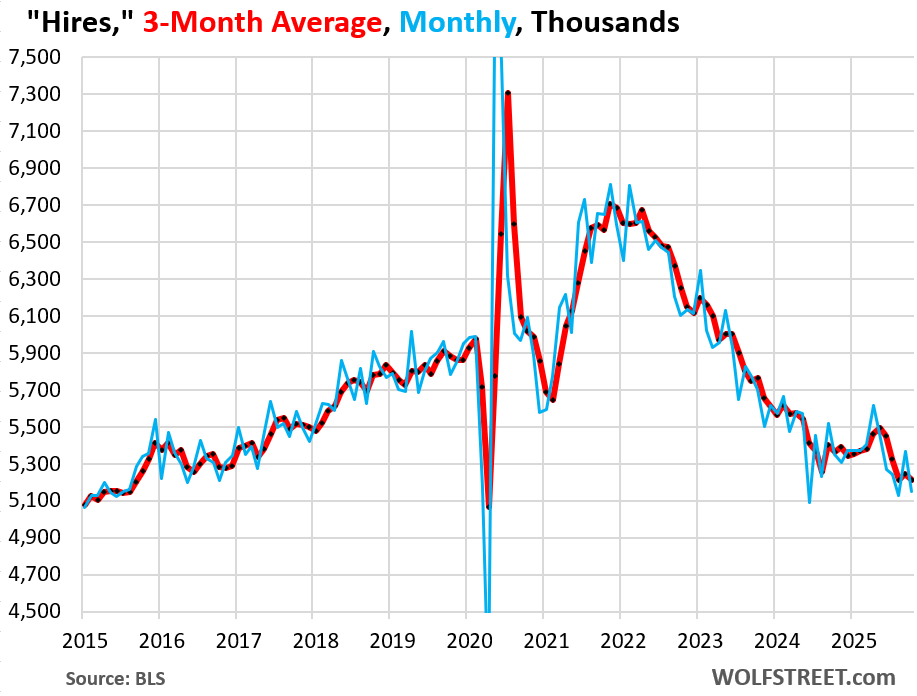

Hires rose by 23,000 in October from August, to 5.149 million.

The three-month average declined by 113,000, to 5.21 million hires, roughly where it had been in August, after the spurt of hiring earlier this year.

Most of these hires replaced workers who’d quit their jobs, or who were discharged or laid off for whatever reasons, and who’d retired, etc. Only a small portion were hired to fill newly created jobs. It’s part of the labor turnover.

But the low number of quits and the relatively low number of layoffs and discharges mean that companies need to hire fewer people to fill the job openings left behind, and job seekers are having a harder time finding a slot.

