Existing home sales rise from multi-decade rock-bottom, still -34% from 2021, -22% from 2019. Supply highest for November since 2018, days on market highest since 2019.

By Wolf Richter for WOLF STREET.

Sales of existing single-family houses, townhouses, condos, and co-ops that closed in November fell to 315,000 homes, according to data from the National Association of Realtors today. During the holiday period – from November through January – sales always drop from the prior months and reach the yearly low in January, and inventories drop too as people pull their homes off the market over the holidays.

Year-over-year, sales rose by 5.0% not seasonally adjusted, from the collapsed sales that closed in November last year after mortgage rates had briefly hit 8%. But compared to November 2021, sales were down by 37%. That’s the extent of demand destruction brought about by too-high prices.

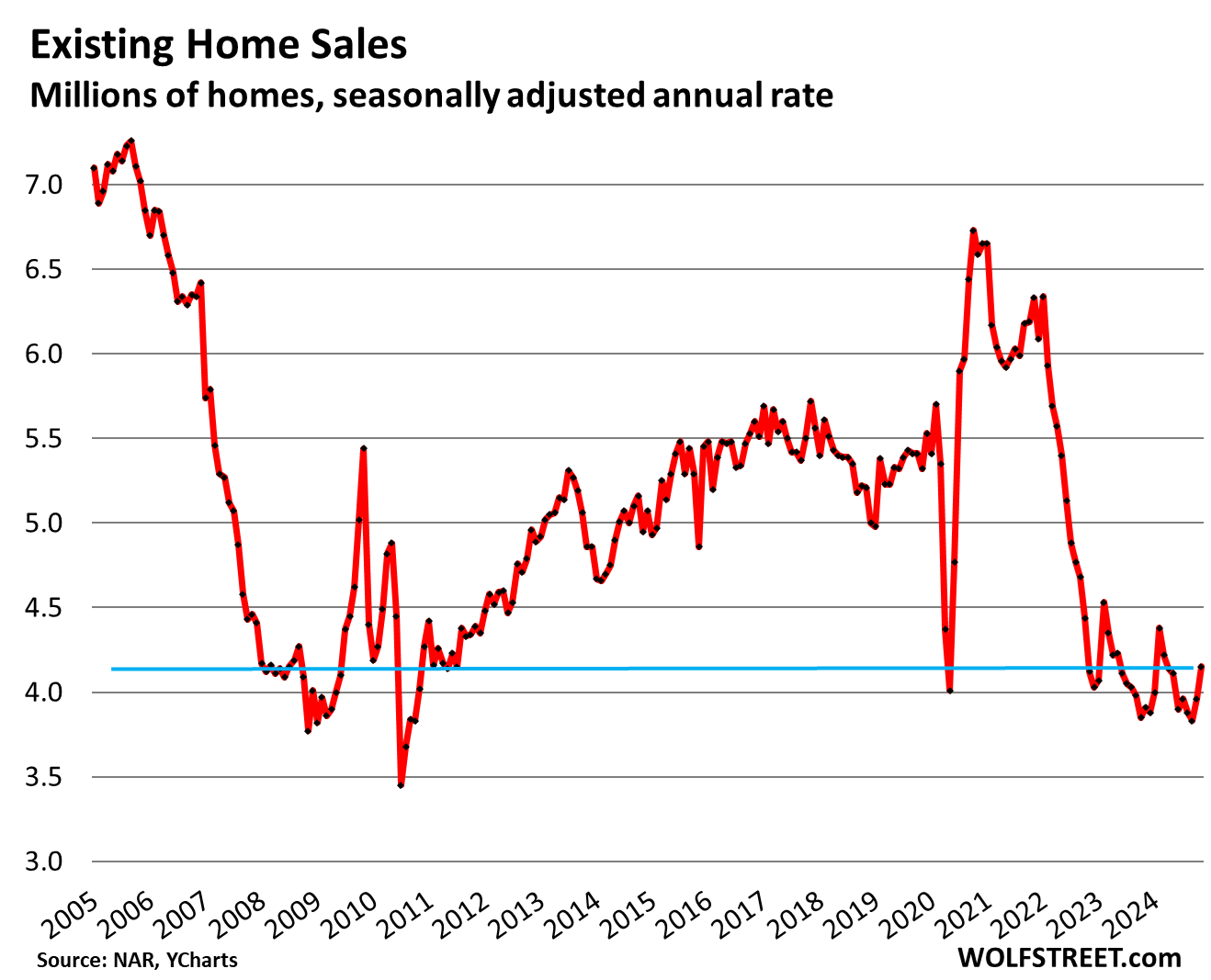

The seasonally adjusted annual rate of sales, which attempts to iron out the seasonal decline over the holidays and multiplies this out to a 12-month period, rose by 4.8% in November from October to an annual rate of 4.15 million homes. This was still down by 34% from the same period in 2021 and by 22% from 2019, wobbling along the bottom for two years (historic data via YCharts):

Buyers’ strike leads to lowest annual sales since 1995.

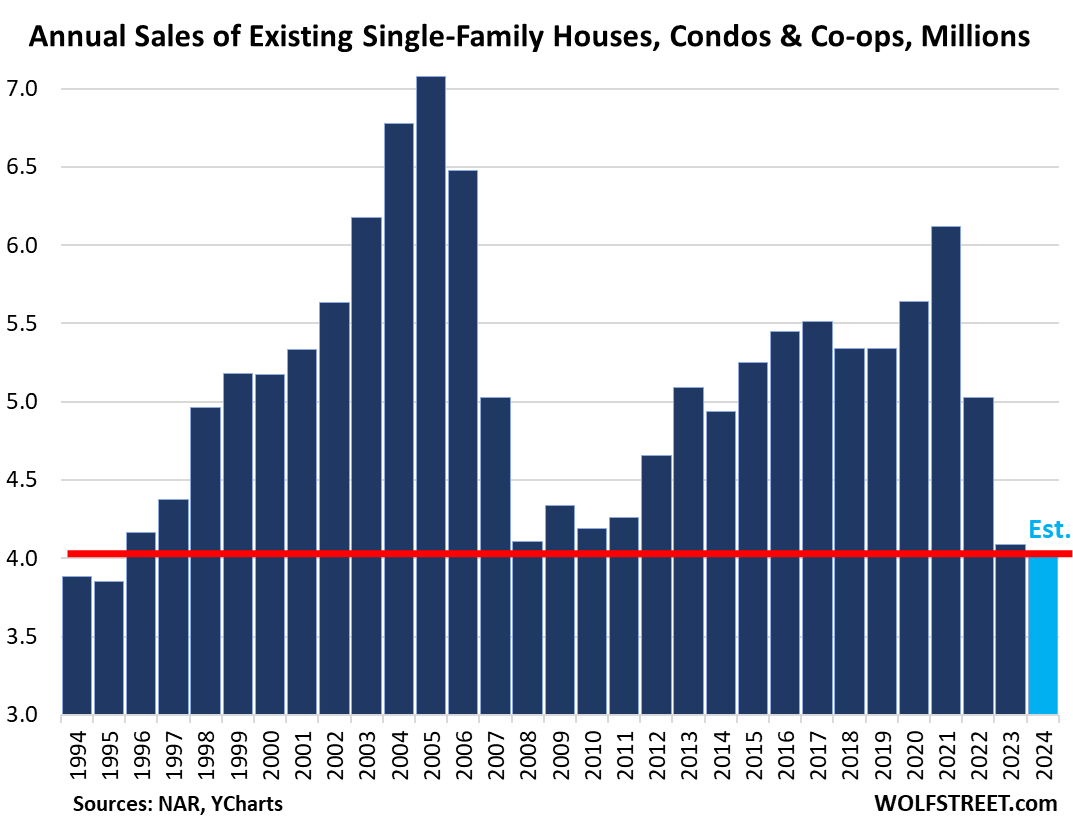

The demand destruction in 2024 has been even larger than during the Housing Bust. With today’s actual sales figures for November (not seasonally adjusted), the WOLF STREET estimate for the whole year 2024 comes in at 4.04 million sales, the lowest since 1995, below even the worst years during the Housing Bust.

During the Housing Bust, demand destruction was caused by an economic and financial meltdown that had been preceded by years of reckless mortgage lending that then came home to roost and turned into the mortgage crisis.

