Domestic private demand, without government and trade, rose by 2.4% adjusted for inflation.

By Wolf Richter for WOLF STREET.

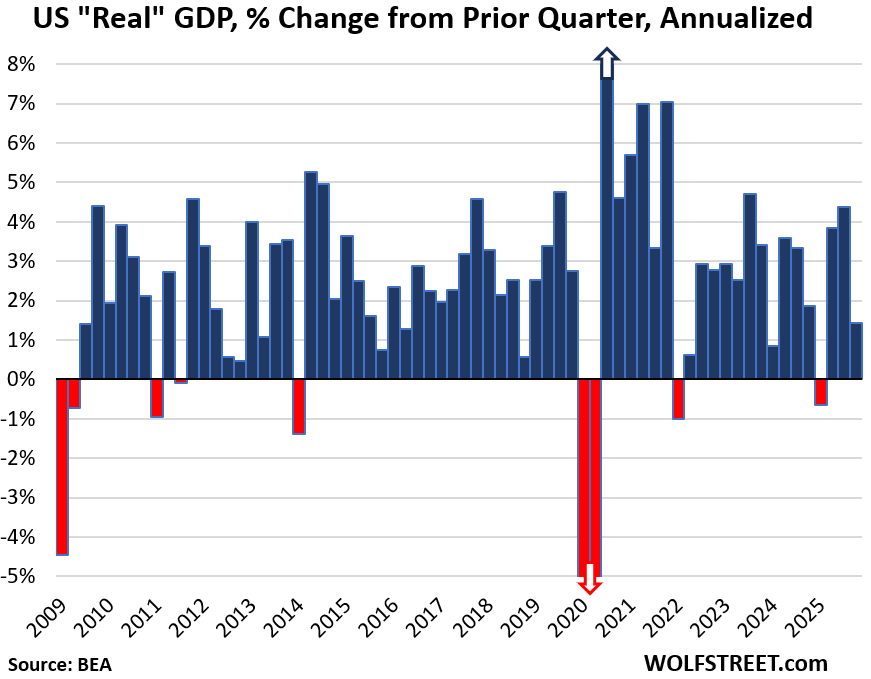

Gross Domestic Product, the broadest measure of spending and investment in the economy, grew by an annual rate of 1.4% in Q4, adjusted for inflation (“real” GDP), after the 4.4% growth in Q3, and 3.8% growth in Q2, according to the Bureau of Economic Analysis today.

Accelerating inflation was a big factor, and the inflation adjustments were the highest in two years. Not adjusted for inflation, “current dollar” GDP rose by 5.1%.

The other big factor was the plunge in federal government spending and investment due to the longest government shutdown in history.

What slammed “real” GDP?

