Worst 6-month PPI inflation since August 2022 (+5.3% annualized). After multiple rate cuts by the Fed, inflation heats up everywhere: services, food, energy, other goods.

By Wolf Richter for WOLF STREET.

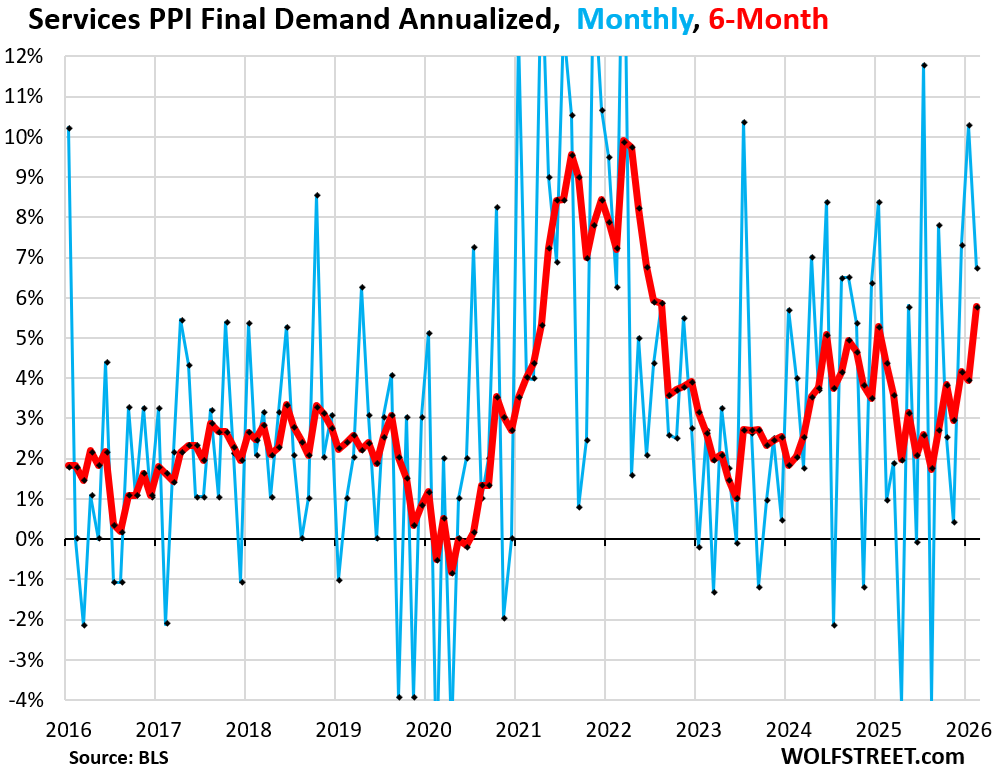

The Producer Price Index final demand for services jumped by 0.54% (+6.7% annualized) in February from January, seasonally adjusted, after spiking by 0.82% (+10.3% annualized) in January, and by 0.59% (+7.3% annualized) in December, which pushed the six-month average to +5.8% annualized, the worst since August 2022, according to data from the Bureau of Labor Statistics today.

The services PPI weighs 68% of the overall PPI. It drives the core PPI (which excludes food and energy components), and even the overall PPI (which includes food and energy). The overall PPI was further driven on a month-to-month basis by big spikes in food prices (+2.4% not annualized!) and energy prices (+2.3% not annualized!).

Within the services PPI:

- Trade services PPI (weighs 19% in overall PPI): +0.4% month-to-month not annualized, after a big spike in the prior month.

- Transportation & warehousing services PPI (weighs 4.9% in overall PPI): +0.3% month-to-month not annualized, after big spike in the prior month.

- Other services (weighs 38% in overall PPI): +0.6%.

