Toronto single-family -19% from Feb 2022 peak, condos hit 3-year low. Vancouver eases further. Calgary condos sag. New highs in some markets.

By Wolf Richter for WOLF STREET.

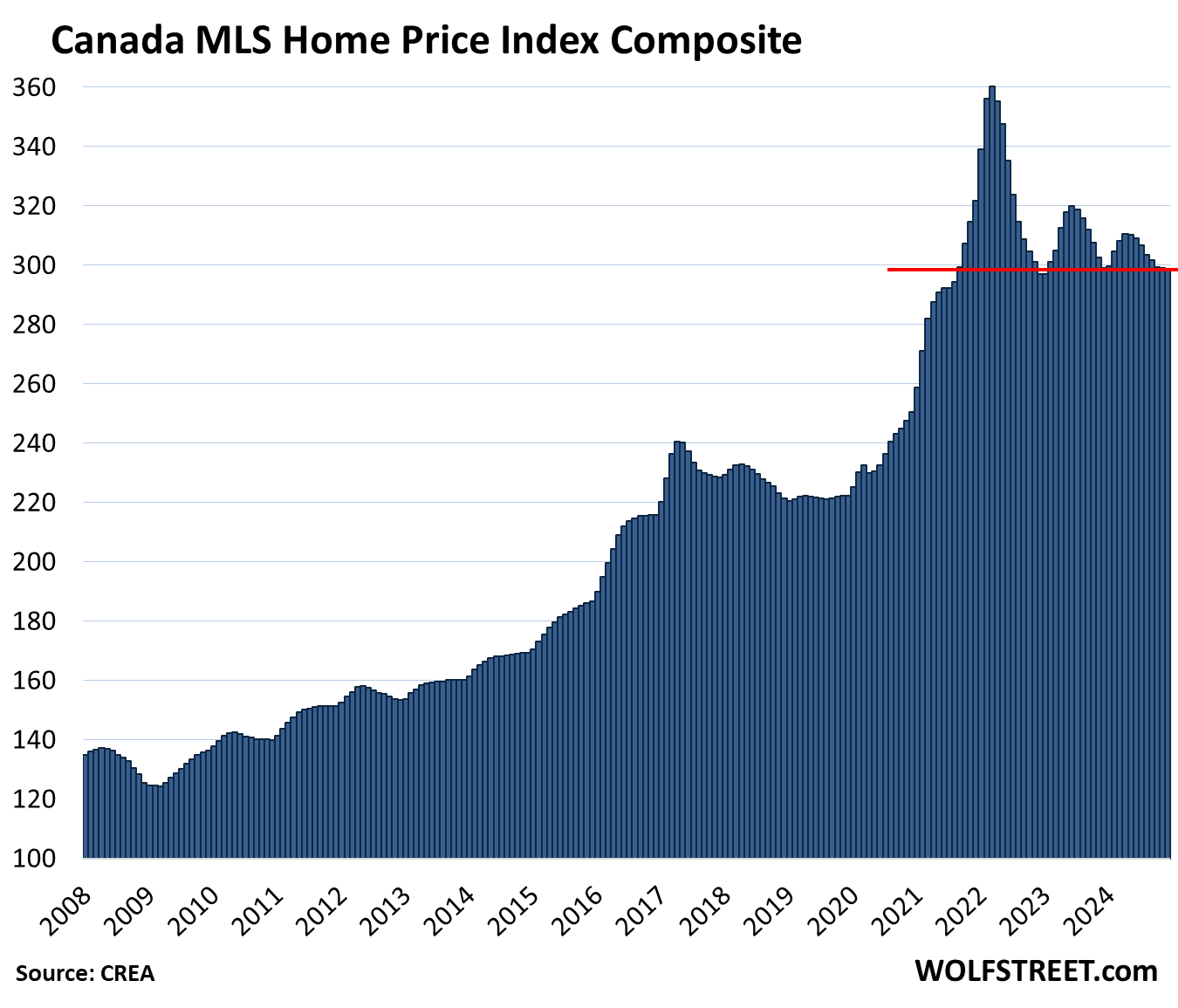

Home prices in Canada dipped by 0.2% in December from November and were down 0.2% year-over-year, the ninth month in a row of year-over-year declines. They were down 17% from the crazy peak in March 2022 and back where they’d first been in September 2021, according to the not seasonally adjusted Canada MLS Home Price Index Composite released by the Canadian Real Estate Association (CREA) today. Condo prices overall were on even shakier ground than single-family dwellings.

Home sales in Canada fell by 5.8% in December from November, seasonally adjusted, after four months of increases, according to data from CREA today. But compared to the frozen volume in December a year ago, home sales were up by 19%.

New listings declined by 1.7% in December from November. But with sales falling faster than new listings, active listings rose by 2.0%, and supply increased to 3.9 months, the highest since September.

Everyone was hoping mortgage rates would plunge after the Bank of Canada’s aggressive rate cuts to 3.25% from 5.0%, starting in June, including two 50-basis-point cuts in October and December. They did drop at first, but then they rose.

As mortgages in Canada come mostly with variable rates or with rates that are fixed for short terms, such as two years or five years, the Canada five-year government bond yield matters a lot to the housing market, and it has risen by 40 basis points since September. This is not what the housing market expected from the two monster rate cuts in October and December.

But every market dances to its own drummer.

When we started this series many years ago to visually document the crazy home price surge in Canada — to accompany our series about the US housing market — we never expected these charts to become this absurd. But this was the era of money-printing and interest rate repression, and absurdities became the norm.

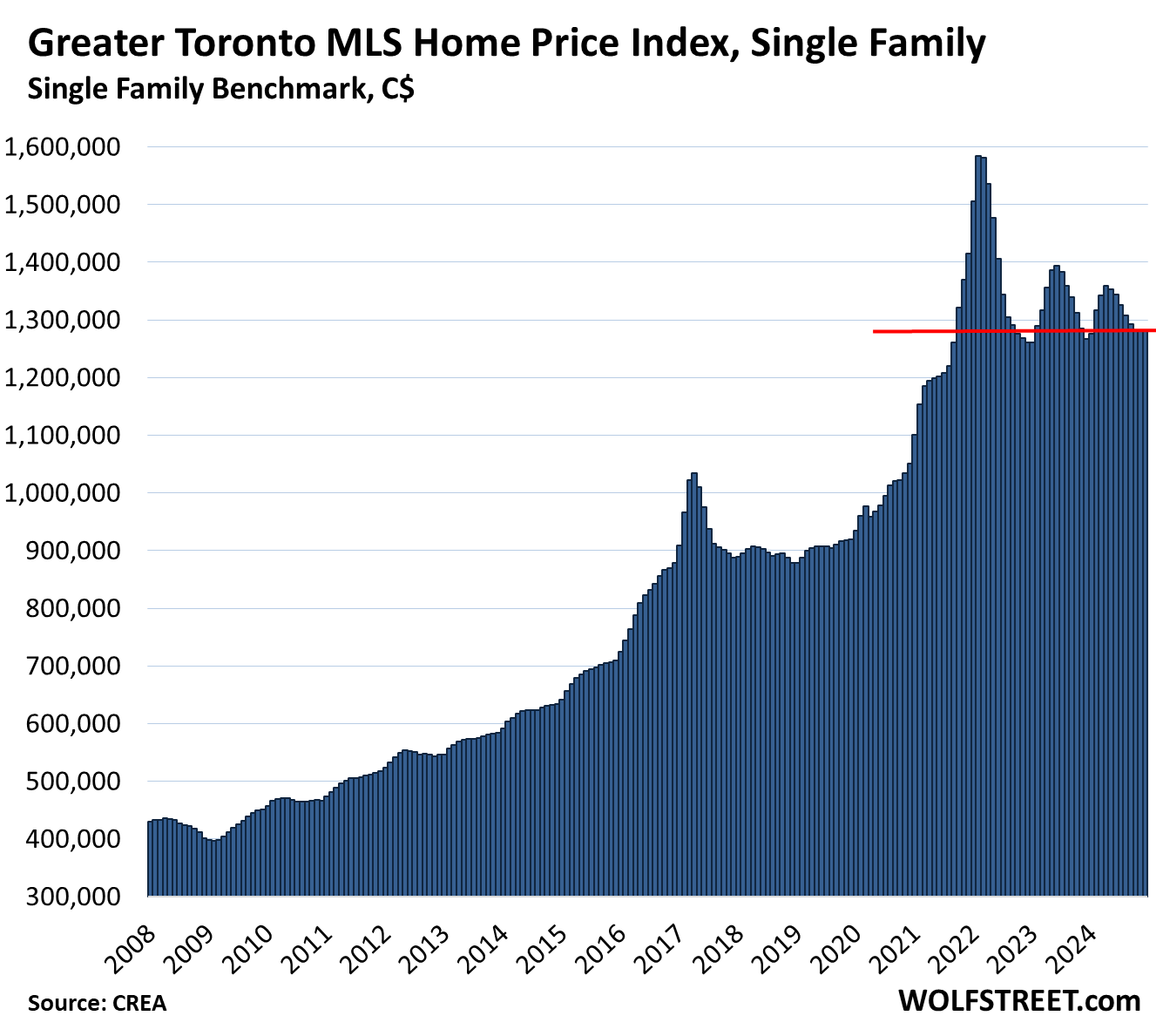

Greater Toronto Area, single-family MLS Home Price Benchmark Index:

- Month-to-month: unchanged, at $1,282,000; where it had first been in October 2021

- From peak in February 2022: -19.1%

- Year-over-year: +1.1%.

The three descending peaks occurred in February 2022, May 2023, and April 2024. The other housing-mania spike occurred in April 2017.

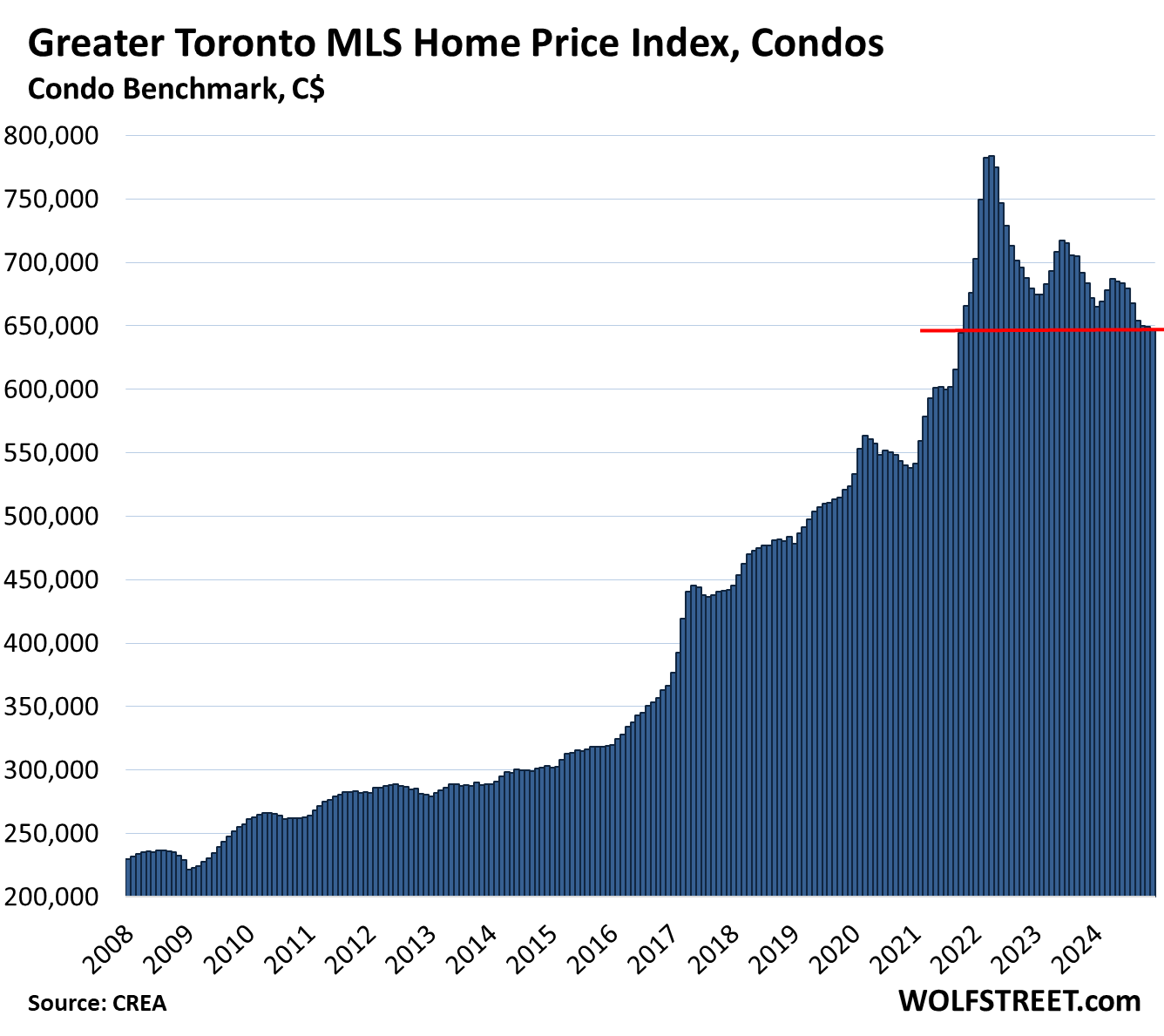

Greater Toronto Area, condo benchmark price:

- Month-to-month: -0.3% to $647,200, lowest since October 2021.

