More consumers, more workers, more jobs, more money. GDPNow jumps upon these retail sales.

By Wolf Richter for WOLF STREET.

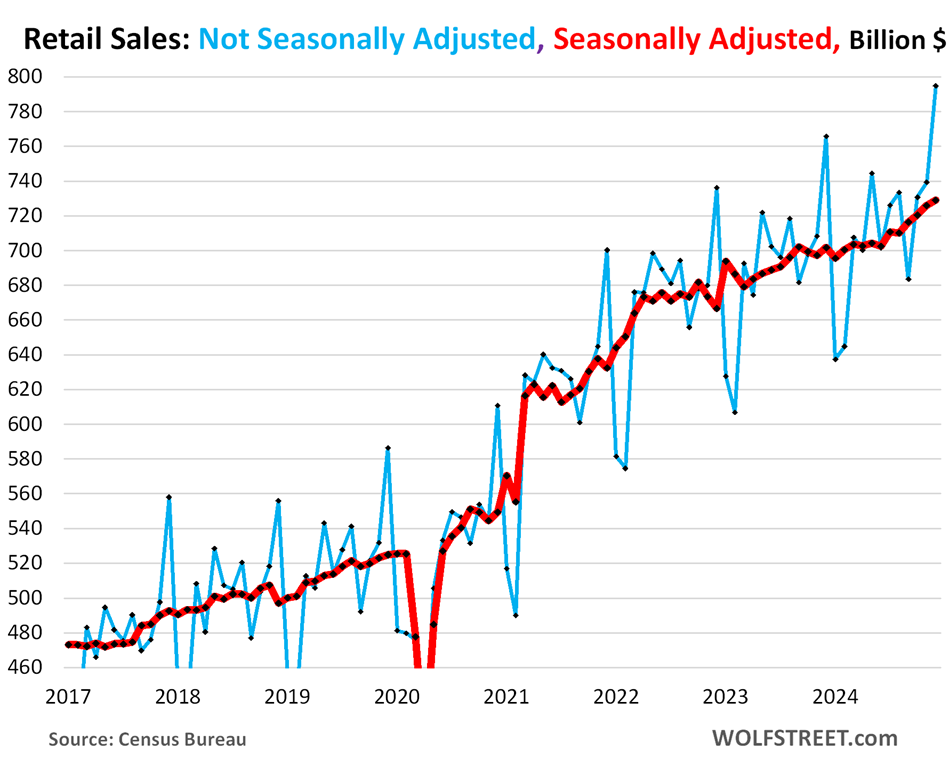

Retail sales rose by 0.45% in December from November (+5.5% annualized), and November and October were revised higher – October from +0.46% to +0.56%, and November from +0.69% to +0.77% – and it’s on top of these upwardly revised sales that December sales grew by another 0.45%, all seasonally adjusted.

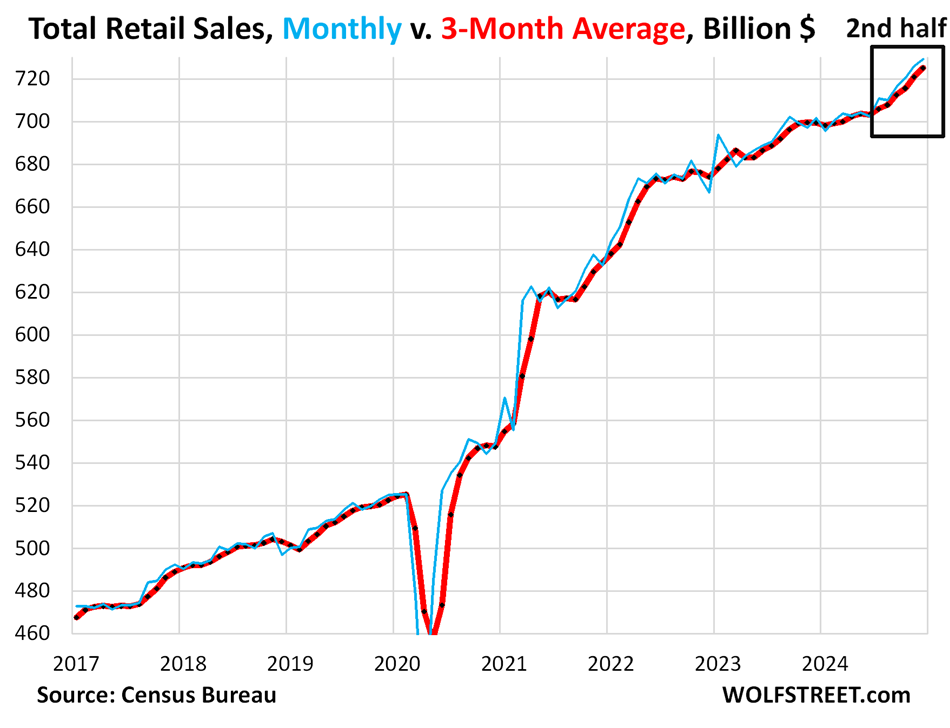

The slow first half was followed by a blistering acceleration in the second half, particularly over the past four months.

Not seasonally adjusted, December sales rose to a record of $794 billion. Ecommerce was a big winner; sales jumped 10.2% year-over-year to $156 billion, for a share of 19.6% of total retail sales, surpassing auto dealers and making it the #1 retailer category for the month.

The acceleration in the second half: Someone turned on the spigot.

The three-month average – which includes the prior revisions, irons out the month-to-month squiggles, and shows the trend better – rose by 0.59% in December, seasonally adjusted, after three-month average growth rates of +0.74% in November, +0.45% in October, and +0.66% in September.

To get a point of reference, on an annualized basis, December’s three-month average growth rate of 0.59% amounts to an annual rate of 7.3%. November’s growth rate of 0.74% amounts to an annual rate of 9.3%. That is huge growth for the US.

Someone turned on the spigot in the second half, and retail sales gushed, after a slow first half. June had been handicapped by the CDK hack of the cloud-based dealership software of thousands of dealers that prevented them from processing sales in June, which then got processed in July, shifting that portion of retail sales from June to July, but that doesn’t explain the surge in retail sales over the past four months of 8.2% annualized:

- 6 months January-June total: +0.1%, annual pace +0.2%.

- 6 months July-December total: +3.8%, annual pace +7.7%.

- 4 months September-December total: +2.67%, annual pace +8.2%.

Note the steepening of the slope over the past six months (black box):

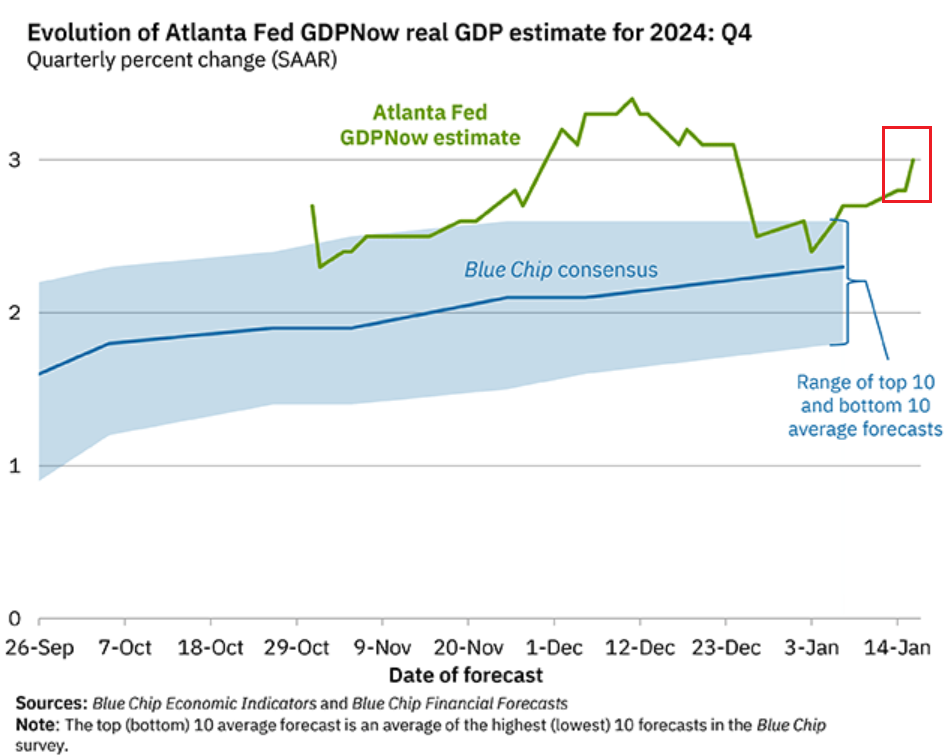

GDPNow jumped to 3.0% due to these retail sales.

The Atlanta Fed’s GDPNow “nowcast” for Q4 “real” GDP (inflation adjusted) jumped to a growth rate of 3.0% today, upon inclusion of the retail sales data.

Over the past 15 years, the US has averaged about 2% “real” GDP growth. If GDPNow is on target, Q4 real GDP would come in at about 3.0%. Over the past five quarters, there was only one weakling, Q1 2024 with 1.6% inflation-adjusted growth. The other four quarters ranged from 3.0% to 4.4% inflation-adjusted growth, which is huge for the US.