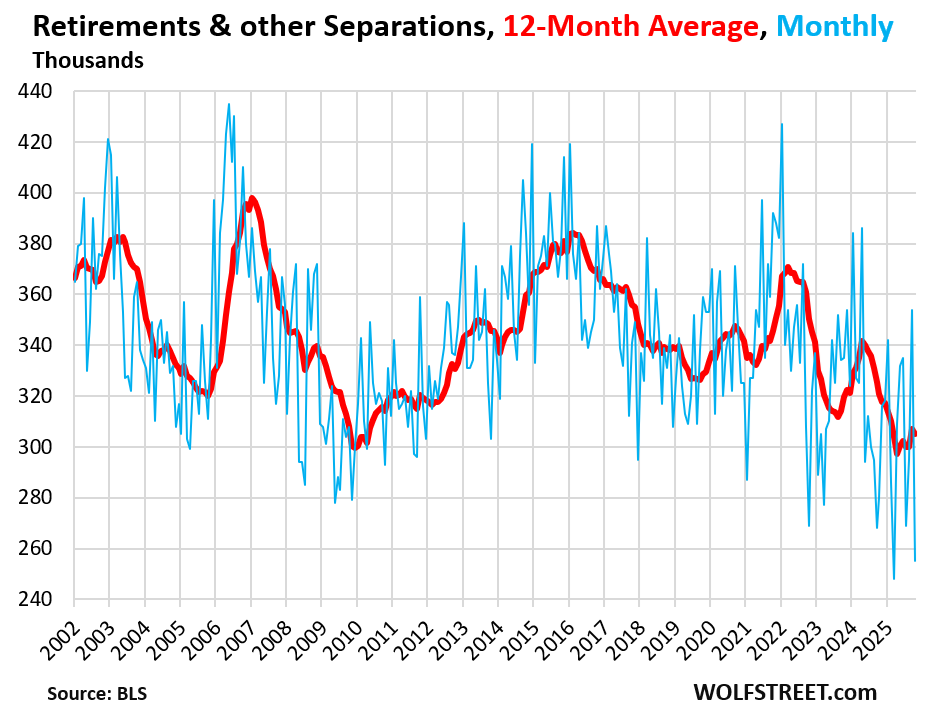

The retirement waves are over. Other separations (retirements, deaths while employed, etc.) totaled 255,000 in October, at the very low end of the 25-year range.

The 12-month average, which irons out the huge month-to-month squiggles and shows the trends, inched down to 305,000 for October.

These monthly totals are small compared to the 7.5 million job openings. There had been a wave of retirements in 2021 and another in 2023 through early 2024, but they weren’t extraordinarily big, as the chart shows:

The main thing to take away from this Job Openings and Labor Market Turnover Survey is that the labor market is in pretty good shape, with a sharp increase of job openings in October, while the red-hot turnover in the labor market in 2021 and 2022 has cooled, with companies hanging on to their workers, and workers hanging on to their jobs – creating a situation that requires less hiring.

But low turnover makes it harder for job seekers to find a job. Each time someone quits a job, a job opening is created that needs to be filled, and the company needs to either promote someone into that job, which creates a lower-level job opening, or hire someone from the outside for that job. When there are lots of quits, it creates more opportunities for job seekers to slide into one of those left-behind job openings. Now there is less movement in the labor market, and therefore less hiring, and people looking for a job are having a harder time finding a slot. And other data has confirmed this trend.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Strong labor market and sticky to increasing inflation… the FED should certainly cut rates tomorrow!!

I agree. The Fed should show that they are on the President’s side and cut by 50-100 bps. Simply dripping with sarcasm, lets make it a hundred for fun. Then the Japanese can tighten by 50 next week. The resulting mayhem should cause a real bloodbath with long end selling due to inflation concerns and carry trade unwinds driving 2s 30s to 500 basis points or more as we demonstrate to the whole world that inflation just isn’t a concern at all for AI America. It really has gotten to the point where its just ridiculous. Then maybe we can have another whack at QE which should then result in a dollar sell off of epic proportions

“Then maybe we can have another whack at QE which should then result in a dollar sell off of epic proportions”

I’d argue that there is a sell off in all fiat currencies that has been occurring for 50+ years. Regardless, there’s plenty of work to do in the American eCONomy, although I did witness a neighbor pay an electrician in silver the other day which I found interesting. Both parties were very happy about the transaction.

Interesting times.

Interesting way of putting it. A global rise in asset prices is really just a fiat currency sell-off.

8 to 4 no cut. If really high employment cost index at 830 than maybe 9 to 3. Jay Powell speech will be hawkish whatever happens. Bitcoin sucker punch rally didn’t hold above 94k. I think it’s voting for no cut.

Let’s play; cut or no cut and vote count.

8 to 4 no cut!

No chance.

Once a cut is “priced in,” they’ll never deviate. They don’t want to “surprise markets.”

Thanks for your no cut vote. Fed watch has 10.9% no cut down from 12% yesterday. Employe cost index is estimated to be .9%. If it comes in hot as I expect let’s say 1.1% or really hot at 1.2% will see what happens to fed watch probability for no cut. It’s a brazen call. It’s the trend of data that is important to the Fed that can’t be ignored.. I get the holidays are coming and no one wants to be Scrooge, but we will see shortly what the ECI is, it’s a extremely valuable report today. No matter what the Fed does the 10y UST yield is marching higher. They have control over the short but are powerless over the long bond, with interest rate decisions. Thanks for voting!

It came in .8% for the third quarter and $tnx gave up some yield, not sure why the data came in lower than expected, will see if if Jay mentions the inconsistency of labor cost growth or mix messages of data today in speech. The long bond will pay attention to what the real whole data is forecasting. Equities still will rollover with the whatever happens, the vote count is super important, still going for 8 to 4 but I could be delusional, you got to be a little crazy to see the truth.

