One of the most fundamental changes resulting from the Financial Crisis was the transfer of mortgage risk from banks to taxpayers.

By Wolf Richter for WOLF STREET.

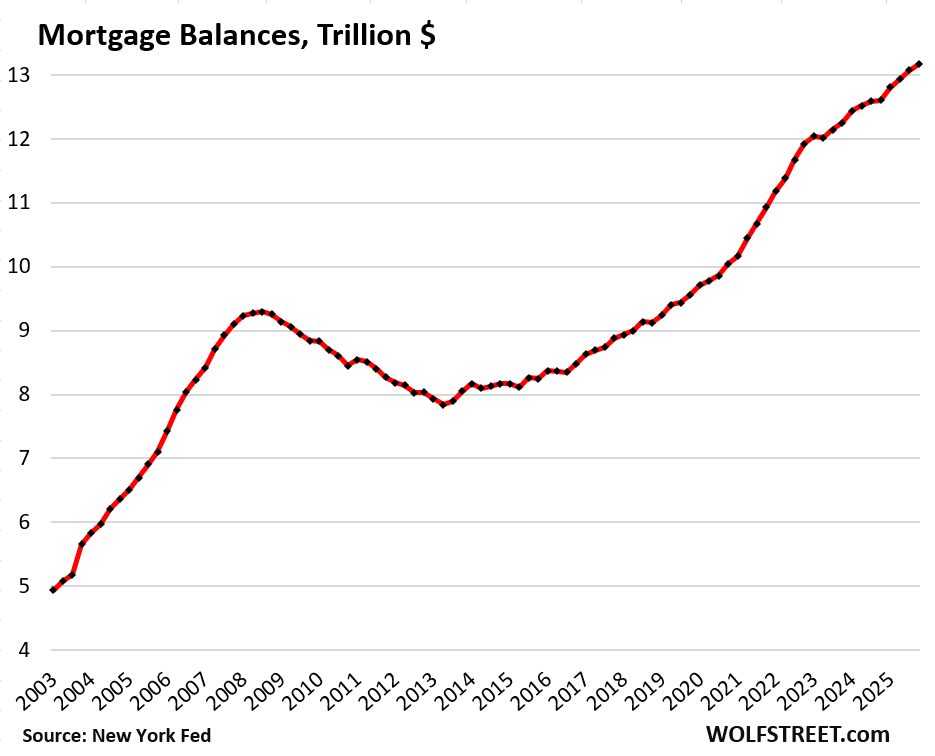

Mortgage balances rose by $98 billion (+0.7%) in Q4 from Q3, to $13.2 trillion, according to the Household Debt and Credit Report from the New York Fed, which obtained this data via its partnership with Equifax.

Year-over-year, mortgage balances rose by $564 billion (+4.5%). Since the beginning of 2020, mortgage balances have surged by 38%, while home prices have surged by 53% over the same period.

Overall mortgage balances grow as a result of several factors: When a buyer finances the purchase of a newly constructed home (growth of the housing stock); when the seller of an existing home has a small or no mortgage (40% of the homes are owned without mortgage), and the buyer takes on a new big mortgage; and when a homeowner does a cash-out refinance of an existing mortgage, thereby ending up with a bigger mortgage on the same home.

Mortgage balances are reduced by the principal portion of mortgage payments and other mortgage paydowns and mortgage payoffs; and by foreclosures that cause the remaining mortgage balance to be written off after the sale of the home – there was a lot of that during the Mortgage Crisis.