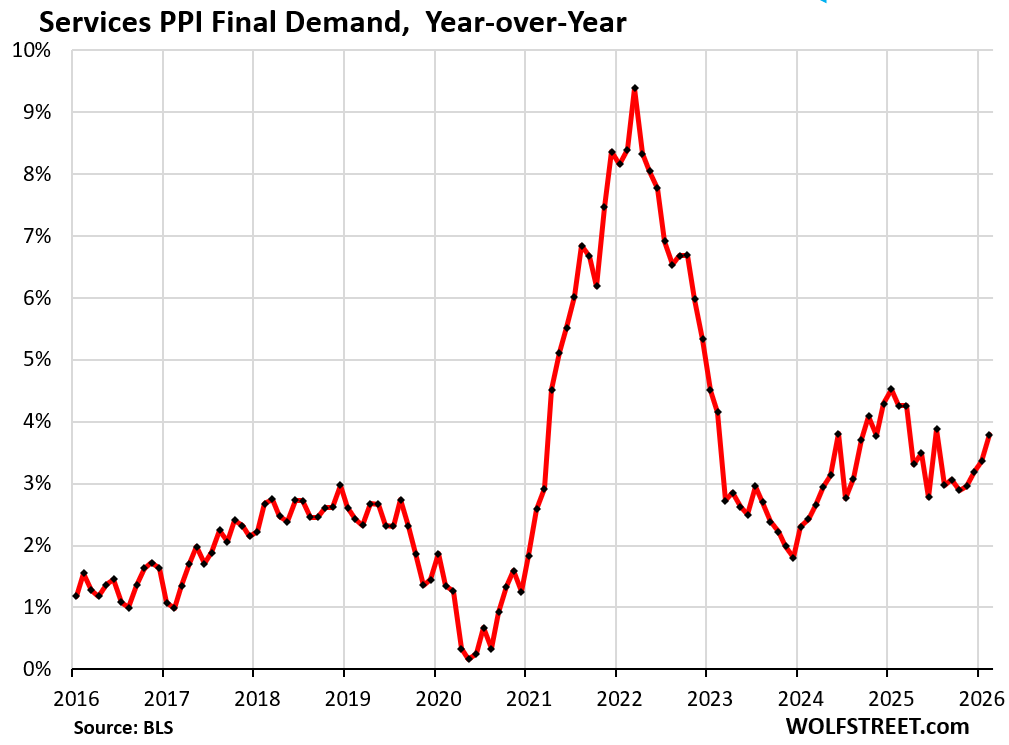

Year-over-year, the services PPI accelerated to 3.8%, the fourth month in a row of acceleration.

The low point, the point of the coolest recent services PPI inflation, was in December 2023 at 1.8%. The inflation rate has more than doubled since then.

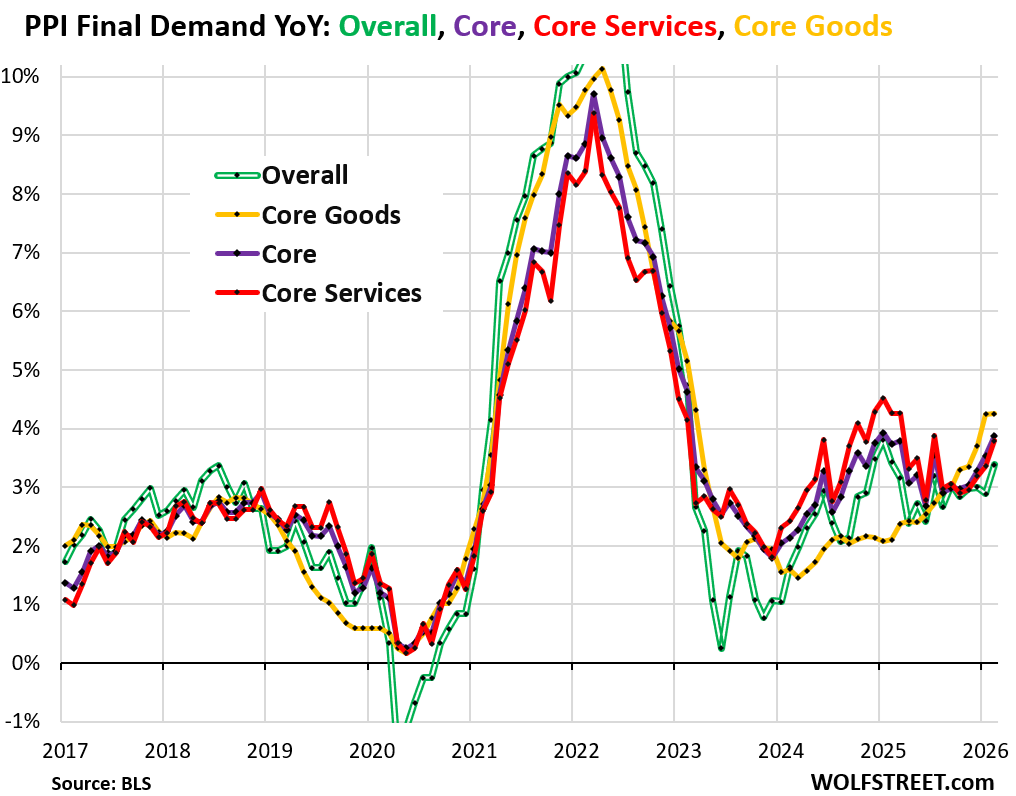

PPI inflation has been broadly accelerating since 2023, with a lull in early 2025, and a steeper acceleration over the past six months.

