Reserves will shrink further when the balance sheet stays flat after QT ends.

By Wolf Richter for WOLF STREET.

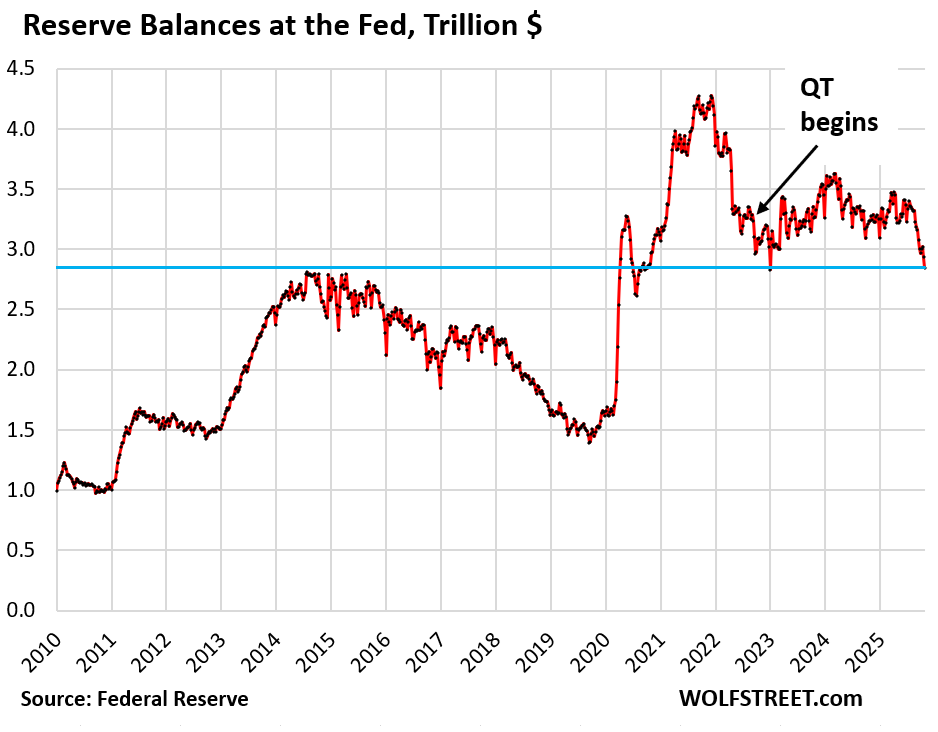

The Fed decided to end the reduction of its securities holdings as of December 1, and keep the balance sheet “steady for a time while reserve balances continue to move gradually lower as other non-reserve liabilities such as currency keep growing,” Powell explained at the press conference on Wednesday. This continued decline of reserve balances is a mild form of balance sheet tightening; which is why Powell brought it up. More in a moment.

