The high-risk, high-profit ecosystem of subprime auto loans is not for the squeamish.

By Wolf Richter for WOLF STREET.

Subprime doesn’t mean “low income.” It means “bad credit” – not paying bills, falling behind on debt payments, piling on too much debt, etc. That young dentist getting into it over his head is a classic example of high-income subprime: big house, expensive cars, student loans, etc., and then he falls behind.

The descent into subprime can be quick. The exit is slow: Getting current, paying down debt, paying everything on time, and gradually the credit score moves back up. Subprime for most people is temporary.

Subprime is only a small part of auto sales.

Of all $1.67 trillion in auto loans and leases outstanding, only about 14% were rated subprime and deep-subprime at the time of origination, according to Experian data.

But in terms of total auto sales, including cash deals – rather than just loans and leases – it’s even less.

Of all used vehicles sold in Q3 2025, only 35% were financed. Of that 35% with financing, 22% had subprime rated loans, according to Experian, which tracks this by liens on titles in the registrations data. In other words, of all used vehicle sold, including cash deals, only 7.7% were financed with subprime loans. It’s just a small part of auto sales.

Of all new vehicles sold in Q3 2025, 81% were leased or financed. Of these leases, fewer than 4% were subprime; and of these loans, 6% were subprime. It’s just a really small part of auto sales.

Subprime is largely handled by specialized dealer-lenders or specialized lenders.

It’s high risk, and high profit, with lots of ugly parts to it, including components of recklessness by the specialized industry and by borrowers, and is not for the squeamish. Subprime deals come with very high interest rates and very high prices on the vehicles. Dealers and lenders want to be compensated for taking the massive risks involved in lending to borrowers who have a history of stiffing their creditors, which is how they got to be subprime.

Subprime dealer-lenders routinely blow up, sometimes amid a mushroom cloud of fraud allegations, such as Tricolor last year. PE firms got into the subprime dealer-lender business, and some of those chains collapsed.

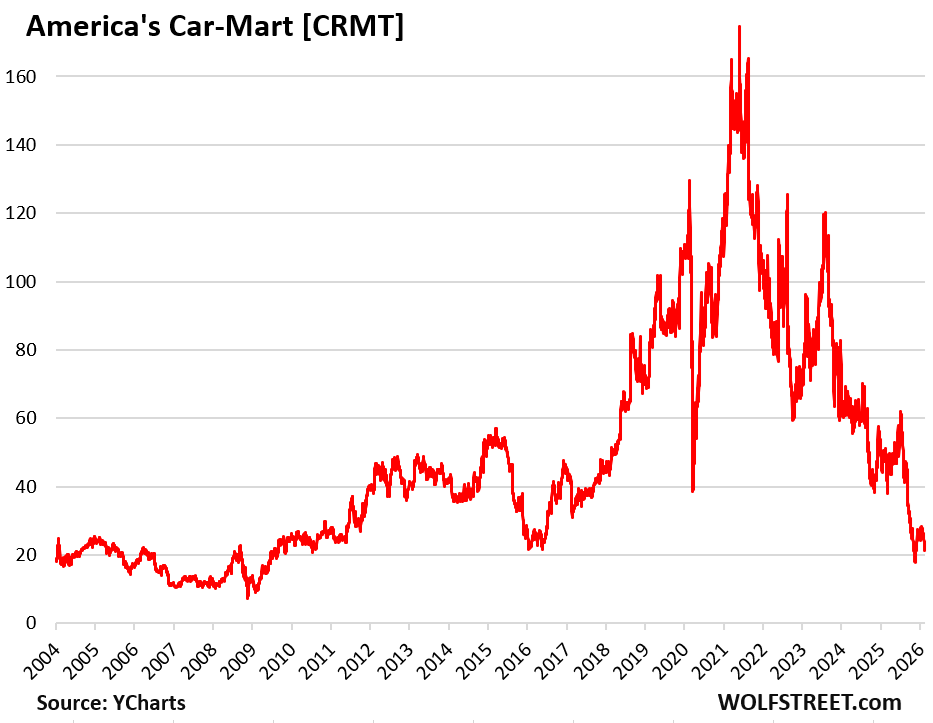

Publicly traded subprime dealer-lender chain America’s Car-Mart [CRMT] got hit, and we featured it here in December 2023 when it began confessing to its issues. At the time, the stock had tanked by 61% from its high in May 2021.