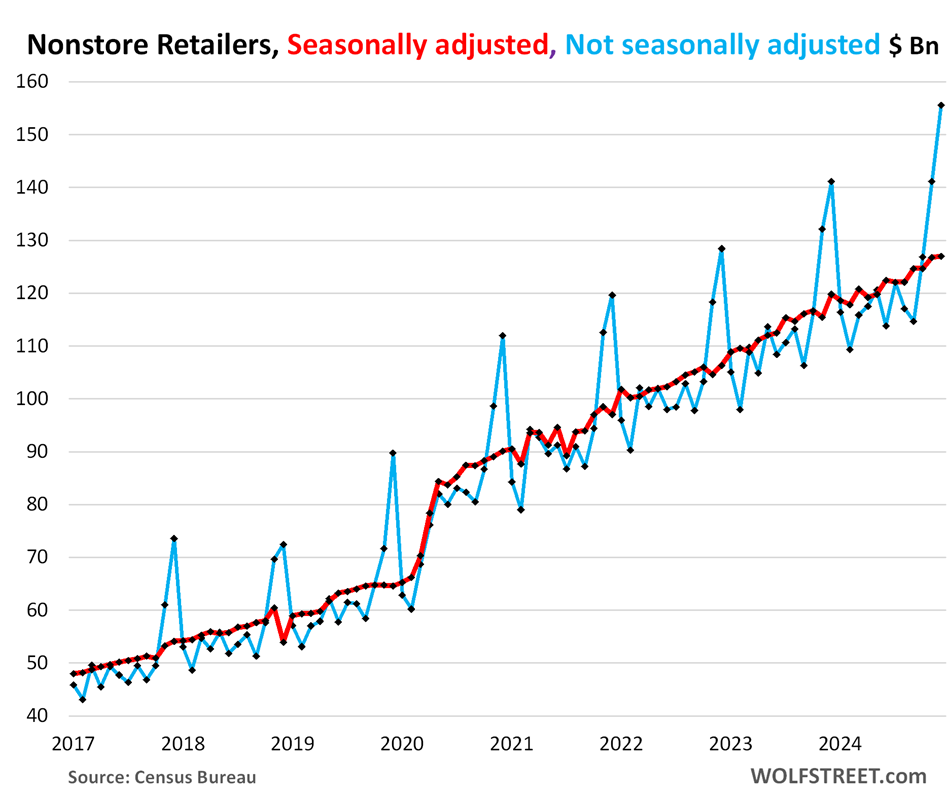

Ecommerce and other “nonstore retailers” (ecommerce retailers, ecommerce operations of brick-and-mortar retailers, and stalls and markets): Total sales not seasonally adjusted jumped by 10.2% year-over-year to $156 billion (blue). Huge seasonal adjustments reduced that to $127 billion (red). The three-month average sales in December from November, seasonally adjusted, jumped by 0.62%:

More consumers, more workers, more jobs, more money.

Our Drunken Sailors, as we lovingly and facetiously have come to call them, are in the mood to spend. The labor market has been solid, with an additional 2.23 million payroll jobs created in 2024, and with hourly earnings up by 4%, outpacing inflation for the second year. Consumers are sitting on vast and ballooning piles of cash in money-market funds and CDs. Stocks, home prices, and cryptos have soared in recent years, and consumers that hold them (64% are homeowners and many hold stocks in their retirement funds) are feeling flush.

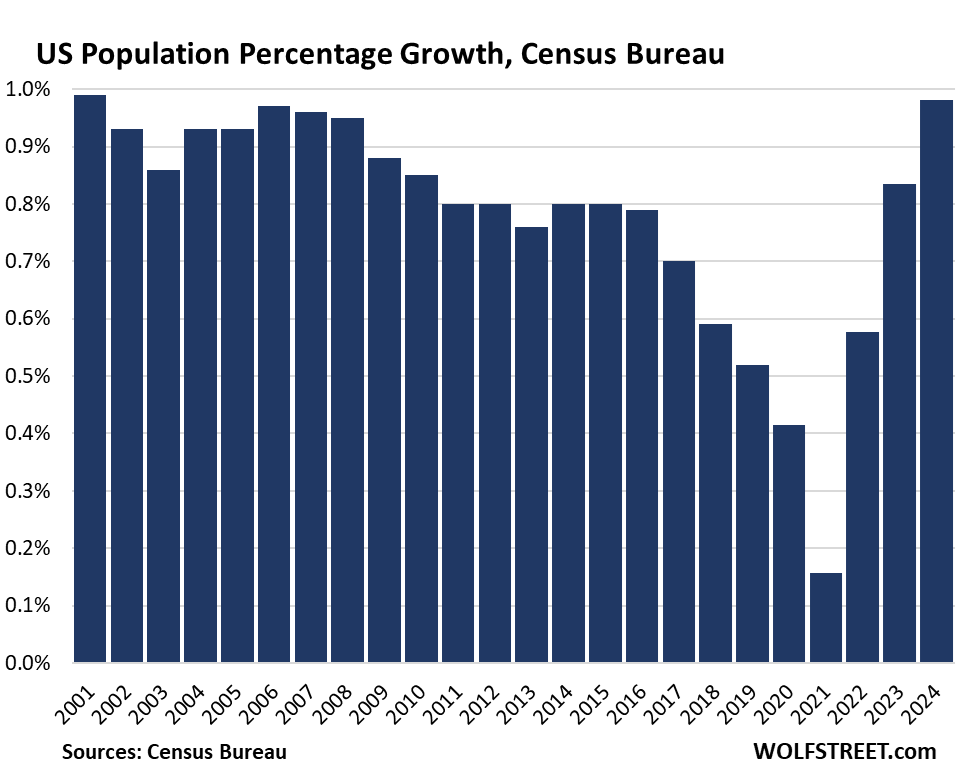

And there are a lot more consumers: net immigration added 2.8 million people to the population in the 12 months through July 2024, and 4.0 million over the prior two months, and so the population of the US over those three years soared by 2.4%, including by nearly 1% over the 12 months through July, the biggest percentage growth rate since 2001, according to the population updates by the Census Bureau in December.

Many of these new arrivals are already working, and they’re spending money too (detailed discussion here):

Amid this strong demand, inflation catches its second wind. The Fed needs to watch out.

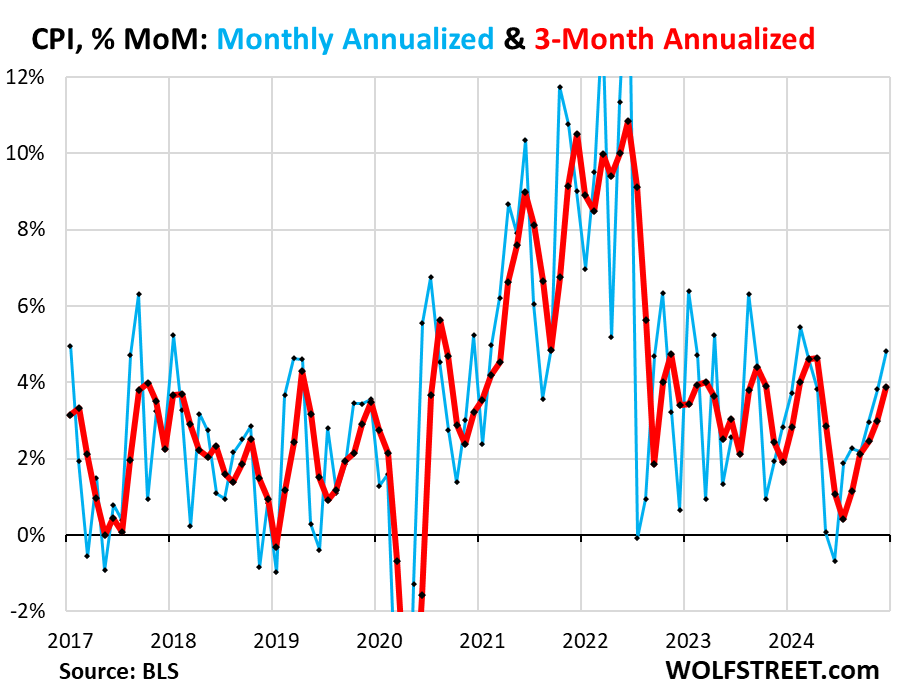

Inflation has been accelerating for the past few months. The latest piece of that puzzle came yesterday: The Consumer Price Index rose by 0.39% (+4.8% annualized) in December from November, the sharpest increase since February 2024. It has been accelerating since the low point in June (blue).

The three-month CPI, which irons out some of the month-to-month squiggles, jumped by 3.9% annualized, the sharpest increase since April, and the fifth month-to-month acceleration in a row.

This acceleration of the month-to-month CPI inflation rate over the past four months parallels the surge in retail sales.

The year-over-year CPI rose by 2.9%, the sharpest increase since July, and the third month in a row of acceleration (detailed discussion here).

But our drunken sailors are not dropping money everywhere equally.

Sales at nonstore retailers (mostly ecommerce) and at auto and parts dealers accounted for nearly 40% of total retail sales in December.

Some of the other major categories also booked strong sales, but not all. Some of the unique pandemic booms, such as home improvements, have blown over and aren’t coming back, it seems.

