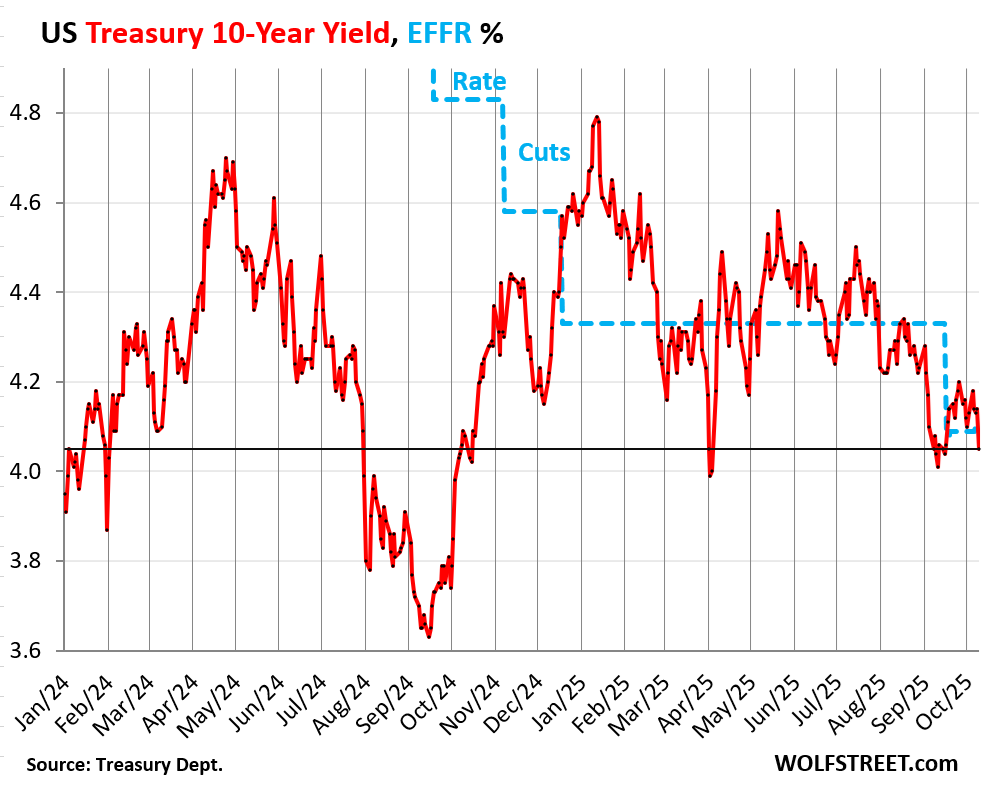

Despite the big drop on Friday, the 10-year Treasury yield is higher than shortly before the September rate cut.

By Wolf Richter for WOLF STREET.

The 10-Year Treasury yield fell by 11 basis points on Friday, much of it after Trump threatened to impose “a massive increase” of tariffs on Chinese imports in retaliation for China’s new export controls of rare earths, which caused stocks to tank and bond prices to jump, and as bond prices jumped, bond yields dropped. A few hours later, Trump clarified helpfully that the US would impose 100% tariffs on China, on top of the existing tariffs, starting November 1, which pushed down stocks and long-term yields further.

The 10-year Treasury yield ended the day at 4.04%, the lowest since September 16. Just before the rate cut, on September 11, it had dropped briefly below 4.0% and closed that day at 4.01%. After Friday’s 11-basis-point drop, it is once again below the Effective Federal Funds Rate (EFFR), which the Fed targets with its monetary policy rates.

Following the Fed’s 25-basis point rate cut on September 17, the EFFR had dropped by 25 basis points, to 4.08%. But since then, it has inched up by 2 basis points to 4.10% (blue in the chart).