The stock has since then plunged further, and today is down by 88% from its peak, and is back where it had been over 25 years ago. It has been in our pantheon of Imploded Stocks for a while, and it shows the high-risk, high-profit nature of the subprime business (data via YCharts):

Subprime depends on securitization. Banks and non-bank lenders don’t carry subprime loans on their books; they’re way too risky. The specialized dealer-lenders and specialized lenders securitize the subprime auto loans into Asset-Backed Securities (ABS) and sell the slices to institutional investors around the world, such as bond funds and pension funds.

The lowest-rated slices of the ABS take the first losses, but also offer the highest yield. When things go wrong, they can get wiped out quickly. Their job is to protect the highest-rated slices of these bonds. So when losses occur, they’re spread across investors that got paid the most to take those losses. But even higher-rated slices have gotten hit.

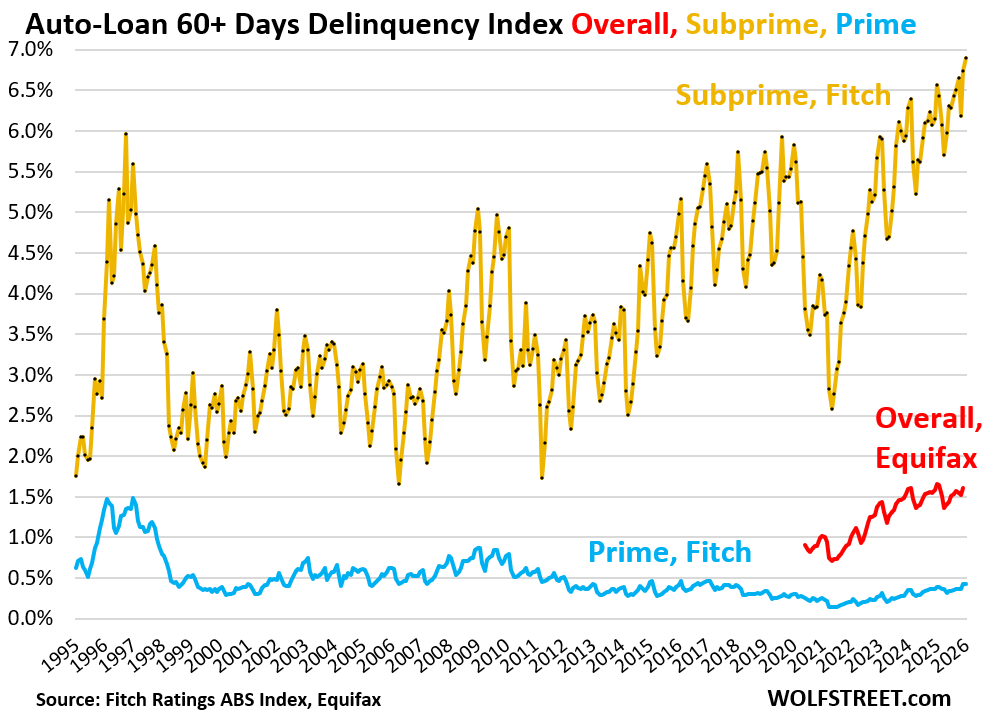

Delinquency rate of subprime auto-loan ABS hit a new high.

The 60-day-plus delinquency rate of subprime auto loans that have been packaged into ABS rose to a record 6.9% in January, according to Fitch Ratings, which rates these ABS (yellow in the chart below).

The delinquency rate is very seasonal, and January is nearly always the high of the year. Compared to January 2024, the delinquency rate was up by 34 basis points (from 6.56%).

But “prime” auto loans are nearly always in pristine condition. The 60-plus-day delinquency rate of prime auto loans that were packaged into prime ABS tracked by Fitch remained at 0.4% in January, same as in December 2025, and same as in January 2018. Even during the Great Recession, the prime delinquency rate maxed out at only 0.9%. There was a bigger problem in the mid-1990s, when securitizing auto loans became a big thing and the nascent industry was climbing up a learning curve (blue in the chart).

The 60-plus-day delinquency rate for all auto loans and leases ticked up 1.61% in December, the latest data available from Equifax. The recent high had been 1.66% in January 2025.

During the Free-Money era of the pandemic, delinquency rates had dropped below 1%. But the monthly Equifax data that is available doesn’t go back further than the low point of the Free-Money era and therefore lacks the comparison to the pre-pandemic normal years (red in the chart below).