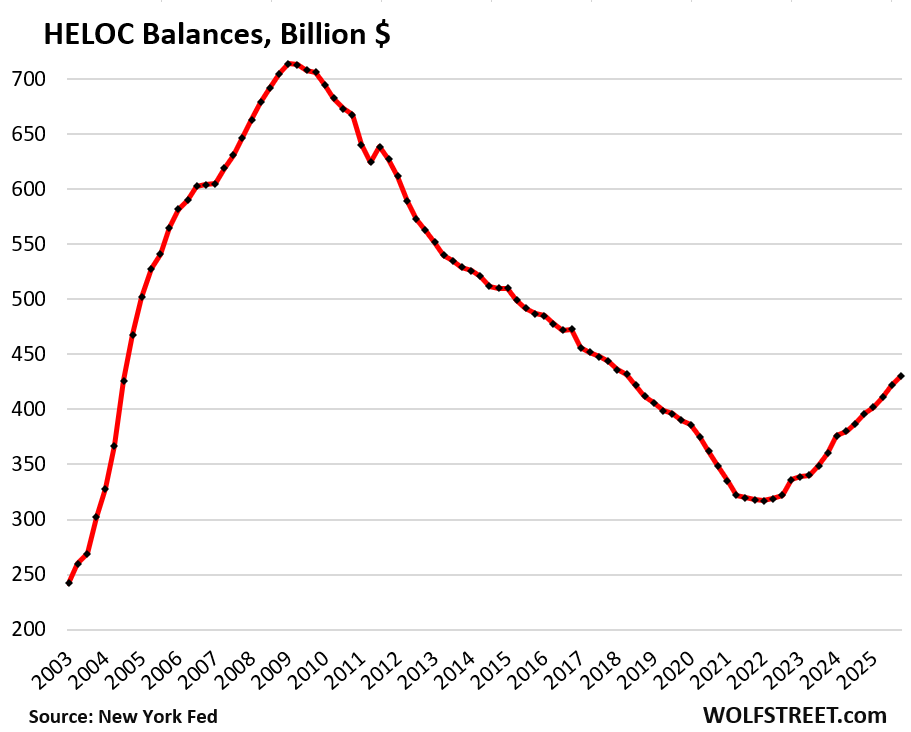

Here come the HELOCs: +36% since Q1 2021.

Balances of Home Equity Lines of Credit jumped by 1.9% in Q4 from Q3, and by 8.6% year-over-year, to $430 billion. Since Q1 of 2021, the low point, HELOC balances have surged by 36%.

HELOCs are lines of credit, and many of them are unused, just sitting there as a standby source of funding. But these balances here are actual balances drawn on HELOCs and accruing interest.

A HELOC is a second-lien loan on the home that, if defaulted on, can lead to foreclosure, even if the first-lien mortgage is current. HELOCs are full recourse loans even in the 12 states, including California, where nonrecourse mortgages are standard, and where lenders, after a foreclosure sale, cannot pursue former homeowners with deficiency judgements on the first-lien mortgage. But they can pursue former homeowners for the balance of the HELOC. HELOCs did some damage during the Housing Bust, and lessons were learned about their risks.

But what caused their disfavor in the years before 2021, and caused their balances to plunge for 13 years, was the ultra-low-rate mortgage. Instead of borrowing on a HELOC, homeowners cashout-refinanced their home. And that trend has now flipped.

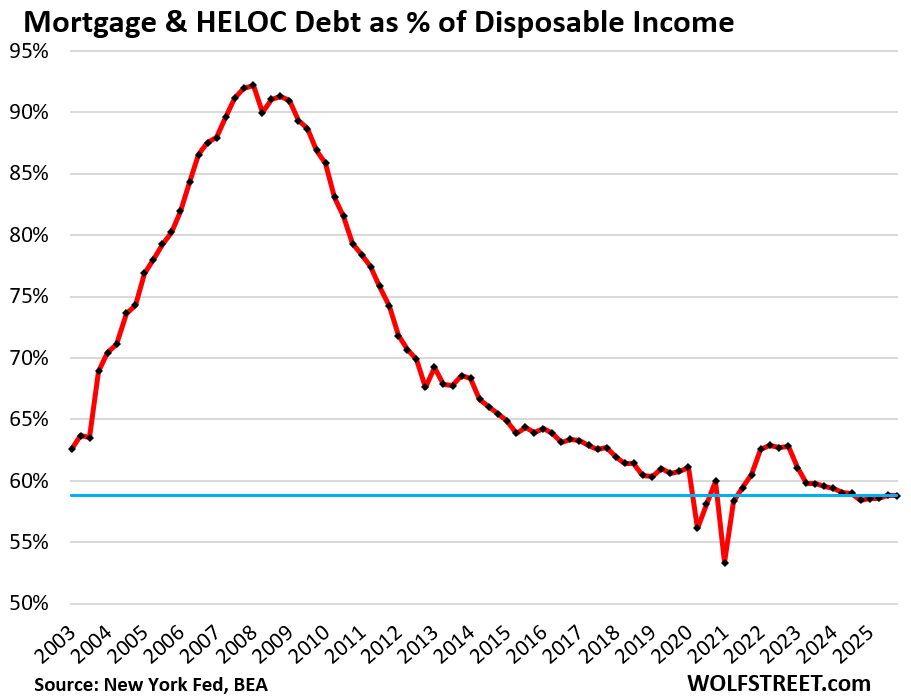

The burden of housing debt.