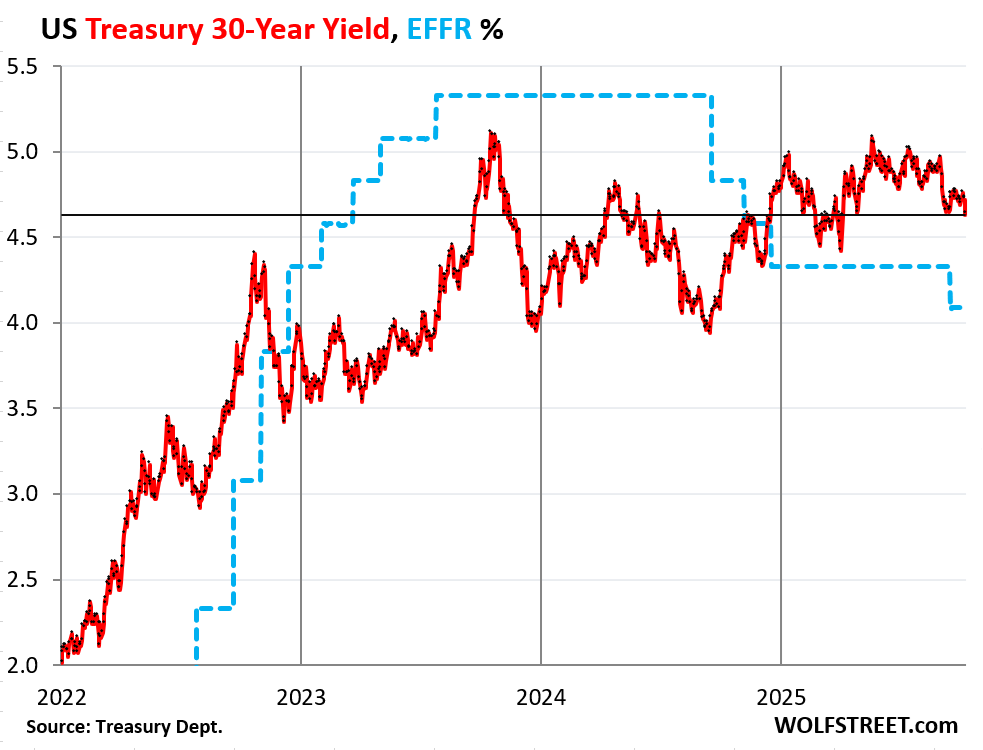

The 30-year Treasury yield fell 10 basis points on Friday to 4.62%, just a hair below where it had been a month ago, and back to where it had been in April.

Long-term bond yields react to fears about inflation in the future, which are heightened by any perception of a lax Fed. They also react to the expected supply of long-term Treasury debt coming on the market that investors have to absorb, and that supply is driven by government deficits, and they’re huge. But the Treasury Department has now begun to shift funding of the new deficits to short-term Treasury bills to take some pressure off long-term yields.

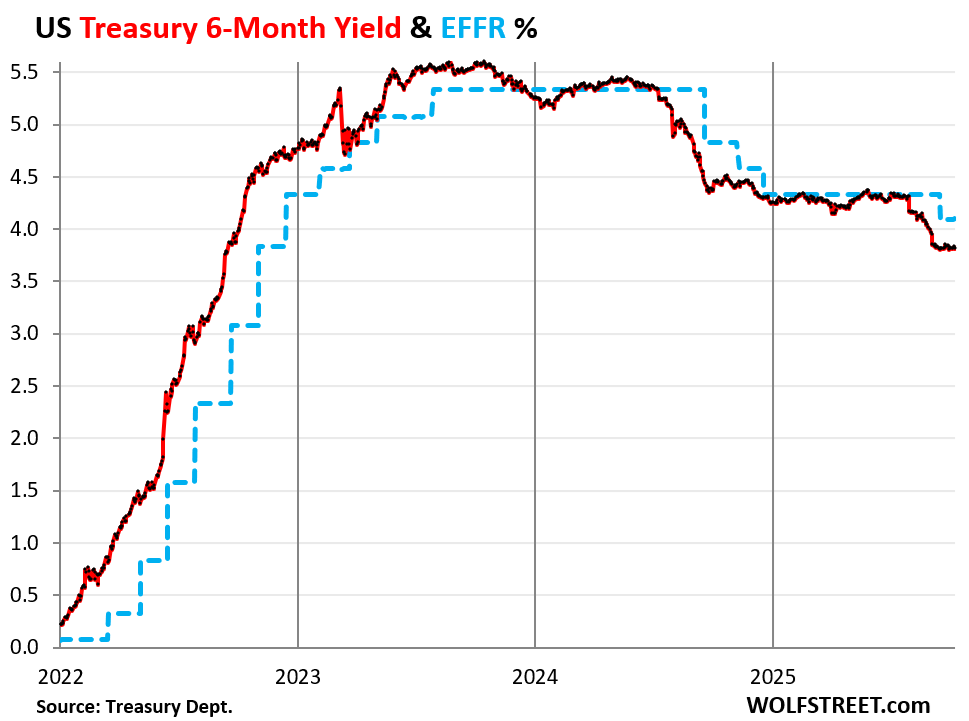

The 6-month Treasury yield closed on Friday at 3.83% and has been in the narrow range between 3.81% and 3.83% for a month.