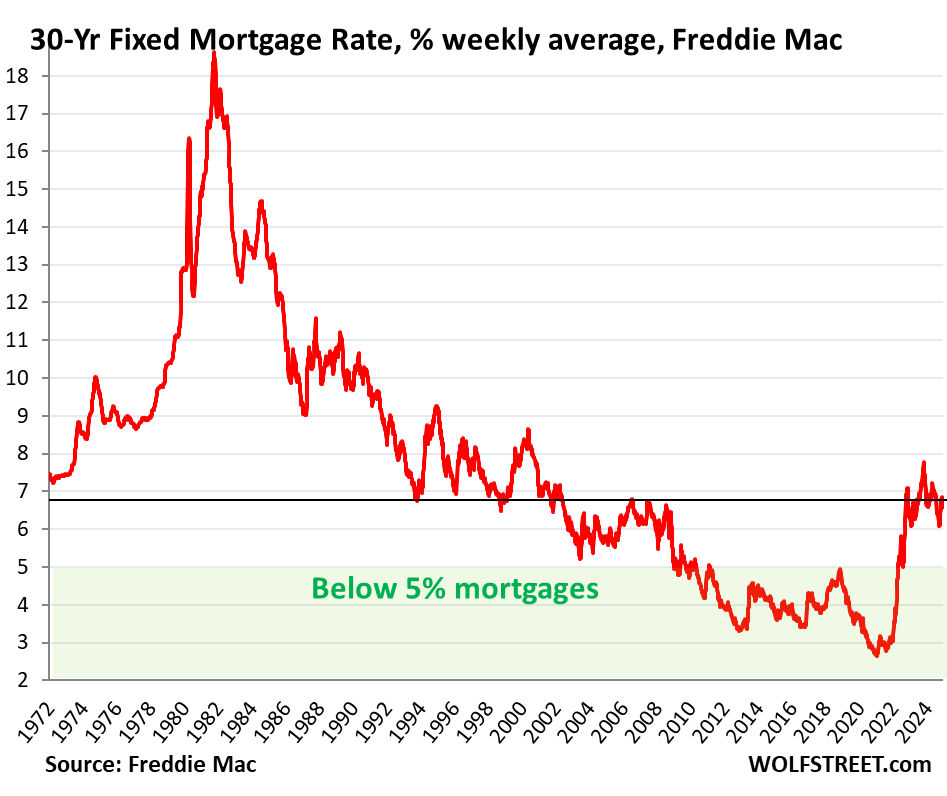

But the 2023 and 2024 demand destruction was caused by a gigantic spike in prices – the NAR’s national median price shot up by nearly 50% from June 2019 through June 2022 – and then in 2023, mortgage rates returned to normal-ish levels in the 6%-7% range, up from the pandemic’s free-money range of less than 3% (historical data from YCharts).

Getting used to 6% to 7% mortgage rates.

The real estate industry has now given up on trying to outwait those mortgage rates and is exhorting sellers and buyers to get used to “a new normal of mortgage rates between 6% and 7%,” as the NAR put it today.

These 6% to 7% mortgage rates are of course the old normal mortgage rates that prevailed in the decades before the money-printing era of 2008 through 2021, and they’re unlikely to go back to the pandemic range.

Fannie Mae, the largest Government Sponsored Enterprise that buys and guarantees mortgages, came out earlier this month, encouraging mortgage investors, the real estate industry, home sellers, and home buyers to get used to these 6% to 7% mortgage rates:

“It is unlikely we will again see the low mortgage rates we had during the COVID-19 pandemic,” Fannie Mae wrote in a blog post, adding that “current mortgage rates and Fannie Mae’s forecast for 2025 rates are well in line with rates over the past several decades. Since 1990, the 30-year fixed-rate mortgage has averaged 6%.”

The average 30-year fixed mortgage rate rose to 7.14% today, according to the daily measure by Mortgage News Daily.

Freddie Mac’s weekly measure of the average 30-year fixed mortgage rate rose to 6.72% today.

Mortgage rates track the 10-year but at a higher level, with a spread between them that varies. And the 10-year yield has jumped by nearly 20 basis points to 4.58% since the Fed’s rate cut yesterday.

Mortgage rates have been above 6% since mid-2022. The market might as well get used to this mortgage rates and deal with them – and lower prices, after the ridiculous spike, will bring up the volume.

Before the 2008-2021 money printing era, 5% mortgages had been essentially unheard of:

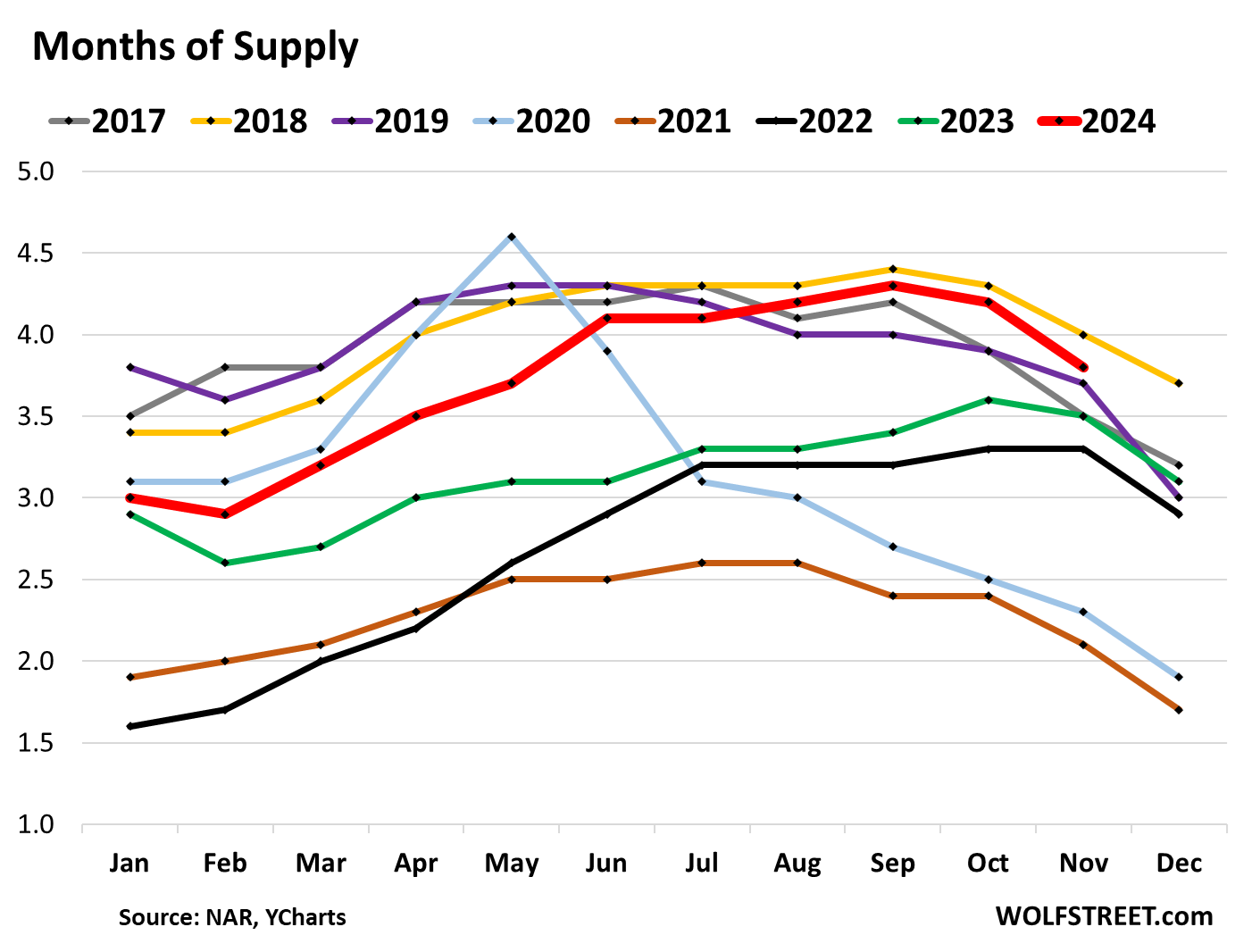

Highest supply for any November since 2018.

Supply of unsold existing homes on the market, at 3.8 months (red line in the chart below), was the second highest for any November over the eight years 2017 through 2024, behind only 2018 (yellow). And that is plenty of supply.