The debt-to-income ratio is one of the classic ways of evaluating the burden of a debt. With households, we can use the debt-to-disposable-income ratio.

Disposable income, released by the Bureau of Economic Analysis, is the monthly after-tax income consumers have available to spend for their daily costs of living, to service their debts, and to save and invest the remainder. So after-tax wages, plus income from interest, dividends, rentals, farms, small businesses, transfer payments from the government such as Social Security, etc.

But it excludes income from capital gains, which is where the super-wealthy make most of their money. And this upper crust of income is excluded here and doesn’t skew the data.

The housing debt for this ratio combines mortgage debt and HELOC debt.

The housing-debt-to-disposable income ratio in Q4 was unchanged at 58.8%, just a hair higher than a year ago, which had been the lowest on record, except for the freak quarters during the pandemic when stimulus funds distorted disposable income.

The chart below shows why the mortgage crisis happened: Consumers were way overleveraged with a housing-debt-to-disposable-income ratio of over 90%. When home prices sank and people started to lose their jobs, the debt imploded and was a big factor in the Financial Crisis.

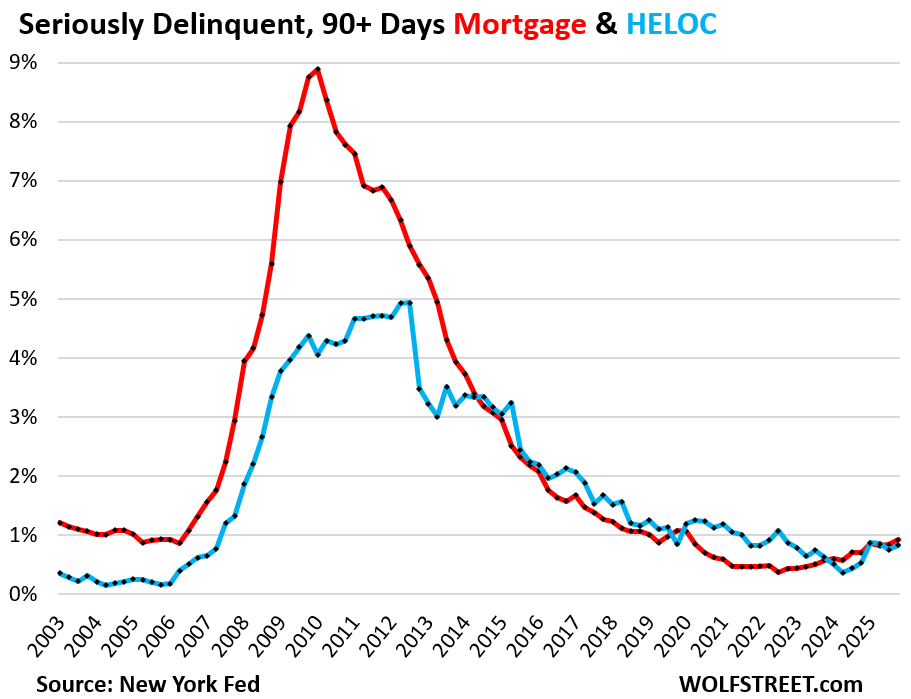

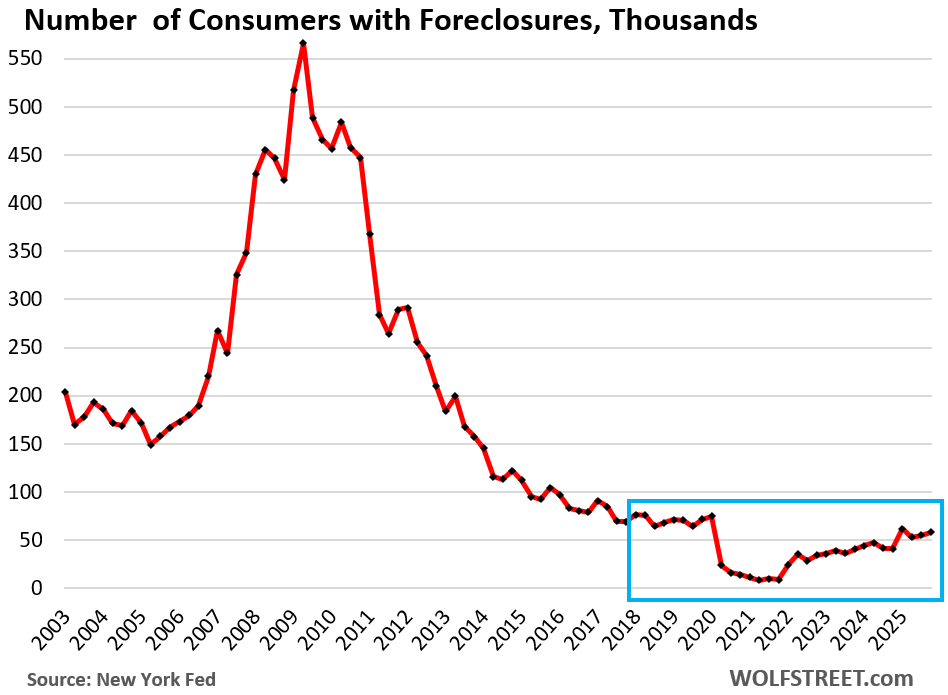

Delinquencies and foreclosures are very low.

Serious delinquency rates – 90 days or more delinquent – in Q4 edged up to 0.92% for mortgages (red in the chart below) and to 0.82% for HELOCs (blue).

These are low delinquency rates. They have returned to normal from the pandemic free-money lows in 2021-2023.

Foreclosures are still historically low. The number of consumers with foreclosures on their credit reports in Q4 edged up a hair to 58,140 consumers, well below the 65,000-to-90,000 range of the Good Times in 2018-2019, and far below those in prior years.

The increase over the past few years comes off the artificially low near-zero level during the era of mortgage-forbearance, when foreclosures were essentially impossible. The current levels aren’t even back to the Good Times normal yet, though they will eventually get there.