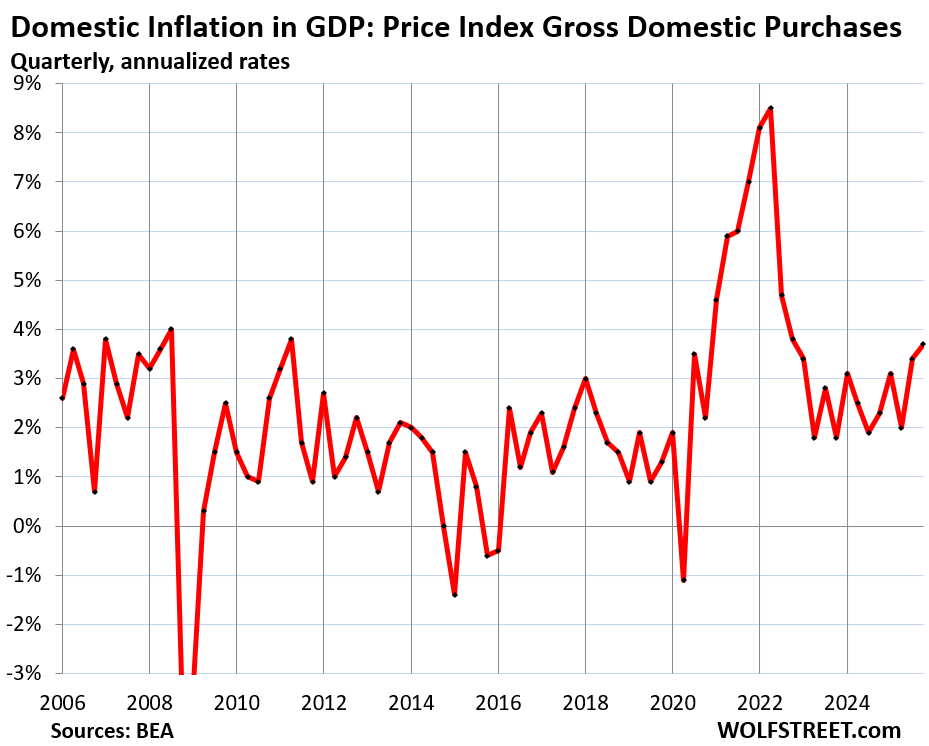

Hot inflation adjustments. The inflation measure for the overall economy, the GDP Price Deflator rose by 3.7% in Q4, after having already risen by 3.7% in Q3, both the hottest since Q1 2023.

The Price Index for Gross Domestic Purchases, which reflects inflation adjustments in GDP except for imports, so domestic inflation, accelerated to 3.7% in Q4, the worst in three years.

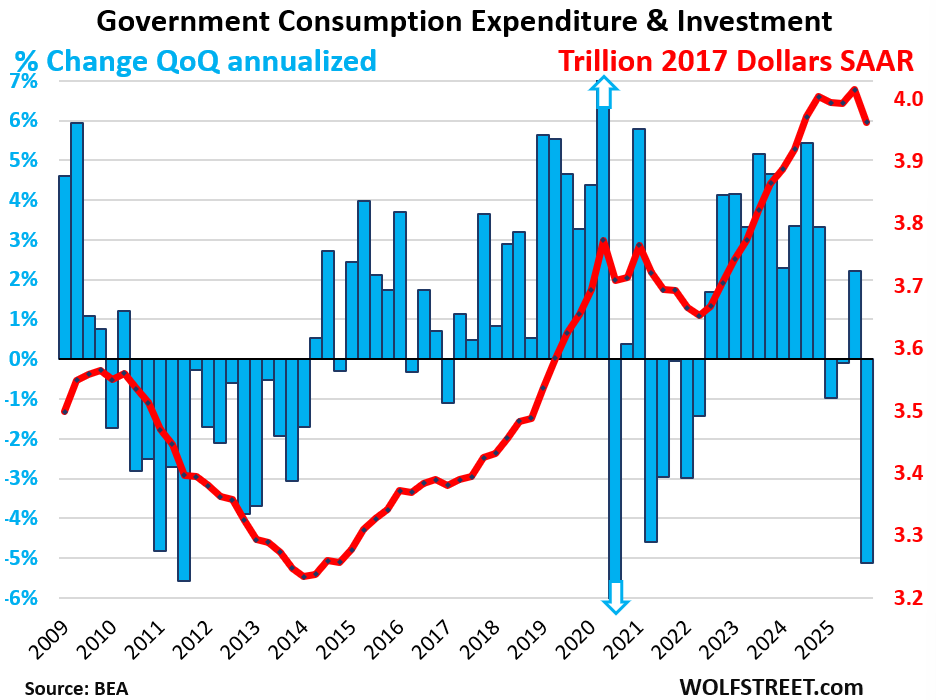

Plunging federal government spending hit real GDP. Government consumption expenditures and gross investment plunged by 16.6% as a result of the longest government shutdown in history: Nondefense spending collapsed by 24.1%. Defense spending plunged by 10.8%.

The plunge in federal government spending subtracted 1.15 percentage points from real GDP growth of 1.4%. That’s a huge hit.

This does not include interest payments. And it does not include transfer payments directly to consumers (the biggest part of which are Social Security payments), which are counted in GDP when consumers and businesses spend these funds.

State and local government spending rose by 2.4%, and contributed 0.25 percentage points to GDP growth.

Combined, federal, state, and local government consumption and investment fell by 5.1% and reduced the GDP growth rate by 0.9 percentage points.