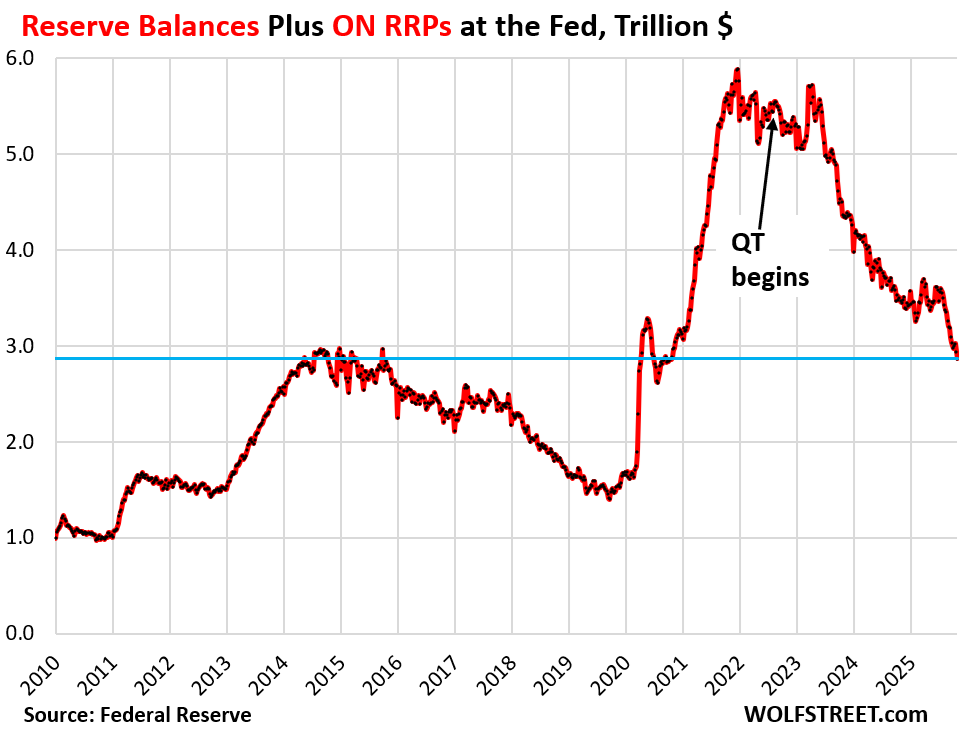

With its QT, the Fed has been targeting these reserve balances. Reserves are liquidity that banks deposit at the Fed and earn interest on (Interest on Reserves, or IOR, 3.9% since the FOMC meeting). Reserve balances had exploded during the years of massive QE.

What had also exploded during QE was the liquidity that money market funds (mostly) put on deposit at the Fed, via the Fed’s Overnight Reverse Repo facility, or ON RRPs, that the Fed currently pays 3.75% interest on.

Both reserve balances and ON RRPs are liquidity, one from banks, the other from non-banks. They’re both liabilities on the Fed’s balance sheet (money the Fed owes). QE ballooned both of them. And QT drained both of them.

As per today’s balance sheet, compared to the peak:

- Reserves dropped by $1.40 trillion to $2.85 trillion (from $4.25 trillion at the peak in December 2021).

- ON RRPs dropped by $2.35 trillion to near zero (from $2.37 trillion at the peak in September 2022).

But the peaks and drawdowns of reserves and ON RRPs didn’t occur at the same time: In 2022 there was a big shift of liquidity from reserves to ON RRPs, and then in 2023 from ON RRPs back to reserves.

So given the shifts between them, it’s useful to look at them combined as a measure of excess liquidity created by QE and drained by QT.

Reserves and ON RRPs combined peaked in December 2021 at $5.87 trillion as QE was being tapered out of existence.

In October, they dropped by $109 billion, according to the Fed’s balance sheet today. Since the peak, they’ve dropped by $3.0 trillion to $2.87 trillion, the lowest since April 2020, and where they’d first been in late 2014 toward the end of “QE infinity.” This is what the Fed wanted to accomplish with QT:

Reserves shrink further as balance sheet stays flat: Powell

Powell explained in the Q&A: “If you freeze the size of the balance sheet, the non-reserve liabilities, currency, for example, will continue to grow organically; and because the balance sheet is frozen, you have further shrinkage in reserves, and the reserves is what we are managing.”