BTCUSD critical level is 50DMA $89,305 and it stopped declining today.

Agree with TSonder305, 12-0 cut 25 bps. Maybe 11-1 bc Moron wanted 100 bps cut or whatever. Whatever is the wrong call to make, this fed is here to make it.

9 to 3 cut 25. Moron wanted 50 cut. Unemployment claims are estimated for 223k tomorrow the charts tell me under 211k maybe 204k. Williams had way with the size of adjustments to t bill on balance sheet and start date. Let’s hear what Jay has to say.

That was a good prediction.

Count me in with all of the “Deplorables” that support the “moron” (as you call him), who is one of the few national figures in the last 20 years who support decency in America.

I bet you hate Dobbs opinion too.

So, we will have more inflation, better employment stats and less abortion. A nation can survive higher inflation, especially in the face of greater automation which is deflationary (like in the 1980’s), and less abortion like before 1973 when America grew like crazy and dominated the world.

Re; Prediction

It is actually quite easy if you have the money….here’s an excerpt from one that succeded, and set the course of history.

“In all fairness, it must be recognized that businessmen have not been trained or equipped to conduct guerrilla warfare with those who propagandize against the system, seeking insidiously and constantly to sabotage it. The traditional role of business executives has been to manage, to produce, to sell, to create jobs, to make profits, to improve the standard of living, to be community leaders, to serve on charitable and educational boards, and generally to be good citizens. They have performed these tasks very well indeed.”

From the 1971 POWELL LETTER, released AFTER Reagan was elected and Powell was nominated to the Supreme Court.

Suggest you do some research MS.

Stock Market Today: Dow edges lower, S&P 500 and Nasdaq flat as Fed decision looms tomorrow; traders digest job openings data

I don’t think “job openings” is a good indicator of employment health. Wolf’s caveat that only a small percentage of these openings represents new jobs is on the money as usual. Every company wants to project an image of growth and vitality, and job openings is an easy way to do that but the question, as always, is how many people are actually getting hired.

“Every company wants to project an image of growth and vitality, and job openings is an easy way to do that”

BS. These job openings are NOT BASED ON ONLINE JOB POSTINGS.

They’re based on HR data (including quits, hiring, firing, retiring, etc.) from 21,000 companies. Read the paragraph under the first chart.

Every single time I post a JOLTS article, I get the same “but yada-yada-yada online job ads.” Month after month, year after year. You have no idea how old this gets.

Wolf!! Funny. To make people not to comment unnecessarily, before the article please write in block letters what the survey is about. Hope they read that before commenting

Right, Wolf, but don’t pretend the data you’re reporting is reliable either. Surveys are surveys. They might be reliable for broader trends and to serve a narrative, but they’re filled with sampling errors. Because your company would be quick to report a negative stat.

1. Data is data. If you want something you can believe in, and be 100% certain about, go to church.

2. “Because your company would be quick to report a negative stat” is more BS piled on top of BS.

Thanks for the clarification, frequently I see comments from people, like “Ray” that lead me to suspect they only read the headline.

I agree Wolf, just too many people aren’t willing to read enough to be informed, instead they just shoot from the hip, with a conclusion that fits their pre-disposition.

Just had someone do that to me in my law practice, turns out i heard from the grapevine that they were looking for another attorney because they thought I was charging them for something they had already paid for, and it turns out they were completely wrong. I had to cut and paste the relevant passage in the agreement that clearly states what they paid for already, and they haven’t yet admitted their error, so I sent them 30 days withdrawal notice.

It’s a nation or morons.

“It’s a nation or morons.”

🤣❤️🍾🎇

“Fed Faces Scenario of Solid Job Market and Accelerating Inflation

Add in new price inflation on groceries. Saw 10% to 20% increase today on many items, especially imported ones, and meats. I had to return some items at the checking counter. I’m going on a buyer’s strike.

My Cable Company, Comcast, just announced a big rate increase on the way next month.

Long term rates are going up as we speak. Mtg rates will follow.

The Fed should NOT cut rates. There is more justification to RAISE RATES.

They do not shop for groceries; they have chefs. With the stock market at an all-time high, they may just do a double-cut of 50 points. They will do exactly the wrong thing at exactly the wrong time, then write self-congratulatory books about it.

