Sold $54B of 10-Year Treasury notes at 4.18% to replace $25B of maturing 1.73% 10-year notes, pushing up amount outstanding by $29B.

By Wolf Richter for WOLF STREET.

The US government sold $701 billion of Treasury securities this week, spread over nine auctions, including 10-year Treasury notes and 30-year Treasury bonds.

Of these auction sales, $160 billion were notes and bonds. The yield at the 10-year Treasury auction (4.177%) was a hair higher than at the 10-year auction a month ago (4.173%). The yield at the 30-year auction (4.750%) was lower than a month ago (4.825%). The yield of the 3-year note fell by over 9 basis points to 3.518%, below most of the T-bill yields that sold this week.

| Notes & Bonds | Auction date | Billion $ | Auction yield |

| Notes 3-year | Feb-10 | 74 | 3.518% |

| Notes 10-year | Feb-11 | 54 | 4.177% |

| Bonds 30-year | Feb-12 | 32 | 4.750% |

| Notes & bonds | 160 |

And $541 billion were Treasury bills with maturities from 4 weeks to 26 weeks, most of them to replace maturing T-bills.

Yields at five of the T-bill auctions, with maturities from 4 weeks to 17 weeks rose by 3 to 5 basis points compared to the same week a month ago. Only the 26-week bills were sold at a lower yield, down by 8 basis points compared to a month ago.

| Type | Auction date | Billion $ | Auction yield |

| Bills 6-week | Feb-10 | 95 | 3.635% |

| Bills 13-week | Feb-09 | 94 | 3.600% |

| Bills 17-week | Feb-11 | 69 | 3.595% |

| Bills 26-week | Feb-09 | 81 | 3.500% |

| Bills 4-week | Feb-12 | 105 | 3.630% |

| Bills 8-week | Feb-12 | 95 | 3.630% |

| Bills | 541 |

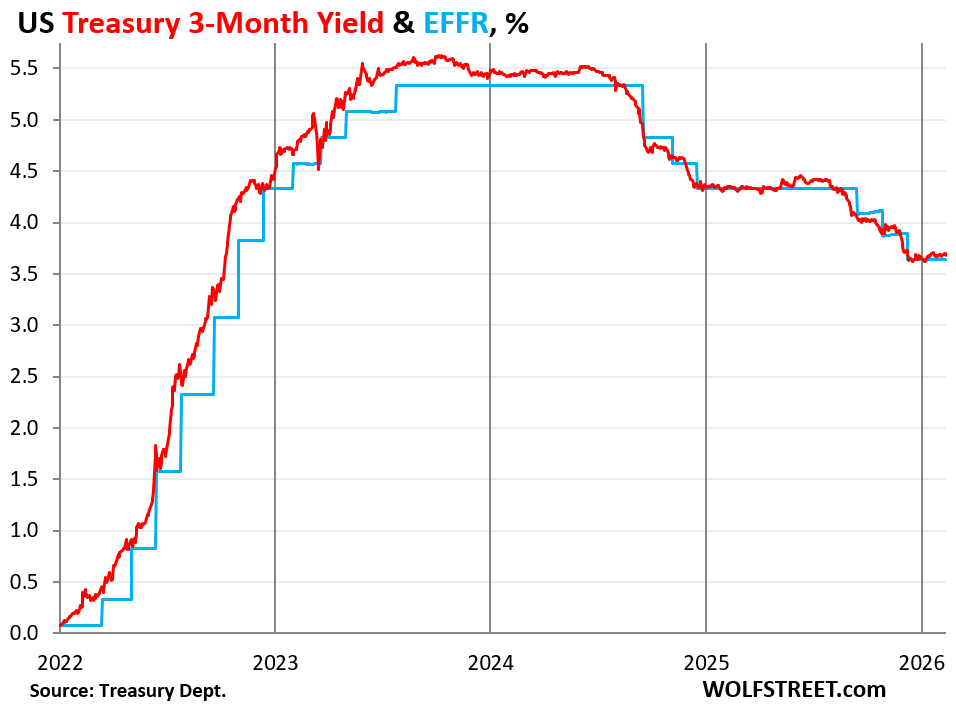

The yield of the 13-week Treasury bills, at 3.60%, was up from 3.56% a month ago, indicating that the market no longer expects a rate cut within the 3-month window of these securities.

In the secondary market, the three-month yield, at 3.68% on Friday at the close, was up just a hair from a month ago (3.67%) and was higher than the Effective Federal Funds Rate (EFFR) which the Fed targets with its policy rates (blue line):