It reacts to expectations of the Fed’s policy rates over the next two+ months, and is a good indicator where the short end of the bond market thinks the Fed’s policy rates will be within this two-month-or-so window.

The FOMC rate decision on October 29 is squarely in its window. The December 10 rate decision is near the edge of its two-month window. So the 6-month Treasury yield is for now showing bond-market expectations of only one more 25-basis-point cut this year.

Deficit funding shifts to T-bills.

Bessent’s Treasury Department had laid out a strategy of increasing T-bill issuance in order to finance new deficits with T-bills rather than longer-term Treasury notes and bonds. The idea was to take upward pressure off the long-term yields so that they wouldn’t rise further, and to reduce interest expenses as the Fed would cut short-term rates.

T-bills, which have terms of 1 month to 1 year, mature in large amounts constantly and are refinanced with newly issued T-bills. So when short-term rates drop, interest expense from T-bills drops fairly rapidly.

Auction sizes of T-bills have increased further. They’ve been increasingly gigantic since the debt ceiling in order to replenish the government’s checking account, the Treasury General Account (TGA) back to the desired level of $800 billion, which it reached in mid-September, and in order to fund part of the new deficits.

Over the auction week through October 10, T-bill auction sizes were larger on average than in the same week in August. (Note: none of the auction figures here include the Fed’s SOMA purchases.)

For example, the 4-week T-bill auction on October 6, at a massive $110 billion, was $10 billion larger (+10%) than in the same week in August. The 6-week auction of $90 billion was $5 billion larger (+6%) than in the same week in August.

| Type | Auction date | Billion $ |

| Bills 6-week | Oct-7 | 90.0 |

| Bills 13-week | Oct-6 | 84.0 |

| Bills 17-week | Oct-6 | 69.0 |

| Bills 26-week | Oct-6 | 75.0 |

| Bills 4-week | Oct-6 | 110.0 |

| Bills 8-week | Oct-9 | 95.0 |

| Bills | 523.0 |

Auction sizes of 10-year notes and 30-year bonds have declined a little, but were still huge. Compared to the same week in August, the 3-year auction size this week was unchanged, but the 10-year and 30-year auction sizes were each $3 billion smaller.