I’ve commented on this before, but the entire media is written by people with a lot of stocks for people with a lot of stocks. They’re all thrilled with high stock prices, so they can’t understand why the national mood on the economy is so sour.

They mention things like “60% of Americans have investments in stocks” which is true, but it conceals the fact that most of those don’t have enough for it to make them feel “rich,” which is what the wealth effect is about.

“They do not shop for groceries”

Imagine Jay Powell in a grocery store

Not a grocery store, but there was that one photo of Jay eating alone in a crappy sports bar after his Jackson Hole speech this summer.

Powell is more likely to be found in a weed store, with Grateful Dead playing in his earbuds.

Groceries, they have a term ‘grocery.’ It’s an old term, but it means basically what you’re buying foods. It’s pretty accurate term, but it’s an old fashioned sound

You still have Comcast? That’s 28 lattes per month.

The best cure for inflation is to consume less. Companies are gouging the public, just look at their profits.

Yep, and ski lift ticket prices are one of the worst examples.

I as I work outside of Boston as always here see plenty of work construction wise at moment,huge hospital merger in Boston will in area definitely be resulting in layoffs according to folks i know there but will see how outside of city proper the med hiring is.

I have a friend who had a employee give notice a few weeks back and said he won’t bother trying to fill after holidays,feel many other folks considering hiring might be the same.

My old local economy barometer was CL gigs ect.,there is a huge slowdown on that site for short term hiring been going on for months in this region,perhaps less just using CL but was the place for folks seeking temp workers/temp helpers looking for a long time around here.

Just my opinion: Craigslist is dead meat. Whether you’re selling something, trying to buy something, looking or offering work, employment or a gig the traffic is on FaceBook. Cl users have to respond by email or phone call, FB users just click to respond. Fraud and spam rates on Cl are sky high. Facebook/Meta has a dedicated job section within its Marketplace, featuring local, entry-level jobs with filters for distance and type, appears in Groups and Pages too; Meta recently reintroduced these local job listings to connect job seekers with nearby opportunities, especially in trades and services. (My apology if this is too far off topic.)

James,

If your barometer is CL, you’re screwed. The reason I post data is so that I don’t have to listen to this nonsense.

More data supporting no rate cut. Let’s hope the FED feels the same.

A cut at this point would be reckless. Unfortunately, Powell has a bad track record in this regard. He’s too much of a Wall Street people pleaser to be trusted.

just a reminder

5% unemployment used to be considered full employment

then they move the goal posts

but 4.3 or 4.4% unemployment is not an issue and not a problem and not a reason to cut

But the coming midterms might be

IMHO – The vote at the Fed that was revealed yesterday indicates that the Fed is now politically neutral.

I’m confused! You say August job openings were 7.73 million and October job openings were 7.67 million. That sounds like a DROP of 60 million to me, not an increase of 443,000. Is there a confusion of seasonally adjusted and non-seasonally adjusted figures here?

That was a typo. August is 7.23 million (should have been a 2 instead of a 7). I corrected that a while ago. Maybe you got a cached version of the page.

Thanks, Wolf, for pointing out that cached version problem. I’ll try to avoid that in the future by updating info.

But another question: Can we be sure that the government has not double counted some current job openings by adding in partial September data with the full October data?

No, of all the problems that the data might have, double-counting is not one of them. The survey (a mix of electronically self-reported data by companies and surveys sent to companies) establishes the total number of job openings in the current month, so October in today’s data (7.67 million). That is the figure, and my charts show that figure (end point of blue line).

Then to get month-to-month and year-over-year changes, or three-month average, or whatever, I (me, moi) subtract a past month, such as August (7.23 million) from the current month, and out comes the change. The month-to-month change is also in the press release, and it’s obviously the same as my month-to-month calculation because the whole data set is based on total job openings each month, not changes from month to month.

So the September total (7.66) was an estimate by the BLS based on a “partial” data set. So it’s a data point in my chart. But it’s not useable for an “October total minus September total” month-to-month figure. But “October total minus August total” is based on two complete data sets. So there cannot be any double-counting.

How significantly does reduced immigration, combined with deportations have on overall jobs picture? In other words, can those two things keep the job market relatively stable even if most are likely not high paying jobs? Or is it just too small a drop in the bucket?