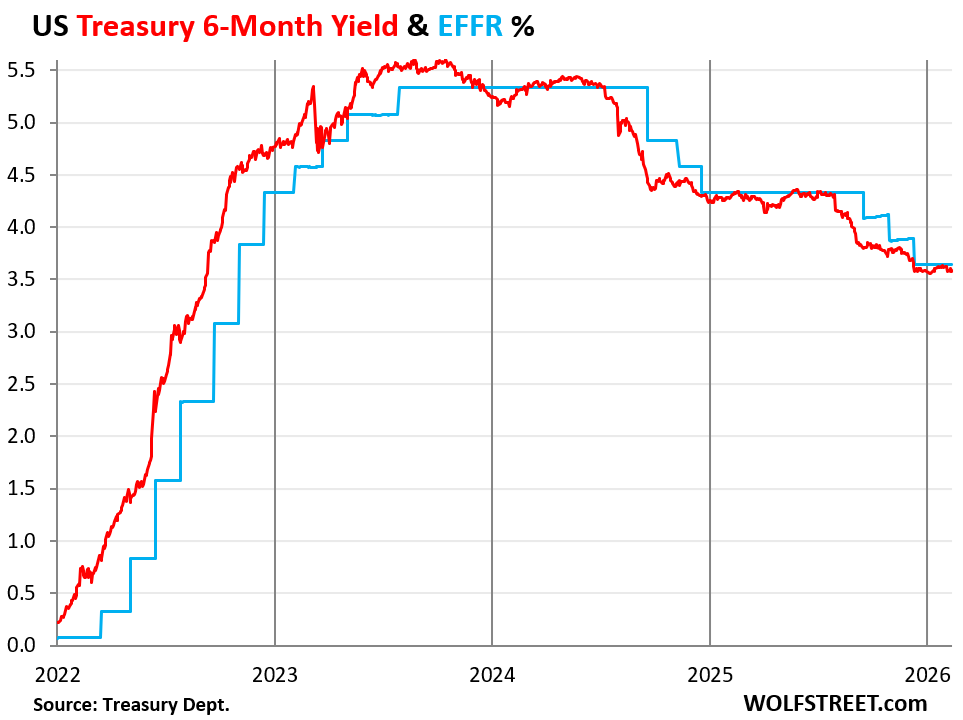

But the 26-week Treasury yield at the auction this week dropped to 3.50%, lower than a month ago (3.58%), and below the EFFR, indicating that the market sees a chance of a rate cut within its 6-month window.

In the secondary market, the 6-month yield closed on Friday at 3.61%, also lower than the EFFR.

The Fed’s rate cuts have pushed down yields at T-bill auctions, but yields at note and bond auctions are determined by the yo-yo of the bond market and reflect the bond market’s aspirations and its views or fears of the future – especially of inflation and of a potential tsunami of supply of Treasuries to fund the ballooning deficits.

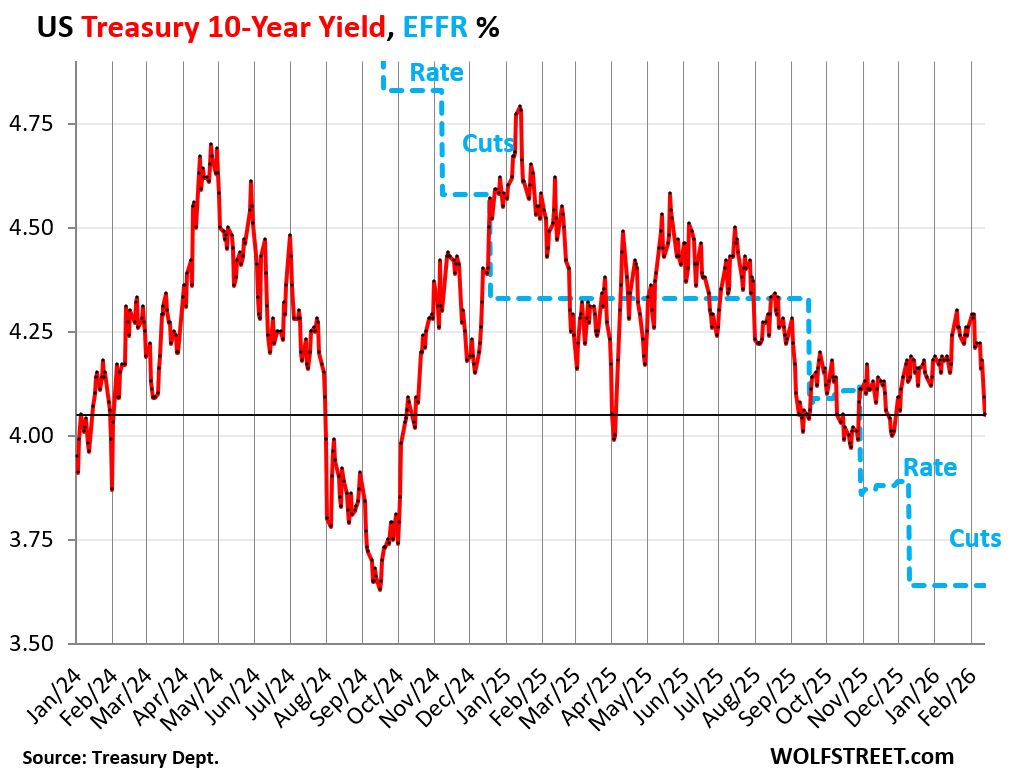

The 10-year Treasury notes sold on Wednesday at a yield of 4.177%, and in the secondary market that day, the 10-year yield closed at 4.18%.

But in the two days since the auction, the 10-year yield dropped by 13 basis points in the secondary market, to close at 4.05% on Friday, the lowest since late November. Since the beginning of February, it has dropped by 24 basis points.

Lower bond yields mean higher bond prices, and leveraged bond traders make a lot of money when prices rise and yields fall. On Wednesday, yields had risen on news of fairly strong hiring in the private sector in January. But on Thursday, the market walked that back, and on Friday, there was lots of stuff floating around in the headlines about a “soft” CPI report, and that’s all it took to push up prices of bonds and notes, and push down their yields. Market yo-yo. Bounce next?

Amount of 10-year notes outstanding increased by $29 billion this week. Bond math, as deficits balloon, is relentlessly brutal. The $54 billion of 10-year notes sold at the auction this week at 4.177% replaced $25 billion in 10-year notes sold at auction in February 2016 at 1.73%, maturing on Sunday. And thereby the total amount of 10-year notes outstanding rose by $29 billion.