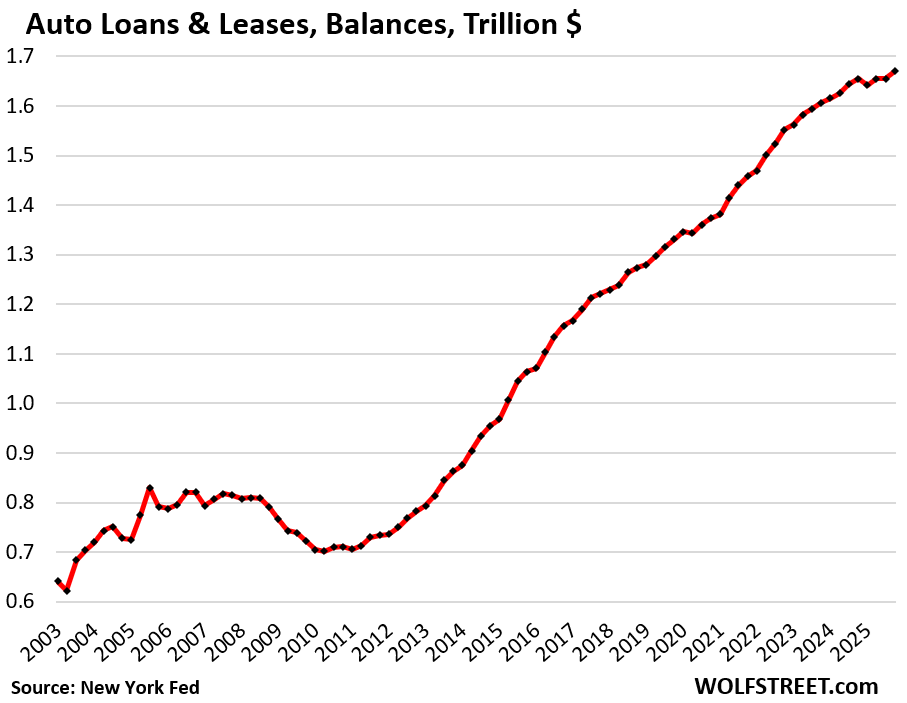

Total balances of auto loans and leases for new and used vehicles inched up by $15 billion year-over-year and for the quarter, to $1.67 trillion, after the dip in Q1 and the flat reading in Q3, according to the New York Fed’s report on consumer credit, based on Equifax data.

The reason auto loan balances surged by 23% in the five years of 2020-2024, despite lower vehicle sales, is that prices of new and used vehicles had spiked.