- From peak in April 2022: -17.5%

- Year-over-year: -3.7%, with year-over-year declines in 23 of the past 24 months.

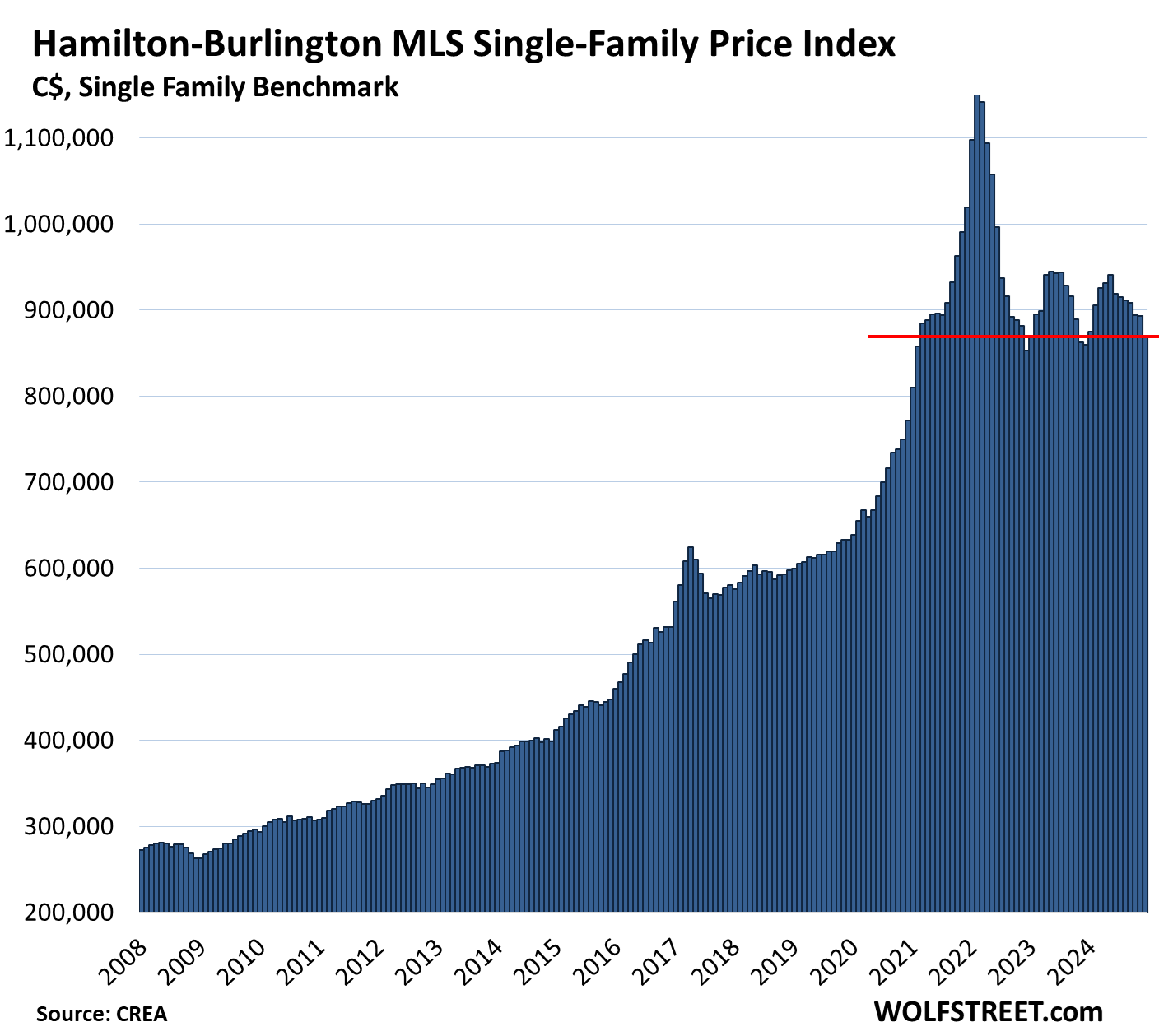

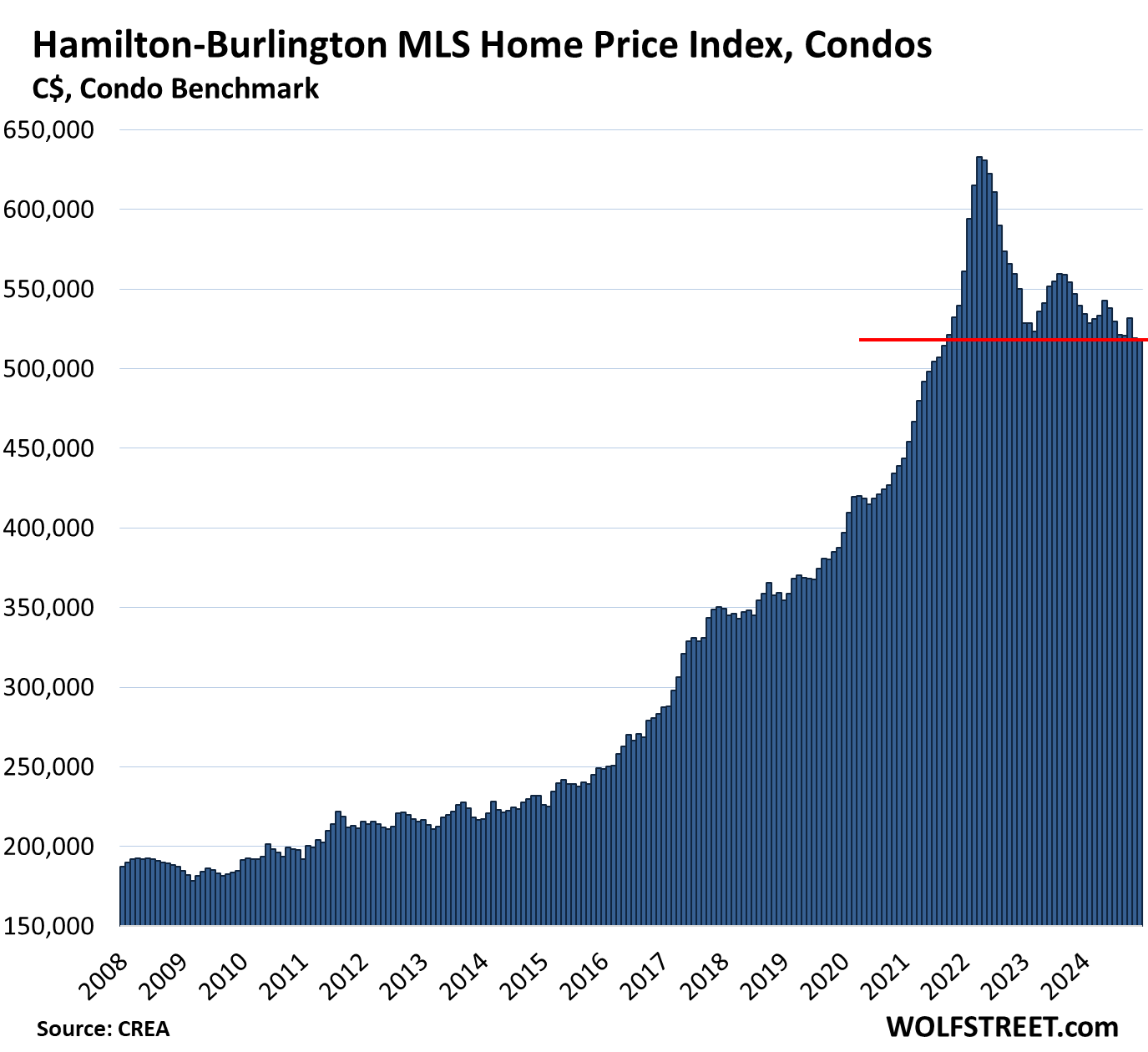

Hamilton-Burlington metro single family benchmark price (part of the “Greater Toronto and Hamilton Area”):

- Month-to-month: -2.7% to $869,100, back to February 2021

- From peak in February 2022: -24.8%

- Year-over-year: +1.1%.

Hamilton-Burlington metro condo benchmark price:

- Month-to-month: -0.3% to $517,700, a new 3-year low, lowest since September 2021.

- From peak in April 2022: -18.2%

- Year-over-year: -4.1%.

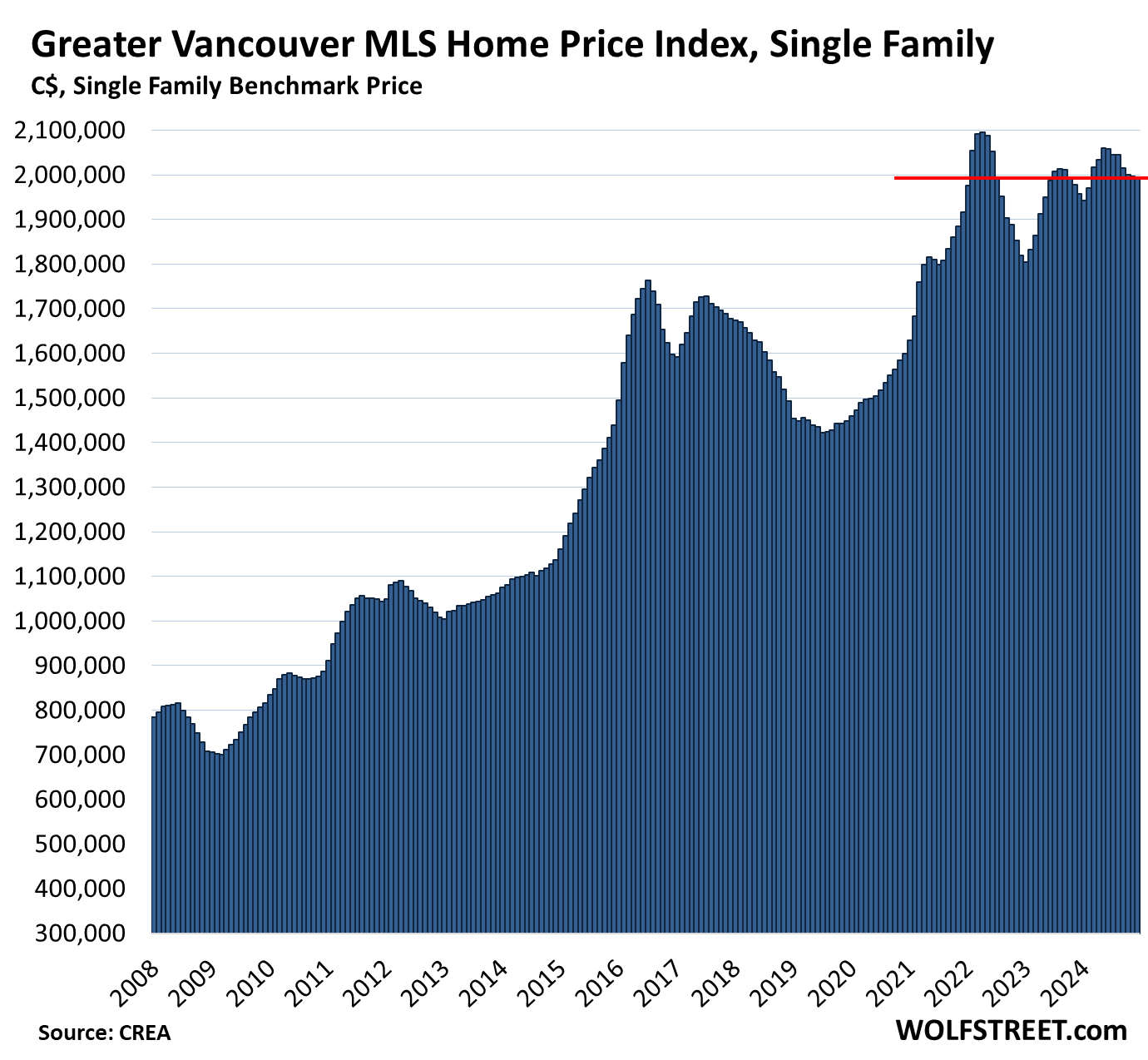

Greater Vancouver single-family benchmark price:

- Month-to-month: -0.1%, at $1,994,600, about where it had been in January 2022.