There will always be foreclosures, but a massive wave of foreclosures won’t happen unless there is a confluence of two factors: Widespread and sharp declines of home prices that make it impossible for a struggling homeowner to pay off the mortgage with the proceeds from the sale of the home; and a high unemployment rate, where lots of people suddenly lost their jobs and cannot make the mortgage payments.

But this time, the banks are off the hook.

Among the most fundamental changes resulting from the Financial Crisis was the transfer of mortgage risk from banks to taxpayers. Now, 65% (or $9.4 trillion) of all mortgages outstanding are guaranteed or insured by the Government Sponsored Enterprises, such as Fannie Mae and Freddie Mac, or by government agencies, such as Ginnie Mae; the FHA insures subprime mortgages with low down payments, the VA insures mortgages of veterans, etc.

The huge system of 4,000 banks and over 4,000 credit unions hold only about $2.7 trillion in mortgages, HELOCs, and second-lien mortgages, according to Federal Reserve data on bank balance sheets, less than 20% of the total. So there won’t be another mortgage crisis for banks. They’re largely off the hook.

The remainder of the mortgages that didn’t qualify for government backing, such as jumbo mortgages, and that banks didn’t want to keep on their balance sheets, about $1.7 trillion in total, were securitized into “private-label” mortgage-backed securities (MBS) and sold to institutional investors around the world, such as bond funds and pension funds, and they’re on the hook for those.

And in case you missed it: Household Debts, Debt-to-Income Ratio, Delinquencies, Collections, Foreclosures, and Bankruptcies in Q4 2025

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Those charts indicate that the U.S. is far away from mass foreclosures, which is one way to drag down housing prices.

2 articles on zerohedge today predicting that the re-adjusted employment numbers released by U.S. gov’t today will lead to interest rate drops of .75 to 1.00 %, which could lower monthly housing costs for mortgagors.