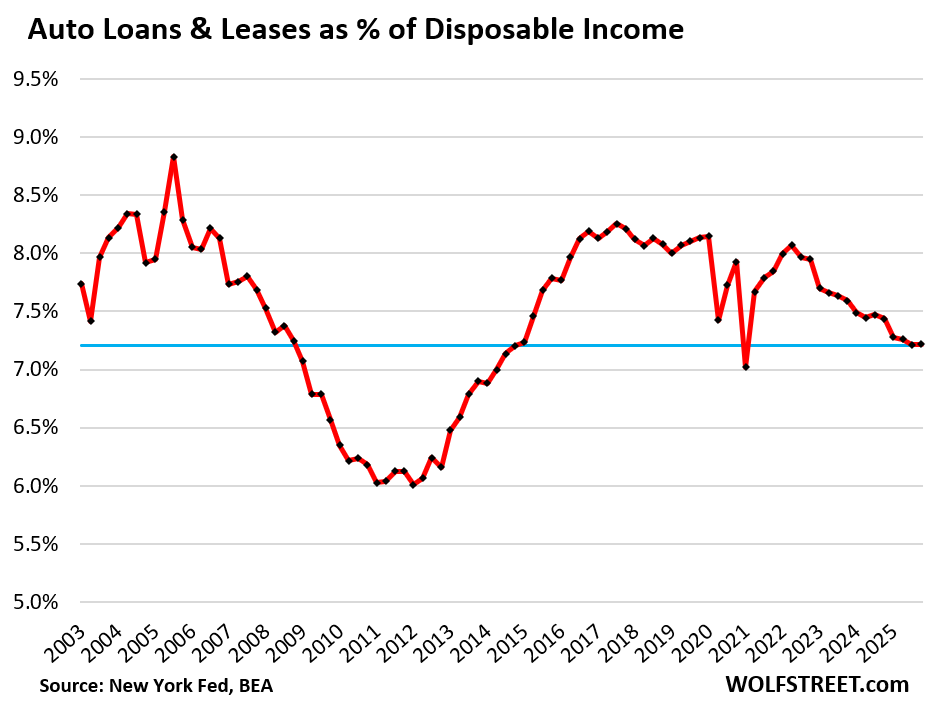

The burden of auto loans and leases — in terms of the debt-to-income ratio, a classic way of evaluating the burden of a debt — is lower than it had been before the pandemic because consumers’ disposable income has risen faster than the balance of auto loans and leases.

The auto-loan-to-disposable income ratio in Q4 was unchanged at 7.2%, the lowest since 2014, except for Q1 2021, when stimulus payments distorted disposable income into absurdity.

Disposable income, released by the Bureau of Economic Analysis, is the monthly after-tax income consumers have available to spend for their daily costs of living, to service their debts, and to save and invest the remainder. So after-tax wages, plus income from interest, dividends, rentals, farms, small businesses, transfer payments from the government such as Social Security, etc.

But it excludes income from capital gains, which is where the super-wealthy make most of their money. And this upper crust of income is excluded here and doesn’t skew the data.

In case you missed them: Here Come the HELOCs: Mortgages, Housing-Debt-to-Income-Ratio, Serious Delinquencies, and Foreclosures in Q4 2025

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Typhoid initially effected the poor neighborhoods in NYC, than Typhoid Mary, brought it uptown to the super rich. Credit problems will move up the ladder to the richest neighborhoods, as wealth collapses problems will be obvious. The storm is here.. great description above Wolf in explaining the sub prime auto issues. Typhoid Mary today is blind greed for more without regards to risk.

I don’t see how only 35% of used vehicles are financed

today a 10 year old vehicle with 100,000(say toyota) is fetching upwards of $25,000++

65% of used vehicle buyers have that much cash??

or is it access to say HELOC

1. 10-year-old Toyota Camrys with 100k miles run between $9,000-$14,000, including at overpriced CarMax in SF Bay Area — not $25,000+ I also see a Camry for $6,000 with 200k miles. And US brands are cheaper, for example, Ford Fusion SE, 2016, 78K miles $7,000. Toyota has only a small slice of total used vehicle sales.

2. You belong to the people that think that most Americans are struggling or poor, which is ignorant BS, and that only poor people buy used vehicles, which is ignorant BS.

3. You should read some of the articles here about the many trillions of dollars in interest-earning cash that households are sitting on, in addition to their 401ks and other stock and bond holdings.

4. Lots of people pay cash for their used vehicles, including us. Many more people are doing it now since used-vehicle interest rates are relatively high, so it makes lots of sense to pay cash. And the percentage of cash buyers has risen over the past four years for that reason.

5. Like many people, we buy 2-3-year-old used vehicles because financially, they’re a much better deal than a new vehicle. The value of a new vehicle drops by many thousands of dollars the moment you buy it, when it becomes a used vehicle. That doesn’t happen with vehicles that are already used.

6. It’s stupid to use a HELOC to buy a car (the home is the collateral, and you can lose the home over it), rather than financing the vehicle (the vehicle is the collateral, and you can lose the vehicle). In addition, HELOC interest rates are about the same as the interest rate on 60-month used-vehicle loans. Rates vary for both depending on lots of factors, including credit rating.

The guy asked a civil question and got an uncivil answer.

No, he didn’t ask “a civil question.” Read his comment!!!! He made a statement, “I don’t see how only 35% of used vehicles are financed.” This statement called the registrations data I cited a liar because the registrations data didn’t fit his silly narrative. This registrations data reflect liens recorded on the titles issued to the buyers after the sale. That’s hard data. You don’t get to argue with that just because it doesn’t fit your narrative. I explained that in the article.

Wolf!! I agree with you. There is this media projection saying Americans are the poorest folks in the world. Many think Americans live paycheck to paycheck. Despite my admiration to Sanders, this is one of few things I disagree with him. Last 30 years he kept saying “paycheck to paycheck”. 62% Americans have done form of equity. With Trump accounts it could become 98% all will have equities.