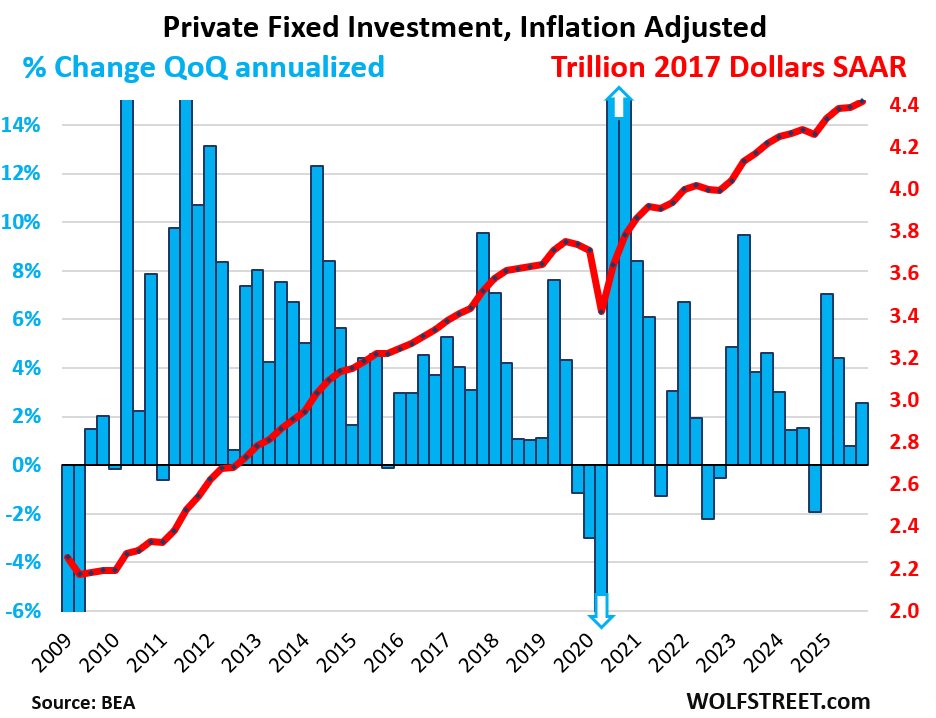

The blue columns show the growth rates (left axis), the red line shows the dollars (right axis), all in seasonally adjusted annual rates (SAAR):

What boosted GDP?

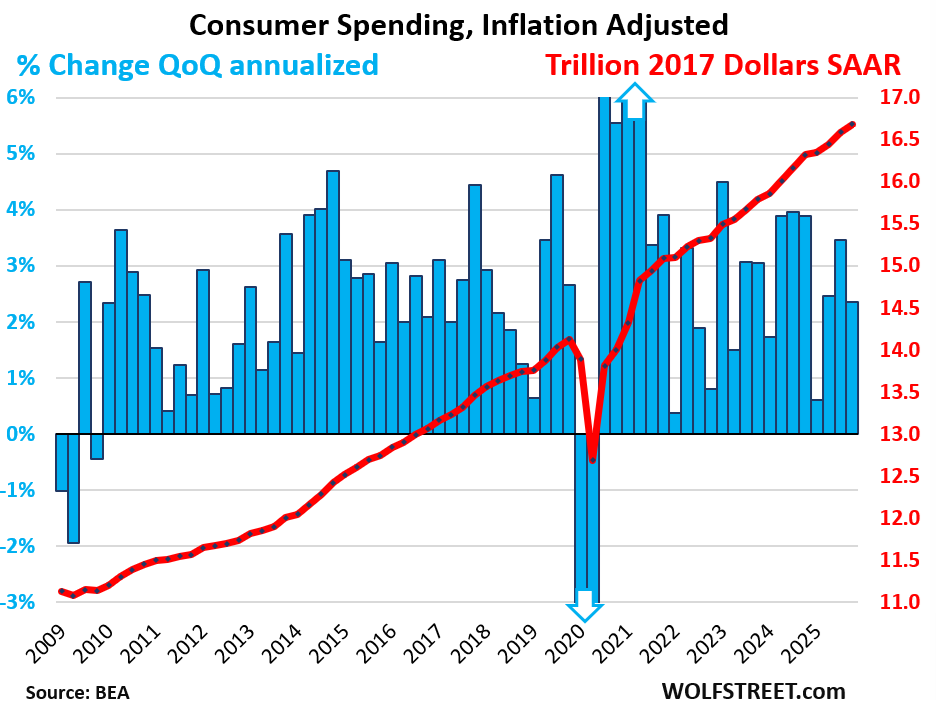

Consumer spending boosted GDP growth. Adjusted for inflation, personal consumption expenditures rose by an annual rate of 2.4% in Q4, despite the government shutdown that had rattled so many nerves.

