US Government sold $651 billion of Treasury securities this week into these rising yields.

By Wolf Richter for WOLF STREET.

It was a rough week in the Treasury market and the mortgage market. Inflation fears spread amid surging gasoline prices and some lousy inflation data that don’t even yet include those surging gasoline prices: The Fed-favored core PCE Price Index for January rose to 3.1%, worst in nearly two years, when the Fed’s target for it is 2%. And worries cropped up about the deficit as the financial costs of the war in Iran would have to be borrowed, and reluctant new buyers would have to be enticed by higher yields to buy that debt.

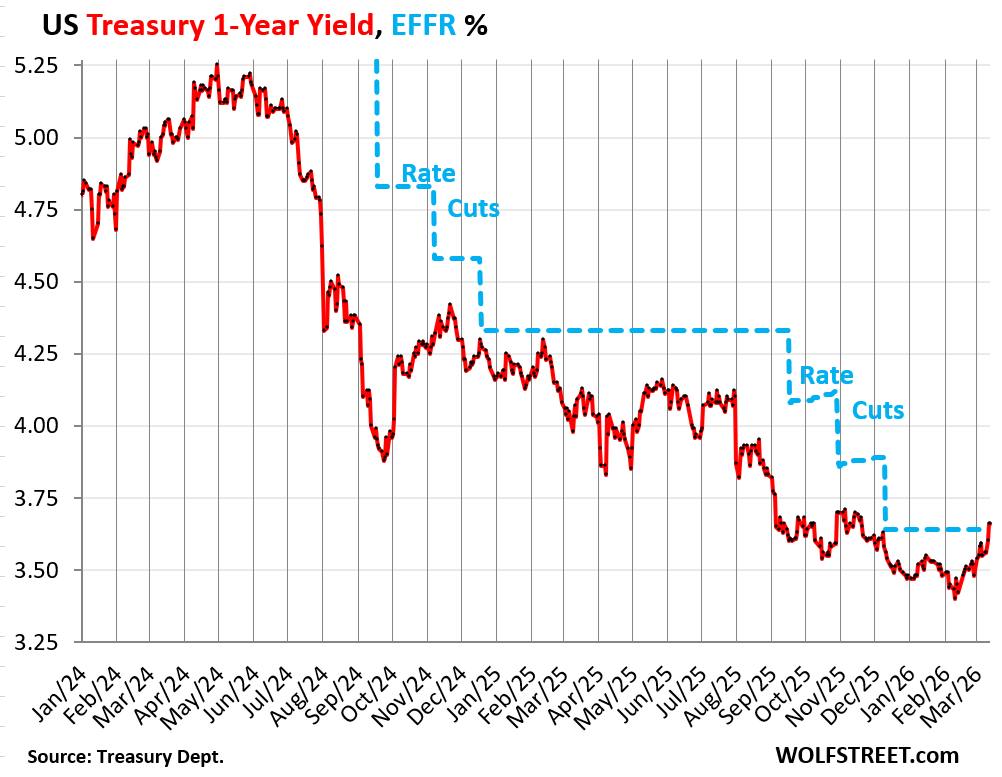

The 1-year Treasury yield squeaked over the Effective Federal Funds Rate (EFFR, blue in the chart) on Friday for the first time since November 2023, which had been nearly a year before the Fed even cut its policy rates. The EFFR is the overnight rate the Fed targets with its policy rates; and with the 1-year yield now at it, the bond market has moved rate cut expectations off the table for this year.

All Treasury yields across the yield curve, including all short-term maturities, are now at or above the EFFR, indicating that, for the bond market, rate cuts are essentially not in the scenario anymore.

The US government sold $651 billion of Treasury securities this week, spread over nine auctions, including 10-year Treasury notes and 30-year Treasury bonds.

Of these auction sales, $532 billion were Treasury bills, with maturities from 4 weeks to 26 weeks, most of them to replace maturing T-bills.

| Type | Auction date | Billion $ | Auction yield |

| Bills 4-week | Mar-12 | 101 | 3.640% |

| Bills 6-week | Mar-10 | 95 | 3.635% |

| Bills 8-week | Mar-12 | 91 | 3.625% |

| Bills 13-week | Mar-09 | 94 | 3.605% |

| Bills 17-week | Mar-11 | 70 | 3.600% |

| Bills 26-week | Mar-09 | 81 | 3.535% |

| Bills | 532 |

And $119 billion of Treasury notes and bonds were sold this week.