Food inflation, after the massive spikes in 2021 and 2022, had calmed down a lot. But that ended mid-2025, when food prices started to accelerate their increases. Prices of energy products had plunged through 2025, but are now spiking.

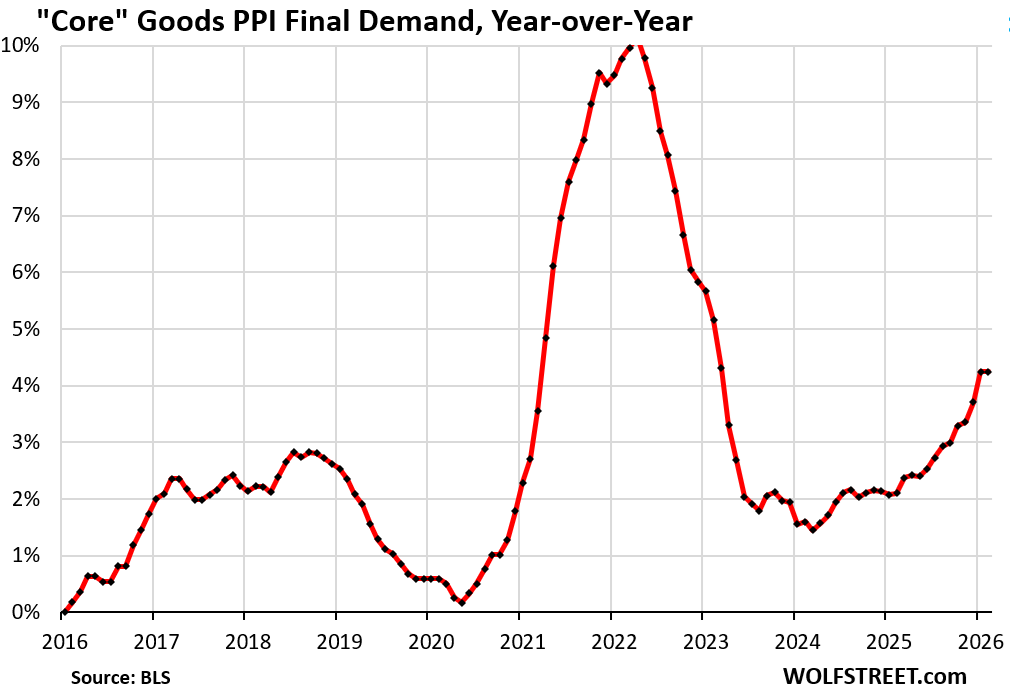

And core goods prices started to accelerate in 2024 and continued to accelerate in 2025, in part fueled by tariffs that companies were paying for.

The chart below shows PPI inflation on a year-over-year basis for overall PPI (green double line), core PPI (purple line), services PPI (red line), and core goods PPI (yellow line).

The services PPI (red) and the core PPI (purple) nearly overlap because core PPI is dominated by the services PPI, with core goods PPI (yellow) being a much smaller factor in core PPI.

And the Fed has been cutting its policy rates during this acceleration period, starting in September 2024.

Goods prices.

The PPIs final demand for both food and energy surged in February from January:

- PPI for Food: +2.4%;

- PPI for Energy: +2.3%.