Unsold inventory dipped to 1.33 million homes in November, as homes got pulled off the market over the holidays and as new listings declined from the prior month, as they always do over the holiday period.

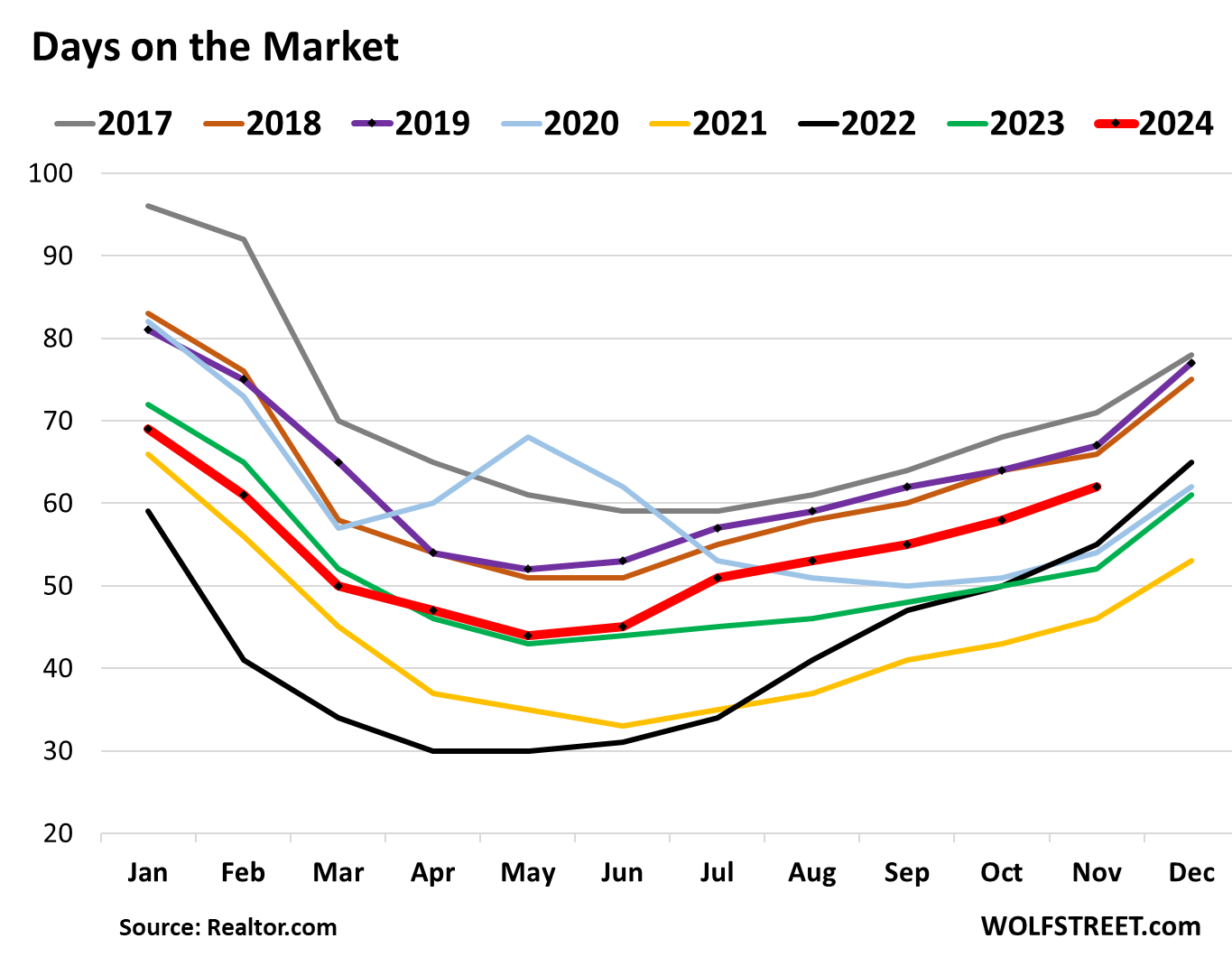

Days on the market keep rising.

The median number of days before the home is either sold or pulled off the market because it failed to sell rose to 62 days in November, the most for any November since 2019, and up from 52 days a year ago, according to data from Realtor.com.

This is in part a measure of how motivated sellers are by letting their home sit on the market when it doesn’t sell right away.

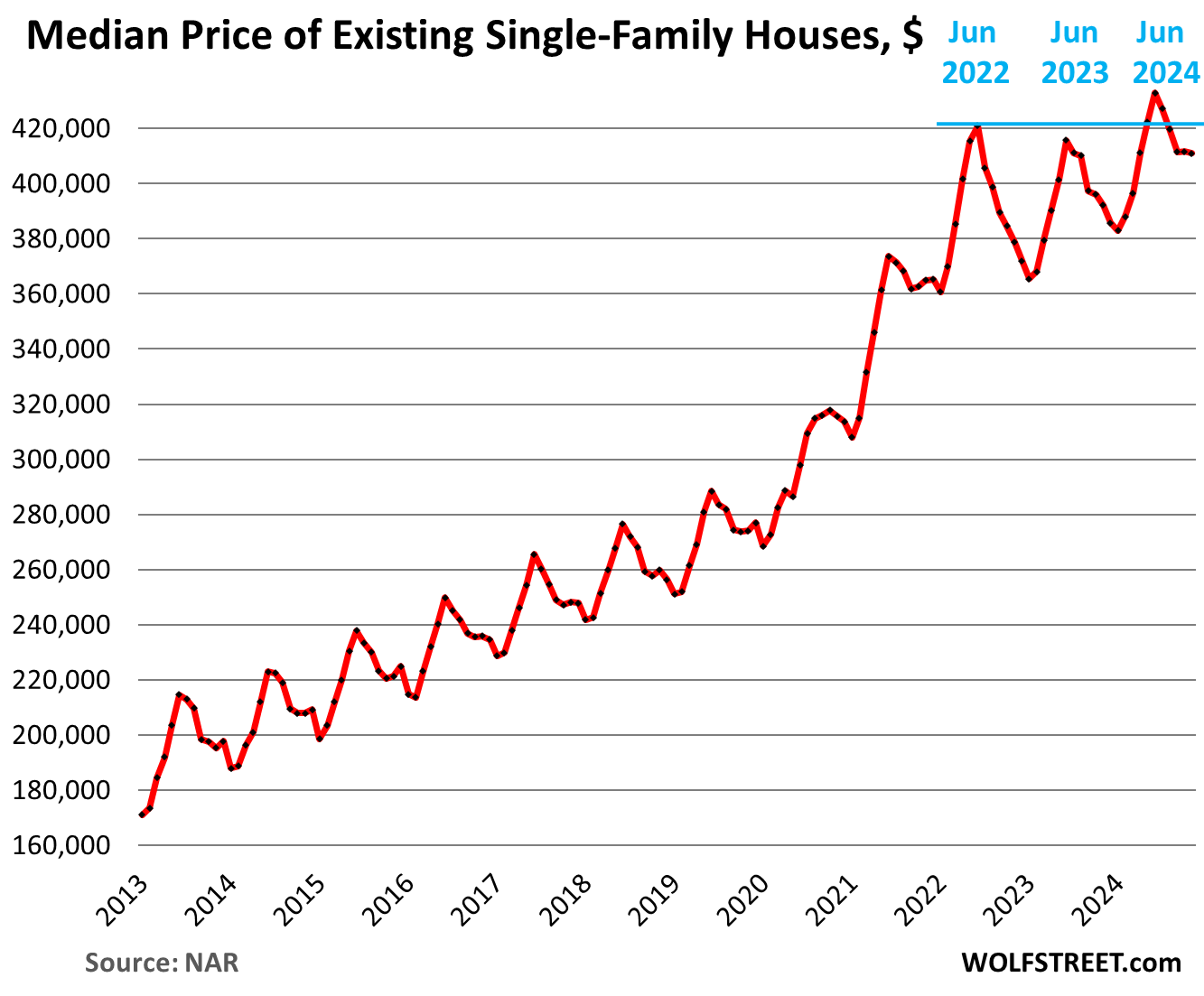

Prices are way too high.

The median price of single-family houses edged down in November to $410,900, with the past three months in roughly a holding pattern, in line with pre-pandemic seasonality over those months through December. This seasonal pattern is usually followed by a big drop in January. Year-over-year, the price was up by 4.8%.