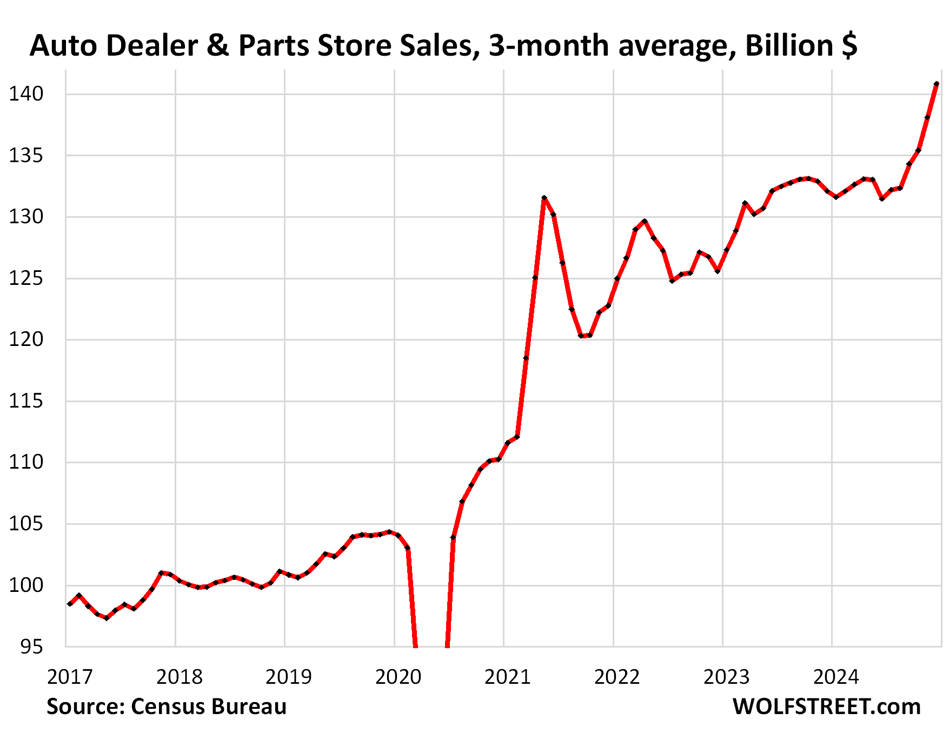

New and used vehicle dealers and parts stores, the second largest category in December: Sales on a three-month average basis soared by nearly 2% (seasonally adjusted) in December from November, and by 7.5% year-over-year (not seasonally adjusted) to $141 billion. This was a very strong finish of a year that had started out somewhat slow-ish.

The spike in dollar-sales of new and used vehicles in 2021 and 2022 was caused by ridiculous price increases in used vehicles and by a combination of addendum stickers, lack of incentives, and higher MSRPs in new vehicles, amid the shortages at the time. Starting in mid-2022, used vehicle prices began to plunge, and new vehicle prices flattened out, and though unit sales increased, dollar sales flattened out.

But over the past few months, new and used vehicle prices have started rising again, which contributed to the worst month-over-month CPI inflation reading since February and the worst year-over-year inflation reading since July, as we discussed here yesterday. These price declines caused the dollar-sales for those 18 months to flatten out, despite rising retail unit-sales.

This recent rise in new and used vehicle prices and the strong volume sales created this spike in dollar sales at new and used vehicle dealers.

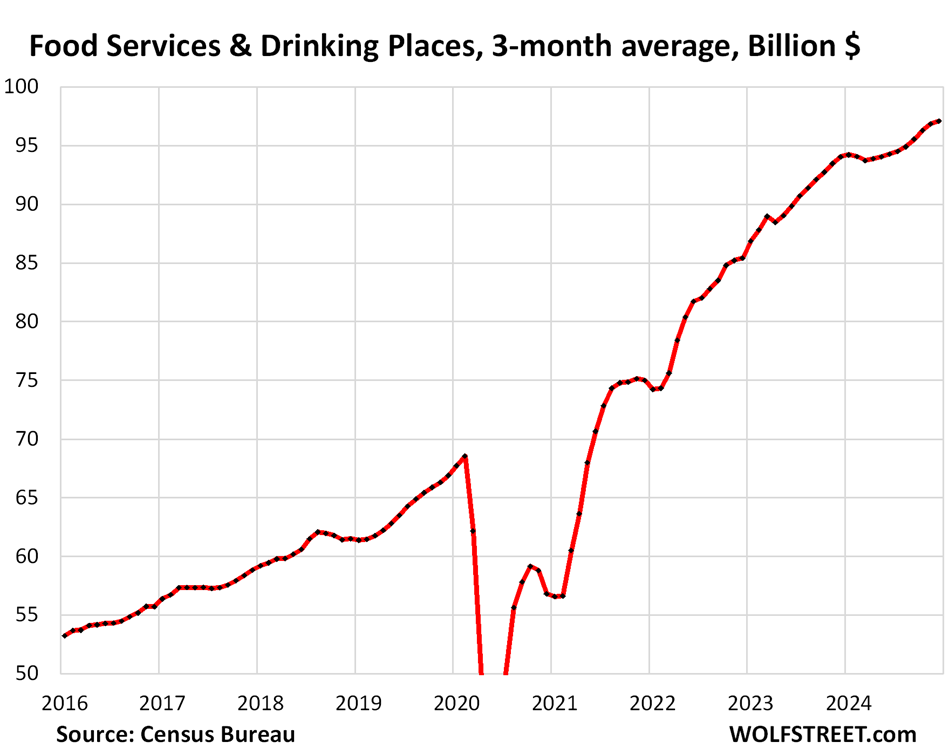

Food services and drinking places (#3 category, 13% of total retail), includes everything from cafeterias to restaurants and bars. After a decline in early 2024, moderate growth resumed:

- Sales: $97 billion

- From prior month, 3-month average: +0.23%

- Year-over-year: +3.2%

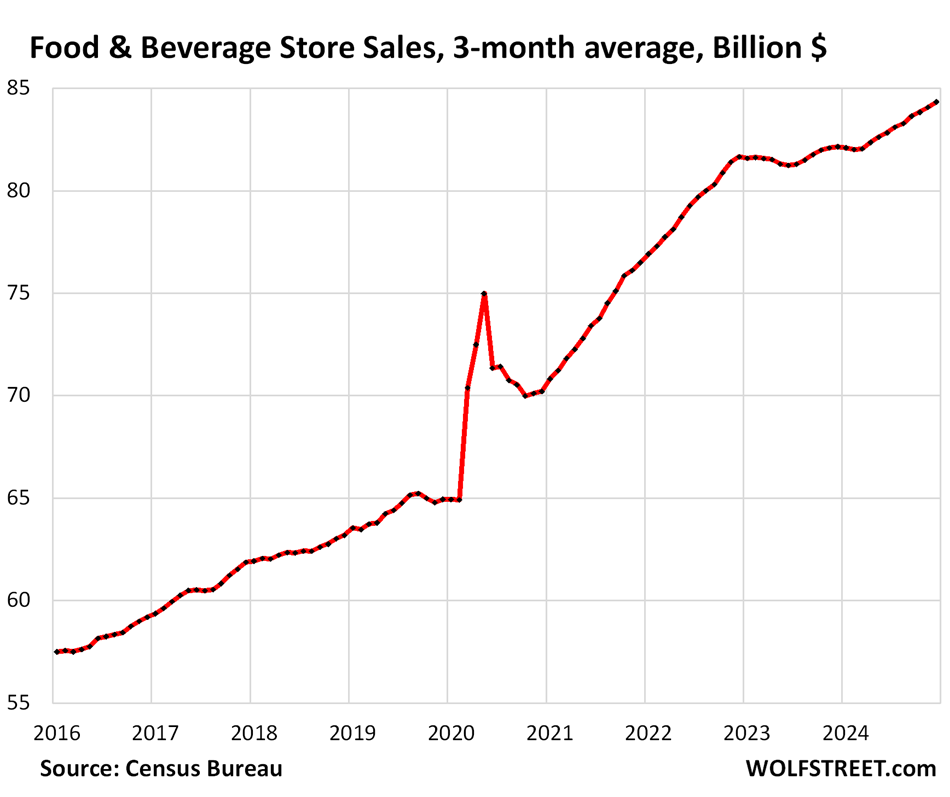

Food and Beverage Stores (12% of total retail). Prices per CPI for food at home exploded from 2020 to early 2023, which caused the spike in sales, then flattened out at high levels for a while, before starting to rise again:

- Sales: $85 billion

- From prior month, 3-month average: +0.30%

- Year-over-year: +2.7%

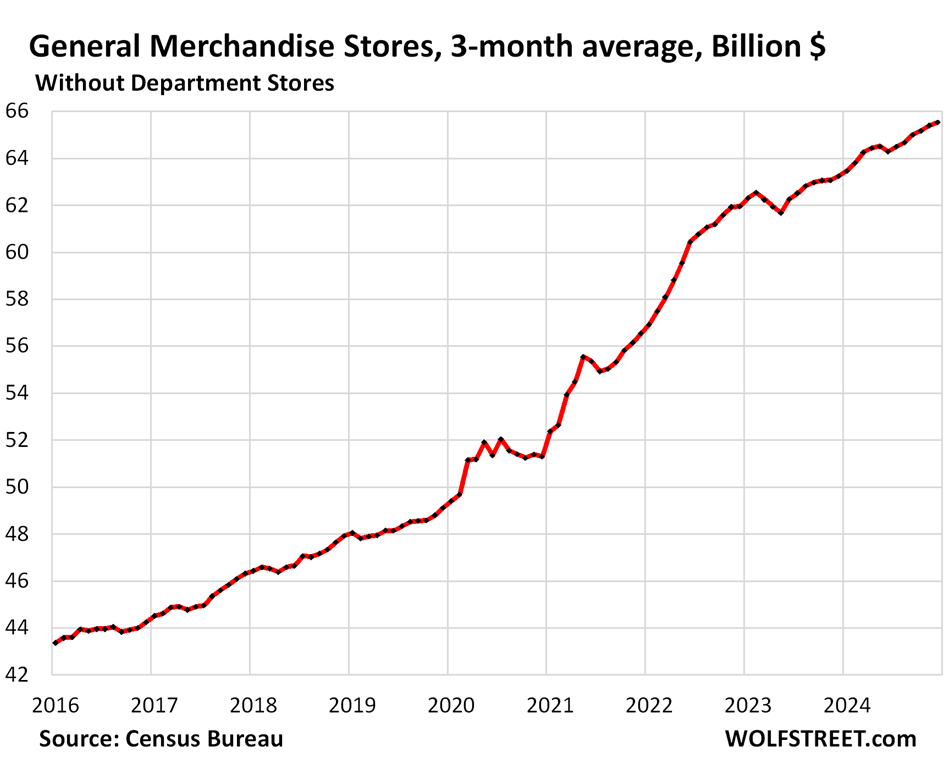

General merchandise stores, minus department stores (9% of total retail), including retailers such as Walmart, which is also the largest grocer in the US.

- Sales: $66 billion

- From prior month, 3-month average: +0.21%

- Year-over-year: +3.6%

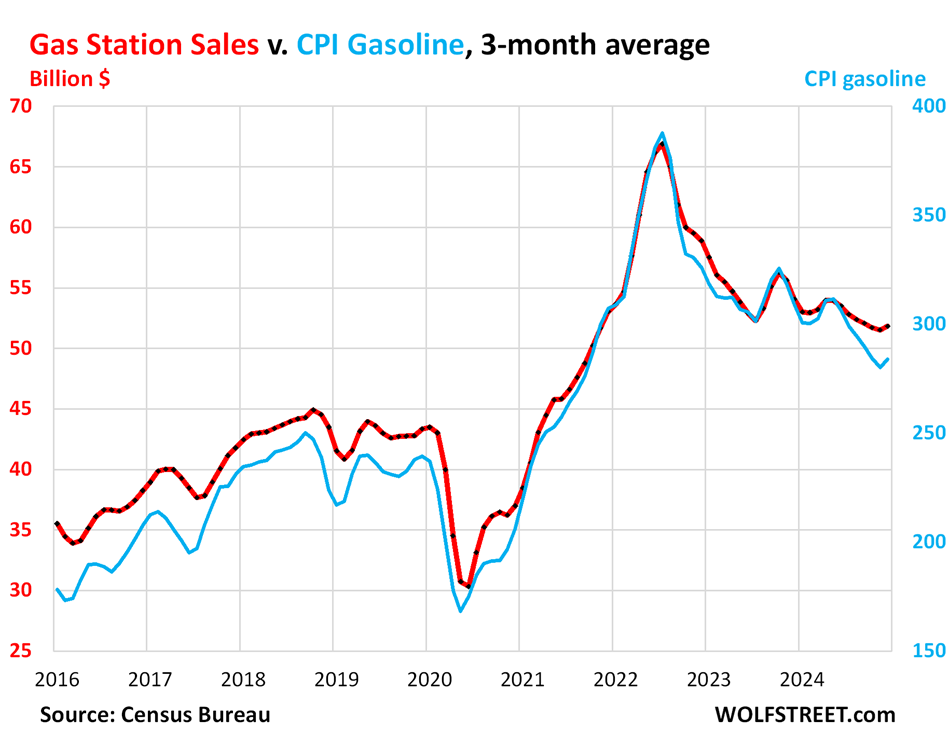

Gas stations (7% of total retail sales). Dollar-sales at gas stations move in near-lockstep with the price of gasoline. The price of gasoline started dropping in mid-2022 and continued to wobble lower until recently. These price declines pushed down dollar-sales at gas stations. Sales at gas stations also include all the other merchandise gas stations sell.

Gasoline prices started rising again recently, and so there’s this little hook for December, a three-month average that includes the price drop in October, a small rise in November, and the bigger rise in December:

- Sales: $52 billion

- From prior month, 3-month average: +0.63%

- Year-over-year: -4.1%

Sales in billions of dollars at gas stations (red, left axis); and the CPI for gasoline (blue, right axis):

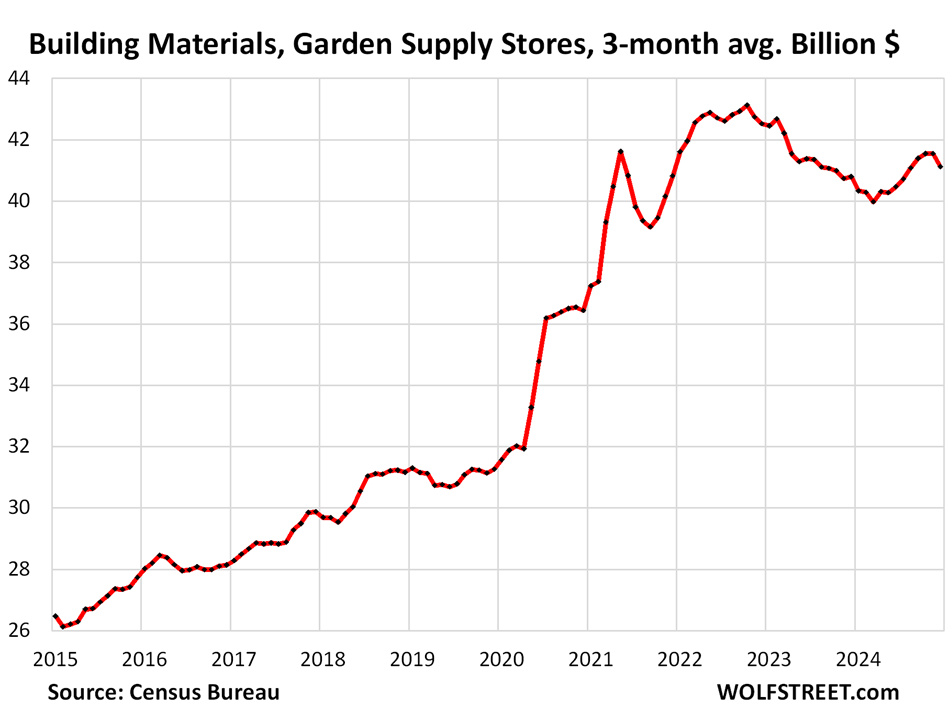

Building materials, garden supply and equipment stores (6% of total retail). The enormous remodeling boom during the pandemic fizzled in late 2022, and sales fell for a while. In 2024, sales started rising again from still very high levels, but late in 2024, they fizzled again:

- Sales: $41 billion

- From prior month, 3-month average: -1.0%

- Year-over-year: +0.8%

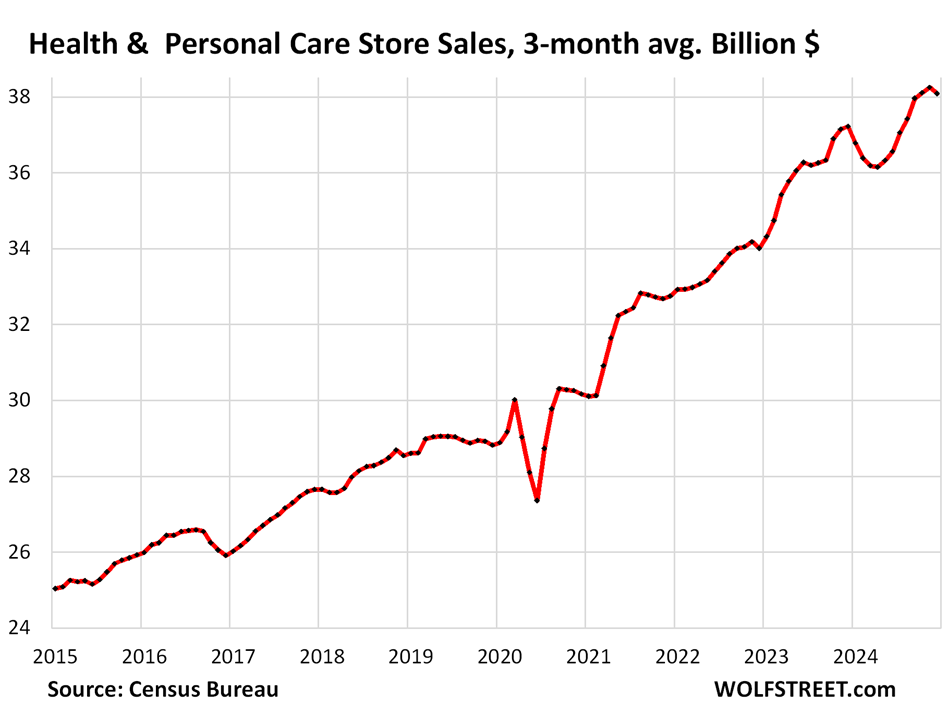

Health and personal care stores (5% of total retail:

- Sales: $38 billion

- From prior month, 3-month average: -0.42%

- Year-over-year: +2.3%

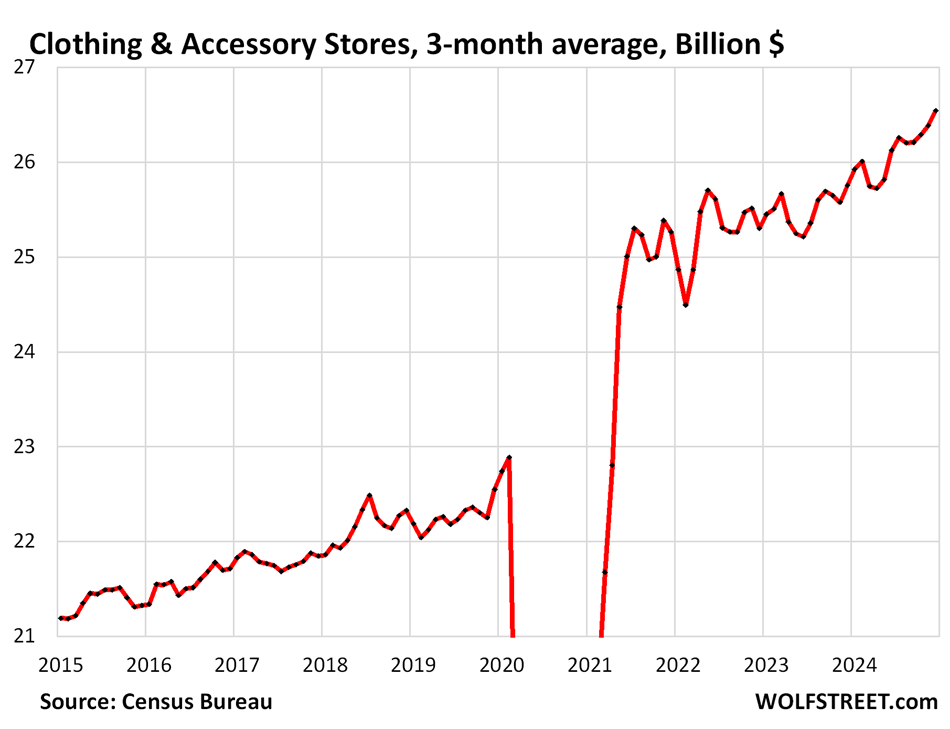

Clothing and accessory stores (3.7% of retail):

- Sales: $27 billion

- From prior month, 3-month average: +0.60%

- Year-over-year: +3.1%

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

It’s hard to believe U.S. retail sales total less than one trillion yearly when Federal deficits are well over 2 trillion per year. What’s wrong with that picture?

And the beat goes on.

This per month! They were $795 billion in December and $8.54 trillion with a T for all of 2024.

OOOPS. Standing corrected, Sir.

“The acceleration in the second half: Someone turned on the spigot”

It’s an everything mania in all assets, concocted by the FED. Just when you think it’s topped out and the ridiculous prices and values can’t go higher, they do. Sh!Tcoins with absolutely no intrinsic value or usage other than 100% pure speculative gambling have served to reinforce said behavior with seemingly endless upside potential. You might as well be selling air.

This is a dangerous place that central bankers and politicians have put the eCONomy. There is not a single thing that is even remotely valued correctly, save for maybe some commercial real estate, but even then you really have to put on your glasses to make sure.

The bottom line is that the FED should have NEVER cut rates. They should have continued to pause, which was premature in and of itself. Now it’s back to “wait and see and may need to raise again.” That’s a piss-poor way of handling inflation and this everything mania, but alas they serve the asset holders, and nobody else.

Makes you think they want inflation. Look at the outcome and deduce the motive. Carl Jung said that I think. I mean they took so long to even acknowledge the existence of inflation when it was clear to pretty much anybody with a pulse that things were out of control. Makes me think the delay was to allow inflation to become entrenched that they could come off the lower bound. Thanks wolf for your exceptional work.

Actually it’s worse – they DID acknowledge inflation but came up with a bullsh!t “it’s transitory” narrative, scoffing at it and dismissing naysayers with impossible levels of hubris while they themselves gambled in risk assets and front ran the markets on their own insider info. Only when the egg on their faces was so deep and dripping with irrefutable evidence did they portray themselves as bold do-gooders and start raising rates aggressively, patting themselves on the back the entire way.

The tactics of “stonewalling” are quite powerful on trusting masses.

When you have to go back to the 80s to find inflation, it seems natural, that the FED had no idea, what that is. It was the new Monetary theory that said, that there can not be inflation (even though QE was in full swing), well, in the end it was all BS, so they had to “do something”.

As Wolf said many times, inflation is a real problem, when you let it out of the box. It comes back and back, when you don’t deal with it properly.

The FED is scared of everything, it is afraid that something will break in the markets … That’s all they care about, so their policy is lax and wrong.

I spend like drunken sailor

just paid jan cc $6.7k, looked next day already at $1,700 and I just put $1,400 more on it yesterday

today easy just $500

Black friday I spent $2,700 on 4 appliances

—–

did I mention they are all for work – ie apartments/maintenance

Yes.

Well that correctly captures my darkest analysis of the current conundrum.

Inflated bubbles mysteriously don’t deflate. Definatly, suspicious happenings that make a mockery of the E101 indoctrination that the market is free and random.

I see the proposed Secretary of the Treasury seemed like weak tea during his testimony. Hopefully he’s not another Ben Bernanke.

You are too generous in your assessment of crypto.

Not only does it have no intrinsic value, it is incredibly wasteful in terms of energy consumption, carbon footprint, and water consumption. Recent estimates place the energy consumption of a single transaction at over 1,000 kWh, more energy than is consumed by the average US household over a month. At national average cost of energy, this is over $160 just for a single transaction.

Rates don’t matter much when people have insanely low mortgages and don’t need to finance purchases.

it’s very clear that the fed wants this asset mania. if not, why did waller open his yapper yesterday about inflation going well and 4 rate cuts?

there’s no legitimate reason for trotting out these speakers, week after week, unless it’s by design.

The funny thing is that the media and everyone here jumped on Waller’s “IF inflation… then cuts” while completely blowing off and ignoring the hawkish comments by other FOMC members, including Cleveland Fed’s Beth M. Hammack, who dissented and voted against the Dec rate cut, and who told the WSJ yesterday: “We still have an inflation problem. We still have a rate-of-change problem that we need to address,” and who wants the Fed to go slow on rate cuts. There were a bunch others in that same ballpark. But no, it’s just Waller who suddenly speaks for the entire Fed??? BS

https://www.wsj.com/economy/central-banking/fed-interest-rates-inflation-beth-hammack-87ed422d

i don’t disagree with you at all, and i read the other statements as well. but the fed needs to know at this point that the media will latch on to whatever “dovish” statement they can find.

it’s almost like my autistic cousin. he gets set off by bright red clothing. it doesn’t matter that it’s irrational, we know at family gatherings that he will behave irrationally if someone is wearing a red shirt, so we just don’t.

it’s the same. waller knows, or should know, how the media will react, and cause the yield on the 10 year to drop and to reignite inflation. thus, he should shut his trap.

I can’t wait for the Trump tax cuts. That will be final douse of lighter fluid.

Tangent: I saw a WSJ (I know could be sketchy) short with an insurance adjuster talking about the cost to rebuild the now hellscape Pacific Palisades. The screen flashed up a $3 / SF cost for finished drywall vs $10 for plaster. Apparently, a lot of these now reduced to ashes homes had plaster. Let’s do that math: A 4×8 sheet of drywall is 32 SF, so this guy is saying it’s going to cost $96 per board. A 1/2″ 4×8 sheet of drywall costs $13.50 in bulk from Home Depot, so let’s assume a big builder is only paying less than $13. So this guy is suggesting that it’s going to cost $80+ to hang & finish one 4×8 piece of drywall?

WTH??? HOLY COW!!! There’s going to be some serious sticker shock for those folks wanting to take 3-4 years to rebuild their homes.

Is there any hypothetical way Trump reverses on his tax cuts plan? Like, what’s the wildest imaginable scenario?

Asking as an outsider.

The reckless fed is on guard 24/7 for any disturbance, without fail. Powell is high up in the tallest tree looking for any signs of smoke from a fire.

Let’s hope he loses his grip up there,

Yeah, while LA is burning, he’s still looking for smoke …

FOMO in full flight.

Drunken Sailor here: Living well in retirement, traveling and enjoying life. The hardest part is avoiding all of the other Drunken Sailors spending their money at Costco and Home Depot any time of the day on any given weekday. Plus, the Drunken Sailors seem to show up at every vacation spot I visit, both domestic and foreign.

Humans are an invasive species.