That’s typical ZH stuff. They predict the collapse of everything, negative interest rates, massive QE, and YCC. Year after year after year.

Is it similar to the old saying, “if it bleeds, it leads”?

No, it’s entertainment. Well-done entertainment.

Indeed, ZH, a decade ago was a useful site, now it’s a contrarian indicator. But to be fair, the Fed’s balance sheet has started growing again…

…which I am sure you will cover that again soon.

They already lowered and Powell said “looks good dawg!”

Well I doubt the 🐶 part

I have HELOC. just paid annual membership

going on 2 years I haven’t had use for it

at 7.5% I’m not gonna use unless I CAN CONSERVATIVELY make 20% ROI in 6 months

50-100% goal

coming soon I suspect

In mean time – I’ll keep 100% investments debt free

Are these real posts?

What is a membership for a heloc?

The random capitalization is suspect

I had a (free) HELOC with Wells Fargo (that I never used), but got a letter last year that they were getting out of the HELOC business and ending all HELOCs. P.S. To joediee there has never been and probably never will be a way to make a 20% ROI in 6 months “CONSERVATIVELY”…

China is selling our debt and putting CCP pressure on its banks to limit buying. Other sovereign nations are toying with the “Sell America” play. Treasury sales aren’t looking stellar for the near future. Outside of a complete stock market crash and a flight to securities, demand is going to continue on a downward trajectory.

Mortgage rates aren’t going anywhere — in fact, they have a higher chance of going UP! — regardless of where the Fed sets the benchmark rate.

People should forget any notions of the housing issues unwinding any time soon. The government has cooked up this problem since the 00’s and we are at the point where the only real solution is to stop toying with the market for a decade plus. EVERYTHING governments have done created these problems or made them worse.

“the chart below shows why the mortgage crisis happened: Consumers were way overleveraged with a housing-debt-to-disposable-income ratio of over 90%. When home prices sank and people started to lose their jobs, the debt imploded and was a big factor in the Financial Crisis.”

Jobs were always hard to come by for all of the seventy years of my life as I remember it with the glow of love as a reason

Do the numbers here include interest costs or just the principal?

just principle

like our corrupt fed govt that issues new debt to pay interest

it’s ponzi scheme foisted upon taxpayers/society

100% fraudulent

Bonds aren’t a ponzi

It seems that if the genius policy makers in D.C., from the White House to Capitol Hill to the Federal Reserve wanted to truly make housing affordable and to limit taxpayer liability, they could simply not allow Fannie, Freddie, VA and FHA to allow HELOCs.

From Gemini..

Fannie Mae, Freddie Mac, VA, and FHA do not directly offer or guarantee Home Equity Lines of Credit (HELOCs), as these are government-backed entities, not lenders. However, borrowers with existing FHA or VA loans can typically secure a HELOC through private lenders, subject to specific lender, equity, and credit requirements.

My mistake, I was thinking that Cash Out Refinances need to be unacceptable to Fannie et. al. This could be accomplished by simply implementing a policy of one time only mortgages by the same person(s) on a single piece of property.

I would suggest that only first time homebuyers qualify for GSE packaged mortgages. Maybe someone could propose this in Congress and see if Bill Pulte has a stroke.

Thankfully government back loans like FHA and VA have vastly stricter standards than conventional loans.

You can’t just waive inspections on a questionable home with an FHA loan. All these buyers in the NE and midwest overpaying for homes and waiving inspections will be screwed in the future.

And in other news…”Realtors report a ‘new housing crisis’ as January home sales tank more than 8% Sales of previously owned homes in January dropped a wider-than-expected 8.4% from December.”

Also, “Nearly 10% of student loan balances are more than 90 days past due, according to the report.”

It seems real estate agents are in a crisis and many are struggling to make ends meet. And with so many struggling to pay student loans, who will pay the over-inflated prices for homes?

Titanic 2.0 straight ahead!

RE agents are dropping out like flies here in Maryland and not renewing their licenses. There were 45,000 here in the state. 3,000 quit last year. More to come. Lawrence Yun is sh$tting in his pants.