In the three years between June 2019 and June 2022, this national median price had exploded by nearly 50%, on top of the large price gains in prior 10 years, and this — driven at the time by the Fed’s interest-rate repression and money-printing schemes — has become the #1 problem in the housing market today:

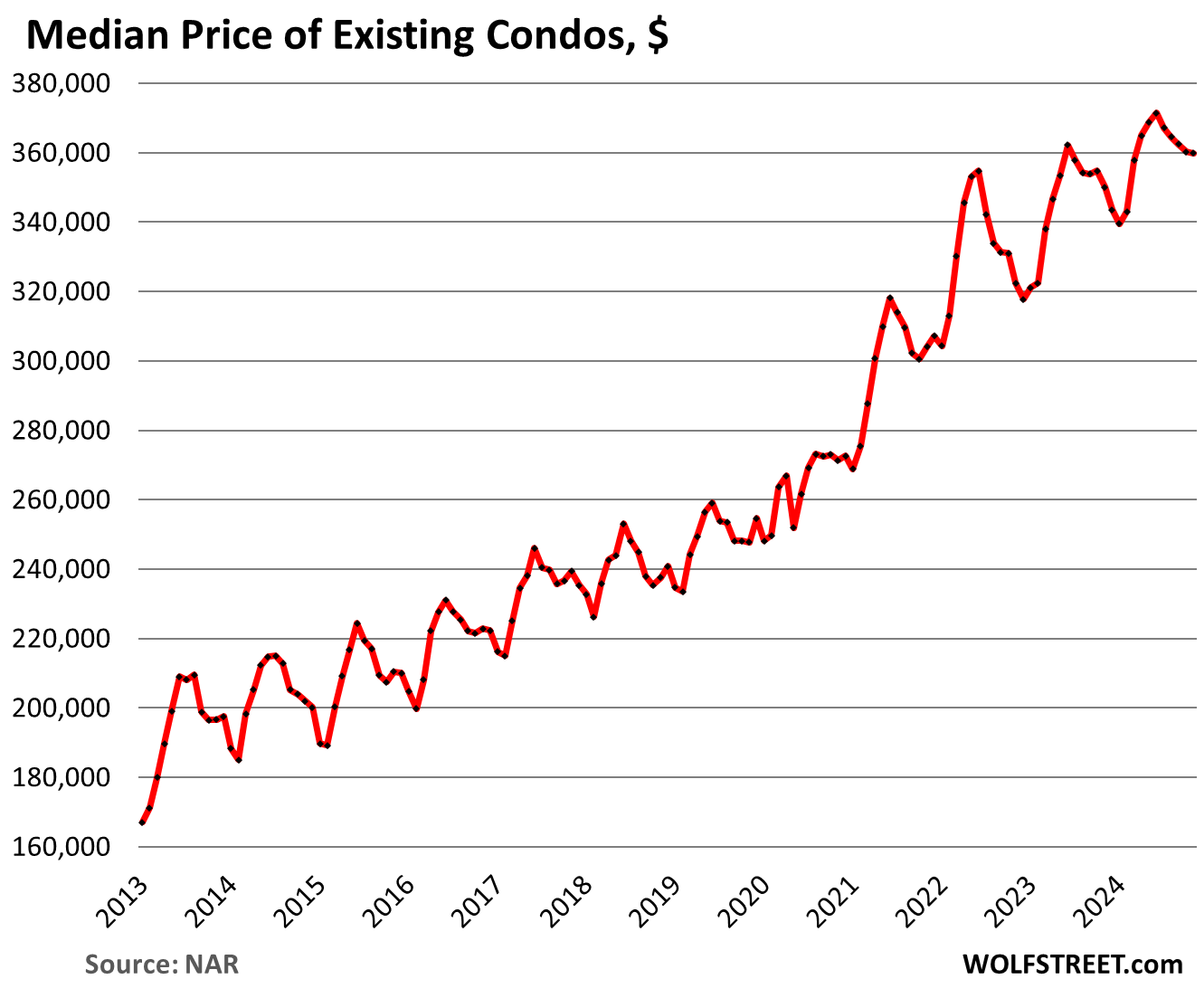

The median price of condos and co-ops dipped to $359,800 in November, for a year-over-year gain of 2.8%. Unlike single-family house prices, the median condo price didn’t experience any outright year-over-year declines in mid-2023.