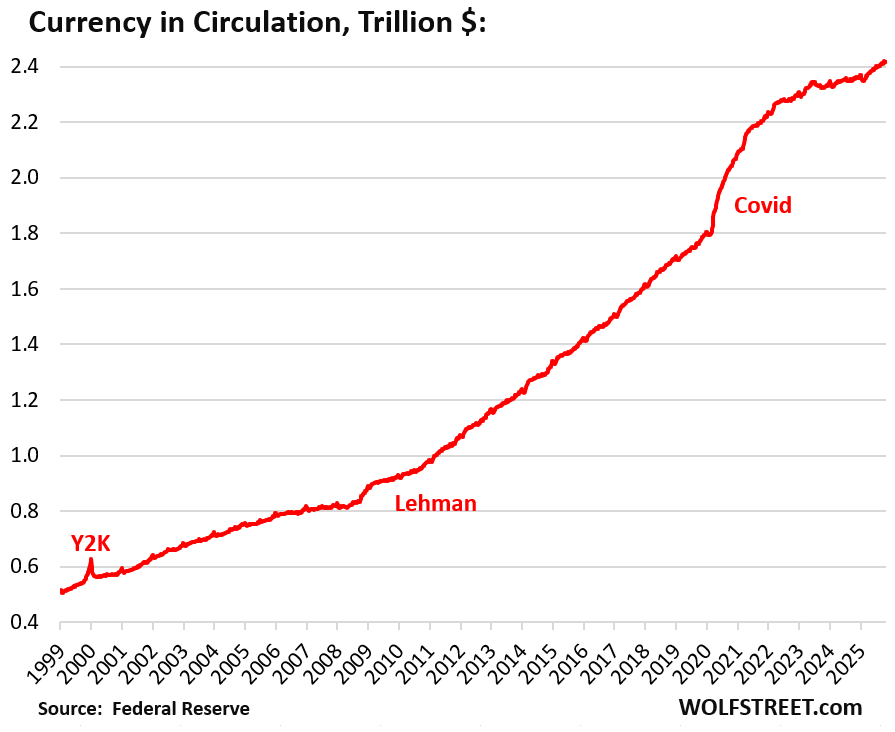

The biggest non-reserve liability is currency in circulation (paper dollars). The amount of currency in circulation is demand-based. Banks have to be able to provide paper dollars when their customers go to the ATM. The banking system has to have enough to meet this demand, and banks get these “Federal Reserve Notes,” as they’re officially called, from the Fed in exchange for collateral, such as Treasury securities. The Fed makes a profit: It exchanges non-interest-bearing paper dollars for interest-bearing securities and keeps the interest.

Currency in circulation is now at $2.42 trillion, up by 2.7% from a year ago, and up by $600 billion from January 2020. During times of uncertainty (Y2K, Lehman bankruptcy, and Covid), there are bursts of demand for currency. During normal times, currency rises gradually.

This rise of currency in circulation will reduce reserves if the balance sheet and thereby total liabilities are kept steady. This also occurred in 2015, 2016, and 2017, the years during which the balance sheet was also kept steady.

Fluctuations in the other two big liabilities – ON RRPs and the government checking account (Treasury General Account) – also impact reserve balances. The TGA can have a substantial impact on reserve balances during and after the periods of the debt ceiling. In addition, there are sharp drops in reserves at year-end. So reserve balances fluctuate widely, but the trends are still clear:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Wolf,

Do you see the balance sheet / QT as potentially being back in play if inflation picks back up (or fails to fall as forecast)? Or is the Fed afraid to go below this point, and any future inflation fighting will be through Fed rates and “twists” to this balance?

-b

Powell is the architect of this mega-balance sheet and of the “ample reserves regime.” He doesn’t want to back away from it. A new Fed chair, if so inclined, could start persuading the other FOMC members that a shift away from the “ample reserve regime” is the way to go. There has been some loose talk on that. But that will never happen under Powell (and it might not under other chairs).

I think an argument could be made we have barely reached “ample” and could resurrect QT for quite a while before reaching the edges of “scarce”. Even there the standing repo facility seems like it should keep anything from blowing up unexpectedly. I do hope a future fed chair reconsiders drawing down the balance sheet further.

Well Said!!

Agreed!

Thanks Wolf.

As usual, FED chickening out little early. They could easily go for another 6 months. QT was already slowed down a lot. In Presser, Powell said the number is low so doesn’t make sense to wait.

It’s not about amount, it is about sending a message to Markets, QT is ON.

Also why to roll ONLY MBS to T-Bills? Why NOT turn maturing Notes and Bonds into Bills for certain time period? I understand there is no demand for 2-3T Bills as of today, but even monthly roll-off amounts are gradual. If you want to change the composition, start it now. FED cant be proactive to stop QT but lazy and reactive when it comes to change composition.

Also no news on selling the MBS. Last year, there was lot of talk. Nothing recently.

“Also why to roll ONLY MBS to T-Bills? Why NOT turn maturing Notes and Bonds into Bills for certain time period?”

This will come, but as you can see, it’s one step at a time. They will announced that step in a future Fed meeting.

Total reserves: Jan 2018: 2,281. Xmas massacre Jan 2019: 1707. Pre covid Jan 2020: 1715. June 2020: 3,026, Apr 2021: 3,888, Sept 2021: 4,193. JP sucked liquidity. Thereafter JP drained reserves: Sept 2022: 3,133. In Sept 2022 DXY peaked at 115. In Oct 2022 SPX dropped to: 3,491. Tariffs: Mar 2025: 3,408, June 2025: 3,356, Sept 2025: 3,068. The Fed drained reserves. ES reached: 6,950. Prof Spencer: the Fed tightened credit. Interest is the price of credit, not the price of money. Money flow matters more than interest rates. Interest rates: bs. Total reserves : H.6 Money Stock Measures.