Buying a 2-3-year-old used Camry may work out for many, but it being a much better deal is somewhat subjective. The new Camry will depreciate up to15% when you drive it off the lot, but the used Camry will depreciate up to 10% when you drive it off the lot. Since the new Camry comes with three years of warranty, and is simply newer, on average you will have more years without inconvenient, and costly, breakdowns on the road. Plus, if you maintain your car properly, you can hold on to it for more years and not worry about having inherited a used car with someone else’s years of abuse.

The podiatrist’s car that invented the arch support for Dr. Scholls was 7 years old. But he owned 4 1/2 miles of shoreline along the Lake of the Ozarks. And his living room had fishing poles from one end to the other.

Not everyone wants a Camry. Luxury cars depreciation curves are far steeper first 3-5 years.

A lot of folks do buy used cars with warranty remaining and you are right there maybe a bit of premium remaining in the price.

It’s well known depreciation curves flatten a lot after 3-5 years.

There used to be a time when buying slightly used (1-2 years) was looking at a 25%+ discount off MSRP, but that may be hard to come by for popular daily drivers these days.

Yeah…

I don’t understand why so many people seem to like the narrative that the average American is struggling and poor.

Sure there are significant problems that need to be addressed, and there are struggling and poor people, wealth gap problems, etc.

I guess maybe people just consider the average person to be riding the “struggle bus” if compared to an ultra wealthy billionaire.

Even if that “struggle bus” was used and was paid for in cash.

Haha

I also buy 2 to 3 year old vehicles which are certified from reputable dealers here in the area. I got my Mitzibushi 2020 Mirage for $11,700. It was in mint condition with 60K miles on it, and came off the lease program in Kansas City MO. I paid cash from the proceeds of the accident settlement with GEICO.

Yikes! What did it replace?

What? Do you get poor or adopt bad financial habits if you shakes hands (the horror) with someone that is?

Subprime isn’t always greed. Sometime life doesn’t always work the way you planned and some don’t have big safety nets. “Live within your means”….you can do that and still default on debt.

The small percentages show blind greed is not at play.

It was just an analogy for the credit bubble popping, the whole world will be affected. Larry Ellison signed a personal guarantee for 40b, his real wealth may be illiquid and he may be unable to pay his debt. We are so deep into this credit bubble, people think the rich won’t be affected. They are going to get hammered when the bubble pops, the next fed chairman doesn’t believe in QE. It’s going to get real, it already started. So much risk was bought with borrowed Yen, we are so close to the yen carry trade unwind! No one is coming to bail the USA out, world order has shifted away from us as a leader. No predictably anymore. When I said blind greed it referred to parabolic credit growth with the belief in central banks will always have the put, the rescue. Wolf said we can’t default in our own currency, but we can default in the value of the US dollar. Think of our equity market as a levy that holds the world’s liquidity, the levy is failing and liquidity is returning home back to the world. Liquidity is leaving us. We will be left with the fixed debt minus tens of trillion in liquidity. I imagine the spy will close under 677 tomorrow and the day after the race will be on to sell America. Americans are sending their liquidity overseas. The SP 500 is underperforming the global Dow since Jan 2025 and will underperform for a long time. After the state of the union what will happen next week? That’s a huge risk, the words of the POTUS creates liquidity movement. We are giving away decades of goodwill in my view of reality, like private equity when you write down enough goodwill the game is up, you are left with an insolvent investment. Paying debt back becomes really hard without goodwill. Sorry if I wasn’t clear, I m not great writer:) yeah I sound like a doomer but it’s the reality i see. It’sTakes time to start to de leverage, more people join in, than it all happens really fast. The time is right. A perfect storm.

Irving Fisher’s over indebtedness won’t lead to falling prices if the FED continues to validate prices. The price elasticity of demand will remain constant.

SPY closed at…686.29 today. You keep on dooming though.

Scott,

Yeah the yen ripped higher by 1% spy went up as a byproduct. What ever day the spy close under 677 the next day we get a series of down days, but BTC broke below 66.6k looking, it above now. When spy close below 677 btc will break below 60k with heavy volume. Looking at this Friday Option ex day.

Cheers proud Doomer :)

Sorry yen crashed by 1% $usdjpy ripped higher, ugh it’s like bond yield easy to make mistake.

Maybe today or tomorrow the yen will rip higher

*think it’s Affect, maybe?

Opps. That’s GILDING……Freudian handle-slip…..