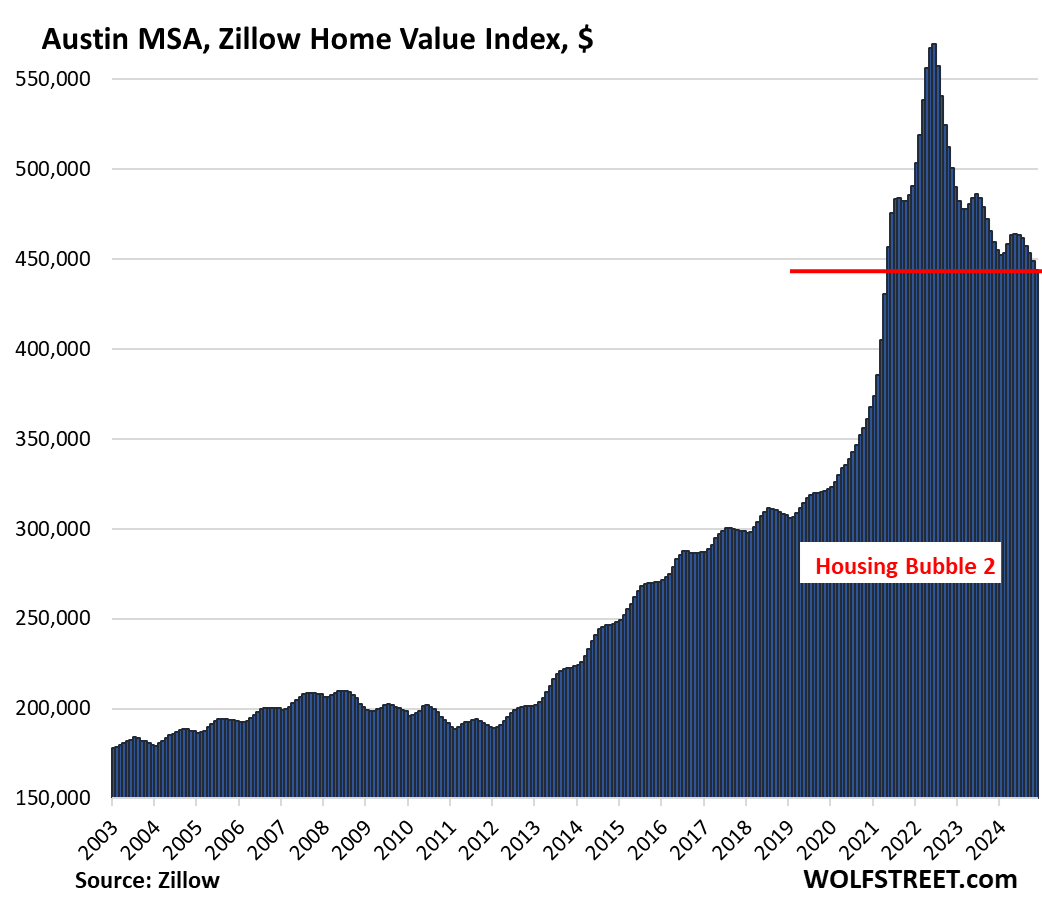

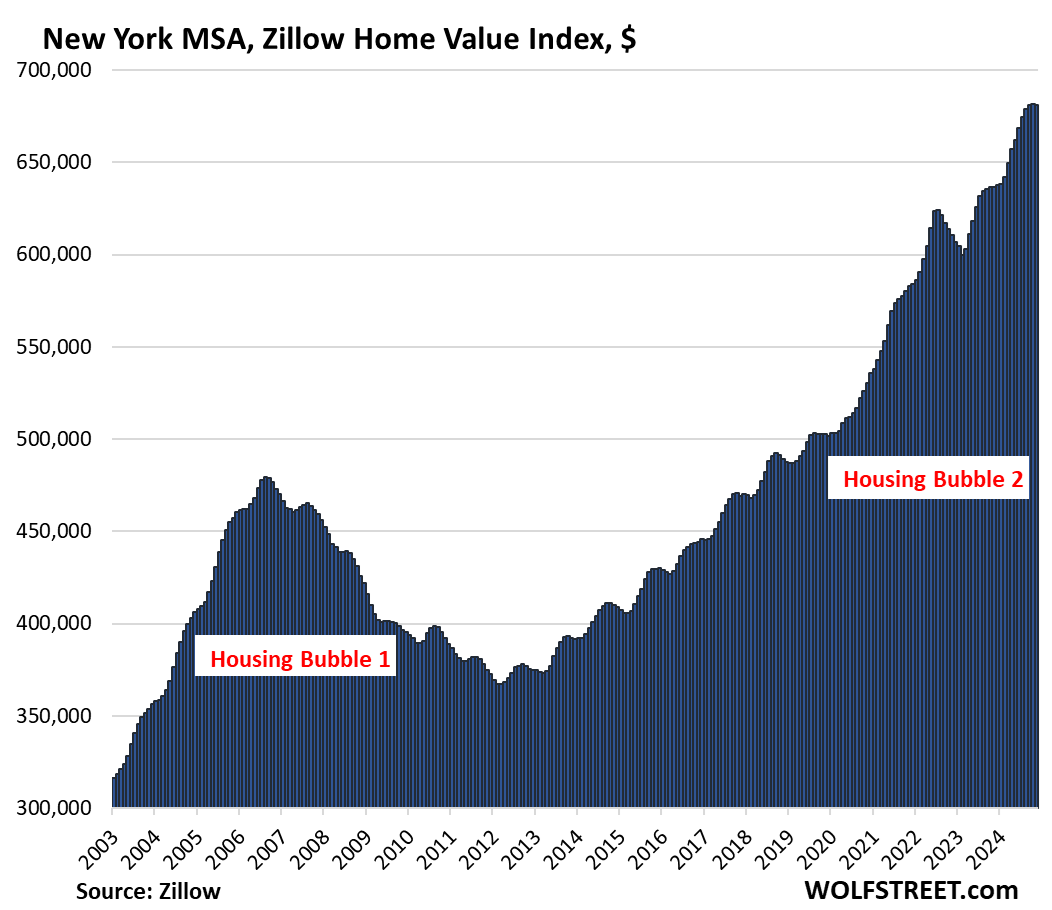

But home prices vary widely by metro. They have been dropping in some metros since 2022, but continued to rise in other metros through the summer, with declines now getting started in metros even where prices are not seasonal, based on Zillow’s “raw” mid-tier home price index. The two bookends of our series covering 33 markets, The Most Splendid Housing Bubbles in America, show the divergence, with Austin prices having plunged by 22% from the peak in mid-2022, while prices in the New York City metro eked out gains through October before seeing the first dip:

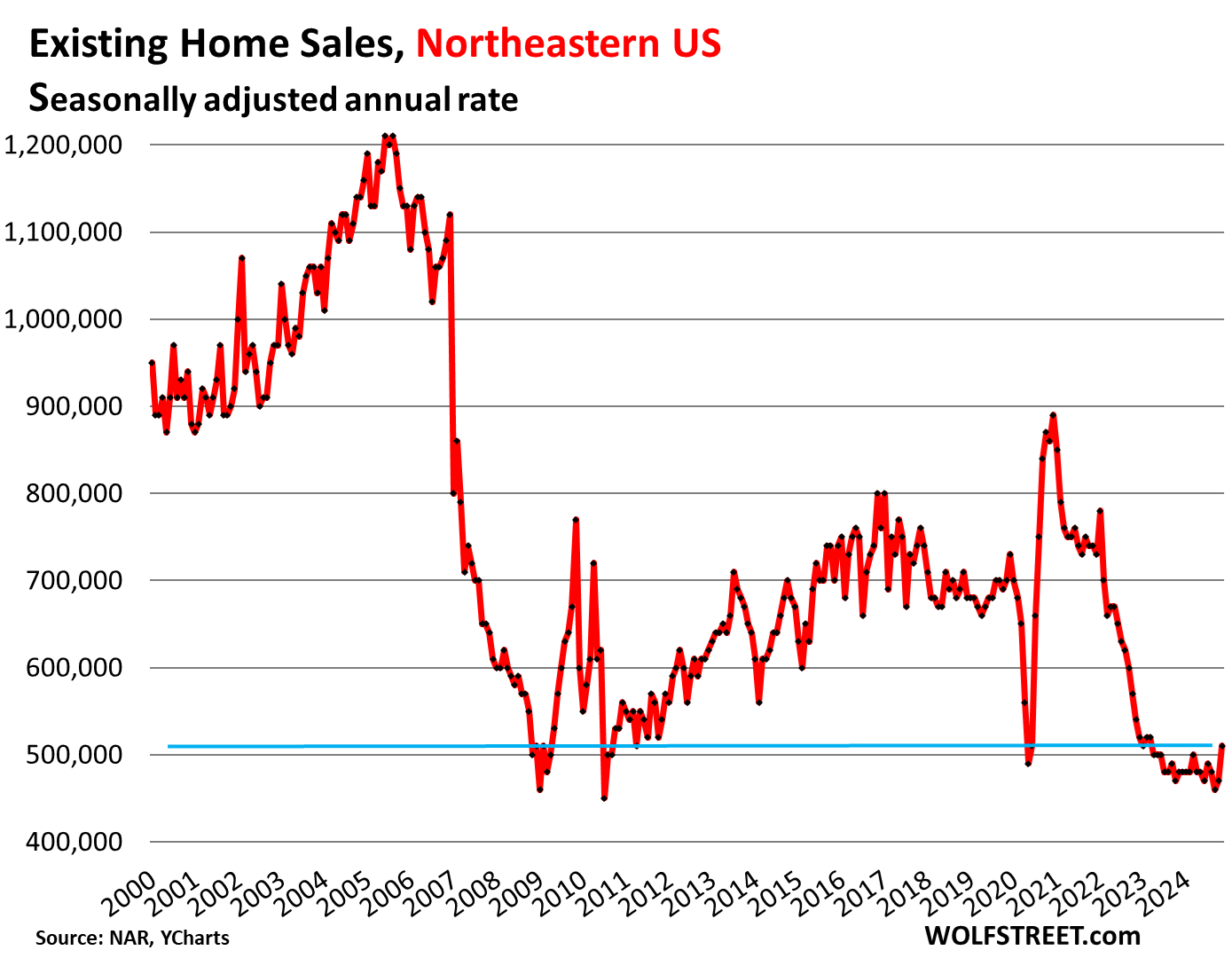

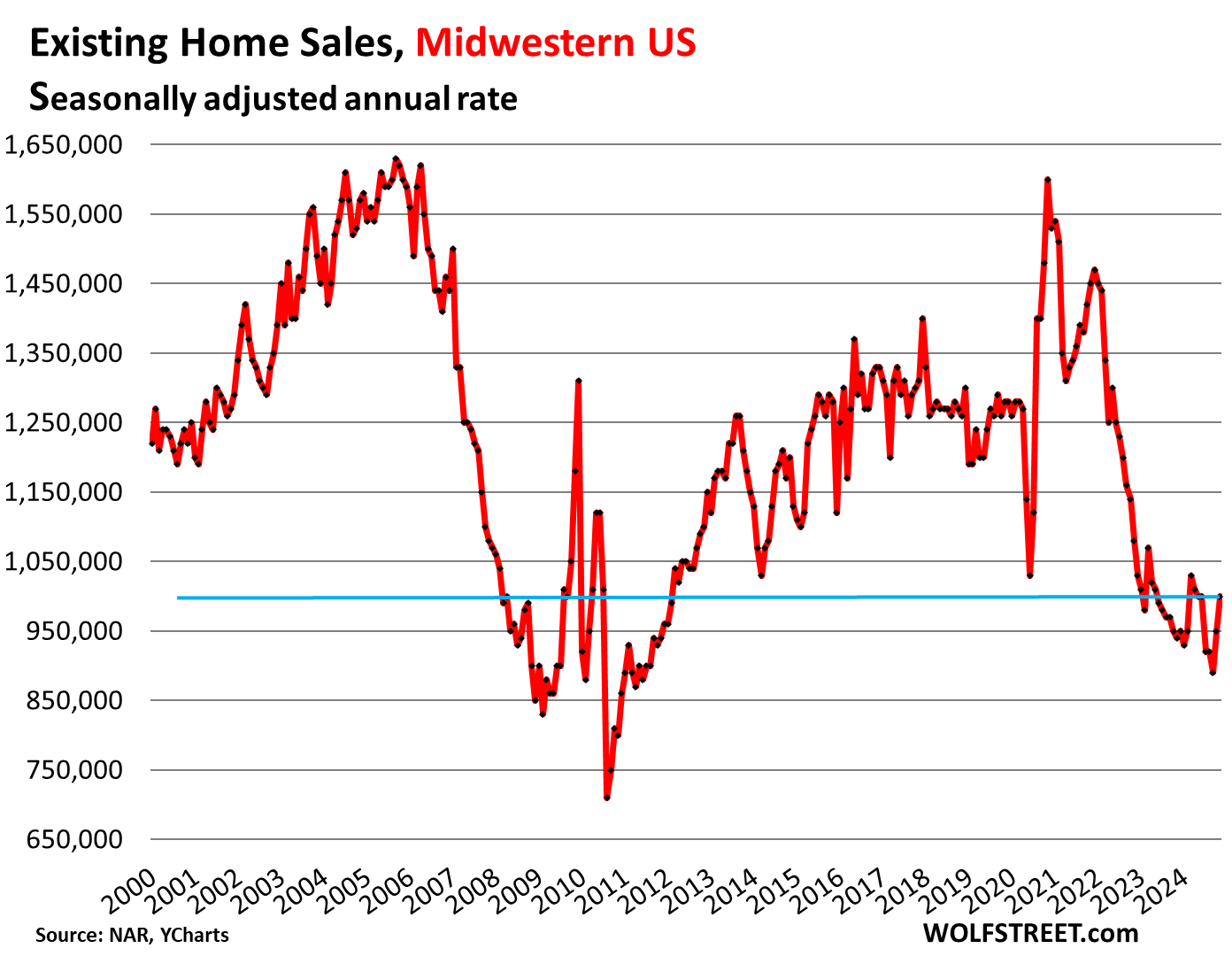

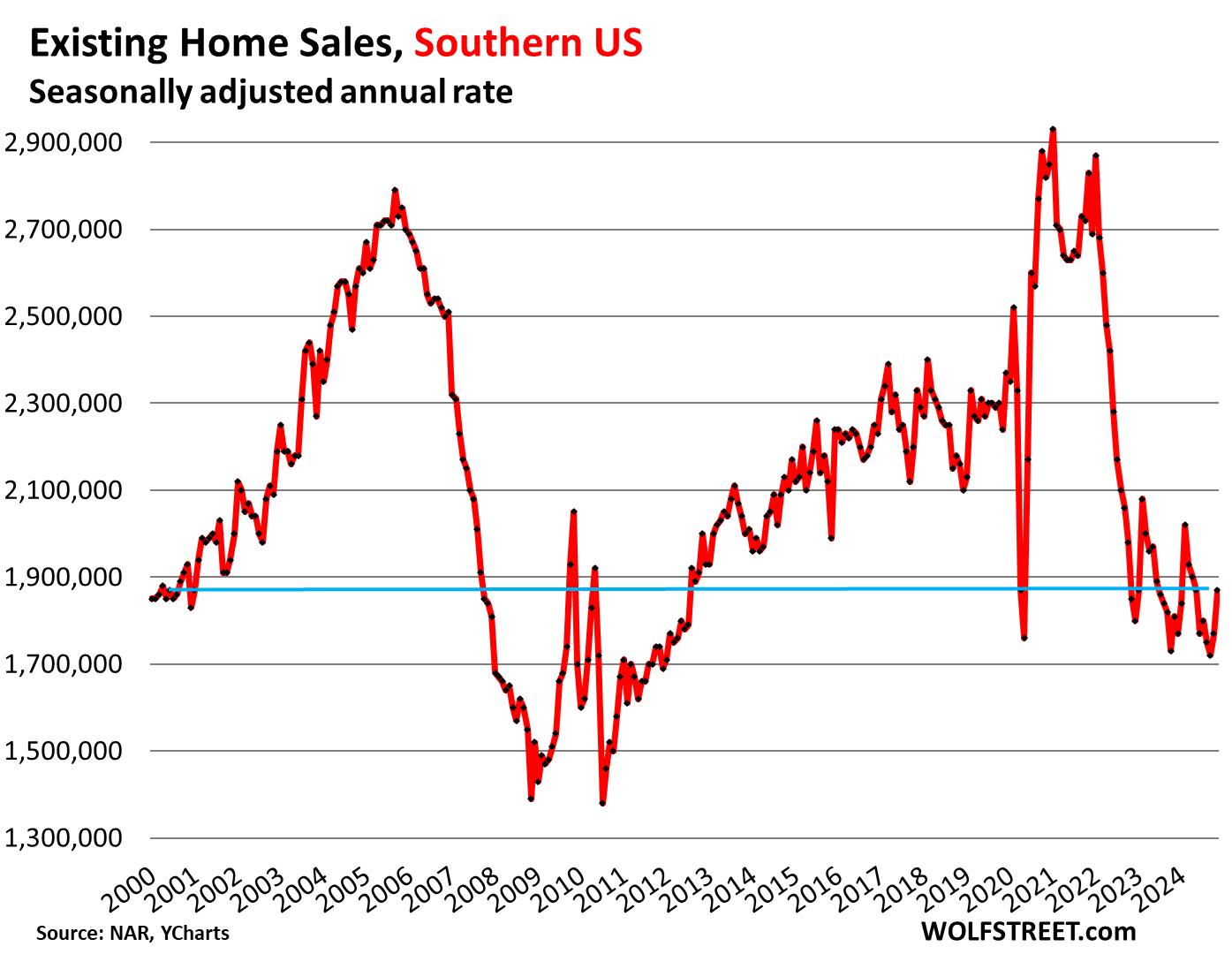

Demand destruction by region.