Friendly reminder, the claim that taxpayers are on the hook for loses on Fannie, Freddie, and FHA loans is misleading. Fannie Mae and Freddie Mac GUARANTEEE loans, meaning if you own one of those mortgages you are guaranteed to receive those payments as the investor. Sounds scary as a taxpayer, but there are two important factors to consider, private mortgage insurance (PMI) and loan-to-value (LTV). For loans with an LTV above 80%, PMI is designed to cover loses stemming from foreclosures. For loans with an LTV below 80%, it’s likely that those loses would also be covered by the proceeds from the sale. Yes, the foreclosure process won’t necessarily recoup the entire market value of the home, but I’d argue that for most markets foreclosure process doesn’t result in the new buyer getting a 20% discount on the property either. So yes, if the PMI and sale proceeds from the foreclosure process doesn’t cover the loss, the taxpayer foots the bill, but a MASSIVE amount cushion exists to avoid that. I’d argue that the benefit of the government guaranteeing these loans and enforcing stricter lending standards (Dodd Frank / Ability-to-Repay) outweighs the risk, especially in the face of affordability concerns. Less risk to investors -> more demand -> downward pressure on mortgage rates.

The same concept applies to FHA, but instead they insure those loans. Last I looked, FHA has a pool of about 4 BILLION dollars to draw from if there were a wave of foreclosures.

Are taxpayers on the line, yes. Is it a risk that consistently gets exaggerated, yes.

🤣 They used the exact same logic to explain in 2006 why the banks were not at risk when mortgages default because … equity, down payments, home prices won’t drop enough to outrun those, etc. Now you’re using the logic to explain why taxpayers are not on the hook (at risk).

Mortgages are never a problem overall unless home prices plunge and unemployment surges. Read the article more carefully.

Read the comment more carefully! You’re comparing apples to oranges. Yes, that logic failed leading up to the financing crisis, but all of the risk you’re describing starts with the lending standards, which saw a complete 180 with Dodd Frank (requiring borrowers to demonstrate their ability-to-repay). The risks are not the same.

You’re arguing about the magnitude of the risk (“the lending standards, which saw a complete 180…”)

I was talking about who is exposed to the risk. I said in the article, “Taxpayers are on the hook” = THEY carry the risk, and NOT the banks. This was the statement you originally objected to with some gobbledygook about the magnitude of the risk.

I said nothing about the magnitude of the risk. But who is exposed to the risk.

You’re twisting this into some kind argument about the magnitude of the risk. Go argue with yourself about that.

I’m simply pointing out that to say taxpayers will foot the bill without any additional context is like saying car drivers will foot the bill for any automobile accidents. It’s partially true, but ignores the insurance aspect. Side note, I’m a massive fan of you and your work. Please keep doing what you do. I’m truly grateful for it.

Bankers will lie about everything and sometimes they just do not understand the current “product” they are selling.

Always does cascading damage.

“Mortgages are never a problem overall unless home prices plunge and unemployment surges.”

Actually, people did see the 2008 blow up of the liar loans coming. It was discussed for years on SI(where Burry also posted). File this under “nobody saw it coming”. Yes, it could also be clickbait but the trend is firmly in place. Time will tell.

“Microsoft AI chief Mustafa Suleyman believes that AI could replace most white collar jobs including lawyers, accountants and more, within the next year. His comments come days after Anthropic’s Claude Cowork shook the stocks of SaaS companies.

Microsoft AI boss Mustafa Suleyman has warned that AI could be coming to take most white-collar jobs soon. Not just coders, but even professionals such as lawyers and accountants, may see their job be automated by AI.

In an interview with the Financial Times, Suleyman revealed that Microsoft was pushing for a bigger share in the enterprise market with “professional-grade AGI.” He referred to this as an AI model that could do almost everything a human professional does. This would allow Microsoft to deliver powerful AI tools to its clients capable of performing routine tasks for knowledge workers.”

@Wolf I don’t know of any bank that ever had a problem with 20% down (or PMI with <20% down) "home" loans.