| Notes & Bonds | Auction date | Billion $ | Auction yield |

| Notes 3-year | Mar-10 | 58 | 3.579% |

| Notes 10-year | Mar-11 | 39 | 4.217% |

| Bonds 30-year | Mar-12 | 22 | 4.871% |

| Notes & bonds | 119 |

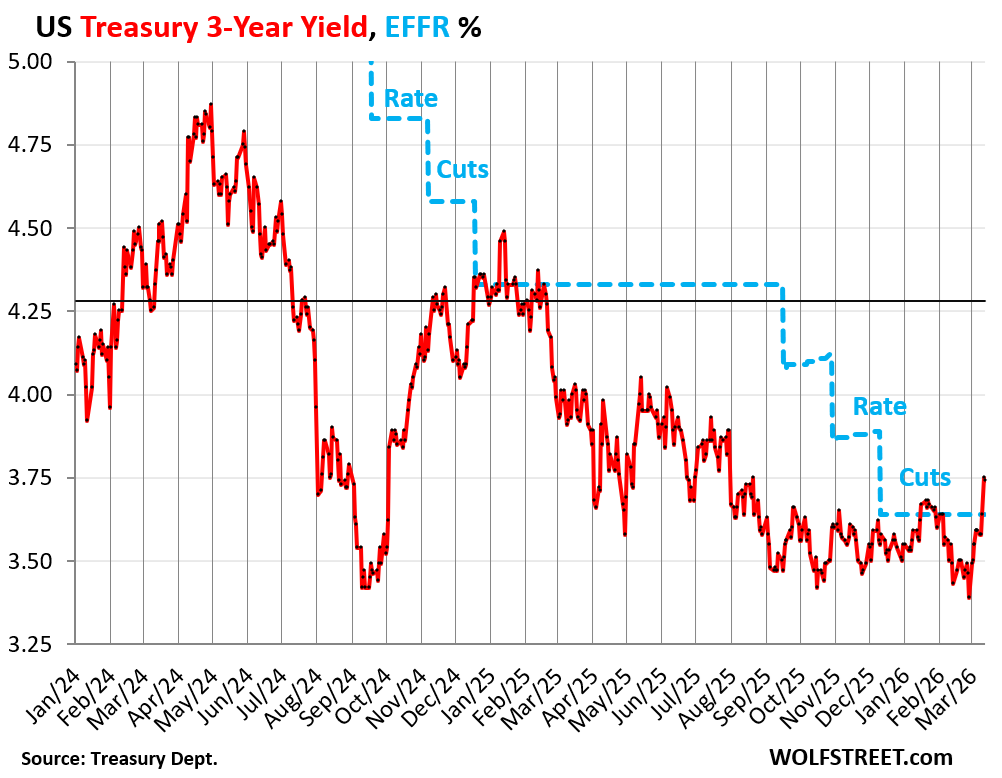

The 3-year Treasury notes sold at auction Tuesday morning at a yield of 3.58%. In the secondary market, the 3-year yield continued to rise for the rest of the week and by Friday closed at 3.74%, having jumped by 16 basis points since the auction. And it brought the yield spike over the past two weeks to 36 basis points. That’s a lot.

The issue with the 3-year maturities in the secondary market was in January and February, when they rallied ferociously (prices rose, yields fell) amid deafening Wall Street propaganda that the 3-year maturities were the sweet spot for whatever reason and that everyone needed to pile into them, and they did, and by February 27, the yield had dropped to an inexplicably low 3.38%. But then the propaganda died, the 3-year maturities sold off, and the yield spiked by 36 basis points in two weeks, the most of any Treasuries in that two-week period.

The three-year yield is kind of a bad deal for yield investors, though it can be a good deal for leveraged price speculators, if they can get out quick enough, which is maybe why it got hyped by Wall Street. The 3-year yield lagged the rate hikes in 2022 and 2023 (prices didn’t drop as much), and then it front-ran the rate cuts (prices fell faster sooner). But then at the end of February, it flipped and the yield spiked as these leveraged speculators tried to get out.

And from another point of view: The spike of the 3-year yield above the EFFR suggests that the possibility of rate hikes next year might be starting to worm its way into the scenario.