I agree. I once described my vision of the concentration of humans as a bee hive engulfing the earth. The universe, heaven, will not even notice that we are gone. The earth won’t either.

The resolution of that very idea may save us.

wife made me go to costco yesterday, challenge finding parking

we only bought 5 items and it was over $100

> The resolution of that very idea may save us.

Malthus saw the “resolution” as a die-off. Many a biologist has observed this. I think our species was mis-engineered by biology — it got shunted onto a track now headed for somewhere very un-pretty.

Yes, I suspect the phrase “We drunken sailors” might be more appropriate. Let’s not put ourselves above the masses, eh?

Who you callin’ “we,” friend? Some of us play tight to the belt (or balance sheet), others not. Hence there is a thing called statistics to sort it.

“Average wholesale prices rose at an annual rate of 2 percent from 1964 to 1968, 4 percent from 1968 to 1972, and 10 percent from 1972 to 1978.” —Arthur F. Burns, The Anguish of Central Banking, September 1979

“Viewed in the abstract, the Federal Reserve System had the power to abort the inflation at its incipient stage fifteen years ago or at a later point, and it has the power to end it today. At any time within that period, it could have restricted the money supply, and created sufficient strains in financial and industrial markets to terminate inflation with little delay. It did not do so because the Federal Reserve was itself caught up in the philosophic and political currents that were transforming American life and culture.”

— Arthur F. Burns, The Anguish of Central Banking

Circumstances are far from identical to today, and I apologize for schlepping history, but this failed bureaucrat’s view from the end of the Great Inflation is worth the read.

Brilliant comment. I have never read A Burns hapless account of his inability to make a monetary decision that was contrary to the philosophic and political currents. I’m sorry but the concept of the Fed independence, is one of those religious relics that we just know are good luck.

Grasping for certainty in a world in which certainty doesn’t exist.

John H- I appreciate the quote from Arthur Burns. The “ philosophic and political currents” were the belief that you could use Keynesian stimulation all the time, rather than just in downturns, to pay for great American projects like the Viet Nam war.

LOL. I am positively, absolutely 100% certain, that Arthur Burns did not start the Viet Nam War.

What is a central banker supposed to do when the politicians say “give us money” ??

Watch and see as we roll further into 2025.

“What is a central banker supposed to do when the politicians say “give us money” ??”

Simple. Exercise the independence supposedly crafted into the role. Would you do something harmful if told to do so by your boss?

We’re losing value, but we’ll make it up on volume!

phleep – ever since reading of Milo’s Mediterranean egg trade in Heller’s ‘Catch-22’, have always considered this the main psychological driver for the acquisition of beyond-massive amounts of human-issued ‘wealth’ (…which never seems to consider an expanding number of the spacecraft crew bag-holders as part&parcel of the exercise…).

may we all find a better day.

Stillastudent-

“The first panacea for a mismanaged nation is inflation of the currency; the second is war. Both bring a temporary prosperity; both bring a permanent ruin. But both are the refuge of political and economic opportunists.”

—Ernest Hemingway, Esquire, 1935

That said, Vietnam was one of many contributors to the inflationary bout in the 1960-70’s, as Burns speech eloquently describes. The overall problem he depicts seems to be the public’s (and their elected officials’) expectation that the federal government can/should cure all of society’s ills — whatever the cost.

At the top of the cost list are unmanageable debt growth and disastrous dollar depreciation.

The mistake was from changing net free or net borrowed reserves to the Fed Funds Bracket Racket in c. 1965.

Bonds celebrated the “good” news with a nice little rally today.

Starting to sound like Groundhog Day, isn’t it…

And next week we are sailing into a drunken “new economic golden age.”

Buckle up.

I think they mean a new economic bitcoin age. Gold and bitcoin who needs dollars?

What happens if unemployment slips? Big problem.

That is why bitcoin like gold fails the currency test of being accepted as payment for a pizza at one of our many pizzerias.

Just owned 18% UST’s and foreclosed real estate in the 1980s. Think we will see it again?

Hey Wolf, might be a good article to distill Bessents answers from his hearing today. Said a number of interesting things but wading through the grandstanding in the 3 hour hearing sucks.

Fart coin is being upstaged by the new b-hole coin. Where is this country going?

It really looks like they are going taxpayer money to support crypto and send it soaring upwards – so that the oligarchs and crypto gamblers can take it all in.

This is not going well. And it is not going to end well.

Right. All of the “whales” in BitCON and crypto are the billionaire crowd. Mark Cuban, Elon Musk, Michael Saylor, etc. They poured in, then they “legitimized” it by incorporating it into financial site stock tickers like Marketwatch, etc., talking about it on the biased MSM financial shows like CNBC, using paid shills to tout it, then rolling it into 401k portfolios and such.

Now, we’re entering a situation where the US government itself, long ago hijacked by said billionaires, is poised to start buying this garbage with US taxpayer funds. Then, when the whole sh!tcart starts to wobble, they’ll bail it out “because the whole system could collapse if we don’t.” These billionaire a$$holes have become a cancer upon society.

“the US government itself, long ago hijacked by said billionaires, is poised to start buying this garbage with US taxpayer funds”

The Fed and .gov don’t even buy equities. Crapto will be a ways behind that.

Maybe you meant they’d buy it into pension funds for FERS or something. Still doubtful.

The precedent is John Law in France in the 1720’s, infiltrating and corrupting the financial system. His gimmick was paper money and worthless pie-in-the-sky stocks.

The question should be why did SEC approve crypto ETF or why did the democrat government being fully aware of the carbon emission and environmental impact of crypto not shut it down like what China did? The whole system is corrupt.

Federal Reserve Governor Chris Waller said today they may be ready to cut even sooner than the market expects. It’s amazing with this data that someone in his position can say something like that. I just don’t understand the need to keep heating up the economy.

They genuinely believe that pivoting back toward accommodation is the right thing to do at this moment.. It’s astounding–and you’d think nothing was astounding after the policy errors of 2020 and 2021.

Steelers Fan

The funny thing is that the media and everyone here jumped on Waller’s “IF inflation… then cuts” while completely blowing off and ignoring the hawkish comments by other FOMC members, including Cleveland Fed’s Beth M. Hammack, who dissented and voted against the Dec rate cut, and who told the WSJ yesterday: “We still have an inflation problem. We still have a rate-of-change problem that we need to address,” and who wants the Fed to go slow on rate cuts. There were a bunch others in that same ballpark. But no, it’s just Waller who suddenly speaks for the entire Fed??? BS

https://www.wsj.com/economy/central-banking/fed-interest-rates-inflation-beth-hammack-87ed422d

Pea Sea,

If they cut 50 basis points this year, the 10-year yield might go to 5.5%. If they cut 100 basis points this year, the 10-year yield might go to 6% (licking my chops), with mortgage rates over 8%. At some point, the bond market is going to get seriously spooked.

I’m starting to think you may have something there, Wolf. It sucks for me as a saver with no appetite for duration, but the Fed really does seem to be pratfalling ass-backwards into higher long term rates.

Wolf, so you see (as I) 6% yield on the 10-yr is close to the limit of what Uncle Sam can afford?

“… the 10-year yield might go to 6% (licking my chops)…”

Sounds like “vigilante justice.” Despite zigs/zags in treasury market, the bond market appears to scent Fed ineptitude around the next couple of corners.

I agree with you

I’m getting 5% on my 1 year CD’s and enjoying every minute of it. I’ll save gambling for my football picks every week.

That’s because you opened those CDs when policy rates were higher.

Still waiting for an example of a new issue CD with a 5% coupon.

ShortTLT – NuVision Credit Union is now offering 5.5% for an 8-month CD.

The rates are there if you want to chase them. I stick to a few banks I trust and go with the highest offer from that group at the time.

The people who are collecting all the chips on the table don’t think they have enough yet. Hubris and greed are a toxic combination.

…attempting to gamble our way to prosperity with an entering Executive whose own casinos went broke…

may we all find a better day.

Yes!

Nothing says gambling quite like pledging future tax receitps to lever up on BitCON. If the US government starts gambling in this toxic casino, we ARE finished.

You guys just don’t “get it,” endlessly soaring profits from fartcoin will be used to pay down the national debt. /s

Was this the guy who pardoned his own casino named hunter?

Tom – …have always wondered why ‘whataboutism’ appears to be employed to solely-deflect and wholly-transfer revealed negative tars instead of asking why those particular laissez-faire actions of the original party are ignored, or even excused, but not the counterparty’s, and by extension rarely resulting in a significant to tarring of both, loudly, roundly and equally…(…in part, perhaps, due to our sports-team zeitgeist appearing to have greatly-abandoned a prior belief that the position of Chief Executive is one of a firmly-scrutinized employee in favor of one of an elected ‘monarch’. Acceptance of outright lies, ‘Walls of silence’, or ‘king has no clothes’-hypocrisies among the public now extensively expected, and practiced by it, probably answers my own question, here…back to Hannah Arendt and my apologies to all…).

may we all find a better day.

This is the exactly point I put in comments for CPI article.

As per Waller, latest CPI report is very good. “IF” such good report data continues they can cut rates even in first half of the year. He said March rate is NOT OFF the table and he sees 3-4 cuts in the year, more than what Market is seeing.