| Notes & Bonds | Auction date | Billion $ |

| Notes 3-year | Oct-7 | 58.0 |

| Notes 10-year | Oct-10 | 39.0 |

| Bonds 30-year | Oct-9 | 22.0 |

| Notes & bonds | 119.0 |

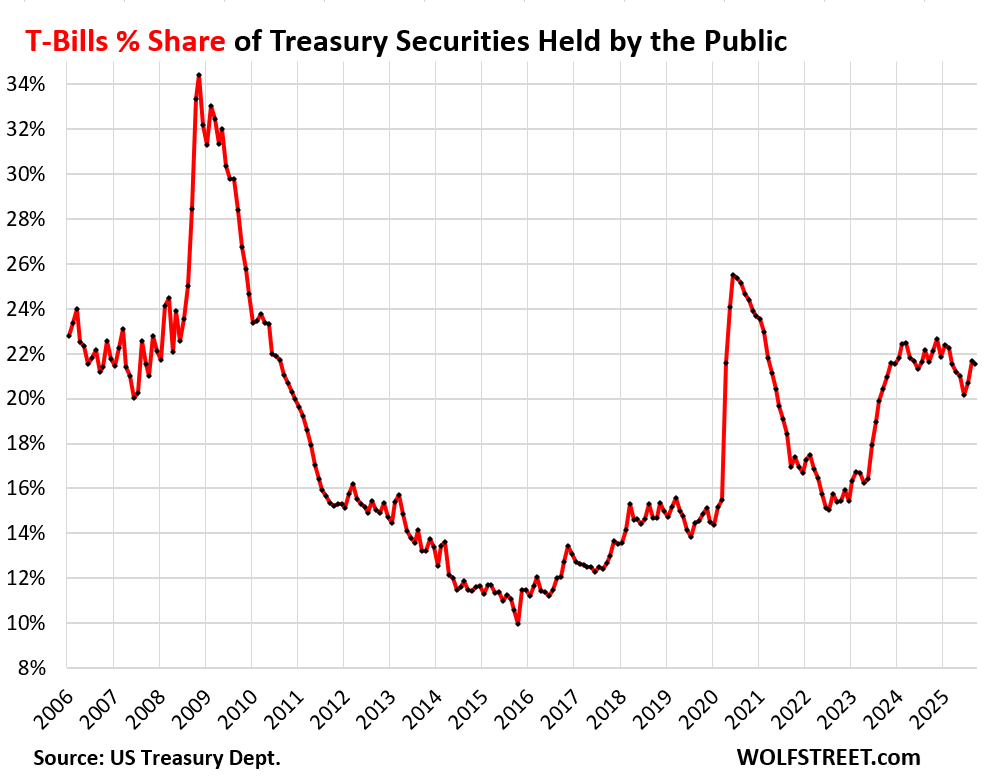

The share of T-bills outstanding, as of the end of September, has not yet reached the 2024 levels, according to the monthly data from the Treasury Department. That is due to the drop in the share of T-bills outstanding during the debt ceiling, when the size of the note and bond auctions were maintained, but T-bill auctions were reduced to keep the overall debt below the debt ceiling.

After the debt ceiling, starting in early July, larger T-bill auctions to replenish the TGA (government’s checking account) brought total T-bills outstanding back to $6.4 trillion by the end of September, where they had been at the end of 2024, just before the debt ceiling.

At the end of September, T-bills accounted for 21.5% of total marketable securities, roughly in the same range since December 2023, and below the 2024-high of 22.5%.

But with the increased T-bill auction sizes, and slightly smaller 10-year note and 30-year bond auctions, the share of T-bills should start creeping up beyond the 2024-highs, and the first signs of that should come with the data for the end of October:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The stock market dropping was using the news of tariffs as an excuse. Look at the RSI and stochastic RSI. RSI has been approaching 80 on the 3 major indexes on the weekly. It rarely crosses over 80. SRSI has been at or near 100 on both fast and slow lines for weeks and weeks and weeks. I’m just waiting to see if this is a longer term correction, start of a large pullback, or just the market shaking out short interest and option contacts.

It will be soft landing into a cliff face.

Well, at least if greater tariffs do happen it happens post our holiday season which is probably well stocked or at least on ships heading here. I am sure China will offer something meaningless for appeasement but hold strong on their strategy. Maybe China will buy some soybeans and the world will be straightened out.

“Maybe China will buy some soybeans and the world will be straightened out.”

China’s buying gold, “hand over fist”. On the books, and off the books.

That’s how “the world will be straightened out”.

As of June 2025, China only owns 2299 metric tonnes of gold which is even less than the 2330 owned by Russia and completely dwarfed by the 8,133 owned by the US Treasury. Gold is a trivial and irrelevant commodity worth less than 1% of global assets in the big picture.

Chinese state media (Xinhua) reported, in 2020, that China’s gold reserves have grown for 15 consecutive years—reaching a sum of 14,727 tonnes. Xinhua News is the PRC’s largest newspaper by circulation.

So the US, the Chinese and the Russians are all out of step, like everyone except,,,

There is no doubt in my mind that China has much more gold than the US. They have been buying for years. This is all to support the move to back the Yuan with gold for cross border settlements. Not Yuan Reserve Currency, China wants no part of that. Gold has already exceeded the US Dollar as the primary reserve asset by central banks. Happened just recently.

You should consider educating yourself a bit more about gold and where things are headed.

Too much money in the system:

Bond prices go up, yields go down. Low yields make housing unaffordable as asset prices rise.

Money out of astronomical stock prices goes to bonds, doesn’t seem to cause problems just sitting in stocks.