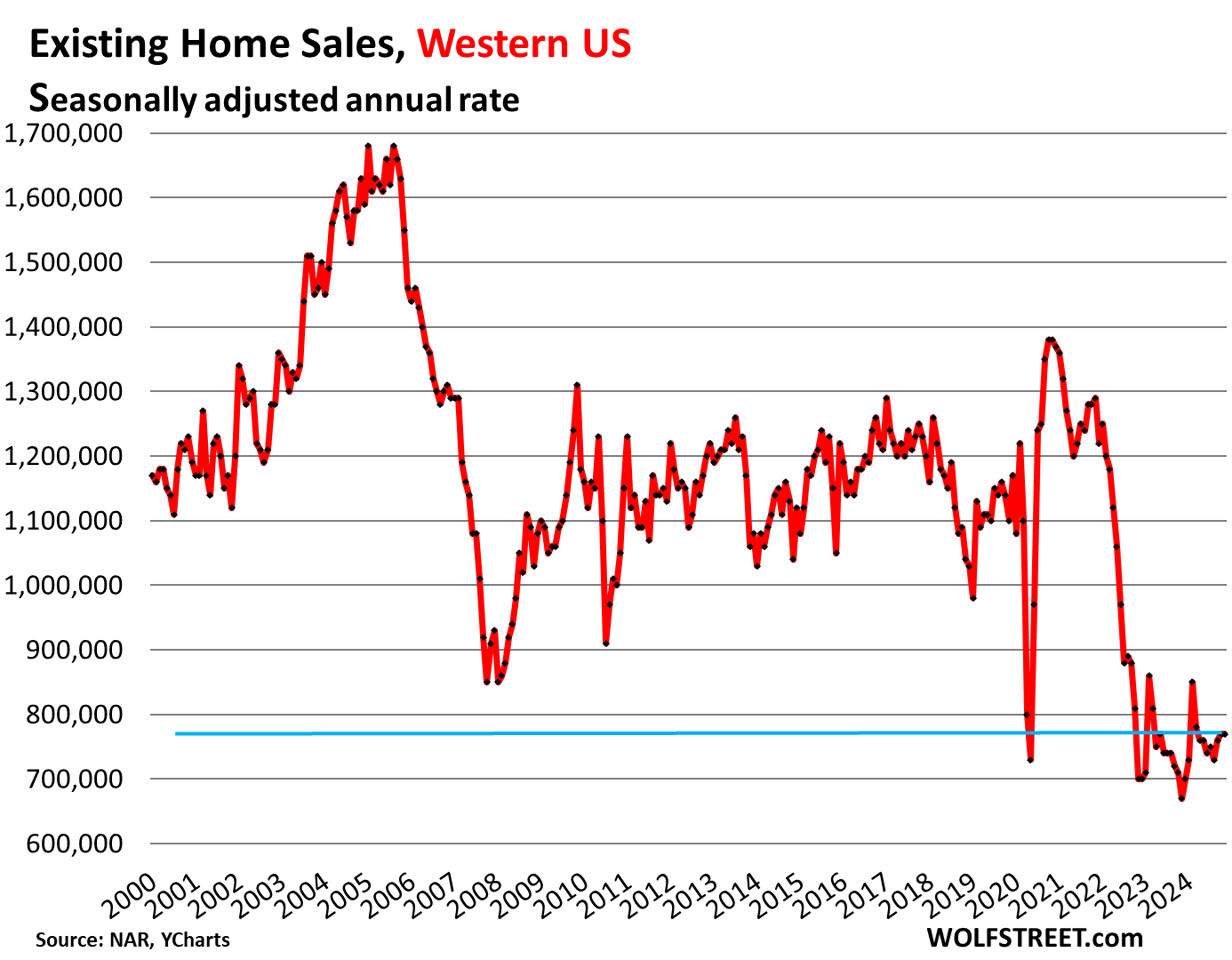

The charts below show the seasonally adjusted annual rate of sales, released by the NAR today, in the four Census Regions of the US. A map of the four regions is in the comments below the article.

Northeastern US: The seasonally adjusted annual rate of sales rose to 510,000 homes:

Midwestern US: The seasonally adjusted annual rate of sales rose to 1,000,000 homes.

Southern US: The seasonally adjusted annual rate of sales rose to 1,870,000 homes.

Western US: The seasonally adjusted annual rate of sales unchanged at 770,000:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Inflation Mandate: Jerome Powell’s Federal Reserve is working hard to get the population to capitulate to the sky high asset prices of housing and then to accept a normal rate mortgage to pair with it; truly creating 30 year indentured “house poor” generation(s).

Employment Mandate: Of course with that asset capitulation is maintaining demand; otherwise without capitulation there is “demand destruction.”

Are RE agents and the rest of the industry now going to tell people to lower their prices so they can start making commission checks again?

Generally, not until after the listing agreement is signed!

RE Agents,

A couple I know are starting divorce proceedings. The realtor strongly recommended they lower their expectations and significantly drop the price to ensure a quick sale. The Ms refused and thought the price should be even higher. This will end very poorly for them.

I think RE agents always ask selling to lower price and buyers to increase budget. This is the way to ensure a deal is made. Only when a deal is made the agent gets a cut.

Once they’re hired. But if the selling agent is still in the courtship period, trying to convince sellers to use him/her (instead of a competing agent) to represent them, the agent has incentive to promise the sellers he/she can get a high price.

after few months of paying rent and mortgage

hubby will default and they then get to go thru foreclosure

by then the acrimonious part of divorce will be evident

maybe then price will become real

I’m going to view a bank foreclosure(already done) and banksters have it priced cost + commission

about 30% to high given total rehab/gut job

est. $100k fixup

Another observation (yes, another meaningless anecdote), 2 years ago my home services business had 22 customers who were realtors. All have cancelled service since then. Home prices are not coming down (yet) but members of that occupation are getting quite desperate.

I am curious how much realtors are charging for their services now. There were supposed to be changes after the settlement of the lawsuit against the National Association of Realtors earlier this year.

Any changes to their commissions or fees? Any changes to how they are working with buyers or sellers? I have not talked with anyone buying or selling a home recently.

Anyone know?

RE agents are pushing back hard on transparency requirements, and would desperately like to return to 1970s age of data opacity, where only agents had access to listings, price changes, days on market, commissions paid, agent performance, etc. They see the removal of buyer agent commission sharing as the first battle win of this war. However IMHO the Internet data genie is out of the bottle, and they won’t be able to put it back.

Yes! Why is no one talking about this? Will it even make a difference if seller and buyer split the commission since most sellers will be buyers?

Buyers need to lay down the law. Any offer includes the seller paying the full commission. Or no deal. (Or, okay fine, we will reduce the offer price accordingly.)

Agents are expecting 3% each from buyers and sellers in Wichita, KS area

I’ve been looking & my agent is getting paid by the sellers as usual.

RE Agents may consider relocating the New Jersey. That’s the only state in the US that still outlaws pumping your own gas. There are many openings for gas station attendants in that state.

The female RE agents I know are already back on the tennis courts!

Good news article. Thank you for this research.

Nothing selling where I live, and no one dropping their asking. I’ve seen this before here, in the late aughts, when houses simply did not sell….for years. 7% is a very reasonable mortgage rate and may push people into more realistic and affordable choices.

I want to buy but I’ll stick with renting for years if I have to. I’ll wait this one out so that I’m not house poor. Prices in Tampa are still so out of wack. A $600k+ house nearby was recently listed for a 1,400 sf home built before 1950. I just don’t understand. Wood frame instead of block. Many more “for sale” signs in a few neighborhoods I’ve driven through the past couple weeks. And that anecdotal increase of listings is between Thanksgiving and Christmas.

Happy holidays all. Safe travels to those who are doing so. Special wishing well for Wolf and Mrs. Every new Wolf Street article is a gift.

Seems clear that rates will stay higher for longer as inflation remains sticky — keeping pressure on mortgages, while home prices remain too high.

Also see: “Treasury yields’ continued rise Thursday comes even after Musk and Trump both came out in opposition to the government’s short-term funding bill that needs to pass by Friday night to avoid a shutdown.

The 10-year Treasury yield jumped eight basis points Thursday to 4.57%. It hit 4.59% intraday, the highest since the end of May. That’s after spiking 11 basis points on Wednesday.”

I see home prices trickling down slowly but not by much. It is going to take years for wages to catch up with all this Inflation so the average homeowner that wants to move or downsize simply can’t sell and give up 3% mortgages. New homes are overpriced for square feet they are offering in the range of $300/sqft. in the development right behind my house while existing homes for sale are less than $200/sqft. Those new buyers are fools.

Those new buyers are getting builder subsidized mortgages at 4.875%

I run a mortage branch and have a builder account. We are offering a temp buydown at 3.875% and the builder is paying for the fixed 4.875%. Payment of a 500k house is 300 less than it 600 less than a Resale at 500k at 7% rate.

In order to get the same payment at 7% the home would have to be sold for 400k.

That’s 100k less. The costs to the builder is 40k per house to offer 4.875%.

Builders are making more money offering buydowns than by reducing prices.

How are these new home loans getting approved at whatever LTV is required without a huge cash down payment, being sold at $300 sq/ft or more with existing homes listed at $200 sq/ft and not selling for months now?

Unless the mortgage is assumable at the same rate (almost certainly not), those buyers will be totally screwed if they are forced to sell by life circumstances. And as sooperedd asks, how are they getting approved at the LTV?

House prices were significantly lower, even if using inflation adjusted amounts, before the money printer went brrr.

In the early 2000s, it used to be C$200,000 at that time, for a starter home in Vaughan or Markham, Canada.

In early 2022, those same homes went for a shopping C$1.5M on average.

“If you can keep your head when all about you

Are losing theirs…”

If Congress approves getting rid of the debt ceiling till 2027 (spend…SPEnd…SPEND!) would it be likely the 10-year bond, and perhaps MBS ,since they are somewhat correlated, would keep rising as a hedge for the very likely incoming tsunami of even more deficit spending? Watching all this play out and how it will affect people trying to buy a house or borrow money for home improvements is very concerning.

The debt ceiling has no effect on the spending that Congress approves. If it did, we wouldn’t have a budget deficit in every year but one over the last 50 years.

The debt ceiling is Congress saying we’re going to spend this much but you can’t acquire the money to make that spending possible. It’s stupid.

“Demand destruction by region.”

Wolf, does this region-specific data exist for new home sales?

Having done the math many times, it is cheaper for me to rent in the Bay Area than buy a fairly cheap house in either Texas or Florida. I am lucky in that my apartment is fairly quiet, crime is non-existent, the landlord fixes the important stuff, and California has a statewide rent control law. Possible long run appreciation from a house purchase does not matter to me, because, as Keynes once said, in the long run we are dead. If I was 20 or 30 I would probably think differently, but then I wouldn’t be able to afford these over-priced houses anyway.