If you are optimistic for future CPI coming down that’s ok too. You can say we have Bad CPI data but foresee good data. How 0.4% MOM and so much upward pressures in all sectors is good in any way?

Calling latest CPI report good makes him completely unworthy, irresponsible FED governor.

We had GDP numbers going up, Super Labor reports and Retail Sales. What else you want to see to know economy doing well, labor market is doing well, inflation has come down but still lot to go for the target.

Most Funny part was to see Market Cheerleader (CNBC Reporter) Sara surprised and puzzled at his super dovish comments. Even she couldn’t believe it for sometime.

AFAIK Waller and Logan are known as balance sheet experts. This makes me doubt FED’s QT plans. If he is so dovish and so eager to drop rates, he can not be trusted.

Muhamed El-Erian was saying don’t raise rates. Don’t try to get to 2%. 3% inflation is just fine and the economy is doing great at 3%. Trying to lower rates further will stifle the economy and innovation.

The CNBC host said: but 3% inflation a year hurts the low income people who do not own stock or assets.

If you want to keep tax receipts flowing, then you don’t want GDP to fall.

I’m reading today, 4 cuts back on the table, since inflation is doing so well. And Trump, that debt ceiling that could constrain QE, I think the writing is on the wall. Throughout his first term, his tweets were non-stop QE advocacy.

I see a future of near 0% interest rates, and the central bank a principle buyer of government debt, like Japan.

I’m hoping that was an editorial! Can’t believe the stuff they’re writing

Dr. Strangelove or: How I Learned to Stop Worrying and Love the Fed, starring Jerome Powell as Dr. Strangelove.

The doomsday device maybe activated and Dr Strangelove can’t stop it.

LOL … great movie. Did you know that Kubrick wanted Sellers to play 4 roles but he had an accident on set that prevented him from entering the set cockpit …. quite frankly I’m glad bc I think Slim Pickens was perfect & Sellers had his hands full.

Slim was perfect for the role,when he goes thru the survival kit and says a guy could have a good weekend in Vegas with it reminds me a bit of me Molle bugout bag!

GDPNow jumped to 3.0% due to these retail sales, all the while US government is running a sevenish negative budget deficit as a result of the obscene trade deficit and Trump era tax reduction legislation which is now about too expire.

The budget deficit means that the revenues into government through tax receipts are not sufficient to fund the government expenditures without borrowing at least the trade deficit and the obligatory percentage increase in the military budget.

Social Security is not included as an item in the Federal budget. It is a self funded social program to provide at least a minimum of care in old age. Which awaits us all.

The questions I have

– how are they paying for this splurge?

– how much of this is bringing forwards large purchases to avoid the tariffs?

– how much of this is disaster recovery?

– how much is return to work spending, more days in the office means I need to update my wardrobe and get a better car.

I suspect a fair chunk is in those last 3 buckets. Also not sure its sustainable in terms or being able to continue to pay for it all, the stock market gains are not going to repeat at the level they have forever, and I’m not seeing earnings rising at the same levels as retail sales. (Putting monthly earnings vs retail sales in FRED as a comparison graph shows its gone out of balance since the pandemic.)

I know I had loads more available since the pandemic to spend on ‘stuff’ without commuting and paying for expensive coffees and lunches at the office, and I know the 2 days a week has now turned to 3 days, soon to be 4 days and things are much tighter now.

I see a downturn coming….

Good Point..

People have been waiting for this downturn/recession for years to come :-)

There’s a built in solution to the childcare crisis in the work from home new wave….however, they want you to buy that coffee, lunches, gasoline, new cars, work attire etc. Uncontrolled capitalism for the workers…think not.

Watching your kids isn’t working. That’s the problem with that model.

RTGDFA

Especially read this section under the subheading: “More consumers, more workers, more jobs, more money.” And click on the links for details about where they’re getting this money.

DM: Walgreens CEO makes stunning claim about the impact locking goods up has had on the industry

Walgreens’ CEO has admitted that locking up items to avoid shoplifting has not worked – and it will close stores instead.

Not only has the practice not curbed theft, it has dramatically hit sales.

Over the past few years, major retailers like Walgreens, CVS, Walmart, and Target have increasingly resorted to locking up everyday items such as toothbrushes, deodorant, laundry detergent, coffee, and even milk.

They just figured that out now? Does this guy live behind the moon?

Apparently that was cheaper than just hiring security. One of the kids worked at Walgreens for a while. She was appalled at the shoplifting but more appalled at the lack of interest from the management and lack of anything resembling effective store management (schedules never posted, bathrooms that went uncleaned, plumbing failures that went unrepaired).

Staff isn’t being compensated for the risk exposures of confronting thieves? Thence to hand of their pittance wages to landlords in toto? (And I don’t mean to base on landlords.) It’s just that, we are not in Kansas anymore. Going to the shopping center as a little kid with mom was a pure pleasure, long ago.

US Treasury Pick Warns Of ‘Economic Calamity’ If US Tax Cuts Not Extended…

Savers were getting near zero percent interest for over a decade. Now they are getting 4.3%. If you had a million you were getting nothing. Now you are getting 43000 per year. That money has to go somewhere. Some back into savings, some into the wall street casino, some to pay down debt, but I bet a big chunk is going into buying stuff, retail stuff.

I have always thought that if the saving rates went up to 10 % + then the economy would flourish because of all the extra cash the savers had getting spent.

Not so good for the people with loans obviously but I didn’t see them losing any sleep when we were getting 1%.

Probably a few other downsides I suppose.

The implication here being that higher interest rates are actually stimulatory? I suppose it’s possible, yet it’s a huge snubbing of the conventional wisdom that only lower rates are stimulatory.

Higher rates benefit lenders at the expense of borrowers.

People with assets are more likely to be lenders, and people without assets are more likely to be borrowers.

Higher rates take from the poor and give to the rich.

By the same logic, lower rates give to the poor in the form of indebtedness? Totally.

You don’t know enough people with assets then.

Yes, higher rates are a stimulus, for big savers and risk adverse. However they are a drag to businesses who need to borrow

…so, what interest-level puts ‘just enough’ brake on what i’m hearing here as ‘necessary speculation’?

may we all find a better day?

CAV, economic decision making is a very tough business. Too many unknown variables.

In a mature economy, money moves a little slower.

DM: Investor who predicted dot-com crash issues chilling three-word warning as another market storm brews

A billionaire investor who predicted the dot-com crash 25 years ago warned that he is ‘on bubble watch’ as warning signs appear to have cropped up in the market.

Could satisfy wave 5 of 5 of 5 on this move.

Anyone who’s looking the charts can see it clearly. The questions are when and how bad. I may be reading the tea leaves wrong, but it seems like the Fed is trying very hard to let the air out slowly and avoid a dot-com/2008 financial meltdown type of event.

Who gets appointed next is a big question, that person is likely to be very open to manipulation and capitulate to demands from the White House – which will be to lower rates to stimulate the economy (especially real estate). So, all bets are off after May 2026.

If Powell tried to raise rates he might be sent to a concentration camp. Imagining that the former owner of the Taj casino is going to encourage or tolerate budget concerns may be summed up in his reply to his chief economic adviser Gary Cohn who did raise them: ‘just print the money’

Source: Bob Woodward

My $20 haircut went to $25 a few years back. Now to $30. It’s amazing. The Fearless Fed is only afraid of one thing. Not price inflation. Not high interest rates. Not income or wealth inequality. Not unemployment. Not financial stability. They only fear Deflation.

My old barber (RIP) went to $30 in 2019. Been cutting my own hair since 2020 (deflation!). It’s kind of fun to improve my skills with a power tool.

I tried that during the early pandemic and all I can say about the result is, thank God I wasn’t able to have a social life.

For me, I am at a stage where I don’t really care how I look though people do say I look pretty good :-)

I just focus mor eon low processed diet, exercise every day, yoga and meditation to stay fit. I feel I look good when I am fit and happier :-)

Jon,

Yes! I have benefited from such constraints a lot. I am slimmer and more fit, and it reflects on mental health too. Been cutting my hair with one cheap rig since 2008. I am not over-concerned with whether people think I have a $200 haircut.

Not wanting to spend $200+ on the Flowbee haircut kit, I found a comparable kit from Remington for $50. My apologies to Rick’s Barbershop.

How exactly do you manage to cut yourself from behind?

I use my wife hahaha

Practice, my dear. Practice.

Flowbee for the win! I have used it since the pandemic. Never going back!

In 2019 I was paying 11 for hair cut now it is 20.

But since covid I am cutting my own hair or let other people in house hold cut.

Reading the costs here makes me happy I live in the low rent zip code. Only $17.

Interesting, the local Krogers is also the cheapest. Usually it is the opposite, the low-rent area stores are higher priced than the upper-class stores (probably due to shoplifting?), but then this is Utah.

At least it is not 1857 anymore.

There’s tons of stuff you can save $$ on by doing it yourself. Haircuts, oil changes, searing your own steak (just taught myself that last one).

Also, the Fed only fears deflation in Treasuries. They can let everything else go to zero.

ShortTLT – If you want a good steak at home, invest in a sous vide. Cooked to perfection every time.

I’m saving money this year by buying a used exotic.

I always get mine cut in vacation.

This year Cuba and it was $1 USD including tip for the cut, hair trimming etc

Should last til next cut on vacation in Laos.