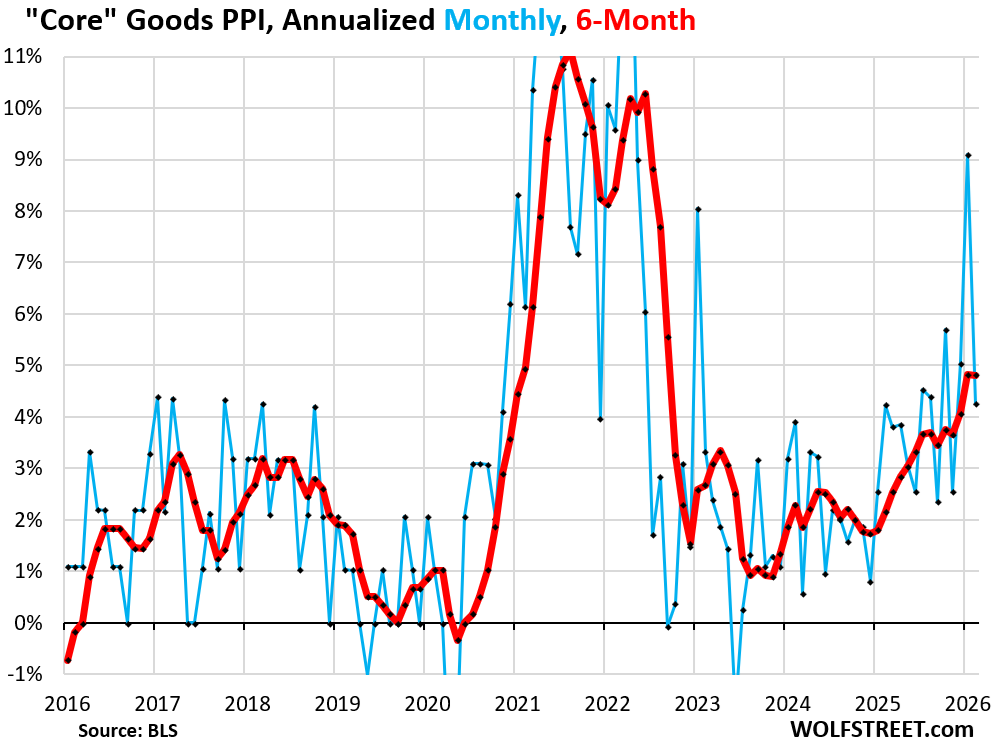

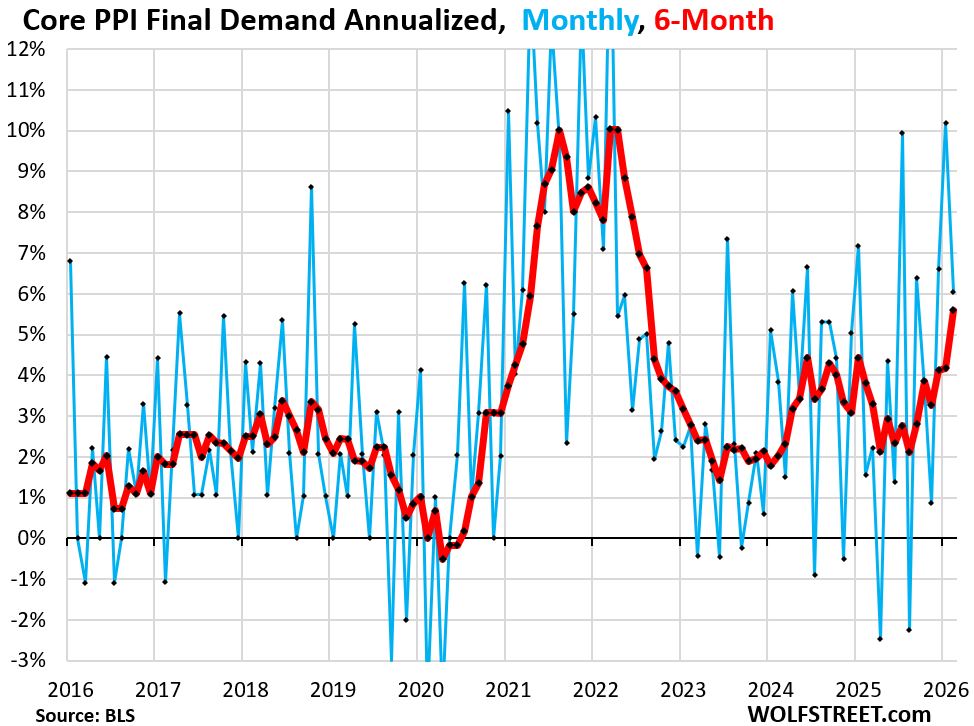

The Core Goods PPI final demand (excludes food and energy) rose by 0.35% in February from January (+4.3% annualized), after a huge spike in the prior month.

The 6-month average rose by 4.8% annualized for the second month in a row. Both were the worst since September 2022.

Companies are trying to pass tariffs on to each other through the goods categories at various stages of the PPI. But consumer-facing companies have resisted price increases because consumers have resisted price increases, and consumer-facing companies had trouble passing on higher costs to consumers without losing sales.

Year-over-year, the core goods PPI jumped by 4.2%, same increase as in January, and both were the worst since March 2023.