I remember reading about the just crazy neg am "liar" loans that took down WaMu and thinking that things will not end well when you sell a $500K home to a guy who makes minimum wage and get him to sign since he can move into the home and pay less than he was paying to rent an apartment

Google gound this:

"The thrift’s signature product was an “Option ARM” mortgage. With these loans, borrowers would pay an initial teaser rate then select one of four options for paying down the rest of the loan: a traditional 30 year fixed rate mortgage, a 15 year fixed rate loan, an interest only loan, or a loan requiring a minimum payment that didn’t cover the monthly intest on the loan. The unpaid interest was then added to the loans as principal putting the borrower deeper in debt.

in 2006 most WaMu loans started at 105% (real) LTV and got worse every month as unpaid interest was added to the loan balance (as home prices were dropping making the LTV even worse).

Many of these loans triggered in a year. Just enough time to flip it.

teaser rate 2% IO

one year trigger rate 12%

Not unusual to see mortgage brokers tacking on 6-8 points to close the loan at signing . The good old days of no “truth in lending”.

When the music stopped in early 2007 those triggers were the fuse….a very short one.

I saw ads on YouTube a couple of months back for a Visa (maybe Mastercard) that was secured via a Heloc and a low rate of 10%. In fact, the actor made it a point, noting he was borrowing from himself and can shop.

I just cannot help but those will cause some real damage down the line. Because I understand what the stats say, but in my neck of the woods, prople are feeling the pain of price hikes and property tax increases and not seeing any salary bumps.

I’m seeing a lot of YouTube ads for something called HomeTap.

Awwwww, isn’t that sweet?

You can tap the equity in your home and make everything nice and wonderful!

OTOH, Arizona Slim lives within easy walking distance of three houses that used to be owned by friends.

Alas, those friends took out HELOCs that they couldn’t repay. Houses went into foreclosure.

Friends are now gone from this neighborhood. And I miss them.

“Among the most fundamental changes resulting from the Financial Crisis was the transfer of mortgage risk from banks to taxpayers.”

That’s “privatize the profits, socialize the losses.” Great business model if you can get it. Shed your business risk onto a 3rd party, keep the profit.

It really seems to me like the financial sector has become the tail that wags the dog. First you have the Fed that exists to protect the financial sector. On top of that, Open Secrets reports that the largest sector to contribute to federal politicians is the “Finance – Insurance – Real Estate” (FIRE) sector – it dwarfs any other single issue donor by many multiples.

If you follow the money, tremendous liquidity injected into the financial sector by the Fed finds its way back to federal politicians, in a “virtuous” cycle. On top of that, you have Citizens United which opened the floodgates for legal constructs (businesses) to contribute to politicians (to be fair, unions had been contributing, which are also legal constructs. Instead of saying only physical persons could donate, CU went the other route saying most legal constructs could donate).

If money is speech, the FIRE sector has a lot more of it than most.

Home ownership is 65%. 40% of homes are mortgage free. In the next

decade many of those mortgage free home will be sold. Mortgage free will be replaced by new mortgages. Total mortgage will be up, even if homeownership will be down.

As housing debt to income shrinks our federal debt to income continues to increase.

Yes, wait till the big tax refunds have been paid out by about June. They’re starting to flow thick and heavy, from what I’ve seen so far.

As always, I greatly admire Wolf’s excellent charts. Thank you, Wolf!

From Wolf’s Mortgage Balance chart:

I don’t understand why total mortgages are increasing from 2022 to present at such a high rate. The slope of the increase is about the same as 2016-2020 when the mortgage rates were slowly declining. From 2022, rates were increasing, home values were drifting lower, home sales were plummeting, and refis were near zero. Also, refis from 2020 at <3% should be causing principal on all refi’d loans to drop at a large rate.

What is causing this increase in mortgage balances?

The amount of HELOC loans increased about 100M while the loan balances increased over 1T so that can’t b explain the increase. Maybe very few people are paying off their houses compared to 2016-2020?

I understand the steep slope from 2020-2022 when the mania from record low mortgage rates and bidding wars caused a dramatic increase in sales and house prices.

Due to my reasons above, I expect mortgage balances to level off and start dropping in the near future.

In the paragraph under the first chart, I explain the factors that cause mortgage balances to increase.

Thanks Wolf!

Due to new build houses, the pool of houses with potential mortgage balances is growing faster than any year from 2016-2020. Even though sales are down from 2016-2020, prices are higher which could grow the mortgage balances with the same slope.

Thanks for pointing this out. Sorry I missed your comment in the article.