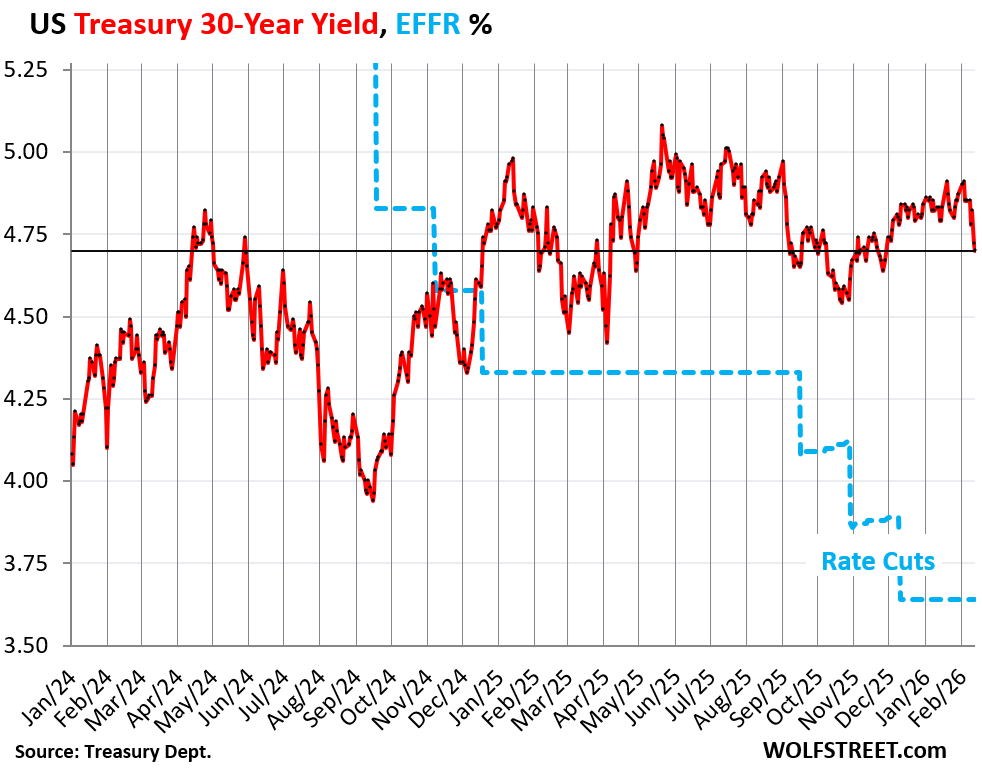

At the 30-year Treasury auction on Thursday, strong demand pushed down the auction yield to 4.75%.

In the secondary market after the auction on Thursday, the 30-year yield declined further to 4.72%, and on Friday eased to 4.70%, down 12 basis points in two days.

But the yield is still above the middle of its two-year trading range.

Jawboning down long-term yields.

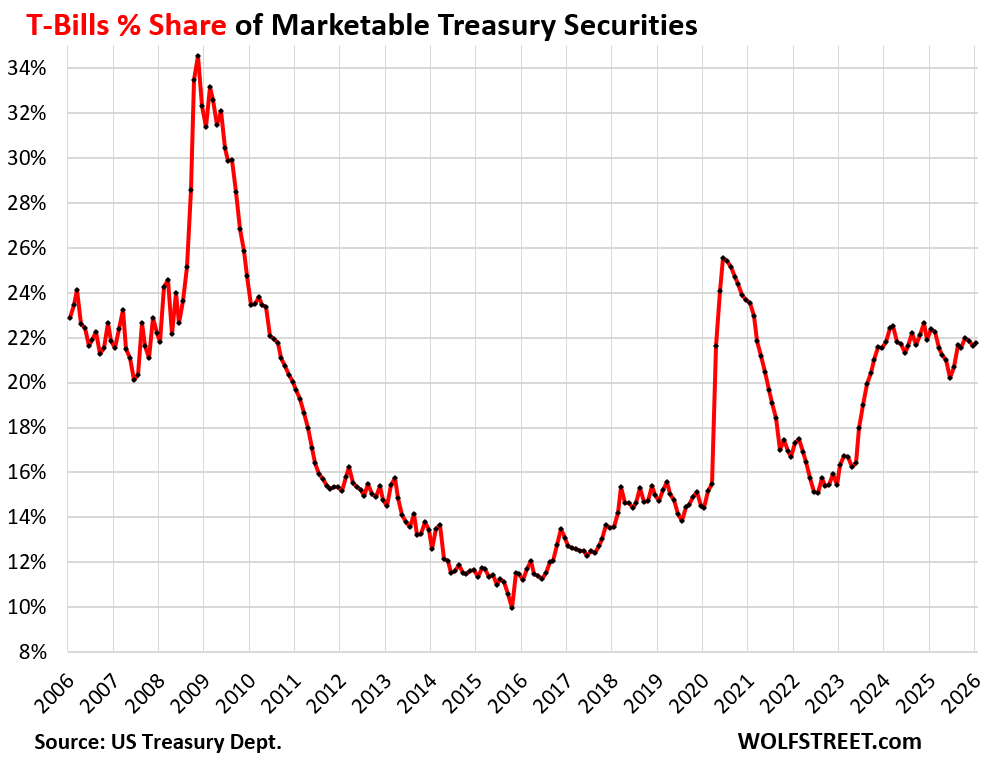

The Treasury Department has said that it would use increased T-bill issuance to fund the deficit, rather than increased issuance of notes and bonds. It has said this to take some upward pressure off long-term yields, as the bond market is concerned about supply in the future of notes and bonds it has to absorb that might require higher yields to bring in new buyers.

But the Treasury Department was just jawboning, and the market loved to hear it.

The ratio of T-bills outstanding to total Treasuries held by the public has remained roughly unchanged for the past four months, and at the end of January was 21.7%, up a hair from December, but down a hair from October and November, and lower than in 2024.

Turns out that the issuance of notes and bonds has increased by about the same rate as T-bill issuance has increased.

The mechanism for it is the relentlessly brutal bond math. This week, the $54 billion of 10-year notes sold at auction replaced the $25 billion in notes sold at auction 10 years ago, that maturing this Sunday, adding $54 billion and subtracting $25 billion, thereby increasing the total 10-year notes outstanding by $29 billion.

This process continues every month with every note and bond auction. And 20-year bonds were re-introduced in 2020, after having been eliminated in 1986. There are no maturing 20-year bonds, and the new issuance doesn’t replace anything. It just adds to the bonds outstanding. Even if the Treasury department doesn’t further increase the size of the note and bond auction, the total outstanding will increase relentlessly.

So the shift to a larger share of T-bills hasn’t actually occurred yet since note and bond issuance is far larger than the maturing notes and bonds they replace, thereby pushing up the total amount of notes and bonds outstanding.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Thanks wolf

“ Bond Math Is Relentlessly Brutal”

What happens when everyone is math class earns an ‘F’?