- From peak in April 2022: -4.8%

- Year-over-year: +1.9%.

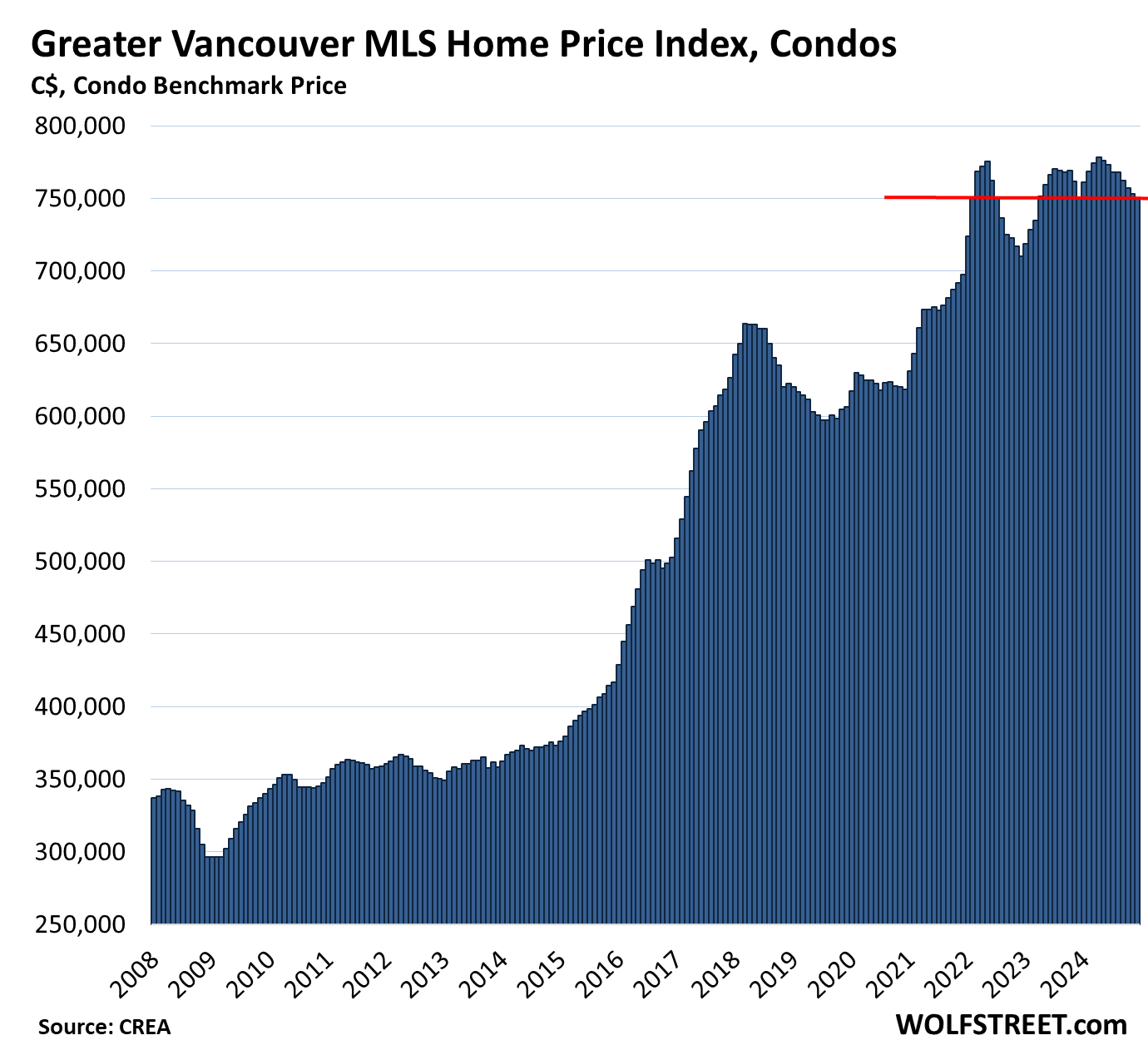

Greater Vancouver condo benchmark price:

- Month-to-month: -0.4%, to $749,900, below February 2022.

- From high in April 2024: -3.6%.

- Year-over-year: -0.1%, sixth year-over-year decline in a row.

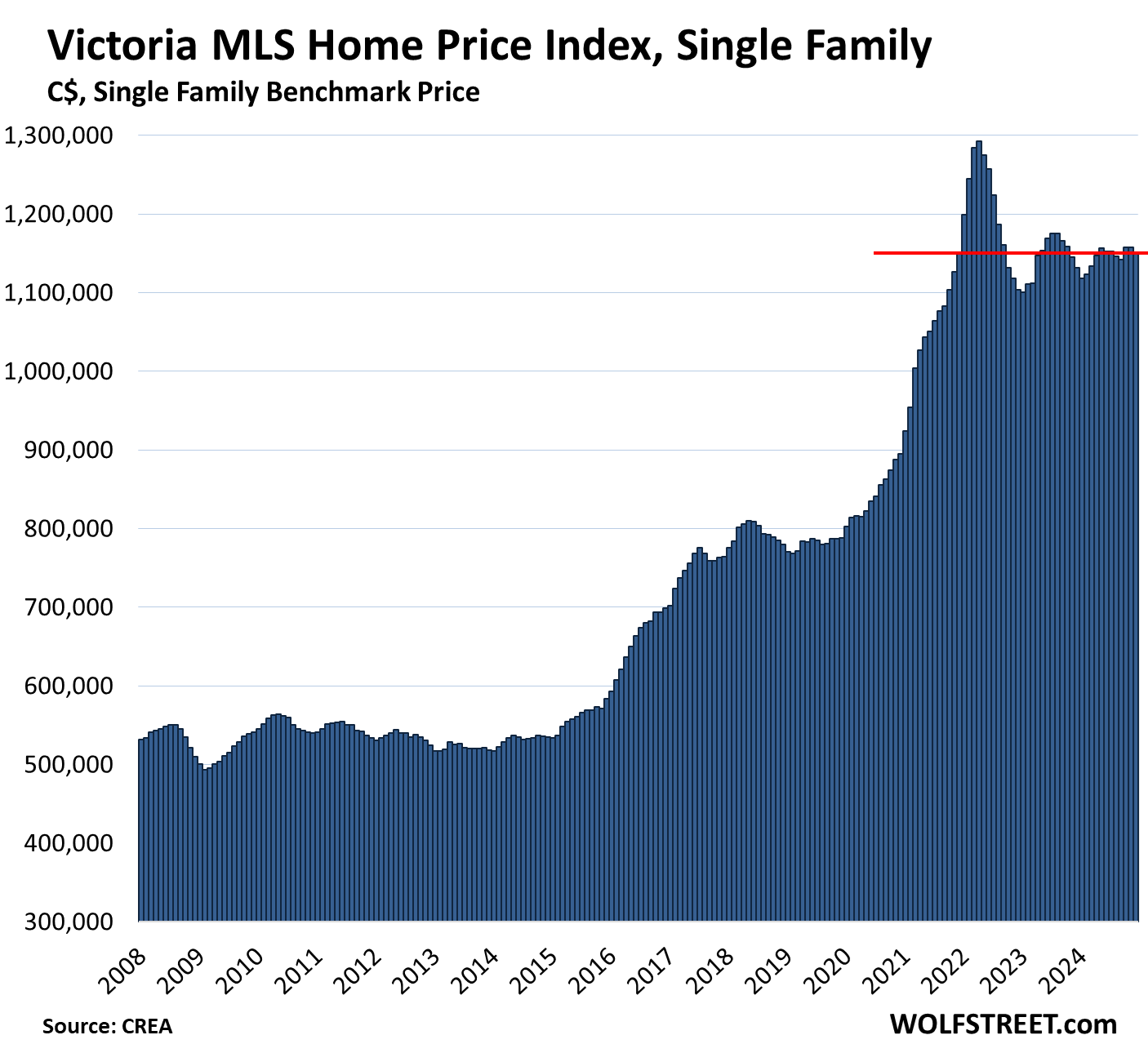

Victoria, single-family benchmark price:

- Month-to-month: 0.5% to at $1,151,200, where it had first been in December 2021

- From peak in April 2022: -10.9%

- Year-over-year: +1.7%.

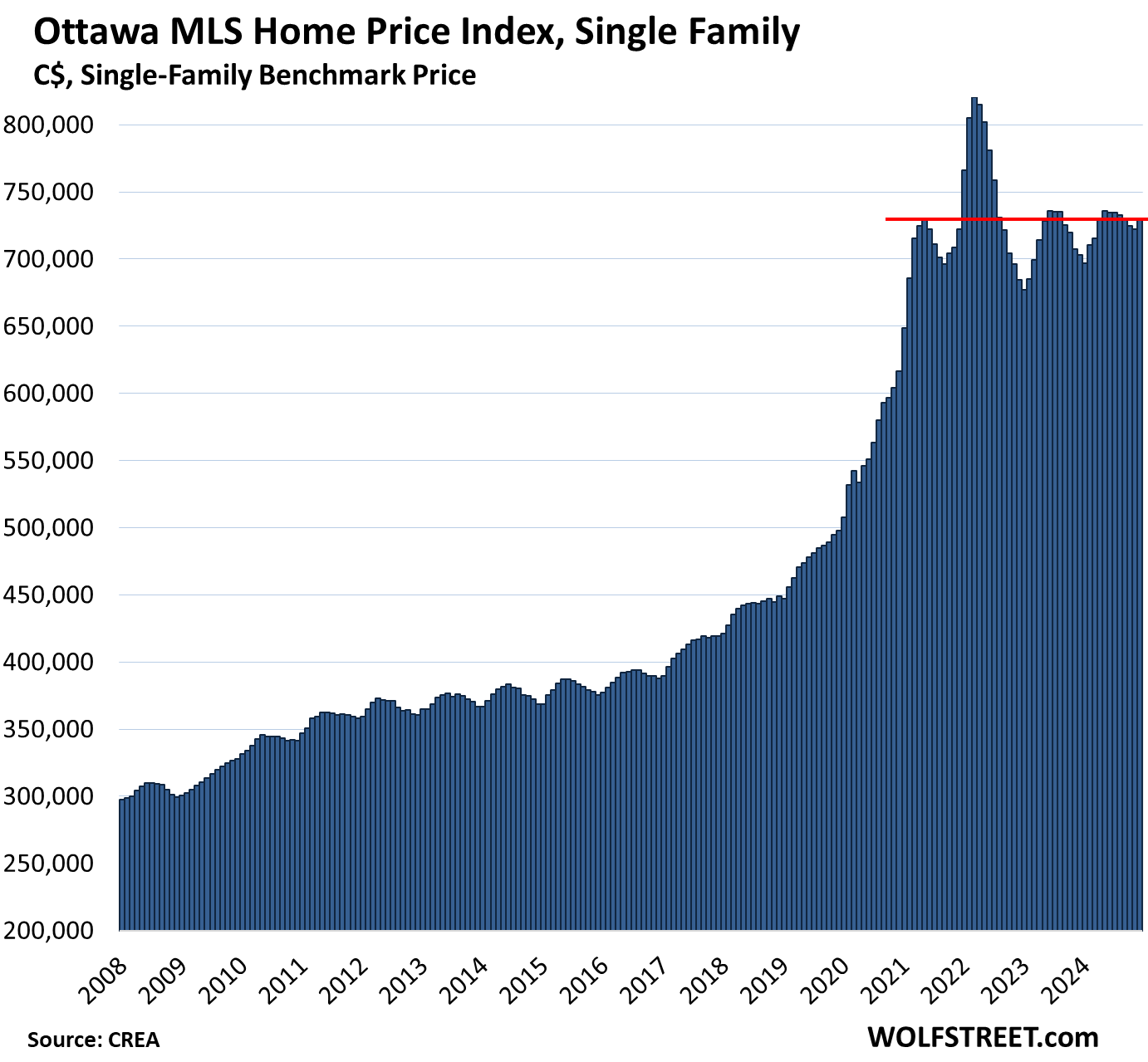

Ottawa, single family benchmark price:

- Month-to-month: +1.0% to $729,300, where it had first been in April 2021

- From peak in March 2022: -11.1%

- Year-over-year: +3.7%.