How about taxing all of that money sloshing around. Could fund everything, including an empire not seen since Rome, including true vassal states shaken down for tribute. Arches of Triumph for Presidents and Senior Senators. Just a thought to stimulate those politicians that would like to see a monument to themselves like Pharoah Ramses II (Ramses the Great), all you have to do is tax the oligarchs.

All money is sitting in bank accounts at all times. Or in wallets, or under the mattress. Imaginary money is sloshing around.

Just when you thought it was safe to go back into the liquidity….SharkRato! Federal Dropcorn will be available at the concession stand until further notice.

What makes the Treasury think there will be enough buyers of short term T-bills, especially if the Fed Reserve continues to lower interest rates?

If inflation is still in the 2.5-3.0% range, I would think buyers will not be interested unless they are making at least 1-1.25% above inflation.

So they are going to sell a shitload more short term T-bills, all the while lowering the short term interest rate, and not achieving the 2% inflation rate until two years in the future. It does not make sense.

There will always be those that will be okay with staying even with inflation as a hedge against a downturn in the stock market. That is my take anyway. Not great for those looking at treasuries as income stream however.

Not sure, but maybe the “Stable Coins” will be the next trick on the block enabling the new debt strategy. Crypto “Stable Coins” have a backing — though opaque — from T-bills and the amount has gone from 1 Trillion to 4 Trillion in just a few years.

Maybe a reason why the US Admin is seen as friendly towards Crypto. It might need to have this trick, and sleight of hand in its tool kit.

‘Maybe a reason why the US Admin is seen as friendly towards Crypto.’

Or because the US Admin and family has launched a bunch of their own coins.

Arbitrage opportuntieis mean there will be enough buyers of short duration t-bills (for example, borrowing overnight at the ON RRP rate and then purchasing 4-week T-bills).

Federal expenditures end up in banks. That is a lot of money. From the bank’s perspective it is better to have it earning some interest on t-bills than just sitting there. And the t-bills can be used as collateral when short term cash is needed.

There’s still tons of foreign cash drawn to US treasuries, even at lower rates, but, that relationship is slowly changing, as the world economies undergo chaos this year, with tariff uncertainties continually evolving, and unsettled. That disruption and volatility causes people everywhere to become more hesitant about investing, resulting in more people shortening their investing ranges — the instability is driving demand for short dated treasuries — versus traditional longer fixed terms.

That in itself causes a loss of faith in future growth and impacts economic growth globally — because no one wants to bet on future growth. However, longer dated treasuries are likely to demand higher yields and react more so to Real inflation, so, maybe like the economy, we have this bifurcated treasury mkt that’s influenced by a savings glut and bond glut — seems like wealthy people will be rewarded by longer yields, while the average Joe sees negative Real yields on the short end.

I know the king and future pawns in the Fed think they want lower rates, but overall, I don’t think that’ll play out with the chaos.

My brother at Google says:

“In summary, the relationship described in Bernanke’s savings glut has been upended. Instead of foreign savings flooding the US and suppressing yields, the US is now experiencing a “bond glut.” This is creating higher yields driven by large Treasury issuance, US fiscal concerns, and diminishing foreign appetite, particularly as tariffs destabilize global trade and reduce the US’s safe haven appeal.”

“There’s still tons of foreign cash drawn to US treasuries”

and Canada is one of the leaders supplying treasury buyers according to Wolf’s data.

Meanwhile, Canada has been identified as a major money launderer for the Cartels by the US gov’t and RCMP:

“Cartels laundering drug sales though Canada’s trade system, RCMP assessment says

Internal 2022 bulletin found Canada had ‘limited resources’ to stop trade-based money laundering.”

Maybe I’m wrong, but is sure looks hinky to me.

That’s a fairly obscure and opaque situation with money laundering — but, it gives interesting color to the Bernanke savings glut theory — which also connects to crypto, as a money laundering machine.

That’s obviously in the fringe of being insanely conspiratorial — but, the amount of demand for low yielding treasuries, and continuous demand for crypto, both suggest excessive liquidity and churn rates.

Apparently cartels do use treasuries and crypto, to launder money — so taking losses in treasury yields is inconsequential in their goal to getting fresh cash back — same with crypto.

I was originally thinking your comment was unrelated to a savings glut, but, there’s probably a tsunami of laundering happening globally — I don’t see that as Canada specifically — and don’t see the USA as doing much to manage this.