The balance sheet is only tangentially related to this, but after reading about Amazon, Google and Microsoft’s results, I find it very concerning that, in an era where the economy grows at 3%, these companies can have their revenues and profits increase by 20-40% every year, year after year. What it means is that they’re taking a larger and larger percentage of the economy, and that will of course lead to their having immense social and political power.

To be clear, I don’t care if they “beat” earnings, as that’s a nonsense Wall Street game. I’m talking about increases in actual revenues and profits.

Monopolies have near infinite pricing power. People love to complain about the price of gasoline going up 10c, even though real prices are basically flat for decades. Yet MSFT can do a 500% price increase on office and no one bats an eye.

Lazy IT managers know they won’t get fired for saying “we should stick with 365”, while every head in the company is charged $35/mo. That’s $35/mo that could be in every employees pay check. Add in random productivity suits (Asana, Confluence, etc), Slack, Zoom, etc and it’s meaningful impact to the income of non-Tech companies.

Yes, it’s exactly why the DOJ and FTC should be enforcing antitrust law. When you’re growing at rates far faster than the economy, it just means that your “success” is coming at someone else’s expense. As you said, that’s why Main Street feels like it’s not doing well, while Wall Street and BigTech are happy as clams.

“.. and that will of course lead to their having immense social and political power.”

During inauguration all billionaires (Zuck, Bezos, Musk, Pichai, you name it) were standing right behind the family and in front of the Secretary of Defense, Treasury Secretary, the whole first echelon of government. Welcome to oligarchy.

Looks like there is no inclination to get back to not paying interest on reserves by reducing the level of reserves to the point they are binding and purchase or sale of Treasuries controls overnight interest rates.

Paying interest on reserves at the margin reduces the incentive for banks to lend to the private sector.

I think an argument could be made to reduce the incentive for banks to lend to the private sector. The U.S. is drowning in government debt. If the government wants to inflate away its debt, then lending to the private sector is going to disproportionately help the folks and businesses taking out loans and hurt the banks, who would get squeezed.

The folks and businesses taking out loans don’t always make their payments either, especially during a downtown. That scenario would put additional pressure on banks. Personally, I’d rather live with the structural integrity of the banking system being more intact with slower growth compared to higher risk to banks for *potentially* higher reward.

And more loans after all the PPP loans and excess capital pumped from QE? Let’s not refill the punch bowl, please.

The money stock can never be properly managed by any attempt to control the cost of credit. So, our money and banking system is being grossly mismanaged.

So have tariffs been good for the U.S. retail. I am amazed how well all the retail stores sales and thus stock prices have been doing. Almost all are up since April liberation day.

Are consumers buying less from TEMU, SHEIN, Aliexpress?

Shopify, Wayfair, Macys are all up 60% or more. Dollar General, Dollar Tree, WMT, Ross and more are doing all increasing sales.

An Economic report that was floating around all the social media sites a few months ago that said 50% of consumer spending is from the top 10% but the stores I listed are middle class and lower income.

I am confused. Was that a BS enoncomic report. I don’t have the source but it was floated everywhere.

“but the stores I listed are middle class and lower income.”

Yes. You put your finger on it.

A big part of consumer spending is ALWAYS by the people with money to spend because that’s where the money is. That is always the case. They buy yachts and Lambos and do $2-million home renovations, and stuff like that, and it adds up in a hurry, and it always does, nothing new.

But the people who spend their salaries… well, there is a record number of workers, and they make record and growing amounts of money because of pay raises, so more workers, and each on average makes more money, which translates into a lot more money to spend, and they’re spending it. This is everywhere. Consumers are doing well, not just the rich. But it’s only the clickbait BS about most Americans being poor and tapped out that gets clicked on and spread.

Be that as it may, but from talking to people at the company I work with, the bottom 60% or so (especially those who don’t own homes but want to) is not happy, even with how well they’re supposedly doing.