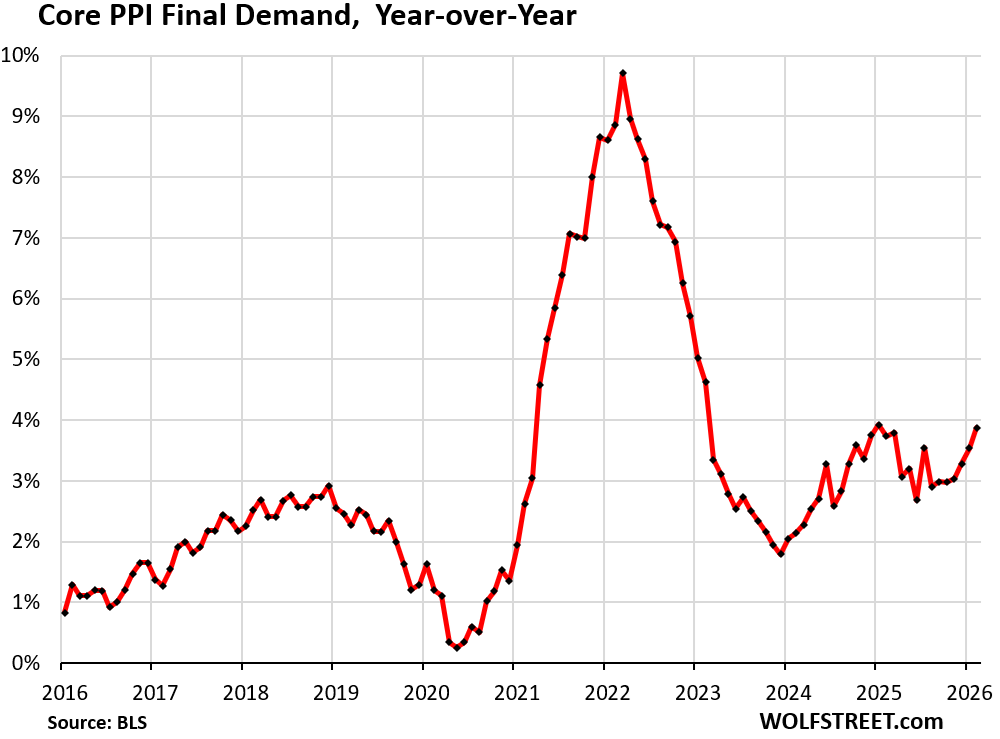

Core PPI Final Demand, which includes all goods and services except food and energy, jumped by 0.49% in February from January (6.1% annualized) seasonally adjusted, after spiking by 0.81% (+10.2% annualized) in January, and by 0.53% (+6.6% annualized) in December.

The six-month average accelerated to +5.6% annualized, the worst since August 2022.

Year-over-year, core PPI accelerated to +3.9%, the worst since January 2025, and both were the worst since February 2023.