What happens when no ‘kids’ (bond buyers) show up to math class?

What happens when the instructor start teaching advanced calculus to kindergartners?

“What happens when no ‘kids’ (bond buyers) show up to math class?”

Could be bond buyers still see the US as the least bad option.

And even if they stop showing up; I suspect the Fed would step in to mop up and purchase any bonds to prevent a spike in yields.

Inertia favors the US, but the country is no longer seen as a safe place.

China may be seen as risky, but it is now the largest trade partner for most countries in the world.

IMO the yield curve seems to be synthetic in the sense that the interest rates do not reflect the inherent risks of a lax monetary policy

Dang, perhaps that there ‘synthetic’ in appearance bond market just may be a reason why gold and silver markets are seeing demand like never before world wide… regardless of what people want to believe. Me thinks the proof is in the pie.

🤣 💔 If there were this demand “like never before world wide,” the price of silver wouldn’t have collapsed by 37% as of now.

Retail investors are learning Costco gold bars are offered 60-70% spot at pawn houses and about 80% at coin shops…guess the demand ain’t really there. What have you heard?

Silver and gold are up several hundred percent. The recent spike and pullback is volatility, certainly no top. Check ✔ out Oliver MSA for the best analysis.

So why is the S&P P/E at crazy 21+?

Bond buyers always show up to buy at an auction.

The real question is at what yield is required to get them to buy.

So far, yield has generally stayed in a band and hasn’t gone up too much or down too much. Obviously you can manipulate the dates on this to drive a narrative, but for the most part they haven’t exploded.

Noting the very small differences between the auction yields (3.51%) on the 3-year note and the 10-year note yield (4.177%) and 30-year bond (4.75%), it seems that a non-trader would only want to stay at the short end of the yield curve. Who is buying the longer-term paper? I’m guessing that some of it is bought by those with long term actuarial obligations like life insurance companies, pension funds and endowments.

After graduate school in the 70s, I naively bought some whole life insurance. One feature of the policies was that I could borrow against the policy values for the phenomenal “low” rate of only 6%. After several years the dividends on the policy exceeded the premiums and even provided some cash. No more. For the past few years, the dividends have shrunk and now policy renewals come with hefty bills to make up for the shortfall between dividends and premiums. I am tempted to cash in the policies, but I am at an age where there is enough value that it will probably be better for my beneficiaries to keep them. My parents insured me for $2,000. At the time it was a reasonable amount but is not worth much now.

Earl,your parents only valued you at 2000 dollars?!

Damn,that must have been a rough childhood!

*LOL*

In the 1950’s $2,000 was a lot of money. Minimum wage was a whopping 75 cents per hour ($0.75/hr). I grew up around people who raised children and bought houses on that wage.

1955 .75 hr was low for the time as the average pay was $4000 year. $2000 was half. Father in service made $4000 as a chief petty officer and with 2 brother’s we struggled pay check to pay check.

I worked for 90c per hour in 1971.

This is a crime. Bankers playing on people fears of risks (that likely are not going to happen) are taking people money, making people lose it with probability of ~100%.

Bankers have been saying that life insurance, bonds etc are safe/conservative play. No, opposite. In the long run they are almost quarantined to lose their money (nominal or lost opportunities).

I’m always pissed off hearing such stories. Seeing it constantly.

Dude there is such a thing as too much risk.

Look up Harry Markowitz

You’re gonna get burned and then feel terrible.

Losing money in investing is The Worst Thing.

It’s not grabbing every opportunity you can by taking every risk like the markets are a casino.

Too much risk is not desired :) Why take too much risk? It even sounds unwise. Too little risk is very risky too in the long run.

Talking about e.g. a decent guy, perhaps going to his bank. The bank, say, is in downtown. Very fancy building, marmur, gold, everything shines. Outside or below the most fancy cars of the “bankers”. Who is paying for that?

Anyway the guy is told that his newborn needs a life insurance, since live is so dangerous. He is told indirectly that if he wants to be a good dad he should get this very special life insurance. Lots of fine print, unexplained. Very smooth PR.

I was pressured like that, long time ago.

Another example that long time ago, when I was at the beginning of my pretty good career, also money wise, I was contacted by my bank that there is something special for me. They pushed very hard to sell me 0.5% CD ladder in my long term tax free retirement account! It was PRed in a way that I did not push strongly initially (I was focusing on my work that minute). I spent weeks later to clear it out.

The hope is that nowadays there is so much more resources online / ChatGPT that pulling such manipulations is way harder.

Skier,

Pretty much any bank you can walk into is going to try to sell you some trash product. That’s how their associates/sales people make commissions.

Heck it wasn’t long ago that if you called AIG investments, they could switch from a fiduciary mode to a sale mode in the same call. They would sell you garbage because the laws said they could.

The genius of governments throughout history is that they are able to deflect blame to everyone from corporations to farmers and have people believe it.

Banks, which are chartered by the government and exist with the government’s grace and favor, are the enablers/agents.

it’s like a COT report with the ultimate producer continuously shorting long term bonds and notes, while speculators keep adding longs.

Or: specs keep bidding the futures up and producers take the other side of the trade until exhaustion takes place. It’s important to remember that producers have the goods and having the goods wins.

A quick glance shows the 10 and 30-year yields going downward in their recent trajectory.

I guess folks are still buying US Federal Debt.

Yes, there is huge demand. Which is why yields are so low.

How / where else can they get guaranteed earned income for funding their boomer pensions, with such a large amount of capital transacted?

Who knows what the yield curve will look like a year from now.

I’m still T Bill and chill. The right choice takes us back to the understanding of the risk of failure inherent in the end of QE.

The cause of the increase in home prices was the zero pct policy that the Federal Reserve Bank of the United States of America thought was a good idea.

Bond holders will regret it. It’s not going to last.

Which makes people wonder, our leaders included, as to why we should be responsible? Why not borrow trillions if we can do so cheaply?

That’s the way they think anyway.