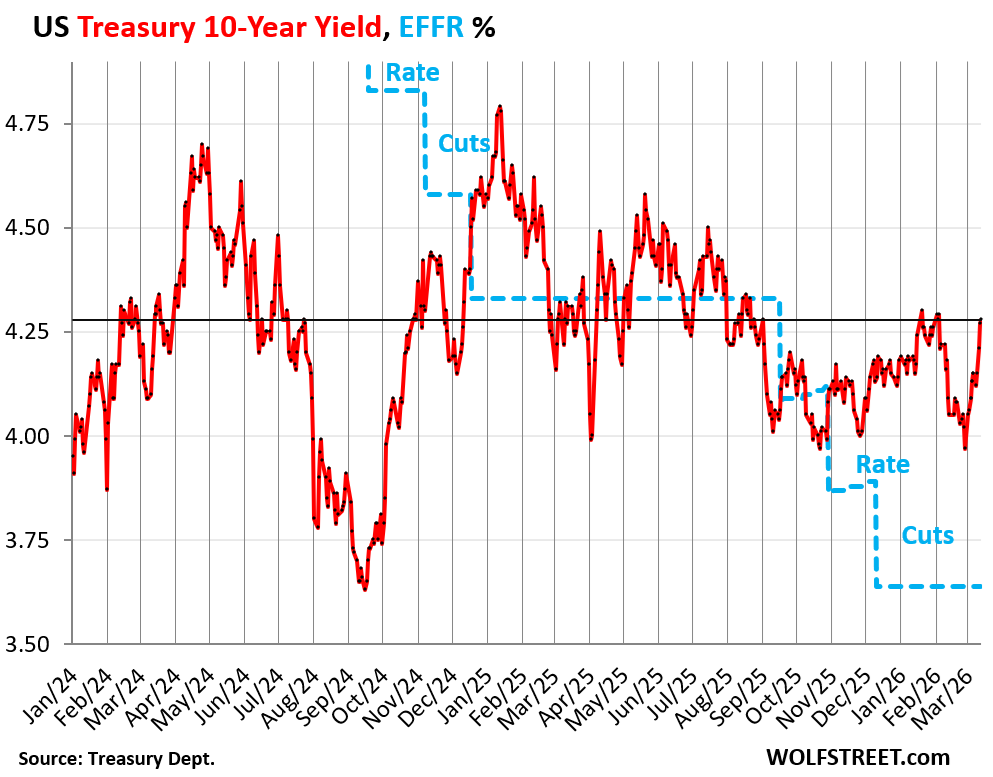

The 10-year Treasury yield rose to 4.28% by the close on Friday, the highest since early February, having risen by 13 basis points during the week.

A week ago on Friday, it had closed at 4.15%. At the 10-year Treasury note auction on Wednesday, they priced at 4.22%. There was nothing panicky about this, just a grind of higher yields and lower prices.