Subprime doesn’t mean “low income.” It means “bad credit” – not paying bills

A fundamental distinction that hinders the society of trust that nourishes our lives. Poor people are often good credit risks.

As for Typhoid i think the Fed has come up with a cure for the rich. But who knows for sure

Pam Bondi used the Dow at 50k as a justification to protect the rich and powerful men who victimized our country’s teenage daughters for their pleasure with impunity. So mad!!! Maybe 2 handle on the Dow will allow justice! To be served! Will see what the PCE brings the Fed this week.

What were the excuses before Bondi?

Tom, Epstein died in Aug 2019 after Trump lost. Sleep joe was sleeping, Trump controlled the GOP during Biden term and the dems in congress got paid off by the perps. Congress just past the bill to release all the files. Why do think it’s being delayed? Interesting to hear other people’s opinion.

It’s the same nonsense that we heard from Biden and the media during his term.

72% of Americans when polled answered that the economy is only fair or poor. That means that a booming stock market doesn’t make the majority of Americans happy.

The issue is one of elites versus non-elites. Elites make most of their money from assets. The non-elite make most of their money from working.

Asset inflation is good for the elite, but not for the non-elite, as the money they earn from their job is worth less.

The elites only hang out with other elites, so they have a hard time internalizing that not everyone has millions in stocks.

At one point, a booming stock market was indicative of a booming economy for the average Joe/Main Street. Now it’s not. It’s an indicator of investor belief that the government has their back and won’t let stocks drop.

It’s hard to break old habits though, so the elite still equate a booming stock market with a booming economy.

Does she realize that one has to buy a stock when it is at 1, to take advantage of all 50,000 of the points?

Hahahaha

I.m not sure what financial typhoid for the rich is but if I had to guess it would be progressive income taxation combined with a wealth tax sufficient to sustain the society that made their good fortune possible

I’d make a lousy American. I’ve had only one “auto loan” in my life and I am now old as Methuselah. Come to that I’ve bought only one new car in my life.

I did buy a brand-new motorbike once but I used the money I’d earned from jobs in the summer holidays from secondary school; casual labour around the harbour – it’s handy being big and strong for your age.

Methuselah,

I agree with you ( and I may be as old). We generally buy a new car every 10-15 years. 15, if it has been reliable. We also sign up for the extended warranties and they have been worth it. Ie, my 2012 Jeep has a lifetime drivetrain warranty offered at the time and I’ve made my money back 3-4X. We generally save up over the 10-15 years and pay cash for the car.

However, car loans offered by dealers for new cars can make the decision financially more complex.

For example, GM offered the following on new cars last year:

1) 0% 60 month loan. No rebates

2) Pay cash. No rebates

3) 7% 48 month loan with a $1200 rebate and no prepayment penalty.

If I had to make the choice, I’d pick 1 and continue to TBill and chill making almost 4% on the cash for now. This would show up as an increase in Wolf’s excellent charts above on loan balances.

My second choice would be #3 and take the $1200 rebate and pay off the loan ASAP with no prepayment penalty.

The worst financial choice would be to pay cash out of my TBill accounts and not collect the TBill interest Or the $1200 rebate.

The payment method is done after you’ve negotiated the price so there isn’t any room to negotiate the deal by offering cash. The dealers don’t care and I think they get more of a corporate kickback if they sign you up for a loan.

I think it is more complex than a home mortgage.

My personal finance professor said the only thing to buy on time in your life was a house. He made a multimillionaire on a teacher’s salary.

Mainstream media headlines describe the subprime and delinquent auto loans with far more Doom than your simple numbers do.

Doom porn is far more exciting I suppose.

It is amusing, and perplexes me as to why so many people that are so well off, fixate on doom and gloom, and complain so much.

The morons in the media constantly conflate “subprime” with low income because that makes better clickbait. But subprime is just a credit rating, it means “bad credit,” it means a history of not paying their financial obligations.

7% delinquent of 14% of the loans is only 1% of the total impacted. Still extremely minimal but may be an early indicator.

Good point I can tell you from experience that being out of work sucks.

I’m here for the doomers that skipped the opening paragraph.

thanks you made me laugh :) I needed that.

I was actually referring to the private jet crowd who brag about their balance sheet of 8 homes who will be liquidating their Lambo and homes before this is done.

Doomer are like a broken clock with enough time they will be right! :)

Cheers!

Great info like always. Thanks Wolf. Best site on the web.