Almost ALL countries operate in debt. I have heard clever ways, besides bond sales, of plans to erase this debt. Such as Crypto and re-evaluation of gold and silver by the Fed, thus repayment when strike prices soar using some of their “stock piles”. Bitcoin was down almost 50% of previous high. So the math works in favor of such strategies. You have also seen the MotelyFool…”If you invested $1000 in Nvidia in 2017…that would be worth a million today!”. Not a bad idea today to buy $2000 split across these assets(unicorn stock, Bitcoin, precious metals) when your kid is born and hold until the reading of the will.

Kirk, yes, but our trajectory is getting worse and worse.

“so low”!. The 10 Year Treasury Yield is higher than the 10 year in Canada and all Euro countries.

Which is preposterous from a fiduciary perspective

And France’s is lower than Canada’s and Germany’s is under 3%.

Germany is debt- averse with laws limiting govt debt. These had to be loosened to allow military spending to rise after Russia invaded Ukraine.

Then why has the Fed’s Balance begun expanding again? If there is so much demand, then let the damn debt mature and roll off. What are they buying with freshly “printed” digits?

They’re buying T-bills to:

1. Replace the MBS that are rolling off, and

2. to increase reserves ahead of Tax Day so that short-term repo rates won’t spike over that five-day period, when huge amounts of money gets sucked out of everything and into the government’s checking account (TGA).

They’re only replacing maturing notes (2-10 years) and bonds (20, 30 years), not adding to them. The balance of the Fed’s holding of notes and bonds has not changed at all.

I have endlessly written about that here.

Total assets are increasing, regardless of portion of the balance sheet they are on. No reason to increase bills. Let the MBS die already, they have plenty of assets to cover tax day (over 6.6 trillion).

WB:

Why is the economy, (probably) the money supply, debt and everything else going up?

The unbreakable mandate is “up and to the right”!

Anything else is worse than the ghostbusters crossing the streams!!!

I agree, but only because of the rating. Moody’s credit rating for the United States was last set at Aa1 with stable outlook. This is hilarious.

“But the (30-year) yield is still above the middle of its two-year trading range.”

Jeff Gundlach is wary.

The 30-year is going to expire valueless.

Hello Wolf,

I continue to enjoy reading your articles. I was originally introduced through Doug Kass where he posts links to your articles but now have you bookmarked.

Anyway, I had a couple questions for you.

– Once before I asked you about the possibility of a US default. At what point does the bond market force deeper fiscal discipline through higher yields? I would have thought it would have happened long ago. Having started in the investment business in the 80’s I remember the double digit yields of that decade.

– My other question was on crypto. You have smart investors like Michael Burry (who I subscribe to on Substack) saying it is worthless – figuzzi – figazzi. Would love to know your thoughts on the matter. Not so much as to when to buy or sell, as just the viability of crypto as a store of value. Part of me sees the entire crypto phenomenon as just a manifestation of excess liquidity and animal spirits.

Thanks again for all the insightful writings you share. Best regards. M

Michael,

1. “At what point does the bond market force deeper fiscal discipline through higher yields?”

The discipline being enforced would come from much higher yields. But currently there is huge demand for Treasury notes and bonds, which is why yields are so low. Every time the 10-year yield got close to 5%, demand just exploded and pushed down the yield. 5% on a 10-year pulls in lots of new investors; just about everyone wants in on it. There is zero bond market discipline in this environment. But it could happen someday.

This administration’s solution now is “to let it run hot.” Higher economic growth generates more tax revenues to deal with the interest expense, and higher inflation reduces the burden of the long-term debt over time.

https://wolfstreet.com/2025/12/24/us-government-interest-payments-to-tax-receipts-average-interest-rate-on-the-debt-and-debt-to-gdp-ratio-in-q3-2025/

2. “My other question was on crypto. You have smart investors like Michael Burry (who I subscribe to on Substack) saying it is worthless – figuzzi – figazzi. Would love to know your thoughts on the matter.”

Cryptos are a gambling token. The bet consists of the hope that you can sell the token for even more to an even greater fool. Cryptos operate on the classic “Greater Fool theory” of investing, where some intrinsic value no longer matters or doesn’t exist, and investors just hope to sell it for more later.

I am curious to know if you think gold falls under this category of “where some intrinsic value no longer matters or doesn’t exist, and investors just hope to sell it for more later.”??

There are a lot of things like that, including art (no intrinsic value), classic cars (the intrinsic value is that of an old used car), etc.

Precious metals have industrial uses, so there is some intrinsic value, but it’s only a small portion of current prices. So gold, even theoretically, will never go to zero because it has a still substantial value as an industrial metal. But cryptos can and do and did already go to zero, when they stop being traded and you can no longer sell the ones you have because you ran out of Greater Fools, at which point they’re worthless.

One can certainly argue that gold is money. It was money—and therefore had intrinsic value—long before ‘industrial metal’ was even a concept.

Gold’s value was historically derived from its unique physical properties—scarcity, durability, divisibility, fungibility, portability, etc. —that made it the ideal form of money. Centuries later, it was discovered that gold could be used in dentistry, and eventually, in iPhones.

andy

“scarcity” is a funny concept. If there is no demand, “scarcity” turns into “glut.” Which is why the price of gold is so hugely volatile. Last time scarcity turned to glut was in 2012, and the price of gold plunged by 50% over the next four years and didn’t recover to the 2012 peak until 8 years later. The concept of scarcity depends on everyone manipulating up demand by hoarders that are hoping for a higher price later, and then the price gets high enough and they start selling, and scarcity turns to glut again.

Precious metals are a good shock absorber in any portfolio. I prefer deep storage – miners, others prefer physical or equivalent in custody (PHYS).

Long term I am a gold bull. If I had headed Wolf’s anti-gold mindset I would have missed a 5.5x bagger on my Agnico Eagle (from May 2020) – when bought it was Kirkland Lake. Now I can trim and re-invest.

There is NO end is sight to how over heated this economy will become. Most central banks have turned a blind eye to inflation for various reasons.