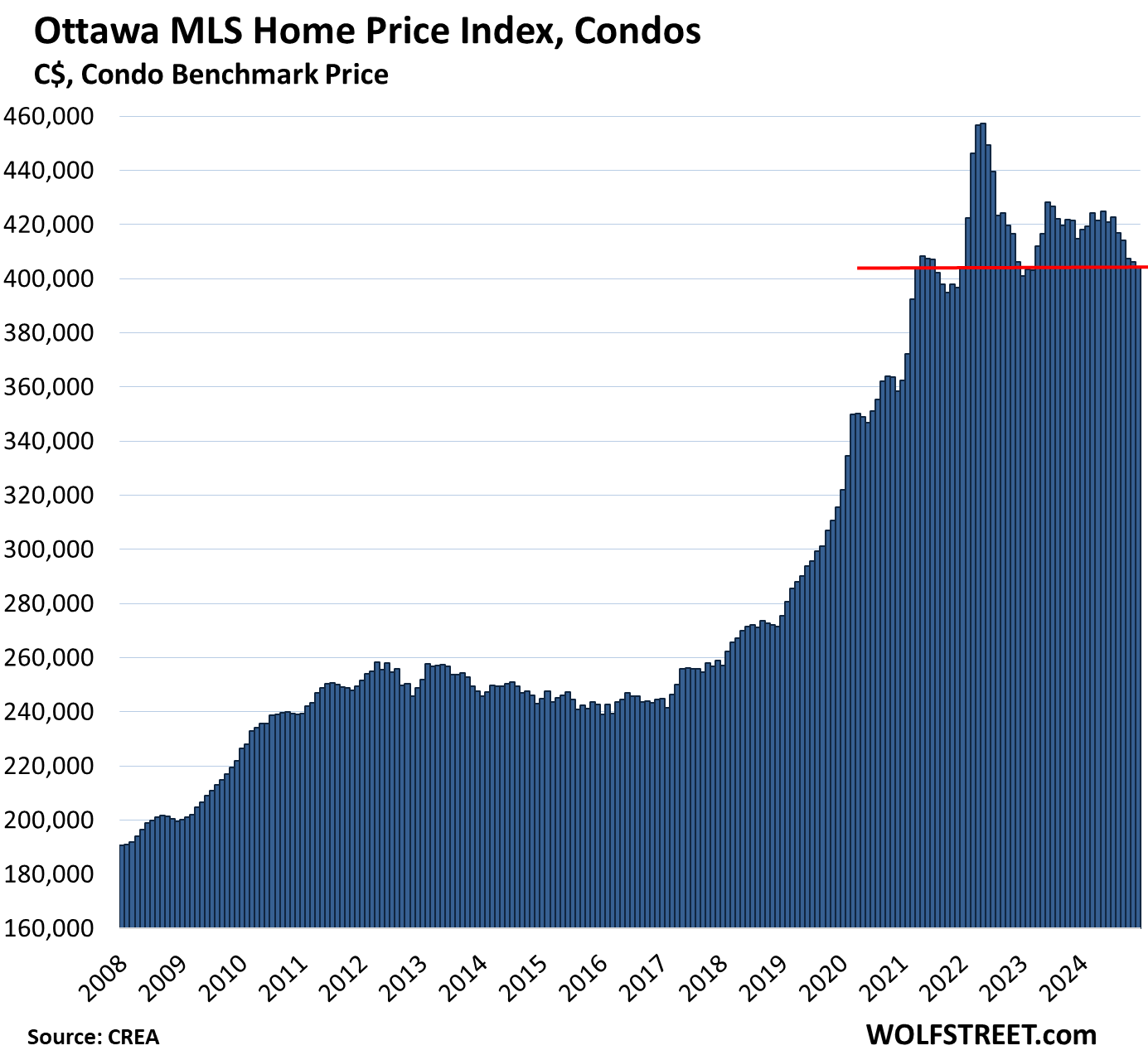

Ottawa, condo benchmark price:

- Month-to-month: -0.4% to $404,400, below April 2021

- From peak in March 2022: -11.5%

- Year-over-year: -2.5%.

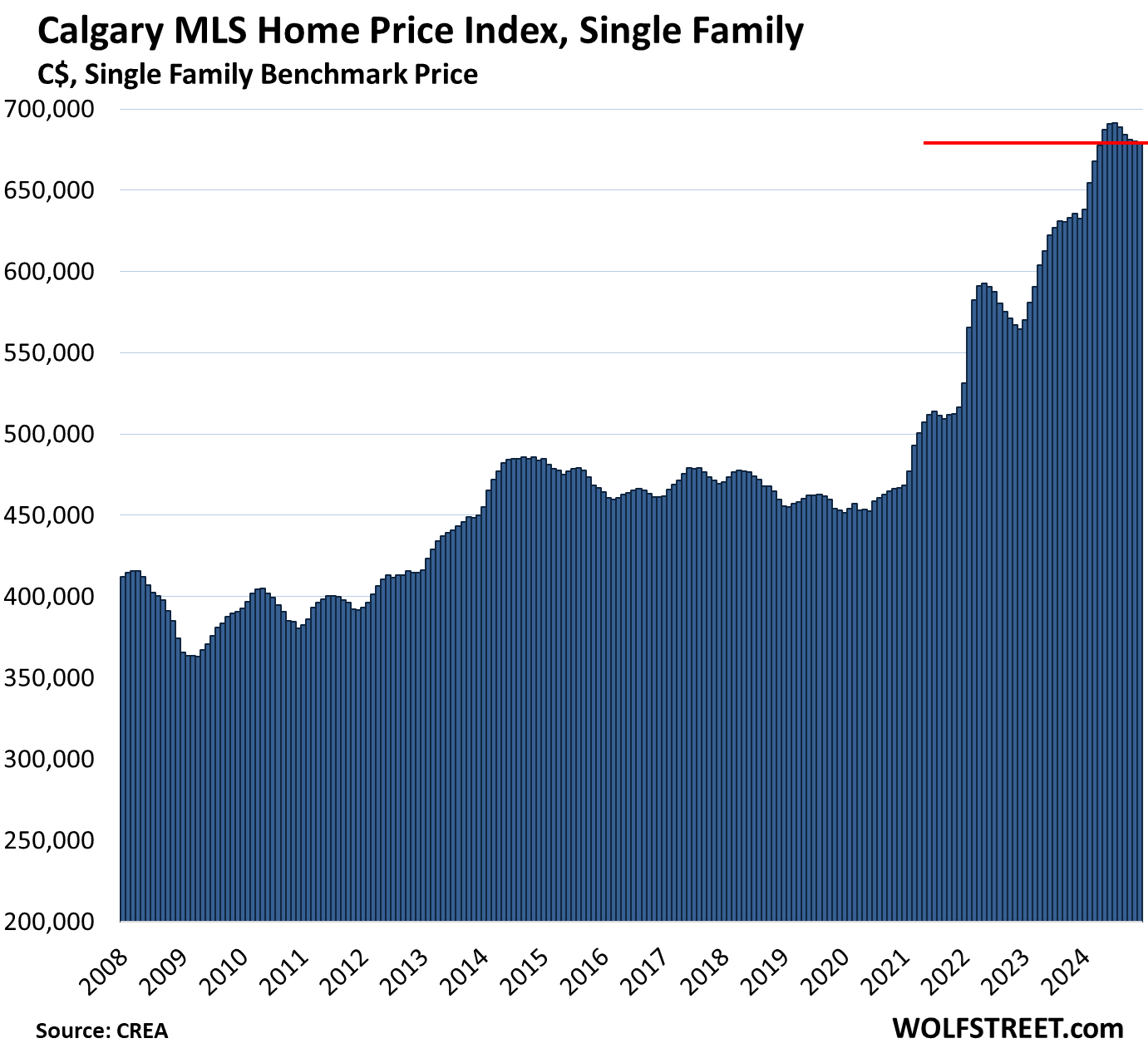

Calgary, single family benchmark price:

- Month-to-month: -0.2%, to $678,900, fifth month-to-month decline after a relentless two-year spike.

- Year-over-year: +7.3%.

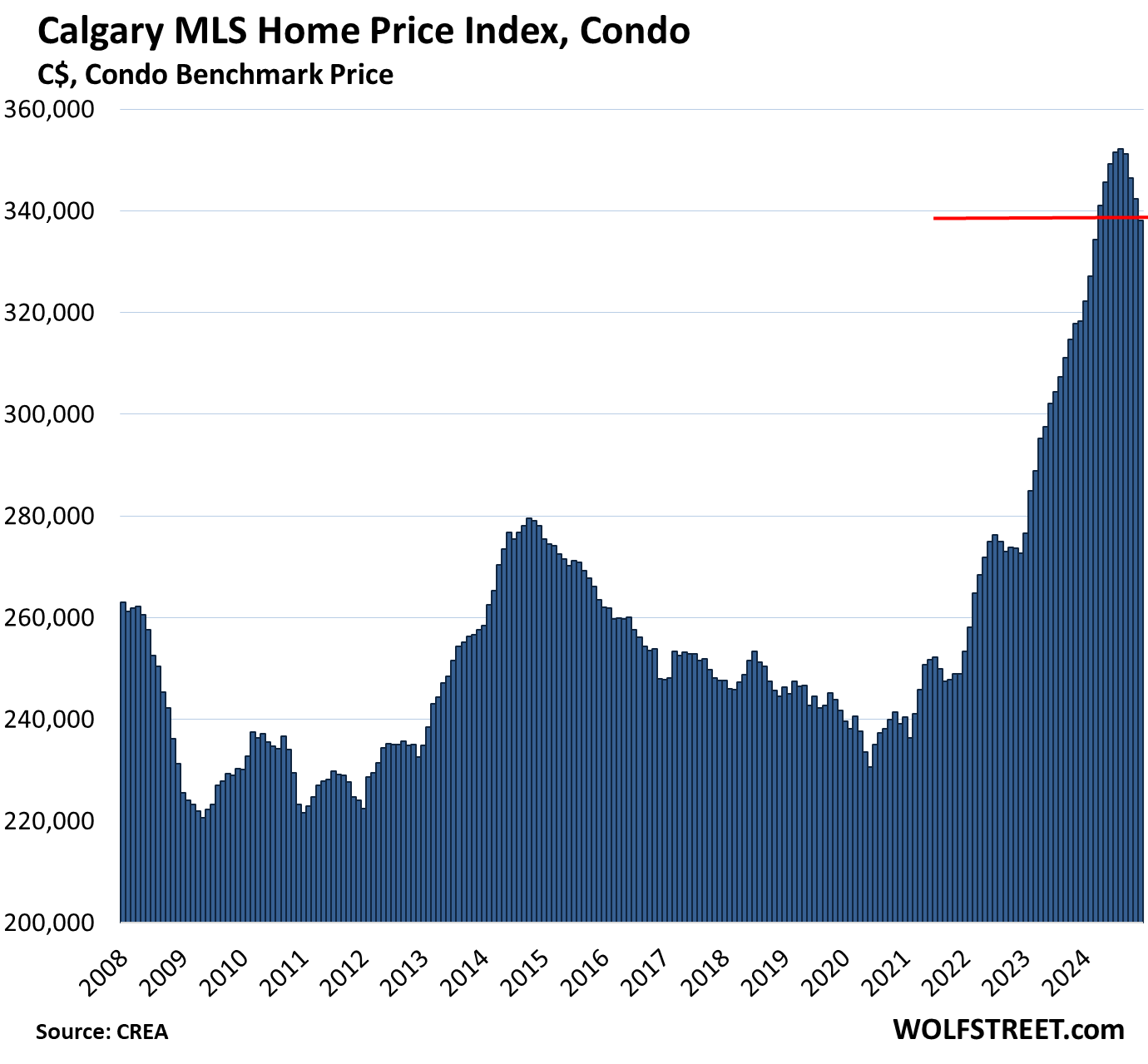

Calgary, condo benchmark price:

- Month-to-month: -1.2%, to $338,100. Fourth month in a row of sharp declines after the gigantic spike.