As I am a “brush hippy” no need to cut me gorgeous long locks of hair!

I save a ton of monies over the decades!

It has been pointed out in the UK press that the Biden administration is rushing funds out before the term ends i.e. there is an ongoing sugar rush

No. That’s not how “funds” flow from the US government. The announcement refers to contracts that they’ve signed. The actual funds flow months or years later, after due diligence, thresholds that have to be met, etc. Plus these contracts are “up to.” A lot of these funds are loans for factory construction… so we’re talking many months and years before they’re being actually disbursed. And they might never be disbursed in full if the thresholds aren’t met. Intel got its first small slice in December of the $23 billion in semiconductor subsidies that were announced with great pomp in March when they signed the contract.

It depends. All of the IRA monies have been pushed out the door, but that stimulates only certain sectors. They wanted all those funds deployed to the states where it would be very, very hard to claw them back. Everyone at the EPA and DOE is preparing for lay offs, many have already left – which has created a bit of a buffet for consulting firms looking for high level talent.

Those moves all started well before the election, when it was “just in case” since the policy preferences had all been telegraphed in advance.

Amazing (but not surprising) how the narrative from Wall Street regarding the PPI and CPI reports has been successfully portrayed as moderating Inflation which will allow the Fed to cut rates more.

The power of Wall Street over the narrative in the MSM is remarkable.

Good to have the sober and excellent analysis from Wolf

Look up who owns the MSM, and who pays for advertising with them.

they’re not owned by wall street. they’re owned by Microsoft, disney, comcast, and a few other big ones.

I don’t believe a single report coming out from the main street media, and business news channels. They are bought and paid for by their advertisers and abetted by the corrupt data collection beaurocracies in the Federal government. What I believe is my own monthly budget which shows service inflation , Insurance, taxes, medical costs, utilities, transportation, home maintenance, all going up at double digits with no end in sight.

Right on. Look at your budget and what you can see in your community. MSM is all lies and distortion.

And may I add some things are going up 30% or more in one year. Like the auto dealer prep charge which went from $500 to $800 in one year. I’ve become insensitized to the price increases. I’m joining the Drunken Sailors. If I want something, I buy it. It’s only the dollars that have become more worthless. Might as spend them before they lose more value. I went out the other day to my favorite Irish Pub and bought a pulled pork dish for $20. It was great, I been searching for a year and couldn’t find anyone in this town that can make that dish like this cook made it.

Bessent should have dropped the mic after this comment “ optimal tariff theory does not support what you’re saying,” said Bessent.

I’m sure everyone was thinking the guys a genius and he knows things that we have no idea what he’s talking about. He’s our guy!

I’d rather take my advice from Janet Yellen ! LOL

I don’t knownwhhat you’re referring to but Tariffs cause deflation by raising rates above neutral. It’s simple demand for money that causes this.

Tariffs cause an increased demand for money and restricts money supply.

LOL, deflation-mongerer. Everything causes deflation 🤣

And yet, the core PCE price index, which the Fed watches closely, has NEVER shown deflation (year-over-year negative).

Suggest you implement reaction buttons (4 options):

– Good point

– Very entertaining

– A little clueless

– What in God’s name is this guy thinking?

Btw, first chart says it all “Christmas”!

1. Never.

2. Not seasonally adjusted = blue. Seasonally adjusted (no Christmas) = red. So if you look at the blue line, compare it to where it was 12 months ago.

MW: No more Fed cuts and a 4.75% 10-year Treasury yield: BofA’s new calls

A Trump Bitcoin Reserve? I am sure that will end well..

I can’t wait to send my IRS money to this fantastic concept. Can I send double? We’re all going to be rich!!

MW: This strategist nailed when the Trump bump would end. He says stocks can fall as much as 40%.

Stocks are not going to fall that’s ridiculous

A significant number have already fallen dramatically and the stock indices are only up due to about 7 stocks all of which are likely headed to big plunges dead ahead as interest rates continue to rise.

People have been forecasting a “big plunge” for years already eventually they might be right. However, by that point it will be 2055 and the S&P will have hit 15k

@Dumb Idiot

Exactly. When the FED paused rates in 2023, I said it was grossly premature and would lead to all-time highs in stocks. I wasn’t wrong. The billionaires own every politician that matters, and control all of the media and every other important too to guarantee they never lose. Look how much they have right now, and they are just getting started. They are taking everything.

*too = tool

Not really, they often fall, the key is to be in when it raises, and out when it falls.

It’s your money so gamble it and lose it however you like.

Yes thank you Captain Obvious

DM: World’s largest comic company shocks fans by filing for bankruptcy after fallout with Marvel and DC

The world’s largest English-language comic company has abruptly filed for bankruptcy.

Oh! And Ms Yell-in suggested the other day that if we had an unemployment rate between 10-14%, inflation would have been lower. Look it up- this is no fantasy.

One Flew Over the Cuckoo’s Nest.

…recalling that not that many decades ago the pre-Murdoch ownership of the WSJ opined that an unemployment rate of 10% would be optimal for the nation…

may we all find a better day.

I can’t emphasize enough that Wolf is wrong and the Fed interest rates are too high and the BoJ interest rates are too low.

This is because Tariffs create a demand for US Dollars which drives US interest rates higher than they would otherwise be. We are being driven well into restrictive territory while Jay “inflation is transitory” Powell thinks inflation is sticky.

We are at risk of massive deflation.

And the Fed will drop rates to zero after the economy implodes and they realize their error.

But they will blame Trump even though it’s the Fed’s fault.

“We are at risk of massive deflation.”

LOL, in my entire life, and it has been dragging on for a while, thankfully, there have only been a few quarters of slight year-over-year deflation (slightly negative CPI year-over-year).

Core PCE, which the Fed focuses on, has NEVER gone into deflation (negative year-over-year). It has always been in inflation. And interest rates were a LOT LOT LOT higher back then. And there were tariffs too.

And yet, at every twist and turn all along the way, the deflation-mongers out there are preaching their manipulative BS when INFLATION has always been not only the risk, but reality right in front of them. Deflation-mongers are the funniest thing on earth. Priceless humor.

Also it’s a proven fact that Gold rallies in deflation only. Never during inflation. There’s research papers written on this. “The Behaviour of Gold in deflation” is the most notable.

It’s because Gold preserves asset valuation during deflation.

So looking at Gold spiking is just another data point proving my point.

Laughably false. Gold prices rising are purely inflationary.

There is no search thing as proven as you are talking about.

It was proven that long rates increase when FED cuts until it has been proven otherwise.

These are not laws of physics.

I don’t see any deflation anywhere.

They say if you remember the ‘70s then you weren’t there, but…

Gold was up 28% outpacing the SP’s 24%.

Didn’t see much deflation.

PS: in 2024

I demand that the euphemism “drunken sailors” be replaced with “drunken congressmen”.

…when the party is worldwide, dipsomania abounds…

may we all find a better day.

I just paid a couple of Latin American dudes $45 for 10 minutes of work to shovel the snow off my driveway and walkways. That’s $300/hr for tax free income for a couple of dudes with the equivalent of a 4th grade education. It used to be you could get a couple of teenage kids in the neighborhood who would do the job for $20. No more. They are out there with their dad’s car taking joyrides. I say, I came out OK, at least I got the job done.

You could have done it yourself for exercise, killing two birds with one stone: save on labor, and save on gym membership fees. Muscles aches are the extra benefit to last for days.

For some reason – i remember this from childhood – middle age and elderly men seem to have a fairly high rate of heart attacks while shoveling snow. Maybe this is one job that is best reserved for youngsters.

“middle age and elderly men seem to have a fairly high rate of heart attacks” that is true without qualifier. A sad truth. If you’re totally out of shape and with a list of health conditions, it’s probably better to start exercising by walking than by doing something hard, like shoveling lots of wet snow.

It would be worth considering a fundamental model for inflation. We have the metaphor of “Drunken Sailors” which suggests that money ends up in the pockets of consumers, and they unwittingly spend it unproductively. In other words, inflation is due to human psychology within a context. The sailor gets leave with his buddies, has money in his pockets, and goes to an area where one would have to be a monk not to spend money willy-nilly–it is a good metaphor for consumer spending. Even if not consumer spending, it would seem “saving for a rainy day” generally feeds into inflation. For example, say one bumps up automatic retirement fund investments from salary in response to money that the government has pumped into the economy. That money generally goes to businesses that turn around and spend it like drunken sailors (for those of us who lived through the dot-com/telecom bubble, this is still visceral).

So what are the ways in which the government could hand out money and inflation would not result? Naively, it seems like simply giving the money back to the government, by buying government debt would not be inflationary. Suppose I want to do my duty as an American and take the money the government has given me, and deploy it so that I do not cause inflation. What should I do (other than put it under my mattress or dump it in a burn barrel)?

Stymie – …again, how much brake on ‘necessary speculation’ is ‘enough’ brake?

may we all find a better day.

If the stimulus were adding broad productive capacity, i.e. each worker becoming more productive, it would make sense. But if it is just burned, effectively, by buying stuff, then it makes people feel better, but we could just burn the money literally if that made us happy. Same as a drunken sailor—just toss the money in the air if it sparks joy!

Stymie needs to put a brake on being a windbag.