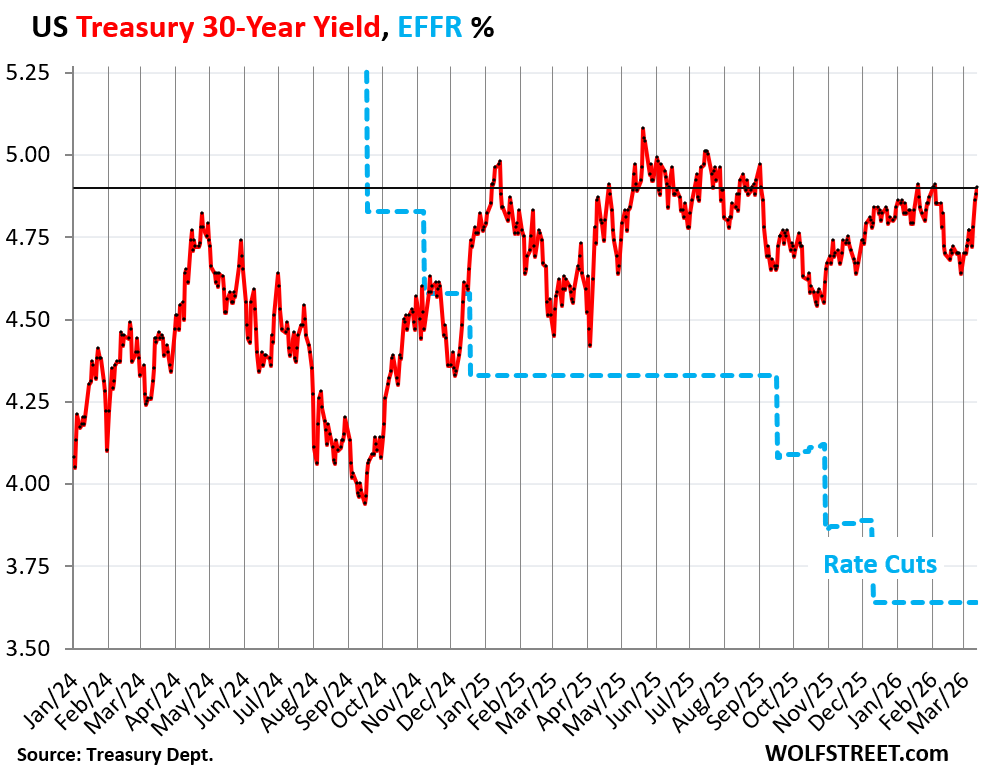

The 30-year Treasury yield rose to 4.90%, the highest since, well, one day in January, and one day in February, and before those two days, the highest since September, three rate cuts ago.

Buyers of the long bond aren’t focused on overnight policy rates. They’re worried about the next 30 years, about inflation during those years that would eat the purchasing power of their investment whose interest payments could be too low to compensate them for it; and they’re worried about even higher long-term interest rates in the future that would tank the market price of their long bonds if they try to sell them before they mature. Three decades is a long time for things to go wrong. And they want to be paid for taking that risk.

At the 30-year bond auction on Thursday, they priced at 4.87%, and in the secondary market, the 30-year yield continued to rise to 4.90% on Friday.

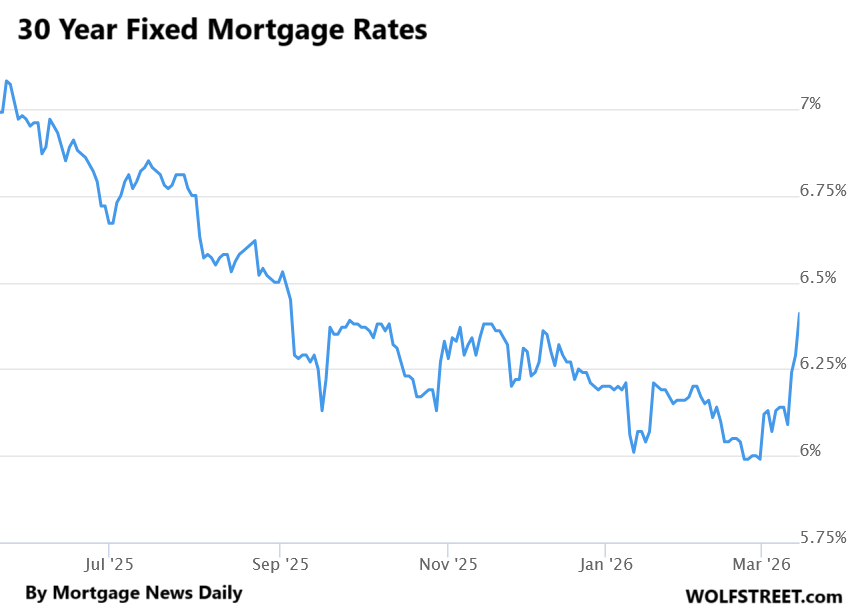

And mortgage rates spiked to 6.41%. The daily measure of the average 30-year fixed mortgage rate by Mortgage News Daily spiked by 27 basis points this week to 6.41% on Friday, the highest since early September, after having jumped by 14 basis points in the prior week.

Over the past two weeks, the daily measure of mortgage rates has spiked by 42 basis points, from 5.99% to 6.41%. The ballyhooed adventure below the 6% line was brief and shallow, and the snapback vicious.

Mortgage rates key off the long-term Treasury market, not the overnight rates targeted by the Fed’s policy rates. They roughly track the 10-year Treasury yield but are higher, and that spread between them varies.

The announced buybacks of MBS by Fannie Mae and Freddie Mac are supposed to shrink that spread, and thereby bring down mortgage rates, and they did that to some extent for a little while. But they cannot do anything about the bond market, and might increase the worries in the bond market as the two GSEs have to shed their Treasury holdings to get the cash to buy the MBS.

In case you missed it – and it’s going to get harder with mortgage rates back at 6.4%: What it Takes to Sell Homes in this Market: Lennar Cuts Average Selling Price to 2017 Level

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The way things are going now, the 10-year US Treasuries and mortgage interest rates will just continue to soar upwards with no end in sight.

MW: It was ‘unthinkable’ a couple of weeks ago, but could the next move by the Fed be a rate hike?