- From peak in August 2024: -4.0%

- Year-over-year: +6.2%, the lowest year-over-year gain since January 2022.

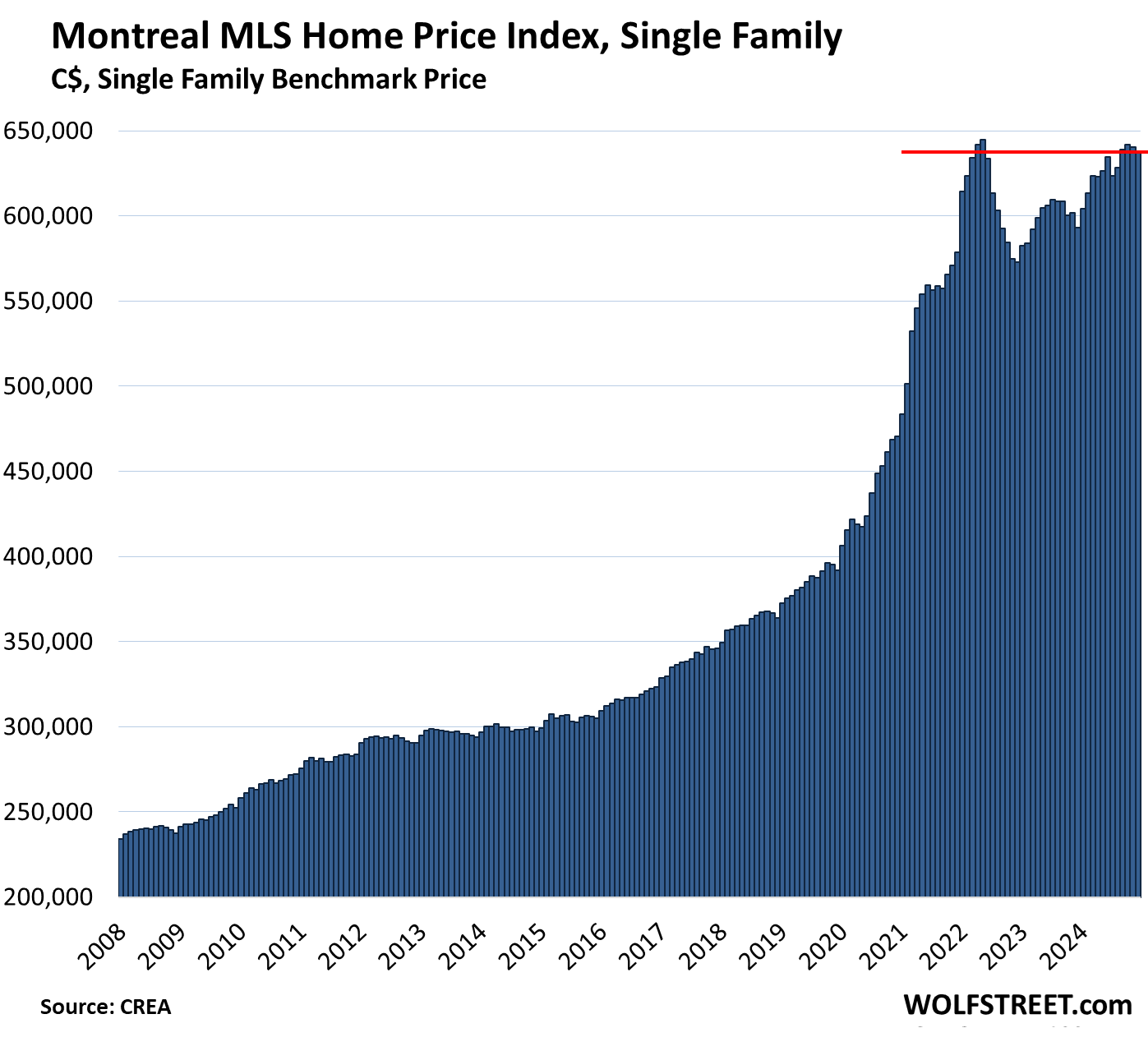

Montreal, single family benchmark price:

- Month-to-month: -0.5%, to $637,400.

- From peak in May 2022: -1.1%

- Year-over-year: +7.5%.

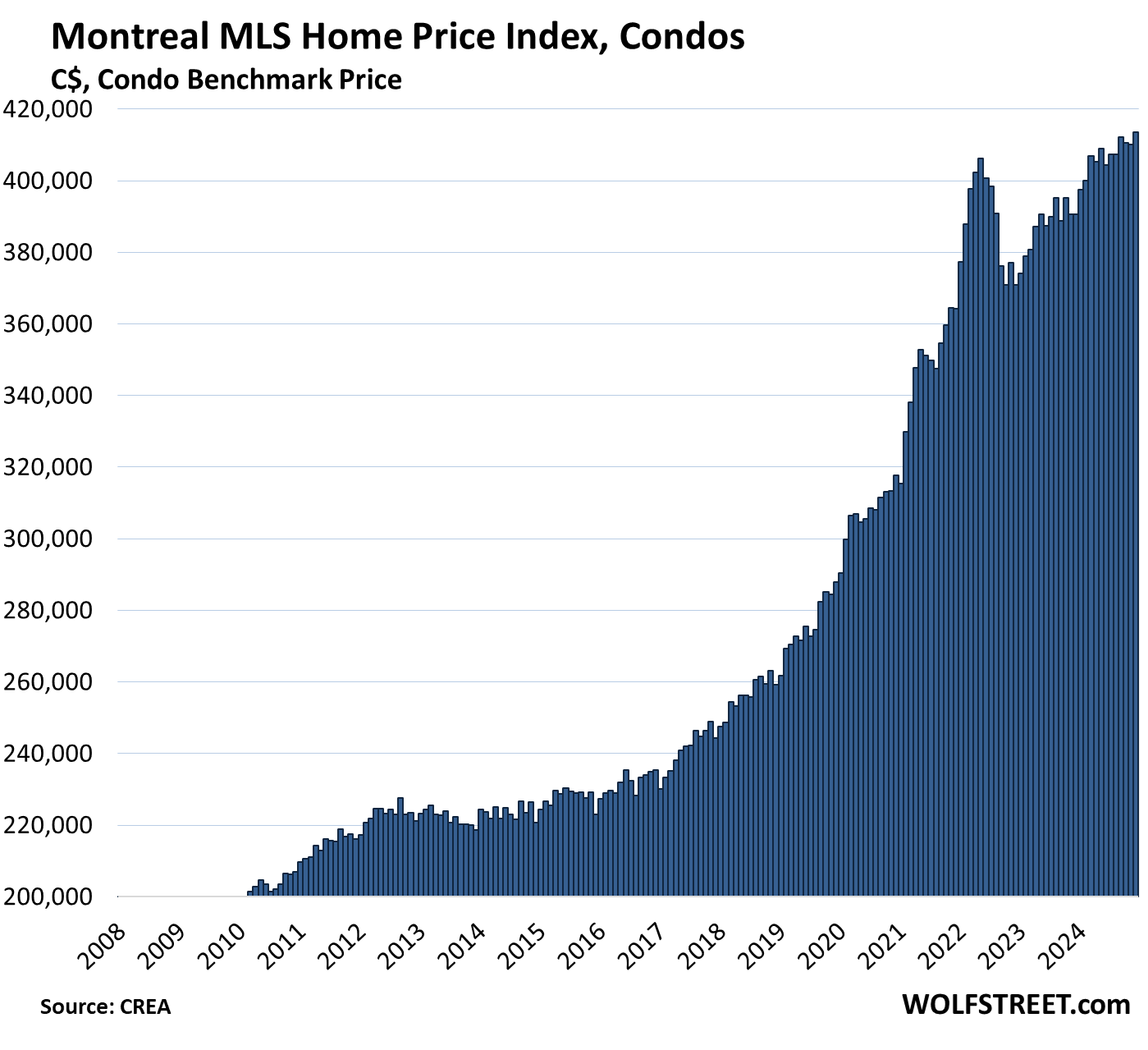

Montreal, condo benchmark price:

- Month-to-month: +0.8%, to $413,600.

- New high

- Year-over-year: +5.9%.

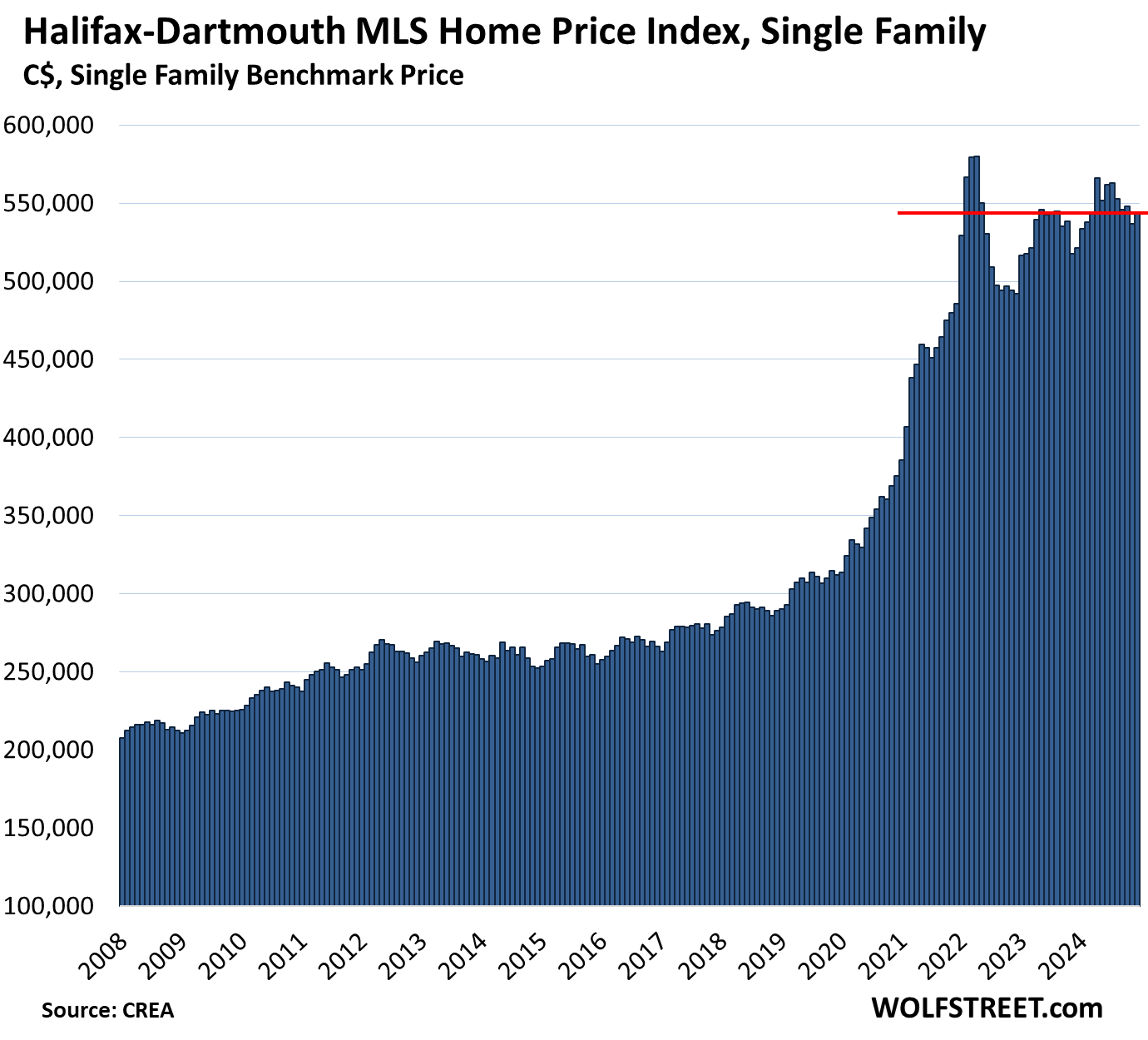

Halifax-Dartmouth, single family benchmark price:

- Month-to-month: +1.2% to $533,500

- From peak in April 2022: -6.3%

- Year-over-year: +4.2%.