I think it’s a fascinating sublayer in global liquidity.

High yields also make housing unaffordable. Most people consider the monthly payment, not the overall cost.

Yields and mortgage rates are NOT high. They’re at the low of of the historical normal range.

You have to remember, Wolf, that mortgage rates have been “low” for a generation now. Expectations have been re-anchored. Economics, at its core, is just advanced Psychology, and the average American mind subconsciously assumes a par rate (a combination of recent rates and comfortable whole numbers – in this case, probably about 5%) to compare everything against.

You say it as if beating inflation (or even staying even) is somehow guaranteed. Are there no times when one picks where to lose less?

Let’s assume bond vigilantes become increasingly concerned about the sustainability of the government’s debt. They would sell longer-duration Treasury bonds, causing the yield curve to steepen. The impact on short-duration Treasury bills would likely be muted, as their yields continue to be driven primarily by the Fed’s financing rate. This must be the case; otherwise, arbitrage opportunities would emerge (for example, borrowing overnight at the ON RRP rate and then purchasing 4-week T-bills).

To some extent, the government can influence the Fed’s financing rate and the ON RRP rate, especially as the independence of the Federal Reserve appears to be eroding. In such a scenario—where bond vigilantes push up long-term yields—the government could continue to fund its deficit by issuing more T-bills. The relative scarcity of long-duration Treasury bonds could, in turn, increase their price (i.e., drive down their yields).

This is one reason I believe long-duration Treasury bonds may currently present an attractive investment opportunity. More importantly, when investors become risk‑averse—as happened on Friday afternoon—Treasury bonds are likely to rise while equities fall. The traditional inverse relationship between bond and equity prices should reassert itself. This relationship broke down when long-duration bonds offered near‑zero yields, as any increase in yields not only reduced bond prices but also raised the discount rate used to value equities.

I think you’re missing the forest for the trees.

Why would someone buy coupons (= duration risk) when there’s no yield premium vs risk-free T-bills? In this scenario the only benefit is if long rates go down – but how is that going to happen when the yield curve is basically flat?

You’re either predicting a) a bunch more policy rate cuts which don’t cause yields on duration to rise (what happened last time), or b) long rates falling some other way, causing the yield curve to go from flat to inverted.

Neither a) nor b) seem very likely to me. Therefore, there’s no benefit to buying coupons over bills with a similar yield.

How One Trader Made $160 Million Shorting Crypto Before Trump’s China Tariff Bombshell

A crypto whale made over $160 million in profit by shorting Bitcoin and Ethereum on Hyperliquid ahead of Trump’s 100% China tariff announcement

The trader closed all ETH short positions for $72.33 million profit and still holds $92.84 million in BTC shorts with 5.38x leverage

Trump announced a 100% tariff on China starting November 1 due to China’s “aggressive position” on trade

The crypto market lost $17 billion in leveraged positions within four hours following the tariff announcement

Bitcoin fell 7.5% to $112,505.92 and Ethereum dropped 12.5% to $3,837.57 in 24 hours

Seriously, who cares? Most people have no idea what coins are or do. Most people don’t care about the price of gold or if it goes up to 10 thousand. Only half the population cares about the stock market.

What they care about is the price of groceries, healthcare, insurance and housing costs.

No, they don’t care. If they did, the situation in this country would be different but it’s not.

Not even sure half the population really cares that much about the stock market. Probably 20% at tops.

And it will never, ever be investigated.

Just teach your kids that White collar crime is not punished in the US. Because that is the truth.

Actually ‘run of the mill’ white collar crime is punished much more severely in US than in Canada. By ‘run of mill’ I mean crime without Grade A political connections. The Enron number 2, (main man died) Skilling got 8 yrs if I recall. 8 yrs, if I recall is the longest bit EVER given in Canada. Madoff would have got 15 to 20, out in 8 -10, not 145 or whatever it was.

If you are planning a white collar scam in North America, look to Canada. Not Mexico? Not only is it unusual for perps to do much time here in Canada, in the rare cases where they are charged and convicted, the jails are better. It is also unusual for them to be whacked by their victims.

It’s high time we need Wolf’s article explaining in simple terms what Bitcoin is.