I have no position in crypto but I get the overall idea. As per a recent Michael Green article he has said it has functioned as a Shadow market for gold for a while and that is shifting now.

Wolf,

I would only argue that the value of gold as money far outweighs its value as an industrial metal. In my view, it is not even close; there are many replacements for gold in industry, but there is no replacement for gold as money outside of promissory notes. Silver lacks portability, and platinum lacks identifiability. Diamonds lack fungibility. And so on. Nothing is quite like it.

“All is not gold that glitters”.

Andy

JP Morgan, when he said, “Gold is money, everything else is credit,” was ridiculing gold. He became rich and powerful because he had credit. Credit makes the world spin around. Without credit nothing works. Without gold, everything would work just fine except for a few industrial applications.

Look, gold can make a very good long-term investment and is a good trading instrument because it’s so volatile, and because there are paper derivatives that can easily be traded and leveraged. But this endless goldbuggery bullshit is just ridiculous. People go nuts over gold.

JamesN,

“Long term” is a funny concept..

James N,

A blind eye? So that’s why in 2022 they raised the rates so high.

And killed the bond market, taking down Silicon Valley bank.

Cuz they turned their blind eye.

Right.

An institution in my city lost like $140 million in 2022 from investments. Prob cuz they were so heavily in bonds, what they thought was safe.

A professor at NYU was asked what he thought the value of a bitcoin was and he replied that he could only quote the price never the value.

I got the fever. Man, I got the fever. The gold RUSH.

I don’t want no cure. I don’t want a cure. Sweetest hangover.

Think about it all the time. Never let it out of my mind.

Andy – “long term” as per my post as a % of my portfolio and I mean always.

Sufferingsucatash – despite all the US FED jawboning PCE is ~= 3% so much for the 2% target. 2022 was perhaps the dawn of a return to normal in terms of policies. Central banks could not keep throwing non-asset holders under the bus. They were forced to act IMO. Anyone who owns corporate bonds need to manage their risk.

Re: ‘many replacements for gold in industry’

Gold is ONLY used in industry where nothing else will work, for the obvious reason of cost.

‘The James Webb Space Telescope (JWST) features a 6.5-meter, gold-coated beryllium primary mirror designed to detect faint infrared light from the earliest galaxies. Its 18 hexagonal segments are coated in a 100-nanometer layer of gold to maximize infrared reflectivity to 99%, far surpassing silver or aluminum.’

A surprisingly small amount of gold covers this large surface because along with other unique properties gold can exist in the thinnest film. In fact it can be beaten so thin light passes through it.

Another important unique property in a metal element: it never corrodes. Gold that went into salt water centuries ago comes out glittering. So for very important electric contacts, they are gold plated. Even a good stereo shop will sell cables with gold- plated contacts. Because the plating is so thin, they aren’t horribly expensive.

Of course, the main interest in gold is not industrial, but as a non- fiat form of money. People who think it doesn’t have this role or wish it didn’t, would like the world to be other than it is. They have some distinguished company: e.g. J M Keynes.

nick Kelly

JP Morgan, when he said, “Gold is money, everything else is credit,” was ridiculing gold. He became rich and powerful because he had credit. Credit makes the world spin around. Credit rules. Without credit nothing works. Without gold, everything would work just fine except for a few industrial applications.

As a regular Wolf Street Comment reader, I often see Posts from people touting their investing “wins” and yet somehow, I rarely (if ever?) see Posts extolling losses.

Who knew investing was so easy?

I have gold and silver in portfolio but I also realize that the intrinsic value of these are are very small.

Most of the current value is coming from same hype valuing cryptos ie finding the bigger fool to sell to.

Crypto has zero intrinsic value

Other pms have some intrinsic value based on industrial use.

Nothing wrong in hoarding pms but keep an open perspective

In 1907 Ole JPM got the US thru a near crash by acting as a Fed, the US at this time having no central bank. He locked bankers in his library until they agreed to kick in (along with himself) and stabilise the markets which were crashing due to the over extension of credit made in an attempt to corner the copper market. In 1929 his son failed in a similar attempt, as the amount of credit in the stock market was too large to prevent an implosion.

If JPM could be resurrected today and was shown the US balance sheet with 36 trillion outstanding, he might instantly be de-resurrected.

Housing and anything else, are also subject to the greater fool scenario.

Sure, there is SOME “intrinsic value.”

OK, “Gold has always been money.” I have a small pile of silver, in case I ever have to try to trade it for…? Groceries? As if there would be a place to do so, when “everything collapses.”

My question is: has “money” always been money? My impression is that money is a man made grift, and not an inherent part of nature (looking for the biological “money receptors”).

I also have a large amount of change as a chaos hedge. The melt value is equivalent to the amount of ammo I can make it into

Look at every alternative to gold. They are all less secure. The gold price will rise until that changes.

I have a simple analysis of rising government expenses. It’s because the lobbies run Washington, D.C.

“But it could happen someday.” “Pig wings! Hot, salted and buttered. Two cents a bag! Get yur pig wings!!” 😂

Suggest you read “Devil Take the Hindmost”, you will learn this kind of greater fool scheme has been running since the Dutch trading ships sailed.

That’s the whole basis of speculation in general. You bet that a greater fool will show up right about the time you need the liquidity.

I bought that, forgot on whose recommendation. Maybe Bill Bernstein or Peter Bernstein.

Still need to read it.

Crypto currency is like Beanie Babbies. Only once those became worthless, your children still had something to play with.

Firstly crypto is not a currency

secondly that even the least flimsy one of them has no army standing ready to enforce the value of the currency

Biggest problem is Tokenization. These tokens to include Bitcoin are treated like money, but they are not money. They are a fad like hoola hops, dutch tulips, pet rocks, ets. You might as well trade s’it.

Crypto is for criminals. I had a randsomware attack on my PC and they demanded payment in Crypto. I told them to go f$ck off. I wound up losing all my pictures from my vacation. Also my backup thumb drive was plugged in my PC at the time. I lost all the .PDF files on there too. When Crypto goes to zero, I’m going out to my favorite Irish Pub and celebrate.