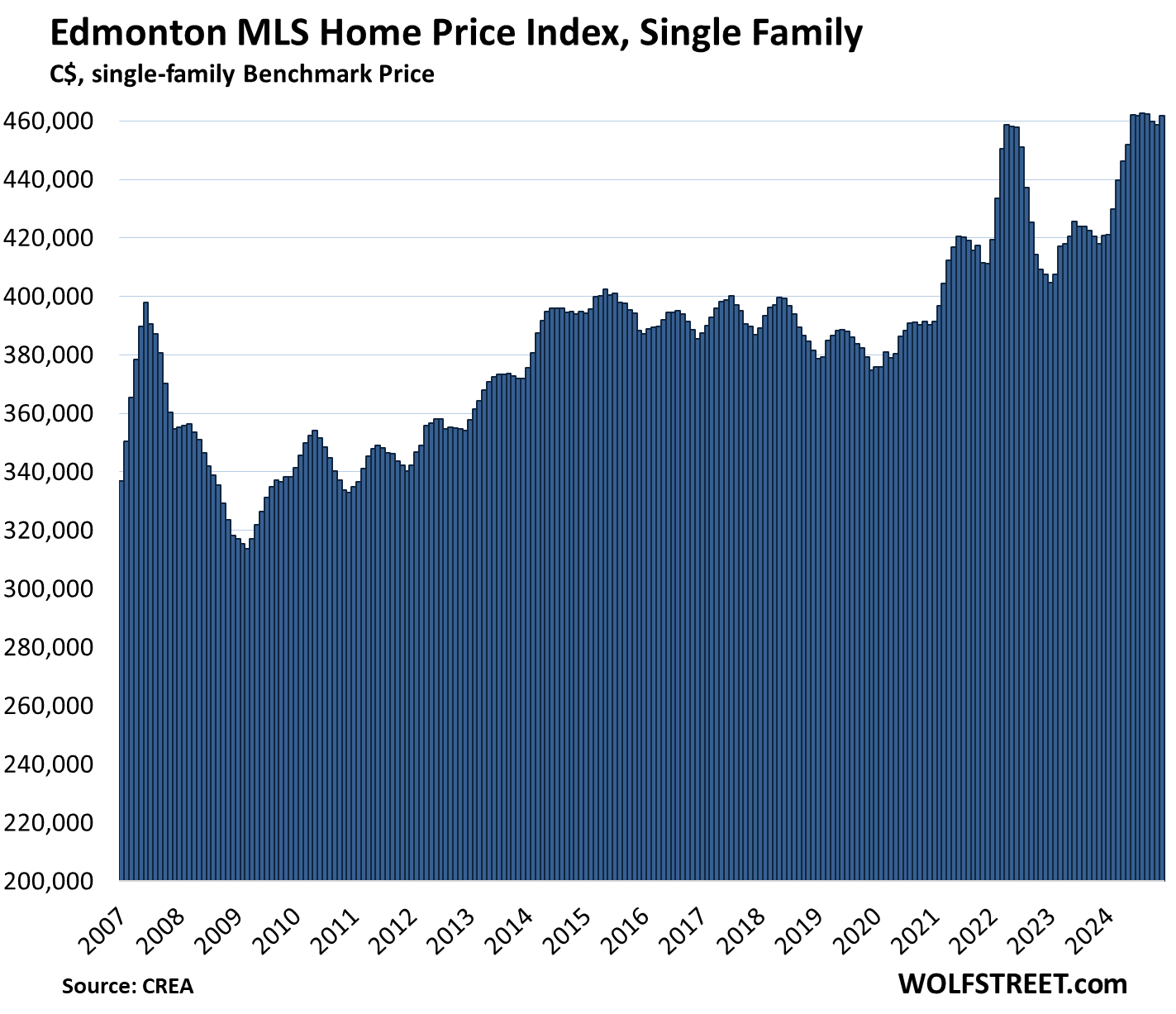

Edmonton, single-family benchmark price:

- Month-to-month: +0.7% to $461,900, roughly unchanged for the past seven months, and down a hair from the all-time high in August 2024.

- Year-over-year: +9.7%

- In the 17 years since the peak of the prior bubble in June 2007, the index is up 16%.

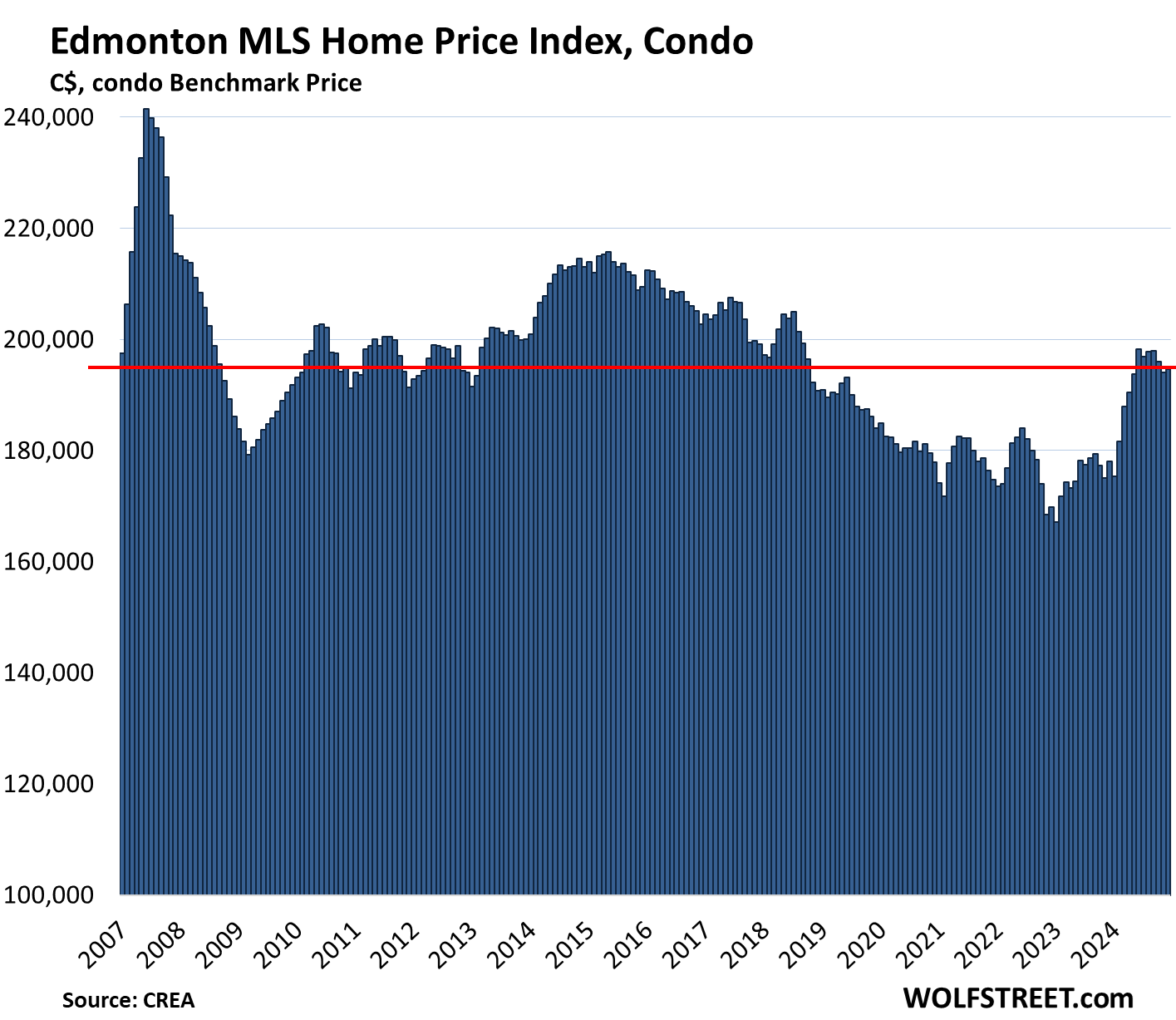

Edmonton, condo benchmark price:

- Month-to-month: +0.3% to $194,700, first seen in 2007.

- From peak in June 2007: -19%

- Year-over-year: +9.4%

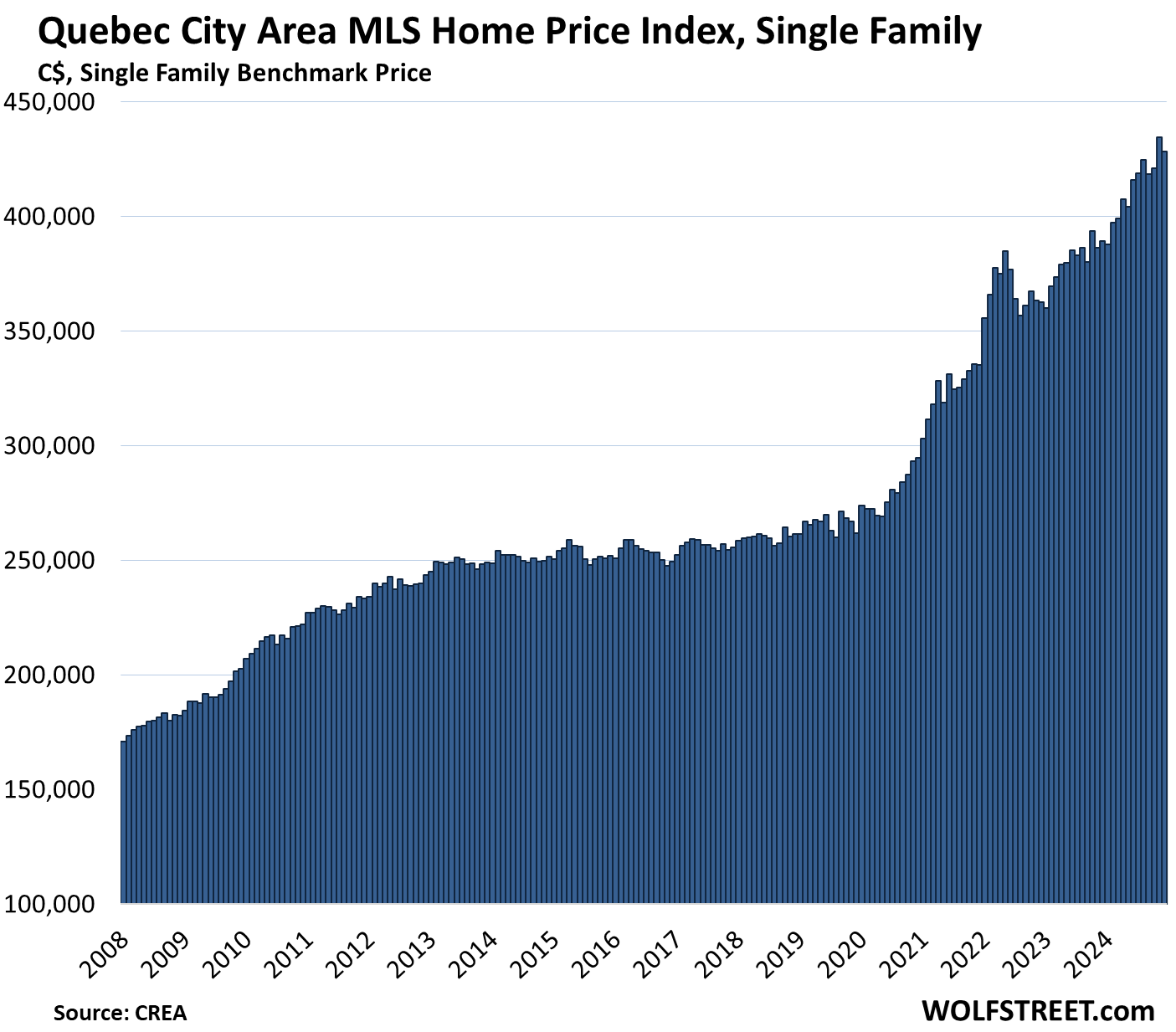

Quebec City Area, single-family benchmark price:

- Month-to-month: -1.4% from the all-time high, to $428,400

- Year-over-year: +10.0%

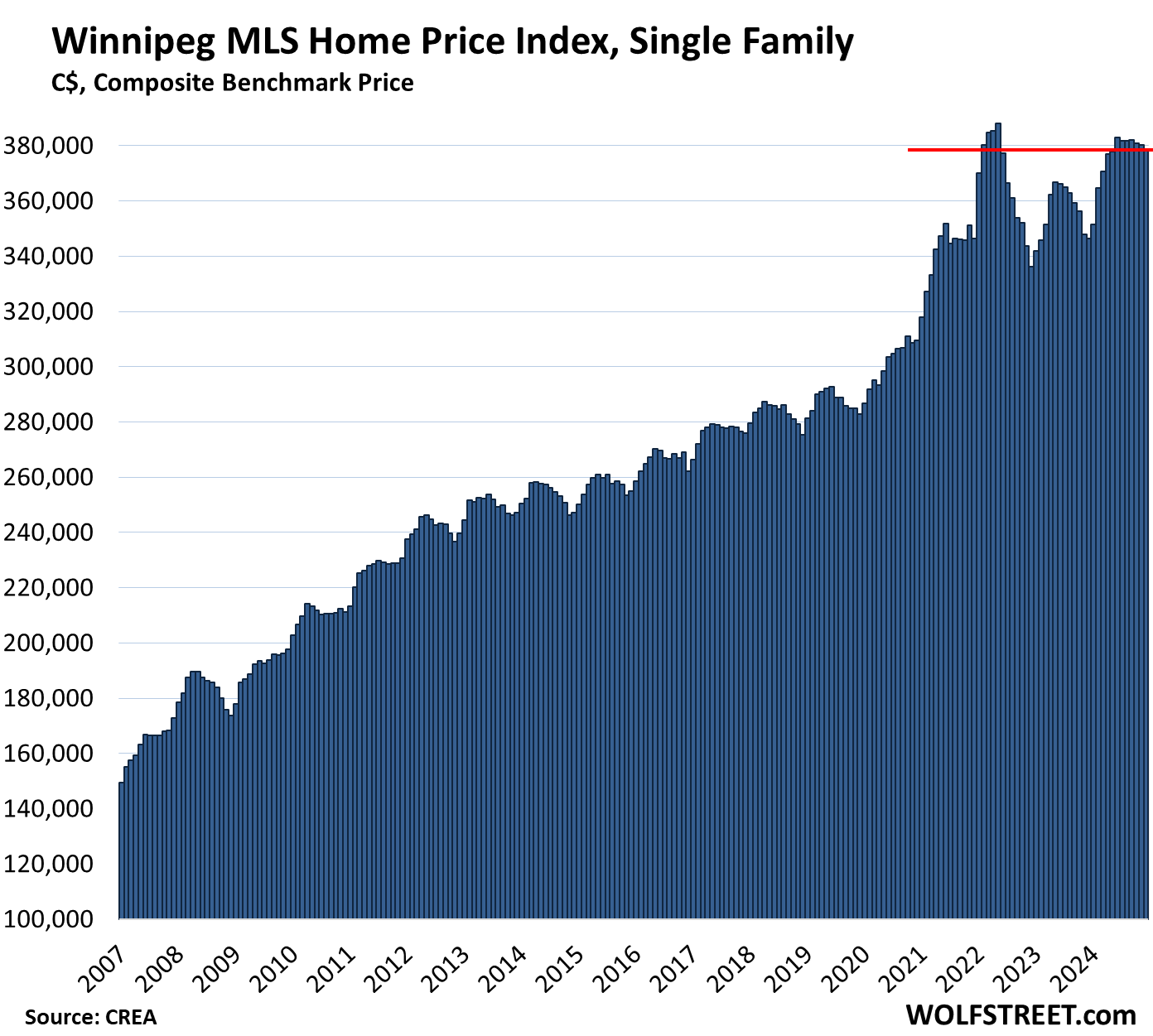

Winnipeg, single-family benchmark price:

- Month-to-month: -0.4% to $378,800

- From peak in May 2022: -2.4%

- Year-over-year: +9.3%

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Unfortunately a 20% drop on a 4x run up in 12 years or so is basically irrelevant.

Amen, amen. I’ve been trying to send out the same message for a while now. It’s like a store jacking up the price 100% on a product and then cutting the price by 25%, to make you think you’re getting a good deal. Except with housing, it’s been a much higher markup.

If a $100 house has a 100% price increase, which is huge even for Canada, it’ll cost $200. If there is a 20% drop, it’ll take it down to $160, and that 20% drop cut the 100% gain down to a 60% gain. A 50% drop wipes out the entire 100% gain. That’s just how the math works.

But the US housing bust lasted about 5 years, so this stuff moves slowly. I understand that crypto mentality has taken over: if the price doesn’t collapse to zero overnight, it’s a nothingburger. But that’s just not how real estate works.

100% agree that RE corrections take time. In Toronto a post WW2 built $350K house in 2008 went to $1.2M or more by 2022. Nearly 4x. That house is now down to $1-$1.1M. Avg. HH income in Toronto is currently $120K. So, 10x price to income. It’s worse elsewhere.

We’re now 2 years into a 20% drop in that market.

I accept slow. But Canada’s RE market has been in an entirely different universe. And has been for a long while. A further 20-30% drop over the next three years wouldn’t return things to rational.

It might just be that Canadian RE has slipped the bonds of gravity, market fundamentals, and all economic and bubble theory.

Good points you bring up, Wolf, however this time, SOMETHING is different. It’s taken way too long for higher interest rates to have any significant effect on home prices. Now, I can’t say what that ‘something’ is, but I have strong suspicions that housing prices are being artificially propped up.

The ‘why’ is also a mystery. Is it because a cratering housing market would expose how fragile this economy is? It’s crazy how many companies are closing stores. Scary too.

Things that defy the laws of physics or economics will eventually come to a reckoning.

We talked about this math some months ago.

“Hey, the value of my house doubled in three years, up 100 percent. I don’t care if it drops 50%.” ‘Except you are right back where you started if it drops 50%.’

I think (my large brain at work) that it’s only a matter of time. After a few years of price drops and still no buyers for the horny home, desperation will set in and at closing time the horny home will leave the bar with whatever is available. So take what’s available now before you find yourself waking up will a walrus.

Referring to Hemingway’s observation of going bankrupt. Slowly first and then all of a sudden. Sentiment just changes all of a sudden, even in hindsight, inexplicably. Humans do not behave like colliding ball bearings, but irrationally.

Wolf,

Perhaps you addressed this in an earlier post (or the data availability hurdles are high) – but only starting the Canadian data in 2008 makes it harder to put Canadian housing inflation in the context of US housing inflation (where I’m pretty sure your graphs start in 2000).

I’m fairly sure that the Canadian RRE mkt was significantly inflating well before 2008, so as insane as the Canadian price inflation has been since 2008 – it likely has been truly lunatic if measured from 2000.

And the crucial story behind these price tracking stories (for the US too!) is the exact nature of the binding constraints on the incremental supply of housing.

Without pervasive, oppressive restrictions on supply you simply wouldn’t see these kinds of rates of return (even with the Speculators’ Crack Cocaine of ZIRP) – additional supply would have long since come into the market (lured by the explosion of prices), causing prices to fall a lot faster than they have.

I’m sure the supply restriction story is a lot harder to tell, but it is the real world factor supporting the price idiocy most, now that ZIRP is no more.

Yup. Insanity unchecked.

And their mortgage rate as of today is around 4.2%, not a crash!

That’s not quite true. If the starting price is 100, then x4, it becomes 400, then -20% you get back to 320. So the total is x3.2.

I recently saw a very interesting video about the 2004 Indian Ocean tsunami that killed almost 228K people. In the vid, a group of elephants became very agitated and broke their chains in order to flee to higher ground – this was before the tsunami happened. Also, amazingly, one father in the video said his son had dreams or premonitions for about a week and had an impending sense of doom. He verbalized it frequently before the tsunami.

It’s interesting how some animals and even a child in that video sense things that most people are oblivious to.

I believe the current real estate market is similar. A disaster is likely to happen. And when it does, many, if not most, will be caught off guard.

Exactly right. You see people walking on the beach and you can see it on the horizon bearing down on them. By the time they start running, it’s too late. A smart homeowner in Canada would get out now and price the house to move.

I live in Northwest Ontario. I did a market appraisal a couple of years ago. While the “value” of my house has tripled in 15 years, it would cost me a lot more than the sale price to rebuild, and I have a home office downtown with ample parking on a fully serviced double lot on the TransCanada Highway. My alternative is to buy rural land and live in a portable home with separate storage buildings. That’s still possible, though I’m 76 years old…. I also won’t have natural gas living out of town. What am I missing?

Mentioned in many news reports these days are stalled condo builds in Vancouver. Unfortunately, in the stampede to home ownership many prospective buyers paid in advance a pre -build price and/or a hefty deposit in order to have a guaranteed unit at a guaranteed price. Yes, the market was that hot and some buyers were that desperate. Now, with higher interest rates, many developers cannot finish their projects and some have even gone bankrupt at various stages of construction.

The buyers have lost their money, at least for the time being. They can’t get their money back and have no home to move in to. No one is rushing to take over the buildings, either. Last week the news featured a developer with three large towers sitting unfinished, and then interviewed buyers who lost their money, at least for now. They are stuck in limbo.

Personal anecdote: From the last housing bubble article that I commented on…..still, not one sale in our rural area. And still, no one has dropped their asking. Yesterday, I received our property tax assessment for 2025. Looks pretty good on paper but we could never sell for the price quoted.

One would think they’d have learned something from the identical housing boom and bust in the US from 2002 – 2010.

Greed, hubris and FOMO apparently trump logic and common sense every time, which is why history both rhymes and repeats

@CCCB people did learn “something from the identical housing boom and bust in the US from 2002 – 2010” (that was more like 2006-2012 in CA). They learned that if you want a house, can afford a house, and are planning to stay in the same area for a long time you should buy it since you need a place to live and you should not care if prices are lower a few years from now. Everyone does not want to own a home, and some people want to buy at the bottom and sell at the top moving every few years, but most people just want to find a home they like and pay off the mortgage before they retire (Google says that 40% of homes are mortgage-free).

IN my hood at least, the cost of buying a home right now Vs renting, renting cost 50% less than owning on monthly basis.

IN this case, it’s a no brainer to not buy and wait up.

Prices have gone up crazy high and are slowly but surely coming down.

Some of my friends have sold their homes for millions, and now renting the same home for 50% or less than owning them.

I have not gone tot hat extreme but always advise people to look at the monthly outlays when buying vs renting.

WSJ: What if the Fed U-Turns and Raises Rates This Year?

How embarrassing would it be for the Federal Reserve to raise rates this year? Could it admit that its aggressive rate reductions last year, including a cut as recently as last month, were a mistake, and put them into reverse?

Investors are starting to think about the idea. While the chance of a hike this year is still put at zero by pricing of fed-funds futures, according to CME Group’s FedWatch, it is a topic of heavy discussion.

This isn’t just a matter of whether the economy stays hot or whether the new Trump administration’s tariff, immigration and tax policies prove inflationary, though both matter. At the heart of it for investors is an important question: Are the barriers to raising rates stiffer than those to cutting? Or put another way, will the Fed need more evidence to hike than it needs to cut?

History shows that the Fed likes to signal big changes far in advance, and takes time to be sure it is right before starting to raise rates.

What is crazy is that around 1980, the Federal debt crossed 1 trillion and now it is over 36 trillion. A cumulative increase of 3500%. Yet the cumulative inflation of CPI since 1980 is 282% during the same time frame. Housing has gone up 650%.

Also, the Fed has added over 6 trillion too.

Amazing how we can print so much debt and yet see so little inflation. Manufacturing and farming efficiencies I guess.

The inflation over time is little if you believe the government inflation data.