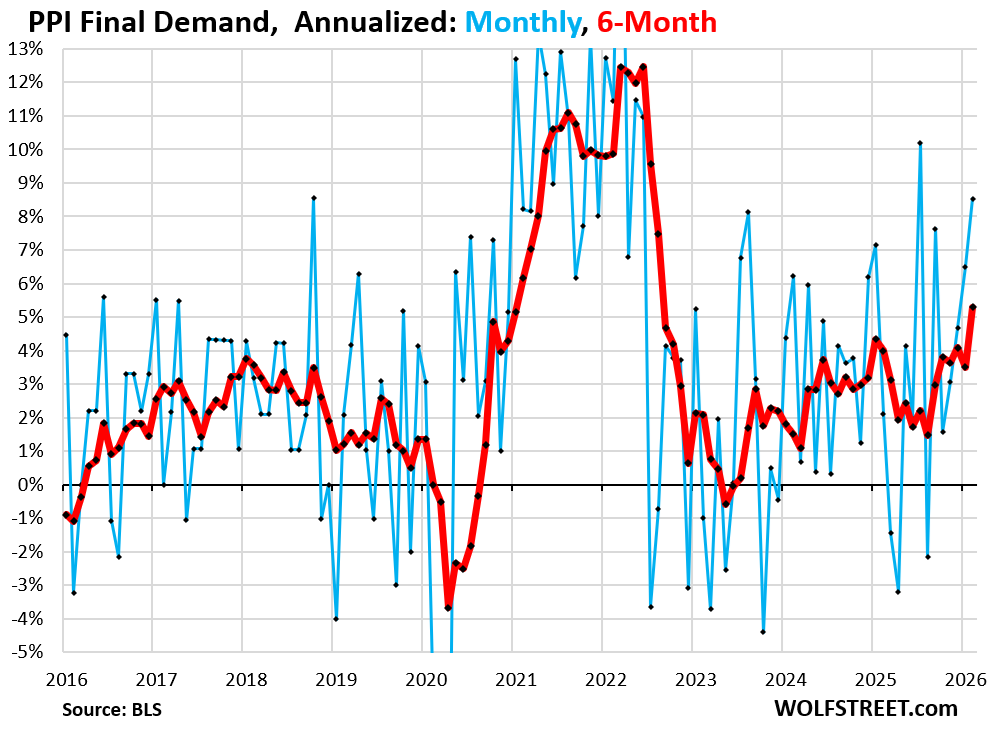

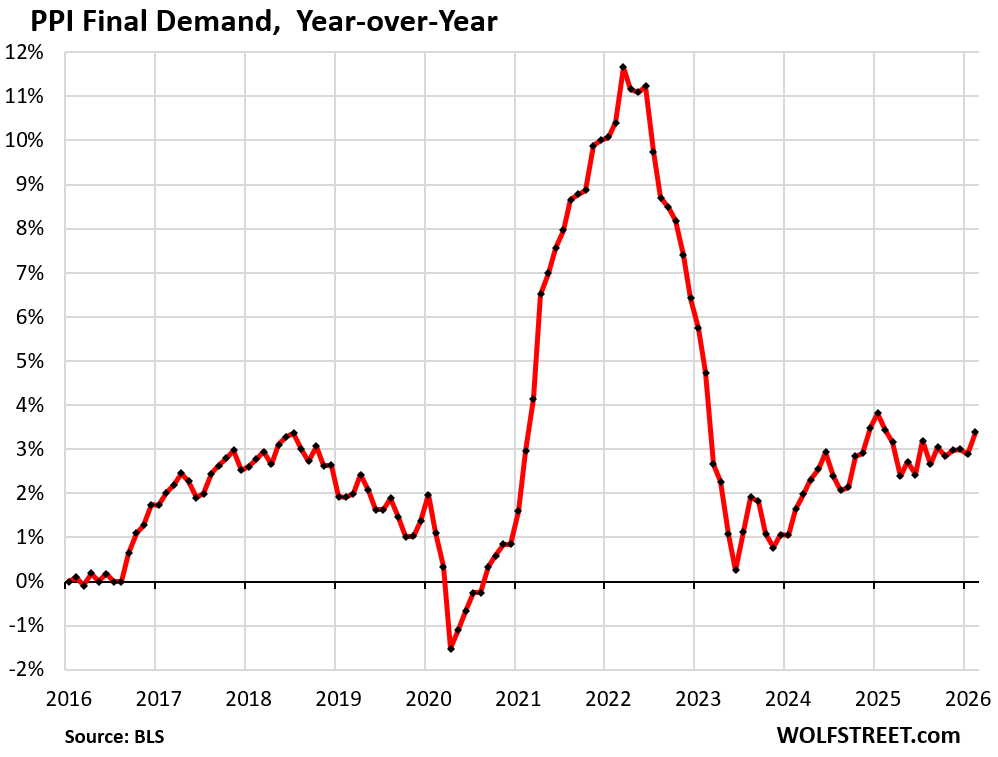

The overall PPI Final Demand, fueled by the spike in food and energy prices, and the surge in services prices, jumped by 0.68% month-to-month (+8.5% annualized).

The six-month average jumped to +5.3% annualized, the worst since August 2022.

Year-over-year, the overall PPI accelerated to +3.4%, as the past six months of month-to-month increases are starting to push the 12-month reading higher:

The Fed has a complex and growing inflation problem on its hands.

Services inflation, goods inflation, food inflation, and now also energy inflation have all been heating up.