That’s a question everyone is struggling with. There is definitely a supply aspect in some of the labor data.

Something to consider is that ‘not high paying jobs’ are about to pay a LOT more as migrant employers have to offer compensation packages to draw citizen labor. Then sectors that already have citizen labor have to raise compensation to keep them. It is a labor shortage that will kick off a whole new inflationary cycle. 8% rates by 2027 are fully possible.

Optimist. I’d love to see 8%+ CDs again. Unfortunately the system is debt-saturated as we have not allowed bad debt to clear, bad actors to suffer (instead we actually rewarded them), and prices to actually deflate (seething we use to allow in a normal business cycle).

Early signs are that this is leading towards a wash or even overall contraction (i.e. contraction in job openings because of a contraction in jobs because of a contraction of the economy because fewer immigrants present). There was a NYTimes economist op-ed about it recently.

Oops, someone forgot the USA was built on immigration.

FWIW and IMHO – the deportations is the major cause of housing prices decreasing in the poor parts of DFW.

Did anyone say anything about AI in this article?

Solid job market + accelerating inflation, that’s when the Fed is supposed to ease up on monetary policy and cut rates, right? Right? 🤣

(I’m joking, in case not obvious.)

If the Fed does not cut rates this week, it is unlikely their reasons will have changed in January. That takes us to the Fed meeting in March. There is no telling how things will look in March.

Dont forget the gov is likely to shut down again in January..

As others have commented, the era of the “transparent” fed has given way to the “data dependent” fed: the data they use is the CME Fed watch tool.

The “independence” of the Fed has dwindled to indecision on whether they depend on the markets or the government to drive their decision.

Full employment and price stability both? =4.

Why? That’s how many branches of the government there are… with the Fed, “independently” opting to be one of them (closely related to the Treasury Department).

Maybe DOGE and the Supreme Court will combine the two positions, ya’know: Efficiency.

“We will be data dependent” J Powell

“We will see through the data when appropriate.” J Powell

Orwellian double speak.

We need the Taylor Rule, hard rail monetary policy.

“All data here are from a survey of 21,000 companies; some of the data were electronically self-reported by companies, and some of the data were obtained via survey methods. This data here are not based on online job postings”.

It seems to me no one reads anymore. Mr. Wolf is clear when he presents data as to where it comes from.

It may also make sense to have an appendix of data sources for the article to train people to understand how an article is written.

My guess is that the Fed will cut but then claim that future cuts

are in doubt. Powell loves to split the baby, inflation be damned.

He always says that future cuts are not guaranteed, but then cuts as long as there is a slight hiccup.

Forbes had an interesting and article on what they called the invisible non-profit crisis. What was interesting is that it focused on the social and mental ramifications on the sector’s employees. I didn’t look at the original survey they cite.

I still see a lot of hiring, though. I haven’t seen the downsizing locally, but I know that many education non-profits dependent on state and federal funding are at least considering rejecting funding based on the anti-DEI and anti-immigrant requirements. Immigrant services have either an abundance of clients for living necessities or a huge drop in clients for optional services (education, job training). “We are funded–for now” is a common refrain in non-profits which seems even more uncertain this year.

Private funding may take up the slack in specific areas like public radio, environmental groups, etc. Health non-profits and public healthy agencies now have to spend time fighting misinformation, an added burden.

There are good and bad non-profits from the perspective of how much they produce for their dollars. There’s always a new idealistic group of young people for these jobs, but they don’t have the experience if there is indeed a mass exodus or downsizing.

Jolts, quits and hires LT trend is down. ACA trend is up. Tariffs + lower

ACA enrollment might reverse the downtrend from down to up.

Accelerating inflation way above the FED’s target (which is a scam in and of itself and should be zero). and a tight labor market. THE FED CUT RATES BY 25 basis points. If this isn’t still “the most reckless FED ever, I don’t know how it ever would be.”

I am pretty sure that Trump et al are expecting big deflation because of AI-driven automation, which may have already started for many employees. I already know one person who was apparently laid-off due to AI.

Musk has said that unemployment will be 100% in as little as 10 years due to AI. I find him to be a credible person.

Musk is one of the biggest liars out there. See “Funding secured.” He just gets away with it.