The Federal Reserve chairman J. Powell and the FOMC may control short term rates but they cannot manipulate the longer term rates. The big question is if the huge increase in the median home price is a bubble? Time will tell…

Yes, but they can and have manipulated long rates before by buying long-term treasury notes via QE. My guess is that’s what’s contributing to the rise in long rates now, the on-going QT, with them selling off those longer dated notes and not finding as many foreign buyers. Along with the heightened entrenched inflation risks.

I continue to say bubble. Second (and third) homes where a big driver in the Covid increases. Yes, low rates helped out there as well. As more tourism destinations cap the number of short term rentals, it makes buying to rent less attractive for investors. With investors fleeing the market, owner occupiers are less inclined to pay ridiculous prices.

The place we’re watching, we track all listings that we’d consider if we were ready to move. List price, reductions, sale price and associated dates. Listing prices have definitely dropped.

A bunch of properties are just not moving and sellers won’t come off their prices.

We also look at the history of the property for clues that it was an investor purchase – usually bought in mid 2020 through 2021. Now those investors are trying to sell for nearly double what they paid. We just laugh at those.

Limiting short term rentals will make the remaining more, not less valuable and potentially more interesting to investors.

I disagree. I’ve been looking at lake homes & there are a lot of former short term rentals hitting the market now. IMO the math doesn’t work since covid is over.

I would image eventually there will be some distressed selling due to demographic aging, unemployment, etc. This is likely to soften the housing market a little help to bring prices back into better alignment with interest rates.

The later Aman. Very distinct colors and don’t seem to close. Have you been check for colorblindness? Pretty easy test.

Maybe Wolf will figure out something for you though.

It went from “date the rate” to a shotgun wedding.

will never understand why Americans, probably the most mobile population in the western world, seem to generally want 30 year fixed rate mortgages ……. or is nothing else being offered ?

UP here, in the great country of Canada, just refinanced, 3 year fixed rate 4.5 %…….had been paying over 8% using 6 month fixed rate mtgs to bridge the high rate period……so two 6 month mtgs got me from the expiry of my previous 3 yr low rate mtg through the high rate period to new 4.5% mtg.

We typically can choose from 6 month term to 7 years ( longer term are available though rarely used ) with a range of rates reflecting current realities/future expectations.

As to house prices, no idea, though own a few and not selling…..want hard assets for what will be a challenging economic period with, imo, rather more inflation than we’re expecting……..

As ever….but what the f do I know…….

Adjustable Rate Mortgages (ARMs) and fixed-rate mortgages with 15-year and 20-year terms, and other types of mortgages are widely available. But a government guaranteed 30-year with a 3% fixed rate is hard to beat. And that’s what they got before 2022.

30-year loan gives the buyer great optionality to either lock in their rate forever, OR lower by refinancing. For those of us who took out mortgages before 2022, the bank is now stuck loaning us money at 3% forever — great deal for us, bad deal for the bank. And practically everyone refinanced down between 2019-2022 if they had the ability to do so.

For me, the 30 year fixed rate was a big part of my overall financial planning when buying the house. I put down a large-ish down payment (30%) so that my monthly PITT expenses were comparable to my previous rent.

Easier to plan for the future when your monthly costs stay relatively fixed.

I assume the mortgages you reference are not amortizing in 6-36 months. What’s the standard amort?

Prices are too high based on interest rates and price appreciation. There are bad times to buy.

Get used to 6-7% mortgages? Sure. At current prices? Nope. But if that is how it goes – buyers capitulating, then mortgage payments should start reducing discretionary spending, finally cooling the economy…?

get used to the rates, not the prices. Stay on buyers’ strike until the prices come down enough.

Maybe…..Anecdote: Went Christmas shopping yesterday at the mall with my daughters. Just getting stocking staffers and picking up a few online orders so did not spend much time at the mall. I found parking right by the entrance. Mall was not crowded. Helpful “sales” associates at ever turn. Plenty of EVERYTHING on every shelf, rack, etc. Walking through the mall did not feel like a crowded NYC train station. Sales galore! Clearance racks jam packed with inventory. Very different from the previous (’20-’23) Christmas times.

The best three neighborhoods in my city have zero houses for sale (Ok, one on the fringes with a clear deficiency) and barely any non-new houses for sale in the rest of the city.

Seems to me that the wealthier people were smart enough to sell already if they wanted to, or are just waiting until Spring if there is no rush.

Desirable places still go quick and often get a little over asking, just not to be rude (like a tip).

You still see a lot of obviously insane sellers, though, especially for crap shacks. There is one asking for over twice market value because they have some drawings available that show 7 extra townhouses crammed on the property, as if I couldn’t come up with something on Sketchup myself.

There’s always one.

“not in my market”, “not where I live”, “good houses still go for a little over”.

You must have really wanted to say that!

Because…that’s not really what I said…

You got all kinds of people horrified because they can’t come up with $400k+ to buy a starter townhouse, yet everywhere I go, people are tripling the size of already expensive houses, at costs of $600k to $1M or more. No wonder so many people are pissed.

Starter townhouse should not be $400K

Just got my new prop tax bill – $422K assessment for 960 sqft on a fifth of an acre (not even a 1/4 acre). Ridiculous. This house would never sell for that much.

I wonder how much of this housing inflation is caused by greedy city gov’ts over-assessing so they can collect more tax$$.

I was was a teenager but I was there when CA’s Prop 13 was passed by voters.

Property taxes in 1975 were 3% of assessed value. Assessed value of my parent’s house was 20K in 1970. By 1976, the assessed value was 80K. 4X increase in taxes. Prop 13 was a taxpayer revolt that set property taxes to 1% and rolled the assessed value back 2 years. It also limited tax increases to 2% per year.

I’ve seen similar ballot measures in other states recently.

Property taxes are a tax on unrealized gains.

If I live and die in this house, it doesn’t matter to me if its theoretical resale value is $400k or $200k or $0. But I pay a different amount of tax based on what the city thinks this theoretical value is.

Yes, Property Taxes are a wealth tax.

You are taxed on unrealized gains.

That makes it difficult for people on fixed incomes. They may have to sell the house, reverse mortgage, or HELOC the house just to pay the taxes.

That was one of the reasons Prop 13 passed in CA. Seniors on fixed incomes were being forced to sell their long-term homes after values exploded 4X and taxes followed in the 1970’s.

IMHO, state, city, county tax income increases should be capped to population growth and inflation.

Governments should not be given a 30-40% (or 400% like in the 70’s) windfall just because people are foolish enough to overbid driving up home and property taxes values.

Seems like we roll from crisis to crisis. we allow all the RE scams of the early 2000s to result in the 2008-2012 crisis. We bail the system out with trillions.

Covid comes and we bail everyone out with trillions after mandating everything close down. QE in full causing 3% 30 year mortgages! Houses get way more expensive.

So much Govt spending/investment we cause inflation.

Then we finance two or three foreign wars. And let’s not forget Biden forgiving billions of dollars of student loans.

Absolutely crazy, but you have to try to ride this wave and take advantage of the opportunities these idiotic moves present.

It’s crazy but look around the world. Since the start of 2020, just before pandemic, America’s real growth has been 10%, three times the average for the rest of the G7 countries. Among the G20 group, which includes large emerging markets, America is the only one whose output and employment are above pre-pandemic expectations, according to the International Monetary Fund.

So we should be thankful that we have such quick reacting central bank a government who take bold and decisive action.

Repeat sorry…

Interesting tidbit:

““Every metro region in Montana is experiencing its lowest level of affordability on record.”

Even though Montana has a net negative population replacement rate — that is, residents are dying faster than the birth rate — that is completely offset and overshadowed by the net in-migration rate, which is the number of people moving here from out of state.

Montana is basically an enclave for rich people who want a quiet and scenic lifestyle. They can share a private plane service in and out of a bunch of major cities.

I’m currently holding off on buying a home because I’m waiting for affordability to improve. Even though I have a good income, I find it difficult to afford living in the Bay Area. As a renter, I save the extra money I can and invest it, hoping for a favorable market trend or downturn that will allow me to buy a property that meets all my criteria.