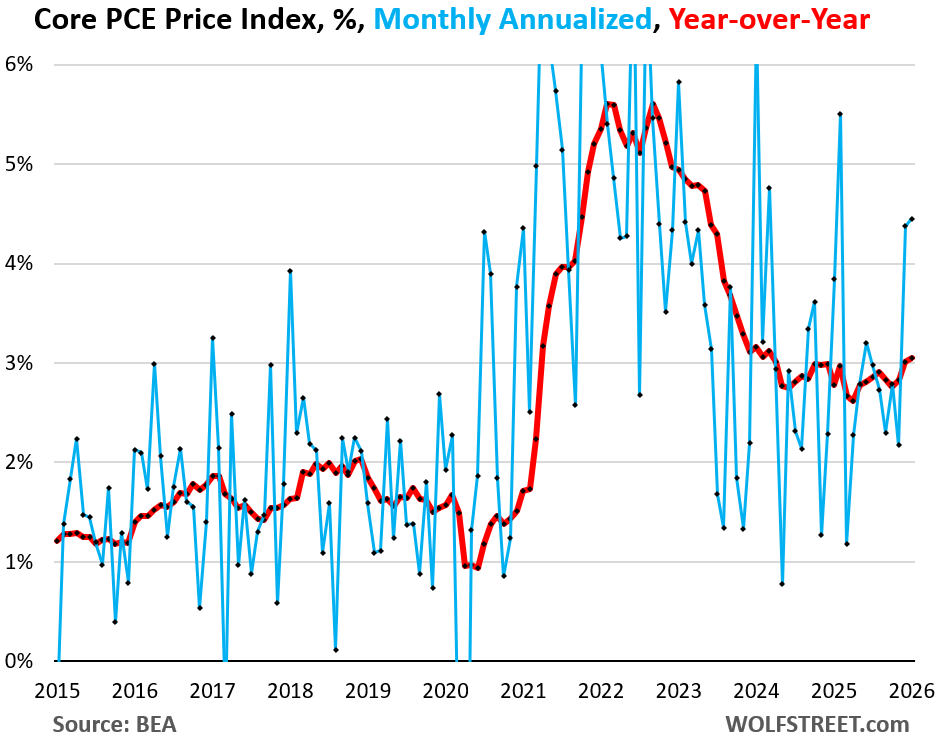

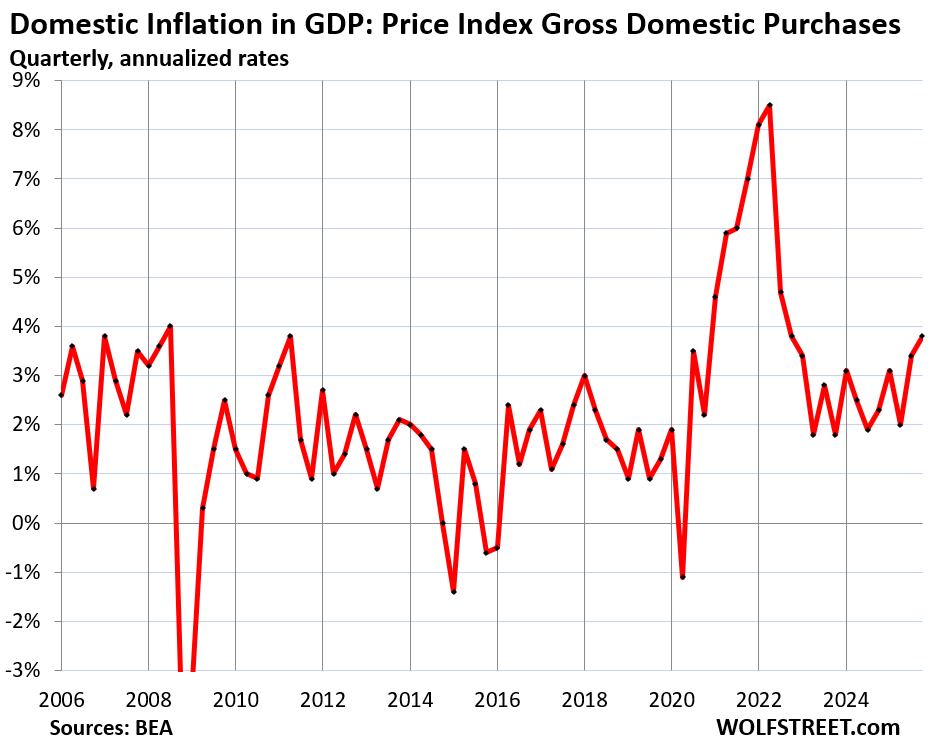

Today’s PPI (producer-facing inflation) added another data point, to what the Fed-favored “PCE price index” (consumer-facing inflation), and the GDP’s “Price Index for Gross Domestic Purchases” (inflation in the overall domestic economy facing consumers, businesses, and governments) have already been saying: Inflation is broadly accelerating.

And if the Fed is talking about rate cuts in this environment, it is clearly stoned.

The Fed-favored core PCE price index, driven by core services, jumped by 0.36% (+4.5% annualized, blue line) in January, even more than in December (blue line).

Year-over-year (red line), it accelerated to 3.1%, the worst in nearly two years. It has been zigzagging higher and ever further away from the Fed’s 2% target since May 2025 (data was released last week; my detailed report is here).

The inflation measure for the domestic economy, the Price Index for Gross Domestic Purchases, which is part of the GDP data and reflects inflation adjustments in GDP except for imports, accelerated to 3.8% in Q4, the worst in three years: domestically bred inflation in the overall US economy:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Hoping this is a repeat of the 2023 into 2025 scenario, and it starts dropping again, but it likely isn’t.