“happy” may have more to do with their spouse, an upcoming divorce, kids getting in trouble, their jobs, etc. Lots of people are married to someone they’d rather not be married to, they’re in jobs they don’t like, etc. Happy has nothing to do with the economy. We see that time and again. All these unhappy griping consumers, and yet they go on with their lives, make money, and spend money. BTW, 65% of households own their own homes, so your numbers are already nonsense. And part of the remaining 35% who are renters are “renters of choice” who could but don’t want to own a home; they rather pay $3,000 or $5,000 or $10,000 in rent and retain their flexibility. This kind of fabricated clickbait nonsense you’re immersing yourself in is why people like you never understand the US economy and will always be surprised by its strength.

I think it could be somewhat of an illusion economy supported by unsustainable two trillion a year in deficit spending and enormous debt piling higher. Unethical to be robbing future generations.

Wolf, do the changes your article describes represent a lessoning of liquidity generally ?

One day you should consider writing a book entitled “The Federal Reserve for Dummy’s” – id buy several copies to give as Christmas presents to my kids.

There are a bunch of people here in the comments that would cross out that title and write in red over it: “The Dummies of the Federal Reserve.”

In terms of your question, here is another installment, dealing directly and rates in liquidity in the repo market, hot off the press. It may answer some aspects of your question:

https://wolfstreet.com/2025/10/31/banks-borrow-record-50-billion-at-feds-new-srf-amid-hot-repo-rates-but-on-rrps-spike-to-52-billion-in-opposite-direction/

Do you think that the government shutdown had anything to do with the Reserves falling? Apparently, government spending can increase Reserves at the Fed ? So do you think the opposite play out ?

I see the small downward drop in total federal reserve notes after Y2K.

Is there any situation that might cause that reduction in Federal Reserve Notes at a longer duration and scale?

It’s hard for me to believe that there is more and more cash in circulation, with more and more of the US going “cashless”.

“Is there any situation that might cause that reduction in Federal Reserve Notes…”

If demand drops, especially from overseas. About two-thirds of the $100-bills are held overseas. So if foreign demand for US bills declines, overall demand would likely decline, and so there would be fewer Federal Reserve Notes in circulation.

In the US, people hold some as emergency cash. Then there are the illicit industries that run on cash, from paying workers under the table to dealing in drugs. In addition there is the everyday commerce in cash, as far as it still exists. But much of the action is now overseas.

In thinking about this a bit more, is it useful to the US to have cash circulate for such purposes?

I’d agree that “emergency cash” is of an important purpose to Americans, but illicit industries, paying workers under the table, and dealing drugs are probably not good for US society.

I’m not sure if allowing a large volume of paper cash to so freely circulate outside of the US is good for the US society, as my first thought is that it exacerbates the trade deficit and the employment consequences of that.

Would a sunset on US $100 and $50 Federal Reserve Notes, similar to the ones on $1,000 and $10,000 Notes, be a worthwhile policy to limit the volume of US cash circulating in such industries? $20 or smaller notes might well be adequate for Americans’ emergency cash needs.

I know there was a campaign of sorts to end the $50 and $100 bills some years back.

Think of it this way: The Fed borrows $2.4 trillion via these interest-free Federal Reserve Notes and invests the proceeds in interest-bearing Treasury securities. This is a very profitable deal for the Fed, and for the US taxpayer since the Fed has to remit all its profits to the US Treasury. This is called “seigniorage.” The part that is held overseas is particularly good because it has no inflation implications at all for the US. The more the better.

The discussion about the legitimacy of the Federal Reserve is a political question that is not solvable mathematically. The rigid fashion of culture is random

The Fed’s balance sheet is an abomination, especially the MBS portion. The primary dealer banks are essentially mafia families at this point in the evolution of the American economy.

If The Fed were truly independent and interested in returning to a free and fair monetary system they would continue QT and hold congress’ feet to the fire.

Hedge accordingly.

Yes abomination is a good description

“Mortgage-Backed Securities (MBS): -$16.8 billion in September, -$654 billion (-24%) from the peak, to $2.08 trillion, where they’d first been in February 2021.”

Overnight reverse repo shouldn’t exist. The money markets should only be able to use treasury bills and if that causes too much inflation due to the short term treasury rates getting low from all the demand, then the fed should do more QT. But I guess their reason is, we need the liquidity to support out policy, but I disagree with that, the economy can do just fine with less money. Prices and wages can naturally decrease and I’m fine with my own wage decreasing.