This growth rate added 1.58 percentage points to the GDP growth of 1.4%.

Consumer spending accounted for 69% of the US economy.

The spending growth came from services (+3.4% adjusted for inflation), with spending on goods dipping a hair (-0.1%):

The blue columns show the growth rates (left axis), the red line shows the dollars (right axis), all in seasonally adjusted annual rates (SAAR):

Private fixed investment boosted GDP growth, rising by 2.6% in Q4, adjusted for inflation. Of which:

- Nonresidential fixed investments: +3.7%:

- Structures: -2.4%

- Equipment: +3.2%.

- Intellectual property products (software, movies, etc.): +7.4%.

- Residential fixed investment: -1.5%.

Private fixed investment accounted for 18% of the US economy.

Trade deficit improved and boosted GDP. Net exports (exports minus imports) were the least bad since Q4 2023 and improved by 11% from Q4 a year ago.

Imports dropped by $12.2 billion from the prior quarter, adjusted for inflation, with imports of goods dropping by $20 billion.

Exports fell by $6.3 billion.

And “net exports” (exports minus imports) improved by $5.9 billion, adjusted for inflation, the third consecutive quarter of improvements. The Q1 trade deficit had been the result of massive frontrunning of the tariffs.

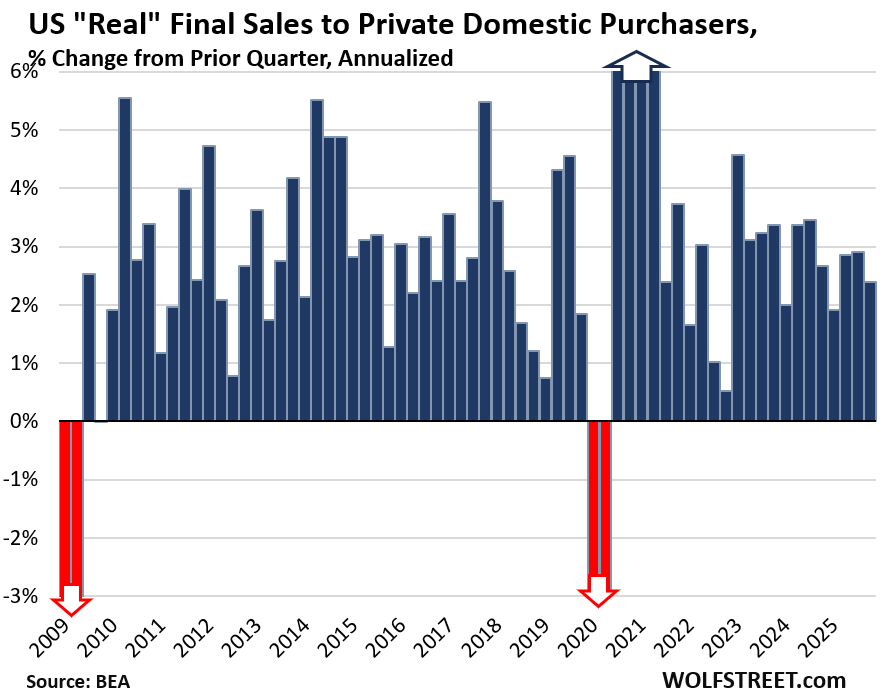

GDP without government and trade deficit.

“Real Final Sales to Private Domestic Purchasers” rose by 2.4% in Q4, adjusted for inflation. Solid domestic demand, despite the big inflation adjustments and the jitters caused by the government shutdown.

The measure is part of the GDP report today and tracks demand in the private US economy. It excludes exports, imports, government consumption expenditures and investment, and changes in inventories. It covers about 87% of GDP and represents the core of the private US economy.