Again, the FED NEVER should have stopped raising rates. They did so prematurely, and then cut prematurely. They are destroying the financial lives of the masses.

When was the last unexpected Fed rate cut – the one that surprised everyone? The last time what they didn’t meet expectations?

The Jumbo Rate Cut 🤔

Everything they do is tilted towards causing more inflation. Even today when they kept rates unchanged, they signaled a rate cut. These guys are a f**king cancer upon society.

We need a rate cut like I need broken bottle glass in the eye.

What makes me crazy is this “we have to balance inflation with unemployment” BS. It’s 4.4%; that’s historically low. I’d call it damn near unnatural, and not normally sustainable without consequence and that makes me TAH 🤷♂️

There is no need to cut rates to save bloated company labor. If nothing else, people will draw those favorable rates to accelerate AI-invested RIFs.

Crazy times man.

Taylor rule says rates should be exactly one quarter point higher than they are right now. So yeah they should raise rates, but really just once for now unless things continue to get worse.

Nice timing—near the start of the current Fed Reserve meeting. Fingers crossed that they stop ignoring the inflation warning signs and start increasing rates.

Fire up the press conference zapper!

For the bingo card: will Trump make up a new name for Powell, or will he continue to be “Too Late Loser”?

We had fantastic rates, low rates going lower, they were going to be the best you’ve ever seen that’s what they’re telling me. TOO LATE

Fire is Burning

The second wave of inflation is just getting started. Thanks Wolf!

Expectation Management:

Federal Reserve’s actions: Powell & Company literally teach the proletariat that interest rates control inflation, that the Federal Reserve is concerned about inflation & jobs that are economic inverses of each other. With jobs overheated, the Federal Reserve drops rates before inflation is lowered even to their worker skimming rate of 2%.

Psychology: AI lists New York times +3: “Federal Reserve held interest rates steady at 3.5%–3.75% for the second consecutive meeting, citing economic uncertainty and inflation risks stemming from the conflict in Iran and rising oil prices.”

The psychology for the serfs is that doing nothing to stop inflation is actually proactive. The bar has been set by propaganda to a rate cut, that by the Federal Reserve’s own teaching would make inflation worse. The Federal Reserve has the masses eating out of their hand like Pavlov’s dog, happily salivating for nothing; and accepting being skimmed like the mafia mob at an old fashioned casino for 2% a year (target).

“And if the Fed is talking about rate cuts in this environment, it is clearly stoned.”

They are not stoned at all. They know what their master wants and they value their extremely cushy jobs.

Do you think these creatures want to get up on a freezing Winter’s morning, and drive to Walmart to spend 10 hours ringing up customers behind a cash register?

Do you think they want to work a shift in an Amazon warehouse?

Heck no. They’ve got it made. As long as they kowtow to whatever the current party line happens to be, a life of preference and privilege awaites them.

Watching today’s press conference — malpractice by the reporters not pressuring Powell on services inflation and letting him continue to characterize this as a goods and housing problem

Over a year ago inflation was going down, GDP very strong, job market good, sentiment strong. What have happen? What are the causes of the decline?

GDP growth in Q3 was HOT. In Q4 it was cold because government spending collapsed due to the shutdown. These not-spent funds are going get spent in Q1 and Q2, on top of the normal government spending, and government spending will jump. We discussed at the time. Should have read that GDP article.

Consumer spending was fine in Q4 despite the chaos of the government shutdown.

“stoned” is one way to look at it. Clueless lackey spittle is another.

“James Bullard, former St. Louis Fed president, believes that while headline inflation may rise due to oil price shocks, core inflation, which excludes food and energy prices, is not expected to increase significantly. He suggests that stable inflation expectations will help mitigate the overall impact on inflation from rising oil prices.” There lots more comments like this today but yahoo has exorcised those mostly since the PPI news broke.

What is your definition of a strong job market and what time horizon?

UE is 4.4% which is near all time lows. 25-54 labor force participation is 83.9 which is near all time highs.

Exactly! Raise those damn rates!

The market is going to force the Fed’s hand, and may already be, but then again, The Fed, and the Federal Reserve Note, may be becoming irrelevant anyway.

Well,have personally seen the diesel/gas prices rise so that will add fuel to the fire(pun intended),feel the mideast situation does not cool soon will get much worse,have a full pantry at minimum.

“And if the Fed is talking about rate cuts in this environment, it is clearly stoned.”

Powell said he is a big fan of the Grateful Dead. If you have ever been to one of their concerts, you will leave stoned out of your mind, whether you were smoking or just breathing.