Despite all the legitimate concerns, I think lots of Retirees are still buying, not just institutions. You need cash flow from your savings in retirement. Can’t get that from gold. Stocks look overvalued, so the dividend strategy seems risky. Fixed income investments really are the “last best option”. Stay diversified, and pray inflation doesn’t destroy your nest egg is about all you can do without a crystal ball.

As Wolf noted above if the 10 year gets to 5% I’m backing up the truck (assuming inflation about the same) as the fixed income portion of my portfolio keeps wandering down on returns, and I’ve shifted a portion into slightly riskier investments to keep cash flow level. My lifestyle isn’t largely effected by recent inflation jumps, and is more sensitive to fixed income cash flow.

You can get cash flow in effect from gold or silver by selling smaller portions such as coins of it over time. But to reduce the chance of selling at a loss, you would want to buy when the price isn’t too high, and that can be tough to judge, such as current prices seeming too high.

Ha took my silver coins i collected as a kid in the 1960s when amount of silver was reduced from coins .

Took to a dealer last week who said he would pay me equivalent of 20 USD/oz

Said miners would only pay the final price after smelting and that might take months . Basically he said no dealers would buy . I can’t eat drink or use precious metals for anything. If one thinks a store could start using gold coins they are sadly mistaken . A retail store only has a few hundred in cash at one time and have a business model set up for self checkout

Sorry to hear. I think there are a probably a decent amount of people in your area that would pay you a lot closer to market price, but I understand it takes time to make those connections and even then it can still be risky, good to be careful such as making the sale in a law enforcement station parking lot.

you went to the wrong dealer ;

Still dunno what retirees are doing with all this inflation.

Social security uses the Cola to keep that part whole, but they IRAs and 401k do not have that function. Guess they would keep those tax free retirement accounts in the market, to take advantage of this tech boom.

Like a 30% loss to retirement accounts in inflation.

Nobody could have planned for that.

A lot of the inflation of the last several years was in housing, which is a huge portion of cost for young people, but a relatively smaller cost for most retirees. But the Fed should be dissolved for their complete incompetence nonetheless.

I’ve been retired for 6+ years. Over time I’ve moved more of my investments from equities to fixed income (mostly short-term treasuries). Recently I asked my financial advisor to reduce some equities even more. The reason is that I’ve had an excellent run on the big tech stocks. Average increase in the past 3 years of 160%. I don’t think that will continue and with the AI hype cycle, it may even go the other way. I’ve always been cautious but not scared. So far, so good.

So you’re not retired you’re actually a trader who is making decisions where to put his money

Retired people manage their investments too.

lol

I agree, The perfectly legitimate class of investment the annuity. A worthy alternative to the lower paying treasuries scared away by the amateurishness demonstrated by the hucksters selling junk

Yep, it’s works pretty well until the interest cost on the debt becomes crippling, and the Fed has to step in and buy new Treasuries that people won’t buy because they see the handwriting on the wall, that dollar dilution will destroy their ROI from Treasuries.

That’s one of the reasons that Trump is adamant that the Fed lower interest rates, he wants the interest cost to be lowered. He wants to pass the buck to the following presidents.

You can still get 6% on bank preferreds, and I’m talking good credits – Wells, BofA, JPM. They pay qualified dividends, too.

There are lots of ways you can get cash flow from gold. Monetary Metals, dividends from miners and royalty companies, capital appreciation, etc.

Couldn’t AGREE more mike…

As a now elderly swabie who became a very well paid ”analyst,” I see ALL our USA navy assets as ”sitting ducks” after the very clear demonstrations of that by Ukranian drones, etc., etc.

I am just hoping that the current GUVMINT intent is to try to bring reality to ALL the efforts of USA to damp down and/or stop all the situations around the globe…

Does not seem likely ATM,,, so suggest ”hedge” accordingly.

Great report.

Big issue (no pun intended). Government spending is out of control. And, the Fed continues to accommodate.

If Trump gets his wishful demand for 1 per cent or lower interest rates, the price we all will pay will be very high.

Thank you,

B

What portion did the dealers have to take, and how big were tails? Tails on short-term go straight to the deficit with a compounding effect.

Despite all the wagging about it, it doesn’t matter because dealers are going to sell the securities to their clients, including hedge funds for the basis trade, or to the broader market, unless they want to keep part of it for specific reasons to make money with them in other ways. For example, the 10-year notes they bought on Wednesday could be sold at a profit on Thursday and Friday, and with leverage, that adds up.

It would be helpful to know that the total weighed average interest rate and the total nominal interest amount on the maturing debt versus the new debt.

You can get the average weighted interest rate on the existing debt. But for the new debt, which changes with every auction every day, you have to look at the auction yields.

https://wolfstreet.com/2025/12/24/us-government-interest-payments-to-tax-receipts-average-interest-rate-on-the-debt-and-debt-to-gdp-ratio-in-q3-2025/

Wolf, Scott bessent keeps saying if we bring debt to gdp ratio that is good enough. It is not the absolute number that matters. My question is “do you see debt to gdp being lower”?

For debt-to-GDP to decline, the debt has to grow more slowly than nominal “current dollar” GDP, so the debt (not adjusted for inflation) divided by GDP (not adjusted for inflation). If the debt grows by 6% and nominal GDP grows by 8% (which it did in Q3), then the ratio declines. But in Q3 the debt exploded because it had been flat for six months during the debt ceiling in Q1 and Q2, and then the government had to borrow massively very quickly to catch back up and replenish its empty checking account. So in Q1 and Q2, the ratio fell, and in Q3 it rose but by less than it had fallen in Q1 and Q2 and was still below Q4 2024.

I’ll speak the obvious here I guess. Government debt and CDs are popular because everything else has more risk, and risk leads to anxiety. Of course money has three purposes: spending, making money with money, and as a personal well being safety net even if you just stick it under your mattress. Chasing rainbows can be fun though I guess. But gambling has gotten out of control lately. Too much coffee, too much traffic, too much anxiety. Also, when you ask someone what their gold, silver, bit coin, real estate, or whatever is worth, they always quote you in dollars. The dollar is still king because it is THE medium of exchange.