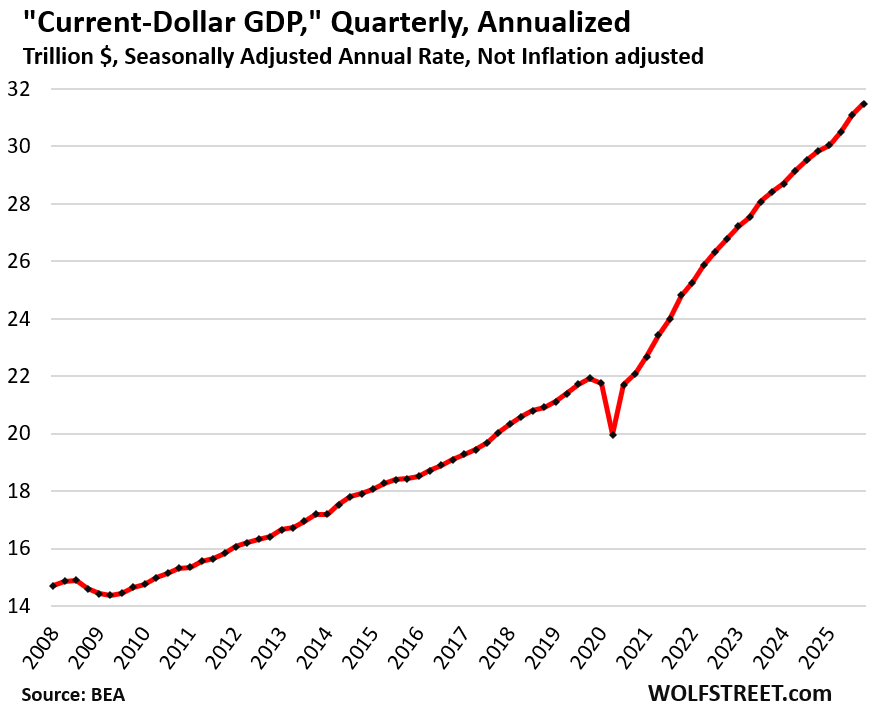

Not adjusted for inflation, “current-dollar GDP” grew by an annual rate of 5.1% to $31.5 trillion, after the 8.3% growth in Q2.

This “nominal GDP” represents the actual size of the US economy in current dollars and forms the basis for the Debt-to-GDP ratio and similar GDP-based ratios.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

This is the only place to get real facts. Thank you

With tariffs under the International Emergency Economic Powers Act now eviscerated, unless the Trump admin can make good on their prediction/promise that they will find other statutes to support executive- ordered tariffs – the trade deficit will go back up, maybe to even higher levels.

They have lots of other options, one of which Trump already invoked, section 122 tariffs, as explained in the opinion of dissenting justice Kavanaugh:

“The decision might not substantially constrain a President’s ability to order tariffs going forward. That is because numerous other federal statutes authorize the President to impose tariffs and might justify most (if not all) of the tariffs at issue in this case—albeit perhaps with a few additional procedural steps that IEEPA, as an emergency statute, does not require. Those statutes include, for example, the Trade Expansion Act of 1962 (Section 232); the Trade Act of 1974 (Sections 122, 201, and 301); and the Tariff Act of 1930 (Section 338). In essence, the Court today concludes that the President checked the wrong statutory box by relying on IEEPA rather than another statute to impose these tariffs.”

The slope change of the “Current-Dollar GDP” curve from pre-2020 to post-2020 is frightening, considering that population is growing *much* slower post-2023.

Wolf, what is your explanation for the 3 month divergence between CPI (now 2.4% annualized and falling) and PCE (now 2.9% annualized and rising). Usually these two metrics follow each other around, but lately they are splitting and going different directions.

The doctored OER in CPI. I have written about it several times.

OER is also in PCE, but with at much smaller weight, with a weight of only about 10% or so, instead of 26% in CPI. All housing combined weighs only about 16% in PCE, v 35% in CPI. But PCE includes things that are not in CPI.

How will the tariff reimbursements work out in the trade deficit / surplus calculations?

The amount reimbursed doesn’t figure into the trade deficit figures. The tariffs collected also don’t figure into the trade deficit figures. They all figure into the budget deficit figures.

Trade deficit and budget deficit are two separate but huge deficits.

The administration should embrace this decision though I wish the court would have ruled much sooner.

The 10% for 150 days or whatever is fine. Some tariffs are fine as well.

Time for stability