“Maybe you could tell me what you think is going on here. And please, speak as you might to a young child, or a Golden Retriever. It wasn’t brains that got me here; I can assure you of that.”

– Margin Call

Andy. In the past, Wolf has explained what crypto is. It is a line of code on a computer somewhere, that is used as a gambling token.

Bit coin is the perfect money laundering device. It is used to be art pieces or diamonds. What’s better than liquid and digital tokens for cleaning illegitimate income?

Gold

That’s my favorite line from the movie. Not the most illuminating, but definitely my favorite.

It’s straight up reckless gambling. Wolf has said so time and again.

Is now a good time to

MW Opinion: This is the dumbest stock market in history

The alleged “wisdom of crowds” is so stupid, so often that it seems crazy to suggest that today’s stock market — which is, after all, just “the crowd” chasing money — is the craziest on record. But a new research note from private-client fund manager St. James Investment Co. makes a case that’s hard to refute.

And that means all of us investors need to stress test our so-called risk tolerance sooner rather than later. Is our 401(k) or retirement portfolio balanced the way it should be? Do we have too much invested in stocks, and in riskier ones? If the market falls out of bed, will we look back on our positioning here and wonder what we were thinking?

At one level, there is no doubt that this is the dumbest market in history, because at this point it is completely dominated by “passive” index investing — the very definition of dumb money, because indexers buy stocks without any regard to valuation. Index funds chase the crowd, but increasingly index funds are the crowd — which is both dumb and crazy. St. James, citing research from Newport Beach, Calif.–based Research Affiliates as well as Morningstar, calculates that the total amount of assets managed by passive investors, typically index funds, now exceeds the total amount managed by active investors, who — for good or ill — actually look at things like balance sheets and income statements before investing in a stock. The lines, St. James estimates, crossed in February of last year.

And yet active investors still cant generate alpha. I got my popcorn out.

Wish John Bogle was still around to witness the upcoming end of ‘indexing”.

“In theory, there is no difference between theory and practice. But in practice, there is.”

There is the famous 2013 quote from Buffett telling the trustees of his wife’s inheritance to “Put 10% of the cash in short-term government bonds and 90% in a very low-cost S&P 500 index fund.” If Buffett died tomorrow, that could turn out to be really bad advice. There have been three occasions where investing in the index has failed to give a real return over ten years. This could prove to be another one.

The problem with the S&P500 index is that it is a market-cap weighted index. As the AI stocks became worth more, more index money was put into them until they now dominate the index and the index no longer represents the US economy. Also, share-buybacks by the big companies have distorted the index. If profits were distributed as dividends rather than buy-backs, that money could produce balanced investments.. Things have changed for the worse since 2013 and John Bogle’s days.

People have copied Buffett without understanding. Four more dangerous words in investing: “I have been told”.

The “dumbest stock market in history “…

Brought to you by the people who get their financial investment information from MarketWatch…

MW: U.S. stock futures rebound as Trump dismisses latest China tariff tensions: ‘It will all be fine’

Pass the taco sauce, please.

Hilarious- wonder how many knew to short on Friday and buy the dip a couple days later…..

Are there any investors left? It seems almost everything is a short term trade. Except the fools in IRA’s and index funds.

Two trillion lost as somebody made a tweet? It may all pop back, but not for those who had to sell or cover their margin.

I wish I could still play as I found it fun, but not at fraction of a second changes.

‘We will have a crash’: Why Andrew Ross Sorkin thinks this market bubble will eventually pop

A prediction of ‘eventually’ X happening does not meet the requirement in logic. It can’t be falsified, it can’t be wrong . It just looks like a prediction.

Wolf, have you digested the latest monthly treasury statement? Deficit of around 1.8 trillion, 1 trillion in net interest paid, 800 billion deficit before interest. If we can lower the interest expense, or keep it flat, keep spending in check, and grow the economy I think we can get out of this mess.

That’s a lot of “if’s”!

Strange that gold has resumed its march towards $5000 and beyond but Bitcoin still leaking air today after Friday’s crash. Seems like one is a store of value and hedge against inflation and the other is…well I’m not sure anyone can actually tell you what it is.

The ten year at 4.0 is fine with inflation likely to stay around 3% for a while. Mortgages “should” settle to around 5.5-6% which will help the painful clearing of the housing market over the next several years.