Who quotes you in dollars? Only people In America willl quote you in dollars. Pretty sure if you ask a European what their house is worth they will quote you in euros. Australians will tell you in dollars but it certainly isn’t the same dollar that I use.

The only thing forcing our dollar to be a median of exchange is the massive aircraft carriers that are parked outside of every single country in the ocean.

Our military industrial complex is what forces the world to stay on the dollar everybody else would have already moved on and some people are trying to anyways

“The only thing forcing our dollar to be a median of exchange is the massive aircraft carriers that are parked outside of every single country in the ocean.”

Nonsense. Businesses in other countries have always done cross-border deals in their local currencies as agreed in the deal. The EUR in deals with countries outside Europe is on par with the USD as trading currency. The RMB is a solid trading currency across China’s borders. Essentially no business in Africa does cross-border deals in dollars. Companies trade with each other in whatever currency they agree on. It’s just dumb and ignorant to think that somehow companies in Brazil would use the USD to trade with companies in Uruguay. During the sale negotiations, the companies agree on the price and a currency. Oil might be priced in USD, and then the purchase agreements specify the currency and the converted price in that currency. Germany didn’t pay Russia/Soviet Union in dollars for its natural gas. It paid in EUR and DM. The amount of obliterating BS floating around out there about the USD is just mindboggling.

The US Dollar is used in more than 80% of all global transactions.

That’s an AI hallucination. I just checked and that’s what Google’s AI fabricated. It apparently sums FX trading, foreign-currency debt issuance, foreign currency banking claims and liabilities, foreign exchange reserves (we discuss this quarterly here), among others. AI search results are going to poison your brain.

In terms of using the currency in global trade (goods and services), the USD is the 2nd largest currency for cross-border trading, with a share of about 15%, same share as the Chinese RMB (15%), and both are behind the #1 trading currency, the EUR (about 18%). Those are also the three largest economic areas in the world, with a huge amount of international trade into and out of their own country/area, which is where most of the usage takes place. Little usage of those currencies takes place between third countries.

The green columns represent the share of global trade of goods and services in these currencies. The gray columns represent the financial use of those currencies (FX trading, foreign-currency debt issuances, foreign currency banking claims and liabilities, foreign exchange reserves, etc.). Data and chart via the Federal Reserve (2025).

Mr. Will,

To your point, I always love asking gold bugs, “what is gold worth it’s WEIGHT in”.

They always answer………..dollars

Any currency in the world 🌎.

Hate to admit such ignorance…….but, how is “interest” paid on Treasuries? Monthly, annually……at the end of the 10 years? How is it refinanced? Why does it appear to cost nearly double to refinance? Perhaps you could explain in one of your Wolf Reports. Thank you sir.

It varies. If sold at a discount (e.g. savings bonds or T-bills), they pay at maturity/redemption. e.g. pay $997 for face value of $1000, which you get (or roll over) at maturity. Otherwise most (all?) of the rest pay every 6 months. Refinanced by new sales/auctions. Doubling here could refer to interest rates (set by the market’s supply/demand) or the size of the auction versus that of the maturing bonds (which may not have all been sold at the same time if reopened) which is set by how much the treasury decides to sell of the different maturities. Over the last couple of years, the treasury has been moving to shorter (lower interest rate generally) maturities, but it looks like Wolf is saying that they don’t seem to be doing that so much now.

Interest is typically paid at maturity, at least that has been my experience with using treasury direct. Then again I have never bought debt beyond a year’s duration.

That’s correct only for T-bills. You buy them at a discount and get paid face value when they mature. The difference between discounted purchase price and face value is the interest. That’s why they’re often called “discount bills.”

Fortunately the deficit doesn’t matter and neither does the interest. The same would be true for all us (and our private debts) as well if we could use one credit card to pay off another in perpetuity

By the way here’s the tell that the US Fed Gov always issues new debt to pay off maturing debt (including interest).

If maturing Fed Gov debt was paid off some other way we would notice one of the following:

– Tax increases to compensate for increased outlays on maturing debt and/or

– Reduced spending to compensate for increased outlays on maturing debt

Personal savings rate was 3.5 percent for November. Net private saving: Households and institutions, fell below a trillion in the 3rd qtr. of 2025 for the 1st time since the 4th qtr. of 2022.

That’s the amount that they earned (not including capital gains) but didn’t spend. And it added to their huge piles of assets.

Could this sell-off be a way of clearing old inventory and tightening the fluctuations in these two bond markets? The view from the graphs appears to show that the fluctuations are tighter and have retreated from the wild swings in volatility.

There is no “sell-off” but a rally: falling yields means bond prices are RISING amid too strong demand.

Moody’s credit rating for the United States was last set at Aa1 with stable outlook. This is hilarious. The debt is skyrocketing and very soon all taxes collected will not be enough to service the debt.

“and very soon all taxes collected will not be enough to service the debt.”

That’s BS.

Based on that graph, it looks like the long bond would have to get up to around 12%-15% for interest payments to consume all tax revenue. That’s a very “static” interpolation of a complex system obviously.

Credit ratings of countries that issue debt in their own currency are meaningless. There is zero risk of default.

Given the “relentlessly brutal” bond math Wolf is describing and the potential for a “tsunami of supply” to further devalue long-term holdings, I’m seriously considering diversifying into international real estate or at least establishing a footprint outside the US. If the 10-year yield is being “jawboned” and the Fed is just swapping MBS for T-bills, the long-term stability of USD-denominated paper feels increasingly fragile. For those of you who have already moved some capital or even relocated to Europe to escape this debt spiral, how are you handling the administrative hurdles? I’m looking at Spain, but the bureaucracy for non-residents seems like a nightmare — has anyone used services like to handle the NIE or residency paperwork remotely, or is it better to just wait until the bond market yo-yo forces a real correction and a stronger dollar window?