Wolf, there has been talk of legislation to cap interest rates on credit cards at 10%. A telling adjective you see in the legislation language is that high interest rates are “predatory”. Is this merely lip service to the pursuit of affordability when there is a clear (albeit risky, to your point) market for subprime loans? While these subprime loan rates look predatory, they also seem to be well justified based on the credit history of the borrower. Is it merely political optics when one source of high rates (credit cards) is targeted but another source (subprime loans) is not? Or am I missing something obvious? Thanks, as always!

If you think it’s anything other than optics ask yourself how they came up with 10%. Why not 8%, or 12%?

And by optics I mean politicians know it’ll never be enacted into law so they can say whatever they want and get credit for trying.

Gaston, that’s a good point and an obvious one I hadn’t considered. I don’t know why they proposed 10%. Personally, I’ve had the luxury of always being able to keep my credit card balances zero so I can’t truly empathize with this issue, but I can certainly sympathize with those who have emergencies that cause debt to pile up and 10% seems like a fair (albeit arbitrary, to your point) midpoint for the borrower and the lender.

And while I am not a pure optimist, I assumed that there would be more traction on the credit card rate cap now that both major parties have pushed for it (Bernie and AOC for the Dems, and Trump and Hawley for the GOP).

If they cap rates at 10% (they won’t), NO ONE will lend to higher-risk borrowers. People may have to have a credit score of 660 or higher to qualify for an auto loan (secured), and maybe 700 or higher to qualify for a credit card (unsecured).

Higher risk borrowers pay higher interest rates. That’s just how it is. Lots of companies are junk-rated, and they can still borrow, but they pay higher interest rates.

When the risk of default is substantial, lenders want to be compensated for taking those risks. If they’re not compensated for it, they won’t lend, and borrowers with lower credit scores will not be able to get any loans or credit cards at all.

If they cap interest rates at 21%, for example (like the old usury caps), it would only block the riskiest borrowers. So the impact would be small, but there would still be an impact.

Wolf, I hadn’t considered the security (secured versus unsecured) of the loans. Appreciate the insight!

I don’t believe in the elimination of usury laws when bankruptcy laws are tightened. We live in a predatory society.

Well firstly, who carries a balance on their credit card paying 21% interest.

It does not compute in my ability to understand

Spot on Wolf. 35 years ago divorce, bankruptcy, broke and needed a car. Dealer asked me what I did for a living. Military officer with 11 years active duty. Without other questioning he had his salesman show me 5 different 1 year old Saturns with similar mileage and said “pick one their all same price”. Was out of there in an hour and was happy with the 18%. I was about as subprime as one could get. It doesn’t necessarily mean poor risk and was indeed “temporary”

Used Car Market Key Trends (Early 2026)

Average Price: Kelley Blue Book reported an average listing price of $25,533 in January 2026.

Price Trends: Prices generally dropped in early 2026 following a rise in December, a normal seasonal trend.

Inventory & Availability: Supply remains constrained, with roughly a 46-48 day supply of vehicles.

Affordability: Vehicles priced under $15,000 are difficult to find.

Comparison to New Cars: The average new car price is over $49,000, making used cars, while expensive, a more budget-friendly.

Wife and I drive 2007 model year vehicles in Colorado with full coverage $250/$500 comp/collision insurance. Used cars are Gold mines right now for investors/sellers/buyers alike. Toyota and Honda products demand a higher price for resale. It’s been great to see a lot of folks getting forced into buying older used cars to lower insurance premiums and make affordable decisions. Gen Z and Millennials can attain more value from finishing the basement or adding additional rooms or renovations to the parents/grandparents property.

“Average vehicle” = buying too much vehicle in most cases. At least half of the people that get a truck or SUV never use its utility. Most would get by just fine with a cheaper hatchback, or even sedan.

If you want bigger then fine, that’s your prerogative. Don’t try and convince people you need it though; it’s your choice.

Per Wolf’s examples, a Camry or Fusion are both fine vehicles.

What the 10-year Treasury’s move toward 4% says about AI anxiety in markets

Sinokor bought and leased 120 used VLCC (very large crude carriers). They are the master of their domain. The top 10 control 50% of the market. They herd together, dictating rates, creating a bubble. New entries are limited. Shipyard rates, for new vessels, are higher. Environment regulations increase cost. VLCC is a moat. It cause inflation.