I don’t see government controlling deficit and overtime govt debt would be growing more and more.

It’d be interesting how the bond market reacts. So far, as obvious, they have revolted as the longer term yields have gone up a lot despite FED cut 100 bps.

I meant US Government Debt

but debt isn’t printing. they’re two separate things.

Good point. It is all a bit confusing. I should have said creating debt. I guess that since the government borrowed 36 trillion, then there had to be at least 36 trillion in M2 or M3 floating around to give to loan to Government. I am not sure what money supply metric covers this. But somehow at least 36 trillion was printed at some point (US treasury?) to give to loan to government?

I sort of doubt there was a total of 36 trillion in money supply in 1980. Where did the extra 35 trillion come from since 1980 to loan to give to the government. Way above my head.

i admit this confuses me too, but you’re forgetting about the multiplier effect from lending. the fact that there are 32 trillion in government bonds out there (excluding the ones held by the fed) doesn’t mean that there is 32 trillion in money supply out there.

MW: California wildfires could slow the economy and boost inflation — and that’s not even the worst of it, economists say

Now that decades of chaparral and other accumulated dry tinder has hot-burnt to powdery ash, can mudslides be far behind, as in the relatively recent past? Prepare for horrific media photo-journalism of cars and homes entombed in quickset concrete when the next rain events occur.

Seems like infrastructure costs (public, private, quasi) and some municipal financial footings face significant additional pressures.

Soon, LA will see a construction boom as insurance money and Federal Disaster money starts flowing in over the next couple of months. It will probably last for a year. Currently, the local economy will suffer but Billions of construction dollars will be flowing in soon.

People will need new homes, fix damaged homes, new cars, new landscaping, utility companies and the city will need to fix their infrastructure.

And the trades will magically appear to get the building done as well as the simultaneous deportation of many experienced workers plus added on tariffs. (And yes I have been building for almost 1/2 my working life). Design limitations, inspections, red tape permits and approvals…. and debris removal will most likely eat up at least 2 years. What will be the finance rate for new builds? Will finance be available if there is no proper insurance coverage? Only time will tell.

I would guess many folks will pull up stakes and leave. Meanwhile, where do they live?

Lots of flowing dollars will arrive, but it could be a decade or more before the rebuild is close to being finished and completed. It will take years to even get the debris removed safely and where will it be dumped?

Con artists are probably working hard on it right now.

Insurance rates and more fire resistant building codes may dampen enthusiasm to rebuild.

To be honest, prices going flat in nominal terms for a long time wouldn’t be the worst outcome. It will be interesting to see how the decline in population growth affects markets, rents are already falling in most places, which lowers the floor for housing prices. Still lots of pain for people for another 2-3 years as people renew to higher rates, but so far not much overall stress in the market as unemployment remains low and wage gains remain solid.

Given the lower recent exchange rate vs US, I’ve seen people who bought places in the US when the CAD was at par selling their US places now and buying back in Canada, so the fx rate vs USD could lend some support to the market as well.

That happened in California in the 90’s. Houses dropped about 20-30% in real terms; nominal prices were flat. I think you could go to sleep now for the next 5 years and find nominal prices about the same in most USA markets. Dunno about Canada.

But this article shows that even the hottest market e.g. Toronto is down almost 20% from the peak. IN real terms, then it is down quite a lot.

So prices are going down in both nominal and real terms.

Well – if Trump goes ahead with the tariffs we will see what Canada house prices look like in a year or so down the road….oh dear!

I remember complaining in 2003 that house prices were a bit on the high side…

Wolf wrote: “Everyone was hoping mortgage rates would plunge after the Bank of Canada’s aggressive rate cuts to 3.25% from 5.0%, starting in June, including two 50-basis-point cuts in October and December. They did drop at first, but then they rose.”

Gary Stevenson addresses this phenomenon with his “the future of house prices”.

I won’t link to the video. But his explanation rests on (1). Who received or accumulated most of the Covid monies, and (2) What do these people tend to do when they have a huge windfall of money?

1) rich people

2) buy assets

Vancouver.. $2,000,000 (MLS) There be gold in those thar Hills.

Well at least for those who have a home, the rest, well, Keep Saving on your minimum wage.

I have a question, who, other than those who are upgrading can afford a $400,000 deposit and (5% on $1.6 million) around $8,000/ month + living expenses and heating.

The seeds of destruction are always in the ripe fruit

@Thunderdownunder The number of people who “saved from a minimum wage job” to buy a home in the US and Canada over the last 50 years could probably fit in my SUV. Most “homeowners” as adults have always made more than the “minimum” wage (if you include tips) and of those that did start at a “minimum” wage few were still making that “minimum after a year. As for your question the people buying a “first” home for $2mm and making a $400K down payment can afford it in many ways from inheritance from grandparent, gift from parents, company going public, lawsuit win, patent sale, lottery win or good/lucky investing (they guys that put a lot of cash into Bitcoin, Tesla or Nvidia in the early days are often paying cash for homes). I live just south of SF in a town with a “median” home price of ~$6mm (up from ~$60K in 1960), the (formerly “middle class”) town next door where I grew up has a “median” home price of just under $3mm (up from ~$22K in 1960 when my parents paid a little above “median” to get west of El Caminio and the RR tracks). Of the young people in my area I hear about buying $2-$4mm homes most seem to have done well in tech or have rich parents (that want the grandkids nearby – I just heard of some parents that sold their beach house in Marin for $6mm and gave the kids $2mm each)

Buying price is one component. Cost of ownership is another high cost.

Sure, buyers ( no choice often), or speculators (legal, some not legal ( read Willful Blindness) and unregulated), are a root cause, as final act of setting a price. But the political, RE & development/construction industries, banking & CBs are hugely culpable, for setting the conditions of this housing mess.

Identifying the culprits is a hope, that better regulation and leadership might occur. As is, it’s a huge fiduciary fail.

The best fix, is when buyers find their hammers. Bring on the very low offers, and hammer away.

As a Canadian, there are only 2 things that will drop the housing market here.

1. Boomers slowly dropping off over the next 15 years.

2. A fairly major rise in professional unemployment.

Nothing else

What triggered the Canadian housing bust in the 1980s? It lasted something like a decade, maybe longer. I don’t think any of these two conditions existed back then.

Unemployment and underemployment definitely were factors in the 1989-96 housing correction in Canada. High interest rates triggered the first downward leg in house prices in 1990. Unemployment followed in 1991, and remained an issue until 1997.

I believe the answer to your question “What triggered the Canadian housing bust in the 1980s?” is, in chronological order:

1. a massive Canadian housing bubble occurring in the late 1970’s to early 1980’s, initiated by inflation and changes to Canadian income tax in 1972 that imposed capital gains tax on most assets other than “principal residence”, thereby creating a privileged asset class, with results obvious today,

2. Mr. Volcker’s raising of interest rates, resulting in double- digit mortgage rates in Canada, and:

3. as per Danno: a major rise in unemployment; in British Columbia, the worst recession since the 1930’s.

Many “Mom and pop landlords” were buying family homes with an intention to rent it out to no less than a dozen international students for at least C$1,000 a head. Living standards were eroded big time with this housing bubble.

A shared mattress still goes for at least C$600 a month in the GTA.

Some mom and pop landlords, but many more specs who don’t themselves occupy the property. Neighbors in many neighborhoods are up in arms. Of course, the GTA recently implemented bylaws effectively eliminating zoning of single-family homes.

The ‘international student’ racket bubble may have popped recently, and the both the big and marginal ‘colleges’ fed by agencies overseas are closing up shop or reducing their facilities and faculties accordingly.

The government just noticed there was an extra 5 million population increase (even net of the ones who illegally migrate to the States) with no accommodation which normally occurs during natural growth.

The problem is most of the international students come to Canada with a donut hole in their pocket. Of the other immigrants coming from India or Pakistan who aren’t international students most purport to be either a doctor or a lawyer to improve their chances of getting to Canada and when they get here the same donut hole in their pocket.

Seriously, for real… a SHARED mattress? C$600/mo ?!

Trump may have many goals, but getting re-elected is not one of them.

It is not native Canadians (or Mom & Pop) doing this it is the 1st/2nd generation immigrants that are doing it to their own people. They know that they can tolerate cramped crappy living conditions. The real failure is on the cities (like Brampton) not fining these people as they are all fire hazards.

The globe and mail.

Bank of Canada to end quantitative tightening within months, turning page on pandemic bond market policy.

In a speech in Toronto, Bank of Canada deputy governor Toni Gravelle said the central bank plans to wind down its quantitative tightening (QT) program in the first half of this year, at which point it will once again start purchasing assets to stabilize the size of its balance sheet.

Mr. Gravelle also laid out how the bank intends to begin purchasing assets later this year. It will start by buying short-term assets, including Treasury bills, in primary government auctions, as it did before the pandemic. Toward the end of 2026, it will begin buying government bonds in the secondary market – that is from investors, rather than straight from the government.

“I want to emphasize that we will not be buying assets on an active basis to stimulate the economy like we did during the pandemic when we were doing QE. Our normal asset purchases before the pandemic were not QE. And our normal asset purchases after QT ends will not be QE either,” he said.

Going forward, the bank will be operating with a larger balance sheet than before the pandemic, with significantly more reserves – which commercial banks use to borrow and lend money among themselves on an overnight basis – in the financial system.

Members of the central bank’s governing council have suggested they’re not keen to use QE in the future, given the hit to the bank’s finances and credibility. The bank has been conducting a postmortem on its pandemic response, which will be published on Friday.

I told you almost a year ago. I estimated back then that the big bond roll-off in September 2025 would breach the QT limit and that QT would end then. What they announced yesterday was a new estimate for the range of reserves, up from a bit from their prior estimate, which moved up the end of QT to June from September.

https://wolfstreet.com/2024/04/07/bank-of-canada-balance-sheet-qt-sheds-64-of-pandemic-qe-assets-indicates-qt-might-end-in-september-2025/

The BOC has been much more aggressive in its QT, it started long before the Fed and other central banks and it went a lot faster.

So far, they have shed 65% of the assets they had added during the pandemic.

👍

What happened was Ponzi Scheme Speculative Housing Bubble. Over the past decade, Investors of all types could not resist easy money and with very low interest rates and very little oversight so they went all in. As a result, mostly overpriced Condos and Townhouses have been built. The Investor would qualify for the mortage a couple of years ago, sometimes with the help of Brokers that submitted fraudulant income statements. They had no intention to live in the unit, but rather to sell before completion. This is called Pre-Construction Sales where they sold it to another greater fool for over a hundred thousand dollars profit, easy money. Until the Peak in 2022, now thousands of projects are coming to completion. The Invester promised to pay the builder 20% more than the unit is worth today, and the rates have gone up AND there are no buyers. They will not be able to close with the bank and likely will loose their deposits. The builder will legally sue for the difference in value that it eventually sells and what the Investor promised to pay. Also, even if you can get approved for the mortage, you can no longer collect enough rent to cover it. Canadians put all their eggs in the Housing Bubble Basket selling over priced houses to one another. The GDP depends greatly on the housing industry. It’s a very terrible situation and obviously unsustainable. Responsible people who aren’t the gambling type as well as young people have been priced out of this market years ago. Of coarse, this is the simplified version of the events that transpired. Basically, everyone blaming Immigrants. SAD

I find it a bit disturbing that our federal government has been desperately trying to salvage their popularity in the form of intervening in the real estate market (FHSA, CMHC increase, mortgage bond purchases, CMHC backed favorable loans to developers, etc.) – not wanting prices to have too severe of a correction and a slowdown due to less starts (construction sector job losses) at the cost of younger generations and new (or soon to be new) Canadians. I believe stats Canada has just reported that the bottom 3 quintiles (1% to 60%) have negative net worth growth in the last quarter.

One last thing, I wonder how much Toronto’s mayor Chow property tax increases (this year is 7% – I think the previous 2 years were 7% and 9.5%) are putting downward pressure on housing prices??? Can’t help but wonder how much the federal government is kicking themselves in the butt – funding Paul Kershaw / generation Squeeze – to research “tax fairness” (with the accompanied narrative- “you’ve been screwed by boomers”) with today’s unaffordable price levels – the liberals (and Kershaw) couldn’t sell it to enough of the public though. Standing on the sidelines – staring at overly inflated prices and knowing they could be gaining even more revenue from it.